Sample Category Title

BoC Rate Decision: Third Rate Cut on the Way

- BoC could easily cut interest rates for the third time on Wednesday

- Macro data favors additional easing but will it be a continuous process?

- USDCAD needs a close above 1.3585 to gain fresh bullish momentum

The easing cycle has more room to go

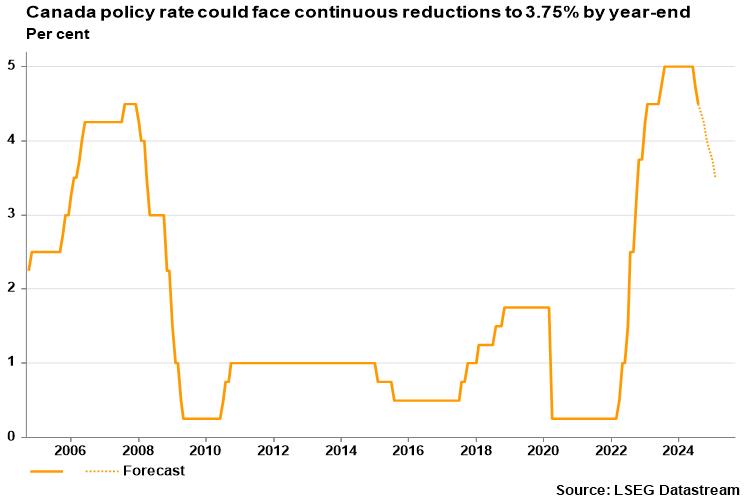

The Bank of Canada (BoC) is in the front of the global easing cycle. Having cut interest rates twice in a row, the central bank is widely expected to announce its third reduction on Wednesday at 13:45 GMT, but it won’t stop there. It is anticipated that interest rates will decline to 3.75% by the end of the year, based on the futures markets. The bank's board is expected to approve two additional 25 bps cuts in October and December, and potentially more in early 2025.

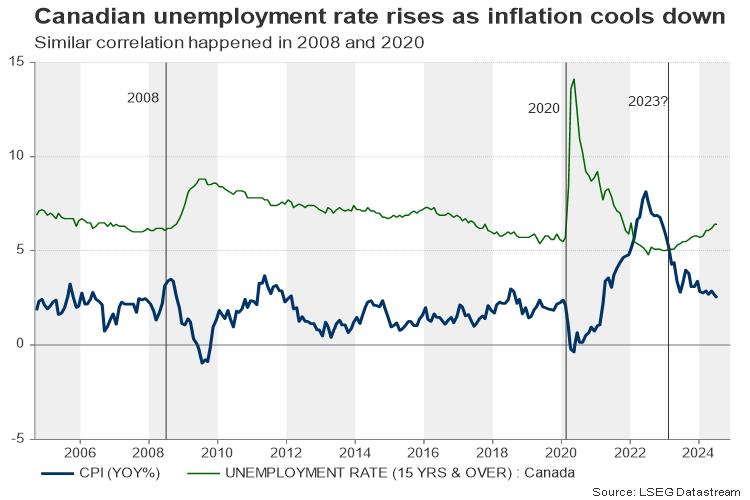

The question that comes instantly to mind is whether the current market pricing is realistic. Driven by base effects, inflation continued to trend down and towards the central bank’s 2.0% midpoint target, with headline CPI inflation falling to 2.5% y/y and the core measure easing to 2.6% in July. Of course, shelter costs remained elevated, but there was a slowdown from the previous month.

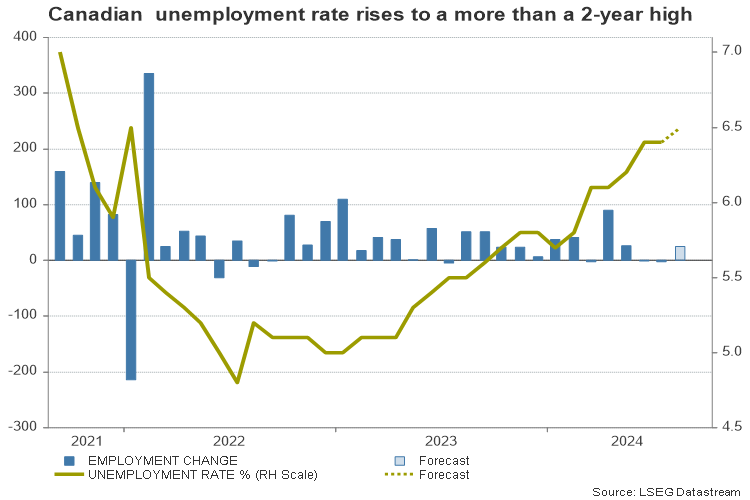

With the battle against inflation looking almost settled, the focus has started to shift to the labor market and to economic growth as interest rates are still hovering at multi-year highs despite easing lately. The unemployment rate has been steadily rising over the past year before stabilizing at a more-than-a-year high of 6.4% and is expected to tick up to 6.5% on Friday when the next employment report is published.

As regards economic growth, GDP rose at a faster-than-expected annualized rate of 2.1% in the second quarter. While the data was encouraging, the details showed that the expansion was driven by factors that could prove transient such as government spending and business investment on engineering structures in oil and gas facilities. Spending on services increased as well but the rise was trimmed by declines in goods consumption, net trade, and residential structure, while growing population squeezed per capita household expenditure to the negative region. Moreover, the monthly GDP readings for July displayed stagnation at the start of the third quarter.

Will the BoC send any strong signals?

Hence, the latest economic developments could justify further monetary easing as Canada is more sensitive to global trade and housing risks than the US. Still, whether there is a need for more aggressive rate cuts, or a continuous easing process remains to be seen. There will be no policy statement or updated economic projections following the rate decision, which reduces the odds for a serious shift in communication.

The certain thing is that messaging such an aggressive dovish strategy or delivering an unexpected 50bps rate cut could sow panic, signaling that things are going out of the central bank’s control. Note that futures markets are currently pricing a small probability of 23% for a double rate cut. Therefore, if that scenario unfolds, the loonie could drift significantly lower, lifting USDCAD above 1.3585 and beyond the 200-day simple moving average (SMA). The 1.3700 number could be the next target on the upside.

If the BoC slashes interest rates as expected but plays down the case of consecutive or double rate cuts, investors might take it as a hawkish signal, helping the loonie to resume its positive momentum. USDCAD might drift back towards the 1.3440 support zone in the aftermath of such a scenario. Failure to pivot there could bolster downside forces towards 1.3300-1.3350.

Perhaps volatility could stay relatively balanced if the policy meeting is uneventful and investors wait for fresh direction from Friday’s jobs report. A worse-than-expected employment report could keep the case of a double rate cut alive in the coming months, putting some pressure on the loonie. Strong numbers on the other hand could help the currency to strengthen. Analysts estimate a positive employment growth of 25.6k versus -2.8k in July and a slight pickup in the unemployment rate from 6.4% to 6.5%.

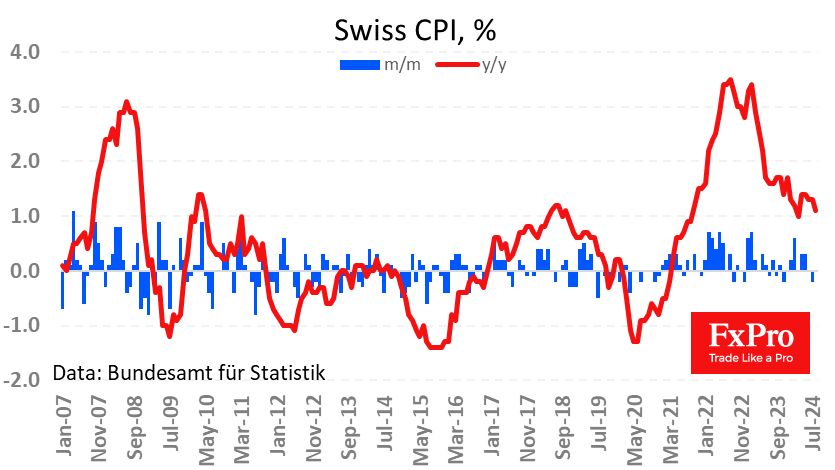

Weak Swiss Inflation Paves the Way for Further Rate Cuts

Swiss inflation slowed to 1.1% y/y in August from 1.3% the previous month, below the 1.2% expected. In April and May, the rate of price increases rose to 1.4% y/y but later started to fall again, losing 0.2% in the last three months.

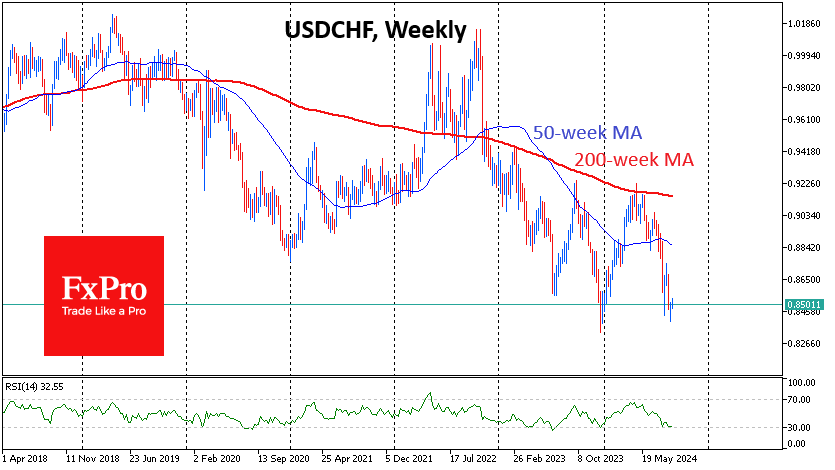

The Swiss National Bank cut its key interest rate twice, in March and June. However, the combination of a further slowdown in price growth and an appreciating CHF opens the door for further monetary easing.

USD/CHF is back below 0.8500, its lows at the beginning of the year. The pair plunged into this area then, as it has now, on the back of rising expectations of a Fed rate cut. At the same time, earlier policy easing in Switzerland did not significantly weaken the franc.

The strength of the franc, which only fell below its current level in 2011, could encourage the monetary authorities to take more aggressive steps to curb the growth of the national currency, including warnings or actual currency intervention.

Too strong a franc hurts the economy by making exports less competitive, which could be a problem for Switzerland’s open economy.

ISM Rises for the Wrong Reasons in August

Summary

A headline increase to 47.2 for the ISM manufacturing index says more about a back-up in inventories than it does about a meaningful improvement for the factory sector. Excluding the inventory contribution, the index would have been down 0.8 points.

Rise & Whine: More of the Same from August ISM

This is not the sort of improvement you want to see if you are rooting for a turnaround in the factory sector. Only two of the five components that feed into the headline rose in August. Employment (up 2.6 to 46.0) and inventories, which rose twice as much (+5.8 points to 50.3). Production, supplier deliveries and new orders were all lower. The most disconcerting development is the 2.8 point drop in new orders, which took this leading indicator to its lowest since May of last year.

While a sub-50 print may indicate a discouraging backdrop for the factory sector, it takes an even lower reading to signal outright recession for the broader economy; 42.5 in fact, according to the ISM. So today's report for August activity is broadly consistent with a theme that has been in place for the better part of the past two years: the economy is still expanding even if the factory sector is not.

Our way of describing this dichotomy has been that the combination of pulled-forward demand for durable goods during the pandemic and higher financing costs has meant that Fed rate hikes have bitten harder in this sector than most others. Both of these dynamics are transitioning in a way that we expect to eventually be favorable for the sector. Even long-lived durable goods need replacing and items purchased during the early days of the pandemic are now four-and-a-half years old and rates are apt to start coming down, perhaps as soon as later this month. But for August, it was more of the same for manufacturing.

In general manufacturing activity remains constrained. The new orders component slid nearly three points to the lowest reading since May of last year, and the only of the six largest industries to report an increase in new orders was the computer & electronic products—which has been a notable bright spot in an otherwise flagging sector. The measure of current production also slid deeper into contraction last month.

As mentioned, most of the strength came from inventories. While inventories can be volatile, it's the first time this component crested above 50 since early 2024 and the release notes manufacturers adjusting to lower output levels and timing issues. In other words, this inventory was unintended and a consequence of slowing demand. Without the inventory build, the overall ISM composite index would have seen a decline twice as large in August.

Slower activity continues to hold back hiring. We often look to the ISM surveys for a hint of what to expect from the coming employment report, and although the ISM's have been more volatile than broader hiring figures, the signal has been clearly one of lost momentum. While employment was less negative in August, it was still consistent with a broad contraction in hiring in August. Only three of 18 industries reported employment growth in August according to the release, and one of them (food & beverage) was said to do so due to seasonal reasons. The employment component has only been above 50, or consistent with an expansion in hiring, for just one month of the year.

The main event this week comes with Friday's employment report. We forecast a partial rebound in hiring and reversal of the unemployment rate from July's increase. With the labor market now largely having normalized from its pandemic-related distortions the only question that remains is by how much will the Fed cut rates in two weeks at its September meeting. Recent public comments of Fed officials indicate few currently see the need for a 50 bps reduction, and we expect Friday's jobs report will likely need to come in weaker than July for such a large rate reduction to kick off the Fed easing cycle.

US: Manufacturing Index Shows Contraction Extends into August

The ISM Manufacturing Index marginally improved in August, rising to 47.2 and just short of expectations of a 47.5 print. As in July, only five industries reported growth for the month, but as some larger industries grew, a smaller share of manufacturing GDP shrank relative to last month (65% vs. 86% in July).

Demand continued to slow as the new orders index fell to 44.6, new export orders remained in contraction, and backlogs continued to shrink.

Output conditions remain subdued, as both the employment and production indexes remain in contraction, despite a slight uptick in the former.

Price pressures picked up again last month, with the index rising to 54.0, now well above the 52.8 reading that is typically associated with an increase in the Producer Price Index for Intermediate Materials.

Key Implications

The takeaway here is that the challenging conditions persist for the manufacturing sector. New demand continues to contract, and weakness remains broad based.

Despite the softness in the report there are reasons for optimism. The Fed is set to begin cutting interest rates, a key impediment to the sector's growth prospects. For manufacturers, the light at the end of the tunnel is starting to emerge, but with the pace of cuts likely to be gradual, the recovery will likely proceed in fits and starts.

Sunset Market Commentary

Markets

Returning after a long weekend due to the Labour Day holiday, US investors see the glass half empty rather than half full looking forward to key US eco data to be published today (ISM manufacturing ISM) and later this week (Jolts openings tomorrow, ADP, jobless claims and services ISM on Thursday and payrolls on Friday). After a positive close yesterday, the EuroStoxx 50 eases 0.50%. The S&P 500 also ceded 0.7% at the open. Major US indices are nearing resistance of all-time top levels. If markets are currently priced for a ‘perfect’ soft landing; maybe both much better than expected data (and higher yields) as well as really negative surprises (recession fears, cfr early last month) might trigger volatility. A further decline in the oil prices also suggests lingering uncertainty on global (including Chinese) demand. Brent oil is touching a new YTD low near $ 74.6 p/b. After trading little changed this morning in Europa, the risk-off repositioning pushed EMU and US yields of a cliff this afternoon. US yields are falling between 3.5 bps (2-y) and -6.2 bps (30-y). Similar story for Bund yields (2-y -5 bps , 30-y -8.4 bps). Even so, we think the downside in ST EMU yields is still rather well protected. Last week’s sticky underlying inflation metrices and financial newswires reporting an on internal debate within the ECB on the neutral policy rate level for this easing cycle, currently makes investors cautious to fully discount additional 25 bps steps at the three remain meeting this year. In FX, the dollar doesn’t profit from the risk-off. DXY trades gains little changed. The euro also still looks vulnerable among the majors (EUR/USD 1.1055). The yen outperforms. The risk-off, a decline in core yields and the BOJ governor Ueda reconfirming the BOJs intention to raise interest rate further if the economy develops as expected, all further supported the yen (USD/JPY 145.55 from 146.9, EUR/JPY 161 from 162.65). Smaller, especially commodity related currencies (CAD, AUD, NZD, NOK) are fighting an uphill battle.

At the time of finishing this report, the US manufacturing ISM is holding most of last month’s decline (47.2 from 46.8). Details are mixed with orders declining further (44.6 from 47.4), but prices paid (54.0 from 52.9) rising. The decline in employment slows (46 from 43.4). In a first reaction, the risk-off repositioning continues.

An important reality check the UK Gilts market as DMO launched a new 2040 bond. Despite recent negative headlines on the state of UK public finances, the sale attracted a big orderbook of over £110 bln for a deal size of £8 bln. UK(LT) gilts today are trading more or less in line with their German counterparts. Sterling initially captured a better bid, but the unfolding risk-off sentiment prevent a new test of the 0.84 support area (currently 0.842).

News & Views

Swiss CPI remained unchanged in August compared to July. Inflation was 1.1% higher compared with August of last year (from 1.3% in July). Both were slightly lower than expected. Details showed higher prices for housing rentals and for clothing and footwear offsetting lower prices for transport, heating oil and international package holidays. Goods and services inflation were both flat on a monthly basis as well with goods prices 0.7% lower Y/Y and services prices 2.2% higher. Core inflation rose by 0.1% M/M to stabilize in Y/Y-terms at 1.1%. An upward revision to Swiss Q2 GDP data showed the economy growing by 0.7% Q/Q instead of 0.5% Q/Q (1.8% Y/Y from 1.5% Y/Y). Adjusted for sporting events, the first indication (0.5% Q/Q) was confirmed. Strong expansions in the chemical and pharmaceutical industry on the back of dynamic exports stood out. An expenditure breakdown pointed at below average private (+0.3%) and government (+0.2%) consumption and mixed investments. Net exports were again the key driver. The Swiss franc is slightly stronger after the data (EUR/CHF 0.94). The benign inflation outlook and stalling domestic demand cement the case for another September rate cut (discounted). Little maneuvering room from the SNB suggests by default CHF-strength as global monetary condition turn less restrictive.

French caretaker finance minister Le Maire warned that the budget deficit could rise from 5.5% of GDP to 5.6% this year instead of the forecasted decline (in April) to 5.1%. Le Monde reports that he recommends immediate savings totaling €16bn. The extra slippage comes from lower than expected tax revenues and from higher spending by local authorities. Time is running short as the 2025 budget bill needs to be finalized by mid-September and debated by Parliament from October 1. Especially since French President Macron still needs to name the next prime minister and future government in the wake of highly divided election results in early July snap legislative elections.

Graphs

USD/JPY: risk-off, lower core yields and BOJ reconfirming policy normalization all favour the yen.

UK 15-y yield: 2040 gilt auction attracting ample investor buying interest, despite fiscal challenges.

EUR/CHF: Swiss franc holding strong evens as soft inflation paves the way for September SNB rate cut.

Brent oil tumbling to YTD low as markets grown ever more uncertain on China/global demand.

US ISM manufacturing rises to 47.2 in Aug, misses expectations

US ISM Manufacturing PMI rose from 46.8 to 47.2 in August, below expectation of 47.8,, indicates a fifth consecutive month of contraction.

Looking at some details,, new orders fell from 47.4 to 44.6. Production fell from 45.9 to 44.8. But employment rose from 43.4 to 46.0. Prices also rose from 52.9 to 54.0.

ISM said: “The past relationship between the Manufacturing PMI® and the overall economy indicates that the August reading (47.2 percent) corresponds to a change of plus-1.3 percent in real gross domestic product (GDP) on an annualized basis.”

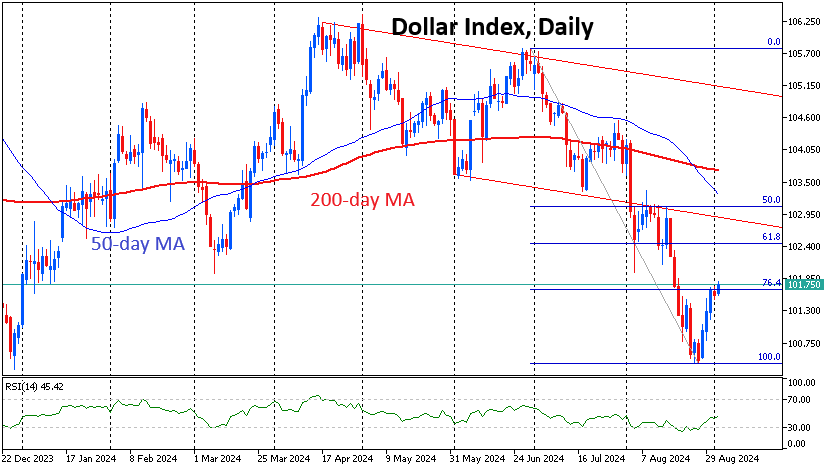

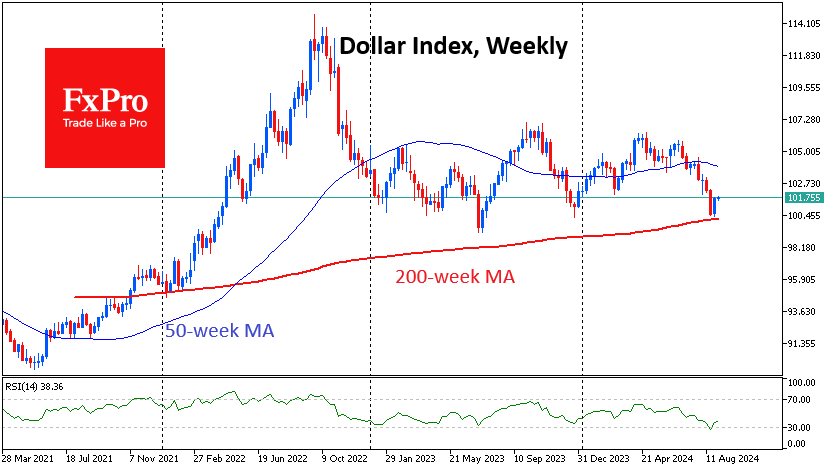

Dollar: Rebound or More?

The US dollar’s recovery continues, and other markets are starting to notice. The dollar index is up 1.4% to 101.7, having found support twice in the first half of last week before falling to 101.4.

The bounce has seen the dollar recover a quarter of the anti-rally from its peak in late July to the lows late last month. The momentum around current levels could be significant as the first retracement level (76.4% of the initial move) is centred here. At this point, there is more evidence to suggest that the dollar will at least attempt a higher rebound.

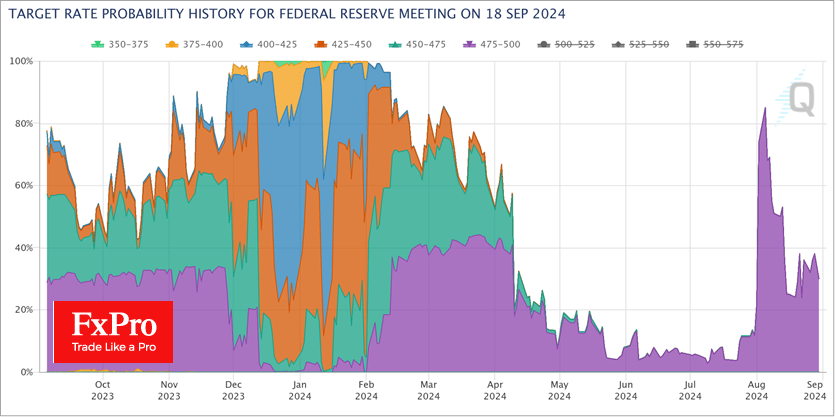

A 61.8% pullback is considered a classic market correction, which, in this case, is at 102.45. The fundamental driver of the dollar’s rally in recent days has been a repricing of the odds of a 50-point Fed rate cut in September. The odds of such an outcome are now estimated at 30%, down from 85% on 5 August (and 100% at the peak of the intraday sell-off).

The recent bounce is also telling, as the dollar bulls have managed to keep the market above the 200-week moving average and the RSI out of the oversold zone on the weekly chart. This looks like the start of a deeper bounce beyond the short-term shakeout.

Some uncertainty may remain until the release of the NFP later this week or even the inflation data on 11 September. Weakness in the macroeconomic data these days has the potential to send the dollar lower again after the chances of a sharp Fed reversal have risen.

However, in our baseline data scenario, which is in line with expectations, we see the odds of a regular 25-point rate cut in September and two more cuts before the end of the year rising. This seems like positive news for the dollar, which could gain around 1% from current levels.

The DXY’s rally may not stop there and could take it to the upper boundary of the 100.5-106.0 sideways range, where it has mostly traded since the beginning of the year.

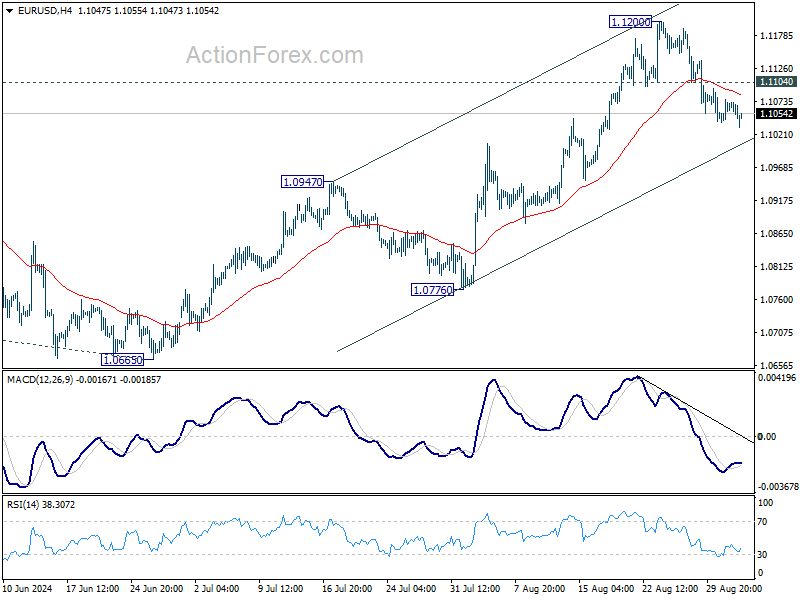

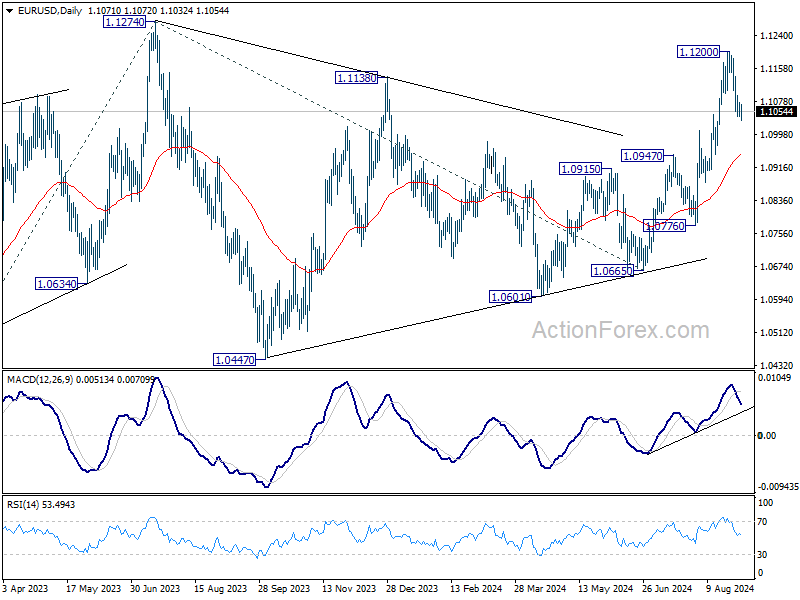

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1050; (P) 1.1064; (R1) 1.1086; More....

No change in EUR/USD's outlook. While retreat from 1.1200 might extend lower, rally from 1.0665 is in favor to continue as long as 1.0947 resistance turned support holds. Above 1.1104 minor resistance will bring retest of 1.1200 first. Break there will target 1.1274 high next.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

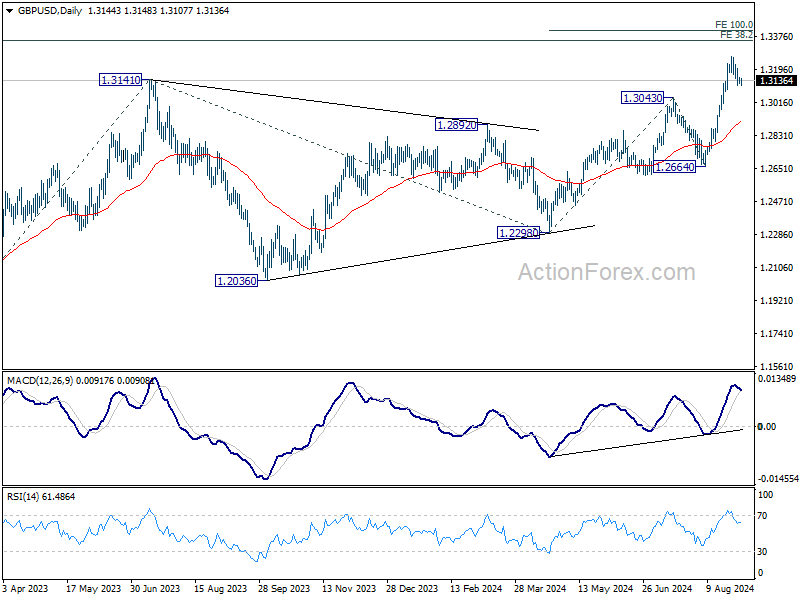

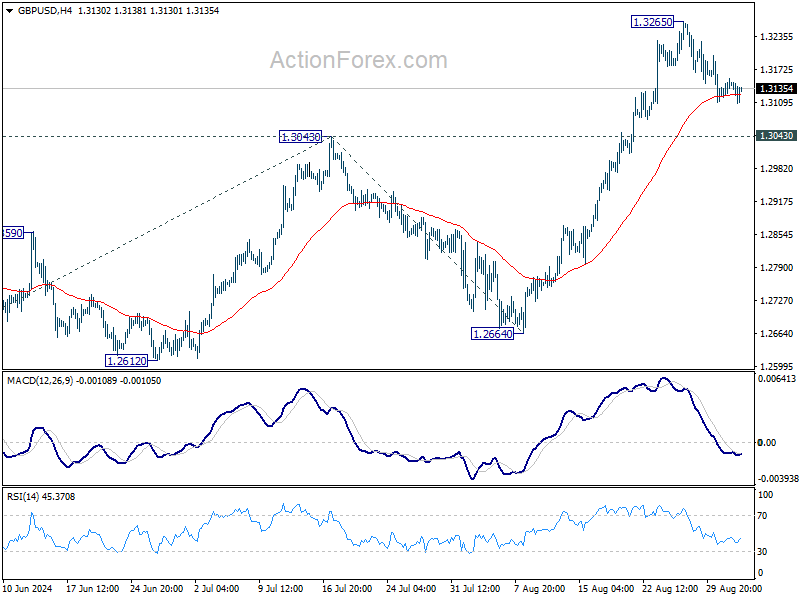

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3126; (P) 1.3140; (R1) 1.3162; More...

GBP/USD is still extending the consolidation from 1.3265 and intraday bias stays neutral. While deeper retreat cannot be ruled out, downside should be contained well above 1.3043 resistance turned support to bring rebound. On the upside, above 1.3265 will resume larger up trend to 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409.

In the bigger picture, up trend from 1.0351 (2022 low) is resuming. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.