Sample Category Title

All Eyes on US CPI Today

In focus today

In the US, the August CPI is due, where we forecast headline inflation to ease to 0.1% m/m SA (2.5% y/y), while core inflation is expected to remain steady at 0.2% m/m SA (3.2% y/y). We foresee a gradual moderation in housing and non-housing services inflation following a modest rebound in July, and do not expect a CPI report in line with our forecast to materially change the pricing of Fed cuts.

In the UK, monthly GBP figures will be released, and the Bank of England will be aware of potential inflation risks from strong domestic demand.

In Sweden, Riksbank's Breman speaks about the history of the Swedish economy and the current situation at 17.45 CET at a small-town business community. We do not expect her to send any monetary policy signals on this occasion.

Economic and market news

What happened overnight

In the US, Kalama Harris and Trump had their first presidential debate, where Harris delivered a convincing performance against Trump. While Trump focused on attacking the alleged shortcomings of the current administration, Harris delivered a more forward-looking vision. While Trump's messages lacked clarity on his planned initiatives and key topics such as immigration, Harris stood out especially on her strong views regarding abortion, rule of law and foreign policy towards wars in Ukraine and Gaza. The overall tone on Trump's comments was gloomy and threatening while Harris appeared more optimistic about the future. Leading up to the debate, prediction markets saw odds of both candidates essentially tied (50.5% to 49.5% in favour of Harris) but after the debate Harris is now seen as the clearer favourite (55% to 45%). This was the only presidential debate scheduled for the fall, although Harris' campaign has already called for another one in October.

In Japan, Bank of Japan (BoJ) policymaker Junko Nakagawa stated that the central bank will proceed with its rate hikes if inflation aligns with forecasts, indicating that last month's market turmoil has not altered their plans. This follows comments from policy board member Hajime Takata, who last week emphasized the need to stay on course with rate hikes while treading carefully to avoid volatile markets harming businesses.

What happened yesterday

In the US, The NFIB Small Business Survey fell to 91.2 in August, erasing July's gain of 93.7, driven by concerns over inflation, labour shortages, and weaker sales expectations. Fed Governor Barr, the central bank's regulatory chief, announced a revised "Basel III Endgame" plan, which will now impose a 9% increase in capital requirements for the largest lenders, instead of the 19% rise initially proposed last summer.

In the UK, the July/August labour market report was mixed. Wage growth was lower than expected at 4.0% (cons: 4.1%), while last month's figure was revised up. The less volatile wage measure ex-bonus came in as expected at 5.1%. Similarly, the unemployment rate was also in line with expectations, down to 4.1% from 4.2%, but likely due to noise from the month prior. Employment growth increased in July, while payrolls in August were weaker than expected at -59k. Given the poor data quality of the LFS labour market data, the report should be taken with a pinch of salt as other indicators suggest a loosening labour market. Overall, wage growth remains elevated which is a concern for the Bank of England, keeping the central bank more cautious in this cutting cycle. We expect a cut in November, with pauses in September and December.

In Norway, headline inflation for August came in lower than expected at 2.6% y/y (cons: 2.7% y/y), while core inflation matched expectations at 3.2% y/y. Disregarding the effect of regulated kindergarten max prices, the core reading was 3.5% y/y - higher than expected but still below Norges Bank's 3.6%-projection. The main surprise in core inflation, excluding the kindergarten factor, came from imported inflation, which increased from 1.4% to 2.0%. The rest of the surprise seems to mainly stem from rent, which rose from 4.2% to 4.5%.

In Sweden, July activity data came in weaker than expected, with the GDP indicator at -0.8% m/m SA. However, this should be taken with a grain of salt, as the indicator has been highly erratic. While other data indicate a dip in production, consumption, which makes up some 50% of GDP, surged. Albeit, it must be noted that this is summer data, making the seasonal adjustment a bit uncertain.

On the commodities front, oil prices continued to decline, dropping below USD 70/bbl in yesterday's session amid concerns of oversupply. At the same time, OPEC lowered its global oil demand growth forecast for 2024 and 2025, citing sluggish economic growth, especially in China.

Equities: Global equities were higher yesterday, lifted by the US, tech, and cyclical growth sectors. Conversely, value and defensive groups did not just underperform; they were outright lower. Energy sectors took the hardest hit, with the price of Brent crude oil dropping below 70 dollars per barrel. Banks in both Europe and the US also saw declines, partly due to falling yields and regulatory changes (a Federal Reserve official on Tuesday announced revisions to a set of U.S. banking regulations that would roughly halve the extra capital the largest institutions need). In the US yesterday, the Dow closed down by 0.2%, the S&P 500 was up by 0.5%, the Nasdaq increased by 0.8%, and the Russell 2000 decreased slightly by 0.02%. Asian markets are lower this morning, and the same goes for European and US futures.

FI: Concerns of over-supply of oil sent yields lower driven by the break-evens. The 10y German bund ended 3bp lower at 2.13%. The decline in oil prices has led to a significant repricing of ECB expectations and while the 2024 ECB market pricing has been steady around the 60-65bp, markets continue to add to the 2025 segment and is now pricing 122bp of rate cuts from the ECB, which is a full 25bp rate cut more than just one week ago. Inflation markets are pricing the average HICP ex tobacco at 1.64% through 2025, which is below our expectations.

FX: In a two-split session risk and commodity sensitive currencies ended yesterday as the clear underperformers with notably EUR/NOK rebounding sharply during the US hours. The rally in fixed income benefitted the JPY and despite the USD staying firm USD/JPY still moved back to multi-month lows just above 142.

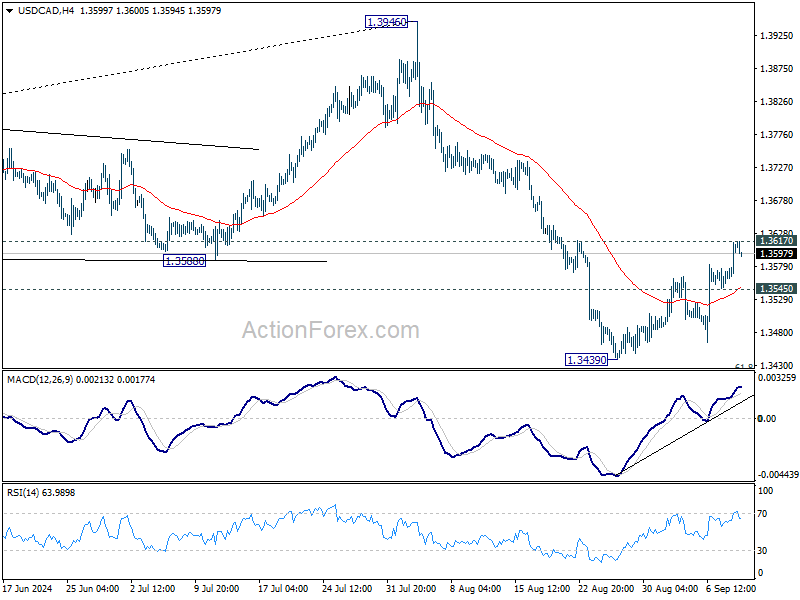

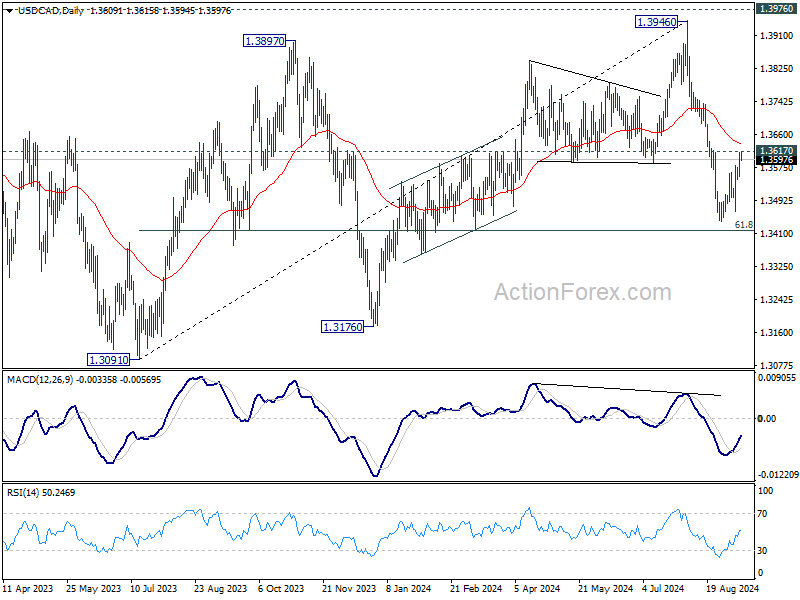

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3570; (P) 1.3593; (R1) 1.3633; More...

USD/CAD's recovery is still limited by 1.3617 resistance and intraday bias remains neutral. Further decline will remain in favor as long as 1.3617 resistance holds. On the downside, below 1.3545 minor support will bring retest of 1.3439 low first. However, firm break of 1.3617 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, current development suggests that corrective pattern from 1.3976 (2022 high) is extending with another falling leg. While deeper decline could be seen, strong support should emerge above 1.2947 resistance turned support to bring rebound. Rise from 1.2005 (2021 low) is still in favor to resume at a later stage.

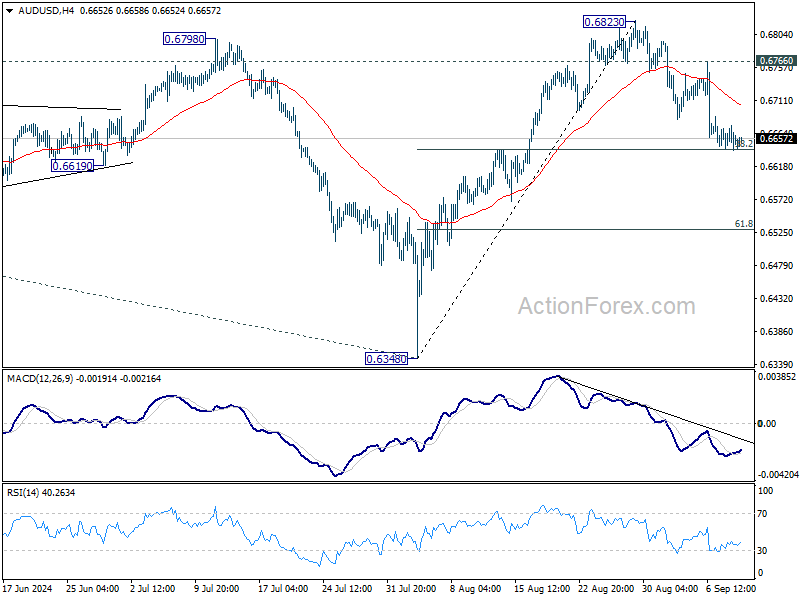

AUD/USD Daily Report

Daily Pivots: (S1) 0.6637; (P) 0.6657; (R1) 0.6673; More...

Intraday bias in AUD/USD remains on the downside for the moment. Decisive break of 38.2% retracement of 0.6348 to 0.6823 at 0.6642 will target 61.8% retracement at 0.6529. On the upside, though, above 0.6766 resistance will bring retest of 0.6823 instead.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with rise from 0.6269 as the third leg. Firm break of 0.6798/6870 resistance zone will target 0.7156 resistance. In case of another fall, strong support should be seen from 0.6169/6361 to bring rebound.

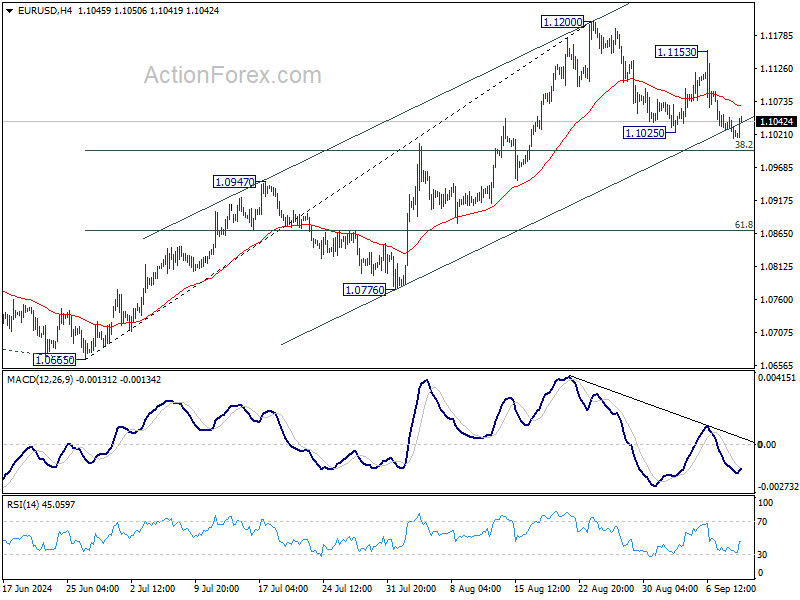

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.1006; (P) 1.1028; (R1) 1.1041; More....

Outlook is EUR/USD is unchanged. While consolidation from 1.1200 could extend lower, downside should be contained by 38.2% retracement of 1.0665 to 1.1200 at 1.0996 to bring rebound. Break of 1.1200 will resume larger rise towards 1.1274 high. However, sustained break of 1.0996 will indicate reversal and turn bias to the downside.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 might have completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

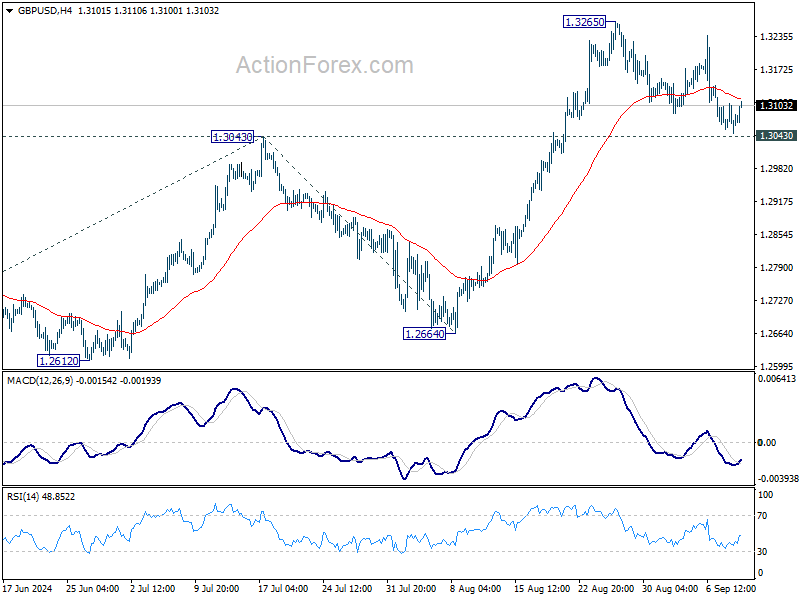

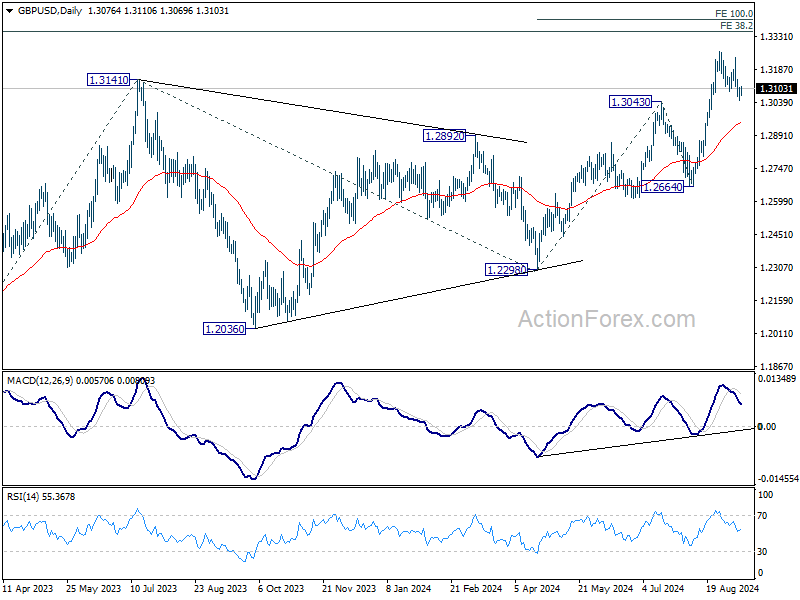

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.3051; (P) 1.3079; (R1) 1.3109; More...

Intraday bias in GBP/USD remains neutral as range trading continues below 1.3265. Further rise is expected with 1.3043 resistance turned support intact. On the upside, firm break of 1.3265 will resume larger up trend to 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409. However, firm break of 1.3043 will turn bias back to the downside for deeper pullback.

In the bigger picture, up trend from 1.0351 (2022 low) is in progress. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

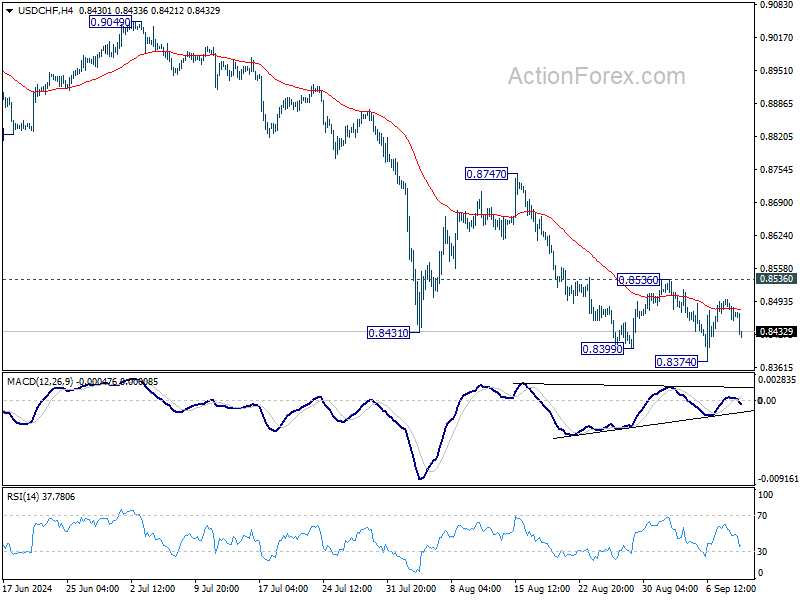

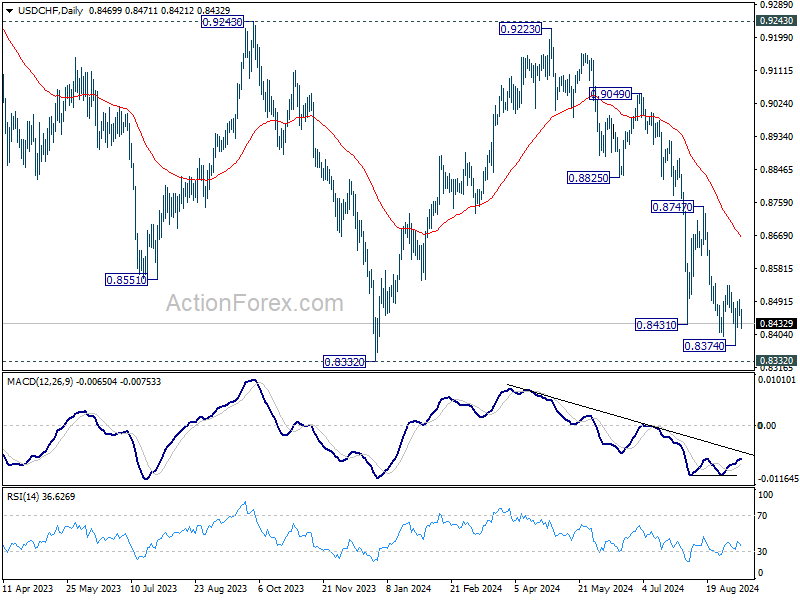

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8450; (P) 0.8476; (R1) 0.8495; More…

Range trading continues in USD/CHF and intraday bias remains neutral. With 0.8356 resistance intact, further decline is expected. On the downside, break of 0.8374 will resume the fall from 0.9223 to retest 0.8332 low. Decisive break there will indicate larger down trend resumption. However, considering bullish convergence condition in 4H MACD, break of 0.8536 resistance will now confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

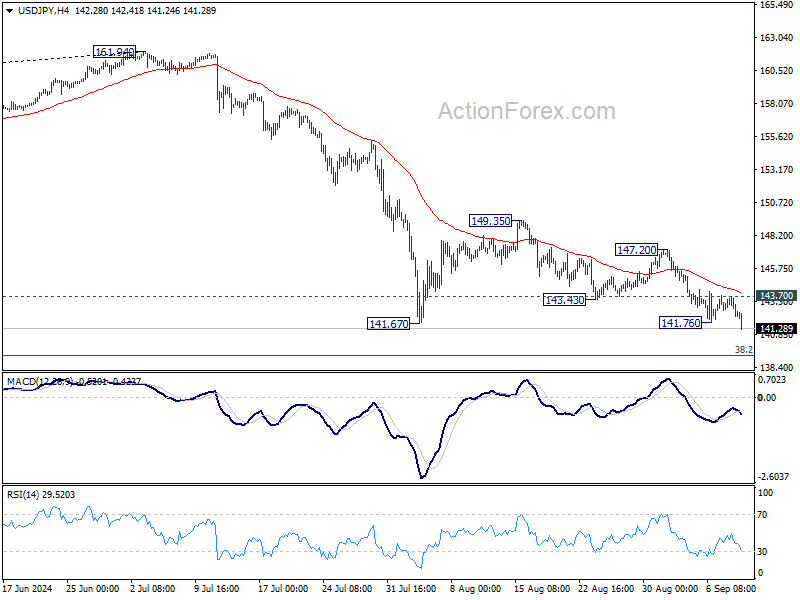

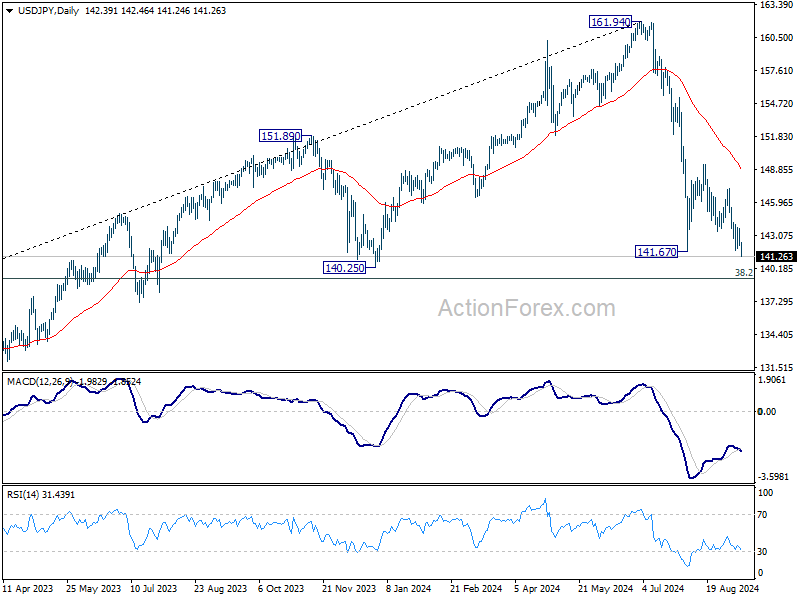

USD/JPY Daily Outlook

Daily Pivots: (S1) 141.86; (P) 142.79; (R1) 143.37; More...

USD's fall from 161.94 resumed by breaking through 141.76 temporary low. Intraday bias is back on the downside for 140.25 support, and possibly further to 139.26 fibonacci level too. On the upside, above 143.70 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 147.20 resistance holds, in case of recovery.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. Strong support could be seen there to bring rebound. But in any case, risk will stay on the downside as long as 55 W EMA (now at 148.93) holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Dollar Weakens as Treasury Yields Slip, Market Awaits US CPI for Clarity on Fed’s Next Move

Dollar softened across the board in today's Asian session, dragged down by extended in US Treasury yields. Investors appear to be setting aside the first presidential debate between Kamala Harris and Donald Trump, focusing instead on the highly anticipated US CPI report, which might hopefully provide clearer direction on Fed's upcoming interest rate cut.

Market expectations suggest that headline CPI will ease from 2.9% to 2.6% in August. However, core CPI, which excludes volatile food and energy prices, is forecast to remain unchanged at 3.2%. This would indicate that disinflationary momentum may be losing steam again, with services and shelter costs keeping core inflation elevated.

A downside surprise in today's report could shift the odds toward a larger 50bps rate cut by the Fed at next week's meeting. But the market reaction could be complicated: a significant undershoot in inflation could, at the same time, signal weakening demand, raising concerns about a broader economic slowdown.

As of now, futures markets are pricing in a 33% chance of a 50bps rate cut, with the majority (67%) betting on a smaller 25bps cut. Looking further ahead, markets are already pricing in a total of 75bps in cuts by year-end, with 90% chance of 100bps in reductions and 53% chance of 125bps.

In terms of market performance, Yen is the standout performer so far this week, buoyed by the drop in Treasury yields. Dollar and Swiss Franc follow closely behind. Euro is the weakest, with New Zealand Dollar and British Pound also underperforming, while Australian and Canadian Dollars are trading in the middle of the pack.

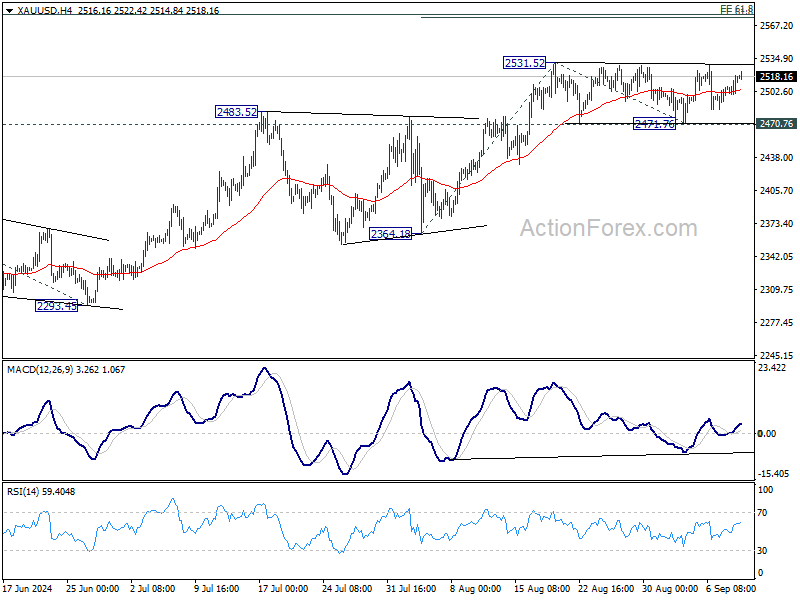

Technically, Gold will be monitored for confirming Dollar's next move in reaction to US CPI release. Consolidation from 2531.52 is still extending for now, but outlook remains bullish as long as 2470.76 support holds. Decisive break of 2531.52 will confirm larger up trend resumption. Next target will be 61.8% projection of 2364.18 to 2531.52 from 2471.76 at 2575.17.

In Asia, at the time of writing, Nikkei is down -0.81%. Hong Kong HSI is down -1.41%. China Shanghai SSE is down -0.86%. Singapore Strait Times is up 0.44%. Japan 10-year JGB yield is down -0.030 at 0.865. Overnight, DOW fell -0.23%. S&P 500 rose 0.45%. NASDAQ rose 0.84%. 10-year yield fell -0.51 to 3.646.

RBA's Hunter anticipates slow cooling of Australia's labor market

In a speech today, RBA Assistant Governor Sarah Hunter highlighted that while conditions in the Australian labor market have eased since late 2022, the market remains "tight relative to full employment."

Looking ahead, Hunter expects labor demand to slow in comparison to labor supply, which should bring the market "into better balance" over the coming quarters. She noted that part of this adjustment is likely to come through a "decline in average hours" worked rather than sharp cuts to overall employment.

Employment growth is expected to persist but at a slower pace, lagging behind population growth. As a result, underutilization measures, including the unemployment rate, are projected to "continue rising gradually." This rise is expected to stabilize once GDP growth returns to a level more consistent with Australia's underlying economic trend.

Hunter's comments underscore RBA's outlook on the labor market, and the hawkish stance that it's not nearing the start of rates reduction cycle yet.

BoJ's Nakagawa signals more rate hikes if economic outlook met

In a speech today, BoJ board member Junko Nakagawa indicated that the central bank will raise interest rates further if the economic outlook aligns with their forecasts. Nevertheless, she also emphasized the need to carefully consider how such moves might impact the broader economy and price stability.

"Given real interest rates are currently very low, we will adjust the degree of monetary support, from the standpoint of sustainably and stably achieving our 2% inflation target, if our economic and price forecasts are met," she noted.

Nakagawa acknowledged Japan's tight labor market and rising import prices as upside risks to the inflation outlook. While affirming that Japan's economic fundamentals remain strong, she highlighted the importance to "look back upon market developments" following July's rate hike before making any further rate adjustments.

Looking ahead

UK GDP and production are the main highlight in European session. Later in the day, US CPI will be the main event.

USD/JPY Daily Outlook

Daily Pivots: (S1) 141.86; (P) 142.79; (R1) 143.37; More...

USD's fall from 161.94 resumed by breaking through 141.76 temporary low. Intraday bias is back on the downside for 140.25 support, and possibly further to 139.26 fibonacci level too. On the upside, above 143.70 minor resistance will turn intraday bias neutral first. But outlook will stay bearish as long as 147.20 resistance holds, in case of recovery.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. Strong support could be seen there to bring rebound. But in any case, risk will stay on the downside as long as 55 W EMA (now at 148.93) holds. Sustained break of 139.26 would open up deeper medium term decline to 61.8% retracement at 125.25.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 06:00 | GBP | GDP M/M Jul | 0.20% | 0.00% | ||

| 06:00 | GBP | Industrial Production M/M Jul | 0.30% | 0.80% | ||

| 06:00 | GBP | Industrial Production Y/Y Jul | -0.20% | -1.40% | ||

| 06:00 | GBP | Manufacturing Production M/M Jul | 0.20% | 1.10% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Jul | -0.10% | -1.50% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Jul | -18.0B | -18.9B | ||

| 12:30 | USD | CPI M/M Aug | 0.20% | 0.20% | ||

| 12:30 | USD | CPI Y/Y Aug | 2.60% | 2.90% | ||

| 12:30 | USD | CPI Core M/M Aug | 0.20% | 0.20% | ||

| 12:30 | USD | CPI Core Y/Y Aug | 3.20% | 3.20% | ||

| 14:30 | USD | Crude Oil Inventories | 0.9M | -6.9M |

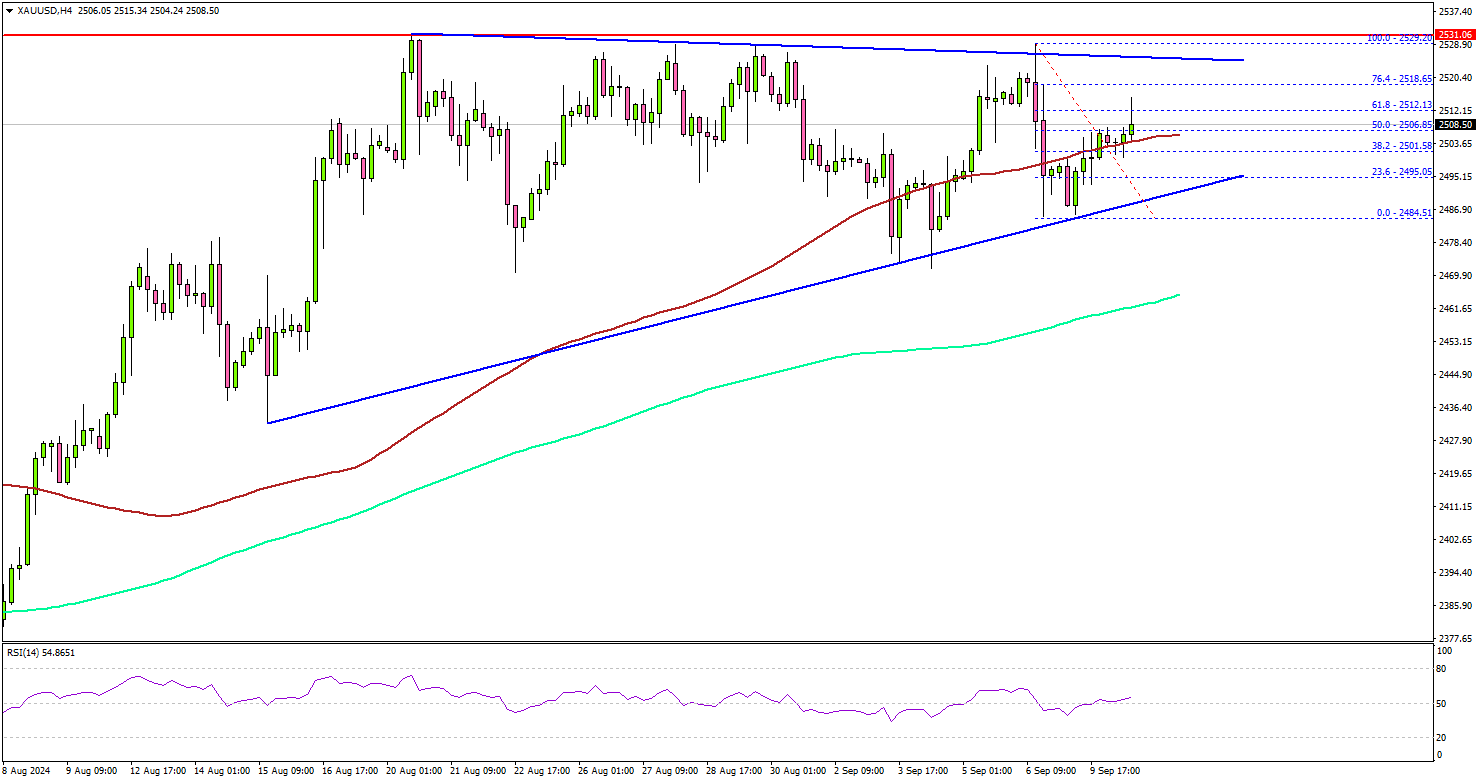

Gold Awaits US CPI Report, $2,530 Presents Resistance

Key Highlights

- Gold is consolidating gains below the $2,530 resistance.

- A key contracting triangle is forming with support at $2,495 on the 4-hour chart.

- Oil prices might extend losses and revisit the $65.00 support.

- The US Consumer Price Index might increase by 2.6% in August 2024 (YoY), down from 2.9%.

Gold Price Technical Analysis

Gold prices started a consolidation phase below $2,530 against the US Dollar. The price stayed above the $2,480 zone but struggled to start a fresh increase.

The 4-hour chart of XAU/USD indicates that the price remained stable above the 100 Simple Moving Average (red, 4 hours) and the 200 Simple Moving Average (green, 4 hours). Recently, there was an upward move within a range and the price climbed above $2,500.

However, the bears remained active below the $2,520 and $2,530 resistance levels. There is also a key contracting triangle forming with support at $2,495 on the same chart.

The main support is now near $2,480. A downside break below the $2,480 support might call for more downsides. The next major support is near the $2,465 level and the 200 Simple Moving Average (green, 4 hours).

Any more losses might send gold prices toward $2,420. On the upside, immediate resistance is near the $2,520 level. The first major resistance sits near the $2,530 level.

A clear move above the $2,530 resistance could open the doors for more upsides. The next major resistance could be near $2,550, above which the price could rally toward the $2,565 level. Any more gains might send Gold toward the $2,580 resistance.

Looking at Oil, the price extended losses below the $68.50 level and there are chances of more downsides in the near term.

Economic Releases to Watch Today

- US Consumer Price Index for August 2024 (MoM) – Forecast +0.2%, versus +0.2% previous.

- US Consumer Price Index for August 2024 (YoY) – Forecast +2.6%, versus +2.9% previous.

- US CPI Ex Food & Energy for August 2024 (YoY) – Forecast +3.2%, versus +3.2% previous.

BoJ’s Nakagawa signals more rate hikes if economic outlook met

In a speech today, BoJ board member Junko Nakagawa indicated that the central bank will raise interest rates further if the economic outlook aligns with their forecasts. Nevertheless, she also emphasized the need to carefully consider how such moves might impact the broader economy and price stability.

"Given real interest rates are currently very low, we will adjust the degree of monetary support, from the standpoint of sustainably and stably achieving our 2% inflation target, if our economic and price forecasts are met," she noted.

Nakagawa acknowledged Japan's tight labor market and rising import prices as upside risks to the inflation outlook. While affirming that Japan’s economic fundamentals remain strong, she highlighted the importance to "look back upon market developments"" following July's rate hike before making any further rate adjustments.