Sample Category Title

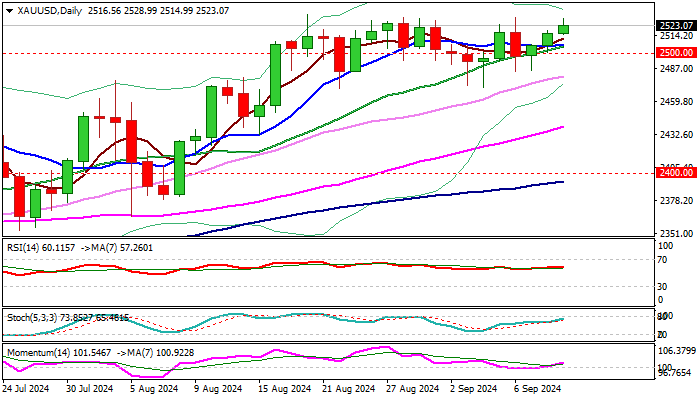

XAU/USD Outlook: Gold Price Nears Record High ahead of US Inflation Data

Gold price rose for the third consecutive day and came ticks ahead of new all-time high in early Wednesday’s trading.

Markets await the release of US August CPI report to complete the picture ahead of Fed policy meeting next week.

If Aug numbers come in line with expectations or better, it will signal that inflation remains in a downward trajectory and heading towards Fed’s 2% target, implying that 25 basis points cut will be likely scenario.

Markets widely expect the Fed to opt for three 0.25% rate cuts by the end of the year, though more aggressive action cannot be completely ruled out, amid recent weaker than expected US economic data which sparked fresh recession fears.

Overall, the yellow metal is expected to remain well supported by expected policy easing, as well as rising geopolitical tensions, which continue to fuel safe-haven demand.

Investors were not impressed by the US Presidential debate and prefer to stick to economic data rather than political promises.

Firmly bullish technical studies on daily chart are expected to contribute to positive outlook.

Although bulls will likely face increased headwinds at record high zone, eventual break above the top of multi-week consolidation range is seen as likely scenario.

Violation of $2431 peak will expose targets at $2554 and $2568 (Fibo projections) and round-figure barrier at $2600, which many analysts see as target for this year.

Near-term action is expected to remain biased higher while the price stays above psychological $2500 support, also the mid-point of the recent $2531/$2470 range.

Res: 2531; 2554; 2568; 2600.

Sup: 2514; 2507; 2500; 2480.

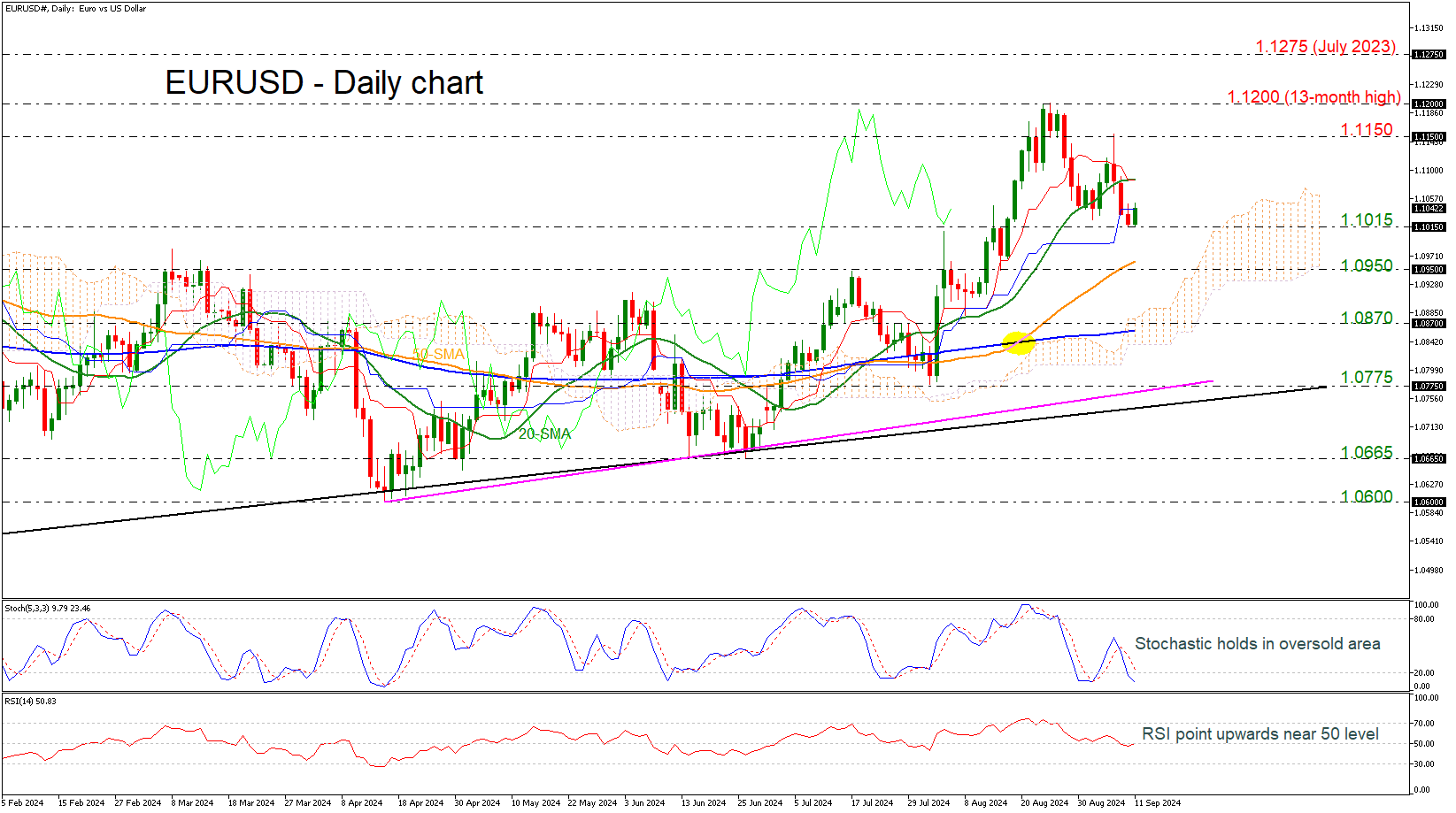

EURUSD Seems to Gave Found a Floor Above 1.1000

- EURUSD is higher again today

- Momentum indicators confirm an upside recovery

EURUSD found some footing around the 1.1015 support level and returned to the upside thereafter. The price failed to penetrate the 1.1000 psychological level where any rally higher may prove valuable to the market. The red Tenkan-sen however remains flat above the blue Kijun-sen and the RSI is currently flirting with the 50 level. Moreover, the stochastic oscillator is trying to tick up in the oversold territory, indicating the end of the bearish correction.

The pair could improve above the 20-day simple moving average (SMA) of 1.1085 to challenge a strong resistance around 1.1150. The 1.1200 area, however, which strictly capped bullish action last month, remains the big highlight.

A pull back may meet immediate support around the 1.1015 barrier, while slightly lower bears could try to overcome the 50-day SMA currently near 1.0965 and the 1.0950 level. Should the price retreat under these areas too, the 1.0870 bar and the 200-day SMA at 1.0860 could come under speculation.

In brief, EURUSD is facing upside pressure above 1.1000, with buyers waiting for a decisive close above 1.1200 to restore optimism over an up-trending market in the medium-term timeframe.

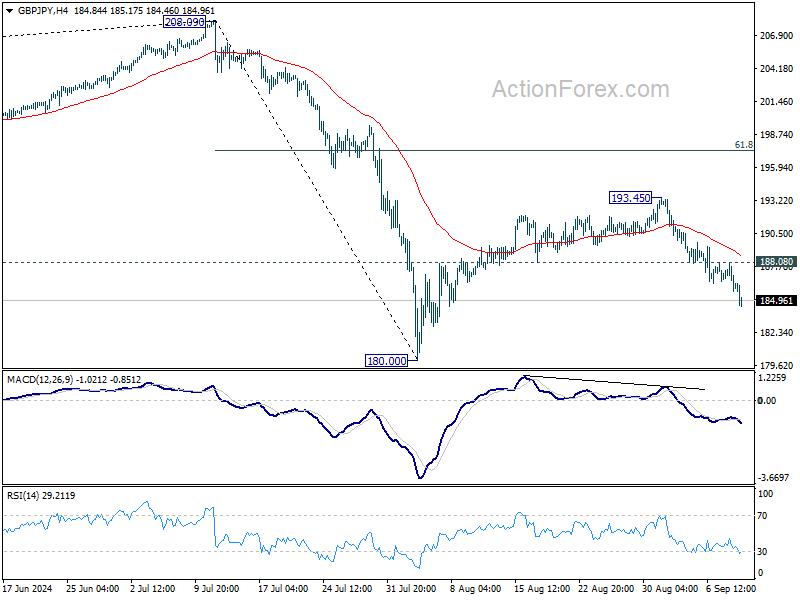

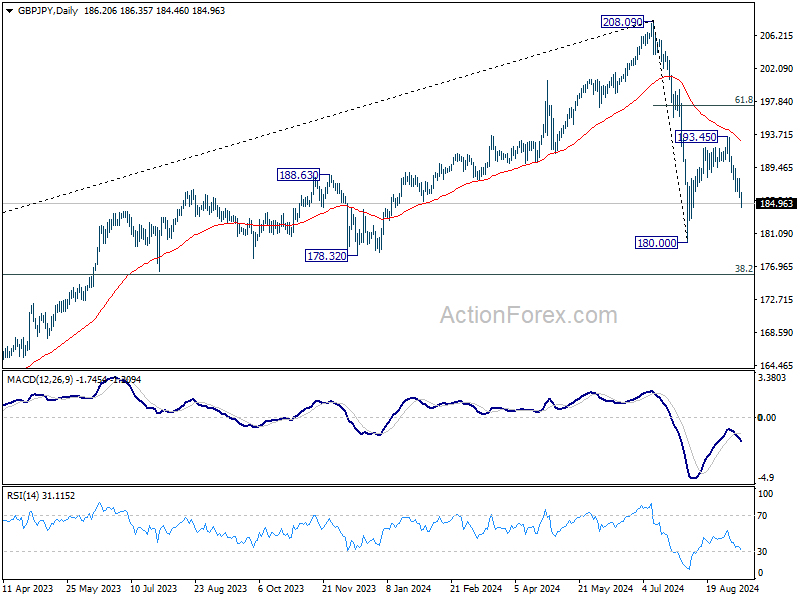

GBP/JPY Daily Outlook

Daily Pivots: (S1) 185.34; (P) 186.72; (R1) 187.71; More...

GBP/JPY's fall from 193.45 extends lower today and intraday bias stays on the downside for retesting 180.00 low. Break there will resume whole fall from 208.09. On the upside, above 188.08 minor resistance will turn intraday bias neutral.

In the bigger picture, price actions from 208.09 are seen as a correction to whole rally from 123.94 (2020 low). The range of consolidation should be set between 38.2% retracement of 123.94 to 208.09 at 175.94 and 208.09. However, decisive break of 175.94 will argue that deeper correction is underway.

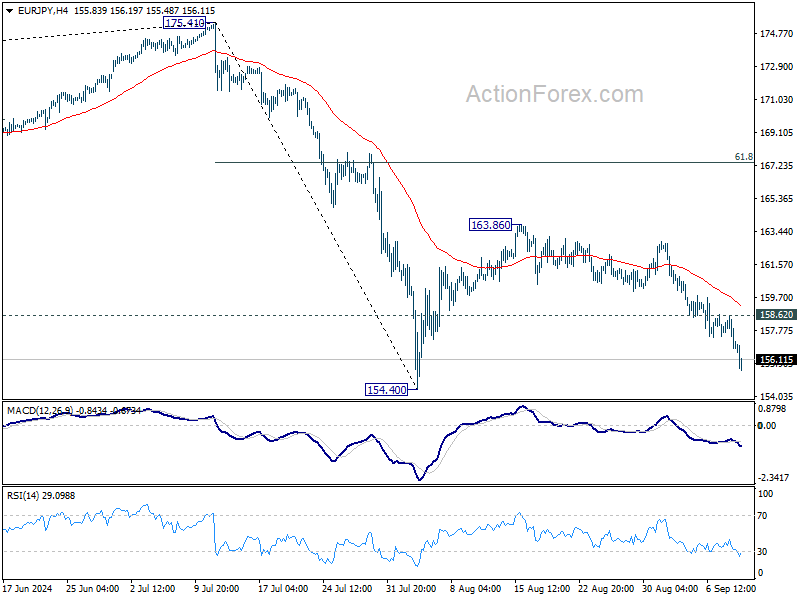

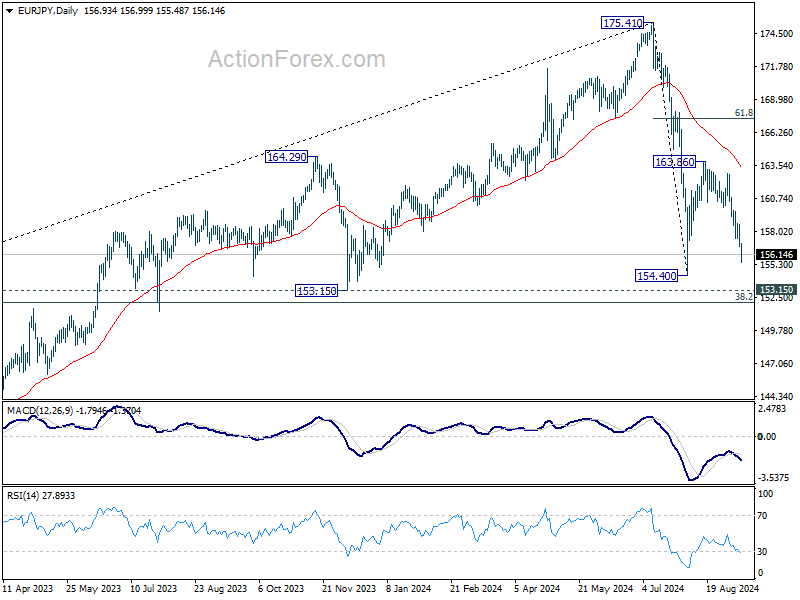

EUR/JPY Daily Outlook

Daily Pivots: (S1) 156.31; (P) 157.47; (R1) 158.15; More....

Intraday bias in EUR/JPY remains on the downside as fall from 163.86 is extending lower. Retest of 154.40 low should be seen first. Firm break there will resume whole decline from 175.41 to 153.15 support. On the upside, above 158.62 minor resistance will turn intraday bias neutral first.

In the bigger picture, price actions from 175.41 are seen as correction to rally from 114.42 (2020 low). The range of consolidation should have been set between 38.2% retracement of 114.42 to 175.41 at 152.11 and 175.41 high. However, decisive break of 152.11 would argue that deeper correction is underway.

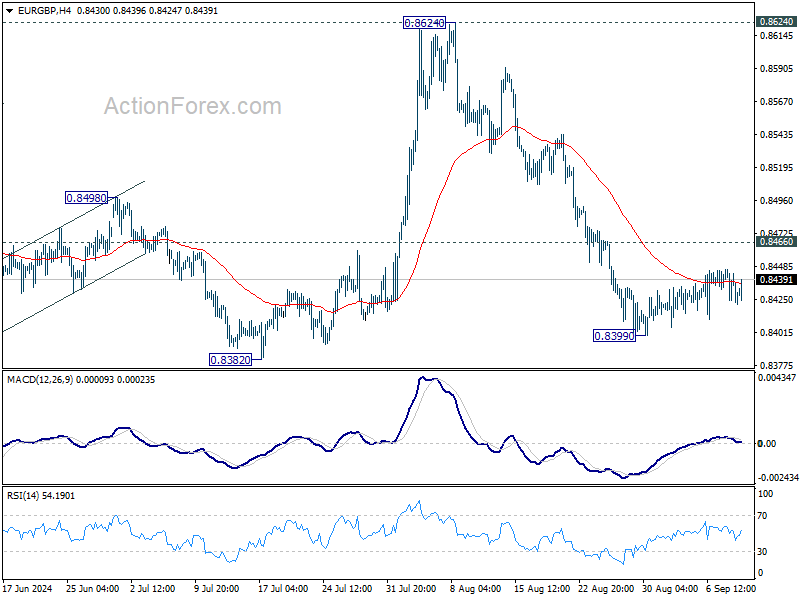

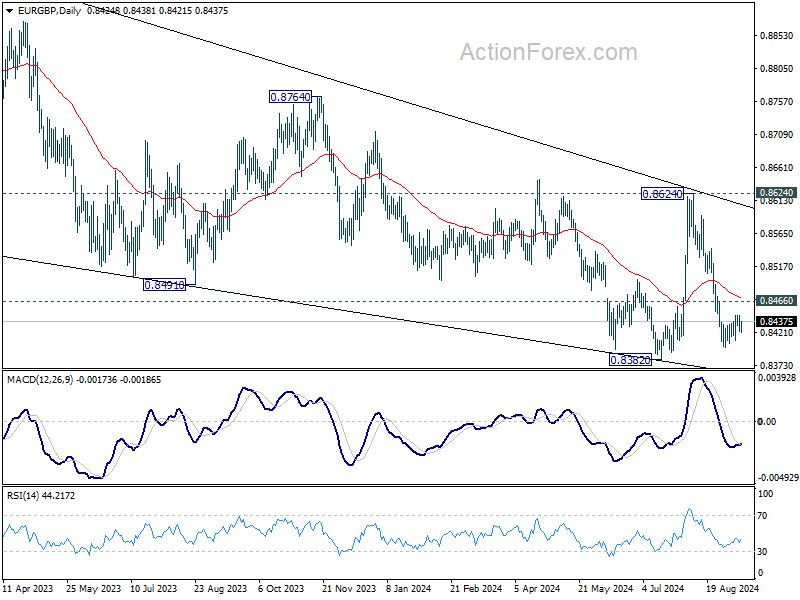

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8417; (P) 0.8432; (R1) 0.8441; More...

No change in EUR/GBP's outlook as consolidation from 0.8399 is still in progress. Intraday bias stays neutral. Further decline is expected with 0.8466 resistance intact. On the downside, below 0.8399 will resume the fall from 0.8624 and target 0.8382 support. Firm break there will resume larger down trend.

In the bigger picture, as long as 0.8624 resistance holds, down trend from 0.9267 is expected to continue. Firm break of 0.8382 will target 0.8201 (2022 low). However, decisive break of 0.8624 will indicate that such down trend has completed, and turn outlook bullish for 0.8764 resistance next.

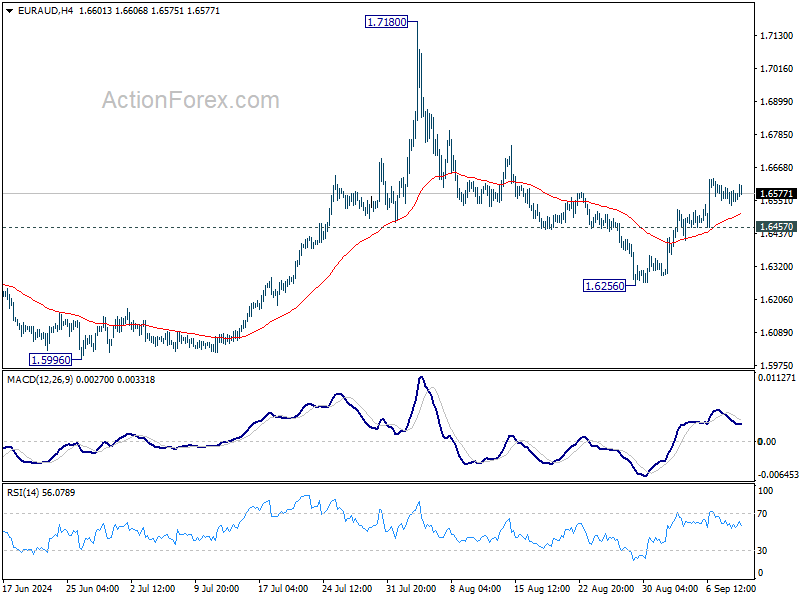

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6536; (P) 1.6568; (R1) 1.6596; More...

Further rally is expected in EUR/AUD with 1.6457 support intact, despite loss of momentum. Rebound from 1.6256 is expected to continue to retest 17180 high. On the downside, however, break of 1.6457 support will turn bias back to the downside for 1.6256 again.

In the bigger picture, outlook is mixed up by the deeper than expected fall from 1.7180. Yet as long as 1.5996 support holds, up trend from 1.4281 (2022 low) is still expected to resume at a later stage. Firm break of 1.7180 will pave the way to 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715.

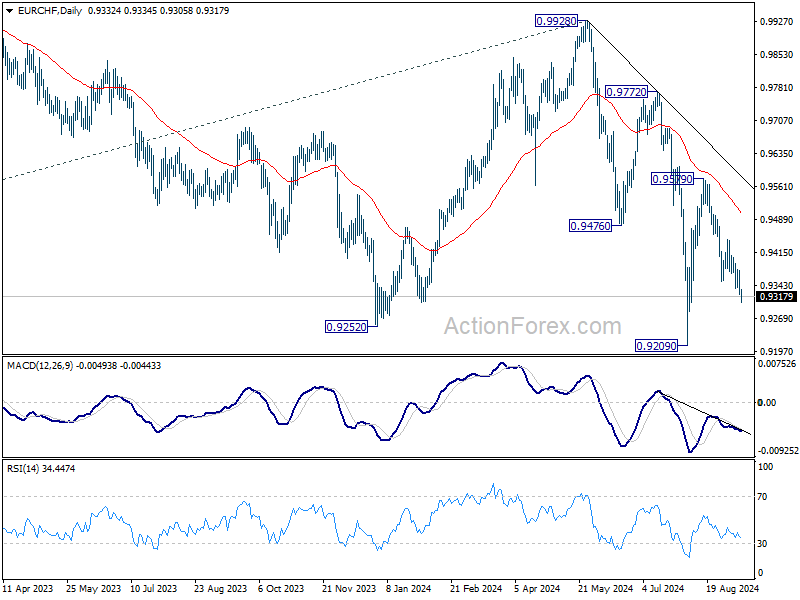

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9312; (P) 0.9346; (R1) 0.9366; More....

EUR/CHF's fall from 0.9579 extends lower today. Intraday bias remains on the downside for retesting 0.9029 low. Firm break there will resume larger down trend. On the upside, above 0.9378 minor resistance will turn intraday bias neutral first.

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

Japanese Yen Taking a Leap This Morning

Markets

Momentum changed yesterday from the US opening as core bonds steamed ahead. The move was triggered by another sudden drop in oil prices. Brent crude prices opened around $72/b, but a break below the recent lows ($70.6 area) accelerated the downleg with an intraday low near $68.5/b. Commodity prices like oil or iron ore keep sending alarms on the global state of the economy. Investors pile up on central bank easing bets, especially in the US, and recession wagers. Bull steepening is the obvious outcome. A very strong $58bn 3-yr Note auction added to the curve move. The auction stopped a significant 1.7 bps below the WI yield with a very aggressive indirect bid and a rising overall auction bid cover (2.66). US yields dropped 3.8 bps (30-yr) to 7.4 bps (2-yr) yesterday. From a technical point of view, the US 2-yr yield arrived at the 2023 low of 3.55%. However, in the current market setting we don’t expect that to play a role. With Fed entering a new phase in its monetary policy cycle, the bottom for the front end of the curve will be defined in first instance by the (market) view on neutral rates (3% area). The US 10-yr yield lost the final support in the 3.66%/3.78%-zone and is now on its way back to the 2023 low of 3.25% which coincides with 38% retracement on the race from 0.31% to 5.02% between 2020 and 2023. US Treasuries continued to outperform German Bunds with German yields ending 2.6 bps (30-yr) to 4.1 bps (5-yr) lower. That makes sense given the approaching ECB meeting and the fact that the Lagarde & co have way less space to make policy less restrictive compared to the Fed. On top, the European inflation outlook doesn’t support the case for rapid or large rate cuts. The dollar’s technical comeback immediately ran into first resistance. Lower oil prices and the loss of interest rate support obviously aren’t helping. The US presidential debate might have added to the move this morning. We argued before that Trump momentum went hand-in-hand with by default USD-momentum as it implied an aggressive trade policy in the disadvantage of the likes of EMU, China,… . Democratic Nominee Harris’ strong performance the debate triggered some reverse action. EUR/USD rebounds towards 1.1044 this morning.

The August US CPI report grabs most attention today. Consensus expects 0.2% M/M price growth for both headline and core inflation resulting in a Y/Y headline CPI drop from 2.9% to 2.5% and a stabilization at 3.2% for the core gauge. We don’t think that inflation data even in case of an upward surprise will be able to alter ruling market momentum. Especially should risk sentiment sour further. A negative surprise will even add to 50 bps rate cuts bets going into next week’s FOMC meeting, our preferred scenario.

News & Views

The Japanese yen is taking a leap this morning. USD/JPY slips towards the 141 lever with a test of the December 2023 low (140.25) increasingly probably. JPY strength dominates the G10 FX landscape following comments from Bank of Japan board member Nakagawa. Having gained a dovish reputation over the years, Nakagawa this time struck a different tone. She said that policy normalization would continue if the outlook for the economy and inflation materializes, echoing comments made by other BoJ members including governor Ueda. Risk number one for Nakagawa is the upside one to inflation with chances that wage growth will deviate from the BoJ scenario due to a tight labour market. Especially her comments about the “extremely low” real rates gained a lot of market attention. They suggest Nakagawa believes there is room for several rate hikes. The central bank meets September 20 but a third hike already then is unlikely after the unexpected July one.

US households’ real, inflation-adjusted, incomes rose in 2023 for the first time since 2019, the Census Bureau’s annual report unveiled yesterday. Household income rose throughout the income distribution with median incomes increasing some 4% to $86 610. The rise reflected a sharp drop in inflation, which eased from an annual 8% in 2022 to 4.1% last year. Despite the increase, median incomes remain some $600 below the pre-pandemic levels. Census also reported that the country’s main gauge of the poverty rate (adjusted for government support including food assistance and tax credits) rose to 12.9%, up from 12.4% in 2022. The official poverty rate dropped to 11.1%, 0.6 ppts above the record low seen in 2019.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June. Stubborn inflation (core, services) make follow-up moves less evident. Markets nevertheless price in two to three more cuts for 2024 as disappointing US and unconvincing EMU activity data rolled in, dragging the long end of the curve down. The move accelerated during the early August market meltdown.

US 10y yield

The Fed in its July meeting paved the way for a first cut in September. It turned attentive to risks to the both sides of its dual mandate as the economy is moving to a better in to balance. The pivot weakened the technical picture in US yields. A string of weak eco data and a risk-off market climate pushed and kept the 10-yr sub 4%. We think we could be up to three 50 bps rate cuts this year.

EUR/USD

EUR/USD moved above the 1.09 resistance area as the dollar lost interest rate support at stealth pace. US recession risks and bets on fast and large rate cuts trumped traditional safe haven flows into USD. EUR/USD 1.1276 (2023 top) serves as next technical references.

EUR/GBP

The BoE delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. Recent better UK activity data and a cautious assessment of BoE’s Bailey at Jackson Hole are pushing EUR/GBP lower in the 0.84/0.086 range.

UK GDP stagnates in Jul with sharp production contraction

The UK economy showed no growth in July, marking a disappointing performance after also stagnating in June. The flat 0.0% mom reading fell short of expectations for 0.2% increase.

Breaking down the numbers, services sector—typically a key driver of UK growth—rose just 0.1% mom in July. Meanwhile, production sector saw a sharp contraction, declining by -0.8% mom. Construction activity also fell by -0.4% mom.

In the three months to July, UK GDP managed to post 0.5% growth compared to the previous three-month period ending in April, largely supported by the services sector, which grew by 0.6%. Construction performed relatively well, with a 1.2% expansion, marking its first positive three-month growth since September 2023. However, production remained weak, contracting by -0.1% over the same period.

Brent Slips Below $70pb – Focus on US CPI

The barrel of US crude tumbled almost 4% to nearly $65pb level, as Brent crude slipped below the $70pb mark after OPEC – which is normally optimistic - lowered its demand forecast for the second time in two months. The API data also showed that the US oil inventories fell by another 2.79 mio barrels last week. As such, US crude has now hit the oversold market conditions, and the rapid selloff suggests that a minor correction would be healthy at the current levels. But the short-term outlook remains comfortably bearish, as the demand worries outweigh the supply side of the story. The price supportive factors like the geopolitical tensions, OPEC’s decision to delay the end of the production restrictions and a hurricane in the Gulf of Mexico go totally unheard. Little need to say that the energy sector had a rough session, yesterday.

Elsewhere, the debate between Trump and Harris went quite well for Harris, which saw her victory odds climbed to 55, and the latter sent Bitcoin 2.50% lower.

Big banks and big tech

Yesterday’s news suggested that US regulators would scale back the increase in capital requirements from 19% to 9%. But news were eclipsed by a conference where the big bank heads gave weak revenue prospects and gloomy outlook. JP Morgan’s CEO said that the $90bn estimate for its net interest income ‘is not very reasonable’ for next year. BoFA said that results for its investment banking will be lower than the Wall Street expectations. Goldman Sach’s CEO said that the bank’s trading revenue will likely drop 10% in the current quarter and Ally Financial warned that ‘credit challenges have intensified’ due to increasing auto loan delinquencies as borrowers faced higher borrowing costs. As a result, JP Morgan saw its share price drop more than 5%, and Invesco’s KBW bank ETF fell 1.83%.

Elsewhere, the European top court told Apple to pay Ireland €13bn in unpaid taxes - putting an end to an eight-year dispute, and Google lost its chance to overturn a €2.4bn fine for abusing its market dominance of its shopping comparison service. Google’s Alphabet didn’t really react to the news – its stock price gained 0.31%, while Apple lost 0.36%, but most of it was probably due to the unimpressive product reveal and insufficient AI promises that the company gave the day before. On the brighter side, Taiwan’s exports rose to a new record of $43.6bn in August thanks to the growing demand for AI chips – and the country’s finance ministry said that the exports should continue to rise steadily in the H2 thanks to robust AI demand. Nvidia advanced some 1.5% yesterday, but TSM gave no reaction to the news. To me, it looked like the continuation of the AI fatigue story.

Overall, the S&P500 still gained 0.45% yesterday, Nasdaq 100 jumped 0.90%, while the Dow Jones index closed with losses due to the bank selloff. The US 2-year yield plunged to 3.56% on rising worries regarding the economic strength and the US dollar gave back most of its advance since Monday. The USDJPY fell to the lowest levels since January as a Bank of Japan (BoJ) member said that the central bank will continue to adjust its degree of easing. Because the expectation is that the BoJ will likely wait until December or January to announce another rate hike, there is room for hawkish readjustment, but the 140 level will likely act as a decent support in the absence of a concrete action.

All eyes on US CPI

Today, all eyes are on the US CPI data. Adobe’s Digital price index printed the biggest drop on record in August for online grocery prices. According to their calculation, the online food prices fell 3.7% in August from a month earlier. Food consumption stands for about 8.6% for of the official inflation measure and is left outside of the core measure, but the decent drop fits the slowing economy and slowing inflation narrative. Combined with the falling oil prices, I would say that the direction for consumer prices looks somewhat clear. In numbers, core inflation - that excludes food and energy prices - is expected to have steadied near the 3.2% level but headline inflation which includes food and energy is expected to have eased from 2.9% to 2.5%. If that’s the case, we will see the headline inflation drop significantly below the 3% level for the first time since last summer. That would be another reason for the Federal Reserve (Fed) to stop worrying about inflation and to worry more about the weakening jobs market. Would that justify a 50bp cut instead of a 25bp cut in September? Hardly. Because announcing a 50bp cut in September would suggest that the Fed accepts to have fallen behind the curve, and they probably want to avoid that.