Sample Category Title

Cliff Notes: China Delivers

Key insights from the week that was.

Following last week’s monetary policy announcements by the US FOMC and other major central banks, this week the spotlight turned to the RBA. The Board’s September meeting was predictably uneventful, with the cash rate unchanged at 4.35% and only incremental tweaks to their communication, which continues to emphasise labour market tightness and the need to bring aggregate demand and supply into balance. On the day, financial markets focused on the revelation that, in contrast to the prior policy meeting in August, this time the Board did not explicitly consider raising interest rates further. We see no reason to alter our view that the cash rate will remain unchanged until February, when we expect the first of four 25bp cuts through 2025.

This week’s new economic data, released after the RBA meeting, highlighted that the economy continues to make progress towards better balance between demand and supply. Indeed, the August CPI print showed a drop in headline inflation from 3.5%yr to 2.7%yr, in line with our expectations and the lowest since August 2021. The 17.6%yr drop in electricity prices, the steepest on record, reflecting rebates provided by the Commonwealth Energy Bill Relief Fund and state governments, was the main factor driving inflation lower. The RBA Governor suggested in Tuesday’s post-meeting press conference that policymakers will largely look through the fall owing to its temporary nature; however, the trimmed mean inflation measure, which excluded the electricity and auto fuel price declines, also eased from 3.8%yr to 3.4%yr, a new low for this inflation cycle. A more comprehensive picture of the developments in consumer prices will be available once the Q3 CPI data is released at the end of October. Our calculations suggest the August monthly figures are consistent with our existing 0.3%qtr and 0.7%qtr Q3 headline and trimmed mean CPI forecasts.

Meanwhile, the Q3 data on job vacancies, a good indicator of labour demand, showed that conditions in the jobs market continue to loosen. A 5.2% drop this quarter left the level of vacancies at 330k, more than 30% below the peak seen in May 2022 but still well above pre-pandemic norms (the long-run average is around 180k).

Public demand, productivity and the implications for inflation also received considerable attention in Westpac Economics’ analysis this week, and was brought together with the RBA view in Chief Economist Luci Ellis’ latest video update. Also of significance for the medium-term, the RBA’s latest Financial Stability Review was released.

Offshore, policy developments in China stole the show. Market participants have long wanted to see authorities in China make a stand over their growth ambitions and neutralise downside risks for the property market and consumption. This week’s announcements exceeded these hopes.

On Tuesday, the PBoC Governor Pan Gongsheng held a lengthy press conference to detail a comprehensive set of new and expanded monetary initiatives to support activity and sentiment across the economy. The 7-day reverse repurchase rate and the mortgage rate for existing borrowers were both cut, and guidance on forthcoming cuts to the loan prime rate and deposit rates given. The PBoC Governor also hinted at households being able to refinance with another lender if their current bank cannot accommodate the planned 50bp mortgage rate reduction for existing mortgages – the average loan rate for existing first-home borrowers is approximately 80bps higher than for new. More importantly, with respect to the quantum of credit in the economy, the reserve requirement ratio was cut by 50bps and a willingness to cut further into year-end shown. An injection of additional capital into the largest banks (who are state controlled and already have very healthy capital positions) was also flagged. Combined, these initiatives will materially increase available credit to all sectors. Also important for sentiment and the functioning of housing markets, second home buyers are being enticed to enter the market through a reduction in the minimum deposit from 25% to 15%. State-owned firms can also now borrow 100% of the principal needed to purchase unsold homes from the PBoC, up from 60% in May.

Also in focus for authorities is the state of the equity market. To aid a robust and sustained recovery in equities, the PBoC Governor announced at least USD70bn of 'liquidity support' for equity markets through a swap facility for participants – allowing less-liquid existing holdings to be swapped for high-quality liquid assets to back additional equity purchases. A re-lending facility will provide another circa USD40bn of liquidity to fund share buy-backs and additional cross-holdings. There was also reference to the potential establishment of a market stabilisation fund, while merger and acquisition activity is to be encouraged.

These initiatives are material and will be deployed with haste, but by themselves are more likely to strengthen and sustain a recovery than commence it. Rather it is the Politburo’s subsequent announcements which will act as the catalyst for recovery in the property market and consumption. Arguably of greater significance than the value of support mooted is official media’s reporting of the Politburo’s pledge to make the property market “stop declining”. This appears to apply to both investment activity and prices and comes in response to consumers' mounting concerns over their wealth and the uncertain timing and quality of dwelling completion. Western media including Reuters and Bloomberg subsequently reported that backing this edict is 2 trillion yuan (circa US$280bn) of special sovereign bond issuance for late-2024 from the Ministry of Finance to fund stimulus targeting consumption and to alleviate the financial pressures of local governments. While late in the year, the combined weight of the monetary and fiscal measures announced and mooted is highly likely to lead to the 5.0% growth target for 2024 being achieved and should also see a similar outcome in 2025. Success thereafter will be determined by how the private sector, particularly the consumer, responds.

Over in the US, the calendar was relatively quiet, with the annual revisions to GDP the only release of material significance. From Q2 2020 through 2023, GDP is now estimated to have averaged 5.5% annualised, up from 5.1% in the initial estimates, with two-thirds of the revision reportedly the result of stronger consumption. For 2022 and 2023 respectively, growth is now estimated at 2.5% (from 1.9%) and 2.9% (from 2.5%).

As has happened a number of times in this cycle, Gross Domestic Income was revised up materially for 2023 and the first half of 2024. In Q2 2024 alone, annualised GDI growth has been revised up 2ppts to 3.4%; and, in 2023, growth is estimated at 1.7% versus 0.4%. These revisions have resulted in the household savings rate being lifted from 3.3% to 5.2%. All told, these revisions show the underlying strength of the US economy, the consumer in particular. But also, cross referenced against the consumer price outcomes of the past two years, the importance of the supply side for inflation. These outcomes will provide the FOMC with comfort over the underlying health of their economy as well as the sustainability of the return of annual inflation to target.

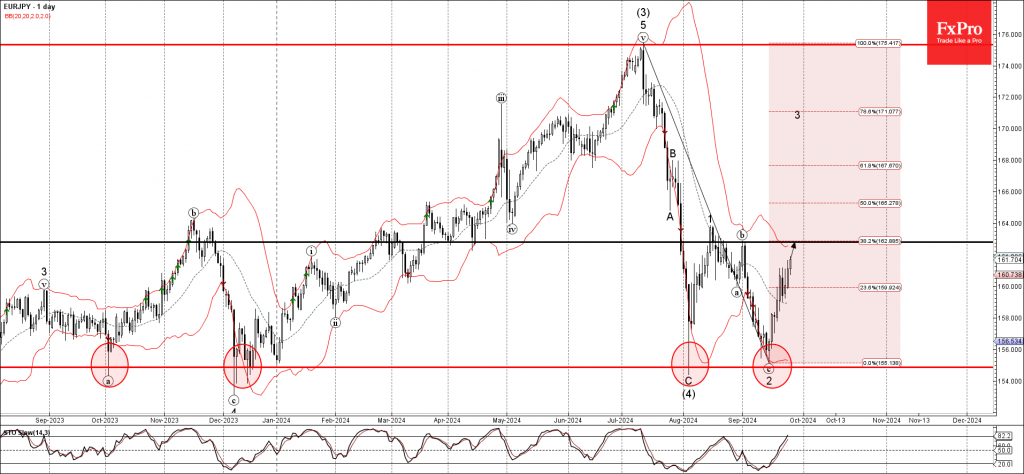

EURJPY Wave Analysis

- EURJPY rising inside minor impulse wave 3

- Likely to reach resistance level 162.8

EURJPY currency pair earlier continues to rise inside the minor impulse wave 3, which started earlier from the support area located between the long-term support level 154.85 (which has been reversing the pair from 2023) and the lower daily Bollinger Band.

The active impulse wave 3 belongs to the intermediate impulse wave (5) from the start of August.

Given the strongly bearish yen sentiment seen across the FX markets, EURJPY currency pair can be expected to rise further to the next resistance level 162.8 (top of wave b from the start of September).

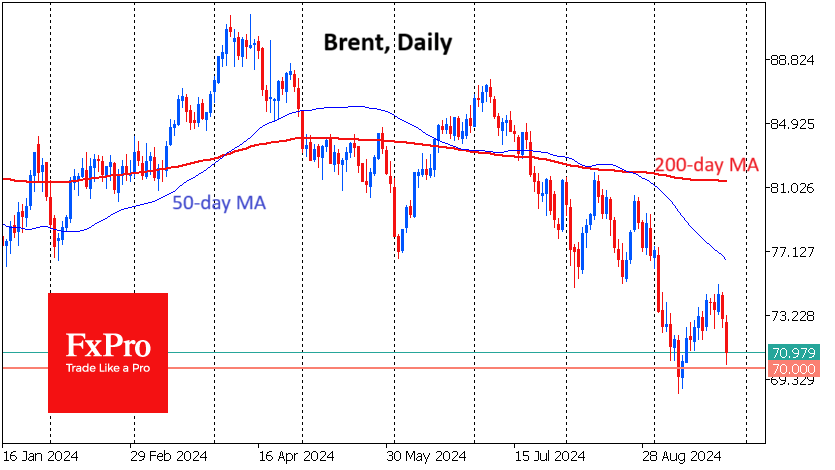

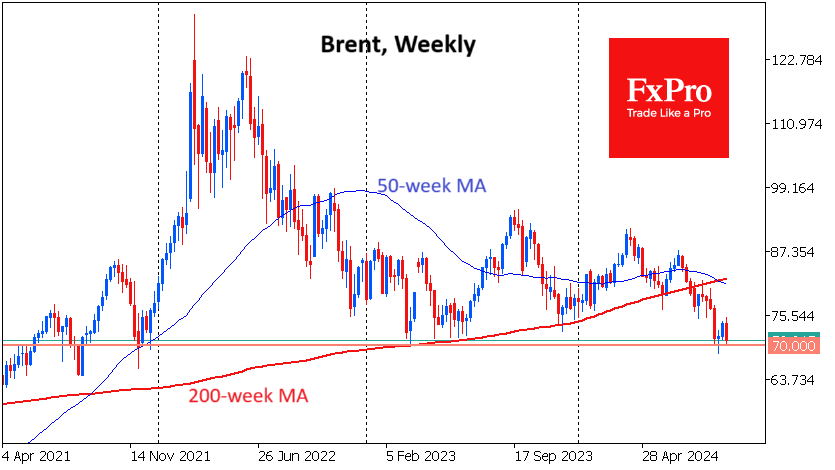

Oil Tests Crucial Support

Oil has lost more than 4% in two days despite the development of a rally in stock markets. The most important news for oil is an article in the FT that Saudi Arabia plans to abandon price targeting at $100 per barrel and intends to increase production. This is similar to the events of early 2020 when, after prolonged OPEC+ coordination, Russia and Saudi Arabia decided to join the fight for market share, which we were quickly taking away.

This news is just as important as in 2014 and 2020 when we saw similar course-changing episodes. Even earlier, in 2008, oil also went into freefall mode when it similarly became too plentiful for the economic conditions at the time. In all three cases, the price after the freefall fell into the $30 area.

So why did oil not go straight into freefall upon the release of such news? There are several reasons.

Firstly, this news needs to be confirmed. The freefall in 2020 and 2014 started after the OPEC meetings when the change of targets was announced publicly and officially.

Second, America is replenishing depleted oil reserves, making the process a regular occurrence with the price of a barrel of WTI near $70.

Third, the U.S. economy maintains a strong growth rate and market optimism is fuelled by speculation that China’s stimulus will boost the economy and commodity prices, including oil.

Fourth, America has been very sluggish in ramping up production and has not invested much in developing new wells. This suggests that if the price falls, the supply from the US could start to dwindle quite quickly.

A new drop in the $30 area looks possible, but it is a very pessimistic scenario. Technically, the Brent price is testing support near $70, which was the 2023 low and reversed the price to the upside.

However, the 200-week average, which is now at $82.1, also provided support, and further declines accompanied a dip below it in July.

Testing the area of last year’s lows is the most important frontier. A failure of Brent below $70 could trigger a freefall. But for now, we cannot rule out the possibility of a rebound.

Sunset Market Commentary

Markets

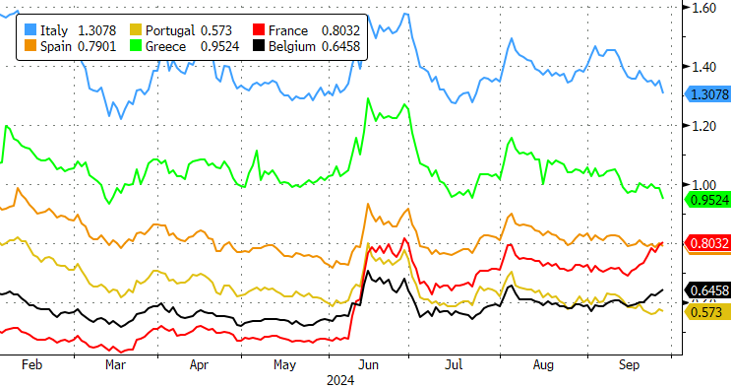

European trading mostly revolved around China’s Politburo promise of more forceful cuts, necessary fiscal spending and vow to stabilize the ailing real estate market in late Asian trading dealings this morning. It fired up stock markets, in particular Chinese. The CSI300 jumped another 4%+ and is headed for its biggest weekly gain in a decade. European markets bathed in the positive spillovers with the likes of the EuroStoxx50 eking out gains of >2% and the Stoxx600 bracing for a record close. The AUD and NZD are the best performers in currency markets. Their respective countries have important trade ties with China. German Bunds outperformed in core bond markets. German yield changes vary between -2.4 (30-yr) and -3.0 bps (2-yr) with the 2-yr testing the recent/March 2023 lows. The French spread vs. Germany’s 10-yr yield is grabbing some headlines. Growing risk premia push it above the Spanish one for the first time since 2007 (80 bps vs 79 bps). Investors increasingly worry about France’s fiscal mess and the inability of a frail coalition government to do something about it. US Treasuries swapped earlier gains for losses after the release of some second tier data. US durable goods orders topped estimates across the board, both on a headline level (0.5% vs -2.6% expected) and in the different core gauges. Shipments – used as a proxy for investment in GDP calculations – came in at the expected 0.1%. Weekly jobless claims eased from 222k to 218k, the lowest since May, defying expectations for an increase to 223k. US yields reversed earlier losses to trade +3 bps (2-yr) higher and flat at the back end ahead of what could have been a potential market mover: Fed chair Powell’s pre-recorded speech at the 10th annual US Treasury Market Conference. “Could have”, since Powell did not touch on monetary policy nor did he comment the economic outlook.

News & Views

The Swiss National Bank (SNB) for the third consecutive meeting lowered its policy rate by 25 bps to 1.0%. Markets in advance even saw some probability of a 50 bps cut to prevent a further unwarranted rise of the Swiss franc. Inflationary pressures decreased significantly (1.1% in August). Imported goods and services contributed to the decline in inflation which also reflects the recent CHF appreciation. Overall, Swiss inflation is mainly driven by higher prices for domestic services. The new inflation forecast (1.2% for 2024, 0.6% for 2025 and 0.7% for 2026) is significantly lower than in in June and would have been even lower without today’s cut. The strong Swiss franc, lower oil price and electricity price cuts announced for next January contributed to the downward revision. With modest Swiss growth this year (1.0%) and next year (1.5%) and slightly higher unemployment, the SNB expects that further rates cuts will be needed to ensure price stability. It repeated that it remains willing to be active in the FX market. In comments to Bloomberg Martin Schlegel, successor to current SNB president Thomas Jordan next week, indicated that current level still gives the SNB some room. He declined to say whether the franc is overvalued, but acknowledged that it is a challenge from some Swiss firms. CHF strengthened slightly (EUR/CHF 0.945).

In their joint economic forecast released today, Germany’s leading economic institutes revised the outlook for growth in the country further down. After a contraction of 0.3% in 2023 growth is again expected to be negative this year at -0.1% (0.2% in previous forecast). Next year’s recovery is expected to be weak (0.8% from 1.4%). Growth in 2026 is seen at 1.3%. In addition to the economic downturn, the German economy is being weighed down by structural change. “Decarbonization, digitalization, and demographic change – alongside stronger competition with companies from China – have triggered structural adjustment processes that are dampening the long-term growth prospects of the German economy.” Economic growth will not return to its pre-coronavirus trend for the foreseeable future. The economic standstill is now also showing clearer signs on the labor market with slightly increased unemployment (seen at 6.0% this and next year after 5.7% in 2023). Inflation is seen holding near 2.0% in the 2024-2026 period.

Graphs

Spreads vs. Germany’s 10-yr of selected countries: France’s tops Spain’s for first time since ’07 as fiscal/political risk premia rises

CSI300 on track for its biggest weekly gain in a decade as authorities promise forceful monetary and necessary fiscal support

EUR/CHF: Swiss franc puts aside SNB’s third consecutive rate cut, sticks near record high levels

AUD/USD: Aussie and kiwi dollar outperform on hopes for Chinese revival. New test of recent highs in the making

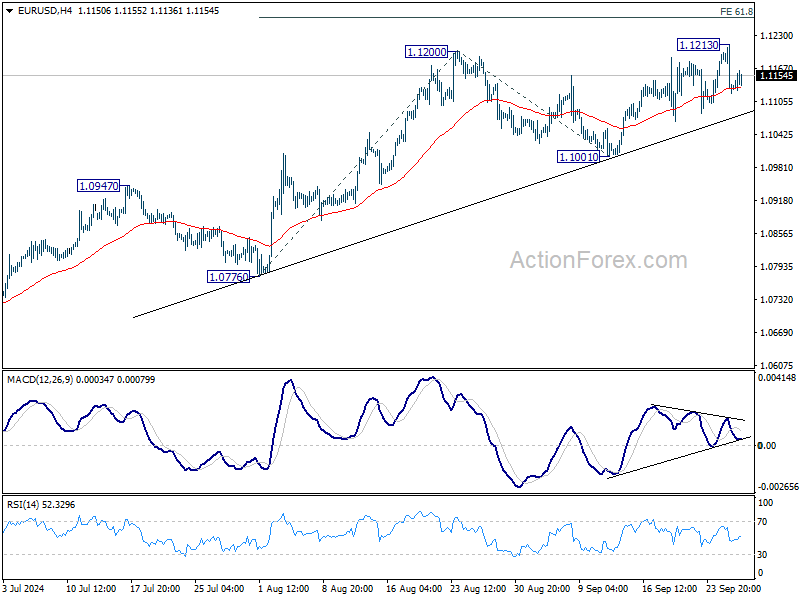

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1099; (P) 1.1156; (R1) 1.1191; More....

Intraday bias in EUR/USD remains neutral for consolidations below 1.1213. Further rally is expected as long as 1.1001 support holds. Above 1.1213 will extend larger rally from 1.0665 to 100% projection of 1.0776 to 1.1200 from 1.1001 at 1.1425.

In the bigger picture, corrective pattern from 1.1274 should have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm resumption of whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.1001 support holds.

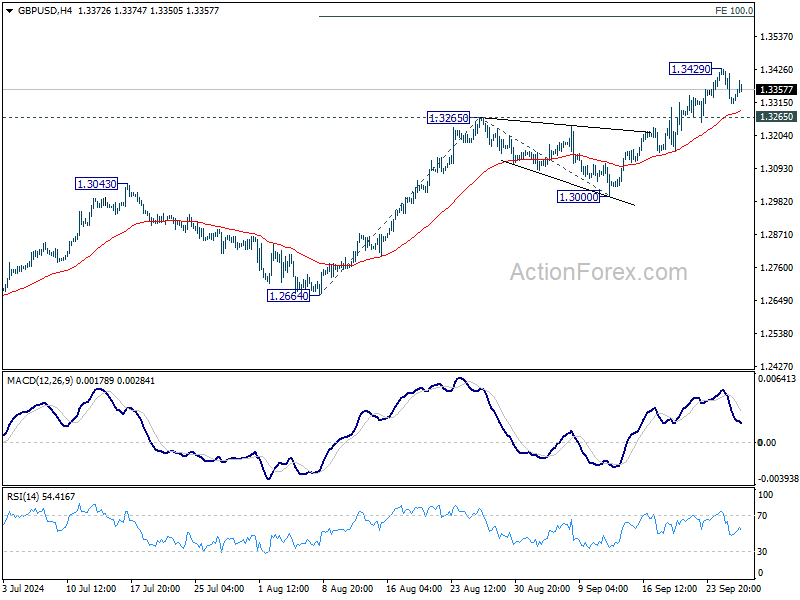

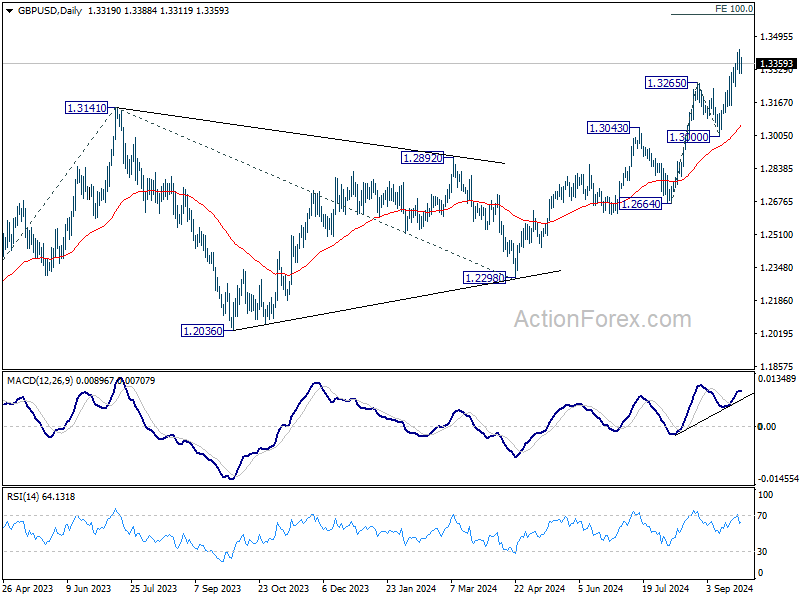

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3281; (P) 1.3355; (R1) 1.3398; More...

Intraday bias in GBP/USD remains neutral for consolidations below 1.3429 temporary top. Further rally is expected as long as 1.3265 resistance turned support holds. Above 1.3429 will extend larger rally to 100% projection of 1.2664 to 1.3265 from 1.3000 at 1.3601 next. Nevertheless, break of 1.3265 will turn bias to the downside for deeper pullback.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 61.8% projection of 1.0351 to 1.3141 from 1.2298 at 1.4022. For now, outlook will stay bullish as long as 1.3000 support holds, even in case of deep pullback.

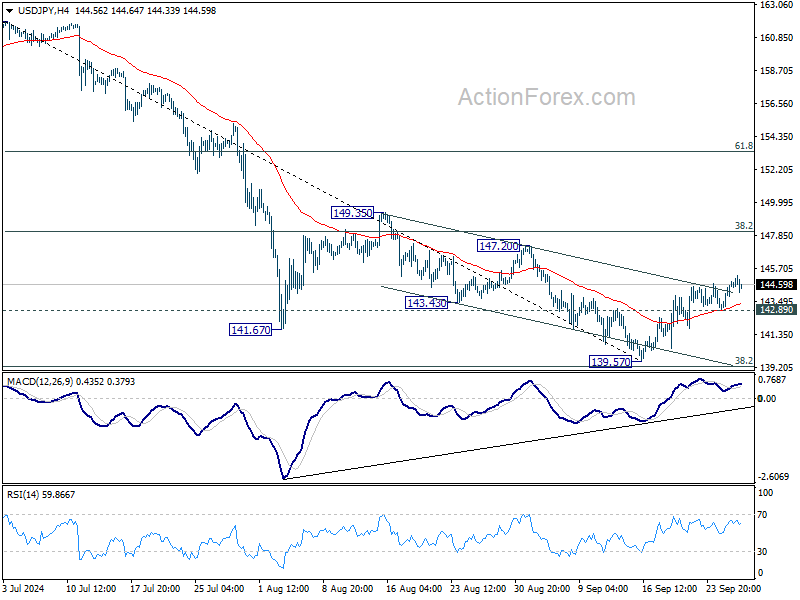

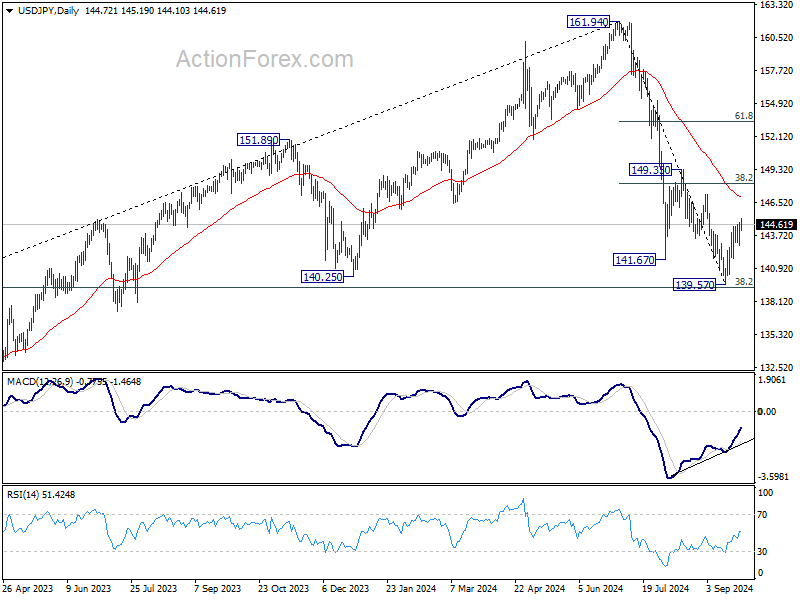

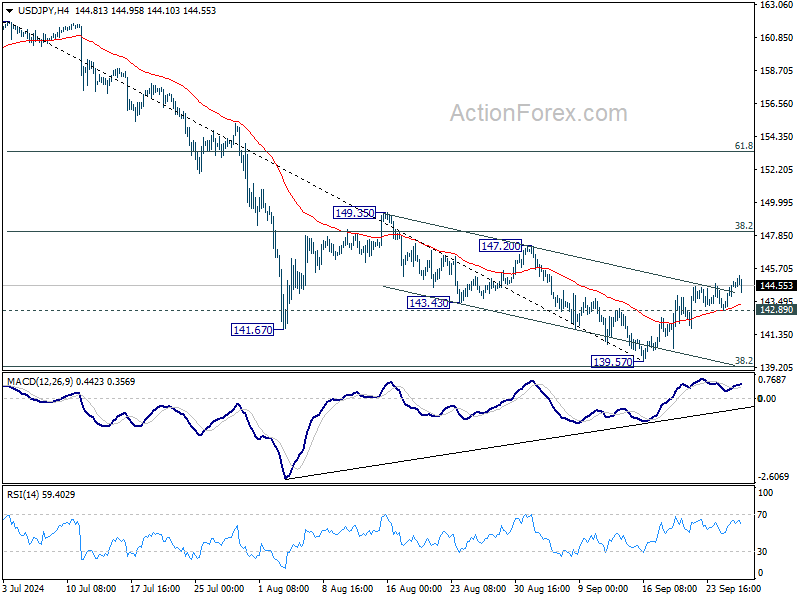

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 143.49; (P) 144.17; (R1) 145.42; More...

Intraday bias in USD/JPY remains on the upside at this point. Rebound from 139.57 is in progress for 38.2% retracement of 161.94 to 139.57 at 148.11. On the downside, below 142.89 minor support will turn bias to the downside for retesting 139.57 instead.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

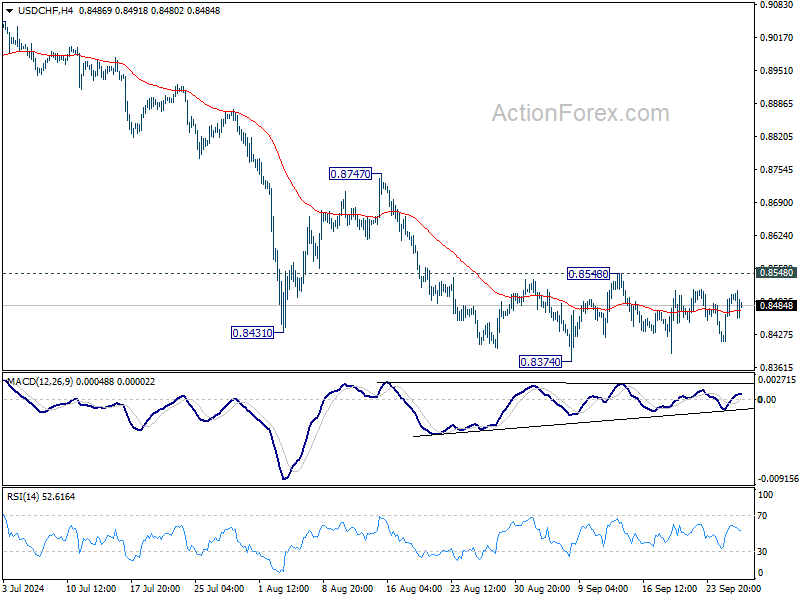

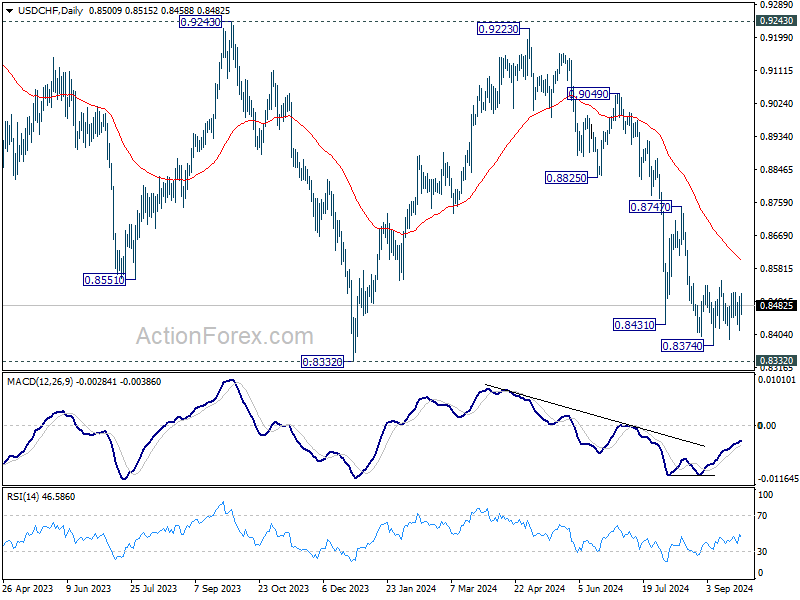

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8444; (P) 0.8475; (R1) 0.8536; More…

USD/CHF is still bounded in range of 0.8374/8548 and intraday bias remains neutral. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, break of 0.8548 resistance will turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

Swiss Franc Steady as Dovish SNB Tone Balances Offsets Rate Cut

Swiss Franc remained relatively stable today following SNB's decision to cut its policy rate by 25bps, bringing it down to 1.00%. This move defied some market speculations that anticipated a larger 50bps reduction. Despite opting for a smaller cut, SNB issued a decidedly dovish statement, sharply downgrading its inflation forecasts. The central bank signaled a clear easing bias, suggesting that further monetary accommodation is on the horizon. Incoming Chair Martin Schlegel reinforced this sentiment by indicating in an interview that another rate cut in December is "not unlikely."

In the broader foreign exchange market, currencies traded within familiar ranges. Dollar softened despite better-than-expected durable goods orders and jobless claims data. Canadian Dollar emerged as the second weakest of the day, while Japanese Yen followed as the third. Australian Dollar led the gains, buoyed by strong risk-on sentiment s in both China and Hong Kong. New Zealand Dollar was the second-best performer, with British Pound also showing strength. Euro and Swiss Franc are mixed, positioned in the middle of the currency spectrum.

Attention now shifts to the upcoming Asian session, where Tokyo's CPI data is set to be released. Core CPI is expected to slow notably from 2.4% to 2.0% in September. BoJ has already communicated its cautious stance on implementing further rate hikes. Cooling inflationary pressures would provide BoJ with additional room to maintain its wait-and-see approach, delaying any further monetary tightening.

Technically, USD/JPY's rebound from 139.57 is still expected to continue, despite weak upside momentum, to 38.2% retracement of 161.94 to 139.57 at 148.11. However, break of 142.89 minor support will suggest that the rebound is over and bring retest of 139.57 low.

In Europe, at the time of writing, FTSE is up 0.29%. DAX is up 1.35%. CAC is up 1.94%. UK 10-year yield rose 0.008 to 4.004. Germany 10-year yield is down -0.031 at 2.150. Earlier in Asia, Nikkei rose 2.79%. Hong Kong HSI rose 4.16%. China Shanghai SSE rose 3.61%. Singapore Strait Times fell -0.03%. Japan 10-year JGB yield rose 0.0182 to 0.831.

US durable goods orders flat in Aug ex-transport rises 0.5% mom

US durable goods orders rose 0.0% mom to USD 289.7B in August, much better than expectation of -2.8% mom decline. Ex-transport orders rose 0.5% mom to USD 188.5B, above expectation of 0.1% mom. Ex-defense orders fell -0.2% mom to USD 271.0B. Electrical equipment, appliances, and components, up two of the last three months, drove the increase, USD 0.3 billion or 1.9% mom to USD 14.4B.

US initial jobless claims fall to 218k, vs exp 226k

US initial jobless claims fell -4k to 218k in the week ending September 21, below expectation of 226k. Four-week moving average of initial claims fell -3.5k to 225k.

Continuing claims rose 13k to 1834k in the week ending September 14. Four-week moving average of continuing claims fell -6.5k to 1836k.

German economy set for 2nd year of contraction amid structural challenges

Germany's economic prospects have deteriorated further as the Joint Economic Forecast Project Group revised its GDP forecasts downward. The group now expects the German economy to contract by -0.1% in 2024, a downgrade from the previously anticipated 0.1% growth.

This adjustment implies that Germany will face two consecutive years of economic contraction, following a projected decline of -0.3% in 2023.

The forecast for 2025 has also been lowered, with GDP growth now expected at 0.8%, down from the earlier estimate of 1.4%. However, a modest recovery is anticipated in 2026, with growth projected to pick up to 1.3%.

Inflation is expected to decline, offering some relief to the economy. After reaching 5.9% last year, inflation is projected to slow to 2.2% this year and stabilize at 2% in both 2025 and 2026.

Geraldine Dany-Knedlik, head of forecasting and economic policy at DIW Berlin, highlighted the challenges facing Germany. She noted that "structural change" is compounding the economic downturn.

Key factors such as decarbonization, digitalization, and demographic shifts, along with intensified competition from Chinese companies, are initiating "structural adjustment processes." These developments are "dampening the long-term growth prospects" of the German economy, noted Dany-Knedlik.

SNB cuts 25bps, slashes inflation forecasts

SNB lowered its policy rate by 25 basis points to 1.00%, citing that inflationary pressure "has again decreased significantly", largely driven by the recent appreciation of Swiss Franc. SNB's statement also indicated that further rate cuts "may become necessary" in the coming quarters to maintain price stability in the medium term.

The revised inflation forecast shows significant downward adjustment compared to June, reflecting factors such as the stronger Swiss franc, lower oil prices, and upcoming electricity price cuts scheduled for January 2025.

The new conditional forecast sees inflation averaging 1.2% in 2024, 0.6% in 2025, and 0.7% in 2026, down from previous estimates of 1.3%, 1.1%, and 1.0%, respectively.

The SNB's forecast is based on maintaining the policy rate at 1.0% throughout the projection period. The central bank also noted that without today's rate cut, inflation forecasts would have been even lower.

On the economic growth front, SNB expects "rather modest" performance in the coming quarters due to the recent strengthening of Swiss franc and slower global economic development. It forecasts GDP growth of around 1% for 2024 and 1.5% for 2025.

BoJ minutes show divided views on rate hike timing

Minutes from BoJ's July meeting reveal a split among policymakers on the pace of future rate hikes. While BOJ raised its short-term interest rate to 0.25% by a 7-2 vote, differing opinions emerged on how quickly further increases should occur.

One member argued that if price trends follow the bank's outlook, it would be "necessary" to proceed with further tightening. Another suggested that with inflation projected to reach its target by H2 of fiscal 2025, the policy rate should gradually rise toward the neutral rate, estimated at around 1%. This member cautioned against rapid rate increases and favored a "timely and gradual" approach to avoid shocks to the economy.

However, some members expressed concerns about the risks of moving too quickly. One warned that monetary policy normalization should not be an end in itself and urged caution in monitoring the risks tied to policy shifts. Another highlighted that inflation expectations were "not being anchored at 2 percent", suggesting the need to avoid excessive market speculation about future rate hikes.

The minutes also reflect "high uncertainties regarding the level of the neutral interest rate" about Japan's neutral interest rate, given the long period without rate hikes. One member noted the difficulty of setting policy based on estimates of the neutral rate, calling for flexibility in adjusting policy based on evolving economic conditions.

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8444; (P) 0.8475; (R1) 0.8536; More…

USD/CHF is still bounded in range of 0.8374/8548 and intraday bias remains neutral. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, break of 0.8548 resistance will turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 23:50 | JPY | BoJ Minutes | ||||

| 06:00 | EUR | Germany GfK Consumer Sentiment Oct | -21.2 | -21 | -22 | -21.9 |

| 07:30 | CHF | SNB Interest Rate Decision | 1.00% | 1.00% | 1.25% | |

| 08:00 | CHF | SNB Press Conference | ||||

| 08:00 | EUR | ECB Economic Bulletin | ||||

| 08:00 | EUR | Eurozone M3 Money Supply Y/Y Aug | 2.90% | 2.50% | 2.30% | |

| 12:30 | USD | Initial Jobless Claims (Sep 20) | 218K | 226K | 219K | 222K |

| 12:30 | USD | GDP Annualized Q2 F | 3.00% | 3.00% | 3.00% | |

| 12:30 | USD | GDP Price Index Q2 F | 2.50% | 2.50% | 2.50% | |

| 12:30 | USD | Durable Goods Orders Aug | 0.00% | -2.80% | 9.80% | |

| 12:30 | USD | Durable Goods Orders ex Transport Aug | 0.50% | 0.10% | -0.20% | |

| 14:00 | USD | Pending Home Sales M/M Aug | 0.90% | -5.50% | ||

| 14:30 | USD | Natural Gas Storage | 52B | 58B |