Sample Category Title

EUR/USD Daily Outlook

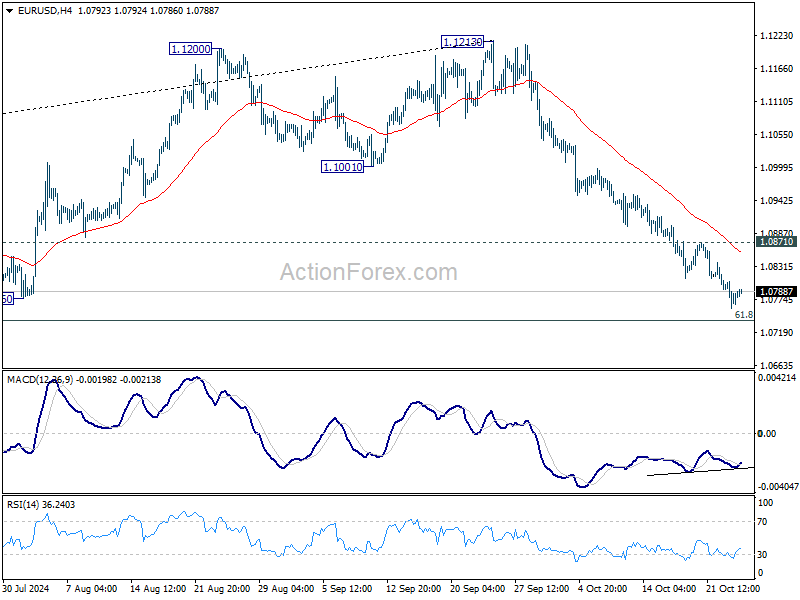

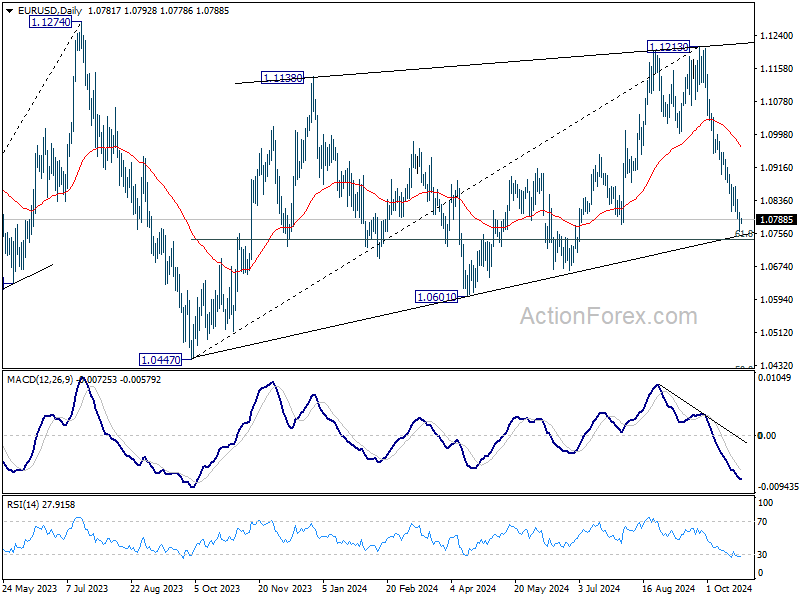

Daily Pivots: (S1) 1.0760; (P) 1.0783; (R1) 1.0806; More...

EUR/USD's fall from 1.1213 is in progress and intraday bias stays on the downside for 61.8% retracement of 1.0447 to 1.1213 at 1.0740. Firm break there will target 1.0601 support next. On the upside, break of 1.0871 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

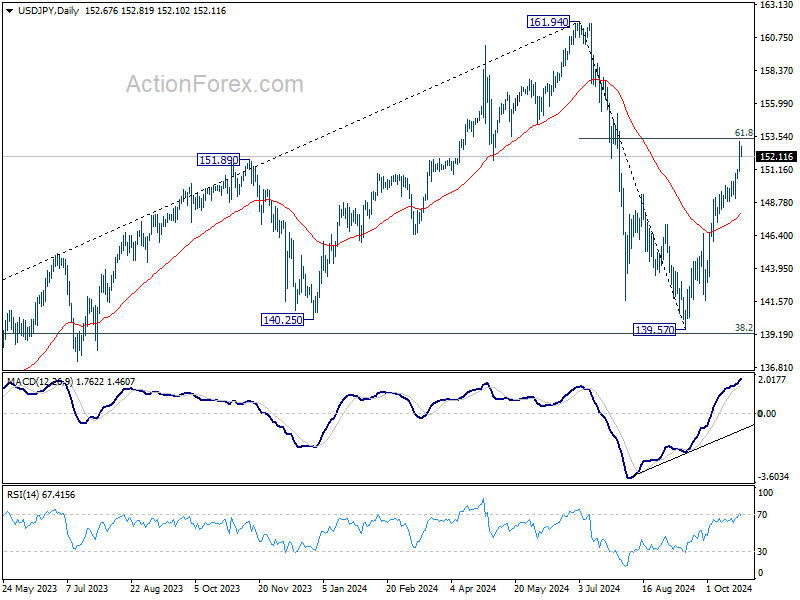

USD/JPY Daily Outlook

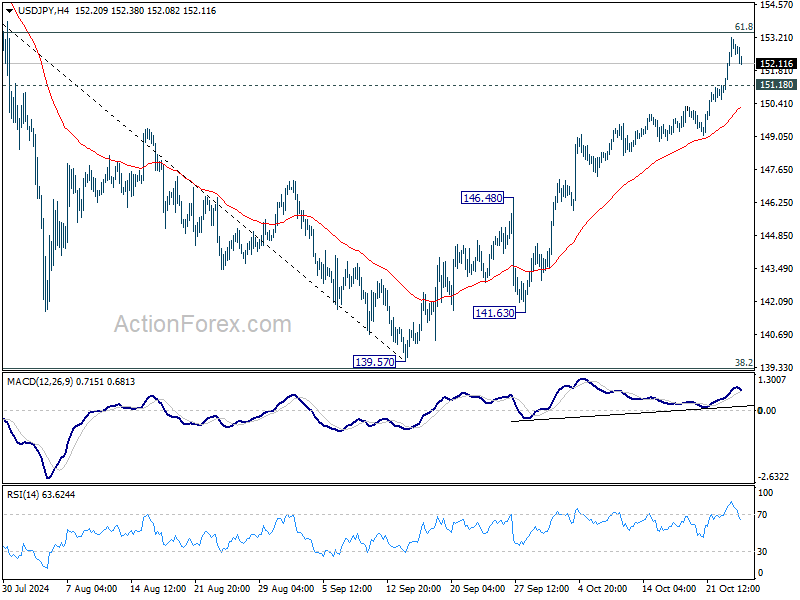

Daily Pivots: (S1) 151.45; (P) 152.32; (R1) 153.64; More...

Intraday bias in USD/JPY stays on the upside at this point. Decisive break of 61.8% retracement of 161.94 to 139.57 at 153.39 will extend the rally from 139.57 to retest 161.94 high. On the downside, below 151.18 minor support will turn intraday bias neutral first. But further rally will now remain in favor as long as 55 D EMA (now at 148.02) holds, in case of retreat.

In the bigger picture, price actions from 161.94 are seen as a corrective pattern to rise from 102.58 (2021 low). The range of medium term consolidation should be set between 38.2% retracement of 102.58 to 161.94 at 139.26 and 161.94. Nevertheless, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

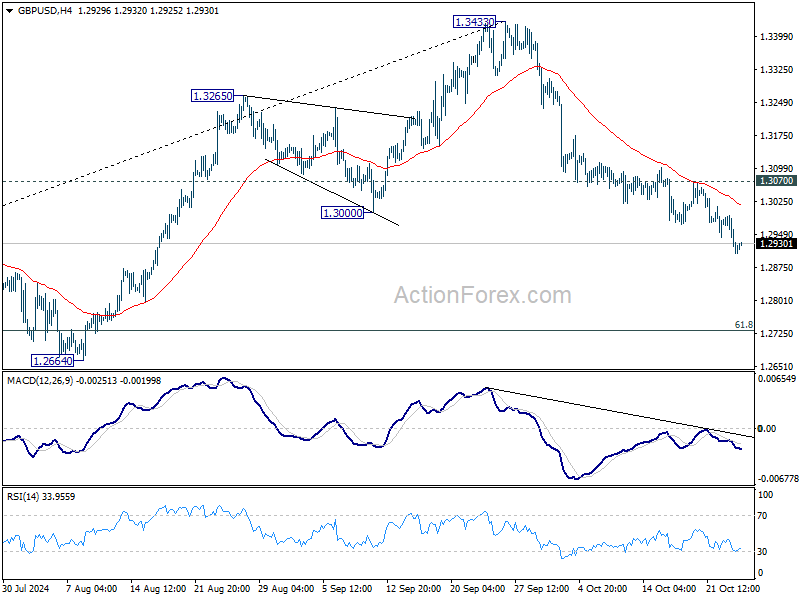

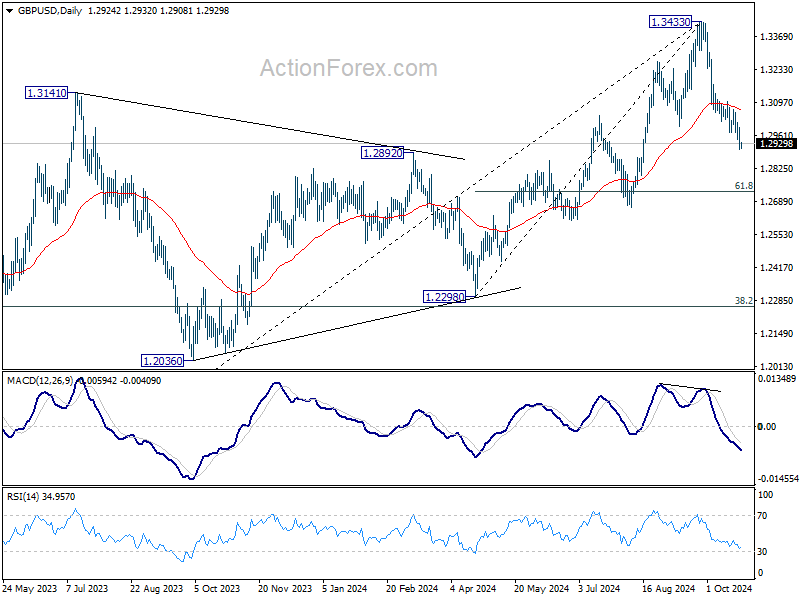

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2887; (P) 1.2941; (R1) 1.2974; More...

GBP/USD's fall from 1.3433 continues today and intraday bias stays on the downside. Deeper decline would be seen to 61.8% retracement of 1.2298 to 1.3433 at 1.2732. On the upside, above 1.3070 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, considering mildly bearish divergence condition in D MACD, a medium term top is likely in place at 1.3433 already. Price actions from there are seen as correction to whole up trend from 1.0351 (2022 low). Deeper decline would be seen to 38.2% retracement of 1.0351 to 1.3433 at 1.2256, which is close to 1.2298 structural support. Strong support should be seen there to bring rebound.

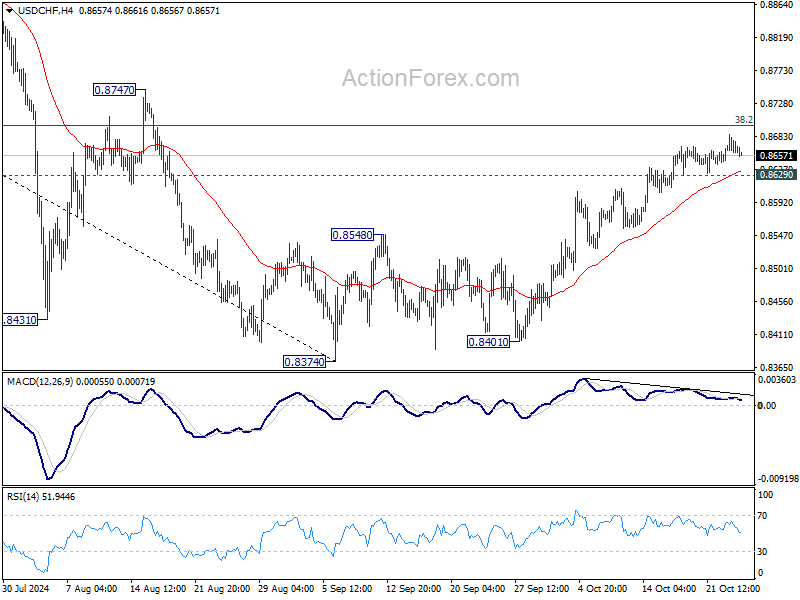

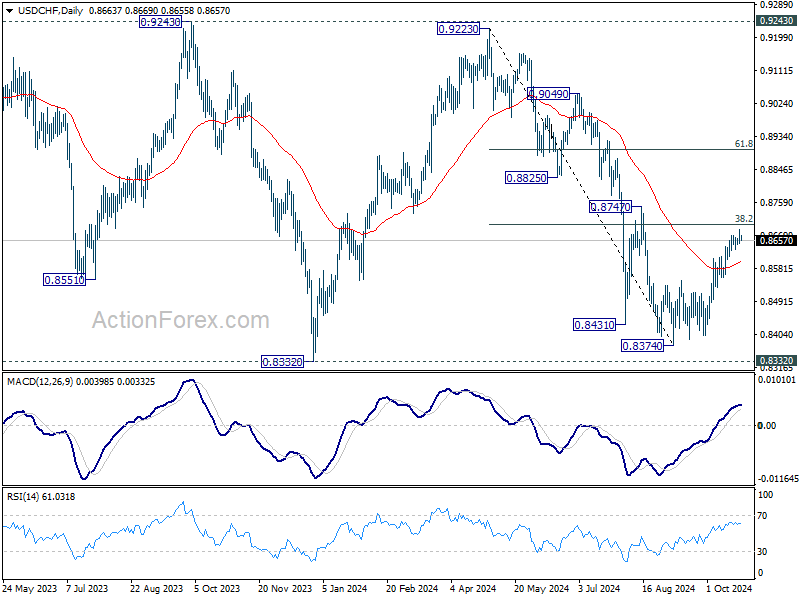

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8645; (P) 0.8666; (R1) 0.8684; More…

Further rally is in favor in USD/CHF with 0.8629 minor support intact, despite loss of momentum as seen in 4H MACD. Firm break of 38.2% retracement of 0.9223 to 0.8374 at 0.8698 will argue that fall from 0.9223 has completed at 0.8374, after defending 0.8332 low. Further rally should then be seen to 61.8% retracement at 0.8899 next. On the downside, below 0.8629 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

Big Rate Cut in Canada

In focus today

In the euro area, focus turns to the October flash PMIs. We expect the manufacturing sector to remain in contractionary territory, while still edging up to 45.4 from 45.0, due to the way in which the PMI index is constructed. We expect the service PMI to remain in growth territory but decline to 51.1 from 51.4 in September. The service PMI is likely supported by a rise in French service PMI following the unwind of the effect of the Olympic Games in August and September. Outside France however, we expect a slight slowdown in service PMIs reinforced by seasonality.

In the US, we also receive flash PMIs, which will likely signal continuing contraction in manufacturing activity and modest growth in services.

In the UK, flash PMIs for October are due for release as well and expected to remain close to unchanged north of the 50-mark.

In Japan, we receive Tokyo CPI Ex-Fresh Food which is expected to decline by 0.3% from 2.0% to 1.7%.

Economic and market news

What happened overnight

In Japan, Japanese Finance Minister Katsunobu Kato warned against currency speculation, as moves in the currency market drive down the yen's value with USD/JPY reaching 153. This comes hours after the BoJ Govenor Kazuo Ueda indicated a careful approach to raising interest rates, emphasizing the need to avoid moving too slowly. He warned that moving too slowly could create a build-up of speculative positions, potentially triggering a slide in the yen, pushing up import costs.

What happened yesterday

In Canada, the Bank of Canada cut its policy rate by 50bp to 3.75% in a move highlighting the new phase of Canadian monetary policy; namely one in which policy rates are brought back quickly to neutral levels amid inflation recently falling within the target interval. In the monetary policy report Bank of Canada stated that its neutral rate assumption remains 2.75% and that the current evaluation on the balance of risk has become balanced. To us this suggests that the base case from here should be another 100bp worth of rate cuts for the upcoming Canadian monetary policy announcements - likely in 50bp increments.

In the US, 10-year Treasury yields climbed to three-month highs as worries of a less dovish Federal Reserve spread. Equity markets dropped as higher yields pressured rate-sensitive mega caps, such as Nvidia (NVDA.O) and Apple (AAPL.O) declining by 3.57% and 3.05% respectively. Furthermore, McDonald's (MCD.N) plummeted by 4.88% after an E.coli infection linked to the fast-food chain killed one and sickened many.

In the EU, euro zone consumer confidence increased by 0.4 points to -12.5 from -12,9 in September. Consumer sentiment also rose in the European Union as a whole, reaching its long-term average after gaining 0.5 points to -11.2. In Denmark consumer confidence declined by 2.1 points to -8.9 from -6.8, reaching the lowest level this year as fears of recession overshadows worries about inflation. We anticipate a gradual rise in consumer confidence as purchasing power is restored and interest rates decline.

ECB President Christine Lagarde cooled market speculation advocating for a cautious and data-driven process. This comes in the wake of a recent push from several ECB policy makers voicing their concerns about undershooting the 2% inflation target and being open to speeding up rate cuts.

Equities: Global equities were lower for the third consecutive day yesterday. Much of what we observed could be reiterated from our previous commentary, as this is not a macro-driven sell-off characterised by a spike in volatility. However, a significant shift occurred yesterday with cyclicals being sold off, most notably with US tech underperforming. While specific company-related news may explain some of these movements, we interpret these events within a broader context. Over the past three months, for instance, US tech and tech sectors in general have been underperforming. With a bit of selective analysis, one can observe a considerable underperformance. This trend is not due to an unfavourable macro environment for tech; rather, it stems from the cessation of extreme earnings outperformance and highly elevated valuations. In the US, the performance yesterday was as follows: Dow -1.0%, S&P 500 -0.9%, Nasdaq -1.6%, and Russell 2000 -0.8%.

This morning, most Asian markets were cloaked in red, while European futures showed a mixed picture. US futures were influenced by late-hour earnings released yesterday, which drives growth-related futures higher.

FI: The front end of the euro curve led the bullish steepening of the curve as expectations for a jumbo cut from the ECB rose on the back of General Committee comments. The comments did not exclude the possibility of ECB cutting rates by more than 25bp at one point.

FX: USD rose further yesterday, where JPY was the big loser among G10 currencies. EUR/USD slipped below 1.08 and USD/JPY rose to 153. It was also a tough day for Scandies with EUR/NOK climbing above 11.80 and EUR/SEK above 11.40.

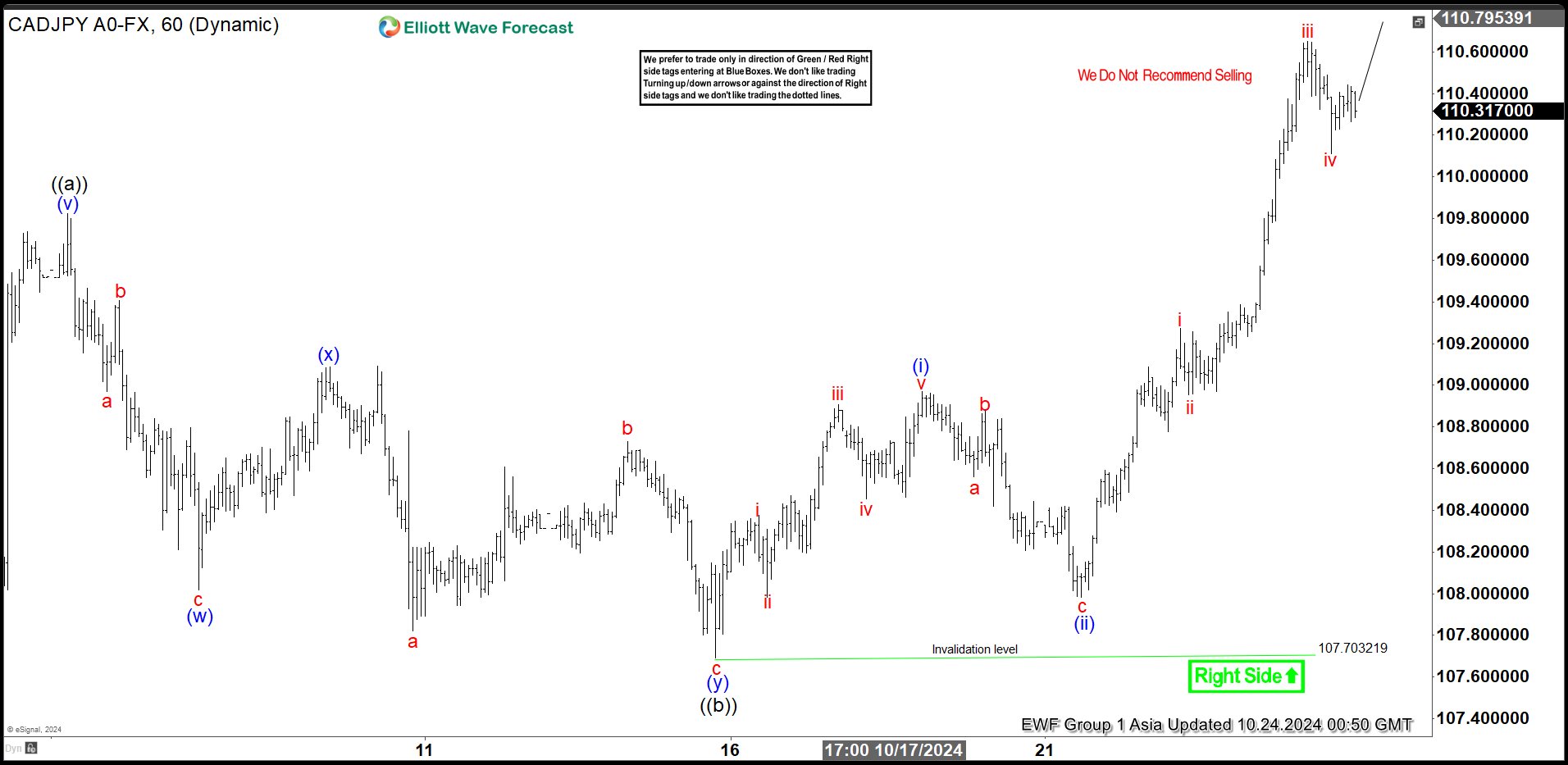

Elliott Wave View: CADJPY Has Reached Area Where Pullback Can Happen

CADJPY has already reached the extreme area from 8.5.2024 low. This suggests that pair is in the zone where it can start to see a pullback soon. Shorter cycle structure however looks incomplete and pair can see further upside a bit more. The rally from 9.30.2024 low is currently in progress as a zigzag Elliott Wave structure. Up from 9.30.2024 low, wave ((a)) ended at 109.82 and pullback in wave ((b)) ended at 107.69. Internal subdivision of wave ((b)) unfolded as a double three structure. Down from wave ((a)), wave (w) ended at 108.02 and wave (x) ended at 109.087. Wave (y) lower ended at 107.7 which completed wave ((b)) in higher degree.

Pair has resumed higher in wave ((c)). Up from wave ((b)), wave (i) ended at 108.97 and pullback in wave (ii) ended at 107.98. Expect 1 more push higher to complete wave (iii), then it should pullback in wave (iv) to correct cycle from 10.21.2024 low in 3, 7, or 11 swing before it resumes higher again. Near term, as far as pivot at 107.7 low stays intact, expect pullback to find buyers in 3, 7, or 11 swing for further upside.

CADJPY 60 Minutes Elliott Wave Chart

CADJPY Elliott Wave Video

https://www.youtube.com/watch?v=h2kbRi4ludo

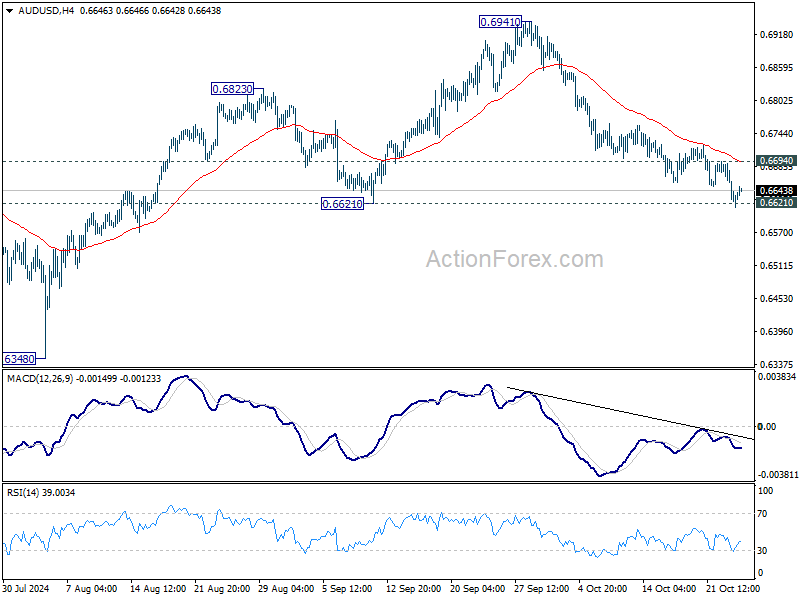

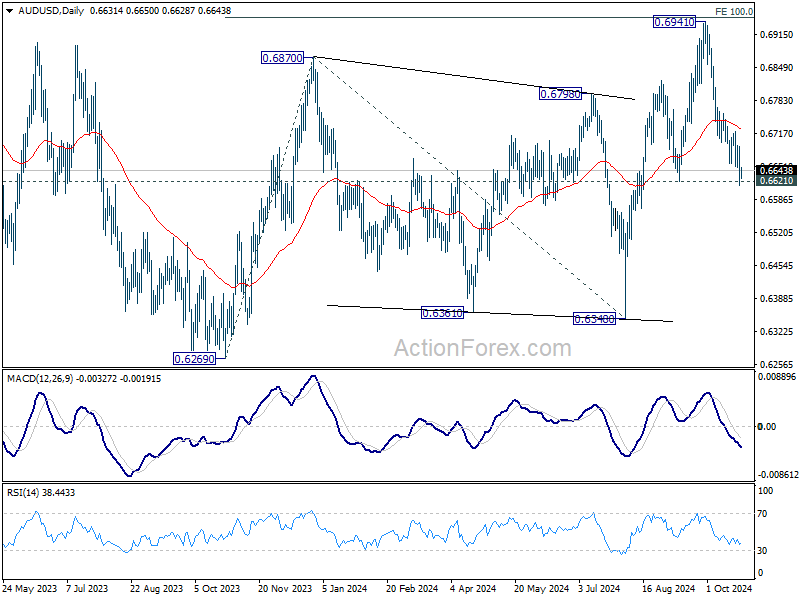

AUD/USD Daily Report

Daily Pivots: (S1) 0.6601; (P) 0.6647; (R1) 0.6679; More...

AUD/USD's fall from 0.6941 is in progress and intraday bias stays on the downside. Firm break of 0.6621 support should confirm near term bearish reversal after topping at 0.6941. Deeper decline should then be seen to 0.6348 support next. On the upside, above 0.6694 minor resistance will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941 will target 138.2% projection at 0.7179. However, break of 0.6621 support will argue that rise from 0.6269 has completed and bring deeper fall back to 0.6269/6348 support zone.

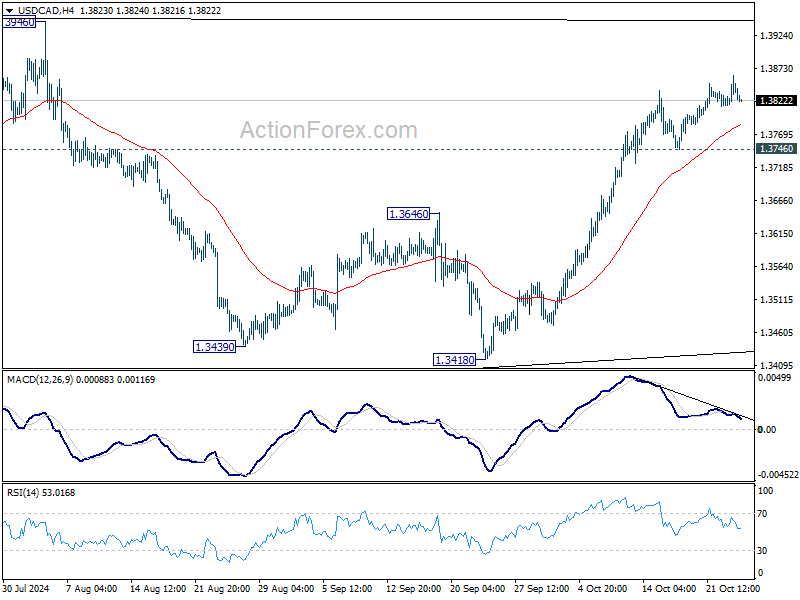

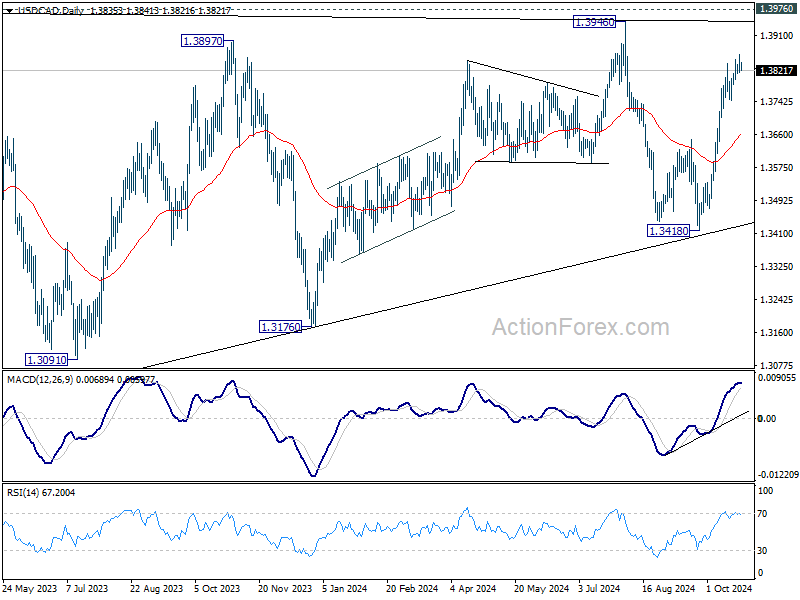

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3814; (P) 1.3839; (R1) 1.3861; More...

Rise from 1.3418 is still in progress in USD/CAD despite loss of upside moment as seen in 4H MACD. Next target is 1.3946/76 key resistance zone. Strong resistance might be seen there to limit upside. However, break of 1.3746 support will confirm short term topping, and turn bias back to the downside.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

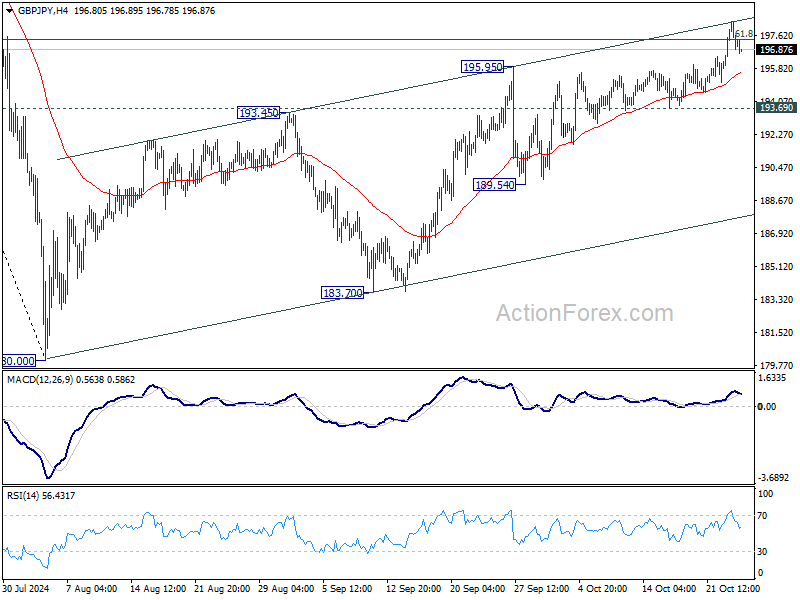

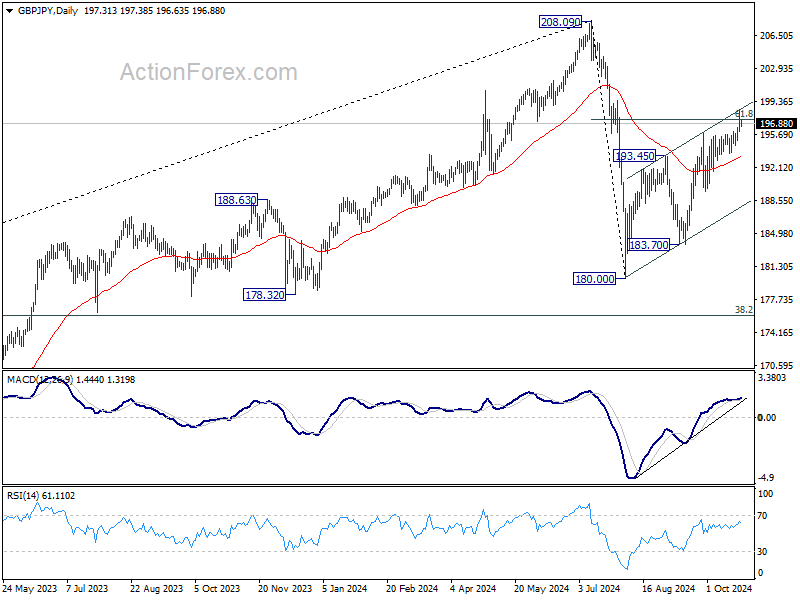

GBP/JPY Daily Outlook

Daily Pivots: (S1) 195.97; (P) 197.20; (R1) 198.63; More...

Intraday bias in GBP/JPY stays on the upside at this point. Sustained trading above 61.8% retracement of 208.09 to 180.00 at 197.35 will target 208.09 high. On the downside, break of 193.69 support is needed to indicate short term topping. Otherwise, further rally will remain in favor in case of retreat.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

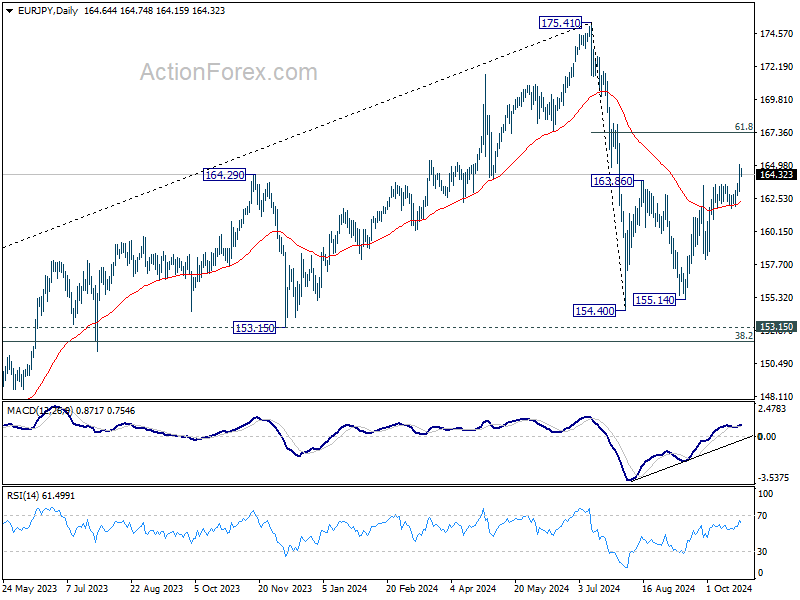

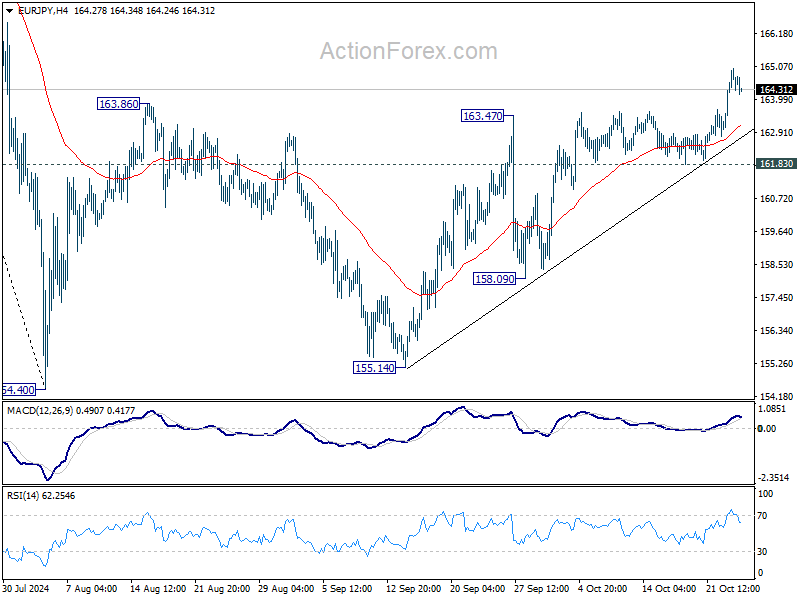

EUR/JPY Daily Outlook

Daily Pivots: (S1) 163.50; (P) 164.26; (R1) 165.47; More....

Intraday bias in EUR/JPY remains on the upside for the moment. Rise from 155.14 is in progress and should target 61.8% retracement of 175.41 to 154.40 at 167.38. Sustained break there will pave the way to retest 175.41 high. On the downside, break of 161.83 support is needed to indicate short term topping. Otherwise, further rally will remain in favor even in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.