Sample Category Title

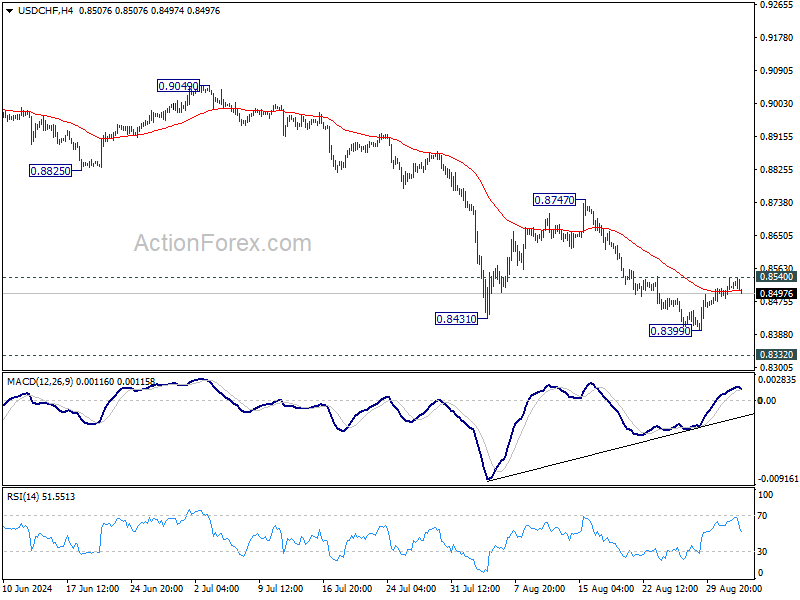

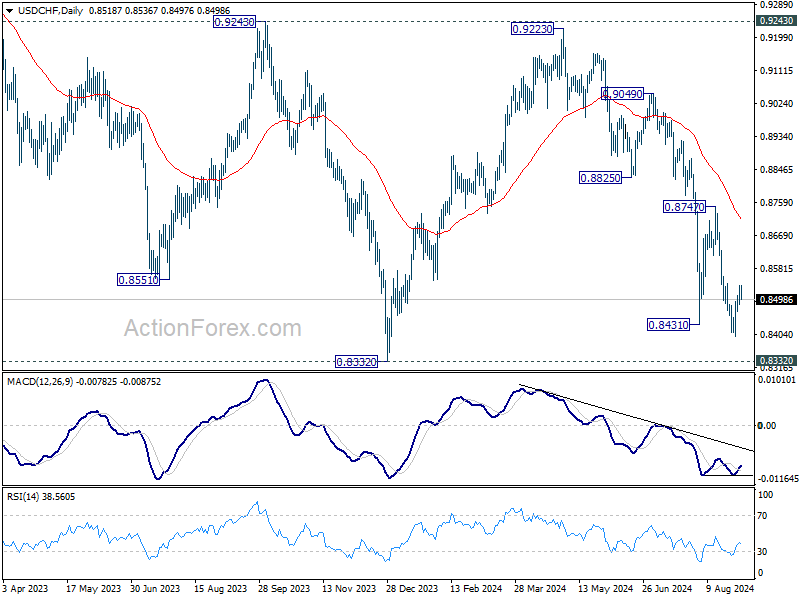

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8489; (P) 0.8513; (R1) 0.8542; More…

Intraday bias in USD/CHF stays neutral at this point, and further decline is expected as long as 0.8540 resistance holds. Break of 0.8339 will resume the fall from 0.9223 and target 0.8332 low. However, considering bullish convergence condition in 4H MACD, firm break of 0.8540 will confirm short term bottoming, and turn bias back to the upside for 0.8747 resistance instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

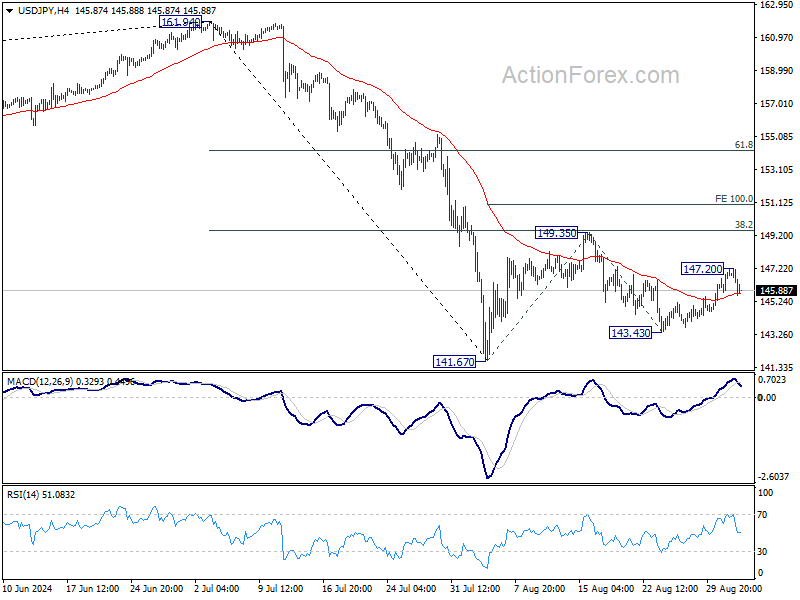

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.08; (P) 146.62; (R1) 147.47; More...

Intraday bias in USD/JPY is turned neutral with current retreat. But further rise will remain in favor as long as 143.43 support holds. Above 147.20 will target 149.35 resistance first. Firm break there will resume the rebound from 141.67 to 100% projection of 141.67 to 149.35 from 143.43 at 151.11, as the second leg of the corrective pattern from 161.94 high. However, break of 143.43 will bring retest of 141.67 low instead.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.47) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

Risk-Off Sentiment Grips Markets Ahead of Key US Data Release

Yen staged a notable rebound today, joined by Dollar and Swiss Franc. In contrast, Australian Dollar is leading losses among commodity currencies. Risk-off mood appears to be taking hold, which is also evident in US futures, which point to a lower open as American markets return from the Labor Day holiday.

Market participants seem to be adopting a more cautious approach ahead of a series of key US economic data releases scheduled for this week, beginning with ISM manufacturing index today. Optimism had been building after Fed Chair Jerome Powell signaled that policy easing might be on the horizon. However, that optimism could quickly evaporate if the upcoming data disappoints, reigniting fears of recession.

Swiss Franc has found additional support against Euro, bolstered by stronger-than-expected Q2 GDP figures. However, its upside has been limited by a weaker-than-anticipated inflation reading for August. This mixed data leaves the door open for SNB's decision later this month, with uncertainty over whether they will opt for a 25 or 50 basis point rate cut. Until then, EUR/CHF pair is likely to be influenced by broader risk sentiment.

Technically, with 0.9455 support turned resistance intact. EUR/CHF's fall from 0.9579 is still in favor to continue. Break of 0.9351, and sustained trading below 61.8% retracement of 0.9209 to 0.9579 at 0.9350 will pave the way back to retest 0.9209 low.

In Europe, at the time of writing, FTSE is down -0.51%. DAX is down -0.29%. CAC is down -0.19%. UK 10-year yield is down -0.0445 at 3.989. Germany 10-year yield is down -0.021 at 2.322. Earlier in Asia, Nikkei fell -0.04%. Hong Kong HSI fell -0.23%. China Shanghai SSE fell -0.29%. Singapore Strait Times rose 0.50%. Japan 10-year JGB yield rose 0.0143 to 0.926.

Swiss GDP grows 0.7% qoq in Q2, above exp 0.6% qoq

Switzerland’s GDP grew by 0.7% qoq in Q2, exceeding expectations of 0.6% qoq and marking an improvement from Q1’s 0.5% qoq growth. When adjusted for sporting events, GDP still showed solid growth at 0.5% qoq, up from the previous quarter's 0.3% qoq.

This stronger-than-expected performance was largely driven by significant expansion in the chemical and pharmaceutical industries, which played a key role in lifting the overall economic output. However, growth across other sectors was uneven, reflecting underlying weaknesses in domestic demand.

Swiss CPI slows to 1.1% yoy in Aug, vs exp 1.2% yoy

Swiss CPI was flat mom in August, below expectation of 0.1% mom rise. Core CPI (excluding fresh and seasonal products, energy and fuel) rose 0.1% mom. Domestic products prices was flat while imported products prices fell -0.1% mom.

For the 12-month people, CPI slowed from 1.3% yoy to 1.1% yoy, below expectation of 1.2% yoy. Core CPI was unchanged at.10% yoy. Domestic product prices was unchanged at 2.0% yoy. Imported price prices fell from -1.0% yoy to -1.9% yoy.

BoJ's Ueda reaffirms commitment to further rate hikes if economic conditions allow

BoJ Governor Kazuo Ueda reiterated today that the central bank could continue raising interest rates if the economy and inflation develop as expected.

In a document presented to a government panel led by Prime Minister Fumio Kishida, Ueda highlighted that, despite the July rate hike, the economy are still solidly supported by current monetary policy, as rates are still significantly negative.

Additionally, members of the government panel, including business leader Masakazu Tokura, submitted a proposal urging careful management of macroeconomic policies, especially in light of the recent market turbulence. This highlights the importance of coordination between BOJ and the government to maintain economic stability as BoJ navigates its gradual shift towards higher interest rates.

NZIER expects Oct RBNZ rate cut, further easing hinges on demand recovery

The New Zealand Institute of Economic Research indicated today that it expects RBNZ to implement another interest rate cut during its October meeting. This follows RBNZ's decision in August to bring forward its easing cycle in response to "deterioration in economic outlook." However, NZIER notes that the pace of further easing remains highly uncertain, with a potential pause in November depending on how quickly demand recovers.

Weaker demand has become a significant concern for businesses, with 61% of firms identifying it as the primary constraint on their operations. This declining demand is also having an impact on the labor market, where there is now more slack as companies reduce hiring in response to the softer economic environment.

Looking ahead, NZIER forecasts GDP growth to remain subdued over the next year, contributing to further decline in inflation. The institute predicts that annual CPI inflation will fall back within RBNZ's target band by the end of this year, which underpins its expectation for another Official OCR cut in October.

However, the uncertainty surrounding the economic recovery suggests that any further rate cuts after October will be closely tied to the extent of demand recovery, with the November meeting likely to be a key decision point.

New Zealand's terms of trade improve in Q2 despite decline in export volumes

New Zealand's terms of trade saw a solid improvement in the second quarter of 2024, rising by 2.0%. This increase was driven by a 5.2% rise in export prices, which outpaced the 3.1% increase in import prices. However, the value of exports decreased by -1.5% to NZD 16.6 billion, largely due to a -4.3% drop in export volumes, even as higher prices provided some support.

Dairy products played a significant role in the export dynamics, with prices rising by 8.0%. Despite this, dairy export volumes fell sharply by -10%, leading to an 8-.0% decline in the overall value of dairy exports. The meat sector, on the other hand, performed better, with prices rising by 7.3%, volumes increasing by 4.1%, and the total value of meat exports up by 6.5%.

On the import side, the total value rose by 4.0% to NZD 18.9B, supported by a 3.2% increase in import volumes. Petroleum and petroleum products were notable contributors, with prices up by 4.0%. However, petroleum volumes declined by -8.0%, leading to a -4.4% decrease in the overall value of these imports.

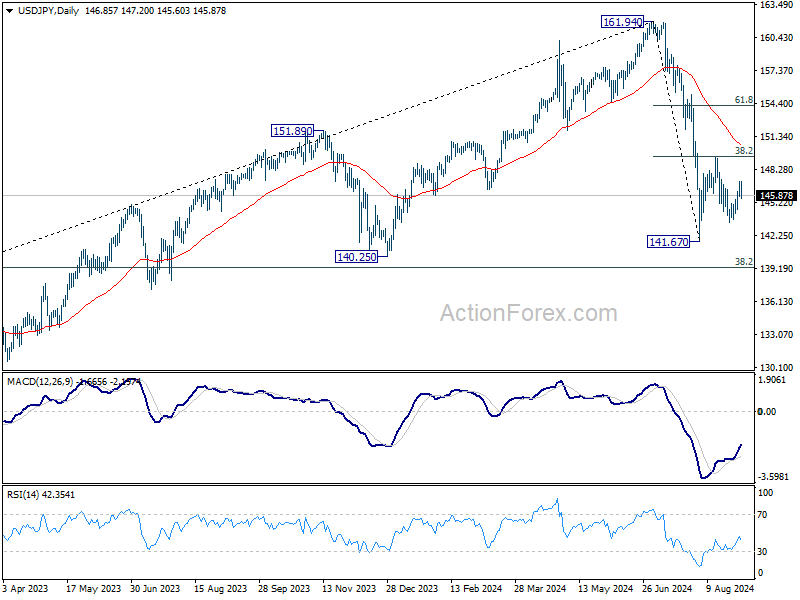

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.08; (P) 146.62; (R1) 147.47; More...

Intraday bias in USD/JPY is turned neutral with current retreat. But further rise will remain in favor as long as 143.43 support holds. Above 147.20 will target 149.35 resistance first. Firm break there will resume the rebound from 141.67 to 100% projection of 141.67 to 149.35 from 143.43 at 151.11, as the second leg of the corrective pattern from 161.94 high. However, break of 143.43 will bring retest of 141.67 low instead.

In the bigger picture, fall from 161.94 medium term top is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.47) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Terms of Trade Index Q2 | 2.00% | 2.60% | 5.10% | |

| 23:50 | JPY | Monetary Base Y/Y Aug | 0.60% | 0.60% | 1.00% | |

| 01:30 | AUD | Current Account (AUD) Q2 | -10.7B | -5.5B | -4.9B | -6.3B |

| 06:30 | CHF | CPI M/M Aug | 0.00% | 0.10% | -0.20% | |

| 06:30 | CHF | CPI Y/Y Aug | 1.10% | 1.20% | 1.30% | |

| 07:00 | CHF | GDP Q/Q Q2 | 0.70% | 0.60% | 0.50% | |

| 13:30 | CAD | Manufacturing PMI Aug | 47.8 | |||

| 13:45 | USD | Manufacturing PMI Aug F | 48 | 48 | ||

| 14:00 | USD | ISM Manufacturing PMI Aug | 47.8 | 46.8 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Aug | 52.5 | 52.9 | ||

| 14:00 | USD | ISM Manufacturing Employment Aug | 43.4 | |||

| 14:00 | USD | Construction Spending M/M Jul | 0.10% | -0.30% |

XAG/USD Analysis: Bulls May Target $30 Again

As the XAG/USD chart indicates today, the price of silver has dropped by over 5% in the past week. Bearish signs are also evident in the price of gold. According to Reuters, market participants are focusing on a series of economic data set to be released this week, which could influence expectations regarding a potential rate cut at the Federal Reserve’s September meeting.

Could the price of silver continue to decline? Technical analysis of the XAG/USD chart shows that since late May, the price of silver has been forming a structure resembling a fan of three expanding lines, marked in red.

Bullish Arguments:

→ The price has broken through the red median line and moved into the upper half of the fan.

→ The price is near the bullish breakout level of the median line, which may provide support.

→ On 2-3 September, the bearish momentum slowed down, indicating potential support, which could be strengthened by the lower boundary of the rising blue channel.

→ The price is at the 50% level of the bullish A→H impulse.

Bearish Arguments:

→ Near the psychological level of $30 per ounce, a bearish head and shoulders (H&S) pattern has formed on the chart, although the potential from the neckline break has almost been exhausted.

Therefore, it is possible that the bulls may try to regain control and make a new attempt to push the price towards the $30 level. Whether this scenario plays out will largely depend on the fundamental backdrop. On Friday, 6 September, at 15:30 GMT+3, US labour market data will be released – this event could have a significant impact on the price of silver.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

AUD/USD Sinks Ahead of GDP

The Australian dollar is sharply lower on Tuesday. AUD/USD is trading at 0.6732 in the European session, down 0.88% today at the time of writing.

Australian GDP expected to remain soft

Australia’s economy has been sputtering and the markets aren’t expecting much change from second-quarter GDP on Wednesday. GDP is expected to trickle lower to 1% y/y, down from 1.1% in Q1, which was the weakest pace of growth since Q4 2020. Quarterly, the market estimate for GDP stands at 0.3%, compared to 0.1% in Q1.

GDP-per-capita is expected to be negative, another indication that economic activity remains subdued. Australia has been hit by a drop in iron ore and core prices and exports fell by 4.4% in the second quarter, which doesn’t bode well for the Australian dollar.

The GDP is unlikely to change the Reserve Bank of Australia’s plans when it meets on Sept. 24. The central bank is closely watching inflation, which remains stubbornly high, as well as the labor market. Governor Bullock has said she has no plans to lower the cash rate from its current 4.35% for the next six months. The RBA has stuck to its “higher for longer” stance and has maintained rates since November.

The Federal Reserve is widely expected to lower rates on September 18, with a 70% likelihood of a quarter-point cut and a 31% likelihood of a half-point cut. Ahead of the meeting is a crucial employment report on Friday. The previous jobs report was much weaker than expected and triggered a meltdown in the financial markets. Another weak jobs report would raise the likelihood of a half-point cut, while a solid release will cement a quarter-point cut.

AUD/USD Technical

- AUD/USD has pushed below support at 0.6780 and is testing support at 0.6737. Below, there is support at 0.6708

- 0.6809 and 0.6852 are the next resistance lines

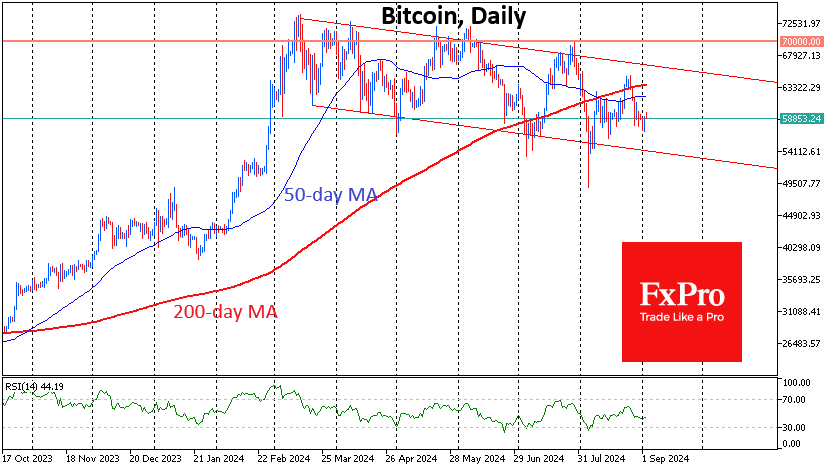

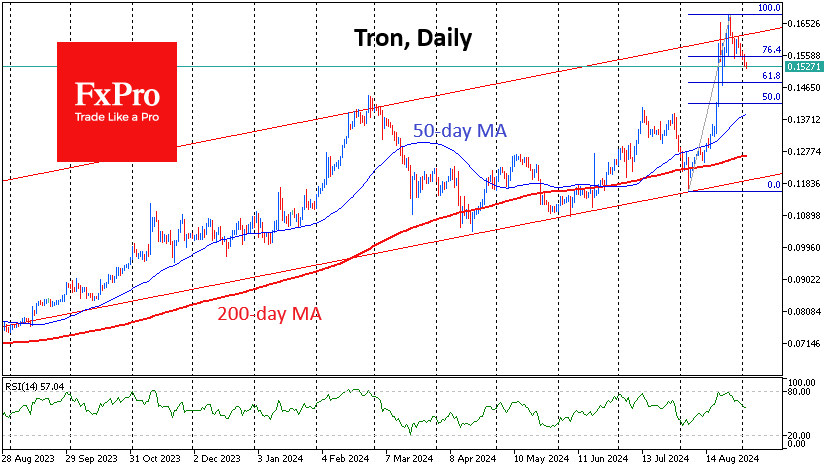

Wary Crypto Market

Market Picture

The crypto market rose 2.3% in 24 hours to reach a cap of $2.07 trillion, growing steadily throughout Monday. However, cautious Asian market dynamics on Tuesday morning have interrupted the recovery near levels seen late last week. This recovery has yet to improve sentiment, with the index remaining at 26 for the third consecutive day.

Bitcoin is trading just below $59K at the start of active trading in Europe, having reached $59.7K at the peak of the Asian session. Despite intraday fluctuations, the BTC exchange rate has closed in the $59.0-59.3K range for the past six days, reflecting the balance of power. The local initiative remains with the bears, as the price is below the 50- and 200-day moving averages, and close to the lower boundary of the descending channel.

Tron remains in a corrective phase, having fallen to $0.1525. In August, the price soared from $0.1160 to $0.1680, flying from the lower to the upper boundary of the ascending corridor since the beginning of 2023. The current correction is helping to ease overheating and attract new buyers, but a dip below $0.1430-0.1480 would set a more cautious tone.

News Background

According to CoinShares, crypto fund investments fell by $305 million last week after three weeks of inflows. Bitcoin investments fell by $319 million, Ethereum by $6 million and Solana by $8 million.

QCP Capital notes Ethereum’s significant decline in August compared to BTC, as well as the underperformance of spot ETFs in the US, and warns that the market’s decline could continue in September.

According to Santiment, the number of bitcoin wallets with a minimum of 100 BTC rose to 16,120, a 17-month high. Experts believe that increased wallet activity is a positive signal for the market. Bitgrow Lab notes that historically, significant whale purchases have often preceded new all-time highs in bitcoin.

According to BiTBO, bitcoin miners’ revenue fell to its lowest level in 11 months in August. The dynamics were affected by an increase in complexity and a decrease in the number of transactions.

The Cardano network successfully passed the Chang hardfork, marking the beginning of the Conway registry era and the ecosystem’s transition to decentralised governance. ADA token holders will be able to participate in a vote to determine the future of the network.

BoJ’s Ueda reaffirms commitment to further rate hikes if economic conditions allow

BoJ Governor Kazuo Ueda reiterated today that the central bank could continue raising interest rates if the economy and inflation develop as expected.

In a document presented to a government panel led by Prime Minister Fumio Kishida, Ueda highlighted that, despite the July rate hike, the economy are still solidly supported by current monetary policy, as rates are still significantly negative.

Additionally, members of the government panel, including business leader Masakazu Tokura, submitted a proposal urging careful management of macroeconomic policies, especially in light of the recent market turbulence. This highlights the importance of coordination between BOJ and the government to maintain economic stability as BoJ navigates its gradual shift towards higher interest rates.

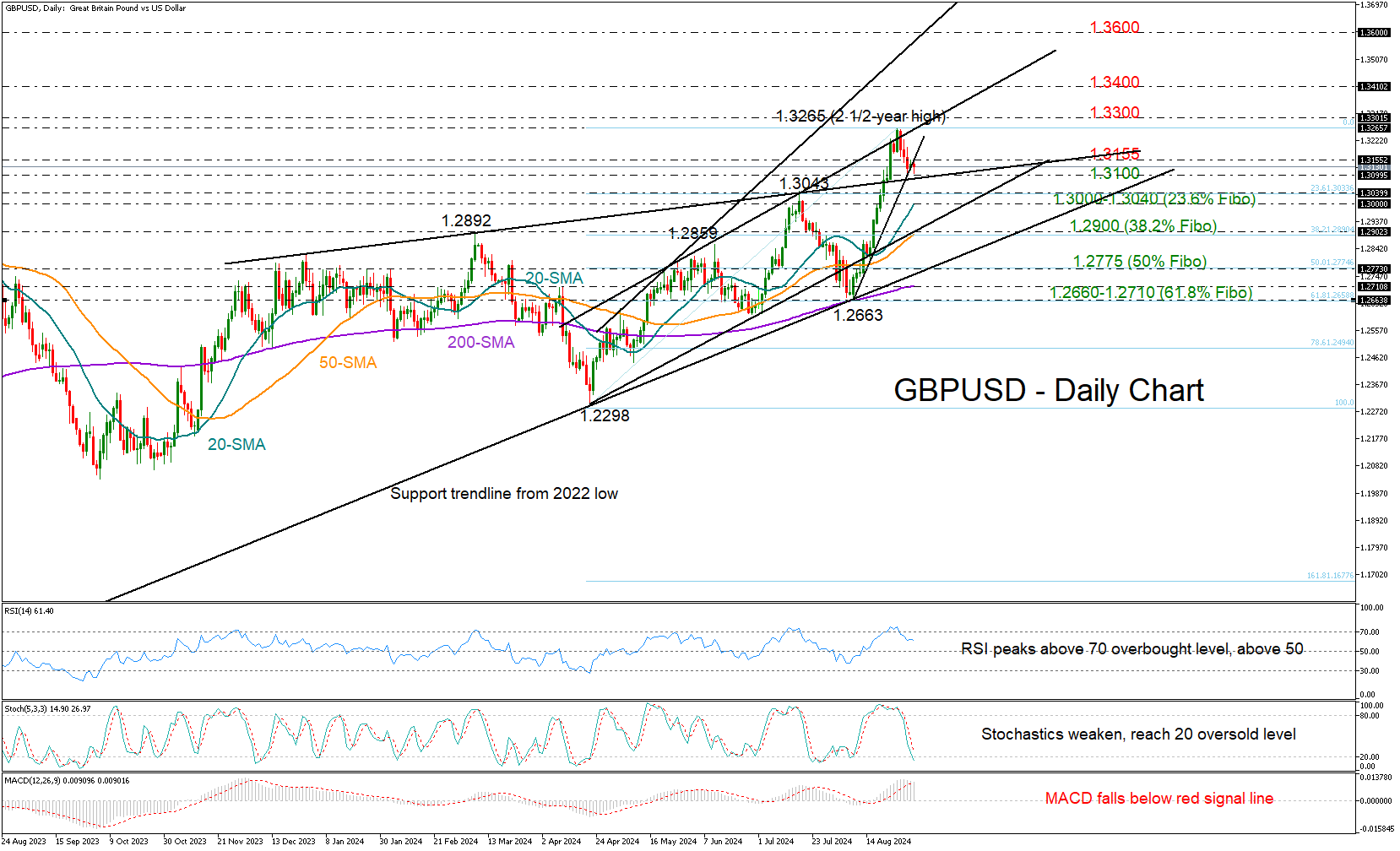

GBPUSD Takes a Negative Turn

- GBPUSD starts a new bearish wave but maintains broad uptrend

- Technical signals reflect appetite for more selling; eyes on 1.310b

GBPUSD resumed its negative momentum during Tuesday’s early European trading hours, crossing below the steep support trendline, which had been curtailing the pullback from the two-and-a-half year high of 1.3265 over the past two trading days.

A decline below 1.3100 could motivate more selling towards the 23.6% Fibonacci retracement of the April-July upleg at 1.3040 and the 20-day simple moving average (SMA) at 1.3000. If the bears dominate there, the negative cycle could stretch towards the 38.2% Fibonacci mark of 1.2900 and the 50-day SMA. Another step lower could confirm a continuation towards the ascending trendline from 2022 seen around the 50% Fibonacci level and the 1.2775 level.

With the RSI and the stochastic oscillator changing direction to the downside and the MACD slipping below its red signal line, it is probable that selling interest will remain intact for the time being. Nevertheless, the rising slope in the SMAs implies that the ongoing bearish wave might be a component of the larger bullish trend.

In the event the price returns above the broken support trendline at 1.3155, the bulls will stage another battle around the 1.3265 peak and the tough resistance line from April. The 1.3300 number will be closely watched as well, and if buyers claim that barrier, the rally could pick up steam towards the 1.3400 round level. Above that, there are no significant obstacles until the 1.3600 level.

In summary, GBPUSD might experience ongoing downward pressure in the next few sessions, especially if it closes below 1.3100. For a bullish continuation, the price must exceed the resistance trendline at 1.3265.

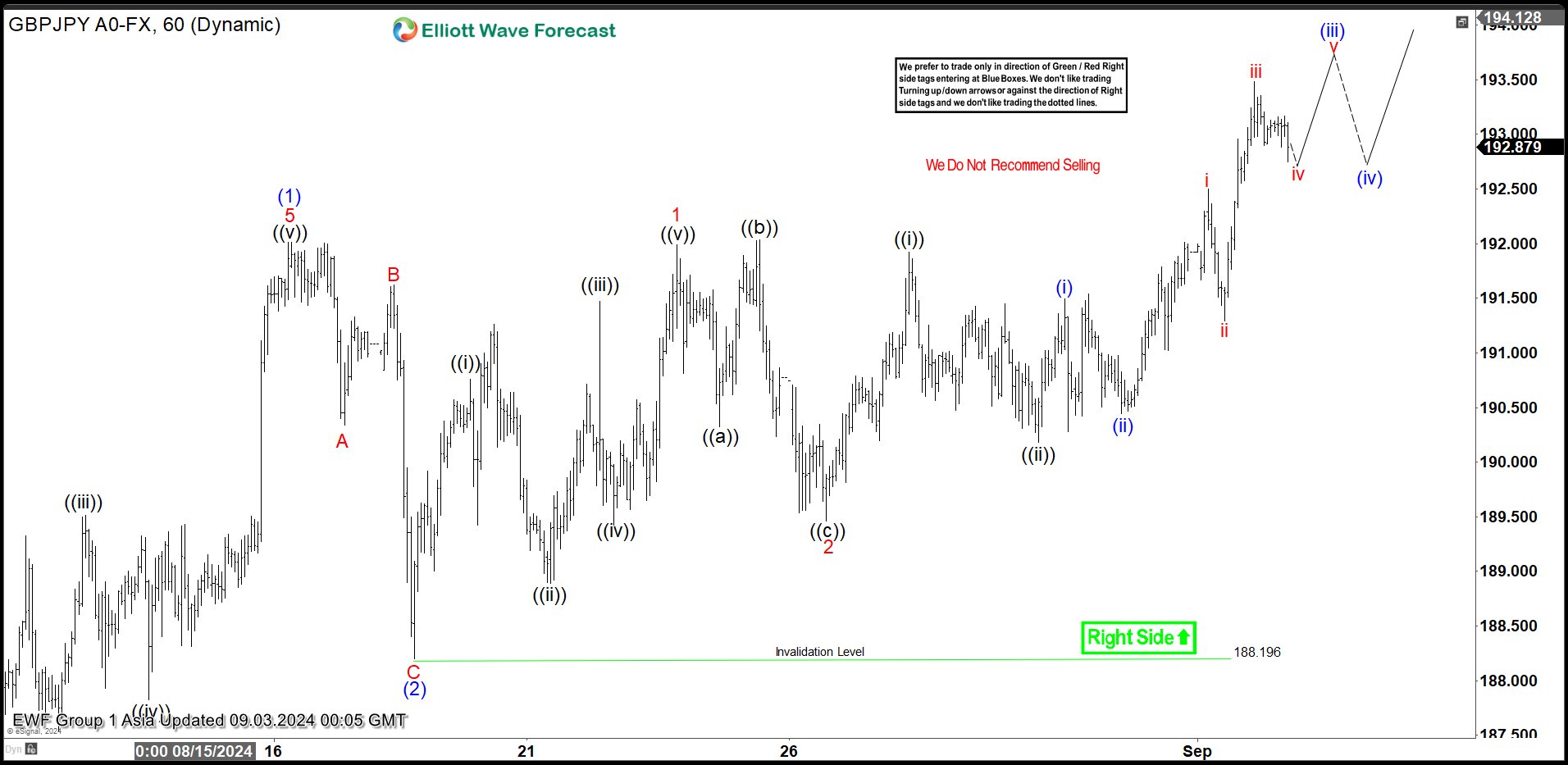

Short Term Elliott Wave Sequence in GBPJPY Calling Further Upside

Short Term Elliott Wave in GBPJPY shows a bullish sequence from 8.5.2024 low, favoring further upside. Rally from 8.5.2024 low is unfolding as a 5 waves impulse. Wave (1) higher ended at 192.01. Pullback in wave (2) unfolded as a zigzag Elliott Wave structure like the 1 hour chart below shows. Down from wave (1), wave A ended at 190.34 and rally in wave B ended at 191.625. Wave C lower ended at 188.19 which completed wave (2) in higher degree. The pair extended higher in wave (3). Up from wave (2), wave ((i)) ended at 190.76 and dips in wave ((ii)) ended at 188.89. Wave ((iii)) higher ended at 191.47 and wave ((iv)) ended at 189.42. Final leg wave ((v)) ended at 192 which completed wave 1 in higher degree.

Pullback in wave 2 ended at 189.46 with internal subdivision as expanded flat. Up from there, wave 3 is in progress as an impulse. Wave ((i)) of 3 ended at 191.92 and wave ((ii)) of 3 ended at 190.18. Pair is nesting higher in wave ((iii)) with wave (i) ended at 191.49 and wave (ii) ended at 190.44. Expect wave (iii) to end soon, followed by wave (iv) pullback before it resumes higher again. Near term, as far as pivot at 188.19 low stays intact, expect dips to find support in 3, 7, 11 swing for further upside.

GBPJPY 60 Minutes Elliott Wave Chart

GBPJPY Elliott Wave Video

https://www.youtube.com/watch?v=kT3uLWSEINA&embeds_referring_euri=https%3A%2F%2Felliottwave-forecast.com%2F&source_ve_path=MjM4NTE

Brent Crude Under Pressure Amid Supply Expansion Concerns

Brent crude oil prices have experienced significant selling pressure recently, dipping to 77.21 USD per barrel on Tuesday. Although there has been a slight recovery from earlier lows, the overall market sentiment remains bearish.

Investors are reacting to recent data from OPEC, which indicates that 8 OPEC+ members plan to increase their production by 180,000 barrels per day. This anticipated rise in supply casts a shadow over the oil market, particularly as it coincides with weakening demand indicators from major economies.

A report from the Department of Energy in the US highlighted a drop in oil consumption in June to levels not seen since the summer of 2020, considering seasonal adjustments. This downturn in demand is mirrored by troubling economic data from China, where factory activity has reportedly reached a six-month low. Moreover, the decline in selling prices and a reduction in new orders from Chinese manufacturing sectors add to the pessimism surrounding future demand.

However, some support for oil prices stems from production issues in Libya, where the largest local oilfield has halted production due to state-imposed force majeure. This disruption could pose supply challenges for major oil consumers and as highlighted in commodities analysis, temporarily cushion the impact of broader negative trends.

Brent technical analysis

The H4 chart shows a previous growth impulse peaking at 81.85, followed by a correction down to 75.20, forming a broad consolidation range at this lower level. There is an expectation for a growth move towards 79.00 today. If this level is breached upward, it may signal the continuation of the growth wave to 82.87. This bullish scenario is tentatively supported by the MACD indicator, whose signal line is below zero but shows signs of an upward trajectory.

On the H1 chart, Brent has formed a corrective structure down to 76.02 and is currently developing a growth structure towards 77.55. A successful breach of this level could open the way for further growth to 79.00, potentially continuing to 82.87. The Stochastic oscillator supports this outlook, with its signal line positioned around 50 and pointing upwards, indicating potential for further price increases.

Overall, while the short-term technical indicators suggest a possible recovery in Brent prices, the broader market context remains challenging due to increased supply forecasts and weak demand signals from vital global markets.