Sample Category Title

XAUUSD: Weekly Outlook

Gold has been on a winning streak, rising for seven straight months and gaining 21% so far this year. The key question now is whether this momentum will continue in September or if the metal will take a break. The future of gold prices will largely depend on upcoming U.S. economic data and interest rate expectations. The overall market trend for gold remains positive, and many believe the metal is still undervalued, especially with ongoing inflation concerns. Additionally, lower bond yields, driven by expectations of Federal Reserve rate cuts, should continue to support gold's strength.

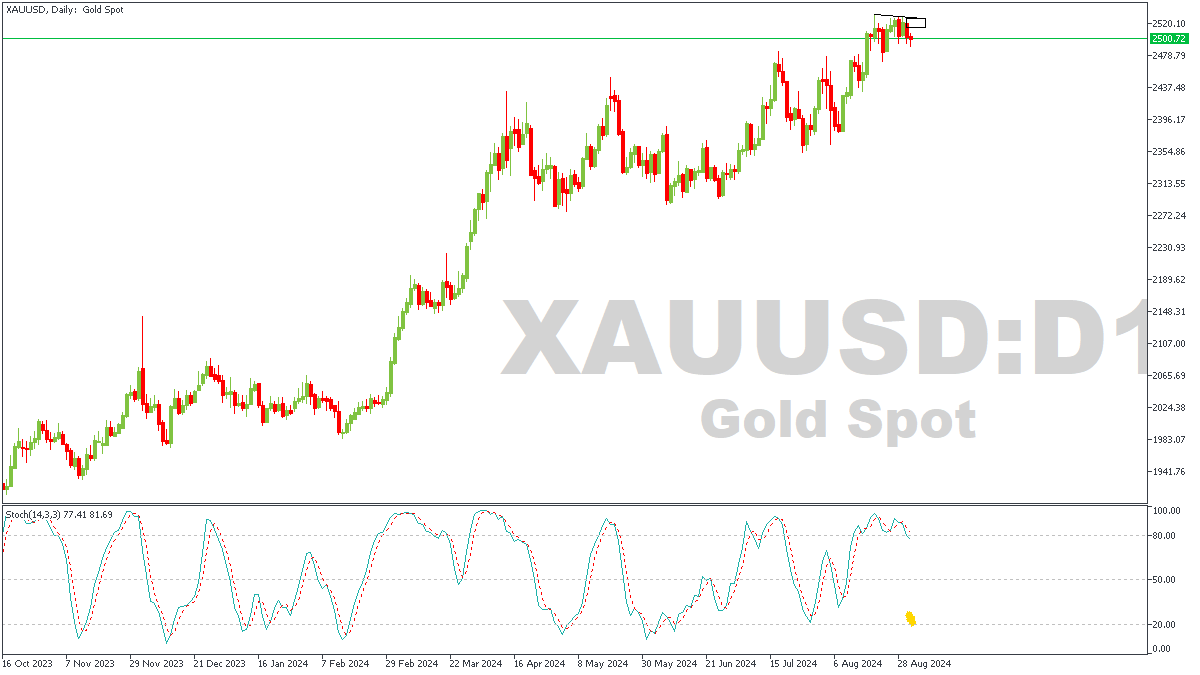

XAUUSD – D1 Timeframe

The Daily timeframe of XAUUSD gives a bare hint at the likelihood of a bearish rally based on the stochastic indicator being overbought; and creating a divergent pattern. This initial indication however needs closer observation before any form of conclusion can be made regarding the outcome.

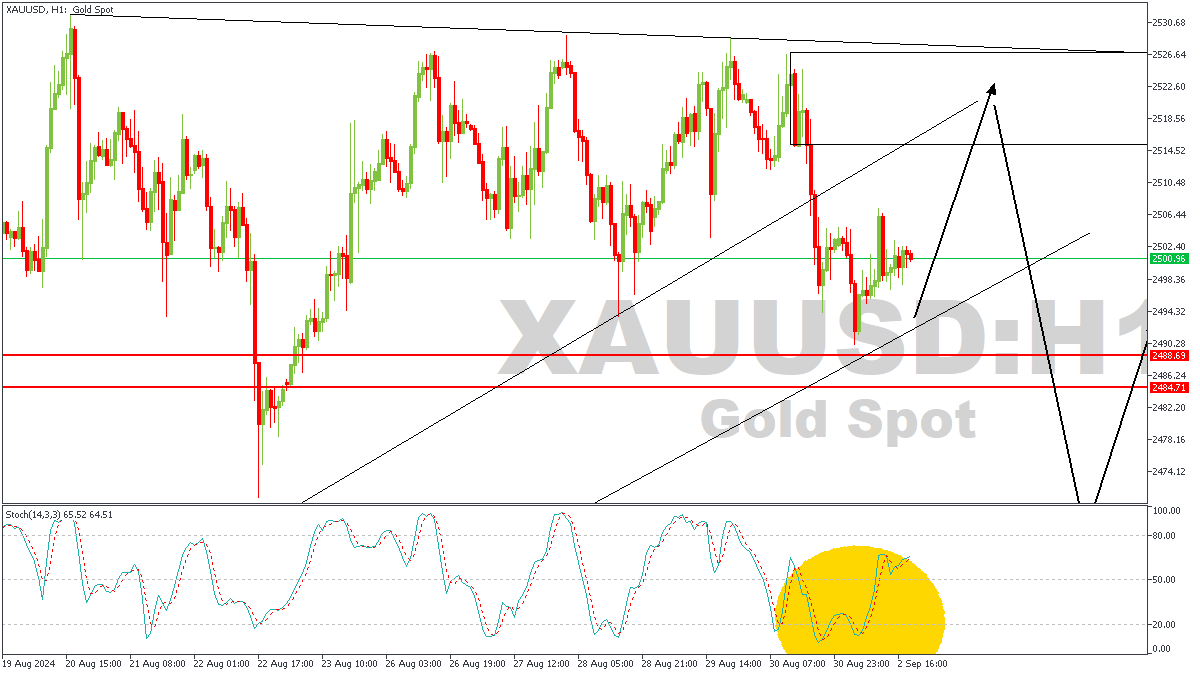

XAUUSD – H1 Timeframe

The 1-hour timeframe presents a more reliable insight into the price action. Here on the chart, we see the supply zone created as a result of the break below the trendline support. Next, price bounced off the daily timeframe pivot zone, heading for the supply area. Now, if the rejection from the supply zone crosses below the secondary trendline support, we would have a confirmation for the bearish sentiment.

Analyst’s Expectations:

- Direction: Bearish

- Target: $2,489.79

- Invalidation: $2,529.10

GBPUSD & EURUSD Outlook

The forex market was relatively quiet during the Asian trading session, with only minor changes seen across currencies. There was a slight dip in commodity currencies due to weaker-than-expected manufacturing data from China, though this was somewhat balanced by better results from the Caixin PMI report. This week will be crucial as traders look for clues on the Fed’s upcoming decisions on interest rate cuts, with important economic data like the ISM indexes and non-farm payrolls expected to provide direction. Here is the prediction from our weekly live analysis on YouTube. Enjoy!

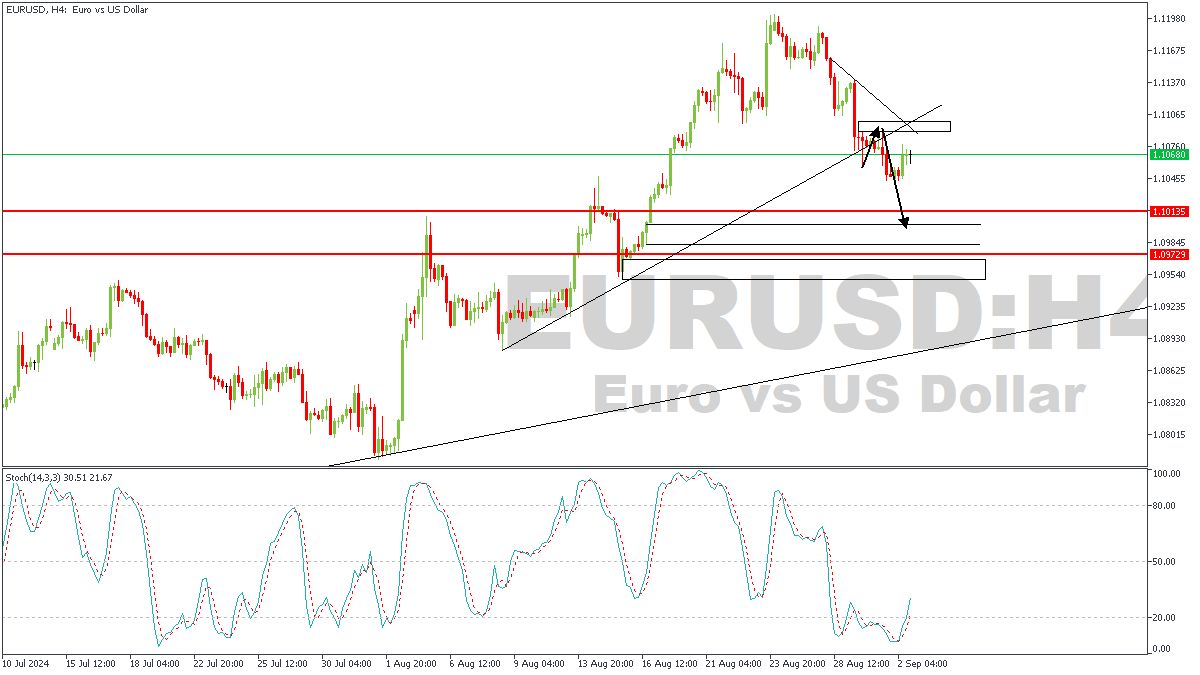

EURUSD– H4 Timeframe

EURUSD began a steady decline last week, followed by a stalling in the price action as price seeks to find its course ahead of the rates decision. This week, I expect to see a continuation of the bearish momentum since price has already broken below the previous structure, and trendline. The retest of the confluence region between the trendline resistance, and the supply zone is my priority entry region.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.10028

- Invalidation: 1.10959

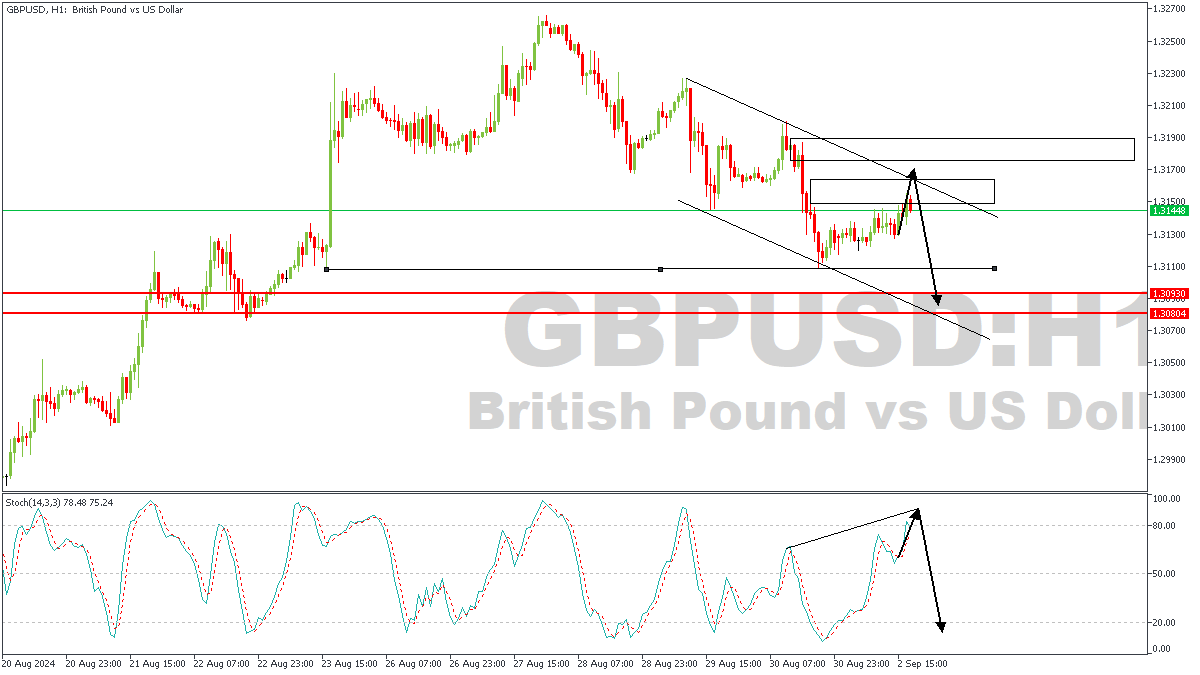

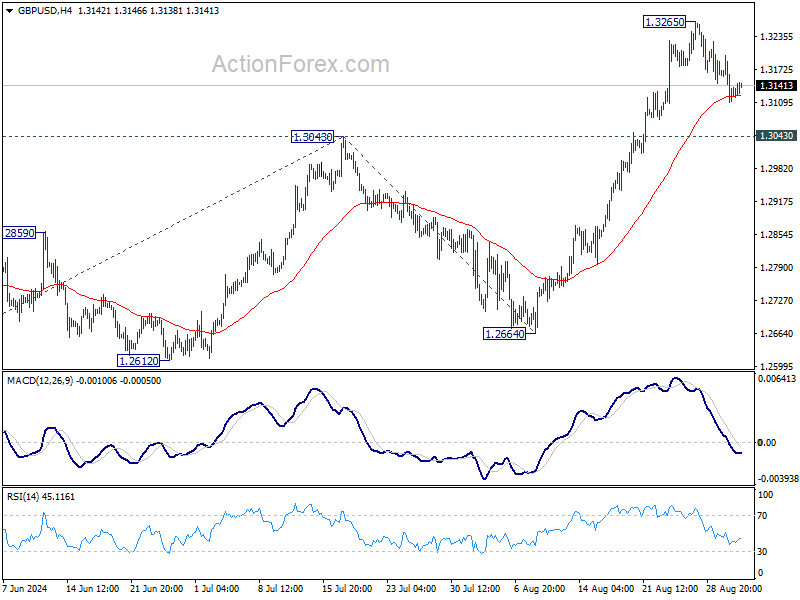

GBPUSD – H1 Timeframe

GBPUSD is currently trading within a descending channel, with the stochastic nearly completing a convergence pattern. This implies that the confluence of the supply zone and the trendline resistance can be expected to carry much more weight as a result of the stochastic confirmation. Ultimately, critical observation of the lower timeframe price action will determine the trigger point.

Analyst’s Expectations:

- Direction: Bearish

- Target: 1.31082

- Invalidation: 1.31928

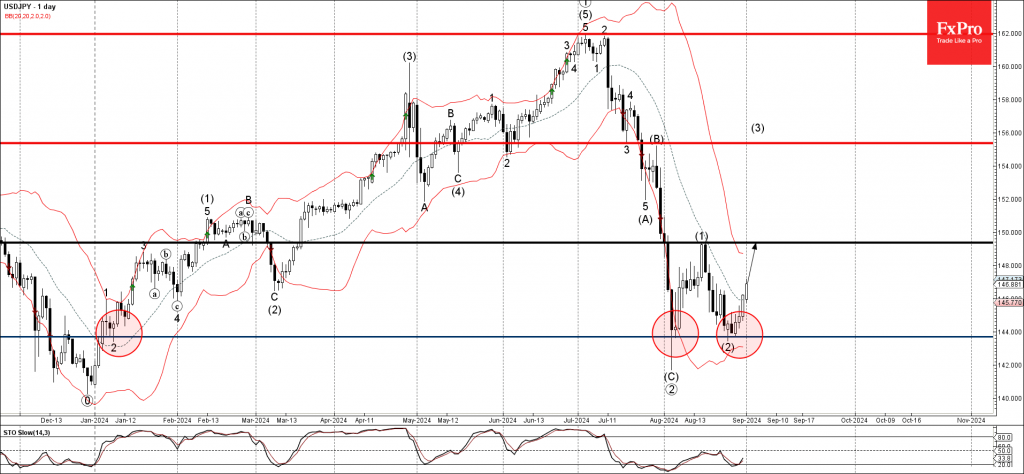

USDJPY Wave Analysis

- USDJPY reversed from support level 144.00

- Likely to rise to resistance level 149.35

USDJPY currency pair recently reversed up from the strong support level 144.00 (which has been reversing the price from January) standing near the lower daily Bollinger Band.

The upward reversal from the support level 144.00 created the daily Japanese candlesticks reversal pattern Bullish Engulfing – which started the active impulse wave (3).

Given the strength of the support level 144.00 and the continuation of the yen sales, USDJPY currency pair can then be expected to rise to the next resistance level 149.35 (top of the previous impulse wave (1)).

USD/JPY Price Forecast – USD Gains Despite Labor Day Liquidity

- USD/JPY rises for the fourth consecutive day, supported by US economic optimism.

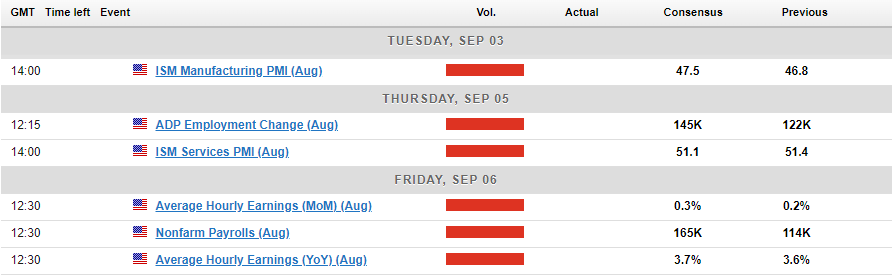

- US employment data this week is crucial for Fed’s September rate decision and USD/JPY direction.

- Japanese economic indicators and seasonality may also influence USD/JPY’s trajectory.

USD/JPY continued its advance on a thin liquidity Monday. The greenback is up around 0.57% against the JPY and on course for a fourth successive day of gains.

The US Dollar has been on a steady rise over the past few days as investors remain optimistic about the US economy following last week’s GDP data. This was followed by a decent PCE print which went some way in allaying recessionary fears and offering the greenback some support.

There is a large swatch of data out of both the US and Japan this week which could shape the trajectory of the pair. The Japanese economy has been on an upward trajectory of late as speculation grows about further rate hikes from the Bank of Japan (BoJ). This is crucial as it comes at a time when Global central banks are looking to cut rates and not raise them.

US Employment Data is Key

I think the biggest impact this week on USD/JPY will come from the US jobs report. The importance of this release has grown in stature since the massive downgrade in job numbers by the BLS. It led markets to start speculating on a potential 50 bps rate cut in September.

A soft jobs print could bring this conversation back to the fore and could play a major role in determining the Fed decision on September 18. A strong jobs number could finally put an end to that debate as it appears that many Fed members are uncomfortable with beginning the rate cut cycle with a 50 bps move.

There are some mid-tier Japanese data releases which should show continued improvement in the Japanese economy. For more information on this please read the weekly market outlook.

Technical Analysis

From a technical standpoint, USD/JPY appears to have bottomed out just below the 144.00 handle before the recovery began. The pair has since posted 3 consecutive days of gains and is on course for a fourth.

Interestingly enough this comes despite the expectations of rate cuts from the Fed and rate hikes from the BoJ putting the two central banks on differing paths. In theory the Yen should be gaining ground against the greenback, however there could be an explanation as to why the greenback is on the up.

The answer may be two-fold as market participants appear to be betting on the US economy following a stellar GDP revision. Also, the initial USD selloff around the rate cut issue may mean that a lot of the expected 25bps cut in September has already been priced in.

Another consideration could be seasonality. Historically the US dollar enjoys a good month of September while US stocks seem to struggle. Will history repeat itself?

Today’s daily candle is on course to close above the 146.37 swing high which would signal a shift in structure where price action is concerned. This would increase the probability of further upside even if we do have a slight pullback first potentially to resistance turned support at 146.37.

USD/JPY Chart, September 2, 2024

Source: TradingView (click to enlarge)

Support

- 146.37

- 145.00

- 143.85

Resistance

- 148.00

- 150.00 (psychological level)

- 151.216 (200-day MA)

Dollar Index Outlook: Bulls Lose Traction But Hold grip, as Markets Await US Labor Data

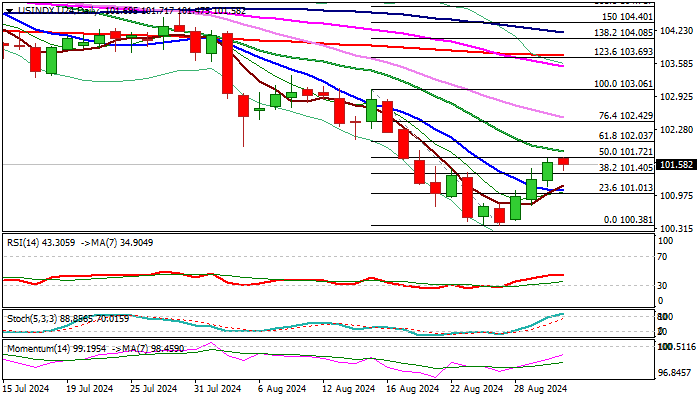

The dollar index eases from new two-week high on Monday, after strong three-day recovery rally showed initial signs of fatigue.

Repeated rejection at 101.72 barrier (50% retracement of 103.06/100.38 bear-leg / 4-hr cloud top) and overbought stochastic contributed to a partial profit-taking, though dips were so far shallow and suggesting that bulls still hold grip.

The dollar was lifted by last week’s inflation data which cooled bets for more aggressive steps by Fed, returning bets to widely expected 25 basis points rate cut.

The pause in rally also comes in days preceding key economic event this week – release of monthly report from the US labor sector, with NFP being particularly in focus.

The latest set of economic data ahead of September’s policy meeting will complete the picture and determine the magnitude of the US central bank’s action.

Expect firmer bearish signal on break and close below broken Fibo barrier at 101.40 (38.2%), with extension below 10DMA (101.07) to confirm reversal.

Conversely, sustained break above pivots at 102.72/85 (50% retracement / 20DMA) to open way for 102+ gains.

Res: 101.72; 101.85; 102.03; 102.43.

Sup: 101.40; 101.07; 100.78; 100.38.

Sunset Market Commentary

Markets

Trading slowed down to a trickle today in absence of US investors (Labour Day holiday) and amid an empty EMU eco calendar. A lot of ink has been spilled about this week’s key US eco data and their impact on markets and Fed policy. It allows us to have a look at this week’s alternative agenda, starting with Swiss eco data tomorrow. Swiss inflation is expected to continue hovering just above the 1% Y/Y mark as it has been doing all year long now. Simultaneously, Q2 GDP growth is expected to be confirmed at a solid 0.5% Q/Q. The Swiss National Bank already in March took conform of inflation being under control, allowing for a scaling down of policy rates. They followed-up on the action in June and we expect them to do so again in September. Despite their relatively early start and pace, the SNB desperately sees the Swiss franc strengthening further. Since the mid-July global market correction, EUR/CHF dived from 0.9750 to 0.9415 currently with a temporary stay below 0.93 early August. The relatively scarce SNB maneuvering room and the global swing towards less restrictive conditions suggest that CHF might remain stronger for longer and stronger than the SNB wants to. Brazilian GDP figures are worth watching as well tomorrow. Consensus expects another strong 0.9% Q/Q on the heels of 0.8% growth in Q1. Such outcome will cement rate hike expectations by the Brazilian central bank. It’s an example of what might be next if you achieve a perfect landing from a central bank point of view. Emerging markets were first to respond to the post-lockdown inflationary pressures, leading global central bank reaction functions by at least a year. The BCB started making policy less restrictive in July of last year. The current policy rate is 10.50% compared with a peak rate of 13.75% but way above the pre-pandemic 6.5% or 2020-2021 bottom of 2%. And the next move will be up instead of down. On Wednesday, we circle central bank policy meetings in Canada and Poland. The Bank of Canada is expected to implement its third consecutive 25 bps rate cut to 4.25%. We don’t think the central bank will be tempted into pushing through a larger 50 bps rate move as it would make the gap with Fed policy and key trading partner US too large. Ahead of the August market repositioning, USD/CAD was bumping into the 1.39 resistance area (weakest CAD-levels since 2003 with exemption of brief spells in 2015 & 2020). The National Bank of Poland will keep its policy rate steady at 5.75%. Apart from 100 bps stealth easing around the time of Polish election in September 2023, they stuck with restrictive policy settings unlike for example their Czech and Hungarian counterparts. NBP governor Glapinski for a while suggested that steady rates would last until at least the end of 2025. During summer, he started making an opening for a faster regime change. Upside inflation risks are subsiding and the reaction of Poland’s trading partners should also be kept in mind. Once the NBP officially changes its forward guidance, the Polish zloty could move away from the bottom to the top of this year’s EUR/PLN 4.25-4.40 trading range. Finally, on Thursday there’s a keynote speech by Reserve Bank of Australia governor Bullock to the Anika Foundation, a charity funded by money market participants. The RBA for now stuck with its peak policy rate of 4.35%, defying global cutting pressure. RBA members indicated that this could remain the case with inflation being a bit stickier than elsewhere. The central bank even remains vigilant to upside inflation risks, not ruling out another rate hike and calling thinking about RBA cuts as being premature. In light of recent strong labour market data and higher CPI, it will be interesting to see what tone Bullock’s speech has. AUD/USD is testing the recent highs near 0.68.

News & Views

The Turkish economy unexpectedly expanded by 0.1% q/q in Q2 of the year. That’s better than the 0.5% decline consensus was braced for but came along with a material downward revision to the Q1 figure from 2.4% to 1.4%. Turkish GDP is 2.5% larger compared to the same period last year, marking a slowdown from the outsized 5.3% in Q1 and missing a 3.2% estimate. The Turkish Statistical Institute noted household consumption increased by 1.6% y/y while that from the government rose by 0.7%. Capital investments were 0.5% higher y/y and a sharp -5.7% drop in imports vs flat exports resulted in a positive contribution from net exports after all. The economy treading water after a pre-election (March local elections), consumption-fueled Q1 suggests the more restrictive monetary policy is starting to filter through. With policy rates at 50% and inflation at >60%, real rates remain deeply negative though – even in case tomorrow’s inflation numbers print the expected major drop towards but still above 50%. That means there’s little room for the central bank to take its foot off the brake for the time being. The Turkish lira eked out a tiny gain against the dollar today. USD/TRY dips just south of the all-time highs around 34.

Graphs

AUD/USD: a vigilant RBA supporting the Aussie dollar

EUR/CHF: Swiss franc stronger for longer and stronger than SNB would like to see

USD/CAD: Loonie was testing multiyear lows ahead of August USD pullback on diverging monetary policy

EUR/PLN: a change of tone at the NBP can propel the pair from the bottom to the top of this year’s trading range

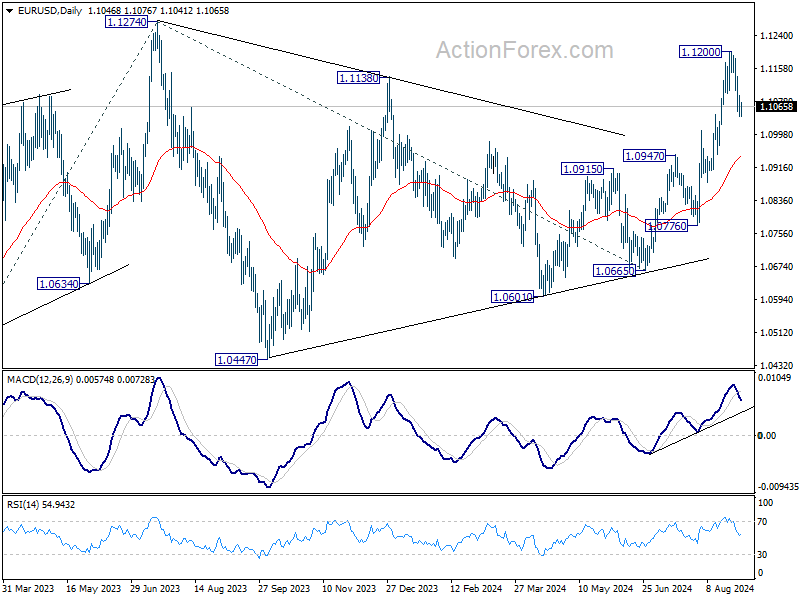

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1029; (P) 1.1062; (R1) 1.1080; More....

Intraday bias in EUR/USD stays neutral and outlook is unchanged. While retreat from 1.1200 might extend lower, rally from 1.0665 is in favor to continue as long as 1.0947 resistance turned support holds. Above 1.1104 minor resistance will bring retest of 1.1200 first. Break there will target 1.1274 high next.

In the bigger picture, prior break of 1.1138 resistance indicates that corrective pattern from 1.1274 has completed at 1.0665 already. Decisive break of 1.1274 (2023 high) will confirm whole up trend from 0.9534 (2022 low). Next target will be 61.8% projection of 0.9534 to 1.1274 from 1.0665 at 1.1740. This will now be the favored case as long as 1.0947 resistance turned support holds.

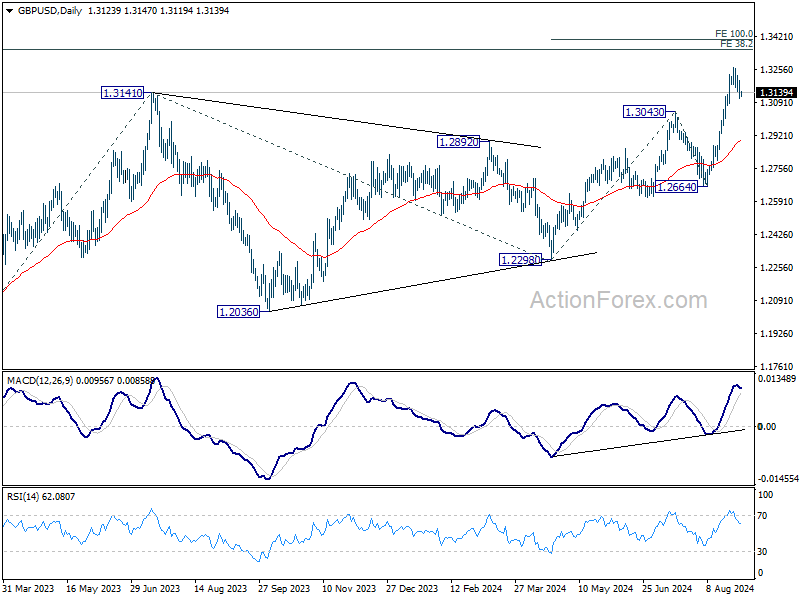

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3091; (P) 1.3145; (R1) 1.3181; More...

GBP/USD is staying in consolidation below 1.3265 and intraday bias remains neutral. While deeper retreat cannot be ruled out, downside should be contained well above 1.3043 resistance turned support to bring rebound. On the upside, above 1.3265 will resume larger up trend to 100% projection of 1.2298 to 1.3043 from 1.2664 at 1.3409.

In the bigger picture, up trend from 1.0351 (2022 low) is resuming. Next target is 38.2% projection of 1.0351 to 1.3141 from 1.2298 at 1.3364. For now, outlook will stay bullish as long as 1.2664 support holds, even in case of deep pullback.

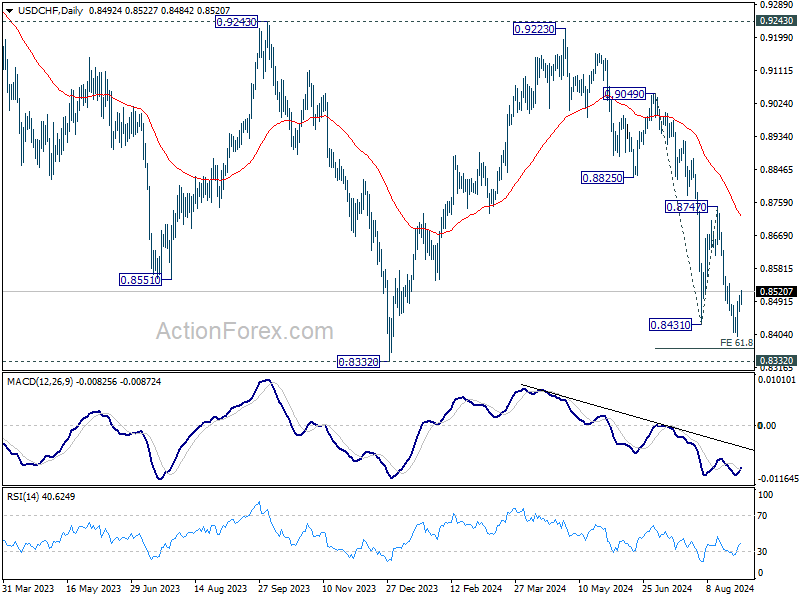

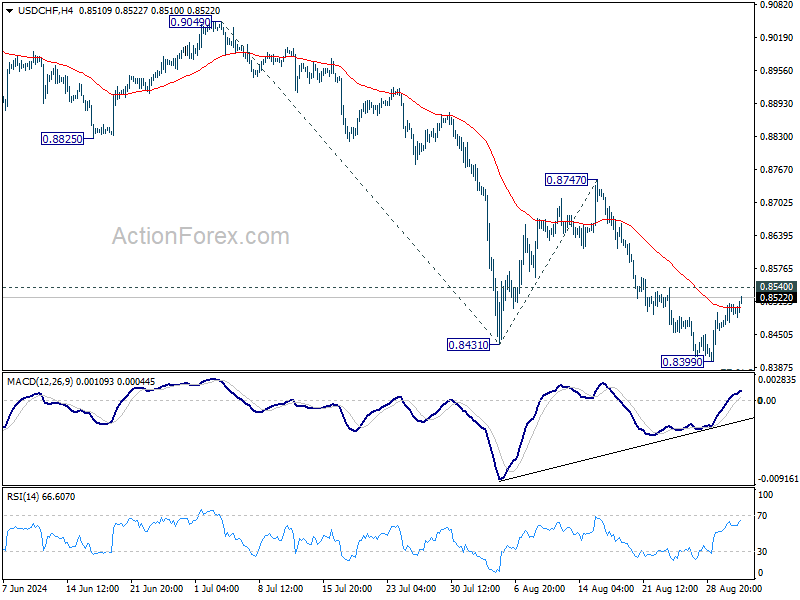

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8470; (P) 0.8491; (R1) 0.8520; More…

No change in USD/CHF's outlook and intraday bias stays neutral. More consolidations could be seen above 0.8399. Further decline is expected as long as 0.8540 resistance holds. Break of 0.8339 will target 61.8% projection of 0.9049 to 0.8431 from 0.8747 at 0.8365, and then 0.8332 low. However, considering bullish convergence condition in 4H MACD, firm break of 0.8540 will turn bias back to the upside for 0.8747 resistance instead.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).