Sample Category Title

Sterling Weak as BoE Rate Cut Odds Rise, But Downside Limited for Now

Sterling is currently the weakest performer in today’s trading, though selling pressure remains somewhat contained for now. Weaker-than-expected inflation data from the UK further strengthened the case for BoE to cut interest rates in November. More critically, markets are now pricing in a higher probability of another back-to-back rate cut in December. Interest rate futures reflect a 90% chance of two 25bps cuts by the end of the year, aligning with BoE Governor Andrew Bailey's remarks about taking a "more activist" approach to monetary easing.

In the broader forex market, Australian Dollar and New Zealand Dollar are following Sterling's weakness. Both currencies are anticipating impacts from tomorrow’s joint press conference featuring China’s Housing Ministry, Finance Minister, People's Bank of China, and National Financial Regulatory Administration. Speculation is building that the Chinese government would announce new support measures to aid the struggling housing market.

On the other side, Euro has risen to the strongest position today, largely due to buying against the Pound. While ECB is widely expected to announce another interest rate cut tomorrow, much of this has already been priced in by the market. Investors will focus on whether ECB signals another follow up rate cuts in December. Dollar and Swiss Franc are also performing well, while Canadian Dollar and Japanese Yen are trading in middle positions.

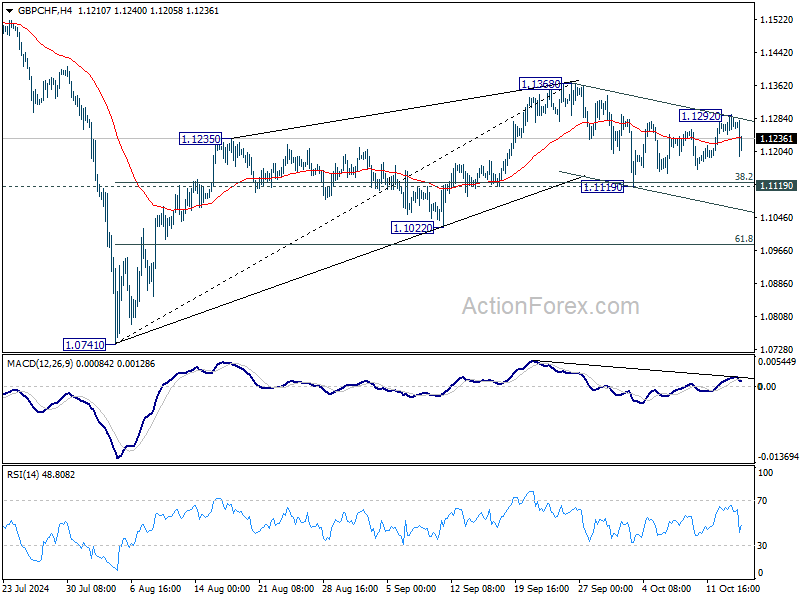

Technically, GBP/CHF will be monitored to see if Sterling's decline is taking off. So far, it's holding well above 1.1119 cluster support (38.2% retracement of 1.0741 to 1.1368 at 1.1220). Rise from 1.0741 is still in favor to resume through 1.1368 at a later stage. However, decisive break of 1.1119 will indicate near term reversal and target 61.8% retracement at 1.0981 and below.

In Europe, at the time of writing, FTSE is up 0.87%. DAX is down -0.19%. CAC is down -0.55%. UK 10-year yield is down -0.087 at 4.082. Germany 10-year yield is down -0.034 at 2.194. Earlier in Asian, Nikkei fell -1..83%. Hong Kong HSI fell -0.16%. China Shanghai SSE rose 0.05%. Singapore Strait Times fell -0.13%. Japan 10-year JGB yield fell -0.0211 to 0.955.

Canada's manufacturing sales falls -1.3% mom to lowest level since Jan 2022

Canada's manufacturing sales fell -1.3% mom to CAD 69.4B in August, better than expectation of -1.5% mom decline, but marked the lowest level since January 2022.

The decline was mainly driven by lower sales in the primary metal (-6.4%) and petroleum and coal product (-3.7%) subsectors. Meanwhile, production of aerospace products and parts (+7.3%) and sales of wood products (+3.8%) increased the most.

With the decrease in August, monthly sales were down -4.4% on a year-over-year basis.

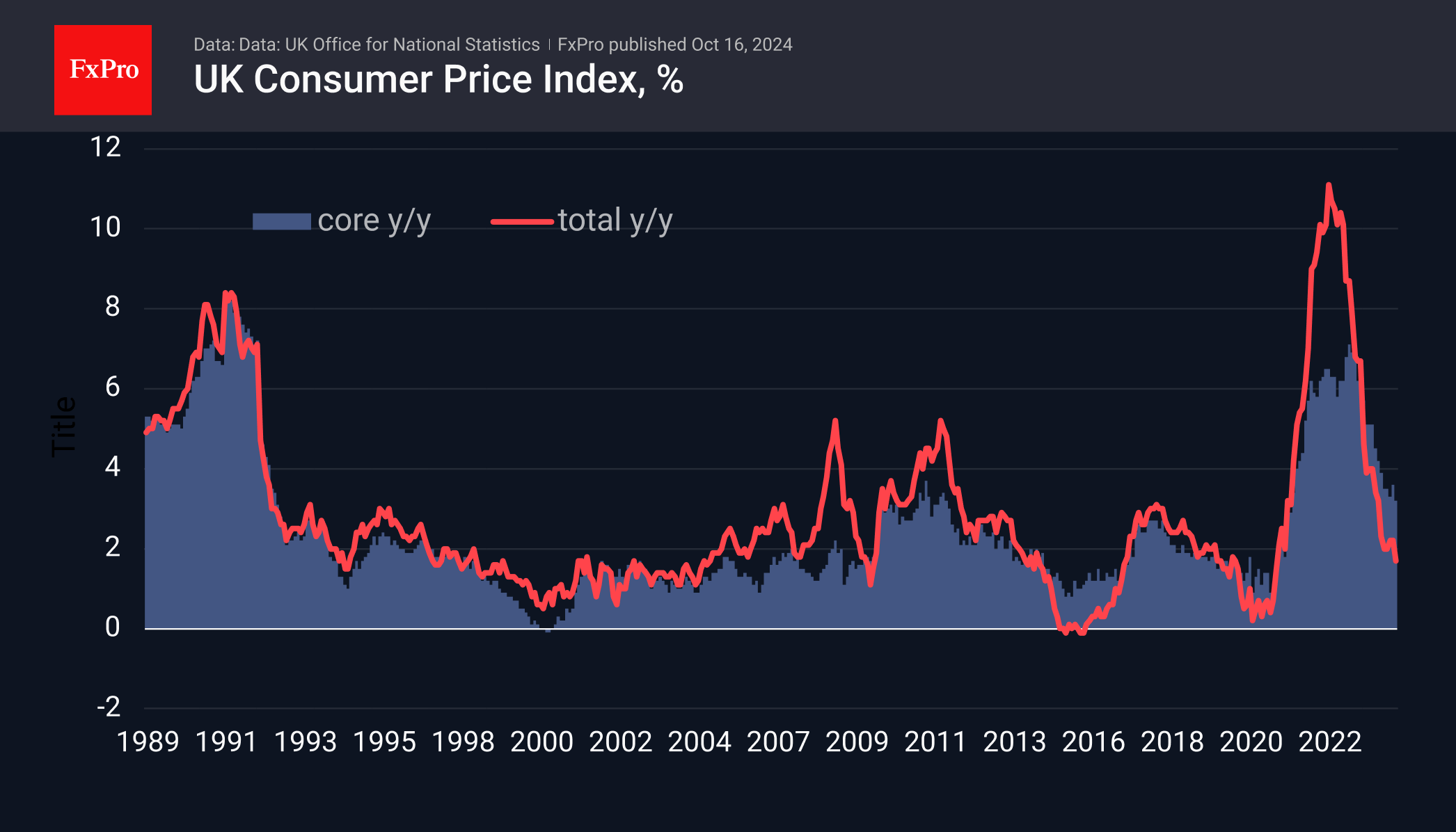

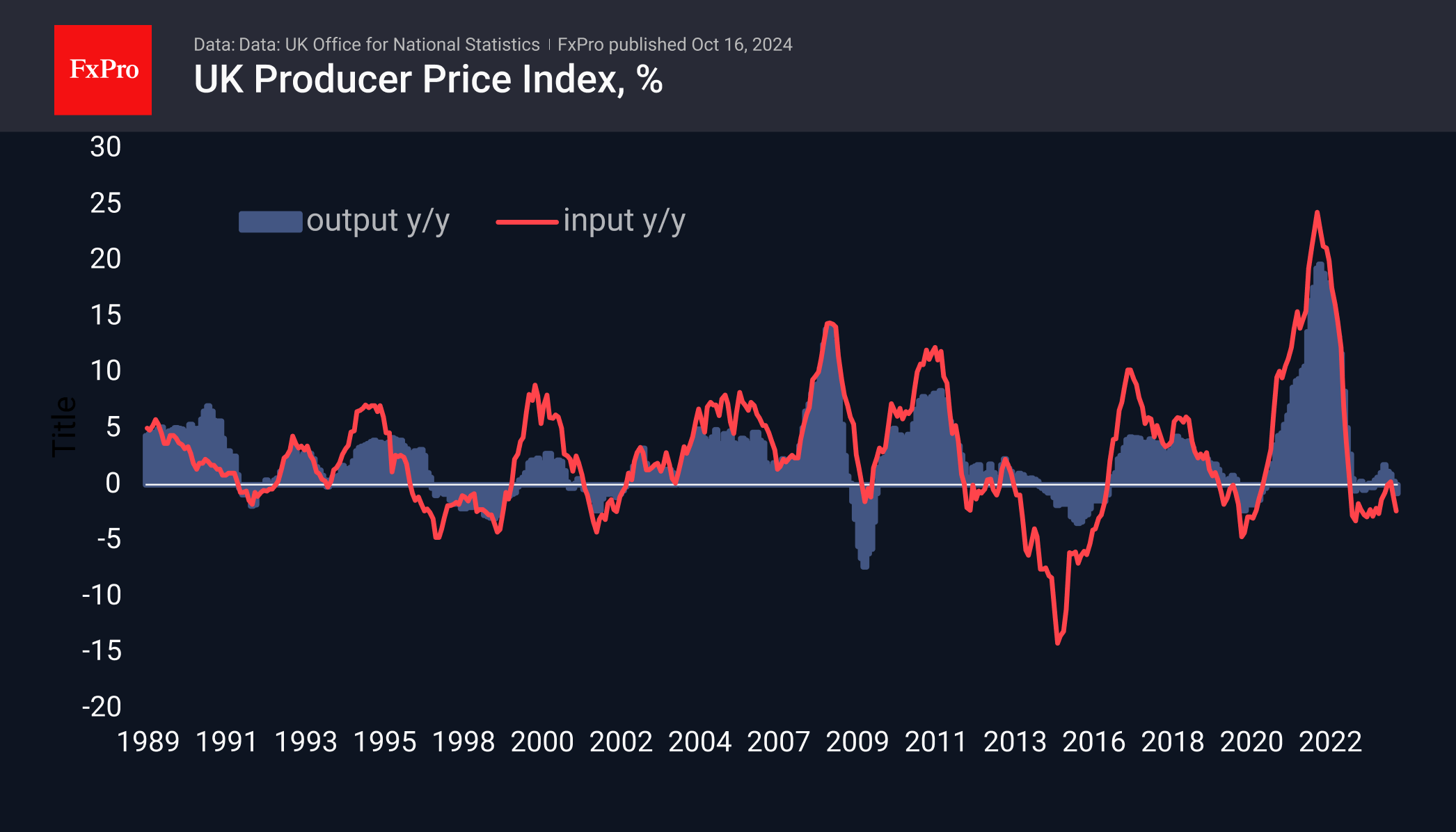

UK CPI falls to 1.7% in Sep, core CPI down to 3.2%

UK CPI slowed more than expected from 2.2% yoy to 1.7% yoy in September, below expectation of 1.9% yoy. Core CPI (excluding energy, food, alcohol and tobacco) slowed from 3.6% yoy to 3.2% yoy, below expectation of 3.4% yoy. CPI goods fell from -0.9% yoy to -1.4% yoy. CPI services also slowed from 5.6% yoy to 4.9% yoy.

ONS Chief Economist Grant Fitzner said: “Inflation eased in September to its lowest annual rate in over three years. Lower airfares and petrol prices were the biggest driver for this month’s fall. These were partially offset by increases for food and non-alcoholic drinks, the first time that food price inflation has strengthened since early last year. “Meanwhile the cost of raw materials for businesses fell again, driven by lower crude oil prices.”

NZ CPI falls to 2.2% in Q3, back in RBNZ's target band

New Zealand's CPI rose 0.6% qoq in Q3, slightly below market expectations of 0.7% qoq. Annually, inflation slowed sharply from 3.3% yoy to 2.2% yoy, in line with forecasts.

This marks the first time since March 2021 that annual inflation has returned within RBNZ’s target range of 1 to 3%. The result was also softer than RBNZ’s own forecast of 0.8% quarterly and 2.3% annual inflation.

Rent prices were the largest contributor to the annual inflation figure, rising by 4.5%. Nearly 20% of the overall inflation increase came from rent.

On the other hand, lower fuel costs, with petrol prices dropping -8.0%, helped balance rising costs, alongside a notable -17.9% drop in vegetable prices following last year’s spike in potato, kūmara, and onion prices.

RBA’s Hunter: Monitoring China’s stimulus and inflation expectations closely

RBA Assistant Governor Sarah Hunter emphasized today the importance of China’s economic stimulus measures for Australia, noting that the central bank is actively assessing their local implications.

In a Bloomberg interview, Hunter explained, “We are factoring it into our forecasts going into November," as China remains a key player in Australia’s economy. "China’s still very important, and we put a lot of our time and attention into thinking through what’s happening there and what it means for the economy here."

In a separate speech, Hunter also addressed the importance of keeping inflation expectations anchored within RBA’s 2-3% target range.

She noted that “the fact that expectations feed into actual inflation outcomes means de-anchored expectations typically lead to greater inflation volatility.”

RBA remains vigilant to ensure inflation expectations remain steady, as de-anchoring could cause significant economic disruption. Hunter stressed the need to constantly track and understand how inflation expectations are evolving to mitigate any risks to the broader economy.

Australia’s Westpac leading index ticks up to -0.15%, growth outlook remains subdued

Australia’s Westpac Leading Index showed a slight improvement, rising from -0.26% to -0.15% in September. However, the index remains in negative territory, indicating "below-trend momentum" that is expected to carry into 2025.

Westpac maintains that while growth will improve next year, it will remain "relatively subdued," with GDP growth forecasted to gradually rise from annualized 1% currently to 1.5% by the end of 2024, reaching 2.4% by the end of 2025—still below the long-term trend of slightly above 2.5%.

As for monetary policy, RBA is not expected to change its cash rate target at the upcoming meetings in November and December.

However, Westpac anticipates a shift in RBA's messages, moving away from its 2024 focus on "inflation vigilance."

Key data releases, including Q3 CPI on October 30 and national accounts on December 4, are likely to confirm a subdued growth environment and provide RBA with enough confidence to start considering less restrictive policies in 2025.

BoJ's Adachi warns against premature rate hikes, urges most conservative approach

In a speech today, BoJ Board Member Seiji Adachi suggested that Japan's economy has met the conditions for beginning to normalize its ultra-loose monetary policy. He pointed to the firm economic outlook and broadening price increases as positive signs.

However, Adachi emphasized the need for caution, stating that until underlying inflation sustainably reaches the 2% target, Japan must maintain an "accommodative" financial environment. He added that any interest rate increases should be at a "very moderate pace."

Adachi also stressed the importance to "avoid raising rates prematurely", suggesting that BoJ should use the "most conservative estimate" when considering policy adjustments.

"Given high uncertainty surrounding global developments, there is significant uncertainty over next year's wage developments in Japan. We must carefully monitor the situation," Adachi added.

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3039; (P) 1.3071; (R1) 1.3106; More...

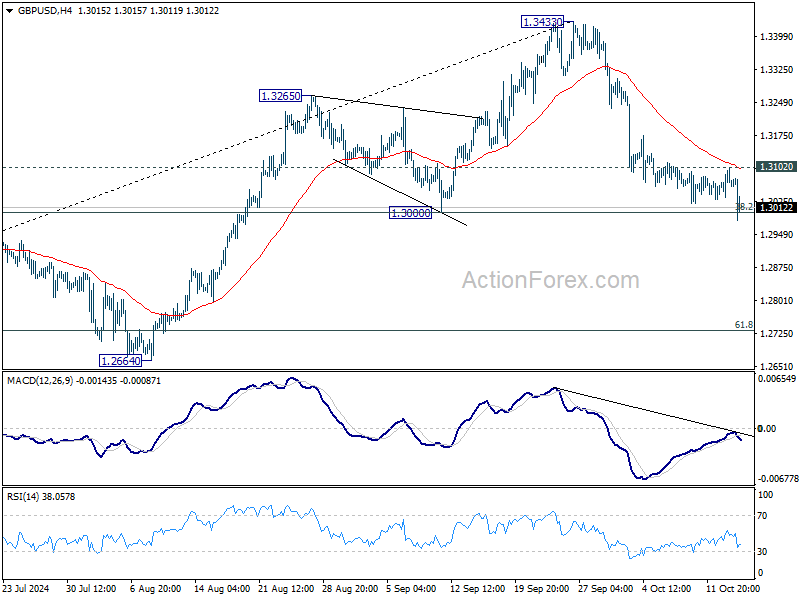

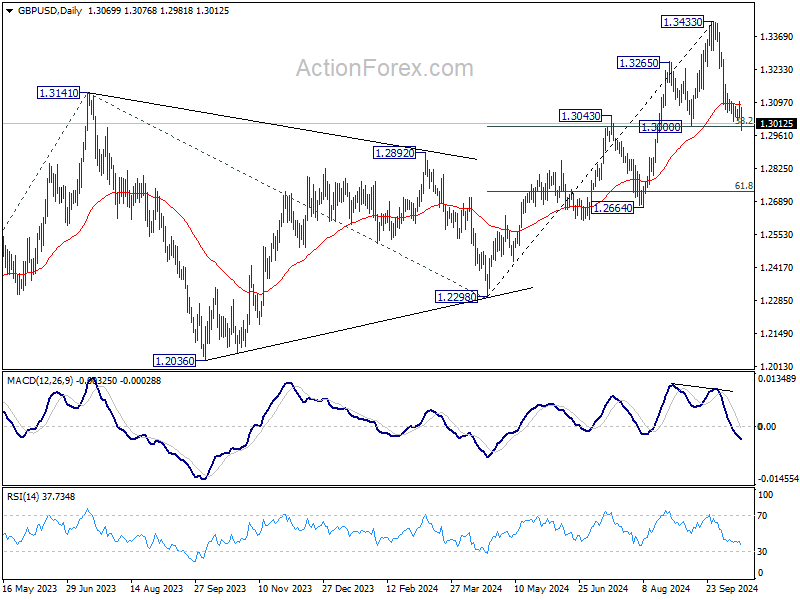

GBP/USD is still defending 1.3000 cluster support (38.2% retracement of 1.2298 to 1.3433 at 1.2999) for now. On the downside, decisive break of 1.2999/3000 will argue that whole rise from 1.2298 has complete,d and bring deeper fall to 61.8% retracement at 1.2732. Nevertheless, strong bounce from current level, followed by break of 1.3102 minor resistance, will turn bias back to the upside for stronger rebound towards 1.3433.

In the bigger picture, as long as 1.3000 support holds, the up trend from 1.0351 (2022 low) is still in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. However, considering mild bearish divergence condition in D MACD, decisive break of 1.3000 will argue that a medium term top is already in place, and bring deeper fall back to 1.2664 support next.

Canada’s manufacturing sales falls -1.3% mom to lowest level since Jan 2022

Canada's manufacturing sales fell -1.3% mom to CAD 69.4B in August, better than expectation of -1.5% mom decline, but marked the lowest level since January 2022.

The decline was mainly driven by lower sales in the primary metal (-6.4%) and petroleum and coal product (-3.7%) subsectors. Meanwhile, production of aerospace products and parts (+7.3%) and sales of wood products (+3.8%) increased the most.

With the decrease in August, monthly sales were down -4.4% on a year-over-year basis.

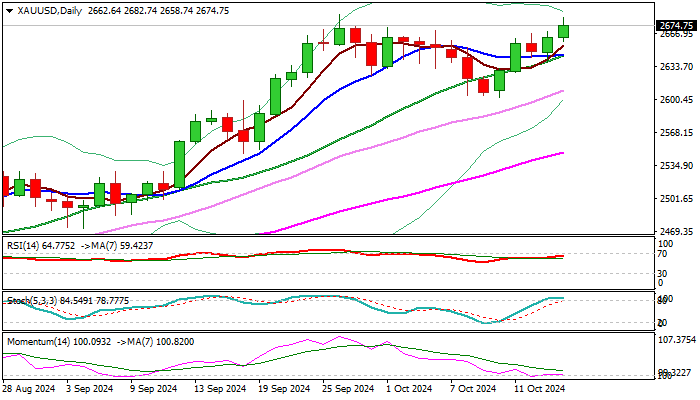

XAU/USD Outlook: Bulls Hold Grip for Retest of New Record High

Gold price came just ticks ahead of new record high ($2685) during European trading on Wednesday, in fresh extension of bull-leg from $2602 higher low of Oct 10 and the bottom of corrective phase from $2685.

The metal remains strongly supported by growing prospects for global monetary policy easing, geopolitical tensions and uncertainty surrounding nearing US election.

Although the Fed officials are divided on the number of rate cuts until the end of the year, the central bank remains on track for more policy easing, with markets awaiting coming economic data from the US to get clearer picture about Fed’s rate cut trajectory.

Bulls are likely to retest $2685 peak, but overbought conditions on daily chart and 14-d momentum in neutral mode suggest that price may hold at this zone for consolidation, before resuming higher.

Converged 10/20DMA’s contribute to such scenario, with dips expected to find ground at $2640 zone to mark a healthy correction however, larger bulls should stay intact while pivotal $2600 support holds.

Round-figure $2700 and Fibo projection at $2705 (123.6%) mark immediate targets, ahead of projected levels at $2717 (138.2%), $2736 (161.8%) and $2748 (176.4% of the upleg from $2602).

Res: 2685; 2700; 2705; 2717.

Sup: 2658; 2645; 2633; 2621.

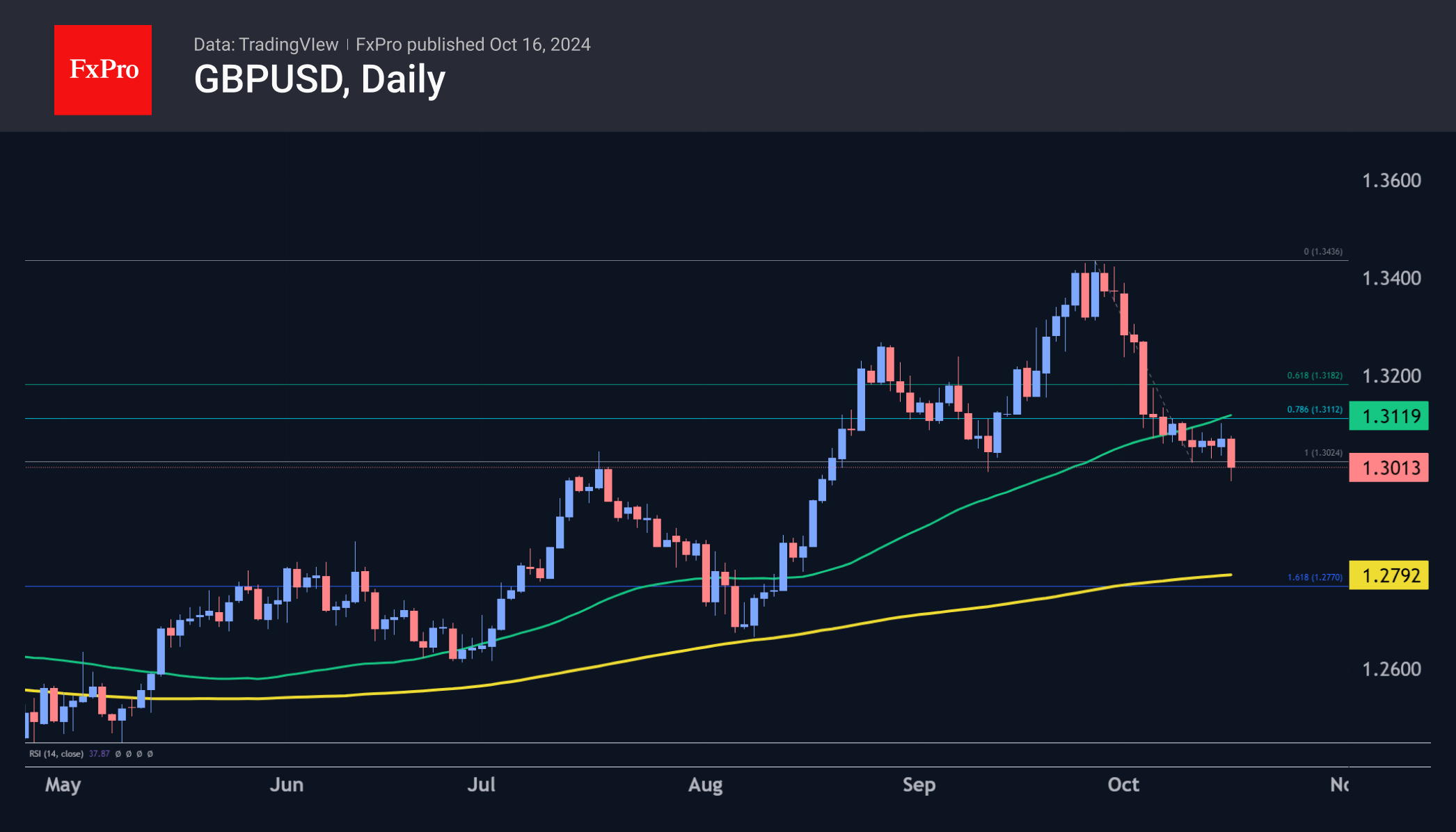

GBP/USD: Dips Below 1.3000 on Weaker Than Expected UK CPI Numbers

Cable accelerated lower and cracked psychological 1.30 support, to hit the lowest in almost two months in early Wednesday.

Sterling was down 0.8% in immediate reaction to economic data which showed that UK inflation fell more than expected in September and dipped below BoE’s 2% target, adding to bets for more rate cuts towards the end of the year.

Fresh weakness generates an initial signal of continuation of a downtrend from 1.3434 (2024 high of Sep 26), with close below 1.30 required to validate the signal.

Sustained break of 1.30 trigger to expose targets at 1.2958/52 (Fibo 61.8% of 1.2664/1.3434/100DMA) and more significant daily cloud base (1.2941) and 200DMA (1.2792).

Technical picture is bearishly aligned with strong negative momentum and the latest formation of 10/55DMA’s weighing on near-term action, however, bears would face a difficult task to clearly break 1.30 level (the last attack on Sep 11 was strongly rejected).

Potential upticks should be ideally capped by cloud top (1.3054) and not to exceed falling 10DMA (1.3076) to keep bears intact.

Res: 1.3049; 1.3071; 1.3113; 1.3140.

Sup: 1.3000; 1.2982; 1.2952; 1.2941.

Pound Suppressed by Weak Inflation

The British pound fell below the 1.30 level against the dollar after weak inflation data across indicators. This sent the pound to a two-month low on speculation that the Bank of England will cut interest rates further in the coming months.

The consumer price index changed little in September, slowing to its slowest pace since April 2021 at 1.7% year-on-year from 2.2% previously and 1.9% expected. Price growth was below the Bank of England’s 2% target, allowing for an acceleration of policy easing to stimulate the economy. The core consumer price index last month was 3.2% higher than a year earlier, down from 3.6% in August. And it has been the lowest since September 2021.

Another bearish factor for the pound is the acceleration of the decline in producer prices. The Input Producer Price Index lost 1% over the month after five months of continuous decline of 2.5% and 2.3% over the past year. The output PPI lost 0.5% in September, after 0.4% previously, bringing the annual trend back into negative territory at -0.7%. In both cases, the figures were well below average expectations.

Only house prices managed to beat expectations, accelerating from 1.8% y/y to 2.8% y/y in August instead of the expected 2.5%. Still, this acceleration was at least partly because of the low base that lasted until last December.

GBPUSD downplayed the news classically, with an impressive sell-off of 0.7% within an hour of the data release. The pound briefly dipped below 1.30, a key round level, where it found buyers. Sterling also predictably rebounded from the previous day’s upbeat employment data but failed to convert the rebound into gains.

GBPUSD met strong technical resistance at 1.3110, where the 50-day moving average and the first correction retracement (of decline from 26 September to 10 October) are centred. The pair also fell below the area of the local lows from 11 September, which gives the sellers the upper hand.

A potentially important downside target is the 1.2800 area, near the 161.8% Fibonacci extension level from the initial decline and the 200-day moving average.

SPX 500: First Sign of Volatility Detected

- Trump’s trade war 2.0 narrative & steep sell-off in ASML spooked the performances of the major US stock indices on Tuesday, 15 October.

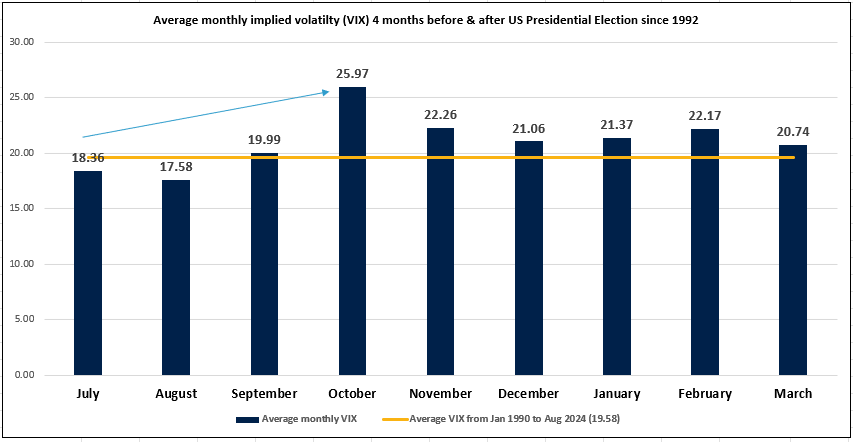

- Implied volatility in the US stock market, measured by the VIX tends to be highest in October based on data during past US presidential election years since 1992.

- VIX/MOVE ratio has started to show outperformance of VIX.

- The S&P 500’on-going 4-week rally has flashed out exhaustion conditions.

The S&P 500 shed 0.75% on Tuesday, 15 October after it printed its 46th record high for 2024 on Monday.

Yesterday’s daily loss of 0.75% was the largest seen in the past two weeks and attributed to the underperformance of the artificial intelligence (AI) juggernaut, Nvidia (second largest market cap stock in the S&P 500) which tumbled by 4.68% after a related bellwether semiconductor chip-making equipment firm, ASML issued a downgrade to its revenue guidance for 2025 that saw its share price plummeted by 16%, its worst daily performance since 12 June 1998.

In addition, an adverse macro factor also attributed to yesterday’s weakness inflicted in all the major US stock indices except for the Russell 2000 which closed almost unchanged; Nasdaq 100 (-1.37%) and Dow Jones Industrial Average (-0.75%).

US trade tensions with China narrative is now back on the radar of market participants after US Republican presidential nominee Donald Trump reaffirmed his preference for higher tariffs on China and the rest of the world’s exports to the US as he remarked that “tariffs are the most beautiful word in the dictionary” during yesterday’s live in-person interview with Bloomberg News organized by The Economic Club of Chicago.

With less than four weeks to go before the 5 November US presidential election day, betting markets are now indicating Trump has a lead of 56% over Democratic presidential nominee Harris (43%) according to betting average data as of 15 October compiled by Real Clear Politics.

October recorded the highest level of VIX during past US presidential election years

Fig 1: Average monthly VIX during US presidential election years since 1992 as of 2 Aug 2024 (Source: TradingView)

Regardless of who wins the White House race, based on past data during US presidential election years since 1992, the VIX, a measurement of the implied volatility of the US S&P 500 has increased in the four months (July to October) before the election month of November; a jump of around 40 percent, and reach an average monthly high of 25.97 in October (see Fig 1).

Hence, the S&P 500 now faces an increased risk of a jump in the VIX which in turn may spark a multi-week risk-off episode in the global financial markets.

VIX is now showing outperformance conditions over the MOVE Index

Fig 2: Major trends of MOVE Index, VIX & VIX/MOVE ratio as of 16 Oct 2024 (Source: TradingView)

The Merrill Lynch Option Volatility Estimate (MOVE) Index reflects the level of volatility in U.S. Treasury futures. The index is considered a proxy for term premiums of U.S. Treasury bonds (the yield spread between long-term and short-term bonds).

The movement of the MOVE Index has a strong direct correlation with VIX (implied volatility of the US stock market; S&P 500) since 2018 (see Fig 2).

Since the week of 16 September 2024, the MOVE Index has surged upwards significantly and cleared above a key medium-term resistance of 112.80.

The VIX has tagged along as well but has yet to break above its key medium-term resistance of 23.38 (currently trading at 20.80).

Interestingly, the ratio of VIX/MOVE has printed a series of “higher lows” and staged a bullish breakout from a major descending trendline resistance on the week of 15 July 2024 which suggests outperformance conditions of the VIX over MOVE Index have surfaced.

All these observations suggest a potential imminent jump in the VIX.

Watch the 5,930 key resistance on the S&P 500

Fig 3: Medium-term & major trends of the US S&P 500 CFD Index as of 16 Oct 2024 (Source: TradingView)

In the lens of technical analysis, the price actions of the US S&P 500 CFD Index (a proxy of the S&P 500 E-mini futures) have started to show signs of fatigue despite a string of record highs reached in the past four weeks.

Since 22 August 2024, the US S&P 500 CFD Index has evolved into a bearish “Ascending Wedge” configuration coupled with a bearish divergence condition sighted on the MACD Histogram in the same period which suggests its medium-term upside momentum has started to wane.

5,930 key medium-term pivotal resistance on the Index and a break below 5,675 key intermediate support (also the 50-day moving average) is likely to trigger a medium-term (multi-week) corrective decline sequence to expose the next medium-term supports of 5,390 (close to the 200-day moving average) and 5,100 (see Fig 3).

On the flip side, a daily close and a clearance above 5,930 invalidate the bearish scenario for a continuation of the impulsive upmove for the next medium-term resistances to come in at 6,110/130 and 6,390 (also the upper boundary of the major ascending channel in place since March 2020 pandemic low).

EUR/USD Continues Downward Amid Economic Uncertainties

EUR/USD has sustained its position below the EMA-200 line, indicating a potential shift into a more defined downtrend. Recent comments from Raphael Bostic, head of the Atlanta Federal Reserve, have influenced this movement. Bostic suggests a modest 25-basis-point cut in interest rates this year – contrary to earlier predictions of a more aggressive 50-point reduction. Federal Reserve officials have underscored that any policy easing would be contingent on upcoming economic data.

The dollar's strength is further bolstered by the Empire Manufacturing Index for New York State, which sharply declined to -11.9 in October, a significant drop from 11.5 in September, marking the lowest level since May. This unexpected downturn, which contrasts with analyst expectations for a slight positive reading of 3.8, highlights a deterioration in regional manufacturing activity. While this data suggests potential headwinds for the US economy, it could paradoxically support the USD if it fuels speculation about a less aggressive rate-cutting strategy by the Fed.

Market participants eagerly anticipate further economic reports, including data on retail sales, industrial production, and the upcoming manufacturing data from FRB Philadelphia. These indicators will be crucial in painting a more comprehensive picture of the US consumer sector and overall industrial conditions, potentially guiding the next moves for EUR/USD.

Technical analysis of EUR/USD

EUR/USD is entrenched downward, aiming for the 1.0777 target level. The currency pair is currently consolidating around 1.0888. A break below this consolidation to 1.0860 could further propel the pair towards 1.0777. Upon reaching this level, a corrective phase towards 1.0996 might be anticipated. The MACD indicator, positioned below zero and poised to reach new lows, supports this bearish outlook.

On the hourly chart, EUR/USD has formed a consolidation range just above 1.0888. A downward break from this range is expected, which could extend the decline towards 1.0857 and potentially continue the downtrend to 1.0777. This scenario is reinforced by the Stochastic oscillator, whose signal line is below 50 and trending downwards towards 20, indicating the likelihood of continued bearish momentum.

GBP/USD Drops Below 1.30 on Soft Inflation Report

The British pound has finally showed some movement on Wednesday after a week of limited movement. In the European session, GBP/USD is trading at 1.2992, down 0.62% on the day. The pound fell below the symbolic 1.30 level for the first time since August 20.

UK inflation drops more than expected

The UK inflation report for September was projected to hit a milestone and fall below the BoE’s 2% target, but the reading exceeded expectations. CPI fell to 1.7% y/y, down from 2.2% in August and below the market estimate of 1.9%. This was the lowest level since April 2021 and was driven by lower prices for petrol and airfares.

Services inflation, which has been stubbornly high, dropped from 5.6% y/y to 4.9%, its lowest level since May 2022. Monthly, CPI was flat, below 0.3% in August and below the market estimate of 0.1%. Core CPI also decelerated in September and was lower than expected (3.2% y/y and 0.1% m/m). As well, wage growth slowed to 4.9% in the three months to August, down from 5.1% previously.

The Bank of England will be encouraged by the drop in inflation and in wages. The UK economy is groaning under the weight of a cash rate of 5% and the markets are looking at a rate cut in November as a done deal, while a December cut is a strong possibility. Many major central banks have shifted their primary focus from inflation risks to the labor market, and we could see the same with the BoE, now that inflation is back below the BoE’s target.

GBP/USD Technical

- GBP/USD has pushed below support at 1.3071, 1.3039 and 1.3004. The next support level is 1.2972

- 1.3106 and 1.3138 are the next resistance lines

Crypto Market Trying to Form an Uptrend

Market Picture

The crypto market cap rose by 1.4% to $2.31 trillion. Cryptocurrencies and equities are now out of sync (there was profit-taking in equities), but they maintain a general upward bias. The crypto market is forming an uptrend, which will be confirmed if local highs exceed the previous high of $2.32 trillion.

Bitcoin received a jolt on Tuesday, first jumping 4% in four hours to almost $68K and then losing over 4.6% to $64.7K. The market digested this influx of stop orders and soon began to rise again, trading near $66.8K at the time of writing. It will be interesting to see the bulls and bears continue to battle on a retest of $68K. The first cryptocurrency was not allowed to go higher in July, but now the bulls have the breakdown of the descending channel and an active pullback from the 200-day moving average on their side. At the same time, the RSI on the daily timeframe is not yet in the overbought territory, leaving room to run.

Ethereum looks weak now, approaching $2,700—the area of previous peaks—but it needs to break through. Perhaps a return of risk appetite in the equity markets will spark new momentum for the second-largest cryptocurrency to rise towards $3,000.

News background

The funding rate for perpetual bitcoin contracts has hit a multi-month high, indicating bullish sentiment and a growing influx of liquidity, notes The Block.

CryptoQuant notes that demand for Bitcoin has surged, rising at the fastest monthly pace since April 2024. Open interest (OI) in derivatives rose to a record $19.8 billion.

Standard Chartered predicts that Bitcoin could hit an all-time high ahead of the US election. Donald Trump’s increased odds of victory, significant inflows into spot bitcoin ETFs, and increased activity in the BTC call options market are fuelling sentiment.

MicroStrategy shares are a leading indicator of a potential bullish breakout, according to Bernstein. They are up 190% year-to-date, while BTC is up just 55%.

The US Treasury Department’s Financial Crimes Enforcement Network (FinCEN) fined TD Bank a record $1.3 billion for facilitating money laundering through cryptocurrencies.

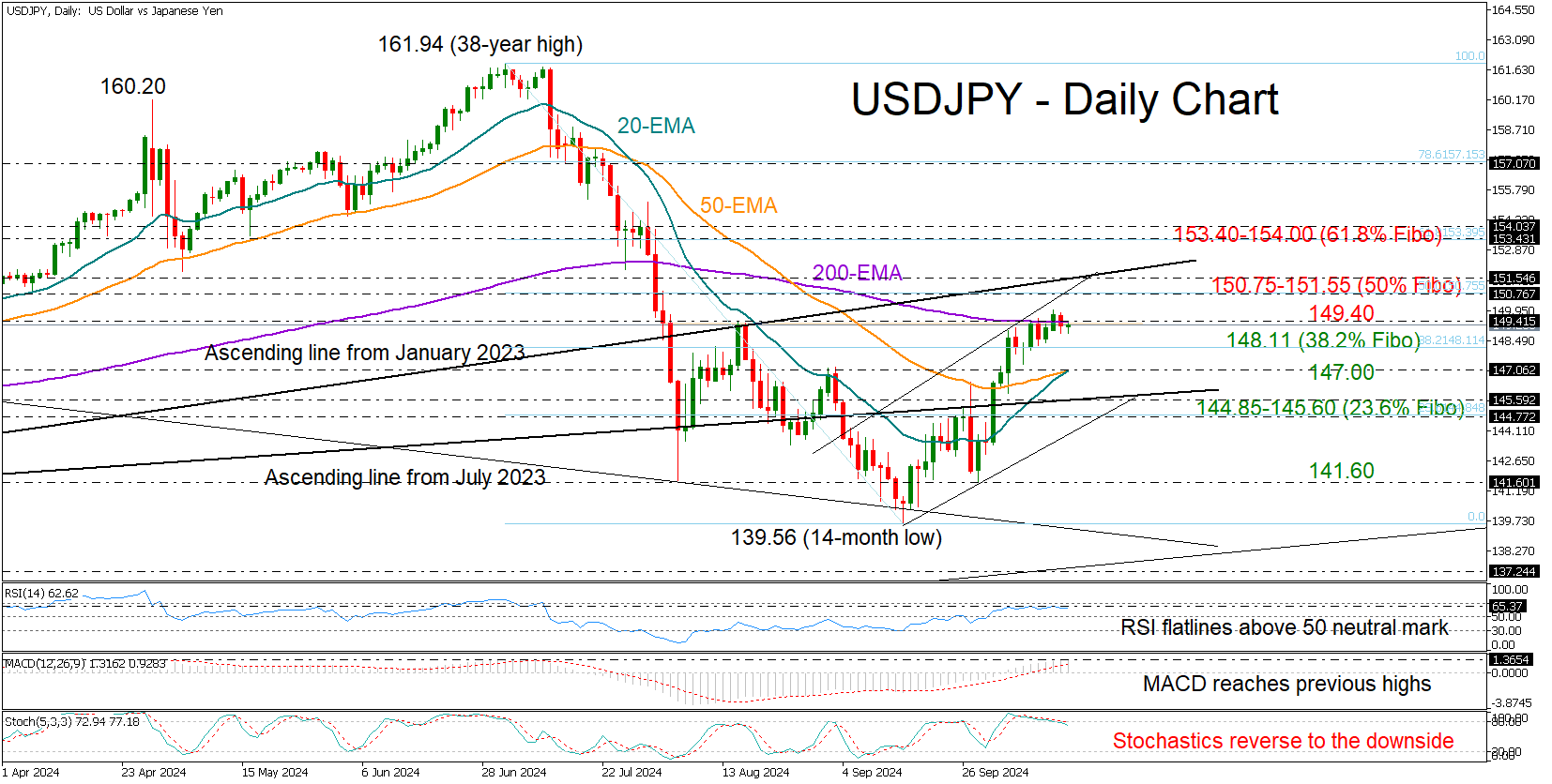

USDJPY Faces a Pass or Fail Test

- USDJPY extends consolidation around August’s bar

- Technical signals weaken, cannot warrant a bullish trend reversal

- US retail sales, jobless claims due on Thursday at 12:30 GMT

USDJPY reached a two-month high of 149.96, but it couldn’t hold its strength above the 200-day exponential moving average (EMA) at 149.40 on Tuesday.

Over the past few days, the pair has been struggling for a bullish breakout, leaving investors wondering whether it’s time for a negative pivot. The slowdown in the technical indicators reflects persisting reluctance among traders as the price hovers around August’s bar. Note that the MACD has reached its ceiling from July and April.

Still, with the RSI hanging comfortably above its 50 neutral mark and the 20-day EMA set to cross above the 50-day EMA, buying appetite may not entirely disappear. In this case, the pair may again attempt to stretch towards the 150.75-151.55 border. The 50% Fibonacci retracement of the July-September downtrend and the crucial support-turned-resistance line from the 2023 bottom are in that price neighborhood. Hence, a breach of that wall could excite buyers, speeding up the recovery process towards the 61.8% Fibonacci mark of 153.40 and the 154.00 barrier. Another success there could trigger a faster rally towards the 157.00 round level.

Should the bears take charge immediately, the 38.2% Fibonacci of 148.11 may provide some protection ahead of the 20- and 50-day SMAs at 147.00. A move lower could stall within the 144.85-145.60 territory formed by the 23.6% Fibonacci and the ascending line from July. If selling forces persist, they could forcefully press the price towards the 141.60 base.

In brief, USDJPY is trading near a decisive territory that could determine its next direction. For a bullish trend reversal, the pair must close above August’s bar of 149.40 and more importantly sustain buying interest above 151.55.