Sample Category Title

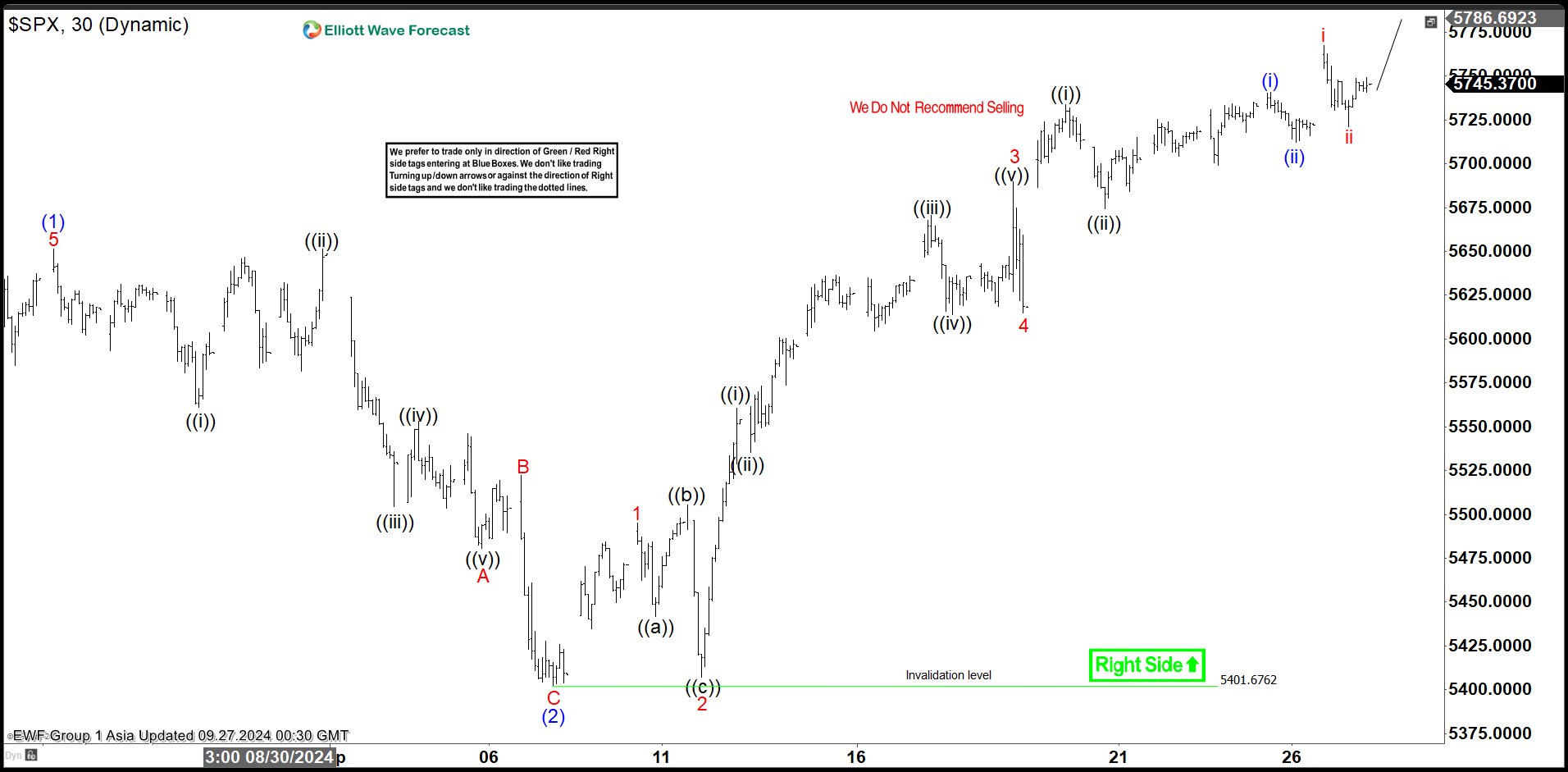

S&P 500 ($SPX) Elliott Wave Sequence Remains Bullish

Short Term Elliott Wave View in S&P 500 ($SPX) suggests that cycle from 8.5.2024 low is in progress as a 5 waves impulse. Up from 8.5.2024 low, wave (1) ended at 5651.62 and dips in wave (2) ended at 5402.62. Internal subdivision of wave (2) unfolded as a zigzag structure where wave A ended at 5480.54, wave B ended at 5522.47, and wave C lower ended at 5402.62. This completed wave (2) in higher degree.

Index has turned higher in wave (3) with internal subdivision as another impulse in lesser degree. Up from wave (2), wave 1 ended at 5495.14 and wave 2 pullback ended at 5406.96. Up from wave 2, wave ((i)) ended at 5560.41 and dips in wave ((ii)) ended at 5528.86. Wave ((iii)) higher ended at 5670.81 and pullback in wave ((iv)) ended at 5614.05. Final leg wave ((v)) ended at 5689.75 which completed wave 3 in higher degree. Pullback in wave 4 ended at 5615.08. Index has extended higher again in wave 5. Near term, as far as pivot at 5401. low stays intact, expect pullback to find support in 3, 7, 11 swing for more upside.

S&P 500 (SPX) 30 Minutes Elliott Wave Chart

SPX Elliott Wave Video

https://www.youtube.com/watch?v=IPCg_kZWIo4

A Rising Tide Lifts All Boats

Markets

A rising tide lifts all boats. Or in this case, a rising Chinese stock market lifts global risk sentiment. More fiscal spending, measures to stabilize the property sector, potential capital injections in the largest banks and forceful rate cuts are now also part of the toolkit announced earlier this week. European stock markets closed up to 2.35% (!) higher for the Eurostoxx50 with main US benchmarks extending their record race (+0.4%-0.6%) though closing off the day’s best levels. Most Asian stock markets show signs of some consolidation this morning, apart from China which adds another 5%-7% to an already record-week.

US eco data included a minor upward revision in the final Q2 print (3% Q/Qa), but especially consensus-beating durable goods orders (August) and lower weekly jobless claims (218k). Although second tier and coming ahead of PCE deflators (today) and ISM’s, ADP employment change and payrolls (next week) they did manage to swing the November Fed pendulum more into balance between a 25 bps and a 50 bps rate cut. Changes on the US yield curve ranged between +7 bps (2-yr) and -0.9 bps (30-yr). Lower oil prices partly help explain the strong curve shift with Brent crude prices dropping from $75/b to $71/b over the past two days. The move is linked to talk that Saudi Arabia is ready to abandon its unofficial $100/b oil price target. The FT reported that they would boost output from December 1st to regain market share. Bullish risk sentiment and lower oil prices balanced out interest rate support for the dollar. The greenback was going nowhere for most of the session and even lost some ground in the final stages of US trading. EUR/USD closed at 1.1177 from a start at 1.1133.

Today’s agenda contains first national European CPI indications for September (France, Spain, Belgium). Together with already released awful September PMI’s, they are the only input for the ECB in the short intermeeting period between September and October. PMI brough the possibility of a 25 bps rate cut back on the radar from a market point of view. We’re still in favour of a pause. When it comes to inflation numbers, ECB Lagarde at the press conference already “hedged” today and next month’s numbers by saying that they could fall somewhat further now before ticking up into year-end as energy-related base effects turn around. We’d be surprised though if markets pick up that nuance today, suggesting that lower inflation numbers could add to short term easing bets. Any potential euro weakness should remain short-lived going into next week’s big US eco week.

News & Views

Tokyo core inflation excluding fresh food printed at 2% Y/Y (from 2.4%) this month, matching the BoJ target. This move was mainly due to a reinstalment of measures to ease the cost of utilities (gas and electricity). The government measures are estimated to have reduced inflation by about 0.5%. A more strict core measure, excluding fresh food and energy was unchanged at 1.6%. Tokyo CPI data are seen as a good pointer for the national figure that will be released later next month. The October CPI reports are more important for BoJ policy setting as they might include price adjustments at the start of the fiscal second half of the year and give an indication on the degree that corporates are passing through the cost of higher wages. The Japanese yen didn’t respond to the inflation data, but suffered a setback (USD/JPY 146.50 from 145) after BoJ easing advocate Takaichi made it to the LDP leadership contest runoff (facing Ishiba).

The Bank of Mexico for the second consecutive meeting lowered its policy rate by 25 bps to 10.50%. Vice governor Jonathan Heath vote for an unchanged decision. The bank was mildly constructive in the inflation outlook going forward. Annual headline inflation decreased from 5.57% in July to 4.66% in the first fortnight of September. Core inflation continued trending downwards(3.95% Y/Y). It estimated that, although the outlook for inflation still calls for a restrictive monetary policy stance, its evolution implies that it is adequate to reduce the level of monetary restriction. The forecasts for headline and core inflation were revised slightly downwards for some quarters in the short term. Headline inflation is still expected to converge to the target in the fourth quarter of 2025. The Mexican CB targets 3.0% +/- a 1.0% tolerance band. The Mexican peso which traded in the defensive since April but came off the early September lows recently, closed yesterday’s session little changed near USD/MXN 19.63.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June and in September. Stubborn inflation (core, services) make follow-up moves less evident. We expect the central bank to stick with the quarterly reduction pace. Disappointing US and unconvincing-to-outright-weak EMU activity data dragged the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed kicked off its easing cycle with a 50 bps move. It is headed towards a neutral stance now that inflation and employment risks are in balance. Conservative SEP unemployment forecasts risk being caught up by reality and with it the dot plot (50 bps more cuts in 2024). We hold our call for two more 50 bps cuts this year. Pressure on the front of the curve and weakening eco data keeps the long end in the defensive for now as well.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large rate cuts trumped traditional safe haven flows into USD. An ailing euro(pean economy) only briefly offset some of the general USD weakness. EUR/USD’s dollar-driven ascent is nearing resistance around 1.12 again.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. But the economic picture is increasingly diverging to the benefit of sterling. EUR/GBP succumbed to horrible European September PMI’s. Support at 0.84 broke and brings the 2022 low (0.8203) on the radar.

Oil Prices Tumble on OPEC+ Supply – HICP Prints to Give Clues on Euro Area Figure

In focus today

In the euro area, focus today is on the September inflation data from Spain, France, and Belgium, which will give clues on the euro area data on Tuesday next week. We expect euro area HICP inflation to decline significantly to 1.8% y/y in September from 2.2% driven by both base effects on energy inflation and declining monthly energy prices. Excluding energy inflation and food, we expect core inflation remained at 2.8% y/y (0.20% m/m s.a.) due to sticky services inflation. The dip in headline inflation below 2% is expected to be temporary due to base effects and we expect inflation to rise above 2% again in November and December.

In Germany, we focus also on data on unemployment as the German labour market has weakened lately in contrast to other euro-area countries.

From the US, headline and core PCE inflation are released today, where markets see prints at +2.3% y/y and +2.7% y/y, respectively.

Although economic activity in Norway has been relatively weak over the past year, there has been only a moderate rise in unemployment. We expect that the unemployment rate increased marginally to 2.1% (seasonally adjusted) in September. Higher real wage growth and a period without rate hikes have improved the purchasing power of households, and private consumption picked up in the summer months. However, we expect that the retail trade was unchanged in August.

We are yet to see results from the Japanese ruling LDP leadership election, which will be interesting for markets due to the recent hawkish turn of the BoJ looking highly politically influenced. Abenomics loyalists preferring a slow normalisation of monetary policies as well as hawks are on the ticket in an election that will be heavily influenced by behind-the-scenes arm wrestling among party heavyweights.

Economic and market news

Oil prices tumbled about 2.5% on the news that Saudi Arabia has allegedly abandoned its (unofficial) price target of 100 USD/bbl. and instead opt to boost production to regain market shares. Note that we have no official communication yet, but the existing OPEC+ production cuts are slated to expire on 1 December, and this will be a shift from the trend since 2022 where focus has been on cutting, rather than increasing, oil production.

The SNB cut its policy rate by 25bp to 1.00% as we expected. Markets were close to evenly split between 25bp and 50bp, which resulted in a slight move lower in EUR/CHF upon announcement, though dovish communication caused the cross to erase losses. See more below.

In China, we got more stimulus signals with both verbal communication from the Politburo on the need for policy action to turn the economy as well as specific details on handouts and spending-vouchers, capital injection into state banks, and support for the property market. The combined package from the latest days highlights the strongest focus on ending the crisis we have seen since 2021 in our view. Chinese stocks, metal prices and the CNY continued to rally during the day.

Tokyo CPI saw core inflation at +0.19% m/m adjusted for seasonality, which is well in line with the BoJ's target of 2% annual inflation. The so-called 'core core' figure, which excludes food and energy, printed at just at 0.06% m/m seasonally adjusted however, indicating somewhat softer price pressure providing downside risk for inflation, and the market reaction was initially for a slightly weaker yen. Broadly, however, the BoJ will be satisfied with the latest print, and it will likely not change the decision in October, where we expect a hold.

Equities: What a day in global equities yesterday, marked by significant global increases and an intriguing sector rotation. On one hand, China is stimulating its economy; on the other, Saudi Arabia is potentially abandoning its oil price target to regain market share. In Europe yesterday, the energy sector was down more than 3%, while the consumer discretionary sector rose by more than 5%, driven by car producers and, notably, heavyweight luxury brands. This serves as a poignant reminder for all of us to check whether our judgments are correct and for the right reasons. It's easy to deceive oneself these days. In the US yesterday, the indices were as follows: Dow +0.6%, S&P 500 +0.4%, Nasdaq +0.6%, and Russell 2000 +0.6%. Most Asian markets are continuing to rise this morning, once again led by significant gains in Chinese stock markets - it looks like we are on track for best week for Chinese stocks since 2008(!).

FI: There was modest movement in European government bond yields yesterday apart from the continued pressure on France, but neither the Bund ASW-spread nor the BTPS-Bund spread has widened as we saw back in June. Hence, we are not seeing the same kind of risk-off movement as we saw back in June when President Macron called a snap election. Revision of US economic data as well as lower-than-expected jobless claims sent US bond yields higher with 2Y Treasuries rising almost 10bp yesterday.

FX: EUR/USD has spent most of the last two weeks within the 1.11-1.12 interval, though with a couple of unsuccessful attempts to break out of the range. USD/JPY tried to establish above 145 but was rejected twice yesterday. The British pound continues to shine on the back of relatively solid data and tight monetary policy stance - yesterday GBP/USD made a new 2.5year high at 1.3430. The Swiss franc strengthened after the SNB cut 25bp and EUR/CHF is back trading in the mid-0.94s. EUR/NOK held on to previous gains just below 11.80, while EUR/SEK was rangebound around 11.30. USD/CNY has fallen below 7.02 in recent days on the stronger stimulus signals and likely new capital inflows to the stock market. Our medium-term view is still that the cross will resume higher as we remain bullish on the USD. But there is rising downside risk to our 7.25 12M forecast. EUR/CNY has fallen to around 7.84, the middle of the 7.70-7.95 range it has traded in for a long time now. We could see more downside in the medium term as it is expected to also get support from a lower EUR/USD. The idiosyncratic strengthening of the CNY has led to a bit of decoupling in the normal high correlation between EUR/USD and EUR/CNY, but we expect it to resume when the dust settles from the recent days action.

Saudi Throws in the Towel

The S&P 500 printed its 42nd record high this year yesterday on the back of a mix bag of economic and corporate news.

First, the latest GDP data confirmed that the US economy grew 3% in Q2 and the price pressures fell. Corporate profits rose 3.5% in Q2 versus a 1.7% gain penciled in by analysts, and up from negative 2% the quarter before! Wait, wait, wait. The initial jobless claims came in lower than expected and continuing claims fell, defying the worries of an alarmingly softening jobs market. And if you put the strong data in the context of questionably dovish Fed, the US economy will soft-land on a mountain. It will be great if – and only if – the loosening monetary policy fed to a strong economy doesn’t boost inflation.

Due today, the Fed’s favourite gauge of inflation, the core PCE index, is expected to remain unchanged at 0.2% on a monthly basis, and print a small uptick – from 2.6% to 2.7% - on a yearly basis. Additionally, the personal income may have risen faster, but personal spending a bit slower than the previous month. A set of data in line with expectations will certainly keep the soft-landing vibes in play and secure a 43rd record high for the S&P500 before the weekly closing bell. But a stronger-than-expected PCE read, God Forbid, could bring the idea that the Fed and the dovish Fed expectations may have gone ahead of themselves and call for some correction. Yesterday’s robust GDP read brough the probability of 50bp cut at the November meeting slightly below 50%, but the chances are still very close to a coin toss.

China’s pandora box

China announced a mix bag of monetary and fiscal measures this week to prop up its economy and bring investors back to its shattered markets. This explosive cocktail of monetary and fiscal measures was what investors were demanding since years. And the satisfaction is clear – at least in the short run. The CSI 300 index gained more than 15% since the beginning of the week. The index pulled out the May-to-date negative trending channel top, and the almost two-year bearish trend top to catapult itself into a greatly overbought territory just before the beginning of a national holiday in China, next week. Likewise, Nasdaq’s Golden Dragon index is up by 20% since the week began and broke above its own two-year downtrending channel top. Buyers were so crowded in Shanghai that Shanghai’s stock exchange encountered problems to follow up orders.

Could this euphoria last? Maybe. The structural and balance sheet challenges, heavy local debt burden, the aging population, deflation and loss of confidence are hard to reverse. Enthusiasm could fade rapidly if the economy doesn’t react. Today, all we have in hand is that the Chinese industrial profits grew 0.5% ytd in August, meaningfully down from 3.6% printed a month earlier.

Ouch

WSJ reported that Saudi Arabia will drop its $100pb price target and start increasing output in December to gain market share. Ouch. This was a possibility that we were exploring since Saudi decided to shoulder production cuts by unilateral cuts. It’s finally happening now. If Saudi is not playing the production restriction game along with its OPEC peers, it will be hard for the rest of OPEC to hold on to a price-supportive strategy Concretely, if Saudi starts pumping, the others must follow to increase their revenue, as well. And that’s outright bearish for oil prices, also provided that the non-OPEC countries are pumping abundantly as well.

Voila, US crude is down to $68pb and the short-term outlook remains strongly negative.

In Europe

The Swiss National Bank (SNB) cut the interest rates by 25bp yesterday, as expected. The USDCHF barely reacted to the news but the SMI index closed the session near the highest levels since the beginning of this month. Beyond the Swiss borders, the Stoxx 600 flirted with ATH levels as the rate cut expectations in the developed world combined to the Chinese stimulus measures boosted appetite for Europe’s China and growth-sensitive stocks. LVMH jumped 10% yesterday as if the Chinese government decided to pump money directly into Louis Vuitton.

Anyway, the early CPI reads for France and Spain for September are due to be released this morning. The figures are expected to point at a further easing in price pressures. If that’s the case, we could see the 1.12 resistance strengthen before the closing bell. But the US dollar, and the PCE report will say the last word.

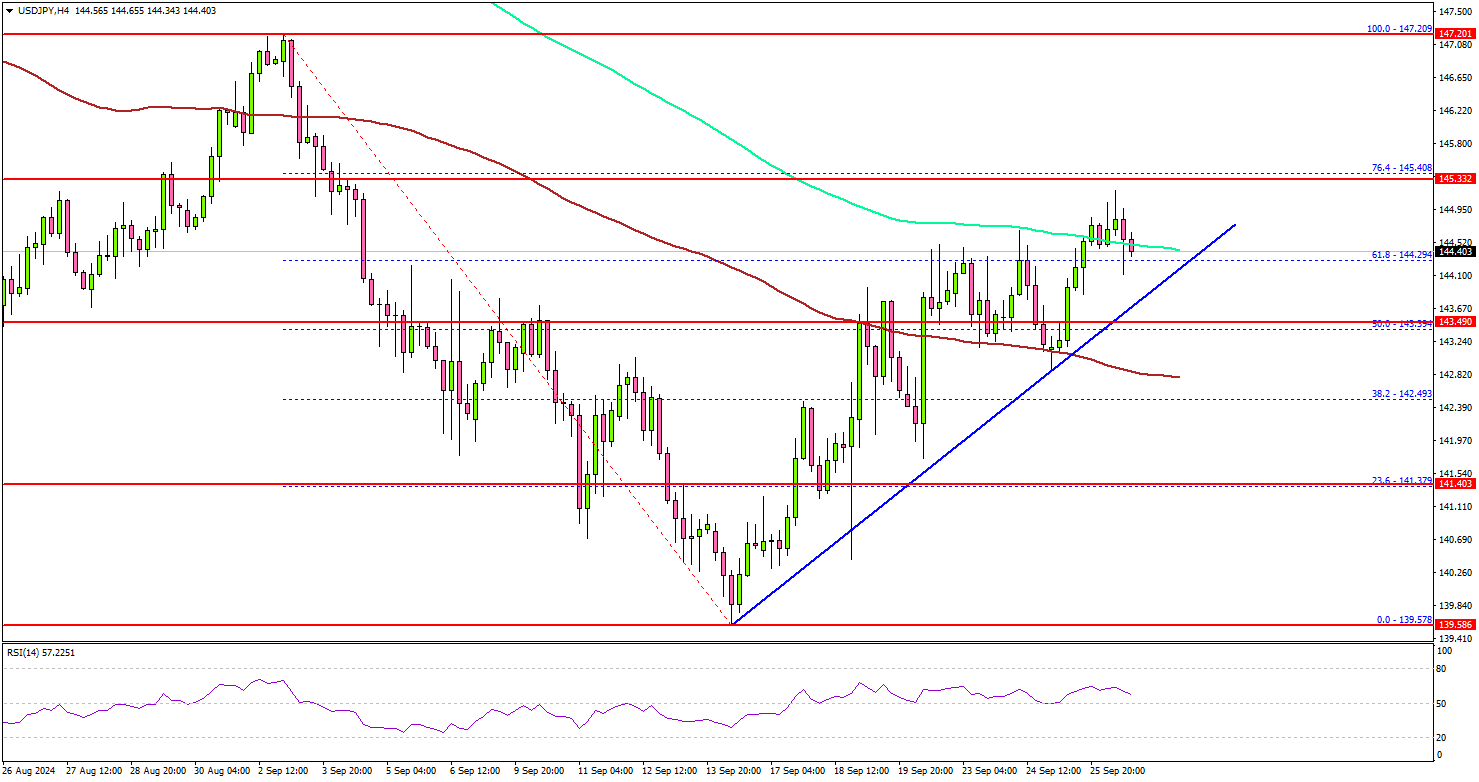

USD/JPY Recovers But Can It Surpass 145.50?

Key Highlights

- USD/JPY started a decent increase above the 142.50 resistance.

- A key bullish trend line is forming with support at 144.00 on the 4-hour chart.

- Oil prices started another decline from the $73.50 resistance zone.

- Bitcoin might aim for more gains above the $65,000 level.

USD/JPY Technical Analysis

The US Dollar found support near 139.60 against the Japanese Yen. USD/JPY formed a base and started a fresh increase above 141.20.

Looking at the 4-hour chart, the pair climbed above the 142.50 and 1.3400 levels. It even settled well above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

There was a clear move above the 61.8% Fib retracement level of the downward move from the 147.20 swing high to the 139.57 low. On the upside, the pair now faces hurdles near the 145.40 zone.

The 76.4% Fib retracement level of the downward move from the 147.20 swing high to the 139.57 low is also near 145.40. A clear move above the 144.40 and 144.50 levels might set the pace for a move toward 145.50. Any more gains might call for a test of the 146.20 zone.

On the downside, immediate support sits near the 144.20 level. There is also a key bullish trend line forming with support at 144.00 on the same chart, below which the pair might test 143.50.

The next key support sits near the 142.80 level and the 100 simple moving average (red, 4-hour). Any more losses could send the pair toward the 142.00 support zone.

Looking at Oil, there was a fresh bearish wave from $73.50 and the bears seem to be back in action.

Upcoming Economic Events:

- US Personal Income for August 2024 (MoM) - Forecast +0.4%, versus +0.3% previous.

- US Core Personal Consumption Expenditure for August 2024 (MoM) - Forecast +0.2%, versus +0.2% previous.

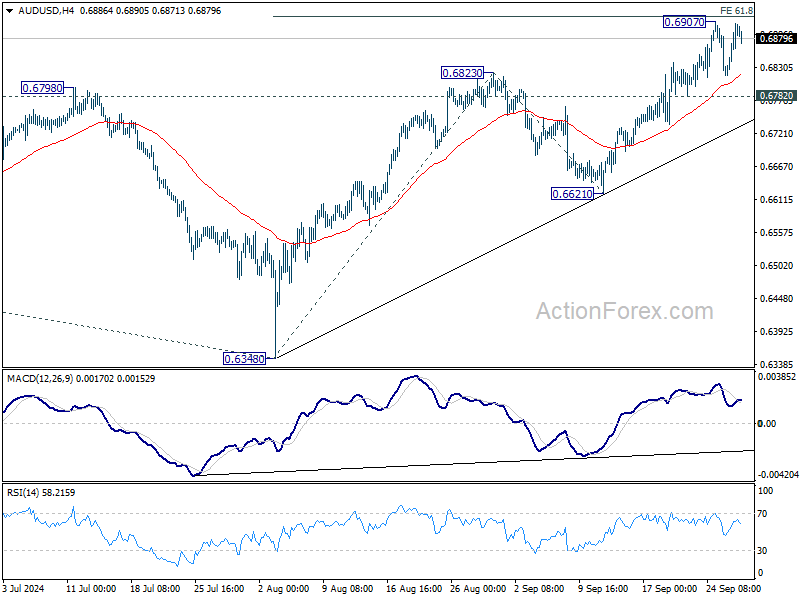

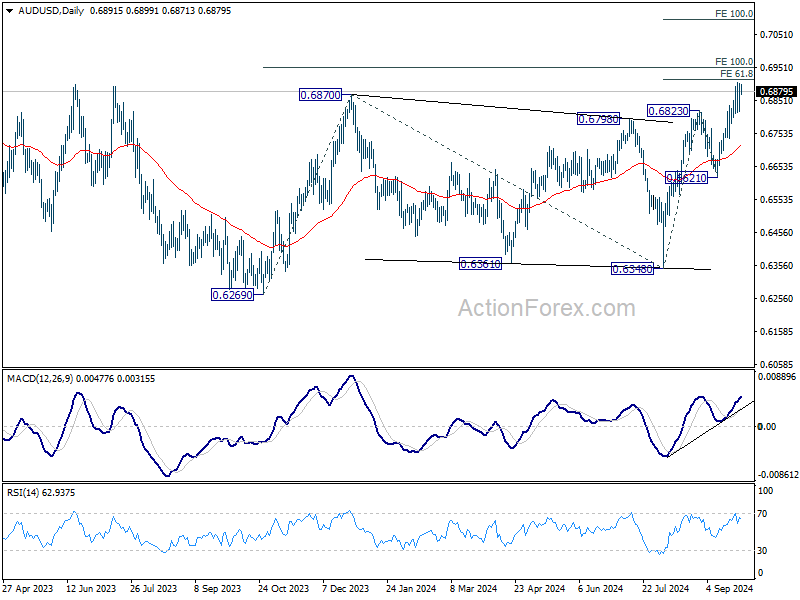

AUD/USD Daily Report

Daily Pivots: (S1) 0.6841; (P) 0.6873; (R1) 0.6927; More...

Intraday bias n AUD/USD remains neutral for the moment, and more consolidations could be seen below 0.6907. But further rally is expected as long as 0.6782 support holds. Firm break of 61.8% projection of 0.6348 to 0.6823 from 0.6621 at 0.6915 will extend the rise from 0.6348 to 100% projection at 0.7096 next.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6870 resistance will target 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941, and then 138.2% projection at 0.7179. This will now remain the favored case as long as 0.6621 support holds.

Risk-On Sentiment Drives Global Gains, Kiwi and Aussie Lead the Charge

Risk-on sentiment continues to dominate global financial markets today, driven by widespread monetary easing and a significant boost from China’s latest stimulus measures. US equities finished strong overnight, with all major indexes posting gains. S&P 500 hit a fresh record for the third consecutive time this week. Meanwhile, Germany’s DAX also surged to an all-time high.

In Asia, stocks in Hong Kong and mainland China skyrocketed as China's stimulus measures began to take effect. The injection of liquidity and supportive policies have renewed confidence among investors, leading to significant rallies in these markets.

The currency markets mirror this risk-on environment. Kiwi and Aussie are the week's biggest winners so far, followed by Loonie. On the opposite end of the spectrum, Japanese Yen has been the weakest, followed by Dollar and Euro. Swiss Franc and British Pound are trading in mixed in the middle. Today’s releases of Canadian GDP and US PCE inflation data are not expected to significantly alter these standings.

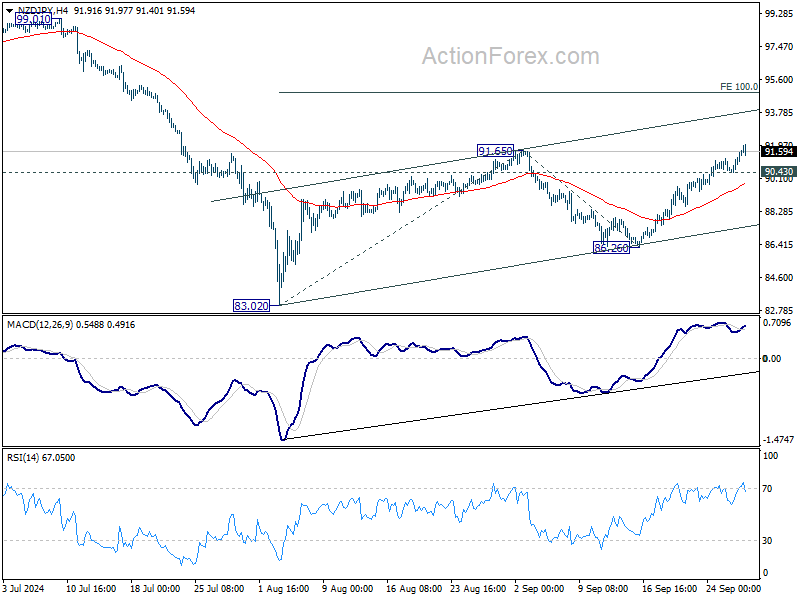

Among key currency pairs, NZD/JPY and AUD/JPY are vying for the top spot this week. NZD/JPY has a slight edge, gaining close to 2% for the week. Technically, NZD/JPY's breach of 91.65 resistance today indicates resumption of whole rally from 83.02. This rise is seen as the second leg of the corrective pattern from 99.01 high. Further rally is now expected as long as 90.43 minor support holds. Next target is 100% projection of 83.02 to 91.65 from 86.26 at 94.89.

In Asia, at the time of writing, Nikkei is up 0.30%. Hong Kong HSI is up 3.90%. China Shanghai SSE is up 2.14%. Singapore Strait Times is down -0.39%. Japan 10-year JGB yield is down -0.0138 at 0.817. Overnight, DOW rose 0.62%. S&P 500 rose 0.40%. NASDAQ rose 0.60%. 10-year yield rose 0.010 to 3.791.

Japan's Tokyo core inflation slows to 2%, supporting BoJ's cautious approach

Japan's Tokyo CPI core (excluding fresh food) slowed from 2.4% yoy to 2.0% yoy in September, aligning with expectations and marking its lowest level since May. Headline CPI dropped to 2.2% yoy from 2.6% yoy , while CPI core-core (excluding food and energy) remained stable at 1.6% yoy.

The primary driver of the deceleration in inflation was reduction in electricity and gas prices, influenced by government energy subsidies reintroduced by outgoing Prime Minister Fumio Kishida. These subsidies helped alleviate the impact of a particularly hot summer, shaving 0.5 percentage points off overall inflation.

This data, especially the stable core-core inflation, supports BoJ's cautious stance regarding more tightening. BoJ Governor Kazuo Ueda recently noted that inflationary risks have diminished, particularly with Yen's recent gains. BoJ is likely to remain on hold during its upcoming policy meeting on October 31.

PBoC cuts RRR and repo rate

In a follow-up to Governor Pan Gongsheng's earlier remarks this week, the People's Bank of China announced today a 50bps cut in the reserve requirement ratio and a 20bps reduction in the seven-day reverse repurchase rate.

This move is intended to release approximately CNY 1T in long-term liquidity, enabling banks to lend more and increase purchases of government bonds aimed at funding infrastructure projects. With the cut, the weighted average RRR will drop to around 6.6%. The central bank also lowered the seven-day reverse repo rate from 1.7% to 1.5%.

Further fiscal measures are anticipated before China's National Day holiday on October 1, as the Politburo has signaled a heightened focus on addressing economic pressures.

Reports indicate that the government will raise CNY 1T via special bonds, which will fund consumer goods subsidies, upgrades to business equipment, and provide a monthly allowance of CNY 800 yuan per child for households with multiple children. Additionally, another CNY 1T in special sovereign debt could be issued to help local governments manage their mounting debt burdens.

Fed's Cook reaffirms support for 50bps rate cut

Fed Governor Lisa Cook said she "whole heartedly" supported last week's 50bps rate cut, emphasizing that it was a reflection of "growing confidence" in Fed's ability to balance a solid labor market with moderate economic growth.

Cook noted in a speech overnight that the cut aligns with the ongoing progress towards bringing inflation back down to 2% target.

Looking ahead, Cook stressed the importance of "carefully assessing incoming data" and weighing risks as Fed considers further policy actions.

She highlighted the return to balance in the labor market and inflation as a sign of the economy’s "normalization" post-pandemic, adding that such balance is critical to sustaining long-term labor-market strength.

The normalization of inflation is particularly encouraging, Cook added, as it provides the foundation for maintaining a resilient job market. This balance between supply and demand will be central to future Fed decisions.

Looking ahead

France consumer spending, Germany unemployment, and Eurozone economic sentiment will be released in European session. Later in the day, Canada will publish monthly GDP. US personal income and spending, PCE inflation, and goods trade balance will be featured too.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6841; (P) 0.6873; (R1) 0.6927; More...

Intraday bias n AUD/USD remains neutral for the moment, and more consolidations could be seen below 0.6907. But further rally is expected as long as 0.6782 support holds. Firm break of 61.8% projection of 0.6348 to 0.6823 from 0.6621 at 0.6915 will extend the rise from 0.6348 to 100% projection at 0.7096 next.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6870 resistance will target 100% projection of 0.6269 to 0.6870 from 0.6340 at 0.6941, and then 138.2% projection at 0.7179. This will now remain the favored case as long as 0.6621 support holds.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Sep | 2.20% | 2.60% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Sep | 2.00% | 2.00% | 2.40% | |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Sep | 1.60% | 1.60% | ||

| 06:45 | EUR | France Consumer Spending M/M Aug | -0.10% | 0.30% | ||

| 07:55 | EUR | Germany Unemployment Rate Sep | 6% | 6% | ||

| 07:55 | EUR | Germany Unemployment Change Sep | 9K | 2K | ||

| 09:00 | EUR | Eurozone Economic Sentiment Sep | 96.5 | 96.6 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Sep | -9.8 | -9.7 | ||

| 09:00 | EUR | Eurozone Services Sentiment Sep | 5.6 | 6.3 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Sep F | -12.9 | -12.9 | ||

| 12:30 | CAD | GDP M/M Jul | 0.10% | 0.00% | ||

| 12:30 | USD | Personal Income M/M Aug | 0.40% | 0.30% | ||

| 12:30 | USD | Personal Spending Aug | 0.30% | 0.50% | ||

| 12:30 | USD | PCE Price Index M/M Aug | 0.20% | 0.20% | ||

| 12:30 | USD | PCE Price Index Y/Y Aug | 2.30% | 2.50% | ||

| 12:30 | USD | Core PCE Price Index M/M Aug | 0.20% | 0.20% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Aug | 2.70% | 2.60% | ||

| 12:30 | USD | Goods Trade Balance (USD) Aug P | -100.6B | -102.7B | ||

| 12:30 | USD | Wholesale Inventories Aug P | 0.20% | 0.20% | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Sep F | 69 | 69 |

PBoC cuts RRR and repo rate

In a follow-up to Governor Pan Gongsheng's earlier remarks this week, the People's Bank of China announced today a 50bps cut in the reserve requirement ratio and a 20bps reduction in the seven-day reverse repurchase rate.

This move is intended to release approximately CNY 1T in long-term liquidity, enabling banks to lend more and increase purchases of government bonds aimed at funding infrastructure projects. With the cut, the weighted average RRR will drop to around 6.6%. The central bank also lowered the seven-day reverse repo rate from 1.7% to 1.5%.

Further fiscal measures are anticipated before China's National Day holiday on October 1, as the Politburo has signaled a heightened focus on addressing economic pressures.

Reports indicate that the government will raise CNY 1T via special bonds, which will fund consumer goods subsidies, upgrades to business equipment, and provide a monthly allowance of CNY 800 yuan per child for households with multiple children. Additionally, another CNY 1T in special sovereign debt could be issued to help local governments manage their mounting debt burdens.

Japan’s Tokyo core inflation slows to 2%, supporting BoJ’s cautious approach

Japan's Tokyo CPI core (excluding fresh food) slowed from 2.4% yoy to 2.0% yoy in September, aligning with expectations and marking its lowest level since May. Headline CPI dropped to 2.2% yoy from 2.6% yoy , while CPI core-core (excluding food and energy) remained stable at 1.6% yoy.

The primary driver of the deceleration in inflation was reduction in electricity and gas prices, influenced by government energy subsidies reintroduced by outgoing Prime Minister Fumio Kishida. These subsidies helped alleviate the impact of a particularly hot summer, shaving 0.5 percentage points off overall inflation.

This data, especially the stable core-core inflation, supports BoJ's cautious stance regarding more tightening. BoJ Governor Kazuo Ueda recently noted that inflationary risks have diminished, particularly with Yen's recent gains. BoJ is likely to remain on hold during its upcoming policy meeting on October 31.

Fed’s Cook reaffirms support for 50bps rate cut

Fed Governor Lisa Cook said she "whole heartedly" supported last week's 50bps rate cut, emphasizing that it was a reflection of "growing confidence" in Fed's ability to balance a solid labor market with moderate economic growth.

Cook noted in a speech overnight that the cut aligns with the ongoing progress towards bringing inflation back down to 2% target.

Looking ahead, Cook stressed the importance of "carefully assessing incoming data" and weighing risks as Fed considers further policy actions.

She highlighted the return to balance in the labor market and inflation as a sign of the economy’s "normalization" post-pandemic, adding that such balance is critical to sustaining long-term labor-market strength.

The normalization of inflation is particularly encouraging, Cook added, as it provides the foundation for maintaining a resilient job market. This balance between supply and demand will be central to future Fed decisions.