Sample Category Title

Week Ahead – As Dollar Recovers, Spotlight Falls on US CPI Inflation

- US CPI data to guide Fed rate cut bets and the dollar

- RBNZ expected to cut interest rates by 50bps

- Wounded pound awaits monthly GDP numbers

- Canada jobs data and BoC business survey also on tab

Dollar rebounds on safe haven flows and upbeat data

The US dollar staged a meaningful recovery this week aided by Fed Chair Powell’s remarks that the US central bank would likely stick with quarter-point rate cuts, adding that they are not “in a hurry”, as new data have bolstered their confidence in the economy. The currency extended its gains not only because of upbeat data but also due to safe haven flows after Iran launched missile attacks on Israel in retaliation for Israel’s operations against Tehran’s Hezbollah allies in Lebanon.

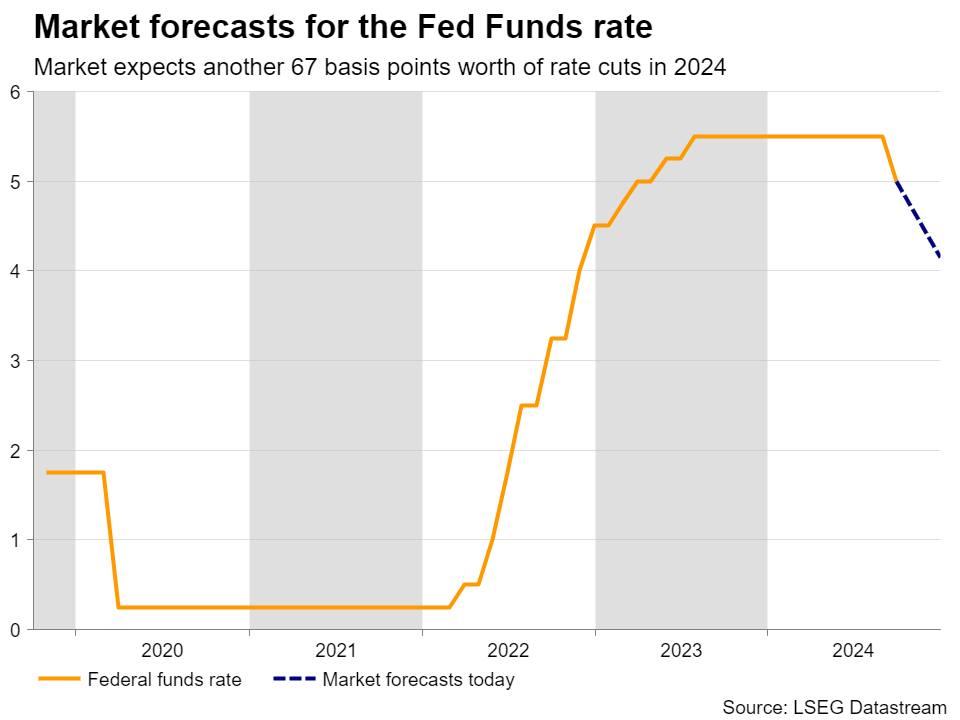

The better-than-expected ADP jobs report and ISM non-manufacturing PMI prompted market participants to scale back their rate cut bets, assigning only a 35% chance for a back-to-back 50bps reduction in November and around 67bps worth of reductions by the end of the year.

Fed minutes and US CPIs on next week’s agenda

Thus, barring any further escalation in the Middle East, dollar traders are likely to keep their gaze locked on the economic calendar. On Wednesday, the minutes of the latest FOMC decision are due to be released. Nonetheless, given that the dot plot pointed to 50bps worth of rate reductions by the end of the year and that most policymakers who spoke after the decision, including Chair Powell, favored quarter-point reductions from here onwards, the minutes are unlikely to shake the markets.

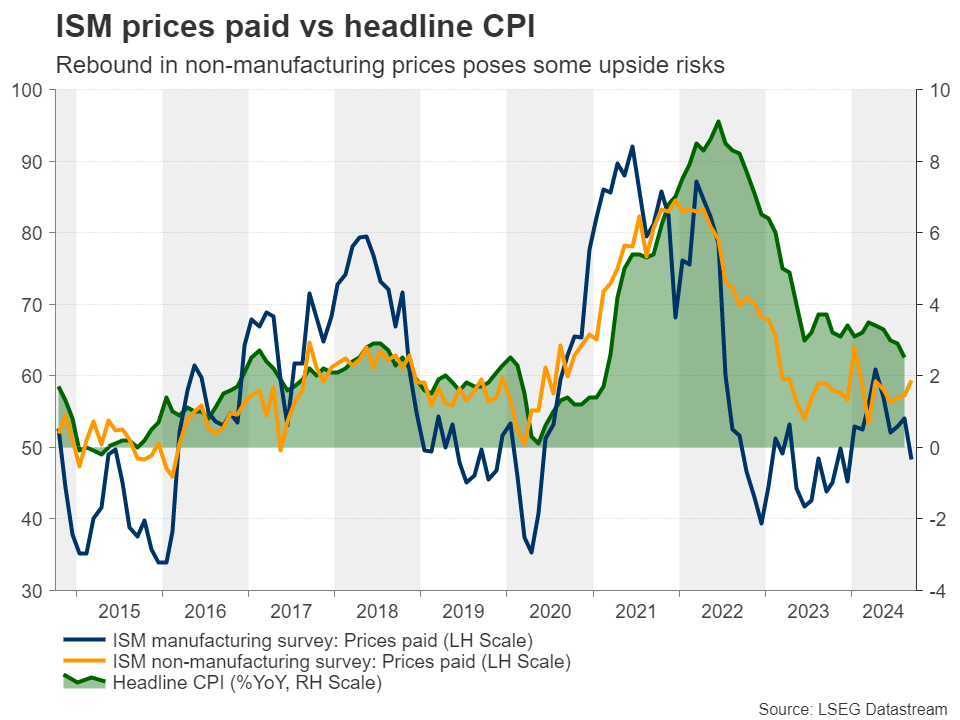

Therefore, the spotlight is likely to fall on the US CPIs for September due out on Thursday. According to the preliminary S&P Global PMIs, prices charged by businesses rose at the fastest rate in six months, and although the ISM manufacturing survey revealed a slide, the non-manufacturing report corroborated the notion of accelerating price pressures.

This implies some upside risks to Thursday’s data, especially to the core CPI rate. The headline rate could still ease somewhat as the year-on-year change in WTI crude oil slipped further into negative territory in September, despite the latest rebound in absolute prices.

Thus, should the data point to some stickiness in inflation, more investors may be convinced that the Fed will proceed as planned, cutting interest rates by 25bps at each of the November and December decisions. This could add more fuel to the dollar’s engines.

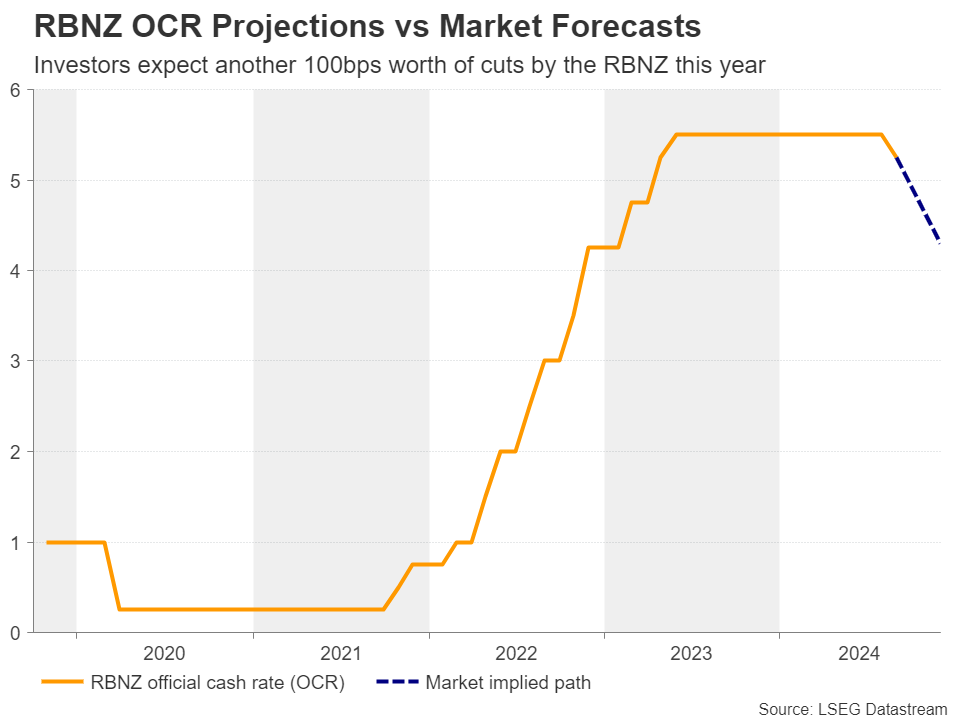

Will the RBNZ cut rates by 25 or 50 basis points?

Passing the ball to New Zealand, its own domestic dollar benefited last week from China’s decision to proceed with bold stimulus measures to revive economic activity. However, the latest wave of risk aversion and the recovery of the US dollar were reasons for a pullback.

Next week, on Wednesday, it will be the RBNZ’s turn to drive the kiwi. The last time RBNZ policymakers gathered was back on August 14, when they cut interest rates by 25bps and signaled that more are coming as inflation is expected to remain near the mid-point of the Bank’s 1-3% target band.

The decision to cut rates came one year ahead of the Bank’s previous forecasts, with the new ones projecting the cash rate at 4.9% in the fourth quarter of 2024. However, investors took a more aggressive stance just after the decision, penciling in more than 30bps worth of cuts for the October decision.

Since then, data revealed that retail sales tumbled more than expected in Q2, and while the overall GDP rate was better than expected, it still revealed contraction. The Q1 print was revised down to indicate a modest 0.1% expansion, after the economy suffered a recession in the second half of 2023.

Now investors are convinced that the Bank will cut interest rates by 50bps next week, and by another 50 in November. This means that the risks for the kiwi may be tilted to the upside because if officials do proceed with a double cut and signal more aggressive easing, this will just confirm market expectations and thereby, the kiwi is unlikely to depreciate much.

On the other hand, if they cut by only 25bps just solely in order to wait for more data and/or because they will not have updated economic projections to work with at this meeting, the kiwi is likely to recharge and resume its prevailing uptrend.

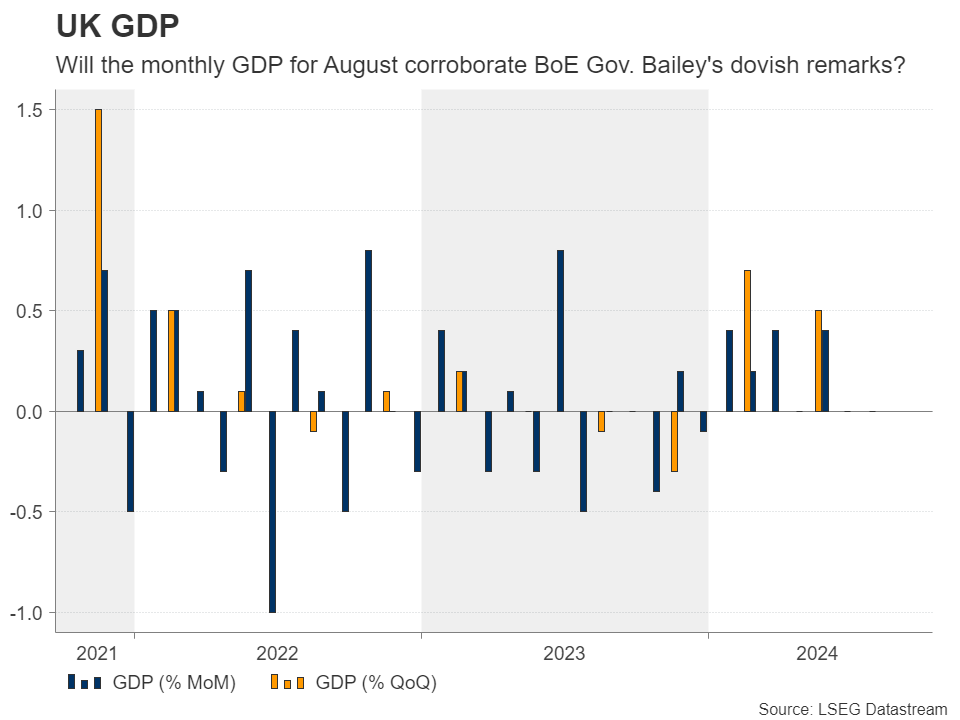

Will the UK data provide a helping hand to the pound?

Among the major currencies, the pound has been the best performer year-to-date and by a large margin. However, it suffered a big blow this week after BoE Governor Andrew Bailey said in an interview with the Guardian that they could turn “a bit more activist” on interest rate cuts if data continues to suggest progress in inflation. The market is now nearly fully convinced that a quarter point cut will be delivered in November, assigning a 65% probability for another one in December.

The next test for the pound could come in the form of the monthly GDP data for August, due out on Friday, which will be accompanied by the industrial and manufacturing production rates, as well as the trade data for the month. A disappointing set of numbers could add credence to Bailey’s remarks and prompt traders to push sterling lower.

Elsewhere, the minutes from the latest RBA decision are scheduled to be released on Tuesday, while on Friday, with loonie traders assigning a 30% chance for a bigger 50bps cut by the BoC on October 23, the Canadian employment report for September and the BoC business outlook survey will attract special attention.

Weekly Focus – Lower Inflation Clears Path for European Rate Cuts

This week saw a further escalation of the conflict in the Middle East, as Israel attacked Hezbollah in Lebanon and Iran launched missiles at Israel. There was little market reaction. Oil prices rose around two dollars per barrel but are still lower than last week, among other things held down by Saudi Arabia's wish to increase its production. It still seems most likely that the conflict will not evolve into attacks or blockades that will seriously affect energy production and exports, but there is clearly a risk of that happening.

Another factor that has contributed to relatively stable oil prices is weak demand growth in China, but it seems that authorities there are now fully committed to supporting the housing market and reigniting economic growth, and the strong rally in Chinese equities continued this week. We have also upgraded our expectations of growth in China. However, we are sceptical that the growth recovery will be strong enough to turn into a seriously inflationary force for the rest of the world and hence be a hindrance for expected rate cuts.

Euro area inflation declined in September to 1.8% y/y and is hence now below the 2% target. Perhaps more important, the month-to-month momentum in service prices dropped to just 0.14% by the ECB's calculation. There are some temporary factors at play and it is just one month, but we now judge the scale to have tipped in favour of an ECB rate cut at the next meeting on October 17, also because of weaker economic data (see Yield Outlook - Arguments for policy restrictiveness fade, 30 September). For example, although euro area unemployment remained at a record low in August, several indicators point to easing labour markets. Not least the reported labour demand from companies in the PMI surveys, which is usually a fairly good indicator of credit growth, has taken a turn downwards in the September data, but the euro area labour market also remains very fragmentated with more weakness to the North and strength to the South.

In the US, job growth of 254,000 in September was much stronger than expected. The unemployment rate declined to 4.1% from 4.2%, whereas average hourly earnings increased 0,4% compared to August, the second month with such a relatively strong increase. Together with other indicators of a relatively strong US labour market, this likely means that the next rate cut from the Fed will be 25bp rather than 50bp as last time. Note however that there will be one more job report before the rate decision in November, and as the September surprise illustrates, the job numbers are hard to predict and could surprise also in the other direction.

The most interesting data release scheduled for next week is US inflation data due on Thursday. The release is unlikely to change the market perception that inflation is mostly a solved problem and not a hindrance for rate cuts and that the labour market is the more important factor to watch, but how sticky service inflation is could well affect the Fed's thinking about the pace of rate cuts. With just a month to go before the election and the race being very close, US politics is also likely to draw attention - feel free to join our webinar on the fiscal, trade and market implications on 10.00 CET Thursday.

Sunset Market Commentary

Markets

US payrolls hit a home run. Literally every bit of the report was outright strong and topped estimates: from employment growth in the establishment survey over details in the household survey (used to calculate the unemployment rate) to upward revisions in previous reports. Starting with the job gains, they were a much bigger than expected 254k. That compares to the 150k median estimate and even crushed the most optimistic one of 220k. It coincided with a +72k revision of the previous two months. Gains were broad-based with manufacturing (-8k) and the transportation & warehouse sector being the exception (-9k). Unemployment eased from 4.2% (seen as the equilibrium rate by the Fed) to 4.1%. Other readings of the household survey were exceptional as well: the labour force expanded by 150k, the number of unemployment tanked by 281k while its own employment estimate came in at a whopping 430k. Wages grew 0.4%, beating the 0.3% forecast, and brought the y/y figure back to 4%. The strong payrolls tops of a week that mostly contained other strong data including a JOLTS uptick and the services ISM.

This critical piece of information is just one of many to come in the run-up to the Fed November 7 meeting and they are bound to trigger market swings in one direction or the other. From a short-term perspective and until we get these other data points, however, it seals the debate on whether the central bank will move by 25 bps or stick to a 50 bps clip. Bets on the latter evaporated. Money markets now expect the Fed to move ahead with 25 bps on the next four meetings. US yields skyrocketed with the front end of the curve underperforming. Net daily changes vary between 7 bps (30-yr) to 15 bps (2-yr). German Bund yields more or less rose by halve the US gains to trade 3.8-8.9 bps higher in similar flattening. Oil prices extend their recent ascent to $78 (Brent) and are in any case not hindering the rise in yields. The dollar tops the FX scoreboard. EUR/USD loses the 1.10 support area to trade at the lowest since mid-August (1.097). DXY pierces through parallel resistance of 102.16-102.36 towards 102.58. USD/JPY (148.55) closes in on the August correction high of 149.35/39. Sterling pared some of the steep losses yesterday after Bank of England chief economist Pill pushed back against Bailey’s plea for a more aggressive stance. He supports a gradual withdrawal of policy restriction and said the central bank needs to guard against the risk of cutting too far or too fast. EUR/GBP eases from 0.84+ to 0.838. The pound is no match for USD of course. GBP/USD slips further to 1.308. UK yields gapped higher at the open and joined the US move higher to add 12 bps at the front.

News & Views

The European Commission announced that a proposal to impose definitive countervailing duties on imports of battery electric vehicles from China has obtained the necessary support from EU Member States for the adoption of tariffs. The vote represents another step towards concluding the EC’s anti-subsidy investigation and results in the EC imposing additional levies of between 7.8% and 35.3% on top of an existing duty of 10%. According to people familiar with the procedure, 10 members states (including France and Italy) voted in favour of the proposal. 12 countries (including Spain, Belgium and the Czech Republic) abstained. 5 members (including Germany, Hungary and Slovakia) are said to have voted against. The EU decision likely will cause retaliation from China as it already started investigations on European dairy products and pork, amongst others. Still the EU indicated that it continues to work hard to explore an alternative solution.

After a protracted decline (-27%) between March 2022 and February this year, the food price index of the Food and Agriculture Organization of the United Nations (FAO) in September showed an acceleration in prices. The index was up 3.0% from August, marking the largest month-on-month increase since March 2022. Prices for all five commodity categories strengthened, with monthly increases ranging from 0.4% for the meat price index to 10.4% for sugar. The FFPI in September was 2.1% higher than a year ago but 22.4 % below its peak reached in March 2022. Cereal prices were up 3.3% M/M but still 10.2% lower compared to September last year. A monthly rise in wheat prices was mainly due to concerns over unfavourable weather conditions in some key exporters (Canada, European Union). Maize prices also increased M/M. Vegetable oil prices reached the highest level since early 2023 due to a continued rise in the prices across palm, soy, sunflower and rapeseed oils. Dairy prices were up 4.6% M/M and 21.7 Y/Y, driven by higher prices across all dairy products. Sugar prices jumped a sharp 10.4%.

Graphs

US 2-yr yield soars after September payrolls blew past every (even most optimistic) estimate

DXY: trade-weighted dollar index takes out first resistance, solidifying the recent bottoming out process

S&P500 gaps higher. Equities bank on the soft (or no) landing narrative instead of fearing a slower return to less restrictive policy

CBR commodity index leaves recent lows further behind, driven by an uptick in soft commodity prices along with the likes of oil and iron

US: Payrolls Come in Well Above Expectations, While Unemployment Rate Falls to 4.1%

Non-farm employment rose by 254k in September, well ahead of the consensus forecast calling for a gain of 150k. Job gains in the two prior months were revised up by 72k.

- Over the past three months, payroll gains have averaged 186k, only slightly below the 203k averaged over the prior twelve-month period.

Private payrolls rose 223k, with most of the gains concentrated in leisure & hospitality (+78k), health care & social assistance (+71.7k), construction (+25k) and professional & business services (+17k). Government hiring chipped in with 31k jobs last month.

- Encouragingly, the breadth of hiring rose to 57.6 in September, or the highest reading in eight months.

In the household survey, civilian employment surged by 430k, well outpacing a more modest gain in the labor force (+150k), which pushed the unemployment rate down a tenth of a percentage point to 4.1%. The labor force participation rate held steady at 62.7% for the third consecutive month.

Average hourly earnings (AHE) were up 0.4% month-on-month (m/m) – a modest deceleration from August's upwardly revised reading of 0.5% m/m. On a twelve-month basis, AHE were up to 4.0% (from 3.8% in August).

Key Implications

Overall, this was a strong employment report. Not only did job gains come in well above expectations, but revisions also showed a stronger pace of hiring in prior months. For the third quarter, payrolls totaled 557k, up from Q2's gain of 442k.

In a speech earlier this week, Chair Powell reiterated that the Fed is in no hurry to cut rates and that his base case is for two additional 25 basis point (bps) cuts by year-end. We know the Fed didn’t cut 50bps last month because the economy was headed towards recession. They cut to recalibrate the level of interest rates closer to the performance of an economy largely moving at a trend pace. However, they haven’t yet stuck the landing on inflation, and now commodity prices are on the rise – potentially impeding further improvement. Today’s report may not prevent another cut in November, but it certainly lends caution to the timing and level of the neutral rate. Following the payrolls release, futures markets are now pricing for just 57bps of additional easing by year-end (down from yesterday's 69bps).

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.37; (P) 146.80; (R1) 147.40; More...

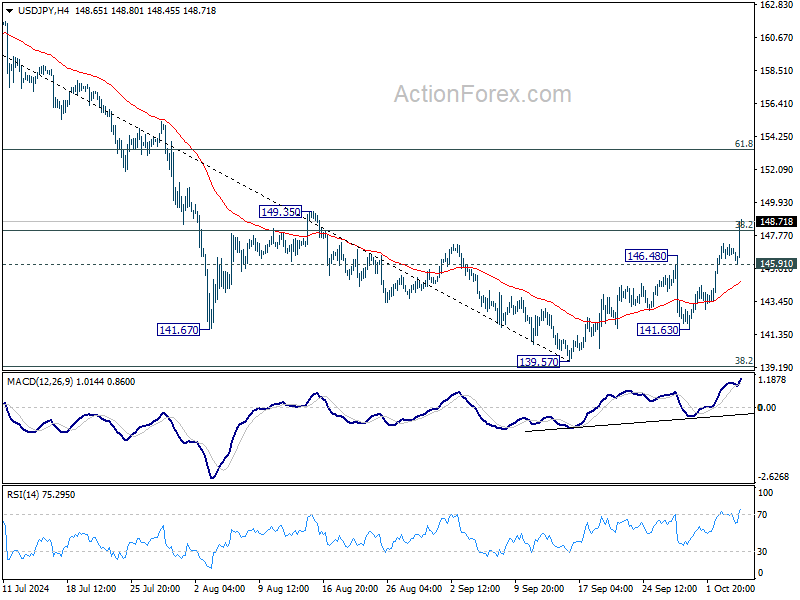

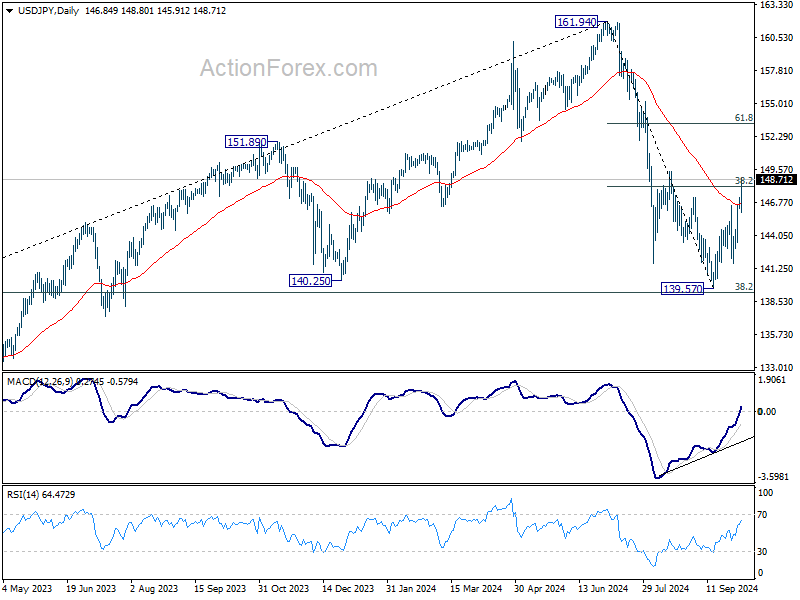

USD/JPY's rise from 139.57 extends higher today and intraday bias stays on the upside. The break of 38.2% retracement of 161.94 to 139.57 at 148.11 argues that whole fall from 161.95 has completed already, just ahead of 139.26 fibonacci level. Rebound from 139.67 is seen as the second leg of the corrective pattern from 161.94. Further rise should be seen to 61.8% retracement at 153.39. On the downside, below 145.91 minor support will turn intraday bias neutral again.

In the bigger picture, fall from 161.94 medium term top is seen as the first leg of the correction to whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. Firm break of 149.35 resistance will indicate that the second leg has started. However, sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

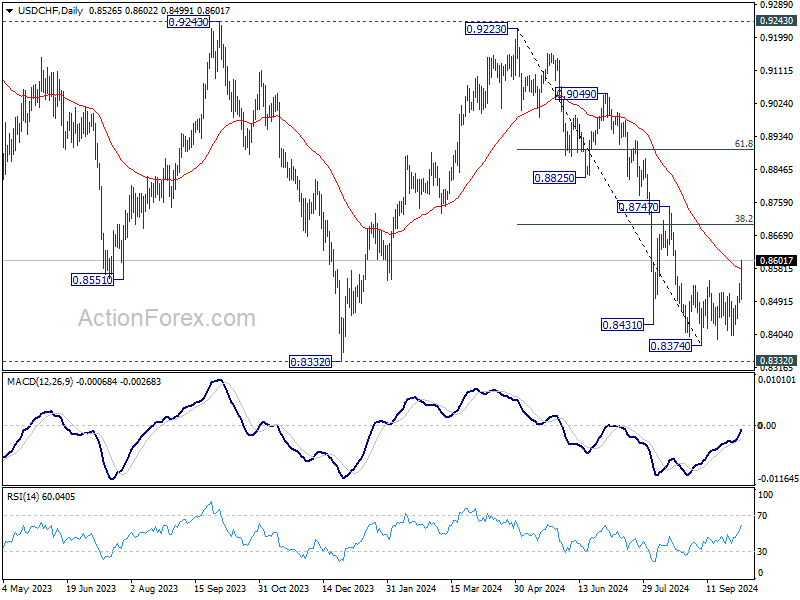

USD/CHF Mid-Day Outlook

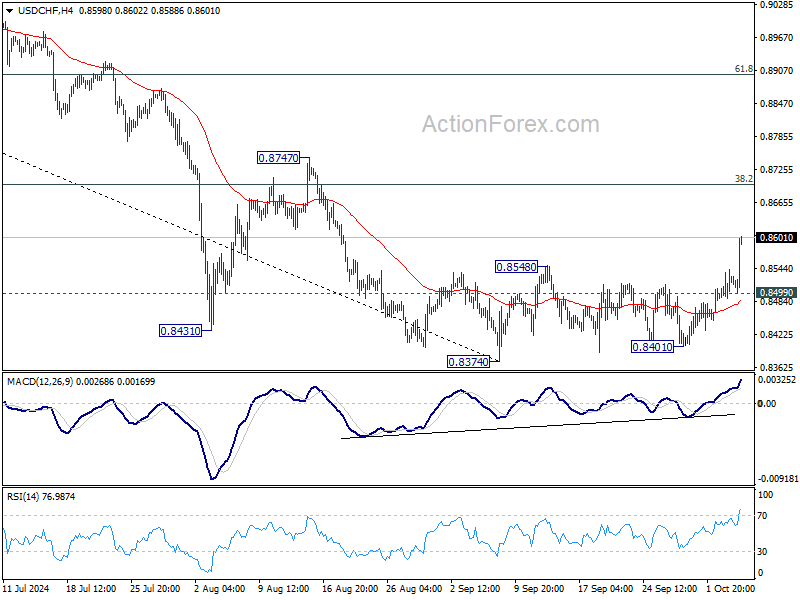

Daily Pivots: (S1) 0.8499; (P) 0.8521; (R1) 0.8551; More…

Intraday bias in USD/CHF is now on the upside with the strong break of 0.8548 resistance. Further rise should be seen to 38.2% retracement of 0.9223 to 0.8374 at 0.8698. Sustained break there will argue that fall from 0.9223 has completed after defending 0.8332 low. On the downside, below 0.8499 minor support will turn intraday bias neutral again.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

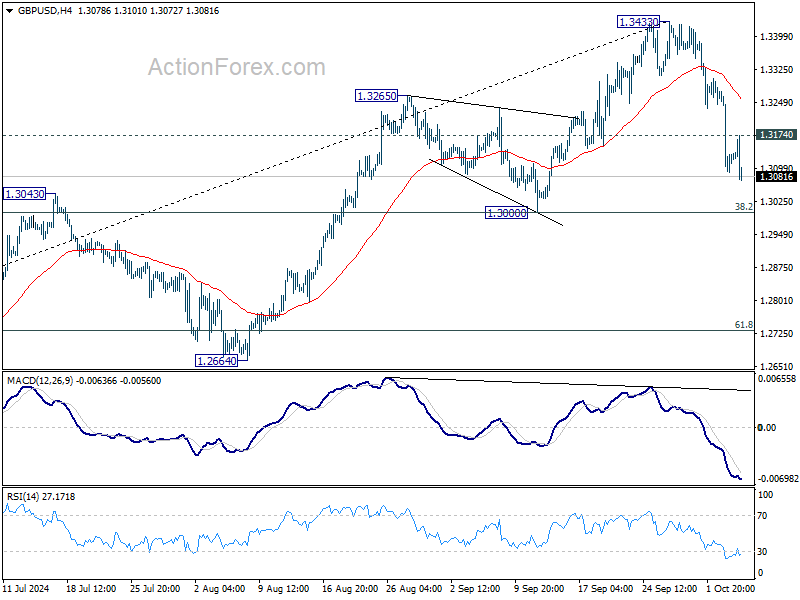

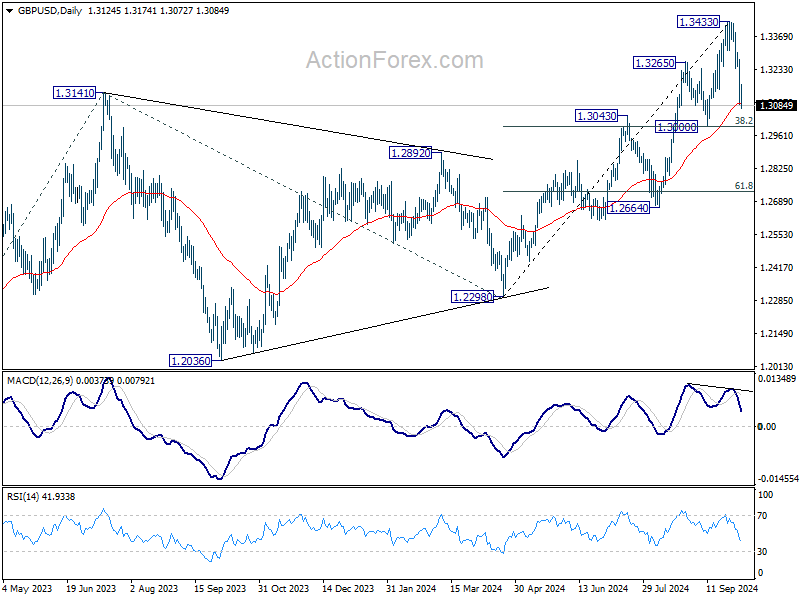

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3050; (P) 1.3166; (R1) 1.3241; More...

Intraday bias in GBP/USD remains on the downside as pullback from 1.3433 short term top is progress. Deeper decline would be seen, but strong support is expected from 1.3000 cluster (38.2% retracement of 1.2298 to 1.3433 at 1.2999 to bring rebound. On the upside, above 1.3174 minor resistance will turn intraday bias neutral first.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. For now, outlook will stay bullish as long as 1.3000 support holds, even in case of deep pullback.

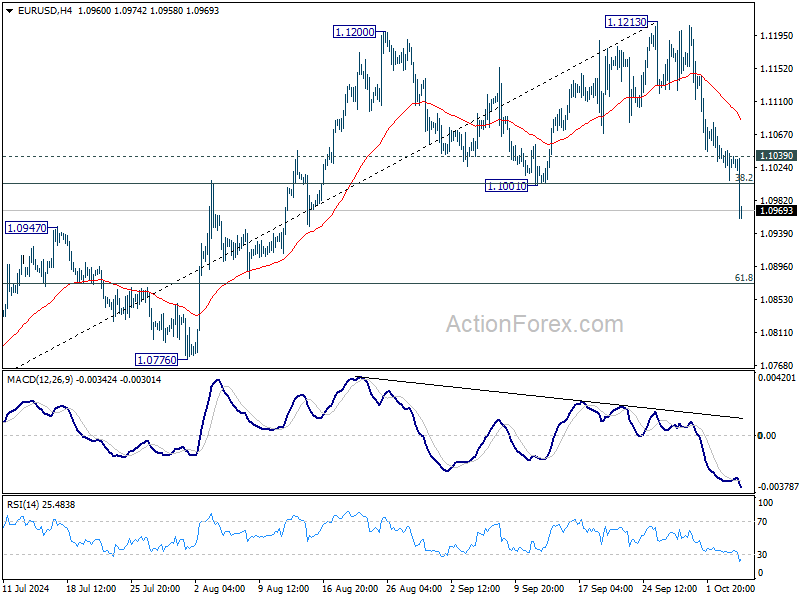

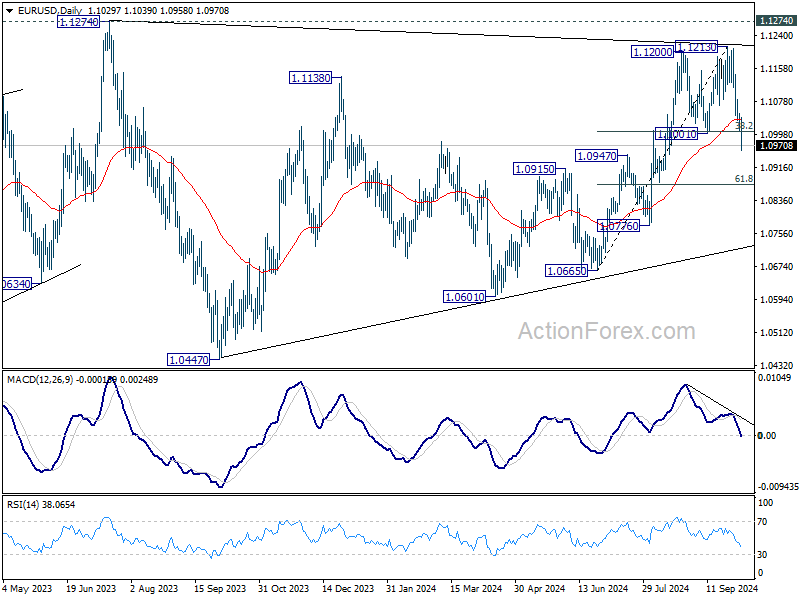

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1008; (P) 1.1030; (R1) 1.1052; More....

EUR/USD's break of 1.1001 cluster support (38.2% retracement of 1.0665 to 1.1213 at 1.1004) argues that whole rally from 1.0665 has completed at 1.1213. Intraday bias is back on the downside for 61.8% retracement at 1.0874 and possibly below. On the upside, above 1.1039 minor resistance will turn intraday bias neutral first.

In the bigger picture, rejection by 1.1274 resistance suggests that corrective pattern from 1.1274 (2023 high) is not completed yet. Instead, decline from 1.1213 might be another falling leg. Sustained break of 55 W EMA (now at 1.0877) will validate this case, and bring deeper fall towards 1.0447 support again.

Dollar Jumps after Strong NFP, Traders Abandon Bets on 50bps Fed Cut

Dollar surged across the board during early US trading after the all-around stronger-than-expected non-farm payroll report. The data showed much higher-than-anticipated job growth, a slight decrease in unemployment rate, and an acceleration in wage growth. This robust set of figures has led traders to largely abandon bets on a 50bps rate cut by Fed in November. Fed funds futures now reflect nearly a 90% probability of a 25bps cut instead.

Meanwhile, stock investors seem unfazed by the reduced chances of a larger rate cut. Stock futures climbed as investors welcomed the strong jobs growth, while bond markets saw an outflow of funds, pushing 10-year yield past 3.9% level and heading toward 4%.

Overall in the forex markets, Yen is currently the day’s worst performer, weighed down further by surging bond yields. New Zealand Dollar follows as the second weakest, with Swiss Franc also losing ground. Meanwhile, British Pound is the second strongest, boosted by BoE Chief Economist Huw Pill’s call for caution on fast rate cuts. Canadian Dollar comes in third, with Euro and Australian Dollar positioned in the middle.

In Europe, at the time of writing, FTSE is down -0.09%. DAX is up 0.69%. CAC is up 1.18%. UK 10-year yield is up 0.110 at 4.133. Germany 10-year yield is up 0.076 at 2.228. Earlier in Asia, Nikkei rose 0.22%. Hong Kong HSI rose 2.82%. China was still on holiday. Singapore Strait Times rose 0.33%. Japan 10-year JGB yield rose 0.0584 to 0.886.

US NFP jobs grow 254k in Sep, unemployment rate dips to 4.1%

US non-farm payroll employment grew 254k in September, well above expectation of 147k. That's also higher than average monthly gain of 203k over the prior 12 months.

Unemployment rate ticked down from 4.2% to 4.1%, below expectation of 4.2%. Labor force participation rate was unchanged at 62.7%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Annual average hourly earnings growth accelerated from 3.9% yoy to 4.0% yoy.

BoE’s Pill warns against cutting rates too quickly

In a speech today, Bank of England Chief Economist Huw Pill urged "caution in" reducing monetary policy restrictions, emphasizing the need for a "gradual" approach to rate cuts.

Pill highlighted that his "modal outlook" aligns with a scenario of "continued disinflation," but warned that this depends on maintaining a "restrictive monetary policy stance to bear down on inflationary pressures."

He stressed the importance of caution, noting there is still "ample reason" to carefully assess whether inflationary persistence is fully dissipating. While further reductions in the Bank Rate are expected if the economic and inflation outlook remains on track, Pill warned against the risk of "cutting rates either too far or too fast."

Pill was one of the four dissenting members of the MPC who voted against BoE's rate cut in August, underscoring his preference for a more measured approach in unwinding monetary tightening.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1008; (P) 1.1030; (R1) 1.1052; More....

EUR/USD's break of 1.1001 cluster support (38.2% retracement of 1.0665 to 1.1213 at 1.1004) argues that whole rally from 1.0665 has completed at 1.1213. Intraday bias is back on the downside for 61.8% retracement at 1.0874 and possibly below. On the upside, above 1.1039 minor resistance will turn intraday bias neutral first.

In the bigger picture, rejection by 1.1274 resistance suggests that corrective pattern from 1.1274 (2023 high) is not completed yet. Instead, decline from 1.1213 might be another falling leg. Sustained break of 55 W EMA (now at 1.0877) will validate this case, and bring deeper fall towards 1.0447 support again.

US NFP jobs grow 254k in Sep, unemployment rate dips to 4.1%

US non-farm payroll employment grew 254k in September, well above expectation of 147k. That's also higher than average monthly gain of 203k over the prior 12 months.

Unemployment rate ticked down from 4.2% to 4.1%, below expectation of 4.2%. Labor force participation rate was unchanged at 62.7%.

Average hourly earnings rose 0.4% mom, above expectation of 0.3% mom. Annual average hourly earnings growth accelerated from 3.9% yoy to 4.0% yoy.