Sample Category Title

DAX 40 Loses Upward Momentum

Today, Germany's PMI data was released, according to Forex Factory:

→ German Flash Manufacturing PMI: actual = 42.6, expected = 40.7, previous = 40.6;

→ German Flash Services PMI: actual = 51.4, expected = 50.6, previous = 50.6.

The DAX 40 index (Germany 40 mini on FXOpen) showed a slight intraday increase, which could be viewed positively, especially given that last week, the index reached a yearly high.

However, the chart for the DAX 40 (Germany 40 mini on FXOpen) shows signs of the upward momentum slowing:

→ The RSI indicator is showing bearish divergence;

→ Price fluctuations are forming a triangle that could turn into a bearish reversal pattern known as a Bearish Rising Wedge (marked by black lines).

If a bearish break below the lower black line occurs, it might indicate that the bulls failed to maintain the momentum above the blue channel, within which the DAX 40 index had fluctuated for most of 2024.

Thus, a potential pullback towards the psychological level of 19,000 should not be ruled out.

Trade global index CFDs with zero commission and tight spreads. Open your FXOpen account now or learn more about trading index CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

UK PMI composite hits 11-month low as business confidence wavers

UK business activity weakened in October, with both the manufacturing and services sectors showing signs of slowing momentum. PMI Manufacturing index dropped from 51.5 to 50.3, marking a 6-month low, while PMI Services index fell from 52.4 to 51.8, an 11-month low. Consequently, Composite PMI also declined to an 11-month low, slipping from 52.6 to 51.7.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, attributed this slump to "gloomy government rhetoric" and rising uncertainty ahead of the Budget. He added that external risks, such as conflicts in the Middle East, the ongoing war in Ukraine, and the upcoming US elections, have further dampened economic confidence.

The early PMI data suggests that the UK economy grew at a meagre 0.1% quarterly rate in October. However, Williamson noted that further cooling of input cost inflation, now at its lowest level in four years, could allow BoE to take a "more aggressive stance" toward rate cuts if the economic slowdown persists.

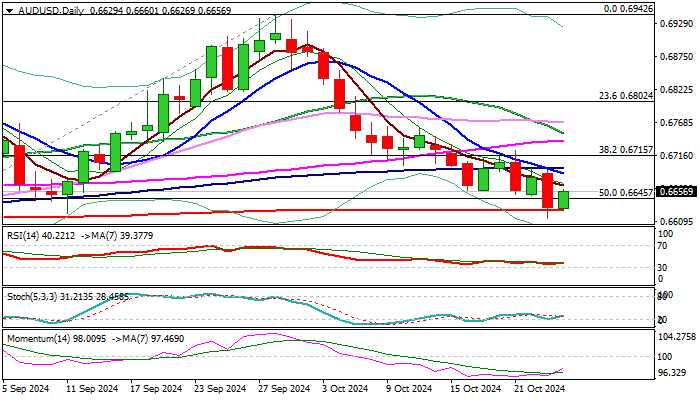

AUD/USD Outlook: Bears Take a Breather

AUDUSD edges higher on Thursday morning after bears repeatedly failed to clear 200DMA support (0.6627).

Recovery is in its early stage and needs more work at the upside to generate firmer positive signal, although near-term action to remain constructive while above 200DMA.

Repeated daily close above here to boost hopes of stronger recovery and Friday’s close above 200DMA to complete a bear-trap on weekly chart and open more prospects for stronger bounce however, 100DMA (0.6794) and daily Ichimoku cloud top (0.6707) mark strong barriers where potential recovery rally may face strong headwinds.

Daily studies remain bearishly aligned (MA’s in predominantly bearish setup and north heading 14-d momentum is still deeply in negative territory) which contributes to scenario of limited correction before larger bears regain control.

Look for firmer direction signals on break of either boundary of daily Ichimoku cloud (base at 0.6593 and top at 0.6707).

Res: 0.6670; 0.6694; 0.6707; 0.6739.

Sup: 0.6627; 0.6593; 0.6575; 0.6563.

Eurozone PMIs: Persistent price pressures lean ECB toward 25bps Dec cut, not 50bps

Eurozone's economic activity showed mixed signals in October, with PMI Manufacturing rising slightly from 45.0 to 45.9, while PMI Services fell marginally from 51.4 to 51.2. As a result, Composite PMI ticked up slightly to 49.7 from 49.6, but remained below the 50-point mark, indicating ongoing economic contraction.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, described the Eurozone as "stuck in a bit of a rut," noting that the economy contracted for the second consecutive month. While the manufacturing sector continues to slump, its negative impact is being balanced out by minor gains in services. De la Rubia added, "For now, it is not clear whether we will see a further deterioration or an improvement in the near future."

According to de la Rubia, for ECB, the data present an "unwelcome surprise," particularly in the services sector. Inflationary pressures appear to be lingering, driven by wage growth, which has been pushing up costs and selling prices for service providers.

This persistent inflation suggests that the ECB may lean towards a 25bps rate cut in December, as opposed to the larger 50bps cut some had speculated.

Germany’s PMI offers slight relief, but structural weaknesses persist

Germany's economic outlook improved slightly in October, as PMI Manufacturing index rose to 42.6 from 40.6, while PMI Services climbed to 51.4 from 50.6. This led to a rise in Composite PMI to 48.4 from 47.5, offering some hope for the start of Q4.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlighted that the start to Q4 is "better than expected." With manufacturing shrinking at a slower rate and services expanding more quickly, he noted that growth in Q3 is a "distinctive possibility."

However, despite these improvements, Germany's GDP is still forecast to remain flat for the year, following a 0.3% contraction in 2023, as projected by the International Monetary Fund.

De la Rubia also pointed to the "structural weaknesses" weighing down the German economy. Key issues such as high energy costs, rising competition from China, and ongoing labor market shortages are continuing to strain the manufacturing sector.

France’s PMI composite falls to 47.3, economic struggles deepen

France's economic woes intensified in October, with PMI data showing further contraction across key sectors. PMI Manufacturing edged down slightly from 44.6 to 44.5. More notably, Services PMI dropped to 48.3 from 49.6, hitting a 7-month low, while Composite PMI fell from 48.6 to 47.3, its lowest point in nine months.

Tariq Kamal Chaudhry, Economist at Hamburg Commercial Bank, emphasized the gravity of the situation, stating, "France remains trapped in economic decline as Q4 begins." HCOB's Nowcast predicts only marginal growth moving forward, placing significant pressure on the French government to implement measures aimed at stabilizing the economy and addressing fiscal imbalances.

The industrial sector remains "mired in a deep crisis," with no signs of recovery in sight. Meanwhile, the services sector is also struggling under "tough conditions," further dampening the overall economic outlook.

EUR/USD Dips to Three-Month Low Amid Strong Dollar Demand

EUR/USD has tumbled to 1.0789, marking a near three-month low as market sentiment heavily favours the US dollar. The dollar's strength is driven by expectations of a gradual and limited interest rate cut by the US Federal Reserve and solid prospects for Donald Trump's re-election, which appears increasingly likely.

Concurrently, the Euro is under pressure due to a significant rate cut by the European Central Bank. This cut has set a clear downward trend for the EUR exchange rate, offering little room for recovery. This week, Fed officials advocated caution in monetary easing, suggesting that while a 50-basis-point cut by year-end is plausible, more aggressive cuts are unlikely.

The combination of Fed caution, rising US government bond yields, and the anticipated political stability under a potential second Trump term are contributing factors to the strengthening US dollar.

Today, the focus will be on key economic indicators, including Markit's October business activity in services and industry. Additionally, data on new home sales and the weekly unemployment benefits report will be closely monitored, especially considering their importance to the Fed's assessment of the employment landscape.

Technical analysis of EUR/USD

The EUR/USD pair has completed a downward wave to 1.0760 and is now rebounding towards 1.0880. After reaching this level, a pullback to 1.0820 is anticipated. The market may form a consolidation range at these lows, with a potential breakout upwards towards 1.0900 and possibly extending to 1.0990. The MACD indicator, currently below zero but pointing upwards, supports the possibility of a corrective rally.

On the hourly chart, EUR/USD is developing a second growth impulse towards 1.0824. Once this level is achieved, a corrective phase will be initiated, targeting 1.0790. The Stochastic oscillator, with its signal line moving towards 80 from above 50, supports this short-term bullish correction within the broader bearish context.

ECB’s Holzmann: 50bps cut in Dec unlikely, but can’t be ruled out

Austrian ECB Governing Council member Robert Holzmann, one of the more hawkish voices, signaled that a 25bps cut is "probable" at the December meeting. While a larger, half-point cut isn't "impossible", it's unlikely.

Holzmann emphasized caution, saying, “I’m still concerned that inflation might prove stronger than expected,” reflecting his hesitation in moving too quickly toward easing.

Despite acknowledging some downside risks, he remarked, "I don’t see enough of them to conclude that they dominate," adding that the view of risks being tilted to the downside is still a minority on the ECB Governing Council.

Separately, Slovenia's ECB Governing Council member Bostjan Vasle echoed the sentiment, expressing support for "going to neutral in measured steps.”

Vasle noted that while data has shown improvement, inflation "has not yet been defeated," and discussions about undershooting the inflation target are premature. He further commented, "Once we get closer to neutral, it may be appropriate to align our language accordingly."

EMU Money Markets Currently Attach Near 50% Probability to ECB Scaling Rate Cuts Up to 50 bps in December

Markets

German Bunds significantly outperformed US Treasuries yesterday, especially at the front end of the curve. The German 2-yr yield lost 7.2 bps compared with a 4.7 bps increase for the US 2-yr yield. EUR/USD as a result tested 1.0778 support a first time (close: 1.0782). ECB governors kept all options open for the December policy meeting in comments on the sidelines of the IMF’s World Economic Outlook in Washington. In brief: downside growth risks could accelerate an already faster-than-expected disinflation process and eventually result in an undershoot of the 2% inflation target. ECB Lagarde underlined that the direction of travel is clear and that the pace will be determined on the basis of backward- and forward-looking elements using the three criteria (inflation outlook, dynamics of underlying inflation and the strength of monetary transmission) and applying judgment. EMU money markets currently attach a near 50% probability to the ECB scaling rate cuts up to 50 bps in December. October PMI surveys are the first piece of the data puzzle today. Over the past months, we’ve seen a divergence between very weak EMU sentiment data and more modest (but often ignored and labelled outdated) hard data. Next week’s Q3 EMU GDP numbers can therefore deliver a (much) better outcome than the 0.0% GDP growth as suggested by the PMI-based model. Consensus doesn’t expect much improvement in today’s (October) PMI’s compared to upwardly revised (but also ignored) September figures. They could be the straw to brake EUR/USD’s back. EUR/GBP yesterday bounced off 0.83-support in the run-up to BoE Bailey’s speech in Washington. He stressed that disinflation is happening faster than expected though services inflation remains higher than is consistent with target. This suggests that he’ll still push for a 25 bps rate cut at the November BoE meeting. UK & US PMI’s and US weekly jobless claims are up for release as well today, offering an interesting and likely volatile mix in an era of extremely data-dependence. Genuine dollar strength and rising US rates propelled USD/JPY from 140 mid-September to 153 yesterday, prompting a first verbal intervention by Japanese Finance Minister Kato against one-sided rapid moves in FX markets.

News & Views

The Bank of Canada upped the pace in its easing cycle yesterday and lowered the policy rate by 50 bps to 3.75%. This came after inflation eased sharply from 2.7% to 1.6%. Aside from declining oil prices, the BoC sees notoriously sticky shelter costs have begun to ease. Excess supply elsewhere in the economy has reduced inflation in the prices of many other goods and services, it said, adding that its preferred measures of core inflation are now below 2.5%. With inflation now back around the 2% mid-point target and a lacklustre economy, the central bank put governor Macklem’s words in September – when he offered the possibility of easing faster - to practice. Canadian GDP is expected to strengthen gradually over 2024-2025-2026 (1.2%-2.1%-2.3%) amid lower rates supporting consumption, residential & business investment. Exports should benefit from robust demand from the US. Inflation saw some small downward revisions in the first two years of the policy horizon to be at 2.5%-2.2%-2.0%. The BoC commits to further cuts if the economy evolves as expected but the timing and pace is guided by incoming data. With yesterday’s move largely priced in the Canadian dollar only lost limited ground to USD/CAD 1.3836. The Loonie had been dropping significantly in the run-up since end-September amid the growing divergence between the US and Canada.

The European Commission has cleared payment of some €800 million of post-pandemic recovery funds it withheld from Slovakia over concerns with the rule of law in the country. The EC formally unblocked the funds already back in July after the Fico government reinstated sentencing for fraud with EU resources. But it stopped short from transferring until after parliament had approved changes to its criminal code which reduced sentences for crimes ranging from petty theft to fraud. The Fico’s government in the meantime reassured Brussels that the amendments do not eliminate the prosecution of crimes related to EU Funds. The EC responded that some of its concerns have been alleviated though adding that talks are ongoing to “clarify the pending issues”.

Nasdaq Futures Rise as Tesla Beats

The first three sessions of the week haven’t been appetizing as the US political uncertainties, the ongoing geopolitical jitters in the Middle East, and the mounting expectation that Federal Reserve (Fed) would slow down the pace of monetary easing pushed investors to the sidelines.

Gold ran from record to record despite the rising US yields which, in return, rise not only because of the weakening dovishness regarding the Fed rate cut bets, but also because of a general lack of appetite before the upcoming US presidential election. The world is worried that a potential Trump win would further hammer international trade and fan global inflationary pressures. The IMF lowered its global growth forecast for next year to 3.2% due to accelerating risks from wars to protectionism. It however left its 2024 projection unchanged, and expects inflation to slow to 4.3% in 2025 from 5.8% this year.

Over at the Fed, Mary Daly said that she hasn’t seen any information that would suggest that they shouldn’t continue cutting rates but other members including Neel Kashkari say that the rate cuts should continue at a moderate speed. Activity on Fed funds futures assess around 92% chance for a 25bp cut in the November meeting, but there is a mounting speculation that the Fed could make a pause to its nascent loosening policy in December.

As such, the US dollar continues to recover against most majors. The greenback is offered this morning in Asia, but the dollar index rallied more than 4% since the September dip. The EURUSD sold off to 1.0761 yesterday as the rate cut bets in the Eurozone remain strong on the back of inflation that seems under control and weak economic and corporate data. Many European Central Bank (ECB) members sound increasingly dovish. Olli Rehn for example said that the zone’s ‘dire economy’ may bolster disinflationary pressures, Bank of France’s Francois Villeroy called for more agility with future rate cuts to avoid acting too slowly and Mario Centeno said that the ECB should consider ramping up monetary easing if the data backs such move. The growing divergence between the Fed and the ECB outlooks should continue to support a deeper selloff in the EURUSD. Price rallies should meet resistance near 1.0870, which shelters the minor 23.6% Fibonacci retracement on September-October selloff and the pair should remain in the bearish trend below 1.0935 – the major 38.2% Fibonacci retracement on that selloff.

Elsewhere, the USDJPY cleared the 150 resistance, pulled out the 200-DMA and is trading past the 152 this morning as the continuation of the rally that started with dovish remarks from the new PM who suggested that the country doesn’t need another rate hike this year. The yen could however need another FX intervention to stop it from falling too fast too low.

In Britain, Cable slipped below the 100-DMA and remains under a selling pressure as the Bank of England (BoE) Governor Bailey says that inflation in Britain is weakening faster than they anticipated, and in Canada, the Loonie hit the lowest levels against the US dollar since the beginning of August after the Bank of Canada (BoC) delivered a 50bp cut yesterday, as expected.

There will certainly be a correction and a consolidation to the US dollar rally, but unlikely before the US election.

In equities, the European stocks remain under pressure. The rising dovish voices at the ECB are favourable but the earnings season is not going well for the European companies. ASML announced weak results, Deutsche Bank warned against rising bad debt due to morose economic environment and announced that it will set aside more money than expected to deal with soaring loans while the European car and luxury good makers are under the pressure of weakening demand at home and in China. Hermes is due to report earnings today and could reveal the slowest quarter in 3 years – a weakness that doesn’t concern business across the Atlantic Ocean.

On the contrary, the US big banks announced a strong quarter, TSM blew past expectations last week hinting that the US chipmakers have likely had a good quarter, Netflix did better than expected and Tesla – which has been struggling lately – came up with better-than-expected results yesterday, after the bell. The company reported a 8% revenue growth and a 17% jump in net income, said that their costs per vehicle were pulled down to the lowest levels (around $35’100), the operating margin got a boost from 7.6% to 10.8% since last year and Cybertruck reached profitability for the first time. Tesla shares jumped 12% in the afterhours trading. The latter could give a boost to the S&P500 and Nasdaq 100 after a few days of hesitation and retreat.