Sample Category Title

NASDAQ Futures (NQ_F) Forecasting the Rally From the Equal Legs Zone

Hello fellow traders. In this technical article we’re going to take a look at the Elliott Wave charts charts of NASDAQ Futures (NQ_F) published in members area of the website. Our members know NQ_F is showing impulsive bullish sequences and we are favoring the long side. In this discussion, we’ll break down the Elliott Wave pattern and forecast.

NASDAQ Elliott Wave 1 Hour Chart 10.23.2024

NASDAQ is giving us wave ((ii)) black correction. The futures has reached extreme zone from the peak at 20129- 19837 area. NQ_F shows clear 3 waves from the high, suggesting pull back could be ending any moment. Consequently , we expect rally in wave ((iii)) to happen any moment. We recommend members to avoid selling the futures and keep favoring the long side. As the main trend is bullish we expect to see rally toward new highs ideally or 3 waves bounce from the equal legs alternatively.

Official trading strategy on How to trade 3, 7, or 11 swing and equal leg is explained in details in Educational Video, available for members viewing inside the membership area.

NASDAQ Elliott Wave 1 Hour Chart 10.23.2024

NASDAQ responded exactly as anticipated at the equal legs. The futures found buyers and made a substantial rally from our recommended buying zone. Eventually we got break of ((i)) black peak , confirming next leg up is in progress. The futures should ideally keep finding buyers in 3,7,11 swings sequences against the 20077.5 pivot.

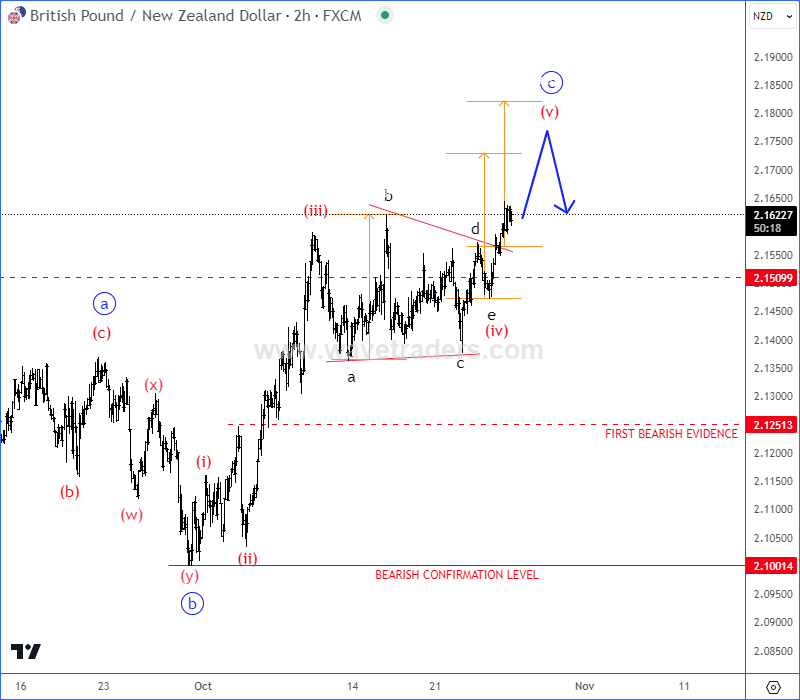

GBP/AUD and GBP/NZD Pairs Step Into Final Leg of a Recovery

GBPAUD pair is now breaking out of a projected bullish abcde running triangle pattern. And, because of a break out of a triangle, it means it’s breaking ouf wave (b) into a wave (c) of a corrective recovery, but there can be still space up to around 1,97 area before it finds the resistance.

GBPAUD 2h Chart

GBPNZD is breaking out of projected subwave (iv) running triangle into final subwave (v) of »c« of a correction, but before bears show up again, we still see room up to 2,17 – 2,18 resistance area.

GBPNZD 2h Chart

A triangle appears to reflect a balance of forces, causing a sideways movement that is usually associated with decreasing volume and volatility. The triangle pattern contains five overlapping waves that subdivide 3-3-3-3-3 and are labeled A-B-C-D-E. The running triangle is a region of horizontal price movement, a consolidation of a prior move, and it is composed of “threes.” That means each of the A-B-C-D-E waves have three subwaves. The triangle pattern is generally categorized as a continuation pattern, meaning that after the pattern completes, it’s assumed that the price will continue in the trend direction it was moving before the pattern appeared. However, triangles also indicate that the final leg is coming before a reversal and that’s why triangles are labeled in wave B, wave X or wave 4.

Yen Slips to 3-Month Low After Japanese Election

The Japanese yen is lower on Monday. In the European session, USD/JPY is trading at 152.63, up 0.22% at the time of writing. The yen weakened as far as 153.88 but has pared most of the losses.

Yen slumps after Ichida loses parliamentary majority

The new trading week has barely begun but the markets are busy digesting the drama out of Tokyo. The snap parliamentary election over the weekend was a disaster for new Prime Minister Shigeru Ishiba, as his Liberal Democratic Party (LPD) coalition won just 215 seats, short of the 233 majority.

Ishiba has been in power for only a month and the snap election backfired as the LDP lost its parliamentary majority for the first time since 2009. It’s unclear if Ishiba will be able to cobble together a majority and the political uncertainly could push the yen, which is trading at 3-month lows, even lower.

The election bombshell comes just ahead of the Bank of Japan’s on Oct. 31. The BoJ is expected to maintain policy settings and will release updated growth and inflation forecasts. The BoJ has intervened in the past when the yen showed a sharp and quick decline and there is speculation that the central bank might intervene if the yen falls to 155 or 160 per dollar.

The US wrapped up the week with mixed results. Durable Goods Orders declined 0.8% in September, unchanged from a revised -0.8% reading in August and above the market estimate of -1%. The UoM Consumer Sentiment index improved slightly to 70.5 in October, above 70.1 in September, beating the market estimate of 69.0.

USD/JPY Technical

- USD/JPY continues to push through resistance lines. The next resistance line is 153.94

- 152.03 and 151.68 are providing support

Nasdaq 100 Technical: Negative Feedback Loop from Rising US Treasury Yields May Overshadow Mega-Cap Earnings Results

- Five mega-cap technology stocks (Alphabet, Microsoft, Meta, Apple and Amazon) will report their respective earnings results this week.

- Bullish momentum of the recent 4-week rally seen in the 10-year US Treasury yield remains intact.

- A continuation of the surge in the 10-year US Treasury yield may challenge the positive vibes from the US mega-cap technology earnings results.

Pivotal week for the Nasdaq 100 as five mega-cap technology stocks; Alphabet, Microsoft, Meta, Apple and Amazon that have a combined weightage of around 31% will report their respective Q3 earnings results this week.

Ex-post earnings share performances of these five mega-cap technology firms after one to two days from their prior Q2 respective earnings results release dates had been lacklustre.

So far rosy expectations have been set for the Q3 earnings results of Alphabet, Meta, and Amazon that are poised for double-digit earnings growth supported by ad spending. Apple may get an uplift on sales of its latest iPhone 16 model from its key China market accordingly to a news report from Bloomberg.

Nasdaq 100 resilience may be tested by rising long-term 10-year US Treasury yield

Fig 1: 10-year US Treasury yield long-term secular trend with Nasdaq 100/S&P 500 ratio & MOVE Index as of 25 Oct 2024 (Source: TradingView, click to enlarge chart)

The Nasdaq 100 has so far managed to notch a month-to-date return of 1.45% for October as of 25 October while the 10-year US Treasury yield has rallied by 50 basis points over the same period, its biggest monthly jump in almost two years.

This recent bout of significant push up in the 10-year US Treasury yield has been accompanied by rising interest rate implied volatility where the MOVE Index has jumped to a one-year high.

Based on past data, such swift increase in the 10-year US Treasury yield and MOVE Index have saw the Nasdaq 100 staged a medium-term corrective decline between July 2023 to October 2023 and November 2021 to October 2022 (see Fig 1).

The “Trump Trade” narrative has gained traction in the recent week due to rising odds of Republican nominee Trump winning the US presidential election based on data from betting markets (61%Trump versus 37% Harris based on Real Clear Politics data as of 27 October).

So far Trump’s proposed key policies of a lower corporate tax rate, and higher trade tariffs on China and rest of the world imports to the US is likely to see a resurgence of inflationary pressure from a medium-term to long-term horizon.

Hence, a rising 10-year US Treasury yield that is driven by inflationary rather than economic growth uplift is likely to be detrimental to the Nasdaq 100 from a valuation standpoint.

Nasdaq 100’s market breadth has remained lacklustre

Fig 2: Nasdaq 100 CFD major & medium-term trends as of 28 Oct 2024 (Source: TradingView, click to enlarge chart)

The 10-day moving average of the Nasdaq 100’s 52-week high minus 52-week low market breadth indicator has continued to print a lower low and inched downwards.

This observation suggests that there are fewer Nasdaq 100 component stocks hitting new 52-week highs; a potential bearish reversal may be looming on the horizon for the Nasdaq 100 (see Fig 2).

Watch the 20,790 key long-term pivotal resistance on the Nasdaq 100 CFD Index (a proxy of Nasdaq 100 E-mini futures), a break below the 19,840 intermediate support (also the 50-day moving average) may expose the next medium-term supports of 19,155 and 18,310.

On the other hand, a clearance above 20,790 long-term pivotal resistance invalidates the bearish scenario to see the next medium-term resistances coming in at 21,680 and 22,470/980.

USD/JPY Chart Analysis: Rate Hits Autumn High

Today’s USD/JPY chart indicates that the U.S. dollar has strengthened against the yen by over 6.6% since the beginning of the month. Starting this trading week, the rate has surpassed 153 yen per dollar, a level not seen since August 31.

This bullish sentiment towards the dollar has been driven by the outcome of Japan’s parliamentary elections over the weekend. According to Reuters, investors believe that the loss of the ruling coalition’s majority in Japan’s parliament reduces the likelihood of a future interest rate hike, contributing to the yen's weakening.

On October 10, there was speculation that bears might halt the October rally (marked by the blue channel) and guide the rate back down within a descending channel from its upper boundary (marked in red), with the psychological level of 150 yen per dollar acting as resistance.

However, bulls maintained their momentum (which originated from the psychological level of 140 yen) and continued the rally, breaking through this resistance. Per USD/JPY technical analysis, the 150 yen level may now serve as a support line.

The RSI indicator currently suggests the formation of a potential bearish divergence, hinting that a slight correction might occur as the market anticipates key upcoming news, which could heavily influence the sustainability of the current USD/JPY rally:

→ The Bank of Japan’s interest rate decision, expected on Thursday

→ Key U.S. labor market data releases scheduled for later in the week

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

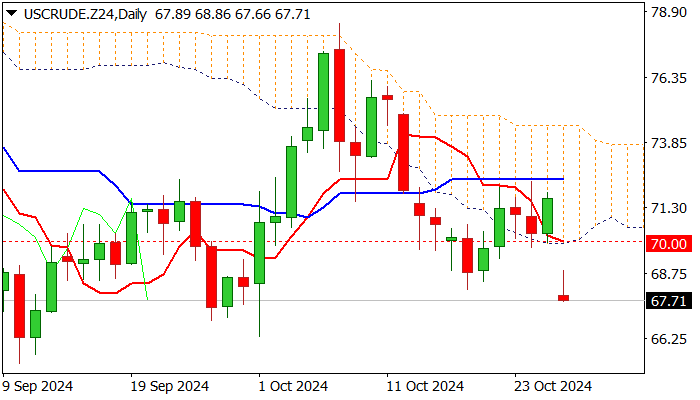

WTI Outlook: Oil Opens With Gap Lower as Supply Fears Fade After Israel’s Attack on Iran

WTI oil opened with wide gap lower on Monday and fell to the lowest levels in nearly one month, registering a drop of around 5% at the start of the week.

Israel’s attack on Iran over the weekend was a main oil driver with Iran’s oil facilities remaining intact that offset fears of energy supply disruption and deflated oil prices.

Monday’s sharp fall generated strong bearish signal on dip well below psychological $70 support (also the base of thick daily Ichimoku cloud) which held the action in past three days.

Also, breach of former higher low of Oct 18 ($68.15) added to negative outlook, along with short-lived recovery attempts in early European trading.

Bears pressure lower 20-d Bollinger band ($67.23) and eye Oct 1 spike low ($66.33) which guards key support at $65.26 (2024 low posted on Sep 10).

Close below $70 is seen as minimum requirement to keep bears in play, while close below $68.15 to reinforce bearish stance, as daily studies are in full bearish setup.

Res: 69.33; 70.00; 70.30; 71.00.

Sup: 67.23; 66.94; 66.33; 65.26.

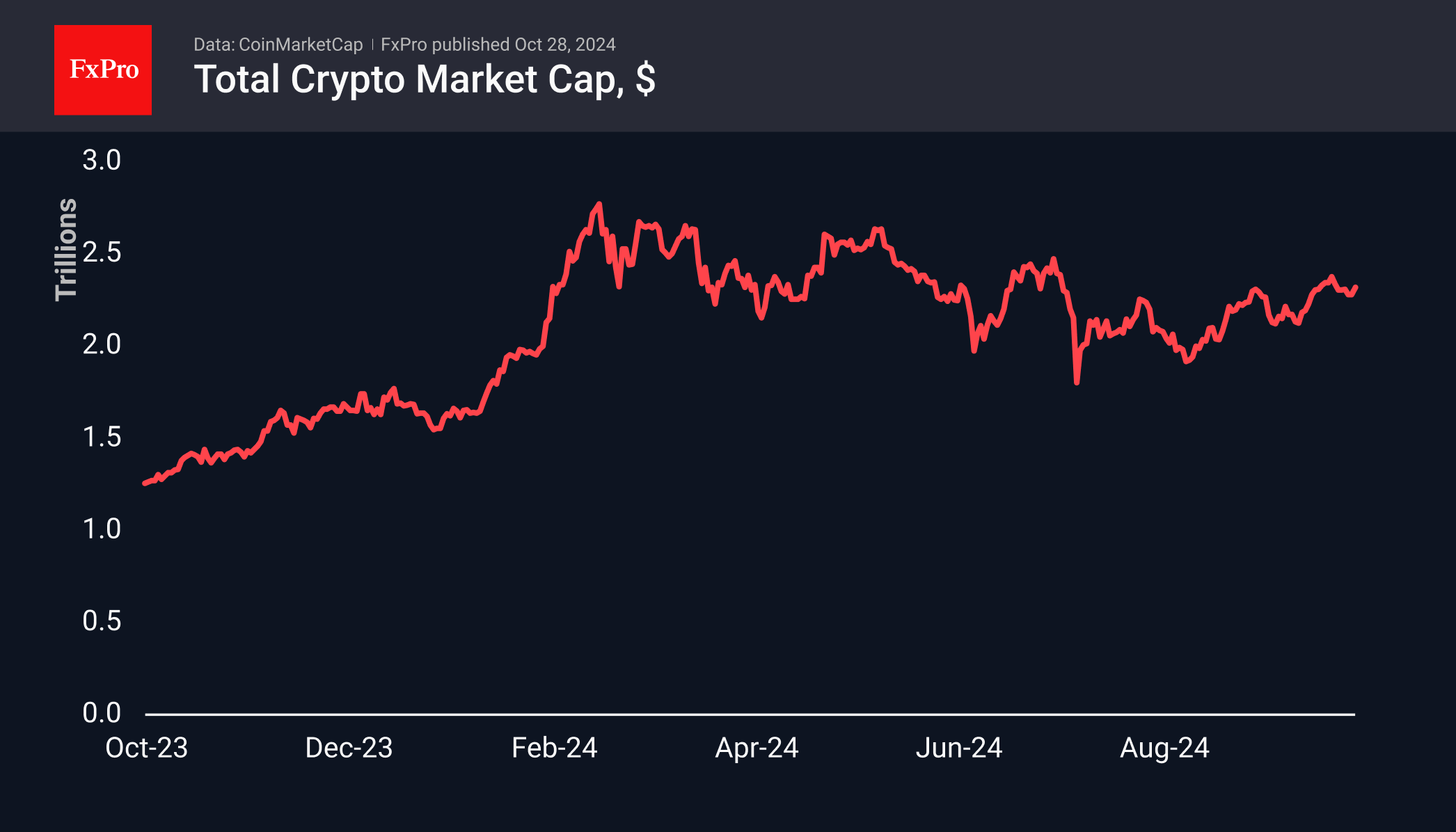

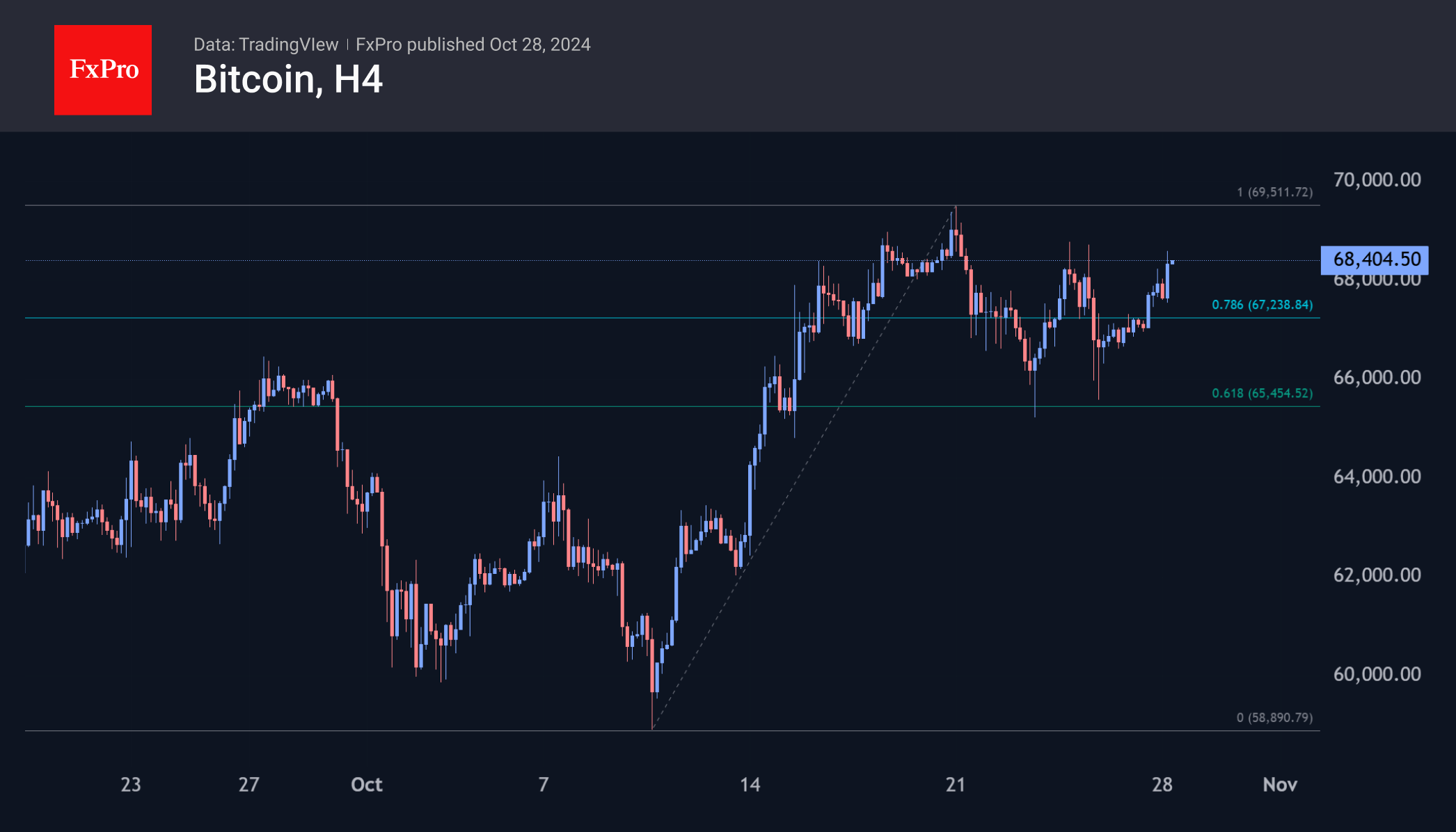

Crypto Overcomes Last Week’s Corrective Sentiment

Market Picture

Last week, the cryptocurrency market was dominated by a risk-off sentiment that saw the total crypto market capitalisation fall from $2.4 trillion to $2.2 trillion. However, on Saturday, higher volumes led to a price recovery, bringing the market back to the $2.3 trillion valuation it started the week with. The sentiment index is at 72, having been in the 69-74 range for the past twelve days.

Bitcoin climbed to $68.4K, entering the range of the last six days. Last week, the market corrected the October 10th-20th gains, potentially paving the way for fresh upside momentum. Fibonacci pattern extensions suggest a potential upside to $76K, but the $70K and $72K areas could be a notable obstacle on the way.

News Background

Inflows into US spot Bitcoin ETFs continued for a third week, albeit at a slower pace. According to data from SoSoValue, inflows into BTC ETFs totalled $997.7 million last week, bringing the total to $21.93 billion since their launch in January.

The Ethereum ETF saw renewed outflows, totalling $24.5 million last week. Net outflows have risen to $504.4 million since the product’s launch.

Options on Deribit indicate only a 10% chance of Bitcoin hitting $100,000, notes CoinDesk analyst Omkar Godbole. Most market participants expect BTC to move towards the $80,000 mark.

Bitcoin alone isn’t enough to kick off the altcoin season just yet. According to Hashkey Capital, the altcoin season will be when BTC crosses $80K. Historically, the altcoin rally has been associated with BTC’s market dominance index rising to levels in the 62-70% range.

According to the Wall Street Journal, US authorities are investigating USDT issuer Tether for alleged violations of sanctions and anti-money laundering rules. Tether CEO Paolo Ardoino denies the information about the investigation.

EUR/USD Dives, USD/JPY Remains In Strong Uptrend

EUR/USD declined from the 1.0880 resistance and corrected gains. USD/JPY is rising and might gain pace above the 153.85 resistance.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro started a fresh decline below the 1.0850 support zone.

- There was a break below a connecting bullish trend line with support at 1.0805 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY climbed higher above the 150.50 and 152.20 levels.

- There was a break above a key contracting triangle with resistance at 152.00 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair struggled to clear the 1.0880 resistance zone. The Euro started a fresh decline and traded below the 1.0850 support zone against the US Dollar.

The pair declined below 1.0820 and tested the 1.0760 zone. A low was formed near 1.0761 and the pair recently attempted a recovery wave. There was a minor recovery wave above the 1.0800 level. However, the bears were active near 1.0840 and the pair started another decline.

There was a move below the 1.0820 level. The pair declined below the 50% Fib retracement level of the recovery wave from the 1.0761 swing low to the 1.0839 high.

Besides, there was a break below a connecting bullish trend line with support at 1.0805. The pair is now trading below 1.0800 and the 50-hour simple moving average.

On the upside, the pair is now facing resistance near the 1.0805 level. The next key resistance is at 1.0840. The main resistance is near the 1.0870 level. A clear move above the 1.0870 level could send the pair toward the 1.0950 resistance.

An upside break above 1.0950 could set the pace for another increase. In the stated case, the pair might rise toward 1.0980. If not, the pair might resume its decline. The first major support on the EUR/USD chart is near 1.0780 and the 76.4% Fib retracement level of the recovery wave from the 1.0761 swing low to the 1.0839 high.

The next key support is at 1.0760. If there is a downside break below 1.0760, the pair could drop toward 1.0720. The next support is near 1.0650, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a fresh upward move from the 149.00 zone. The US Dollar gained bullish momentum above 150.50 against the Japanese Yen.

It even cleared the 50-hour simple moving average and 152.00. There was a break above a key contracting triangle with resistance at 152.00. The pair climbed above 153.50 and traded as high as 153.88.

It is now consolidating gains above the 23.6% Fib retracement level of the upward move from the 151.45 swing low to the 153.88 high.

The current price action above the 153.20 level is positive. Immediate resistance on the USD/JPY chart is near 153.85. The first major resistance is near 154.20. If there is a close above the 154.20 level and the RSI moves above 65, the pair could rise toward 155.00.

The next major resistance is near 155.85, above which the pair could test 157.00 in the coming days. On the downside, the first major support is 153.20, below which the bears could gain strength.

The next major support is visible near the 50% Fib retracement level of the upward move from the 151.45 swing low to the 153.88 high at 152.65. If there is a close below 152.65, the pair could decline steadily. In the stated case, the pair might drop toward the 152.20 support zone. The next stop for the bears may perhaps be near the 151.45 region.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

A Bearish Gap on the Brent Crude Oil Chart

As the XBR/USD chart shows, Brent crude oil prices formed a gap at the start of this week: while Friday’s session closed at 75.60, Monday’s opening price dropped below 72.60.

According to Reuters, this development is tied to the fact that Israel’s recent missile strike on Iran did not impact oil or nuclear facilities, reducing the immediate risk of escalation.

Will Brent Crude Oil Prices Continue Falling?

In terms of technical analysis for XBR/USD today:

→ The price is within a descending channel (shown in red) that has been active since early summer. A bullish breakout attempt on 7 October was unsuccessful (marked by a red arrow), and Brent crude has since dropped over 10%. Price consolidation between 17-22 October near the median of this red channel confirms its current relevance.

→ Bulls had an opportunity to show strength with a bounce (marked by a blue arrow) from Support Line 1, which forms part of an upward structure represented by blue lines. However, today’s bearish gap erased these gains.

This allows traders to consider two scenarios:

→ Bearish Scenario: After breaking below Support, Brent could continue along the red descending channel. If the channel’s median line holds as resistance, this bearish outlook may be confirmed.

→ Bullish Scenario: Today’s bearish breach of the 18 October low could prove false, leading to a potential recovery back toward the structure of three blue lines.

Ultimately, which scenario plays out will largely depend on volatile news related to geopolitical tensions, the U.S. presidential election, and economic data from major economies.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

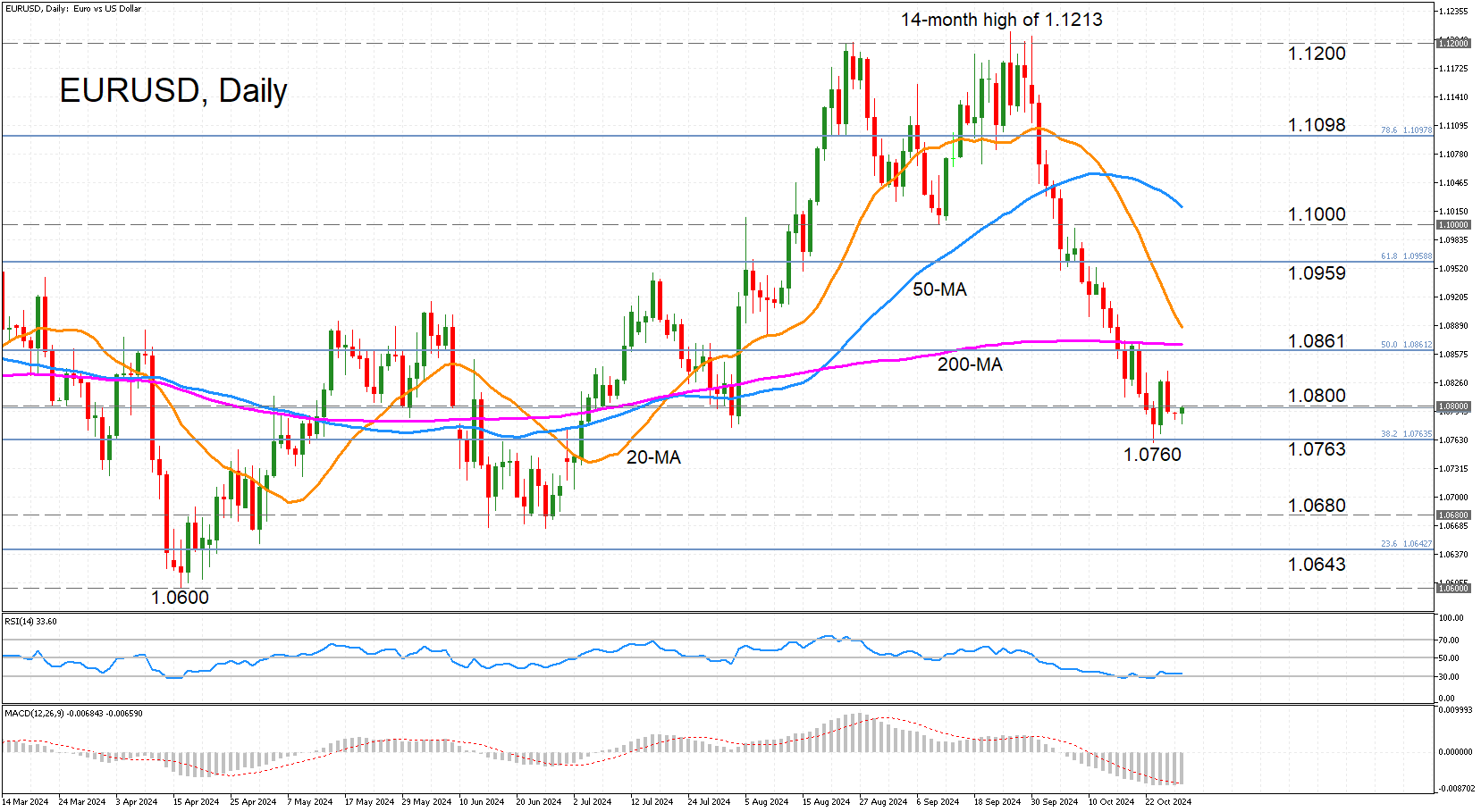

EURUSD Halts Decline But Downside Risks Persist

- EURUSD turns flat around 1.0790

- But momentum indicators stuck deep in bearish territory

EURUSD has steadied around 1.0790 after its rebound from the 16-week low of 1.0760 faltered. However, whilst there is slight positive energy on Monday, with the price inching higher, the momentum indicators are overwhelmingly within the bearish zone.

Nevertheless, the selling pressure appears to be easing and a bullish reversal is possible in the near term as the RSI has flatlined just above the oversold level while the MACD has just crossed above its red signal line.

However, for any rebound attempt to succeed, the bulls would first need to overcome the immediate obstacle of 1.0800. A climb above it would clear the path towards the 50% Fibonacci retracement of the July-October 2023 downleg at 1.0861. The 200-day simple moving average (SMA) is descending towards it, making this a critical resistance area. Higher up, the 61.8% Fibonacci of 1.0959 is the next major hurdle before attention turns to the 1.1000 handle and the 50-day SMA that’s approaching it from above.

If, though, the price dips lower again, the October low of 1.0760 is likely to be revisited. A break below it would reinforce the bearish outlook in the medium term and the focus would then shift to the 1.0680 support and the April trough of 1.0600.

To sum up, there is some hope of an upside reversal in the near term despite the bearish signals. But for any rebound to get off on a solid footing, the price would have to recover at least until the 200-day SMA.