Sample Category Title

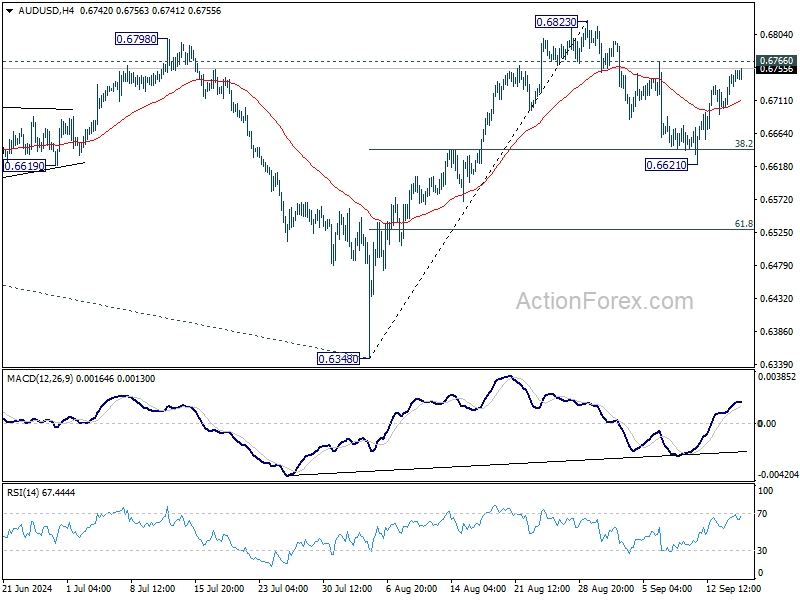

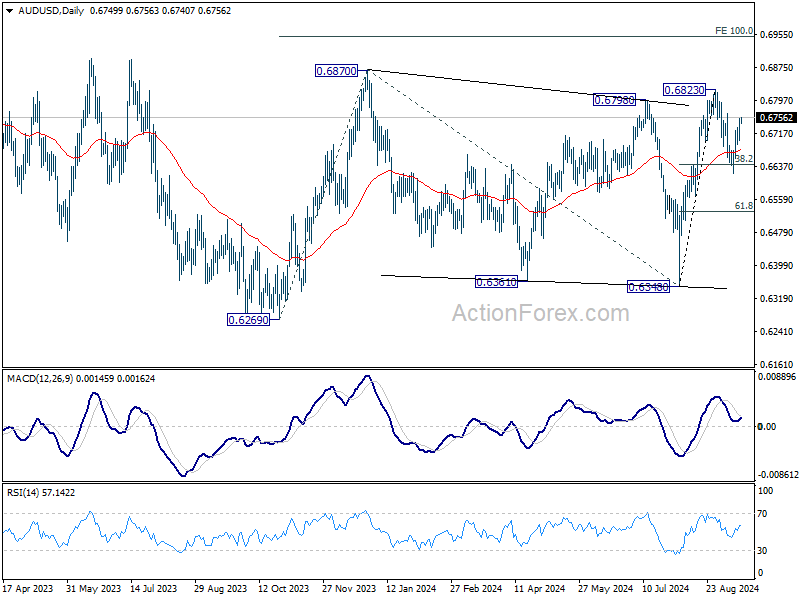

AUD/USD Daily Report

Daily Pivots: (S1) 0.6714; (P) 0.6734; (R1) 0.6771; More...

Intraday bias in AUD/USD remains neutral and outlook is unchanged. On the upside, break of 0.6766 resistance should confirm that corrective pullback from 0.6823 has completed at 0.6621 already. Retest of 0.6823 should be seen next. On the downside, however, sustained break of 38.2% retracement of 0.6348 to 0.6823 will target 61.8% retracement at 0.6529 instead.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

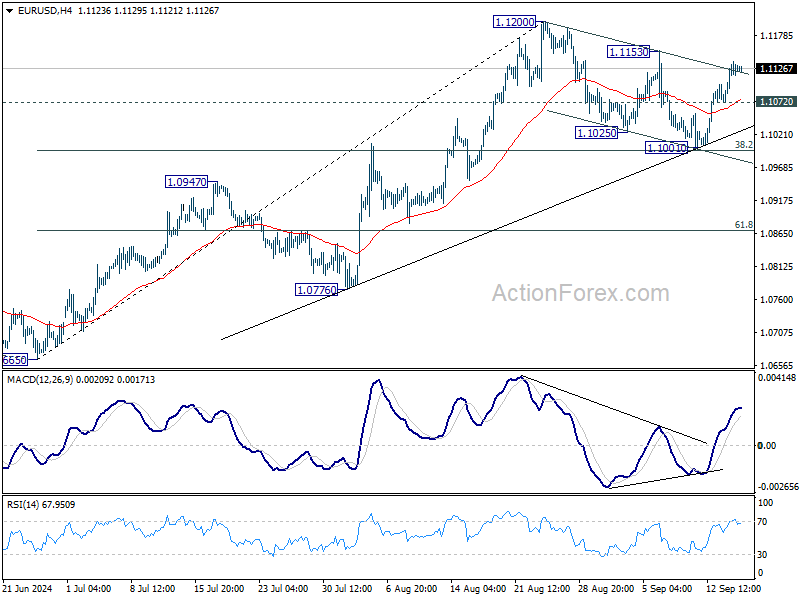

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1093; (P) 1.1115; (R1) 1.1156; More....

Intraday bias in EUR/USD remains neutral for the moment. On the upside, break of 1.1153 resistance will suggest that later rally is ready to resume and target 1.1200, and then 1.1274 high. On the downside, below 1.1072 minor support will turn bias back to the downside for 38.2% retracement of 1.0665 to 1.1200 at 1.0996 again.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

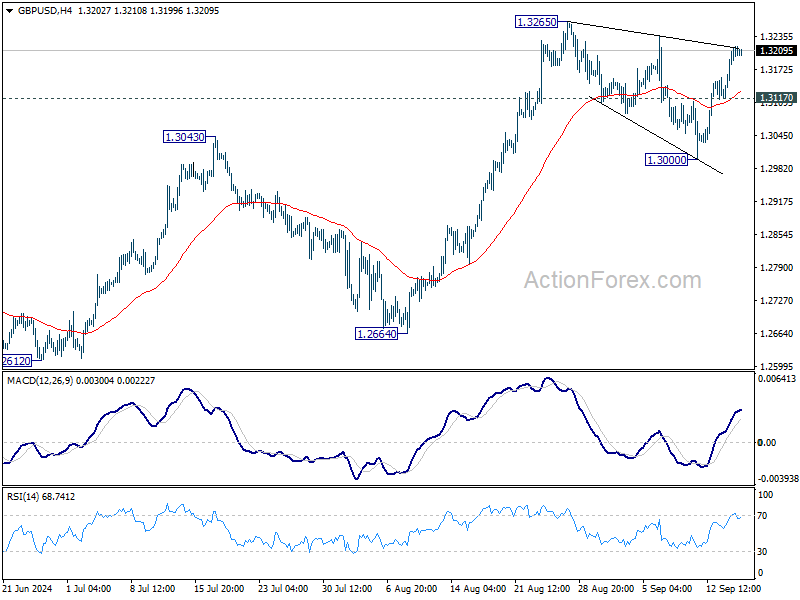

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3150; (P) 1.3185; (R1) 1.3251; More...

Intraday bias in GBP/USD stays neutral for the moment. On the upside, decisive break of 1.3265 will resume larger rally 1.3364 projection level next. On the downside, below, 1.3177 minor support will turn bias to the downside, to extend the correction from 1.3265 through 1.3000 support.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

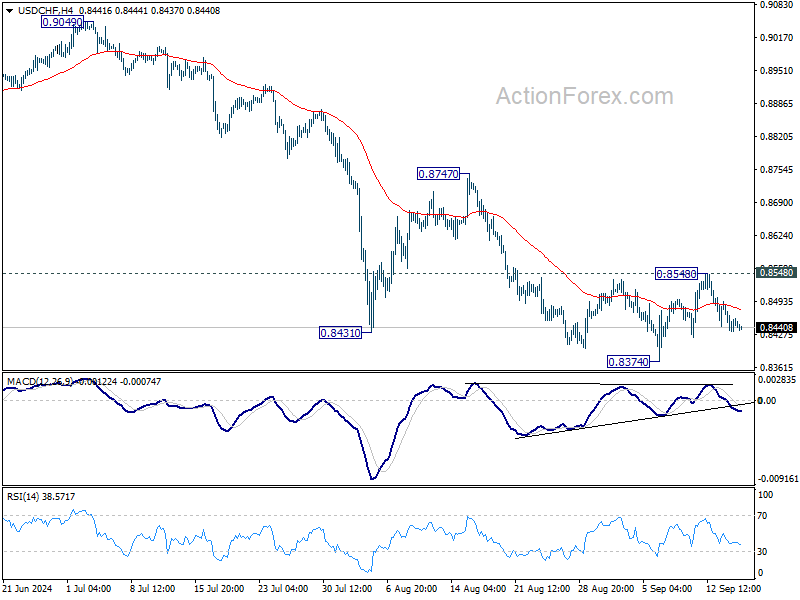

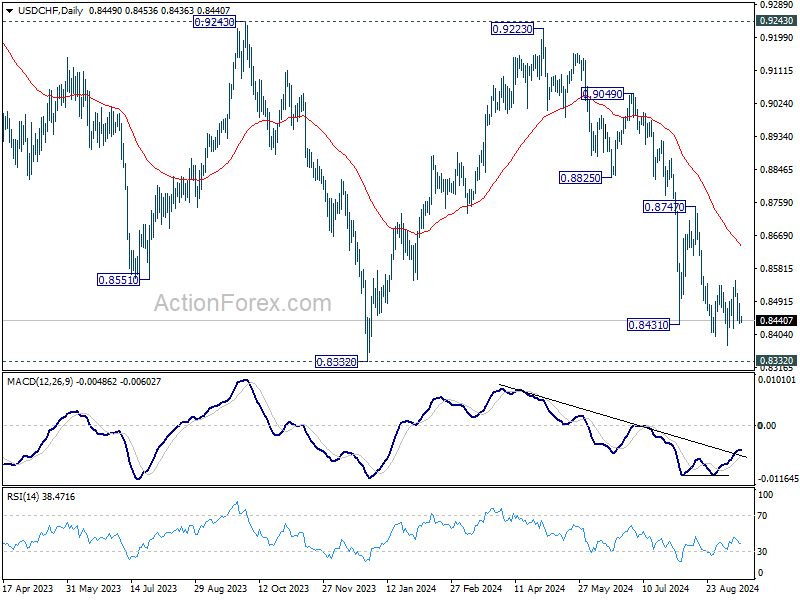

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8426; (P) 0.8457; (R1) 0.8479; More…

Intraday bias in USD/CHF remains neutral as range trading continues. With 0.8548 resistance intact, further decline is still expected. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, considering bullish convergence condition in 4H MACD, break of 0.8548 resistance will confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

Will It End in Tears?

Either the Federal Reserve (Fed) doves are going seriously ahead of themselves, or there will be a big disappointment when the Fed will announce its policy decision tomorrow. Or... the Fed will align with the market and give investors want they want, to avoid creating further panic. The expectation of a 50bp is now assessed nearly 70% chance. The US 2-year further dived below the 3.53% level yesterday, the 10-year yield is hanging around 3.62% this morning and the US dollar index remains under a decent selling pressure, much intimidated by the rising bets for a 50bp cut from the Fed tomorrow.

The reality is that, no one knows what the Fed will do right now. I still firmly believe that a 25bp cut would be the best option due to unalarming economic figures of the moment. It’s better to start slow and accelerate if needed. But I am also increasingly confused and think that the disappointment would be so massive that the Fed may – maybe - not dare giving the market just 25bp cut. And we also start hearing that some Democrats are putting fuel to the fire asking for a 75bp cut. So, it is in this atmosphere of high confusion that the Fed will start its two-day meeting today.

Good news is, the Fed confusion doesn’t really derail the S&P500 stocks from their upper trajectory. The index closed yesterday slightly higher, a few points below its ATH level – which absolutely doesn’t show any necessity for a 50bp cut by the way. Better news is that the equal weight index is catching up with the normal-weighted, technology heavy index, as the rate cut bets fuel the rotation trade. The Dow Jones hit a fresh record yesterday – another place where we see no emergency for a 50bp cut. And small caps are trading near their post-pandemic highs. Again, here as well, there is no apparent need for a 50bp cut.

And let me tell you this. If the economic data doesn’t show enough weakness after a potential 50bp cut, the Fed may have to stop and rethink, and that would be a bad, bad thing for markets.

In the FX and commodities, the dollar’s weakness makes the others look strong. The EURUSD spiked above the 1.11 mark yesterday and Cable trades just at the 1.32 this morning. US crude drilled through the $70pb offers and is consolidating timidly above this level this morning. The idea that the Fed could deliver a 50bp cut is appreciated among the oil bulls. But a 50bp cut could also backfire by giving the ones that call for recession reason. Consequently, the $70/72pb offers could be hard to drill.

In precious metals, gold consolidates gains near its ATH levels, benefiting both from a soft US dollar, the falling US treasury yields and a flight to safety on confusion and uncertainty about what the Fed will deliver tomorrow. Silver, on the other hand, is loving the idea of a larger rate cut from the Fed. That’s because silver has a higher proportion of industrial use than the yellow metal; it's used in electronics, solar panels, and other technologies. And when interest rates are cut, it generally signals an effort to stimulate economic growth, which boosts industrial activity. And the latter increases the demand for silver due to its widespread industrial applications. The price of an ounce jumped more than 10% since last week, and more than 15% since the beginning of August. The mint ratio – which is the ratio of gold to silver – is diving back toward the 60-80 average range, and has room to further fall with the upcoming rate cuts.

Intel jumps

Intel jumped more than 6% yesterday on news that it sealed a deal with Amazon’s AWS. According to the news, the companies will co-invest in a custom semiconductor for AI computing. Intel also confirmed that it will well separate its foundry business from the rest, to unlock its external foundry potential by giving its customers a better image of independence of its foundry unit. The news pleased investors, for once. A growing number of companies are exploring the potential of developing their own custom chips, a vision that Intel’s independent foundry services could help bring to life.

USD Easing Ahead of Fed Rate Decision

In focus today

We receive the German ZEW data for September today. The assessment of the current situation has been stuck at very low levels the past year and the expectations component has fallen in the past two months following a strong rebound. As risk sentiment in markets in September has been sour, we expect another weak ZEW reading.

From the US, August retail sales and industrial production data is due for release for August. This will mark the final piece of economic data before the Fed's September rate decision tomorrow, but it is unlikely to change the decision. We expect a 25bp case and guidance for more cuts to come.

Economic and market news

What happened yesterday

ECB's Kazimir and Kazaks commented on monetary policy. Kazimir said that ECB should wait with its next rate cut until the December meeting, to make sure not making policy mistakes in easing too quickly. He said that for him to back a rate cut in October he would require a powerful signal, but that is not likely to happen since there will be only little new information before the October meeting. Kazaks said that rates will continue to go down, and he sees no reason why not to agree with market pricing for 2025, so rates will hit 2.50% by mid-2025. We expect ECB to deliver its next rate cut at the December meeting.

USD eased yesterday with markets split between a 25 and 50 bp rate cut on Wednesday. In the absence of new data, markets shifted from pricing below 20% likelihood of a 50bp rate cut mid-last week to over 50%. EUR/USD ended yesterday around the monthly high of 1.113 mark. USD/JPY briefly fell below 140 on Monday morning, for the first time since last summer. Later it increased to above the 140 mark again. JPY has strengthened since early June when USD/JPY peaked around 161, as the Bank of Japan has signalled further rate cuts, while Fed and ECB have begun monetary easing cycle. We expect JPY to strengthen further and USD/JPY to decline steadily to 135 over the next 12 months.

Equities: Global equities were marginally higher yesterday, with defensive value stocks outperforming. Or perhaps more accurately, tech and consumer stocks underperformed. It is unusual to see defensive value sectors, including banks, outperform on a day when equities are higher, and yields are lower. This suggests that while investors still welcome lower interest rates, their appetite for tech has diminished. This shift is not due to weak earnings in the tech sector but likely because tech and similar sectors have reached a valuation premium that has investors increasingly looking elsewhere. To put it into perspective, tech has been the worst-performing sector over the last three months in a positive market, with financials outperforming tech by more than 10%. Similarly, value stocks have outperformed growth stocks by 7% over the last three months, despite US 10-year yields being down more than 50 basis points during the same period. Asian markets were very mixed this morning, with Japan emerging as the notable loser. US futures are marginally lower, while European futures are higher.

FI: Global rates fell further through the Monday session as markets added to rate cut expectations ahead of tomorrow's FOMC decision. OIS markets now have 39bp discounted, up from 34bp on the Friday close, despite the US Empire Manufacturing Survey printing much stronger than expected in yesterday's release. EGB curves generally saw a rather synchronized drop with the Bund curve down by some 2-3bp across tenors. Long-term EUR inflation swap rates (e.g. 5y5y) continued their rebound, as commodity prices seem to have bottomed for now.

FX: The USD started the FOMC week on the back foot, broadly weakening in the G10 space. This caused EUR/USD to trade above 1.11 and USD/JPY to breach 140 for the first time since July of last year. Scandies also gained against the USD but traded sideways against the EUR, with EUR/NOK remaining just below 11.80 and EUR/SEK just above 11.30. EUR/GBP edged lower during yesterday's session.

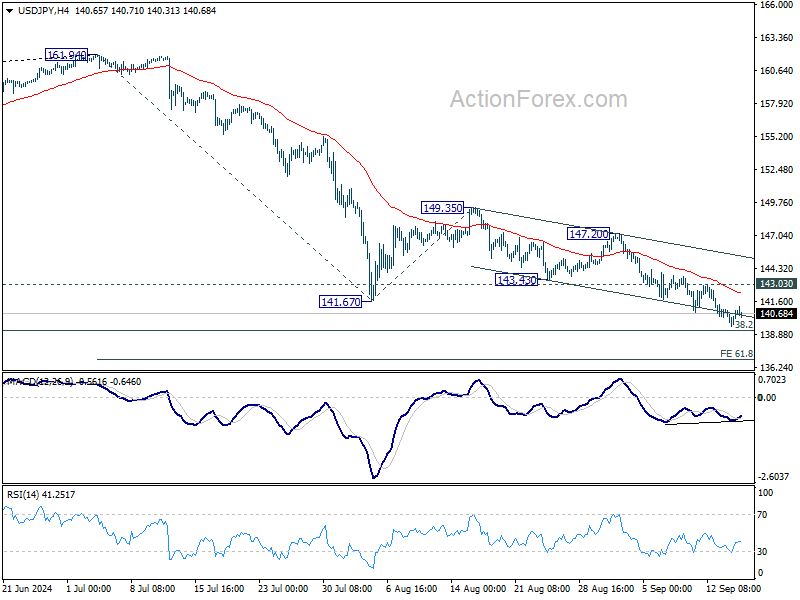

USD/JPY Daily Outlook

Daily Pivots: (S1) 139.82; (P) 140.37; (R1) 141.17; More...

Intraday bias in USD/JPY is turned neutral first as it recovered just ahead of key 139.26 fibonacci level. Considering bullish convergence condition in 4H MACD, break of 143.03 resistance will indicate short term bottoming and turn bias back to the upside for rebound towards 147.20. However, decisive break of 139.26 would carry larger bearish implications, and target 61.8% projection of 161.94 to 141.67 from 149.35 at 136.82.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Investor Sentiment Wavers Despite DOW’s Highs, Loonie Pressured Ahead of CPI

Investor sentiment is currently mixed, reflecting the heightened uncertainty surrounding this week's crucial Fed meeting. While DOW surged to a fresh record high overnight, and S&P 500 edged closer to its historical peak too, the tech-heavy NASDAQ struggled, ending the session in negative territory. The mixed performance extended to Asia, where Nikkei fell sharply in its first session after a long weekend, contrasting with the rally in Hong Kong's stock market.

In currency markets, Yen's strength faded quickly after a brief rally on Monday. The steep appreciation since July has raised concerns within Japan, with Finance Minister Shunichi Suzuki stating today that "rapid fluctuations in exchange rates are not desirable." He also pledged to monitor the rising Yen's impact on the economy closely and to take appropriate action if necessary.

Canadian Dollar, meanwhile, is underperforming, lagging behind its peers in the face of Dollar's broad-based weakness. It is currently the weakest performer in the currency market this week. Traders are eyeing today's Canadian inflation report, which could provide direction for the Loonie. The data will be critical for assessing the BoC's next move, especially after dovish comments from BoC Governor Tiff Macklem, who recently hinted that the central bank might be open to a more aggressive policy easing if economic conditions warrant it.

Overall, Australian Dollar has been the standout performer this week so far. Sterling is also holding up well, with investors eyeing Thursday's BoE rate decision. At the other end of the spectrum, Loonie and Dollar are lagging, but the broader picture remains fluid. Most currency pairs are still trading within familiar ranges, leaving the door open for sudden shifts based on upcoming events.

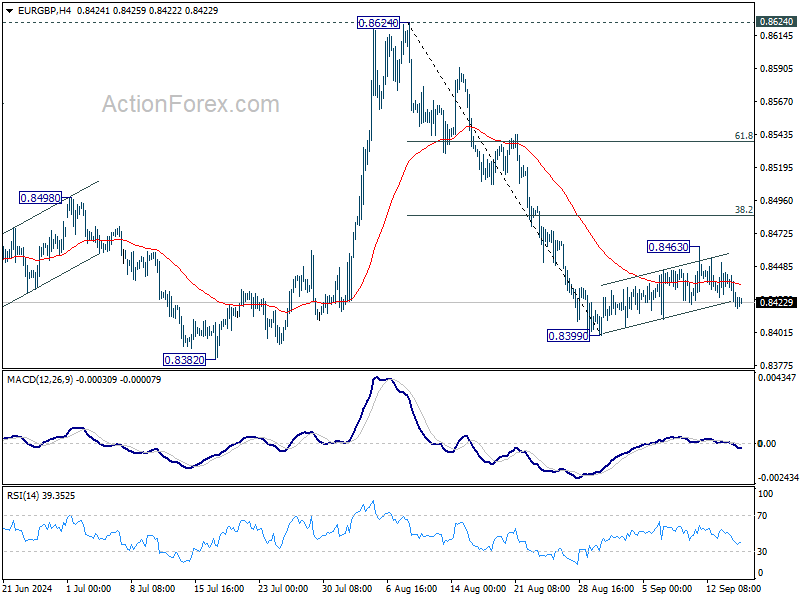

Technically, one of the focuses now is whether EUR/GBP's corrective recovery from 0.8399 has already completed at 0.8463. Break of 0.8399 could prompt downside acceleration through 0.8382 low to resume the medium term down trend. If realized, that could give GBP/USD an extra lift through 1.3265 resistance with upside acceleration.

In Asia, at the time of writing, Nikkei is down -1.82%. Hong Kong HSI is up 1.42%. China Shanghai SSE is down 0.48%. Singapore Strait Times is up 0.55%. Overnight, DOW rose 0.55%. S&P 500 rose 0.13%. NASDAQ fell -0.52%. 10-year yield fell -0.029 to 3.621.

Canadian CPI in focus after as BoC's Macklem signals potential for faster rate cuts

Canadian inflation data is set to take center stage today, particularly after dovish signals from BoC Governor Tiff Macklem hinted at the potential for accelerated monetary easing should the economy weaken further. Progress in disinflation could provide the BoC with more leeway to shift toward a more aggressive policy stance.

Headline CPI is forecasted to decelerate from 2.5% yoy in July to 2.1% yoy in August, edging just above BoC's 2% target. If realized, this would mark the lowest inflation rate since March 2021. While the bulk of the inflation slowdown is attributed to falling gasoline prices, core inflation metrics are expected to reflect improvement too, with the three-month annualized growth rate projected to ease from July's 2.6% yoy.

In a recent Financial Times interview, Macklem voiced growing concerns about the labor market's softening and the impact of lower crude oil prices on the broader economy. He emphasized that as inflation approaches target levels, the "risk management calculus changes," and the focus shifts toward downside risks.

BoC's current forecast anticipates 2% economic growth in 2024 and 2.1% in 2025. However, Macklem acknowledged that if these growth projections falter, "it could be appropriate to move faster [on] interest rates."

Presently, economists expect BoC to cut rates by 25bps at every meeting through mid-2025, bringing the policy rate down to 2.50%. However, weaker economic data could prompt a faster pace of cuts or even a lower terminal rate.

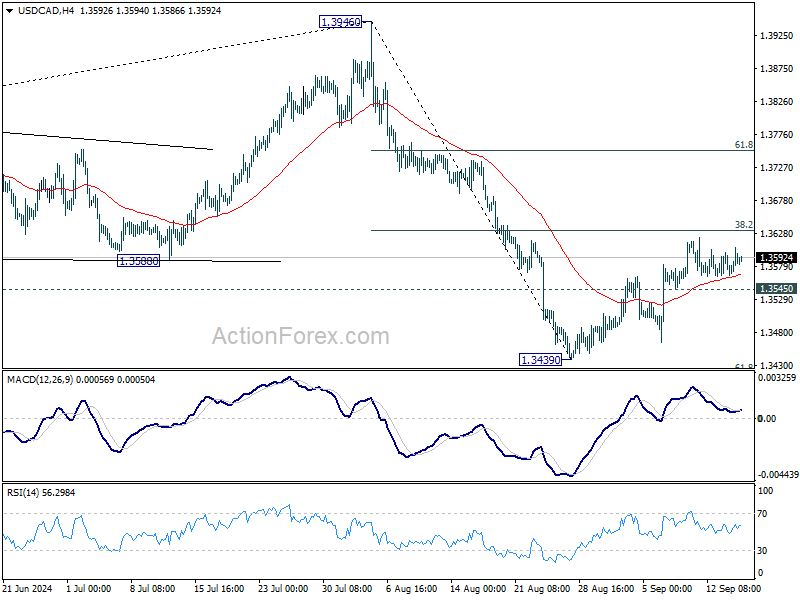

Technically, Canadian Dollar has been sluggish to rally against the greenback even though the latter has been pressured across the board on speculation of a 50bps rate cut by Fed this week. Decisive break of 38.2% retracement of 1.3946 to 1.3439 at 1.3633 in USD/CAD could argue that the decline from 1.3946 has completed. Stronger rally would then be seen to 61.8% retracement at 1.3752 and above.

ECB's Kazaks: Rate cuts not over, could fall to 2.5% by mid-2025

ECB Governing Council member Martins Kazaks indicated that after two rate cuts this year, "this is not the final destination." Borrowing costs remain "pretty restrictive", and "these rates will continue to go down," he added.

Kazaks noted that the speed of these rate cuts will largely depend on the path of services inflation and the broader outlook for Europe's struggling economy.

"If we look at what financial markets expect — and I don't have any serious reason not to agree with them — then by the middle of next year, rates are expected at 2.5%," he added.

Looking ahead

German ZEW economic sentiment is the main focus in European session. Later in the day, Canada will release housing starts and CPI. US will publish retail sales, industrial production, business inventories and NAHB housing index.

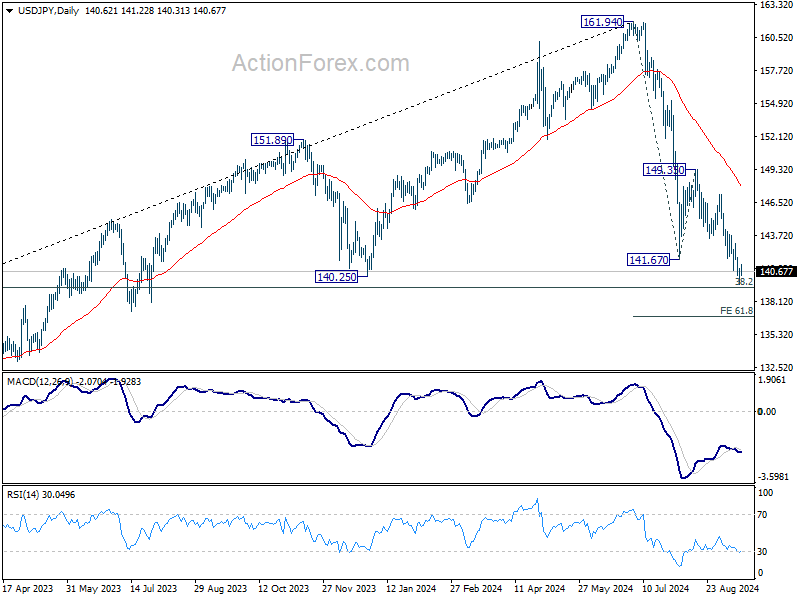

USD/JPY Daily Outlook

Daily Pivots: (S1) 139.82; (P) 140.37; (R1) 141.17; More...

Intraday bias in USD/JPY is turned neutral first as it recovered just ahead of key 139.26 fibonacci level. Considering bullish convergence condition in 4H MACD, break of 143.03 resistance will indicate short term bottoming and turn bias back to the upside for rebound towards 147.20. However, decisive break of 139.26 would carry larger bearish implications, and target 61.8% projection of 161.94 to 141.67 from 149.35 at 136.82.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Strong support could be seen from 38.2% retracement of 102.58 to 161.94 at 139.26 to contain downside, at least on first attempt. But in any case, risk will stay on the downside as long as 149.35 resistance holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Economic Indicators Update

| GMT | CCY | EVENTS | ACT | F/C | PP | REV |

|---|---|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Jul | 1.00% | -1.30% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | 18.6 | 19.2 | ||

| 09:00 | EUR | Germany ZEW Current Situation Sep | -77.3 | |||

| 09:00 | EUR | Germany ZEW Economic Sentiment Sep | 17.6 | 17.9 | ||

| 12:15 | CAD | Housing Starts Y/Y Aug | 246K | 280K | ||

| 12:30 | CAD | CPI M/M Aug | 0.20% | 0.40% | ||

| 12:30 | CAD | CPI Y/Y Aug | 2.20% | 2.50% | ||

| 12:30 | CAD | CPI Median Y/Y Aug | 2.30% | 2.40% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Aug | 2.50% | 2.70% | ||

| 12:30 | CAD | CPI Common Y/Y Aug | 2.20% | 2.20% | ||

| 12:30 | USD | Retail Sales M/M Aug | -0.10% | 1.00% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Aug | 0.20% | 0.40% | ||

| 13:15 | USD | Industrial Production M/M Aug | 0.20% | -0.60% | ||

| 13:15 | USD | Capacity Utilization Aug | 77.90% | 77.80% | ||

| 14:00 | USD | Business Inventories Jul | 0.40% | 0.30% | ||

| 14:00 | USD | NAHB Housing Market Index Sep | 42 | 39 |

Canadian CPI in focus after as BoC’s Macklem signals potential for faster rate cuts

Canadian inflation data is set to take center stage today, particularly after dovish signals from BoC Governor Tiff Macklem hinted at the potential for accelerated monetary easing should the economy weaken further. Progress in disinflation could provide the BoC with more leeway to shift toward a more aggressive policy stance.

Headline CPI is forecasted to decelerate from 2.5% yoy in July to 2.1% yoy in August, edging just above BoC’s 2% target. If realized, this would mark the lowest inflation rate since March 2021. While the bulk of the inflation slowdown is attributed to falling gasoline prices, core inflation metrics are expected to reflect improvement too, with the three-month annualized growth rate projected to ease from July’s 2.6% yoy.

In a recent Financial Times interview, Macklem voiced growing concerns about the labor market's softening and the impact of lower crude oil prices on the broader economy. He emphasized that as inflation approaches target levels, the “risk management calculus changes,” and the focus shifts toward downside risks.

BoC’s current forecast anticipates 2% economic growth in 2024 and 2.1% in 2025. However, Macklem acknowledged that if these growth projections falter, “it could be appropriate to move faster [on] interest rates.”

Presently, economists expect BoC to cut rates by 25bps at every meeting through mid-2025, bringing the policy rate down to 2.50%. However, weaker economic data could prompt a faster pace of cuts or even a lower terminal rate.

Technically, Canadian Dollar has been sluggish to rally against the greenback even though the latter has been pressured across the board on speculation of a 50bps rate cut by Fed this week. Decisive break of 38.2% retracement of 1.3946 to 1.3439 at 1.3633 in USD/CAD could argue that the decline from 1.3946 has completed. Stronger rally would then be seen to 61.8% retracement at 1.3752 and above.

Crude Oil Prices Recovery Begins: Can It Sustain?

Key Highlights

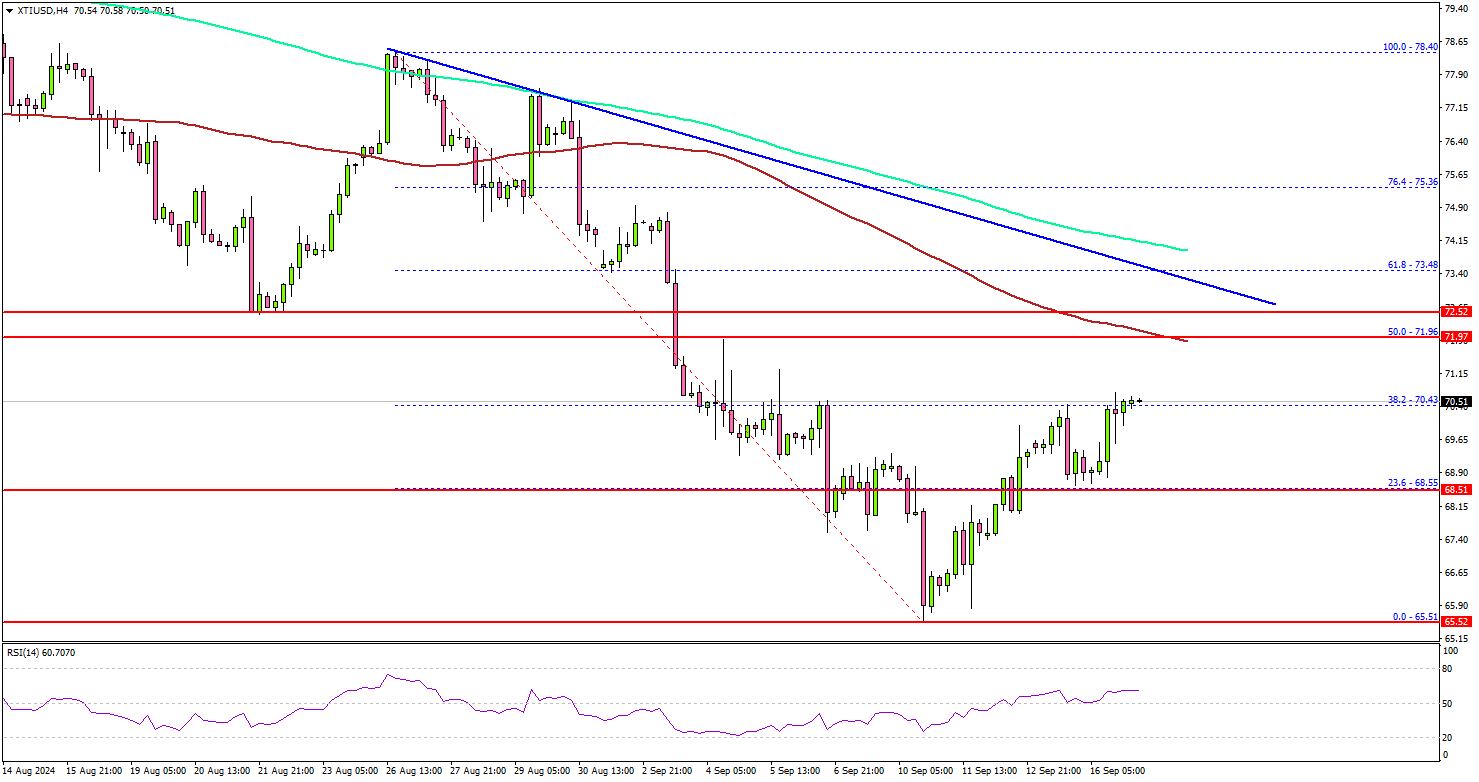

- Crude oil prices started a recovery wave from the $65.50 support.

- A major bearish trend line is forming with resistance at $72.50 on the 4-hour chart.

- Gold consolidated gains after trading to a new all-time high above $2,580.

- EUR/USD regained traction for a move above the 1.1100 level.

Crude Oil Price Technical Analysis

Crude oil prices tested the $65.50 zone before the bulls appeared. The price formed a base and recently started a recovery wave above $67.50.

Looking at the 4-hour chart of XTI/USD, the price was able to clear the $68.50 resistance, but it remained well below the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

There was a test of the 38.2% Fib retracement level of the downward move from the $78.40 swing high to the $65.51 low. On the upside, the price might face resistance near the $70.50 level.

The next major resistance is near the $72.00 zone or the 50% Fib retracement level of the downward move from the $78.40 swing high to the $65.51 low, above which the price may perhaps accelerate higher.

In the stated case, it could even visit the $72.50 resistance. There is also a major bearish trend line forming with resistance at $72.50 on the same chart.

On the downside, the first major support sits near the $68.500 level. A daily close below $68.50 could open the doors for a larger decline. The next major support is $65.50. Any more losses might send oil prices toward $60.00 in the coming sessions.

Looking at Gold, the price is consolidating below the $2,600 level and there are chances of a downside correction toward $2,550.

Economic Releases to Watch Today

- Canadian Consumer Price Index for August 2024 (MoM) – Forecast +0.1%, versus +0.4% previous.

- Canadian Consumer Price Index for August 2024 (YoY) – Forecast +2.4%, versus +2.5% previous.

- US Retail Sales for August 2024 (MoM) – Forecast +0.1%, versus +1.0% previous.