Sample Category Title

Asian Markets Bounce Back; Eyes on Local Data, Not Just US CPI

- Asian equities extend rebound ahead of key data

- Japanese GDP, Aussie jobs and Chinese indicators on the agenda

- Any upsets could roil the fragile sentiment

A cautious rebound for stocks

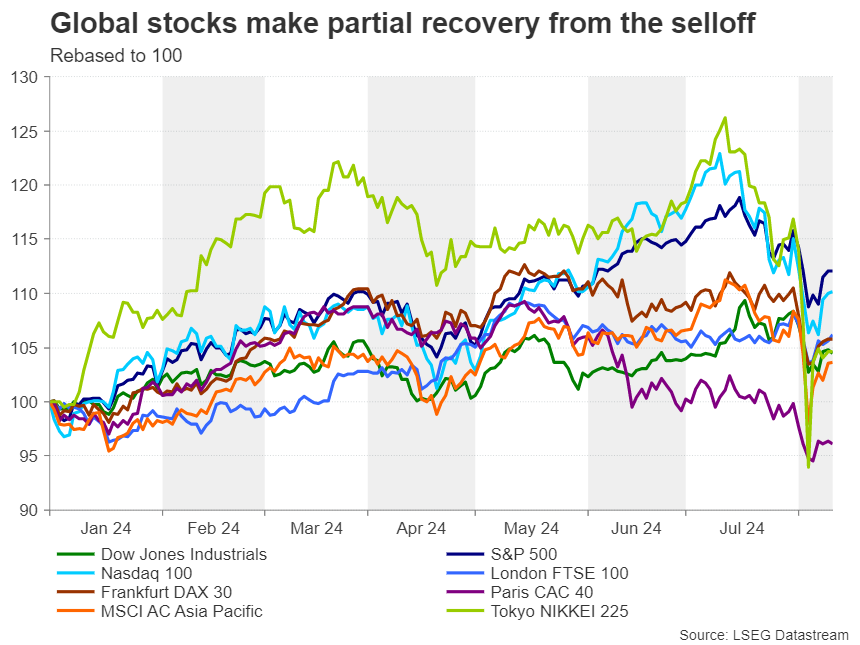

Stock markets in Asia have not been immune to the global selloff in August amid the unwinding of the yen carry trade and renewed fears about a US recession. Japanese stocks, in particular, were hit hard by the sudden surge in the yen; the Nikkei 225 Index tumbled by almost 20% between July 31 and August 5.

But a recovery is underway, with the Nikkei recouping about 50% of its losses, while the MSCI AC Asia ex Japan Index has gone a step further and reached the 61.8% Fibonacci retracement of its decline.

However, markets remain quite jittery and it’s been a cautious recovery, not just in Asia, but on Wall Street too. A lot is riding on the latest CPI and retail sales reports out of the US due on Wednesday and Thursday, respectively, to further calm market nerves. But it’s not just concerns about the US economy that’s weighing on risk sentiment.

Asian tigers no longer roaring

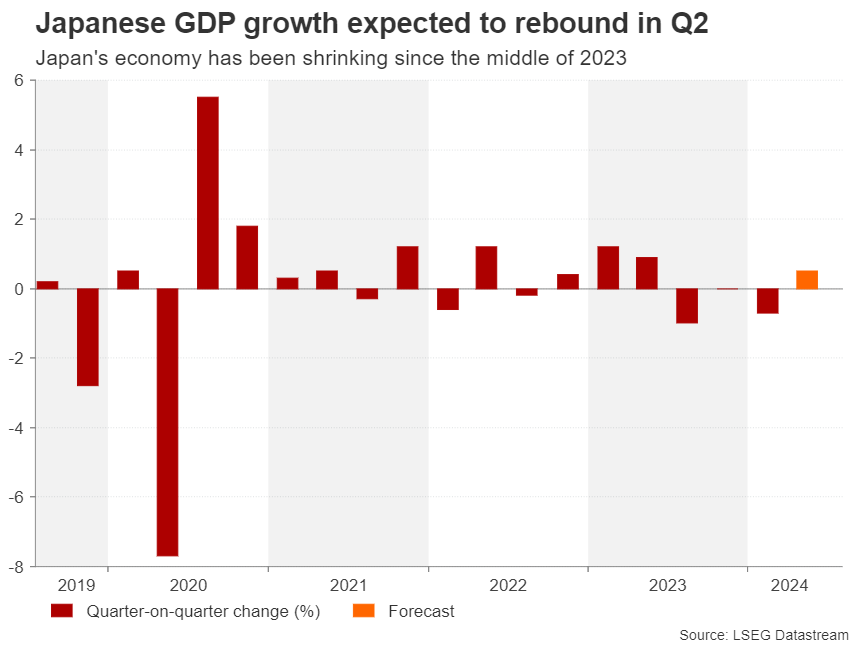

The Chinese economy seems to be stuck in a rut, while Japan’s economy has been shrinking since the third quarter of 2023. GDP figures for the latter are out on Wednesday (23:50 GMT) and analysts expect positive growth of 0.5% quarter-on-quarter for the second quarter.

An in-line or somewhat softer-than-projected reading would probably help ease concerns that the Bank of Japan is proceeding too rapidly with policy normalization, potentially boosting both the Nikkei and the yen. But a much stronger-than-expected rebound in GDP could spur a negative reaction as it would increase bets that the BoJ will hike interest rates again this year.

RBA’s next move more likely to be down

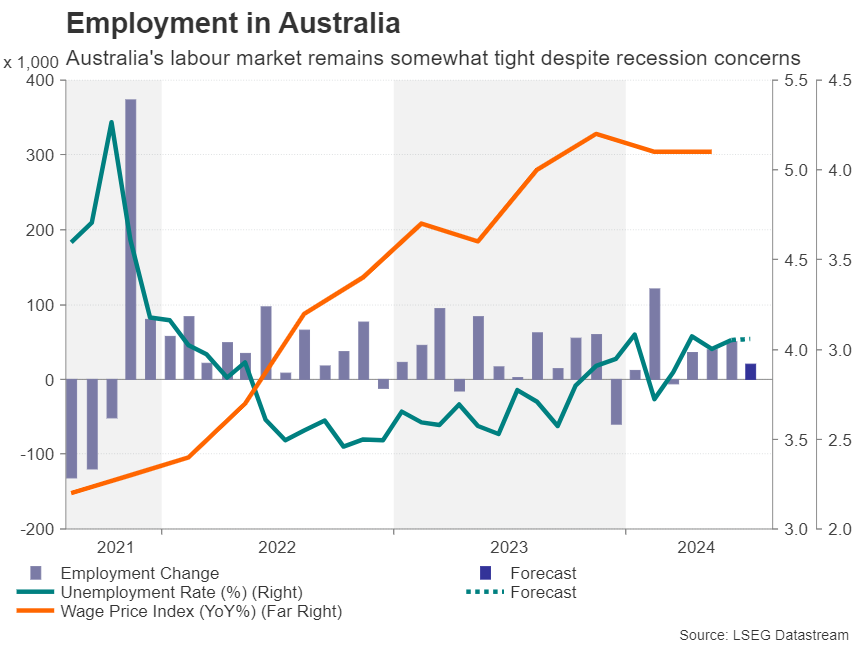

Next doing the rounds will be the Australian employment report on Thursday at 01:30 GMT. Australia’s labour market likely added 20k jobs in July, down from the prior 50.2k. The unemployment rate is expected to have held steady at 4.1%. Figures released earlier this week showed that wage growth was unchanged at a near historical high of 4.1% y/y in Q2, supporting the case for no rate cuts anytime soon.

Worries about the economy have kept the Reserve Bank of Australia on the sidelines despite persistently high inflation. But there’s been some progress more recently on reducing inflation and investors no longer see any chance of an RBA rate hike this year. That could easily change, though, if the jobs numbers point to an improving labour market.

Chinese consumers still not spending

The Australian dollar could certainly benefit from some upbeat data as it’s still down by about 9% against its US counterpart from its July peak. However, just as significant for the aussie will be China’s latest stats on industrial output and retail sales coming up 30 minutes later.

Although Chinese industrial production continues to grow at a satisfactory pace in spite of all the challenges, sluggish consumer spending poses a dilemma for authorities who seem opposed to big fiscal stimulus packages. Retail sales were up just 2.0% y/y in June and are expected to have picked up slightly to 2.6% y/y in July.

Risk of increased volatility

If the incoming data are mostly positive and contribute to brightening the market mood, the aussie, stocks and other risk assets could enjoy a further bounce back over the next few days, though the yen might suffer a pullback unless it can find support in the Japanese GDP numbers.

On the whole, it’s more likely that the data will add to the choppiness in the markets, amid all the uncertainties and thinner trading volumes during the peak summer holiday season, with the primary focus remaining on Fed expectations and US recession risks.

Sunset Market Commentary

Markets

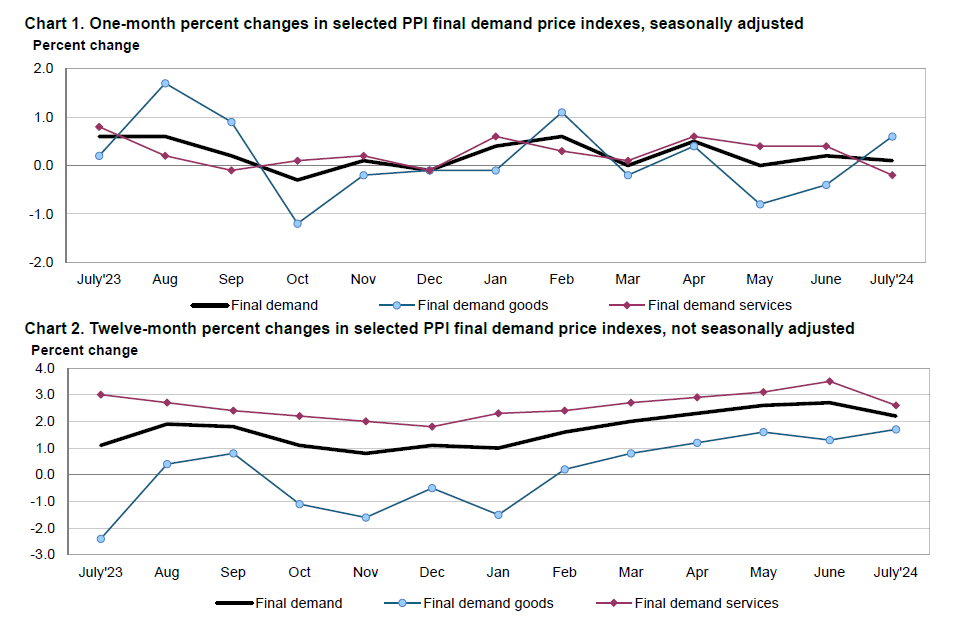

US producer price inflation rose by 0.1% M/M in July for the headline number and stabilized for the gauge excluding food and energy. Both were below consensus (+0.2% M/M), resulting in sharper-than-expected drops in the Y/Y-figures. Headline PPI printed at 2.2% from 2.7% and core PPI at 2.4% from 3%. Details showed a discrepancy between a first monthly drop in services costs this year (-0.2% M/M) and an acceleration in prices for goods driven by gasoline costs (+0.6% M/M). The PPI release triggered a small outperformance of US Treasuries with the front end of the curve outperforming. Markets argue that waning price pressures free up the hands of the Fed to respond to a slowing economy in September. The balance between taking off with a 25 bps or a 50 bps rate cut shifted from 50/50 ahead of PPI’s to 40/60 in favour of the larger move after the PPI’s. That contrasts with post July FOMC-speak suggesting that such larger cut is not something they are considering. US yields currently cede 4.1 bps (30-yr) to 6.5 bps (2-yr). Early last week’s lows remain out of reach for now though. German yields head south as well. Yields started drifting away after disappointing German ZEW investor sentiment (see News & Views) and trade 3 to 5 bps lower. EUR/USD initially lost out but recovered on USD weakness with the pair rebounding from an intraday low around 1.0915 to currently 1.0965. US stock markets open positively, rising by up to 1.15% for Nasdaq at the bell. At the time of finishing this report, Israeli reports of two Hamas rocket attacks against Tel Aviv are sparking some additional (risk-off) volatility. US officials yesterday already warned for retaliatory attacks after last week’s assassination of an Hamas leader in Tehran.

Solid UK labour market data helped sterling at the start of trading. EUR/GBP set an intraday low at 0.8531 from a start at 0.8563. Cable (GBP/USD) rose from 1.2770 to 1.2818. UK employment rose by 97k in the April-June quarter, beating 3k consensus. The first indication for Q3 (July payrolls) was better-than-hoped as well (+24k vs +10k expected). A significant increase in jobless claims (+135k in July) was the odd one out. Weekly earnings ex bonuses rose as expected by 5.4% annualized in Q2. UK Gilts initially underperformed, but eventually followed the global bond rally. Later this week, we’ll still see CPI data, Q2 GDP and retail sales

News & Views

German ZEW investor sentiment deteriorated significantly in August, falling from 41.8 to 19.2 (expectations component; lowest since January 2024). The assessment of the current situation was less bright as well, falling from -68.9 to -77.3. Both outcomes were below consensus. The ZEW institute in a comment warned that the German economic outlook is breaking down. In a global setback, especially the export-intensive German sectors are at risks. High uncertainty, driven by ambiguous monetary policy, disappointing business data from the US economy and growing concerns over an escalation of the conflict in the Middle East drive the pessimism.

The International Energy Agency expects world consumption to increase by just under 1mn barrels/day this year and next as growth is tempered by the subdued economic backdrop and a shift toward electric vehicles. That’s significantly below OPEC’s suggestion yesterday of 2.1mn b/d growth this year. The IEA believes that the oil market will move from deficit to surplus next quarter if OPEC+ proceeds with plans to boost supply. “For now, supply is struggling to keep pace with peak summer demand, tipping the market into a deficit,” the IEA said. “As a result, global inventories have taken a hit,” with stockpiles declining in June by 26.2 mn barrels.” Brent crude more or less holds to yesterday’s Middle-East tensions’ driven increase, trading at $81.5/b.

Graphs

GBP/USD: combination of GBP strength (UK labour market data) and USD weakness (PPI)

US 2-yr yield: money markets lift probability of 50 bps rate cut lift-off by the Fed from 50% to 60%

Brent crude: clings to gains related to Middle-East tensions in spite of more warnings of slowing oil demand growth

Nasdaq extends rebounds as slowing inflation frees the hands of the Fed to support a slowing economy

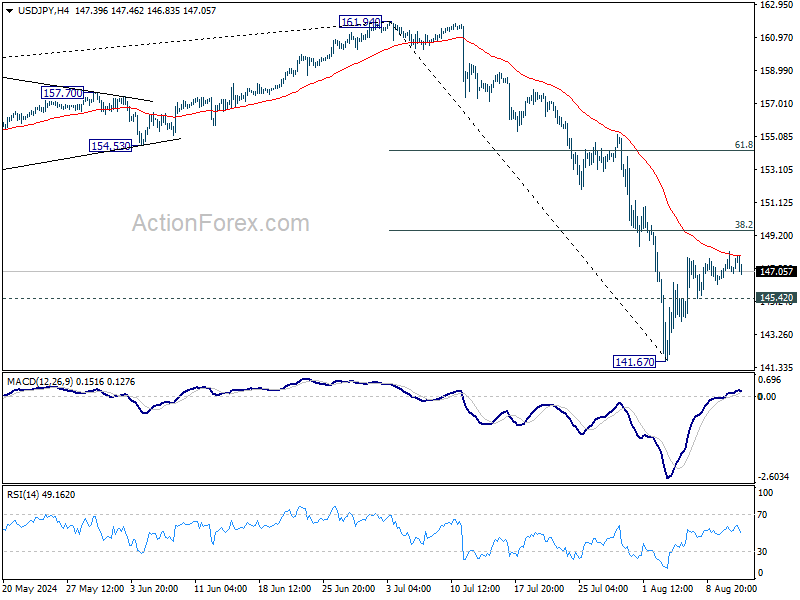

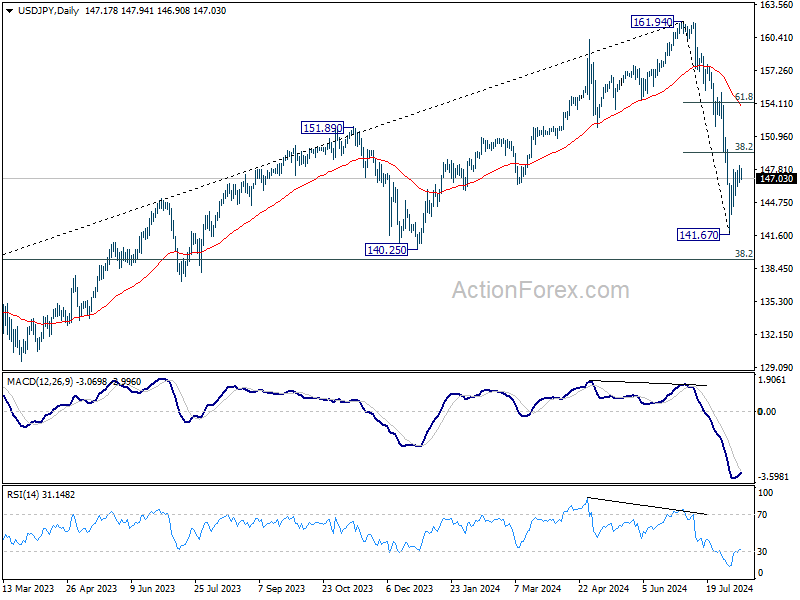

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 146.43; (P) 147.32; (R1) 148.11; More...

Intraday bias in USD/JPY stays neutral and outlook remains bearish with 38.2% retracement of 161.94 to 141.67 at 149.41 intact and intraday bias stays neutral. Below 145.42 minor support will turn bias to the downside for 141.67. Break there will resume the fall from 161.94 to 140.25 support next. Nevertheless, decisive break of 149.41 will bring stronger rally to 61.8% retracement at 154.19, even as a corrective move.

In the bigger picture, fall from 161.94 medium term is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.77) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

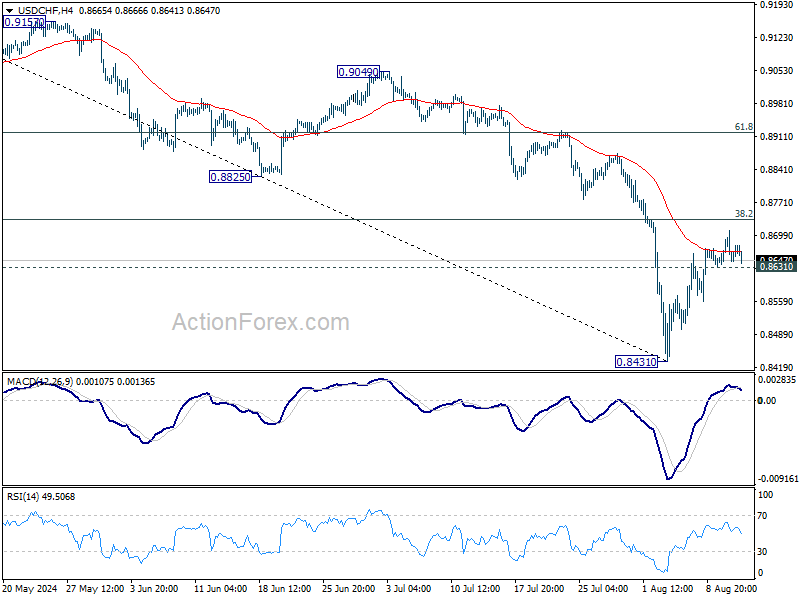

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8623; (P) 0.8667; (R1) 0.8697; More…

Intraday bias in USD/CHF stays neutral first. Outlook remains bearish with 38.2% retracement of 0.9223 to 0.8431 at 0.8734 intact. On the downside, below 0.8631 minor support will bring retest of 0.8431 first. Break there will resume the fall from 0.9223 to 0.8332 low. Nevertheless, firm break of 0.8734 will bring stronger rally to 61.8% retracement at 0.8920, even as a corrective move.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

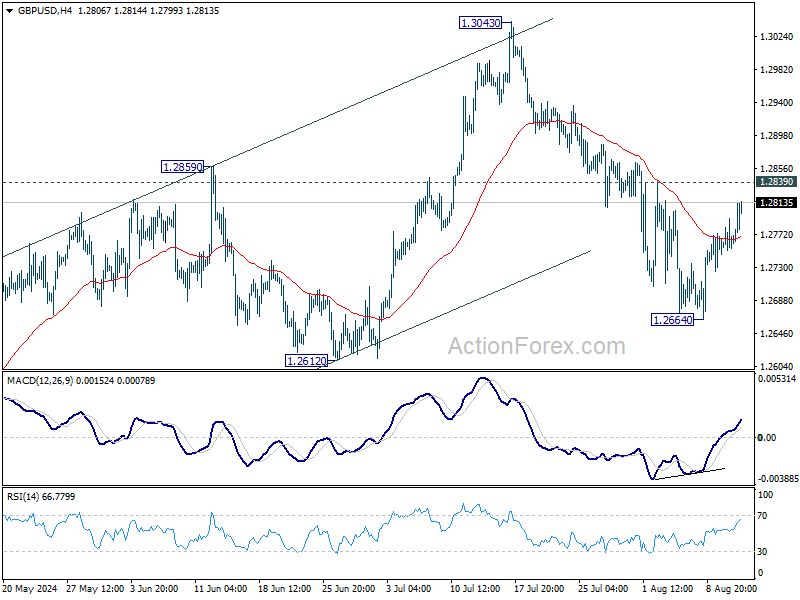

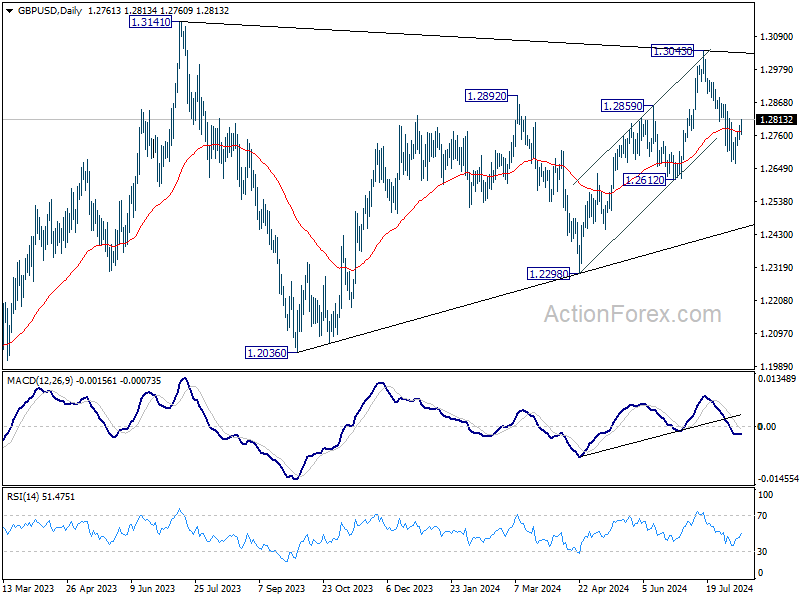

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2743; (P) 1.2769; (R1) 1.2790; More...

GBP/USD is still capped below 1.2839 resistance despite today's rally. Intraday bias stays neutral first. On the downside, break of 1.2664 will resume the fall from 1.3043 to 1.2612 support. Decisive break there should confirm that rise from 1.2298 has completed, and target this support next. However, break of 1.2839 resistance will argue that the pull back from 1.3043 has completed and turn bias back to the upside.

In the bigger picture, current development suggests that corrective pattern from 1.3141 is extending with fall from 1.3043 as another leg. Break of 1.2612 support would strengthen this case. But still, downside should be contained by 1.2036/2298 support zone even in case of deep decline. Rise from 1.0351 (2022 low) remains in favor to resume at a later stage.

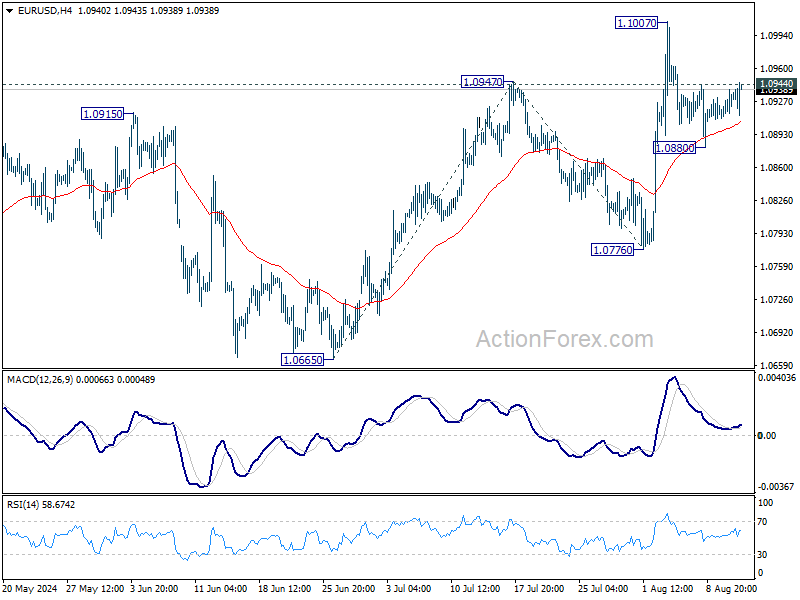

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0915; (P) 1.0927; (R1) 1.0944; More.....

Immediate focus is on 1.0944 minor resistance in EUR/USD. Firm break there will indicate that pullback from 1.1007 has completed at 1.0880 already. Retest of 1.1007 should be seen first. Further break there will resume rally from 1.0665 to 100% projection of 1.0665 to 1.0947 from 1.0776 at 1.1056 next. However, break of 1.0880 will bring another decline towards 1.0776 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0776 support will extend the correction with another falling leg back towards 1.0447 support.

Dollar Softens after PPI, Kiwi Strong Ahead of RBNZ

Dollar weakens broadly in early US session after July's PPI came in lower than expected, signaling easing in inflationary pressures. This development was well-received by investors, with stock futures ticking up slightly and 10-year Treasury yield dipping in response. While the softer PPI readings provide some relief to those hoping for monetary easing from Fed, the real test comes tomorrow with the release of CPI, which will play a decisive role in determining whether Fed moves towards a rate cut in September.

Kiwi is currently the strongest one for the day, as traders await tomorrow's RBNZ rate decision. The majority of the markets are expecting OCR to be unchanged out of the meeting. The central bank would use the new economic projections to lay down the groundwork for policy easing later in the year, either in November or earlier in October if needed. But that's not a total consensus. A significant minority have been betting on a rate cut. Kiwi could be given a pop should RBNZ deliver even a neutral hold.

Elsewhere in the currency markets, Sterling is following as the second strongest, as lifted slightly by today's job data. Swiss Franc is the worst performer, followed by Yen, and the Dollar. Euro and Canadian are positioning in the middle.

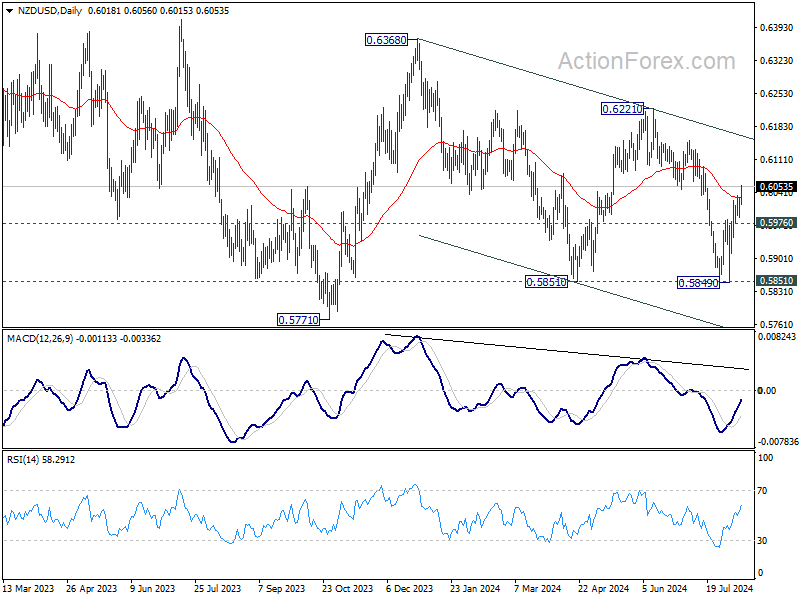

Technically, NZD/USD's strong break of 55 D EMA today should confirm that fall from 0.6221 has completed at 0.9849. Further rise is expected as long as 0.5976 support holds. Even just as a corrective move, NZD/USD should target falling trend line resistance (now at 0.6165) next.

In Europe, at the time of writing, FTSE is up 0.11%. DAX is up 0.26%. CAC is down -0.03%. UK 10-year yield is down -0.0203 at 3.900. Germany 10-year yield is down -0.032 at 2.201. Earlier in Asia, Nikkei rose 3.45%. Hong Kong HSI rose 0.36%. China Shanghai SSE rose 0.34%. Singapore Strait Times rose 0.72%. Japan 10-year JGB yield fell -0.0105 to 0.847.

US PPI at 0.1% mom, 2.2% yoy in Jul, below expectations

US PPI for final demand rose 0.1% mom in July, below expectation of 0.2% mom. PPI goods rose 0.6% while PPI services fell -0.2% mom. PPI less foods, energy, and trade services rose 0.3% mom.

For the 12 months ended in July, PPI rose 2.2% yoy, slowed from 2.7% yoy, below expectation of 2.3% yoy. PPI less foods, energy, and trade services rose 3.3% yoy.

German ZEW plummets to 19.2, economy breaking down

Germany's ZEW Economic Sentiment index took a significant hit in August, falling sharply from 41.8 to 19.2, well below the expected 30.6. This marks the steepest monthly decline since July 2022. Current Situation Index also worsened, dropping from -68.9 to -77.3.

Similarly, Eurozone's ZEW Economic Sentiment index fell from 43.7 to 17.9, missing expectations of 35.4. However, Current Situation Index for Eurozone showed a slight improvement, rising by 3.7 points to -32.4, although it remains in negative territory.

ZEW President Achim Wambach noted that the economic outlook for Germany is "breaking down." He highlighted that this month's survey revealed the sharpest decline in economic expectations over the past two years, not just for Germany, but also for the Eurozone, the US, and China.

Wambach pointed out that expectations for "export-intensive" sectors in Germany are particularly bleak. He attributed this deterioration to ongoing high uncertainty, driven by unclear monetary policy directions, disappointing business data from the US, and escalating concerns about the Middle East conflict.

UK payrolled employment grows 24k in Jul, unemployment rate falls to 4.2% in Jun

UK payrolled employment rose 24k or 0.1% mom in July. Median monthly pay increased by 5.6% up sharply from June's 3.8% yoy, but below May's 6.0% yoy. Claimant count jumped 135k versus expectation of 14.5k.

In the three months to June, unemployment fell from 4.4% to 4.2%, versus expectation of a rise to 4.5%. Average earnings including bonus rose 5.4% yoy, slowed from 5.7% but beat expectation of 4.6%. Average earnings excluding bonus slowed to 4.5% yoy, down from 5.7%, below expectation of 4.6%.

Japan's PPI rises to 3% yoy as Yen weakness fuels import costs surge

Japan's Producer Price Index rose by 3.0% yoy in July, aligning with market expectations and slightly up from June's 2.9% yoy increase. This marks the sixth consecutive month of acceleration and the fastest rate of increase in 11 months.

A significant driver of this rise was the 10.8% yoy increase in yen-denominated costs for imported materials, which accelerated from a revised 10.6% yoy rise in June. This highlights the ongoing impact of the weak Yen on import prices, contributing to higher overall production costs.

On a month-over-month basis, PPI rose by 0.3%, again matching consensus estimates.

Australia's wage growth slows in 0.8% qoq in Q2, with private sector lagging

Australia's wage price index rose by 0.8% qoq in Q2, slightly down from the previous quarter's 0.9% qoq increase and falling short of expectations for another 0.9% qoq rise. On an annual basis, wage growth remained steady at 4.1%, unchanged from Q1.

In the private sector, wage growth slowed to 0.7% qoq, down from 0.9% in the previous quarter. This marks the lowest increase for a second quarter since 2021 and ties for the lowest growth for any quarter since Q4 2021.

On the other hand, public sector wages grew by 0.9% qoq, up from 0.6% previously, making it the strongest June quarter increase since 2012. This stronger rise in the public sector was attributed to the newly synchronized timing of Commonwealth public sector agreement increases.

Australia's Westpac consumer sentiment edges up amid small relief over steady rates

Australia's Westpac Consumer Sentiment Index saw a modest increase of 2.8% mom in August, rising from 82.7 to 85.0. Westpac attributed this uptick to a "small sigh of relief" from consumers after RBA decided to keep interest rates unchanged, coupled with the positive effects of tax cuts and other fiscal measures.

However, despite the rise, the index remains historically weak, hovering within the 78–86 range that has persisted for over two years. Westpac's analysis highlighted ongoing concerns among consumers about the cost of living and potential future rate hikes, which continue to "weigh heavily" on sentiment.

Looking ahead to RBA's next meeting on September 23-24, Westpac noted that data flow leading up to the meeting is unlikely to provide significant new insights into inflation trends. With RBA having already ruled out near-term rate cuts, it is expected that the central bank will maintain its current interest rate at the upcoming meeting.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0915; (P) 1.0927; (R1) 1.0944; More.....

Immediate focus is on 1.0944 minor resistance in EUR/USD. Firm break there will indicate that pullback from 1.1007 has completed at 1.0880 already. Retest of 1.1007 should be seen first. Further break there will resume rally from 1.0665 to 100% projection of 1.0665 to 1.0947 from 1.0776 at 1.1056 next. However, break of 1.0880 will bring another decline towards 1.0776 support instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0776 support will extend the correction with another falling leg back towards 1.0447 support.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | PPI Y/Y Jul | 3.00% | 3.00% | 2.90% | |

| 00:30 | AUD | Westpac Consumer Confidence Aug | 2.80% | -1.10% | ||

| 01:30 | AUD | Wage Price Index Q/Q Q2 | 0.80% | 0.90% | 0.80% | 0.90% |

| 01:30 | AUD | NAB Business Conditions Jul | 1.00% | 4 | ||

| 01:30 | AUD | NAB Business Confidence Jul | 6 | 4 | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Jul | -2.10% | 9.70% | ||

| 06:00 | GBP | Claimant Count Change Jul | 135.0K | 14.5K | 32.3K | 36.2K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Jun | 4.20% | 4.50% | 4.40% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jun | 5.40% | 4.60% | 5.70% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jun | 4.50% | 4.60% | 5.70% | |

| 09:00 | EUR | Germany ZEW Economic Sentiment Aug | 19.2 | 30.6 | 41.8 | |

| 09:00 | EUR | Germany ZEW Current Situation Aug | -77.3 | -68.9 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Aug | 17.9 | 35.4 | 43.7 | |

| 10:00 | USD | NFIB Business Optimism Index Jul | 93.7 | 91.7 | 91.5 | |

| 12:30 | USD | PPI M/M Jul | 0.10% | 0.20% | 0.20% | |

| 12:30 | USD | PPI Y/Y Jul | 2.20% | 2.30% | 2.60% | 2.70% |

| 12:30 | USD | PPI ex Food & Energy M/M Jul | 0.00% | 0.20% | 0.40% | 0.30% |

| 12:30 | USD | PPI ex Food & Energy Y/Y Jul | 2.40% | 2.70% | 3.00% |

US PPI at 0.1% mom, 2.2% yoy in Jul, below expectations

US PPI for final demand rose 0.1% mom in July, below expectation of 0.2% mom. PPI goods rose 0.6% while PPI services fell -0.2% mom. PPI less foods, energy, and trade services rose 0.3% mom.

For the 12 months ended in July, PPI rose 2.2% yoy, slowed from 2.7% yoy, below expectation of 2.3% yoy. PPI less foods, energy, and trade services rose 3.3% yoy.

AUD/NZD: A Dovish RBNZ May Maintain Aussie Outperformance Over Kiwi

- New Zealand’s core inflation trend has decelerated at a faster pace than Australia.

- RBNZ may use tomorrow’s monetary policy meeting to offer dovish guidance and bring forward its projected first interest rate cut in H1 2025.

- A dovish hold by RBNZ may reinforce the continuation of the AUD/NZD medium-term bullish trend with key support at 1.0890/0840.

On Wednesday, 14 August, the New Zealand central bank, RBNZ will announce its monetary policy decision and issue its quarterly Monetary Policy Statement with fresh forecasts on growth, inflation, and monetary policy outlook.

The consensus is expecting RBNZ to maintain its official cash rate (OCR) steady again at 5.5% after it extended its rate pause for the eighth consecutive time in the July meeting where it peppered its July monetary policy statement with a dovish tilt that indicated the current high-interest rate environment in New Zealand had led to a decline in economic activities.

A possible dovish hold by RBNZ cannot be ruled out

In the previous quarterly Monetary Policy Statement released in May, the RBNZ signalled that the first interest rate cut in New Zealand would occur after Q2 2025.

However, given the latest lacklustre data on growth and inflationary trends in New Zealand, RBNZ is likely to relook at its monetary policy projection and may bring forward its first interest rate cut to the first half of 2025 as Q2 core inflation rate has declined significantly to 2.8% y/y from 3.7% y/y recorded in Q1, its slowest pace of growth in three years.

Hence, RBNZ may utilize Wednesday’s monetary policy meeting to offer guidance and lay the groundwork for an imminent interest cut cycle in New Zealand while maintaining its OCR unchanged at 5.5%.

New Zealand’s inflation trend is decelerating at a faster rate than Australia

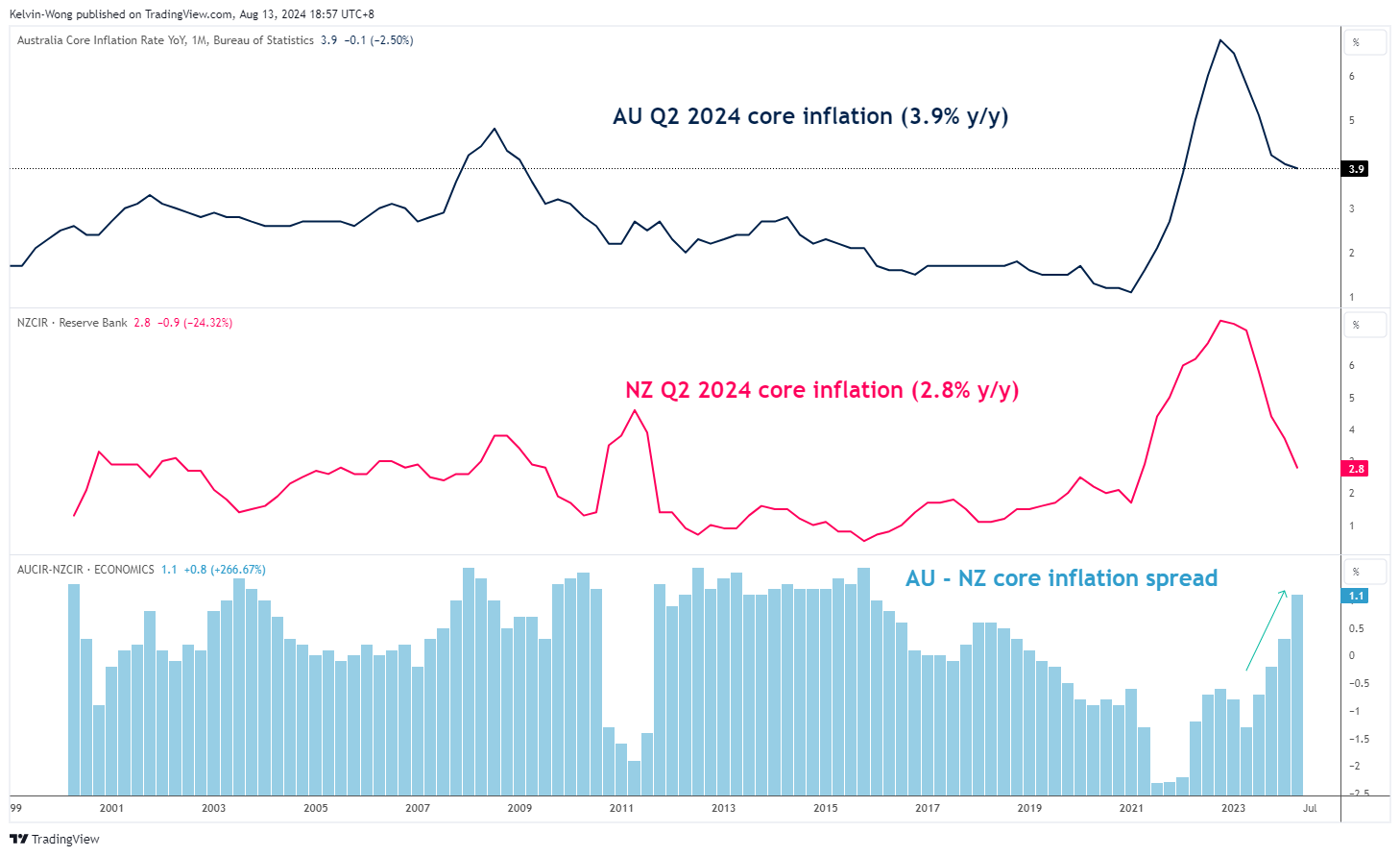

Fig 1: Australia & New Zealand core inflation trends as of Q2 2024 (Source: TradingView, click to enlarge chart)

The path of the inflationary trend is slightly different from the two Antipodeans. The Q2 core inflationary rate in Australia was still rather sticky as it recorded almost the same rate of growth as seen in Q1 (3.9% y/y vs. 4% y/y).

Therefore, the current picture of Australia and New Zealand’s inflationary environment is a stark contrast when we measure the difference between them; since Q2 2023, Australia’s core inflation rate has been decelerating at a slower pace than New Zealand’s core inflation rate (see Fig 1).

Therefore, this difference in inflationary trends supports a further potential RBNZ dovish monetary policy guidance which in turn may trigger an outperformance of the Aussie dollar over the Kiwi.

The recent slide in AUD/NZD managed to find support at the key 200-day moving average

Fig 2: AUD/NZD major and medium-term trends as of 13 Aug 2024 (Source: TradingView, click to enlarge chart)

The recent decline of 2.80% from its 17 July 2024 swing high area of 1.1165/1190 has managed to stall at a key medium-term pivotal support at 1.0890/0840 (also the 200-day moving average).

In addition, the price actions of the AUD/NZD cross pair have started to oscillate within a medium-term ascending channel since the 22 February 2024 low of 1.0570 (see Fig 2).

A clearance above 1.1030 intermediate resistance may see a retest on the 1.1165/1190 medium-term resistance in the first step.

However, a breakdown below 1.0840 invalidates the recovery scenario to expose the next medium-term support at 1.0735.