Sample Category Title

EURJPY: Trade Projection

The EURJPY pair hit a new 14-week high near 164.50 during the European session on Wednesday. This rise comes even as some European Central Bank (ECB) officials hint that the Deposit Facility Rate, currently at 3.25%, might drop below neutral levels due to worries about low economic growth in the Eurozone. Officials believe inflation could stay below 2%, and Germany's economy is expected to shrink by 0.2% this year, marking the second year of contraction.

While traders have already factored in another ECB rate cut in December, this has weakened the Euro against other major currencies. However, the Euro has strengthened against the Japanese Yen amid uncertainty around whether the Bank of Japan (BoJ) will raise interest rates this year. BoJ's next meeting is set for October 31, but many expect no rate hikes, especially with upcoming U.S. elections adding to global economic uncertainty.

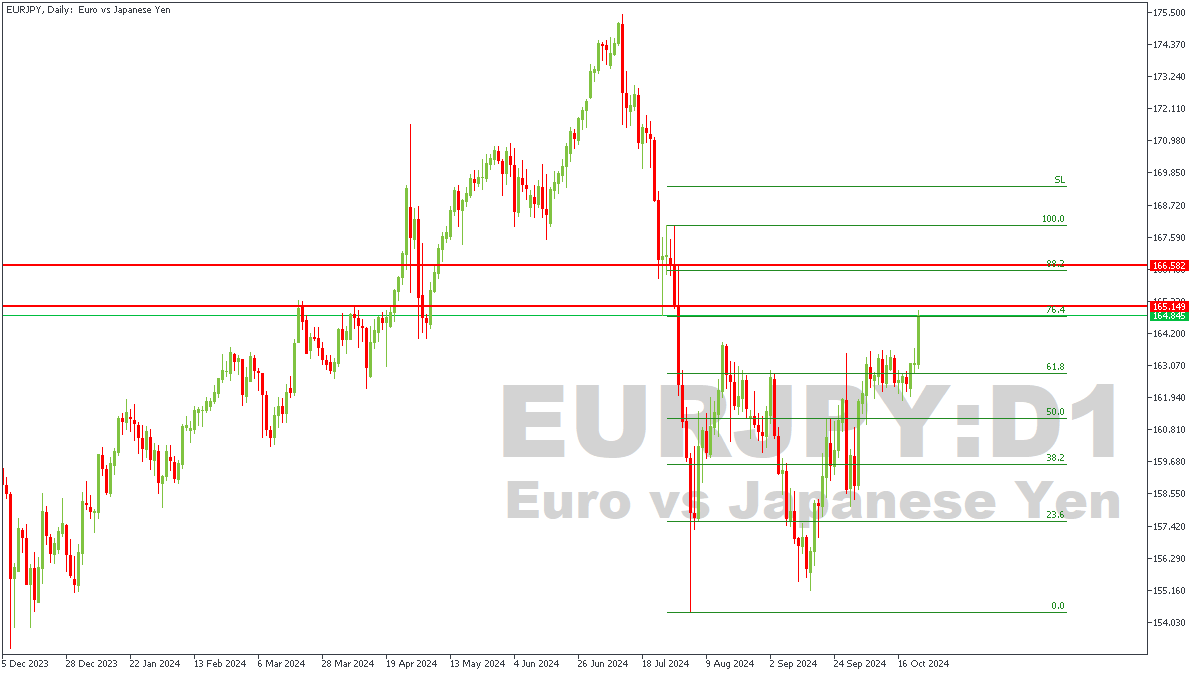

EURJPY – D1 Timeframe

Price recently broke below the previous low, and has reached the pivot zone on the daily timeframe of EURJPY, with an impulsive move over the last couple of hours. The pivot zone falls within the 76% of the Fibonacci retracement, which is another crucial confluence in favor of the bearish continuation. The pivot zone also overlaps a critical rally-base-drop supply zone; a change of character on the lower timeframe would be an optimal entry for a bearish movement.

Analyst’s Expectations:

- Direction: Bearish

- Target: 159.667

- Invalidation: 166.709

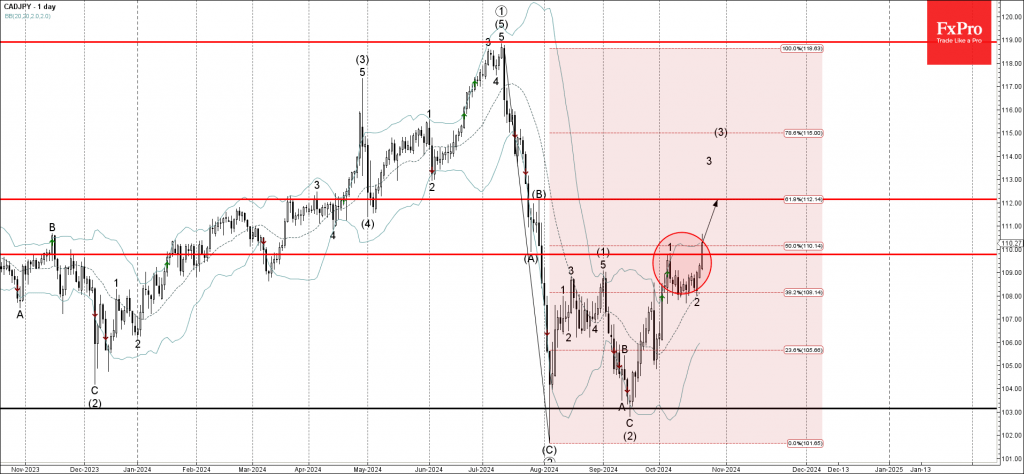

CADJPY Wave Analysis

- CADJPY broke resistance zone

- Likely to rise to resistance level 112.00

CADJPY recently broke the resistance zone between the resistance level 110.00 (which stopped the previous impulse wave 1) intersecting with the 50% Fibonacci correction of the downward correction from the start of July.

The breakout of this resistance zone accelerated the active short-term impulse wave 3 of the higher impulse wave (3) from the start of September.

Given the strongly bearish yen sentiment seen across the FX markets today, CADJPY can be expected to rise toward the next resistance level 112.00 (which stopped the previous correction B).

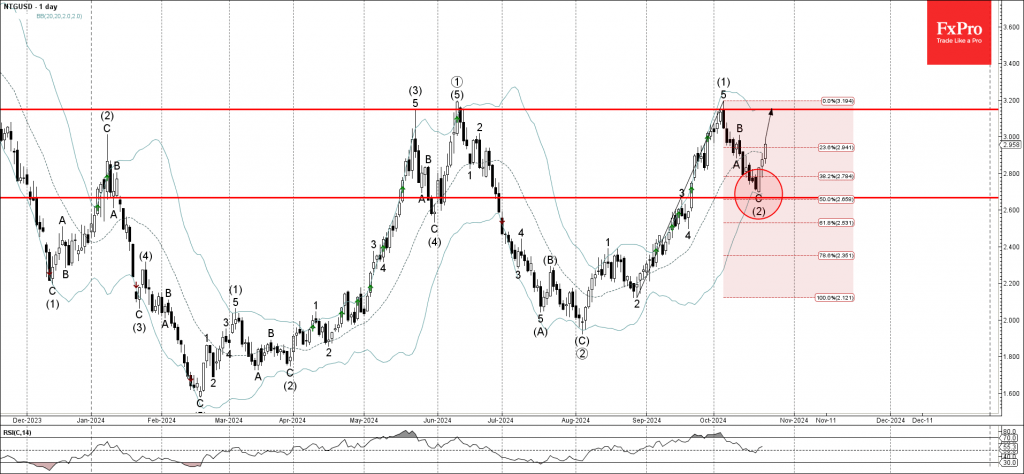

Natural Gas Wave Analysis

- Natural gas reversed from support zone

- Likely to rise to resistance level 3.150

Natural gas recently reversed up from the support zone between the support level 2.665 (former minor resistance from September) intersecting with the lower daily Bollinger Band and the 50% Fibonacci correction of the upward impulse from August.

The upward reversal from this support zone started the active medium-term impulse wave (3) – which belongs to the longer-term impulse wave 3.

Natural gas can be expected to rise toward the next resistance level 3.150 (which stopped the three earlier impulse waves (3), (5) and (1)).

ECB’s Lagarde satisfied with inflation progress, eyes growth impact on policy

At an event today, ECB President Christine Lagarde expressed contentment with the current inflation levels, stating that the central bank is "rather satisfied" as inflation has slowed to below the 2% target.

However, she emphasized that the central bank is keeping a close watch on economic growth, as it significantly influences inflationary trends. Lagarde pointed out, "We are attentive to growth because it impacts inflation. It’s different from the Fed,” highlighting a key difference in policy focus compared to Fed.

Separately, Chief Economist Philip Lane acknowledged that while "some of the recent data raised some questions about the recovery," the overall outlook remains positive.

Lane affirmed that the narrative of a good economic recovery is still "very close to the baseline." Lane highlighted "fundamental reasons" to expect a rebound in consumption and investment for the remainder of this year and into the next.

BoC Accelerates Pace of Rate Cuts

The Bottom Line:

- The BoC made the leap to cut the overnight rate by 50 bps today, amid accumulating evidence that the economy and labour markets are weakening by more than what is necessary to achieve the 2% inflation target.

- The reduction won’t be the last one. The level of the overnight rate is still restrictive at 3.75% and the BoC in the press release hinted at future rate cuts will follow to support a return to stronger GDP growth.

Impact to Our Forecasts:

- We continue to expect one more 50-bps rate cut from the BoC this December to bring the overnight rate to the top end of the BoC’s estimate of its neutral range (3.25%) before a return to a more gradual pace of easing in 2025.

- Our base-case macroeconomic forecasts are weaker than the BoC’s. We think real GDP growth is more likely to stay subdued for longer in Canada as interest rates remain restrictive until 2025.

- We expect GDP growth of 1.3% in 2025, below the BoC’s projection of 2.1% and not meaningfully different from ~1% growth expected for this year.

- We also expect labour markets will continue to soften, with unemployment rate rising to 7% in the coming quarters and for softening activities combined to bring more disinflationary pressures in 2025.

- In terms of the terminal level of interest rates, we think BoC will cut to 2% by July next year, stimulative and a touch below the lower bound of the BoC’s own estimates of neutral rate at 2.25% - 3.25%.

The Details (meeting recap):

- BoC’s rate cut today was close to fully priced in in markets ahead of the meeting. Adding to odds of the 50-bps cut were the Q3 Business Outlook Survey and September’s inflation data last week, both pointed to lower present and future expected inflation in Canada.

- Governor Macklem led off his press conference saying that “we are back to low inflation” in Canada. Rather than focusing on a weak economy and the disinflation pressures that could follow, the BoC today highlighted balanced risks on inflation.

- On the upside, shelter and wage growth remain the main concerns but are both expected to slow. On the downside, a slower economic recovery (as we are anticipating) is "the biggest risk".

- With the output gap still deeply negative (the BoC's estimate was -0.75% to -1.75% in Q3) and monetary policy still restrictive, we think it'll take longer for demand to rebound and excess supply in the economy to be absorbed.

- Rate cuts will boost the economy with a lag. Even with interest rates moving lower, many borrowers can continue to expect debt payments to go up in the years ahead. That speaks to more urgency to “front-load” the easing.

Bank of Canada Accelerates Rate Cuts, Points to Greater Confidence in Inflation

The Bank of Canada (BoC) cut its overnight rate by 50 basis points, to 3.75%, while stating that it will continue with normalizing its balance sheet.

With inflation having "declined significantly" over the last few months, the bank said it "expects inflation to remain close to the target over the projection horizon." Notably in the Bank's Monetary Policy report (MPR), the quarterly forecast for core inflation is unchanged at +2%.

The bank highlighted the moderate pace of economic growth, stating "the economy grew at around 2% in the first half of the year and we expect growth of 1¾% in the second half. Consumption has continued to grow but is declining on a per person basis." The Bank expected GDP growth to "strengthen gradually" over the coming quarters supported by lower interest rates.

On the future path of policy, the bank noted that "if the economy evolves broadly in line with our latest forecast, we expect to reduce the policy rate further." However, it also noted that the timing and pace of further reductions will be guided by the data.

Key Implications

Now that headline CPI inflation has dropped below the 2% target, the BoC has gained confidence that it can cut rates at a quicker pace. While there isn't much in the way of a changing economic narrative - slow GDP growth and core inflation above 2% remain - the central bank is set on doing what it can to boost economic growth. Will a 50 bp move achieve this? Probably not, but the central bank felt it should do something with economic data continuing to show that the country is stuck in a rut. Hopefully we get a bit more clarity on this in the press conference.

This won't be the end of rate cuts. Even with the succession of policy cuts since June, rates are still way too high given the state of the economy. To bring rates into better balance, we have another 150 bps in cuts penciled in through 2025. So while the pace of cuts going forward is now highly uncertain, the direction for rates is firmly downwards.

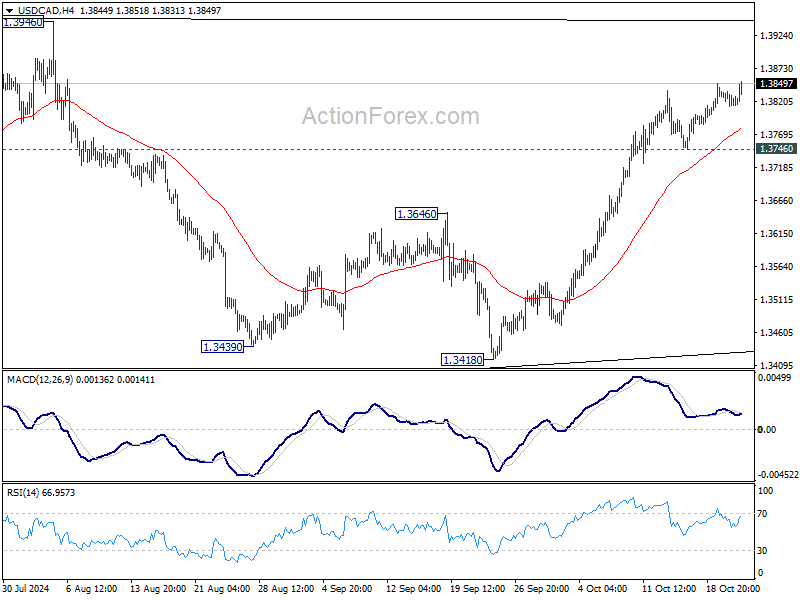

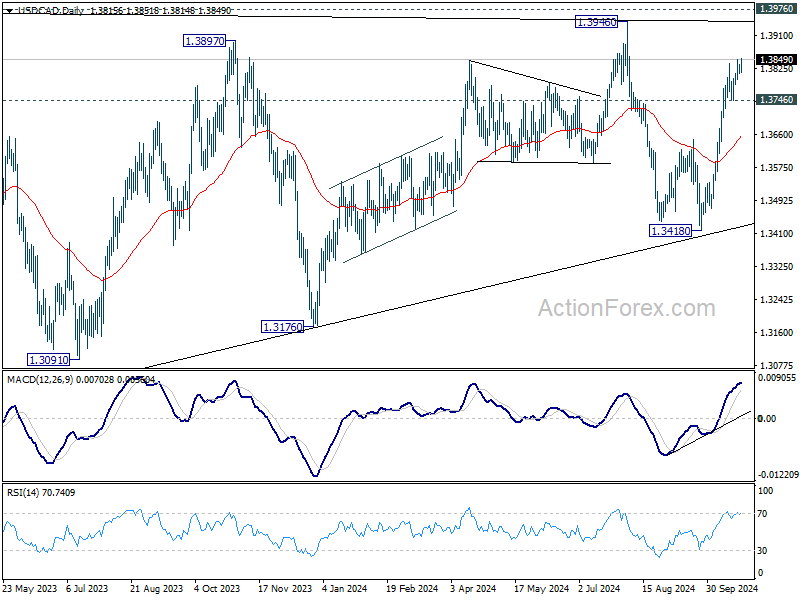

USD/CAD Mid-Day Outlook

Daily Pivots: (S1) 1.3805; (P) 1.3825; (R1) 1.3835; More...

USD/CAD's from 1.3418 is extending in early US session. Intraday bias stays on the upside for retest of 1.3946/76 key resistance zone. Strong resistance might be seen there to limit upside. However, break of 1.3746 support is needed to confirm short term topping. Otherwise, further rise will remain in favor in case of retreat.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

Debate heats up at ECB on possibility of a 50bps cut in Dec

A growing debate is emerging among ECB policymakers about whether to accelerate the pace of rate cuts, with some members suggesting a potential 50 bps reduction in December. The possibility arises after inflation data in September came in significantly lower than expected, fueling discussions on the appropriate policy response.

Portuguese ECB Governing Council member Mario Centeno signaled openness to a larger cut, telling CNBC, “Certainly 50 basis points can be on the table because we continue to be data dependent and the data we are getting points in that direction.” He emphasized the surprising nature of the recent inflation figures, stating, “The truth is that the print of inflation in September was very low, way lower than what we were expecting.”

Echoing the possibility of a sizable rate reduction, Dutch ECB Governing Council member Klaas Knot acknowledged that a half-point interest rate cut could not be excluded at the December meeting. However, he cautioned that such a move would require further economic deterioration. “I would also say that I see the risks surrounding that baseline as reasonably contained,” Knot added, suggesting that while the option is on the table, it is not yet the central scenario.

On a more cautious note, Austrian ECB Governing Council member Robert Holzmann expressed skepticism about the need for a 50 bps cut under current conditions. Speaking to CNBC, Holzmann said, “I’m sure some of my colleagues will go for a big cut, others not. In my case, I will say I will look at the data.” He added, “If things really get as bad as some claim, we can have another 25, 50 I would say at the moment with the data, no.”

Sunset Market Commentary

Markets

Yesterday’s ECB comments coming from Washington (IMF World Economic Outlook) almost exclusively sounded dovish. The disinflation process is running faster than hoped, downside growth risks might accelerate the process and even result in an inflation undershoot and more rate cuts towards neutral are coming. Central bankers didn’t push back against growing market odds of a 50 bps rate cut at the December meeting even if we still get two PMI surveys (starting tomorrow), two inflation readings, Q3 GDP data and Q3 wage numbers. Press agency Reuters this morning added to the debate. Citing sources close to discussions, they ran an article suggesting that ECB officials are starting to debate whether interest rates will need to be lowered to a level that stimulates economic activity i.e. below neutral (<2%). A small, but growing group of governors fears that the central bank fell behind the curve. They also want to drop the reference to restrictive rates in the policy statement to show that they are taking downside risks seriously. The current phrasing is: “the Governing Council is determined to ensure that inflation returns to its 2% medium-term target in a timely manner. It will keep policy rates sufficiently restrictive for as long as necessary to achieve this aim.” German Bunds outperform US Treasuries on the growing divergence between ECB and Fed. The German yield curve bull steepens with front end yields sinking up to 7 bps. US yields add 1.8 bps (2-yr) to 3.7 bps (10-yr) as the focus remains on November 5th presidential elections and a Trump risk premium. The single currency succumbs to growing pressure with EUR/USD changing hands below 1.0778 support. A sustained break, eg in case of weak PMI’s tomorrow, opens the path to the April low at 1.0601. EUR/GBP did a second attempt to take out the 0.83 big figure, but seems to be waiting for the thumbs up by BoE governor Bailey who speaks in Washington as well tonight. The trade-weighted dollar adds to this month’s impressive rally with DXY rising to 104.50 for the first time since early August payrolls and following market-meltdown. Full retracement to the 106-106.50 is the most likely way forward from a technical point of view. JPY is obviously the biggest victim of higher US yields and the stronger dollar. USD/JPY today surges from 151 to 153, putting the Bank of Japan again in a difficult position with JPY weakness adding to the policy & inflation puzzle. USD/CAD tests the recent top around 1.3850 after the Bank of Canada accelerated its cutting cycle to a 50 bps move (4.25% to 3.75%) meant to boost growth and keep CPI close to 2%. More rate cuts are coming with data determining the pace. The BoC lowered its CPI outlook to 2.5%-2.2%-2% for the 2024-2026 policy horizon with the GDP outlook little changed at 1.2%-2.1%-2.3%.

News & Views

National Bank of Poland member Kotecki said that weaker retail sales (-5.7% M/M & -3% Y/Y in September vs -1% & +1.8% expected) data give hope for a somewhat faster decline in inflation, but at present the conditions for any policy modification are not yet met. Kotecki assessed the retail sales data as worrying, but wants further information to draw conclusions. At the same time he pointed out that headline inflation since July is again rising, admittedly due to temporary factors, and that the peak is still ahead of us. Core inflation also stopped declining, indicating that conditions are not in place to modify policy. He concluded that data point to moderate economic recovery but at the same time relatively persistent inflation. High wage growth remains a source of concern. Given the weak economy in Europe, Kotecki finds the 3.9% expected 2025 growth in the Polish budget as too optimistic. The zloty weakness substantially further today with EUR/PLN jumping from the 4.32 area to currently 4.345.

South African headline inflation printed at 0.1% M/M in September, slowing the headline figure to 3.8% from 4.4% in August, the lowest since March 2021 and dropping back below the mid-point of the South African Reserve Bank’s (SARB) 3%-6% target. The decline was supported by positive base effects compared to last year and transport inflation (-2.8% Y/Y). Food price inflation was 4.7% Y/Y, but the monthly rise (0.6%) was the fastest since January. Core inflation (ex-food and energy) was 0.3% M/M and 4.1% Y/Y (also 4.1% in August). The SARB cautiously cut its policy rate for a first time in September by 25 bps from 8.25% to 8%. Inflation data keep the door open for gradual follow-up cuts (next meeting on Nov 21). The rand, which had a good run between February and end September, is losing some further ground today, trading at USD/ZAR 17.7 (compared to a YTD low at 17.03 end September).