Sample Category Title

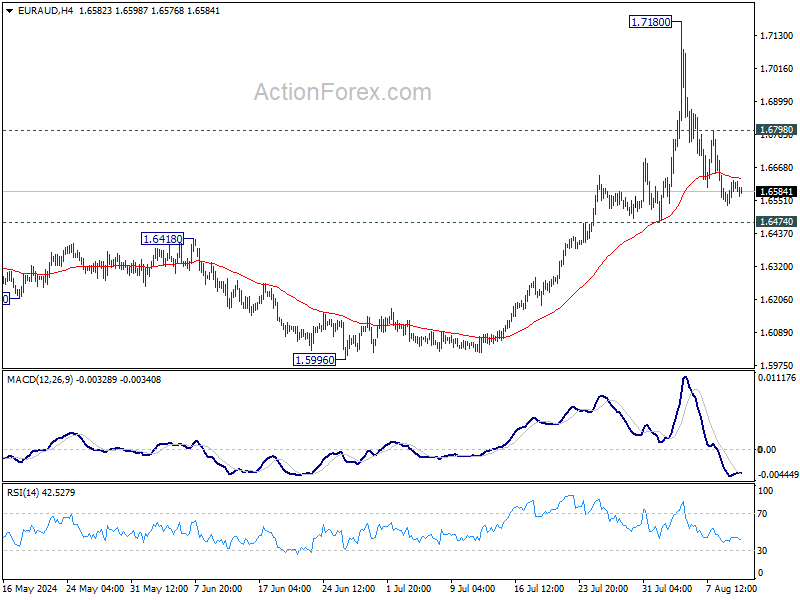

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6555; (P) 1.6589; (R1) 1.6642; More...

Intraday bias in EUR/AUD remains neutral for the moment. Outlook is staying bullish with 1.6474 support intact. On the upside, above 1.6798 minor resistance will bring retest of 1.7180 resistance first. Firm break there will resume larger up trend to 1.7715 fibonacci projection level next.

In the bigger picture, corrective fall from 1.7062 medium term top should have completed at 1.5996. Larger up trend from 1.4281 (2022 low) is resuming. Next target is 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. This will now remain the favored case as long as 1.6474 support holds.

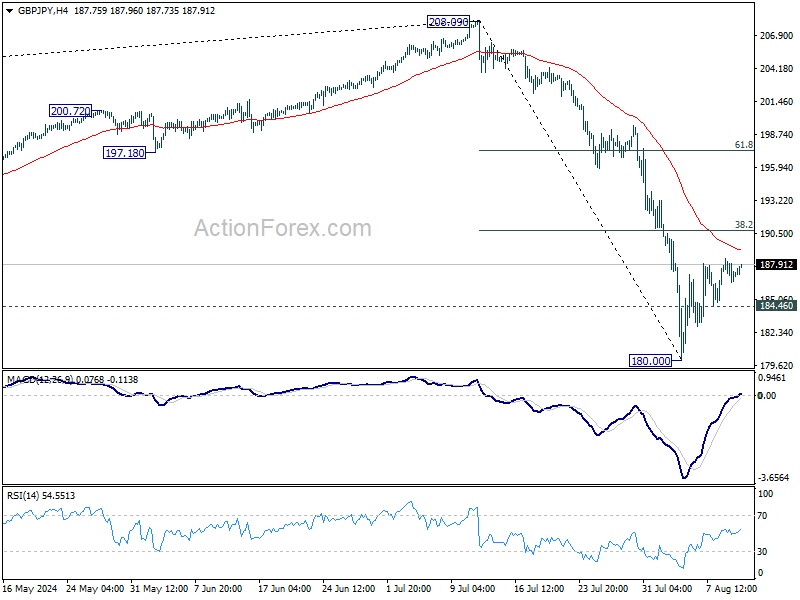

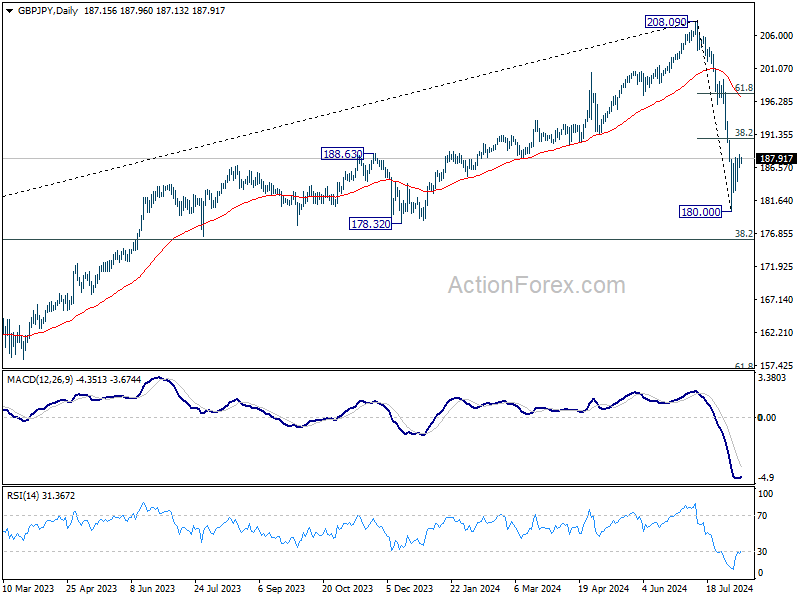

GBP/JPY Daily Outlook

Daily Pivots: (S1) 186.17; (P) 187.30; (R1) 188.12; More...

Intraday bias in GBP/JPY remains neutral for the moment. While recovery from 180.00 might extend higher, outlook will stay bearish as long as 38.2% retracement of 208.09 to 180.00 at 190.73 holds. On the downside, below 184.46 minor support will turn intraday bias back to the downside for retesting 180.00 low. Break there will resume the fall from 208.90 to 178.32 support next. However, firm break of 190.73 will extend the rebound to 61.8% retracement at 197.35, even as a corrective move.

In the bigger picture, fall from 208.09 medium term top is seen as correcting the up trend from 123.94 (2020 low). Deeper decline is in favor as long as 55 W EMA (now at 189.18) holds. But strong support could emerge between 178.32 and 38.2% retracement of 123.94 to 208.09 at 175.94 to bring rebound. Meanwhile, sustained trading above 55 W EMA will suggest that the range for the medium term corrective pattern is already set.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.49; (P) 160.44; (R1) 161.05; More...

Intraday bias in EUR/JPY stays neutral for the moment. While recovery from 154.40 might extending, outlook will remain bearish as long as 38.2% retracement of 175.41 to 154.40 at 162.42 holds. On the downside, below 157.71 minor support will bring retest of 154.40 first. Break there will resume the fall from 175.41 to 153.15 support next. However, sustained break of 162.42 will bring strong rise to 61.8% retracement at 167.38, even as a corrective move.

In the bigger picture, fall from 175.41 medium term top should be correcting the whole rise from 114.42 (2020 low). Deeper decline could be seen as long as 55 W EMA (now at 161.88) holds. But strong support should emerge between 153.15 and 38.2% retracement of 114.42 to 175.41 at 152.11 to bring rebound, at least on first attempt. Meanwhile, sustained trading above 55 W EMA will argue that the range of the medium term corrective pattern has already been set.

Quiet Forex Start Masks Anticipation of US CPI-Driven Volatility

The forex markets have started the week on a subdued note, typical of a Monday morning in Asia, particularly with Japan on holiday. Yen remains in a consolidation phase, holding steady after its recent gains and staying as the strongest currency this month so far. Swiss Franc is not far behind, ranking as the second. This picture reflects the persistent caution in the market. The preference for these safe-haven currencies underscores the vulnerability in risk sentiment.

However, this calm is unlikely to last. Market participants are gearing up for a surge in volatility later in the week, driven by US CPI data. Recent sharp selloff in stock markets has amplified calls for Fed to ease its monetary policy sooner rather than later. Some analysts are even speculating about the possibility of a more significant rate cut in September. Nonetheless, if CPI data surprises to the upside, it could put the Fed in a tough position, trapped between the need to control inflation and the risk of exacerbating recession fears. Such a scenario could heighten market anxiety, leading to further turbulence across financial markets.

Meanwhile, the British Pound is struggling, currently the weakest performer among the major currencies this month. Pound's decline comes at a time when BoE's MPC is deeply divided on the path forward. This week's economic data releases will be crucial in providing guidance on whether the MPC will continue with interest rate cuts in the near future. Dollar is not faring much better, positioned as the second weakest currency this month, just ahead of Canadian Dollar. Meanwhile, Euro, Australian Dollar, and New Zealand Dollar are trading in the middle of the spectrum.

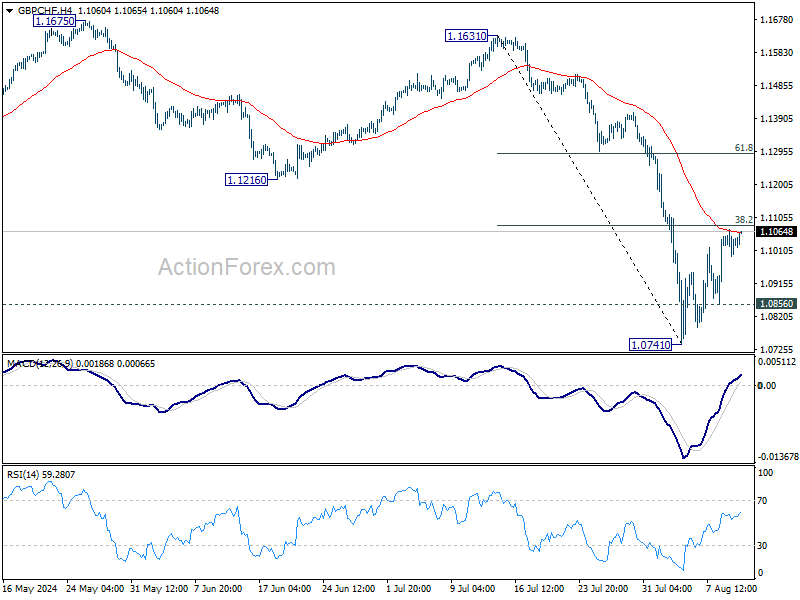

Technically, GBP/CHF's recovery from 1.0741 is so far capped by 55 4H EMA as well as 38.2% retracement of 1.1631 to 1.0741 at 1.1108. Larger fall from 1.1675 is still expected to continue. Below 1.0856 minor support will argue that this decline is ready to resume through 1.0741 towards 1.0634 (2023 low). Nevertheless, firm break of 1.1108 will bring stronger rebound back to 1.1216 support turned resistance or above. The direction of this movement will likely become clearer as the week progresses, particularly with the release of key economic data.

In Asia, Japan is on holiday. Hong Kong HSI is up 0.18%. China Shanghai SSE is up 0.13%. Singapore Strait Times is down -0.82%.

Fed's Bowman underlines priority on price stability

Fed Governor Michelle Bowman noted during a Saturday event that her "baseline" expectation is for inflation to decline further under the current policy stance. She added that if incoming data shows inflation moving sustainably toward the 2% target, it could become appropriate to "gradually lower the federal funds rate." This would prevent monetary policy from becoming "overly restrictive" on economic activity and employment.

However, Bowman stressed that monetary policy is "not on a preset course," with decisions to be guided by data. By the time of Fed's September meeting, the committee will have additional economic data, including one employment and two inflation reports, as well as a broader view of financial conditions.

She acknowledged that while equity prices have been "volatile" recently, they remain "still higher than at the end of last year," indicating resilience in financial markets.

Despite some progress, Bowman expressed concerns that inflation remains "somewhat elevated" with "some upside risks." She emphasized the need to "pay close attention to the price-stability side of our mandate," while also monitoring for any significant weakening in the labor market.

RBNZ to hold, US CPI in spotlight with UK data

RBNZ is at the forefront this week, expected to keep its Official Cash Rate steady at 5.50%. Despite recent speculations of an early rate cut at this meeting, the central bank seems poised to hold off on easing for now. Instead, the spotlight will be on the Monetary Policy Statement, where new economic projections could lay the groundwork for policy easing later in the year.

Currently, November is seen as the most likely month for RBNZ to initiate the policy loosening cycle, but there's a possibility that the timeline be brought forward to October if economic conditions warrant. The economic projections would hopefully provide clarity on these questions.

In the US, focus is squarely on July CPI and retail sales data. With a September rate cut by Fed already fully priced into the market, the debate now centers on the magnitude of this cut. Fed officials appear well-prepared for a reduction in rates, but the question remains: will incoming data warrant a 25 basis point cut, or will Fed need to take more aggressive action with a 50 basis point reduction?

The key factors here are inflation and consumer spending. Should inflation slow significantly and consumption weaken, the case for a larger cut strengthens. Conversely, if the data merely meets expectations without major surprises, Fed may stick to a more modest adjustment. The prospect for a total of 75 basis points in cuts by the end of the year is on the table, though some analysts are even contemplating a full percentage point reduction if the economy shows further signs of distress.

Across the Atlantic, the UK is bracing for a flurry of important economic data, including GDP, employment figures, CPI, and retail sales. BoE recent decision to cut interest rates was a close call, with a narrow 5-4 vote. Notably, Chief Economist Huw Pill dissented, underscoring the division within the MPC.

A rebound in July CPI in the UK, coupled with slowdown in Q2 GDP growth, would present the MPC with a complex dilemma. On one hand, resurgence of inflation pressures might argue for a pause in further rate cuts, while on the other, slowing economic growth could push the MPC to continue its easing cycle. The coming data will be critical in determining the BoE's next steps, as the central bank seeks to balance the conflicting signals from the economy.

In Asia Pacific, Japan's Q2 GDP data is expected to reveal a strong rebound driven by consumption. However, BoJ faces limited room for continuing with rate hikes, especially if global financial markets remain unstable. In Australia, employment data will be under scrutiny, alongside key economic indicators from China, including industrial production, retail sales, and fixed asset investment.

Here are some highlights for the week:

- Monday: Canada building permits.

- Tuesday: Japan PPI; Australia Westpac consumer sentiment, NAB business confidence wage price index, UK employment; German ZEW economic sentiment; US PPI.

- Wed: RBNZ rate decision; UK CPI, PPI; Eurozone GDP revision, industrial production; US CPI.

- Thursday: Japan GDP; Australia employment; China industrial production, retail sales, fixed asset investment; UK GDP, production, trade balance; Swiss PPI; Canada wholesale sales; US retail sales, jobless claims, Philly Fed survey, Empire State manufacturing, import prices, industrial production, business inventories, NAHB housing index.

- Friday: Japan tertiary industry index; UK retail sales; Eurozone trade balance; Canada housing starts, manufacturing sales; US building permits and housing starts; U of Michigan consumer sentiment.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 159.49; (P) 160.44; (R1) 161.05; More...

Intraday bias in EUR/JPY stays neutral for the moment. While recovery from 154.40 might extending, outlook will remain bearish as long as 38.2% retracement of 175.41 to 154.40 at 162.42 holds. On the downside, below 157.71 minor support will bring retest of 154.40 first. Break there will resume the fall from 175.41 to 153.15 support next. However, sustained break of 162.42 will bring strong rise to 61.8% retracement at 167.38, even as a corrective move.

In the bigger picture, fall from 175.41 medium term top should be correcting the whole rise from 114.42 (2020 low). Deeper decline could be seen as long as 55 W EMA (now at 161.88) holds. But strong support should emerge between 153.15 and 38.2% retracement of 114.42 to 175.41 at 152.11 to bring rebound, at least on first attempt. Meanwhile, sustained trading above 55 W EMA will argue that the range of the medium term corrective pattern has already been set.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 12:30 | CAD | Building Permits M/M Jun | 5.60% | -12.20% |

Research Japan: Hawkish BoJ Keen on More Hikes

- The BoJ has taken up a much more aggressive strategy and we no longer expect them to wait for all the pieces to fall in place before tightening policies further.

- We expect the BoJ will hike its policy rate to 1% within the coming 12 months.

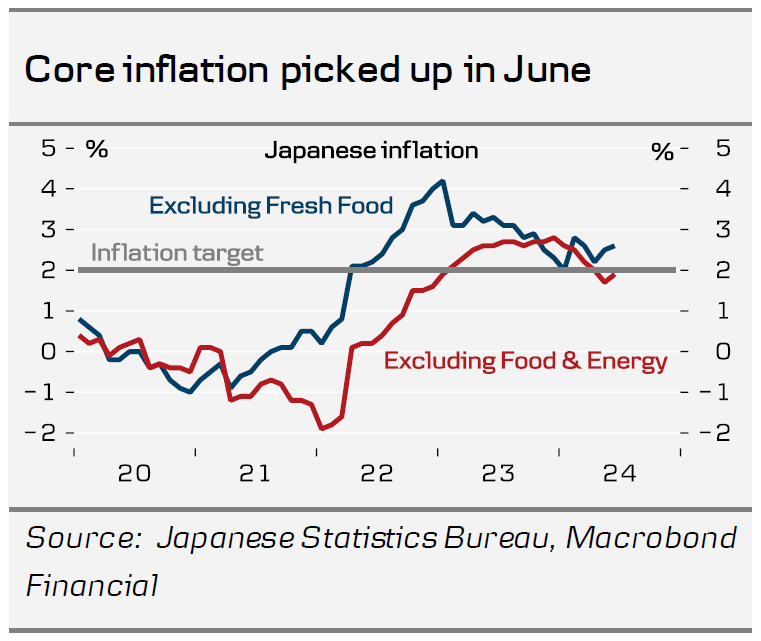

The rate hike on 31 July was pivotal for how we see the Bank of Japan (BoJ) moving forward. On the press conference following the meeting, Governor Ueda had turned much more hawkish and the building of an economic momentum fostering 2% selfsustained inflation no longer seems to be the only thing that matters. Instead, the yen has taken centre stage. Earlier, FX moves was just one of many parameters, the BoJ monitored when gauging inflation momentum and it was never the key factor. An obvious example of this was the Friday 26 April policy meeting, when a dovish governor Ueda did not pay much attention to a very weak yen. As a result, USD/JPY tested 160 the following Monday and the Ministry of Finance ordered the BoJ to step in to prop up the yen. Now Ueda says, "FX moves are more likely to affect inflation than before". So why this turnaround? The BoJ has intervened for USD161 billion since they stepped in for the first time in September 2022. It is a costly affair to defend the yen and intervention was probably never meant to be a long-term solution.

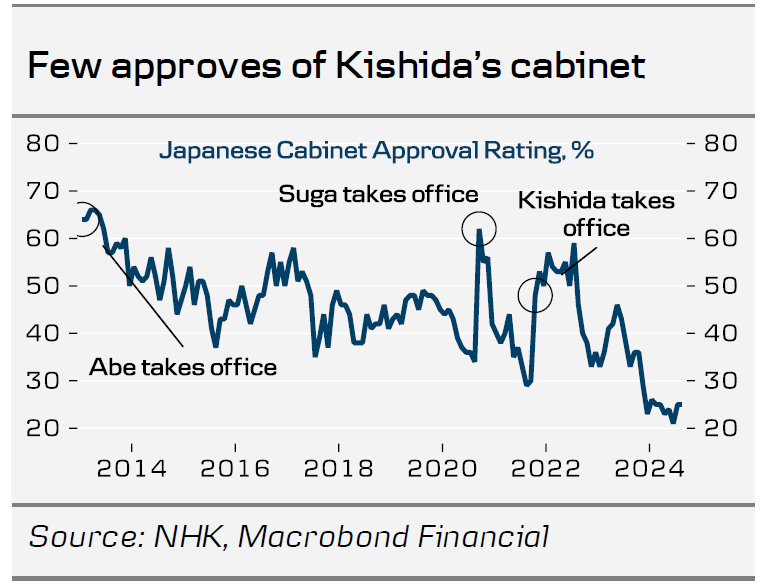

The hawkish turnaround should perhaps also be viewed in the light of a very low approval rating for PM Kishida and his cabinet. Just 25% approved in August, below the so-called danger level of 30%, an uncomfortable situation for Kishida considering recent history and the upcoming Liberal Democratic Party leadership election in September. Excluding Shinzo Abe's eight-year reign from 2012-2020, the last seven prime ministers have only had about one year in power.

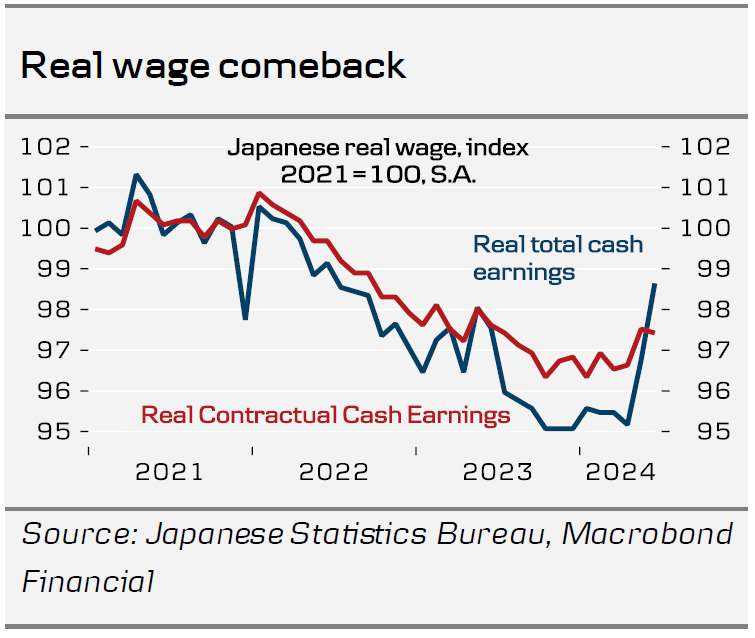

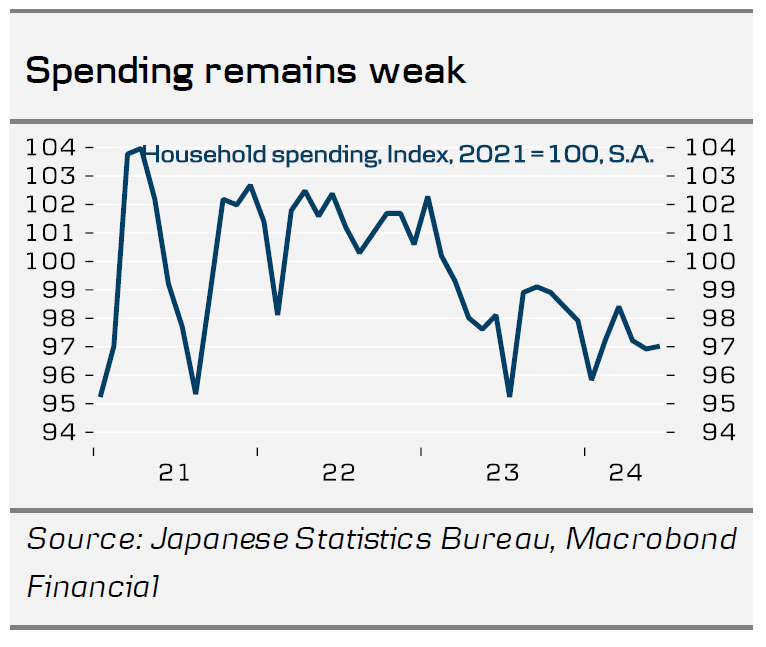

A very weak currency is usually not popular with the public and in Japan it creates quite visible inflation due to the status as a major energy importer. Gasoline for instance costs JPY175 per litre now, which is about JPY25-30 more than pre-pandemic levels. That is a big price increase in 4-5 years. Back in May, a poll from the private think tank, Teikoku Databank, showed 64% of companies see the weak yen as having a negative impact on their profits. Afterall, most Japanese companies are not in a position to exploit the advantages of a weak currency on export markets but only experience the flip side, which is higher import costs. About half of the respondents saw USD/JPY at 110-120 as an appropriate level. Largely, a weak currency benefits major exporters at the expense of consumers. That process can create inflation but will be painful for consumers until business profits are passed on to employees. We have seen the beginning of that process with the spring wage increases and real earnings recovered most of the lost purchasing power from 2021, in Q2. A lot of the June pay increases are one-off payments, though, and growth in real contractual cash earnings remains modest. The reality for most consumers is still that much of their purchasing power has been eroded and that is also key to understand why real household spending was still down 1.4% yoy in June.

If the long-term goal to sustainably reach the inflation target was the only game in town, we think this would bode for a cautious approach, and hiking rates again only when private spending shows signs of picking up. It seems, however, that the BoJ has come under pressure to incorporate the yen more explicitly in its policy decisions. Even if household spending shows only modest improvement, we expect the BoJ to hike by another 25 bps this year followed by another 25bps in Q1 and Q2. Given the recent global, and particularly Japanese, market turbulence, we expect the BoJ will be a bit more cautious at the fall policy meetings, though. This is based on our expectation that investors' Fed pricing is too aggressive and US treasury yields will trade higher again, adding some renewed headwinds for the yen.

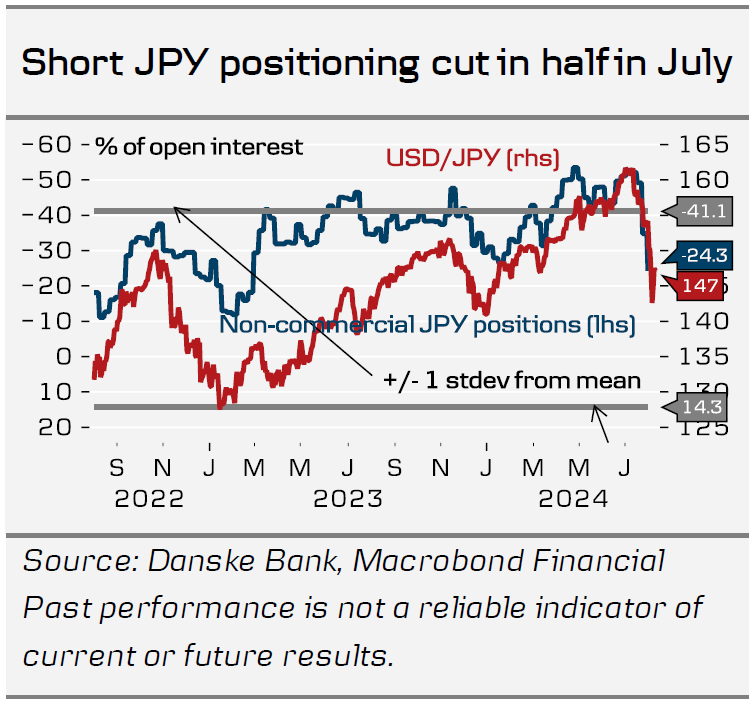

US outlook remains key for the yen

As mentioned above, USD/JPY has experienced some extreme swings over the summer, resulting in notable JPY appreciation. Since 1 July, the JPY has strengthened by around 10% against the USD, pushing USD/JPY below 150. Several factors have supported the Japanese currency, including a massive unwinding of carry trades, lower US rates, declining oil prices, more strategic Japanese FX intervention, and a hawkish hike from the BoJ. The prospect of narrowing rate differentials between Japan and other G10 economies is currently a significant tailwind for the JPY, making it the clear outperformer in the G10 space. It seems that global factors have a greater influence on the JPY than domestic developments in Japan. Consequently, whether the BoJ hikes 1-3 more times over the coming year may not impact USD/JPY as much as changes in US yields or oil prices. We believe there is further room for decline in USD/JPY over the strategic horizon and remain bearish on the cross. If we are heading for more volatile times, the carry trade will lose its attractiveness, as evidenced by the halving of short JPY positions in July. Additionally, the tail risk of a US recession, which could force the Fed to lower rates quickly and aggressively, might prompt USD/JPY to decline sharply, even if the BoJ stops further hikes. However, in the near term, with the recent strong rally, we could see a temporary reversal as we expect the dovish repricing of the Fed to reverse. With USD/JPY having already dipped to 141.70 last week before bouncing back above 145.00, we suspect the market will remain in "sell rallies" mode if there is a significant bounce, even if risk assets manage to sustain a rebound. Overall, we see USD/JPY declining below 145 on a 12-month horizon.

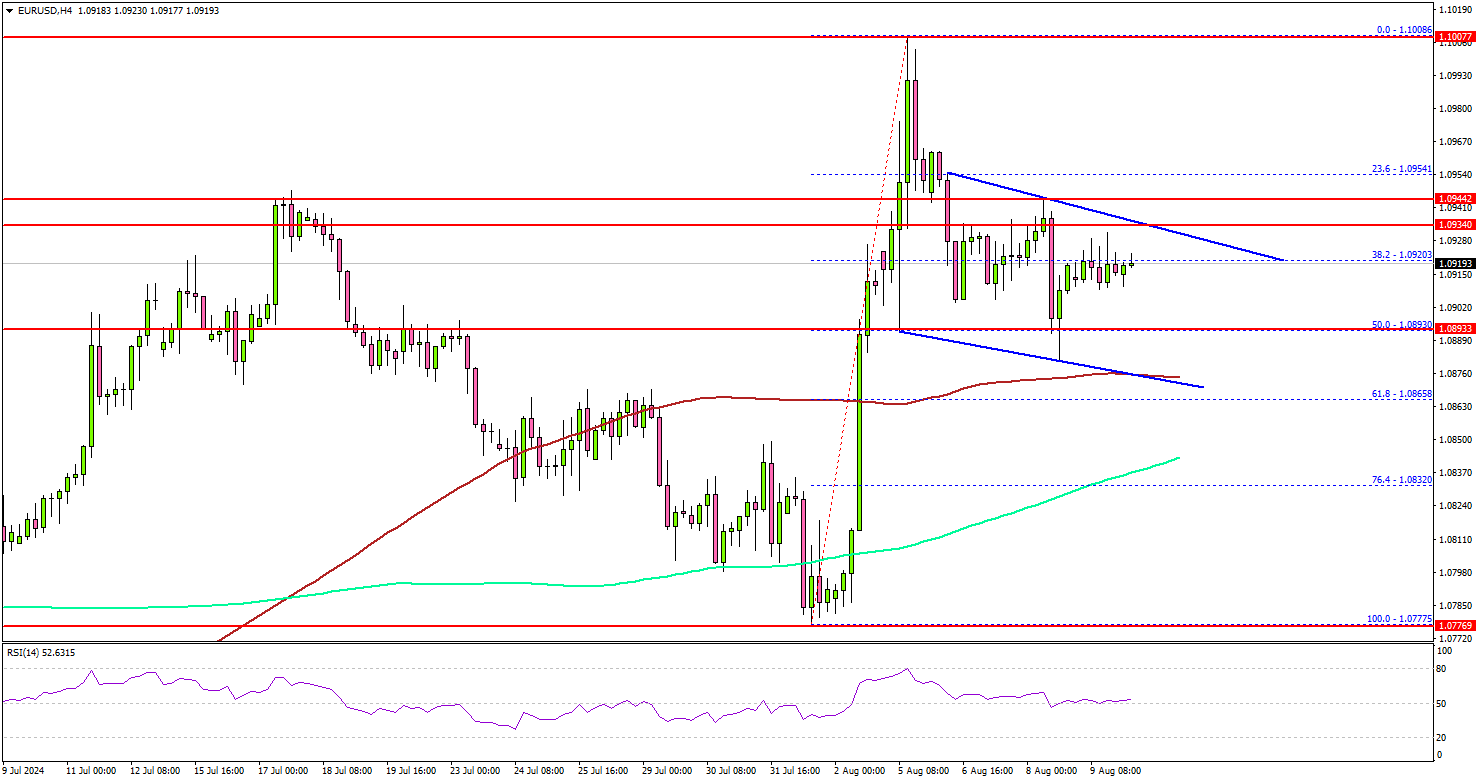

EUR/USD Looks Upward: Is A Breakout Imminent?

Key Highlights

- EUR/USD is aiming for a fresh increase above the 1.0930 resistance.

- A key declining channel is forming with resistance at 1.0925 on the 4-hour chart.

- GBP/USD is eyeing a recovery wave above the 1.2800 resistance zone.

- Oil prices are gaining pace for a move above the $77.00 resistance.

EUR/USD Technical Analysis

The Euro started a downside correction from the 1.1000 resistance zone against the US Dollar. EUR/USD could start another increase if it clears the 1.0950 resistance.

Looking at the 4-hour chart, the pair remained stable above the 1.0850 level, the 200 simple moving average (green, 4-hour), and the 100 simple moving average (red, 4-hour). The pair tested the 50% Fib retracement of the upward move from the 1.0777 swing low to the 1.1008 high.

The pair is now consolidating near the 1.0920 level. There is also a key declining channel forming with resistance at 1.0925 on the same chart.

Immediate resistance sits near the 1.0925 level. The next resistance sits at 1.0950. A clear move above 1.0950 could open the door to more gains. In the stated case, the pair could rise and test 1.1000. Any more gains could send the pair toward the 1.1050 level.

Immediate support is near the 1.0885 level. The next major support is near the 1.0850 level. A downside break and close below the 1.0850 support zone could open the doors for more losses. In the stated case, EUR/USD might decline toward the 1.0780 level.

Looking at Oil, the price started a recovery wave above the $76.50 level but the bears might remain active near the $77.50 level.

Economic Releases

- US Monthly Budget Statement.

Fed’s Bowman underlines priority on price stability

Fed Governor Michelle Bowman noted during a Saturday event that her "baseline" expectation is for inflation to decline further under the current policy stance. She added that if incoming data shows inflation moving sustainably toward the 2% target, it could become appropriate to "gradually lower the federal funds rate." This would prevent monetary policy from becoming "overly restrictive" on economic activity and employment.

However, Bowman stressed that monetary policy is "not on a preset course," with decisions to be guided by data. By the time of Fed's September meeting, the committee will have additional economic data, including one employment and two inflation reports, as well as a broader view of financial conditions.

She acknowledged that while equity prices have been "volatile" recently, they remain "still higher than at the end of last year," indicating resilience in financial markets.

Despite some progress, Bowman expressed concerns that inflation remains "somewhat elevated" with "some upside risks." She emphasized the need to "pay close attention to the price-stability side of our mandate," while also monitoring for any significant weakening in the labor market.

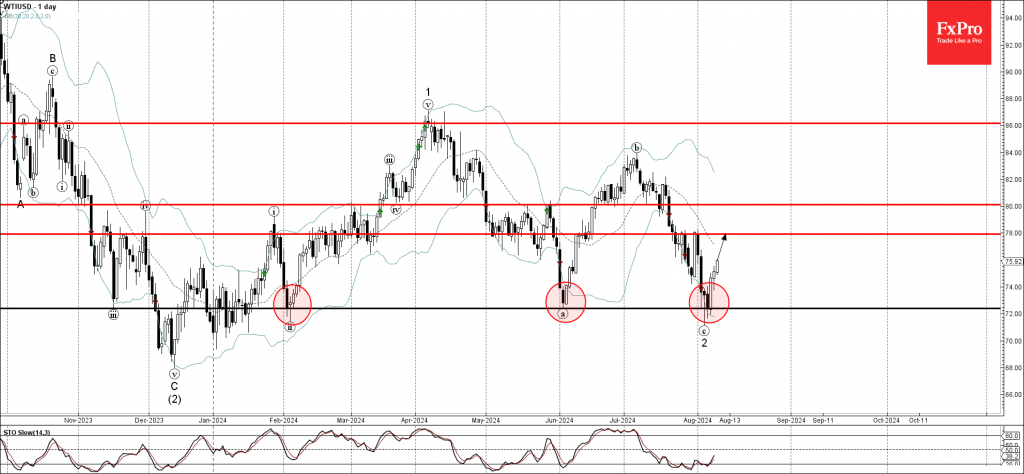

WTI Wave Analysis

- WTI reversed from support zone

- Likely to rise to resistance level 78.00

WTI crude oil recently reversed up from the support zone set between the strong support level 72.40 (which has been reversing the price from February) and the lower daily Bollinger Band.

The upward reversal from this support area stopped the c-wave of the previous downward ABC correction 2 from the start of April.

WTI crude oil can be expected to rise further toward the next resistance level 78.00 (which reversed the price twice at the end of July).

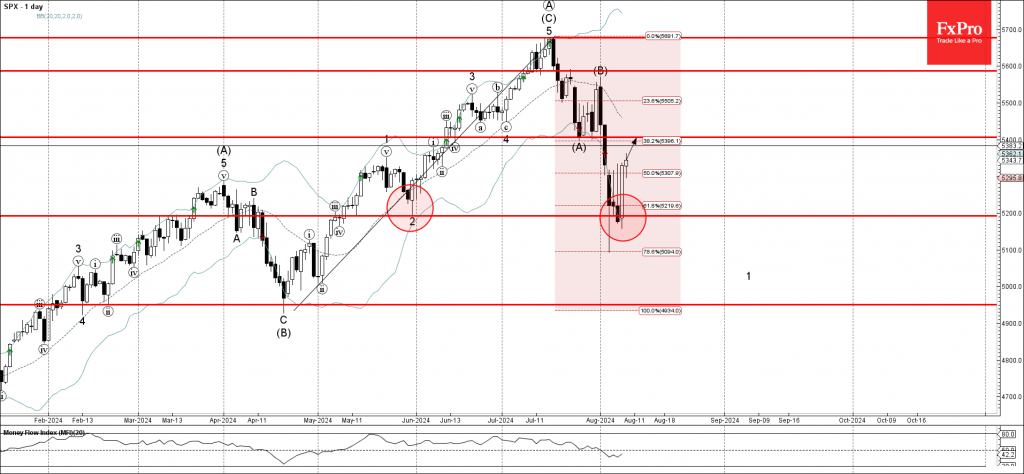

S&P 500 Wave Analysis

- S&P 500 reversed from resistance zone

- Likely to rise to resistance level 5400.00

S&P 500 index recently reversed up from the support zone located between the key support level 51900.00 (former low of wave 2 from May), lower daily Bollinger Band and the 61.8% Fibonacci correction of the upward impulse from April.

The upward reversal from this support zone created the daily Japanese candlesticks reversal pattern Bullish Engulfing.

Given the predominant daily uptrend, S&P 500 index can be expected to rise further toward the next resistance level 5400.00 (former support from the end of July).