Sample Category Title

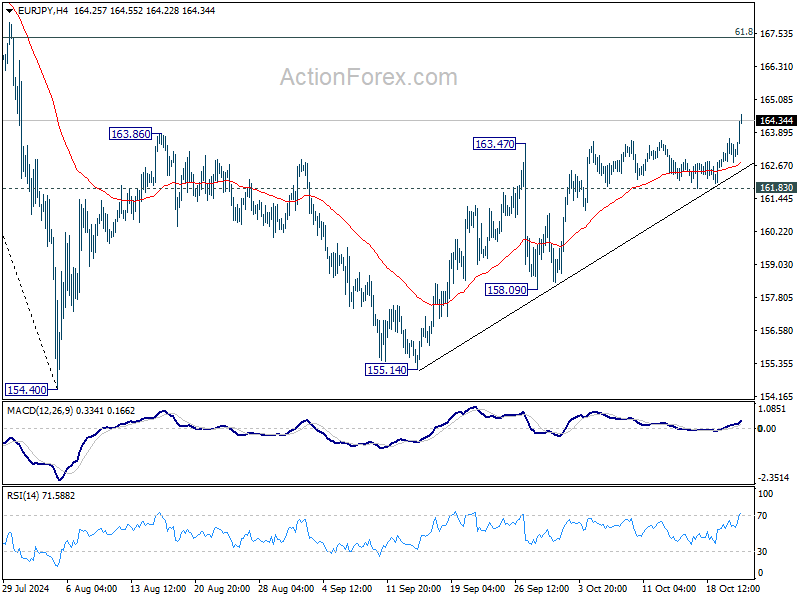

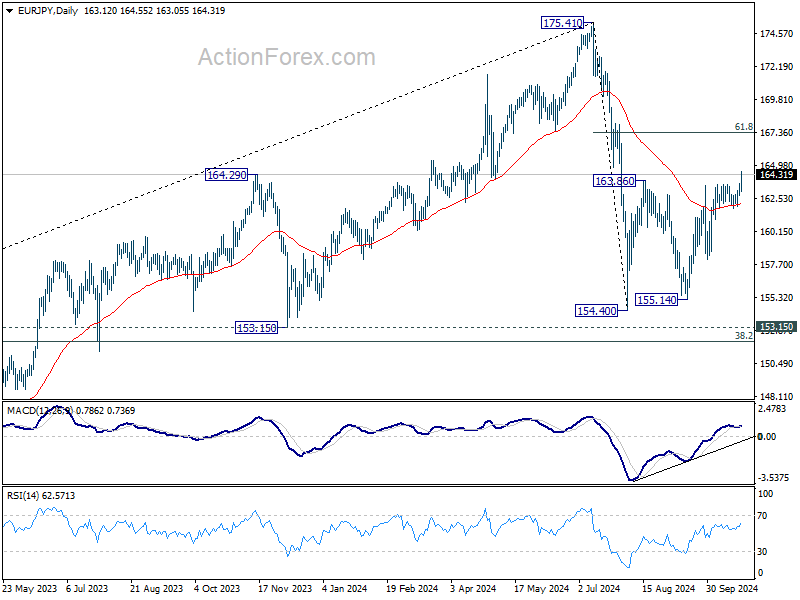

EUR/JPY Daily Outlook

Daily Pivots: (S1) 162.74; (P) 163.20; (R1) 163.62; More....

EUR/JPY's rebound from 154.40 finally resumed by breaking through 163.86 resistance. Intraday bias is back on the upside for 61.8% retracement of 175.41 to 154.40 at 167.38. Su stained break there will pave the way to retest 175.41 high. On the downside, break of 161.83 support is needed to indicate short term topping. Otherwise, further rally will remain in favor even in case of retreat.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

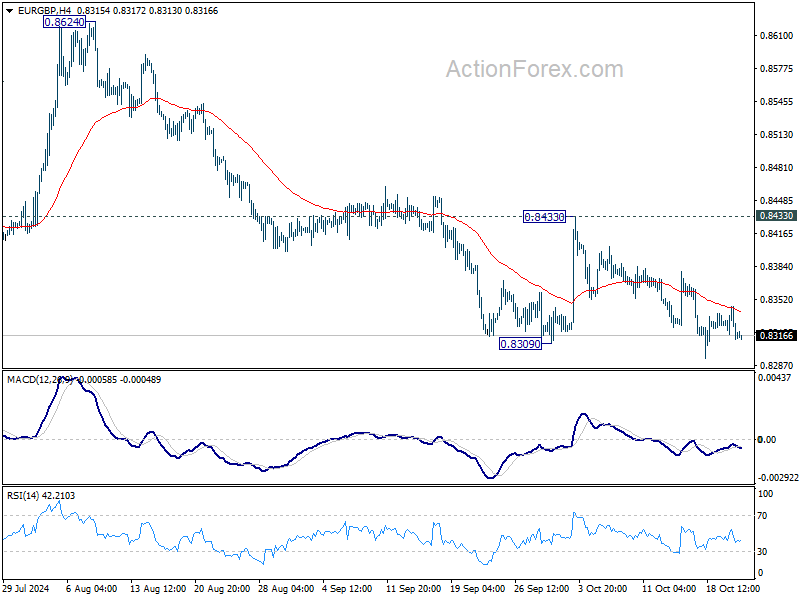

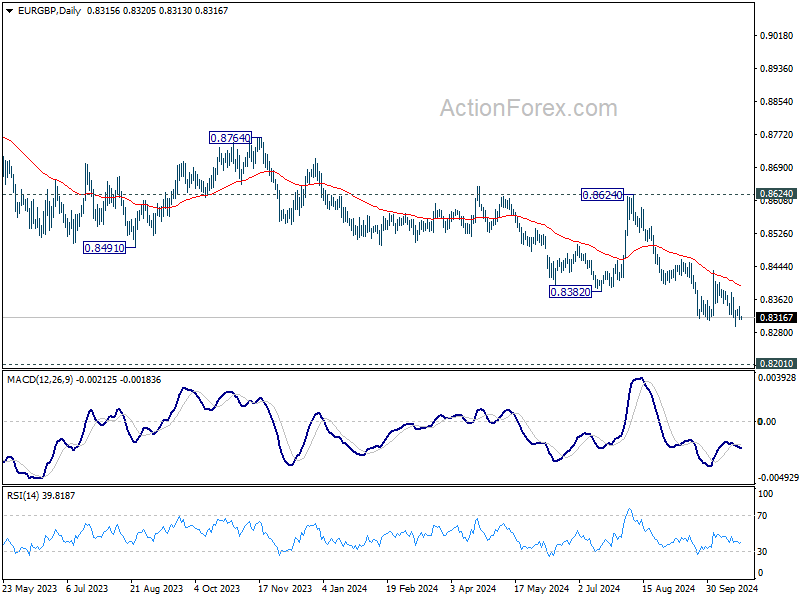

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8304; (P) 0.8326; (R1) 0.8337; More...

No change in EUR/GBP outlook. As long as 0.8433 resistance holds, current down trend is still in progress for 0.8201 key support next. Strong support could be seen from there to bring rebound. But for now, break of 0.8433 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 (2022 low), but strong support should be seen there to bring rebound. However, outlook will remain bearish as long as 0.8624 resistance holds even in case of strong rebound. Decisive break of 0.8201 will indicate long term bearish reversal.

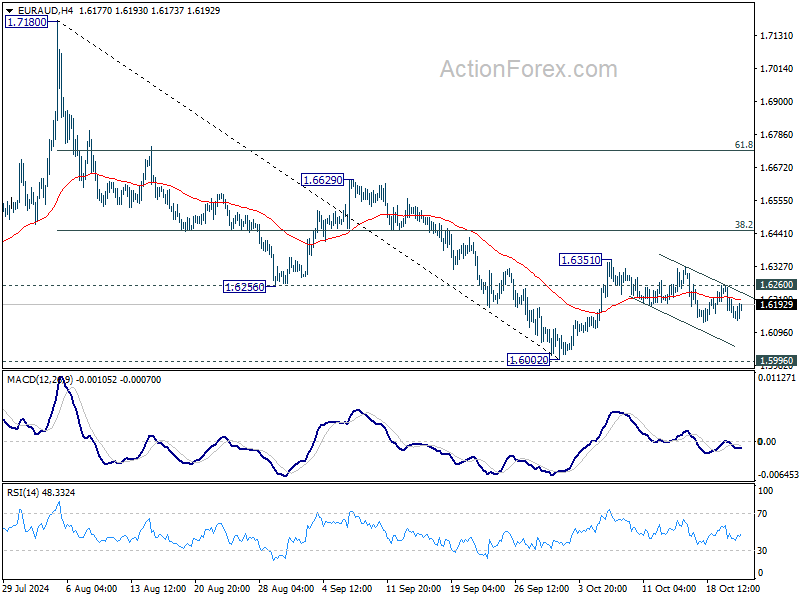

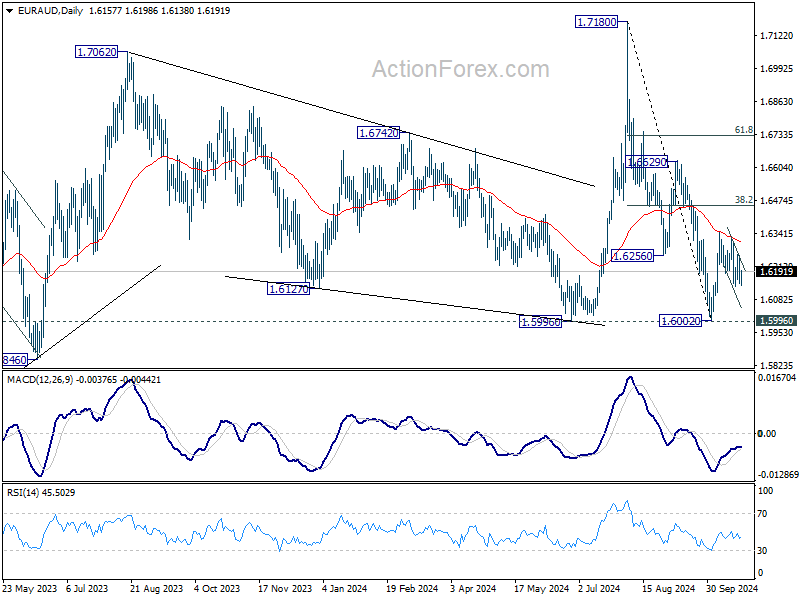

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6118; (P) 1.6190; (R1) 1.6231; More...

Further decline is mildly in favor in EUR/AUD as long as 1.6260 minor resistance holds. But considering that price actions from 1.6531 are corrective in nature, downside should be contained above 1.6002 low. On the upside, break of 1.6260 will turn bias back to the upside to resume the rebound from 1.6002. Next target will be 38.2% of 1.7180 to 1.6002 at 1.6452.

In the bigger picture, as long as 1.5996 cluster support holds (38.2% retracement of 1.4281 to 1.7062 (2023 high) at 1.6000), up trend from 1.4281 (2022 low) is still expected to resume at a later stage. However, decisive break of 1.5996 will argue that the medium term trend has reversed and turn outlook bearish.

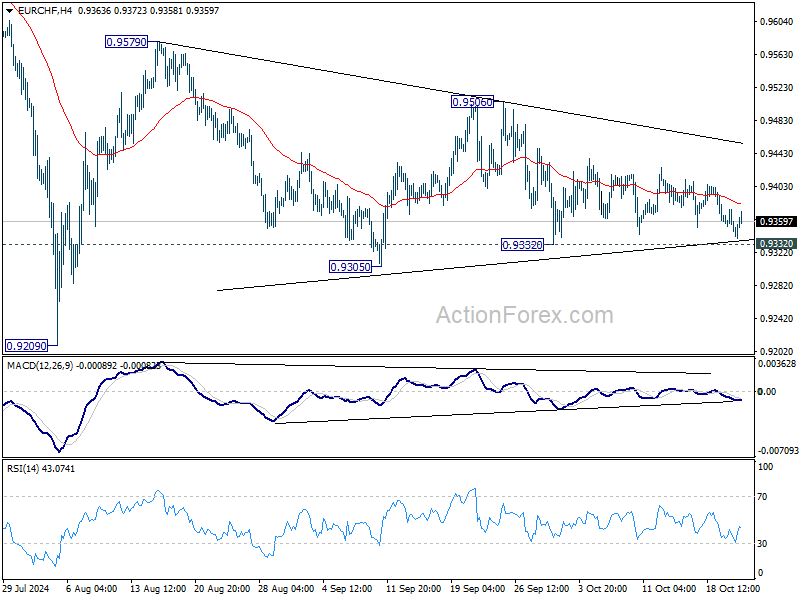

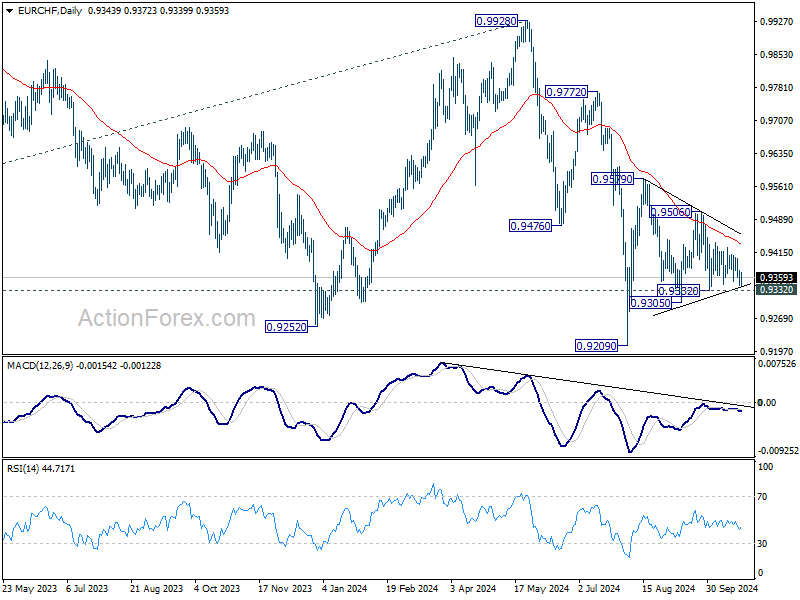

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9334; (P) 0.9355; (R1) 0.9367; More....

EUR/CHF recovered ahead of 0.9332 support as range trading continued. Intraday bias stays neutral for the moment. On the downside, break of 0.9332 will resume the fall from 0.9579 towards 0.9209 low. On the upside, break of 0.9506 will turn intraday bias to the upside for 0.9579 resistance and above.

In the bigger picture, fall from 0.9928 is seen as part of the long term down trend. Repeated rejection by 55 D EMA (now at 0.9432) keeps outlook bearish for breaking through 0.9209 low at a later stage. Nevertheless, sustained trading above 55 D EMA will confirm medium term bottoming and bring stronger rebound back towards 0.9928 key resistance.

US Note Future Keeps Drifting Away

Markets

Core bonds closed near/below Monday’s sell-off lows despite a very brief intraday rebound attempt. US yields closed up to 2 bps higher at the front end with German yields grinding 2.5 bps – 3.5 bps higher across the curve. During overnight Asian trading, the US Note future keeps drifting away. We set out before that this move, together with USD strength (EUR/USD closed below 1.08 for the first time since August 1st), is a momentum trade going into US Presidential elections. Both president-candidates are running on a platform of fiscal stimulus (Trump > Harris) on top of already bloated public finances. Yesterday’s Bund underperformance was somewhat at odds, especially at the front end of the curve, with most ECB comments tilting to the soft side. ECB Centeno doesn’t believe that the projected inflation uptick in the final months of the year will reach much above 2%. At the same time, the EMU is not growing, investment is almost flat and labor market resilience is faltering. He therefore sees a risk of undershooting the inflation target, suggesting a gradual continuation towards neutral policy rate levels. Centeno sees neutral at about 2% or slightly below. If data deteriorate further, Centeno is willing to step it up (50 bps rate cut) on the path to neutral. ECB President Lagarde confirmed that the direction of travel is clear and that the pace will be determined on the basis of backward- and forward-looking elements pointing to inflation sustainably returning to the 2% inflation target. That’s expected to happen somewhere next year. Some components likes services inflation remain sticky, but wage pressure for example shows signs of abating. With these comments, Lagarde in any case doesn’t push back against building market odds (50/50) that the ECB could lower its policy rate by 50 bps in December already. Tomorrow’s PMI surveys are the first of a number of data in the long build-up to that meeting. ECB Holzmann pointed out that the disinflation process is running faster than expected with ECB Villeroy flagging significant downside risks to both growth and inflation, suggesting that the ECB can’t err on the side of leaving its restrictive policy in place for too long. ECB Rehn warned as well that weaker growth could increase disinflationary pressures. Today’s eco calendar contains another avalanche of central bank speakers while eco data are confined to EMU consumer confidence and the release of the Fed’s Beige Book. We don’t fight ruling market trends.

News & Views

The IMF in its updated World Economic Outlook lowered global output growth in 2025 by 0.1 ppt to 3.2% while keeping the one for this year unchanged at 3.2%. US forecasts were lifted for both 2024 and 2025 to 2.8% (+0.2 ppts) and 2.2% (+0.3 ppts) on stronger consumption. Persistent weakness in manufacturing in Germany and Italy pushed the euro area prognosis down for this year (0.8%, -0.1 ppt) and 2025 (1.2%, -0.3 ppts). China over the same horizon was cut to 4.8% and left unchanged at 4.5% respectively. Inflation should slow from 5.8% this year to 4.3% in the next. The new estimates come with several warnings. Risks are building to the downside and uncertainty is growing on geopolitics and regional conflicts, the rise of protectionism and potential trade disruptions. Tariffs and trade uncertainty could shave 0.5 ppt of global economic output in 2026, the IMF’s chief economist said. It once again stressed the need to stabilize borrowing. Risks to the debt outlook are heavily tilted to the upside “With little political appetite to cut spending amid pressures to fund cleaner energy, support aging populations and bolster security.” The same IMF last week warned that global debt would top the $100tn mark, or 93% of GDP, by the end of this year.

A Chinese policy think tank called on the country’s leaders to issue CNY 2tn (or some $280bn) of special treasury bonds to set up a stock market stabilization fund, a national business newspaper reported. As a part of its quarterly report on the economy, the Institute of Finance & Banking (IFB) said this could steady the market by buying and selling blue-chips and ETFs. The central bank’s governor Pan Gongsheng last month said that a study of such a potential setup of such a stabilization fund was under way. The IFB also proposed more investment by long-term capital to act as a stabilizer, suggesting China could raise the ceiling of stock investment by insurance companies and the national pension fund.

Investors Eye Asset Havens Amidst Continued Unrest in the Middle East

In focus today

Today the Bank of Canada announces its October monetary policy decision. Both markets and analysts are leaning towards a 50bp rate cut to 3.75% although it is a close call. Our base case is for a slight hawkish surprise as we pencil in a dovish 25bp cut to 4.0%.

Focus in the euro area is on the consumer confidence for October. Consumer confidence has risen greatly during the past year, but remains below its historical averages, which is likely one of the reasons for the weak private consumption.

Otherwise, market focus will remain on the earnings season following a continued decline for most asset classes since Monday. Oil and metals continued gaining since Monday, as unrest in the Middle East pushes investors to asset havens.

Economic and market news

What happened yesterday

In the US, equities broadly moved sideways amid investors digesting higher treasury yields, earnings reports and polls/prediction markets on the upcoming US presidential election.

US-China relations are set to intensify regardless of the US election outcome, with a potential new trade war under Trump leading to global economic uncertainty and CNY weakening, while a Harris win would continue Biden's strategy of managed competition, supporting Taiwan but avoiding provocation. For more on this, see Research Global - Trump vs Harris - what it means for US-China relations 22 October.

In the EU, risk of inflation undershooting ECB's 2% target combined with sluggish growth is a worry to central bank policy makers, as the speed of rates cuts may need to increase. Market economists argue that inflation is already near target, while rates are still at a constraining level.

In Hungary, the central bank announced it would maintain a rate decision of 6.5% in line with market expectations.

In the Middle East, the situation continues to escalate as Israel continued to strike Lebanon and Hezbollah announced new attacks on Israeli targets. Israel confirmed it had previously killed Hashem Safieddine, generally considered the 'number two' in Hezbollah before Hassan Nasrallah's assassination. This happened as the U.S. Secretary of State Antony Blinken visited Israel in the hopes of peace talks following the death of Hamas' leader Sinwar.

In metals space, unrest in the Middle East, the US election and falling interest rates continue to drive demand for metals as an asset havens. Notable gains were gold 0.95%, silver 2.89% and platinum 2.77%.

In Oil markets, Oil futures continued to gain following last week's decline. Both Brent and WTI ended the day up by 2.2%. This comes as investors were unconvinced U.S. Secretary of State Antony Blinken's visit to Israel would bring about any resolution to the Middle East situation.

Equities: Global equities were lower again yesterday, with broad-based declines across regions. When writing 'again' please note this marked the first time since early September that we saw back-to-back declines in the S&P 500. A significant reason for this is the comforting labour market data received over the last 1½ months following the spike in uncertainty in early August. Yesterday's declines were not massive, and three of the defensive sectors ended higher. In Europe, cyclicals even outperformed. This wait-and-see approach could very well continue for some days. We have numerous earnings reports coming up, but investors will likely postpone many of their decisions until after the US election on 5 November. In the US yesterday: Dow -0.02%, S&P 500 -0.1%, Nasdaq +0.2% and Russell 2000 -0.4%.

FI: Markets traded with a firm handle around the 2.31% in 10y Bunds yesterday while the 2y point briefly dived from 2.17 to 2.12% and back in the afternoon. The front-end, reaction came on the back of ECB governing council members being open to all options, not least Centeno highlighting the potential of 50bp depending on incoming data. Market added 3bp of rates cuts to the 2025 pricing to 111bp. Swap spreads continued tightening with the Bund-ASW spread now at 17bp.

FX: EUR and JPY lost out to commodity currencies yesterday. Among the notable moves, EUR/USD tested a drop below the 1.08 level and EUR/NOK fell below 11.80.

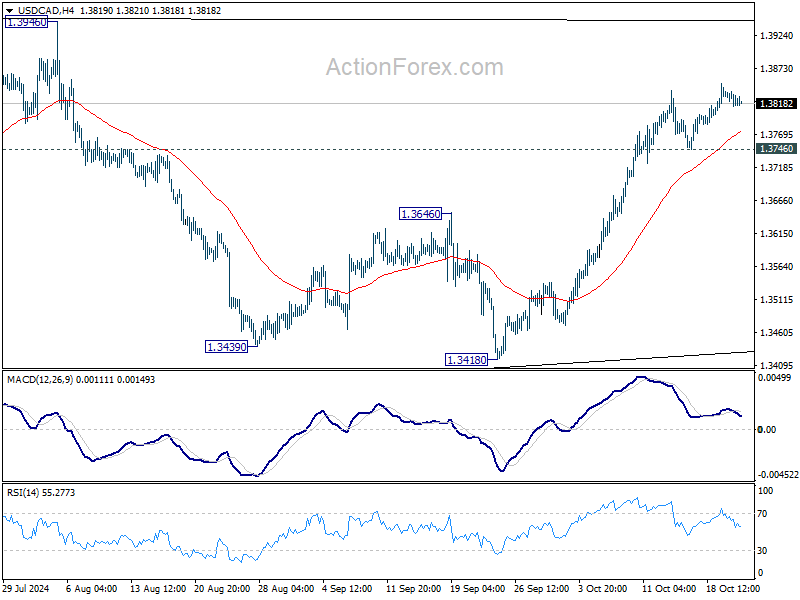

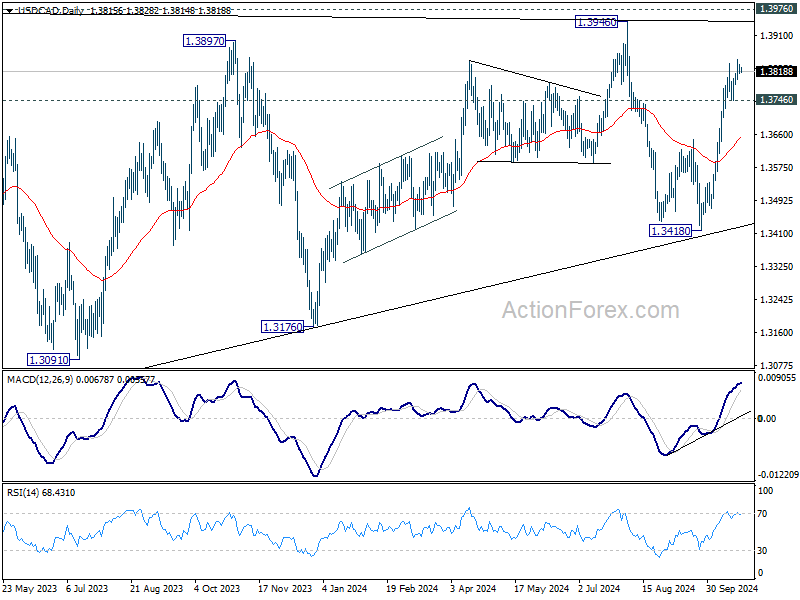

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3805; (P) 1.3825; (R1) 1.3835; More...

Further rally is expected in USD/CAD with 1.3746 support intact, despite loss of momentum as seen in 4H MACD. Current rise from 1.3418 should target 1.3946/76 key resistance zone. However, break of 1.3746 will indicate short term topping, and turn bias back to the downside for deeper pullback.

In the bigger picture, sideway consolidation pattern from 1.3976 (2022 high) might still extend further. While another decline cannot be ruled out, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

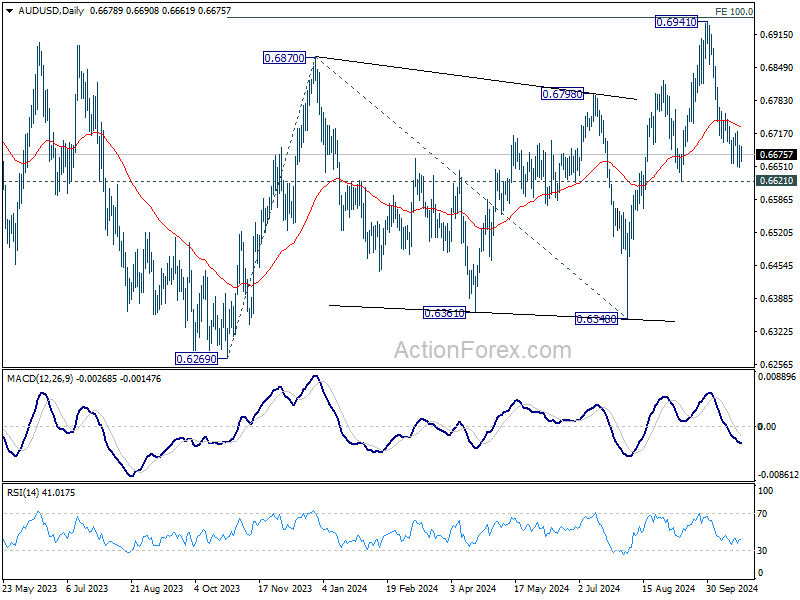

AUD/USD Daily Report

Daily Pivots: (S1) 0.6658; (P) 0.6676; (R1) 0.6702; More...

Further decline is expected in AUD/USD as long as 0.6758 resistance holds. Firm break of 0.6621 support should confirm near term bearish reversal after topping at 0.6941. However, break of 0.6758 will suggest that pullback from 0.6941 has completed and turn bias back to the upside.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941 will target 138.2% projection at 0.7179. However, break of 0.6621 support will argue that rise from 0.6269 has completed and bring deeper fall back to 0.6269/6348 support zone.

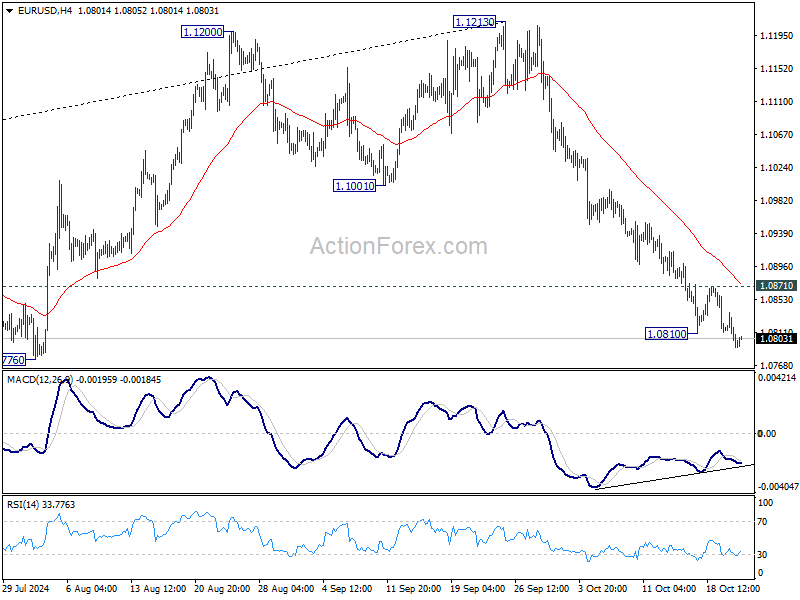

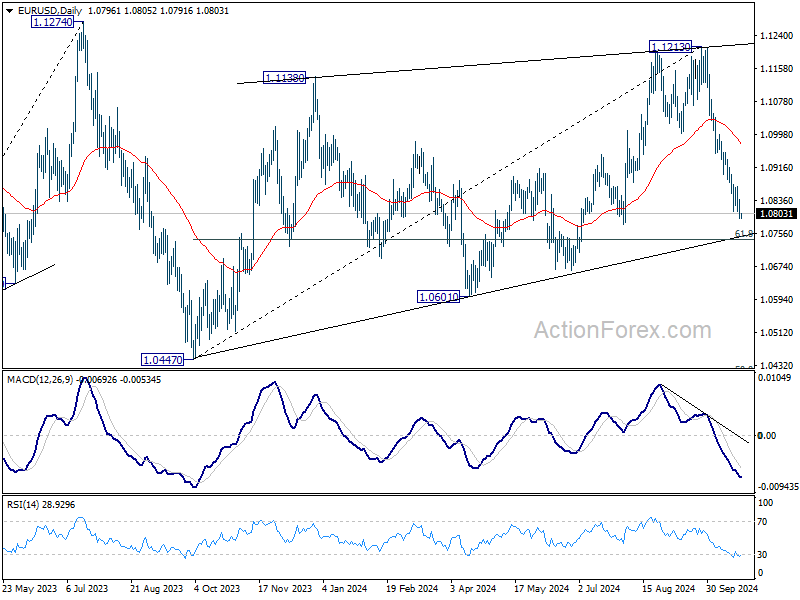

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0782; (P) 1.0810; (R1) 1.0827; More...

EUR/USD's fall from 1.1213 resumed after brief consolidation and intraday bias is back on the downside. Next target is 61.8% retracement of 1.0447 to 1.1213 at 1.0740. Firm break there will target 1.0601 support next. On the upside above 1.0871 minor resistance will turn intraday bias neutral again first.

In the bigger picture, price actions from 1.1274 (2023 high) are seen as a consolidation pattern to up trend from 0.9534 (2022 low), with fall from 1.1213 as the third leg. Downside should be contained by 50% retracement of 0.9534 (2022 low) to 1.1274 at 1.0404, to bring up trend resumption at a later stage.

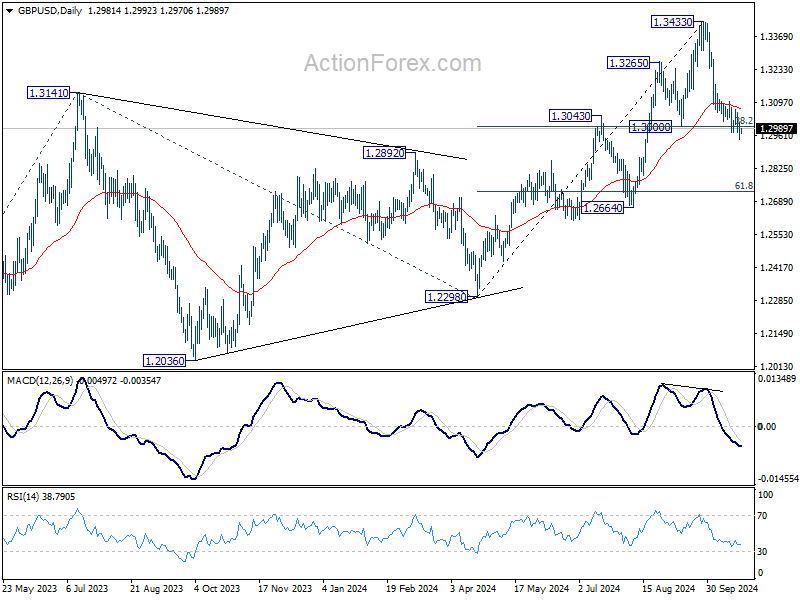

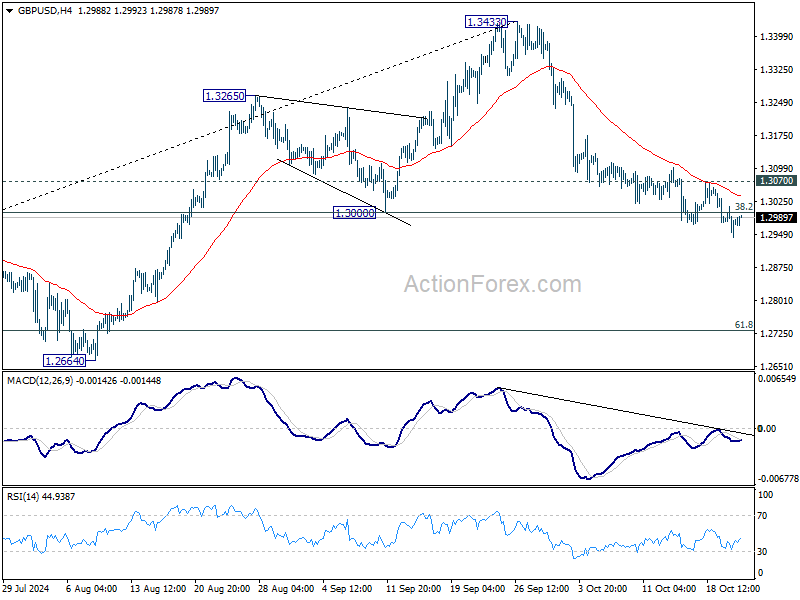

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2949; (P) 1.2982; (R1) 1.3019; More...

Intraday bias in GBP/USD remains on the downside as fall from 1.3433 is in progress. Sustained trading below 1.3000 cluster support (38.2% retracement of 1.2298 to 1.3433 at 1.2999) will argue that whole rise from 1.2298 has completed and bring deeper fall to 61.8% retracement at 1.2732. On the upside, break of 1.3070 minor resistance will turn bias back to the upside for stronger rebound.

In the bigger picture, considering mildly bearish divergence condition in D MACD, decisive break of 1.3000 support will suggest that a medium term top is already formed at 1.3433. Price actions from there would be tentatively seen as correcting the up trend from 1.0351 (2022 low). In this case, deeper fall would be seen to 1.2298 structural support, strong support should be seen there to bring rebound.