Sample Category Title

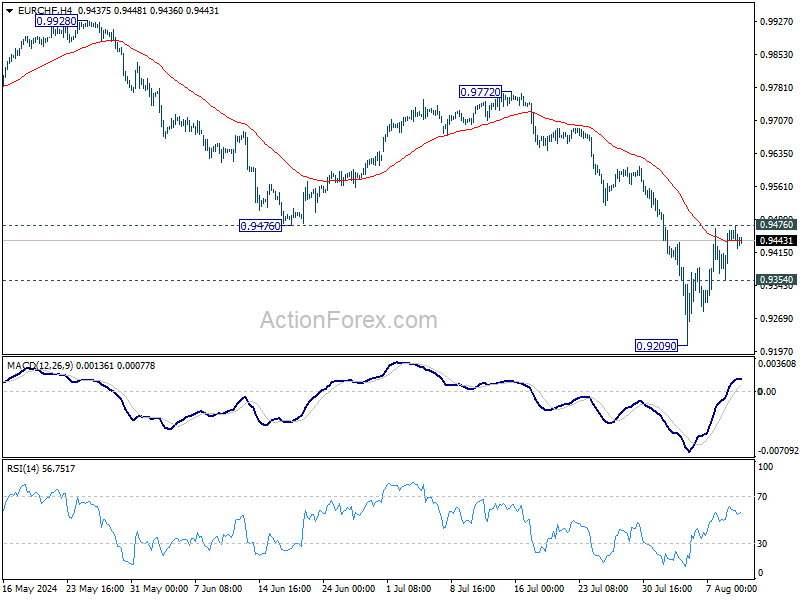

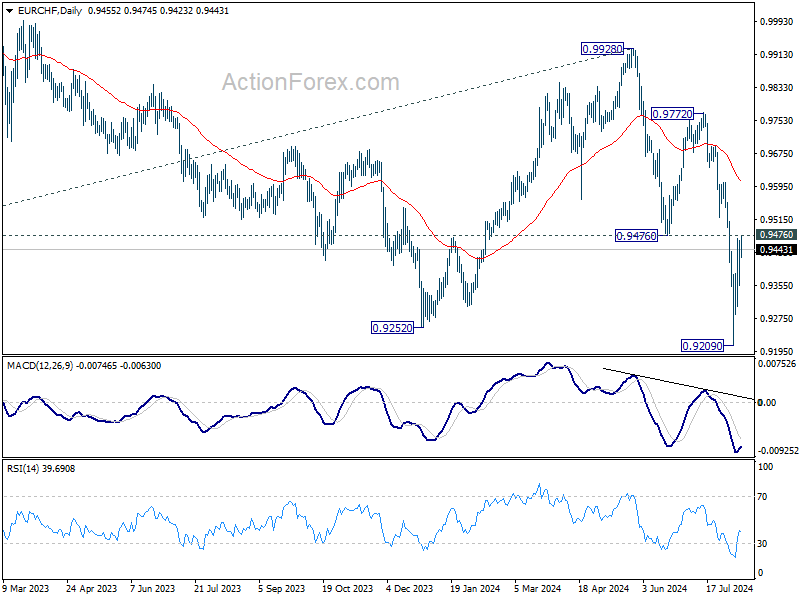

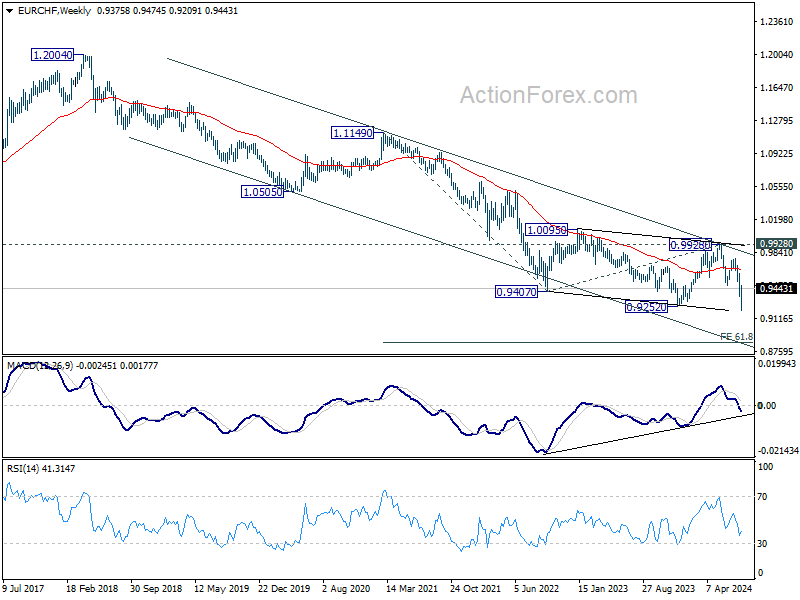

EUR/CHF Weekly Outlook

EUR/CHF rebounded strongly after initial dive to 0.9209 last week. But upside is limited by 0.9476 support turned resistance so far. Near term outlook remains bearish for now. On the downside, break of 0.9354 minor support will turn bias back to the downside for retesting 0.9209 low first. On the upside, however, sustained break of 0.9476 will turn bias to the upside for strong rise back to 55 D EMA (now at 0.9606).

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

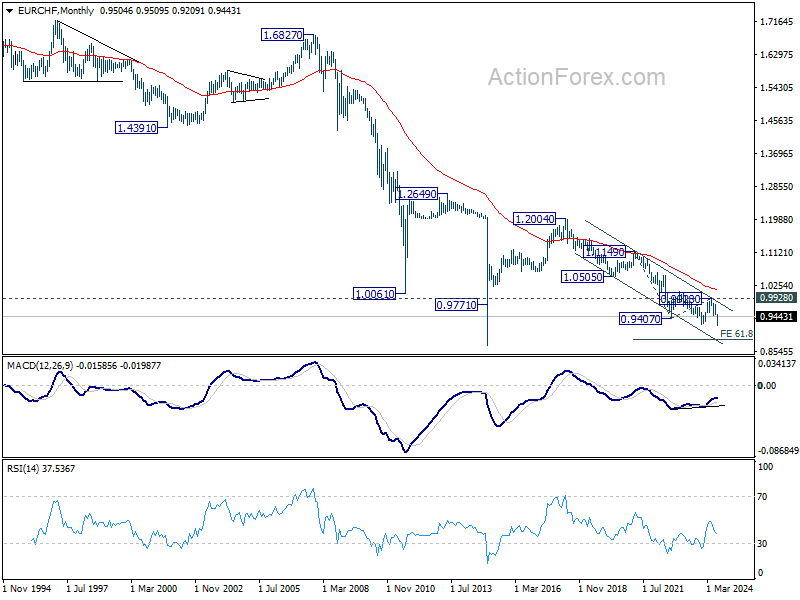

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 0.9928 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Market Panic Subsides as Consolidations Take Hold, but Sentiment Remains Fragile

The global financial markets started last week in a state of panic, driven by a sharp selloff in stock markets, with Japan's Nikkei index experiencing particularly heavy losses. However, as the week progressed, this initial wave of panic appeared to subside, with market sentiment stabilizing somewhat.

This calmness, however, should be viewed with caution. The markets may have simply entered a temporary consolidation phase rather than a full reversal. Underlying investor sentiment remains fragile, a fact underscored by the aggressive expectations in the futures markets, where traders are now pricing in a significant 50 bps rate cut by Fed in September. There has even been talk of the possibility of an emergency inter-meeting rate cut, reflecting the nervousness in the markets.

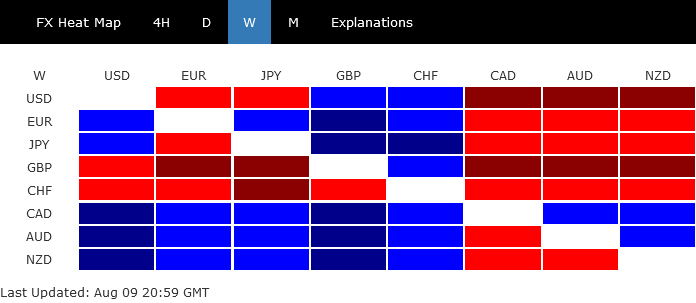

In the currency markets, Canadian Dollar ended the week as the strongest performer. Australian and New Zealand Dollars followed behind, benefiting from slight recovery in risk appetite. On the opposite end of the spectrum, Swiss Franc was the worst performer, followed by British Pound and Dollar, both of which struggled amid mixed economic signals. Euro and Japanese Yen found themselves in middle positions.

It's important to highlight that the price movements seen in the currency markets this week were largely corrective in nature. For instance, Japanese Yen and Swiss Franc, both of which saw significant gains during the height of the market panic, seemed to be consolidating those gains rather than building on them. Similarly, commodity currencies such as Canadian and Australian Dollars, while showing strength, were primarily recovering from earlier losses. This suggests that the markets have turned into a wait-and-see mode, with participants reluctant to make decisive moves until more clarity emerges.

Recession Fears Fuel Speculation of Aggressive Fed Rate Cuts, NASDAQ and Dollar Index Face Critical Support

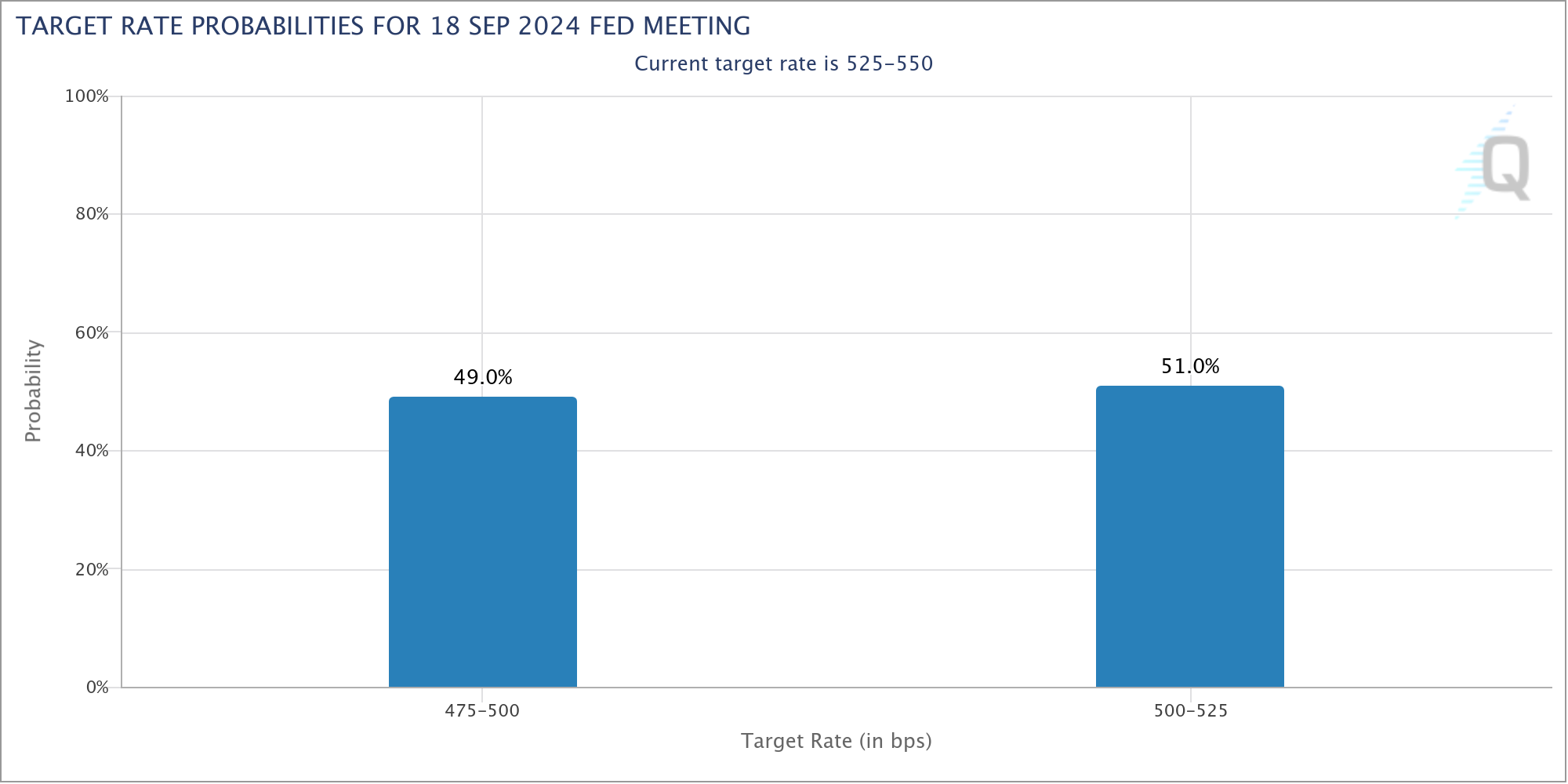

As concerns over a US recession intensified, traders are increasingly positioning themselves for a more aggressive response from Fed. Currently, Fed fund futures are signaling a 49% likelihood of a significant 50 bps rate cut at the September meeting, which would lower the federal funds rate to a range of 4.75-5.00%.

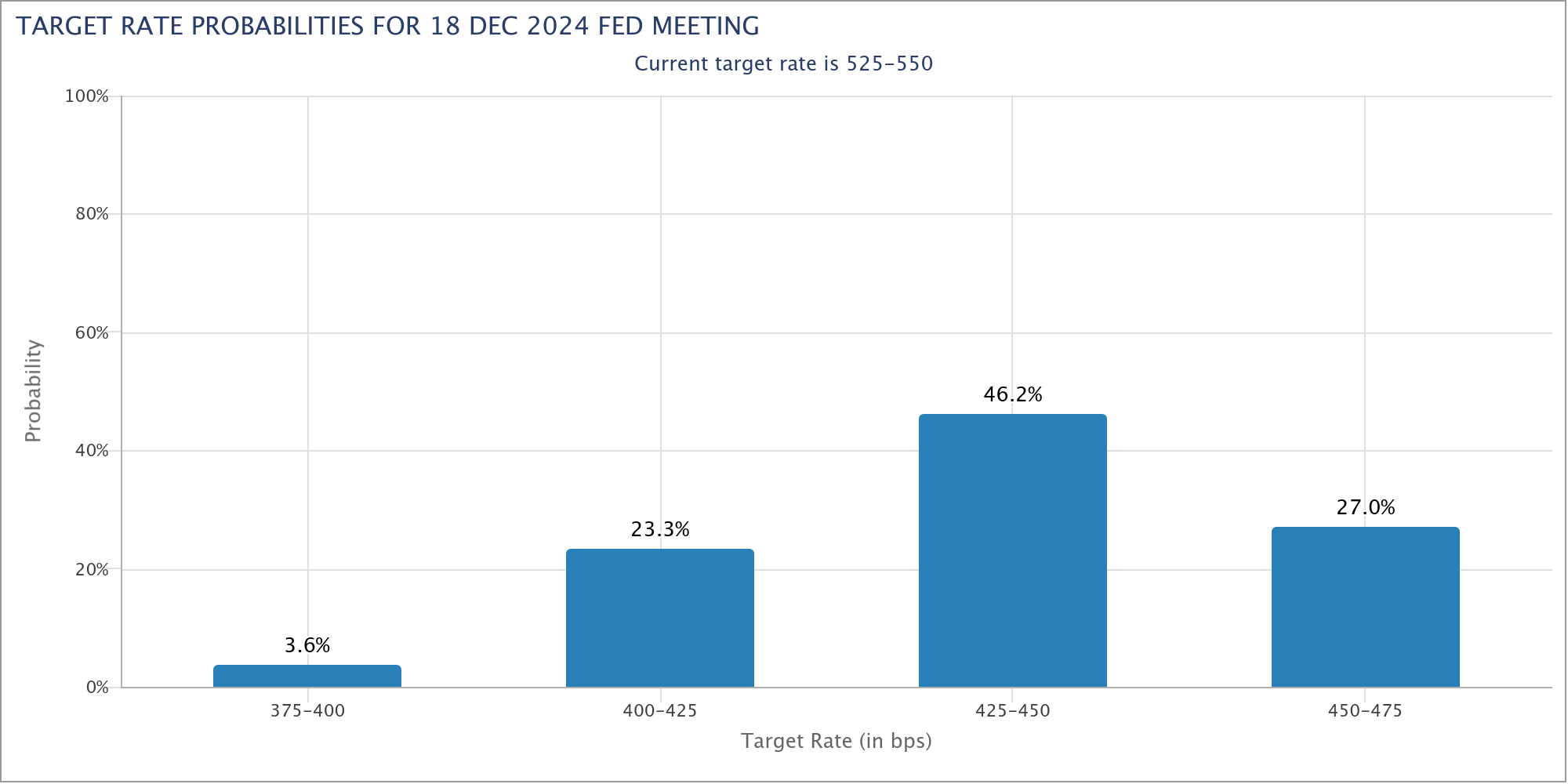

Moreover, the markets are now factoring in additional rate cuts in November and December, which could see the rate drop by a total of 100 bps to 4.25-4.50% by the end of 2024. The probability of this scenario is estimated at 83%, reflecting a growing consensus that Fed may need to act decisively to counter economic weakness, and the market turmoils.

Despite these market expectations, Fed officials have remained composed, viewing recent data on the labor market as indicative of a slowing economy rather than an impending recession. There has been no indication of panic among policymakers, who appear to be taking a measured approach.

This sentiment is echoed by economists, who, according to a recent Bloomberg survey conducted between August 6-8, overwhelmingly expect only a modest 25 bps cut in September. The view is that calls for a more substantial 50 bps cut are overreaction, driven more by recent stock market volatility, with no substantial economic shock to justify such a move.

With more than a month to go before FOMC's next policy meeting on September 17-18, there is still ample time for market dynamics to evolve. Key data releases, including two sets of CPI data scheduled for release on the coming Wednesday and September 11, as well as the non-farm payrolls report on September 6, will be critical in shaping Fed's decision. Additionally, there remains risks for further declines in stock markets and bond yields during this period.

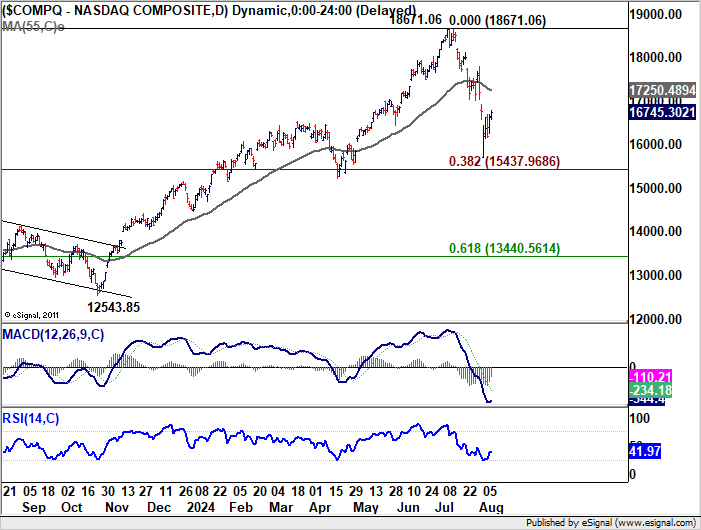

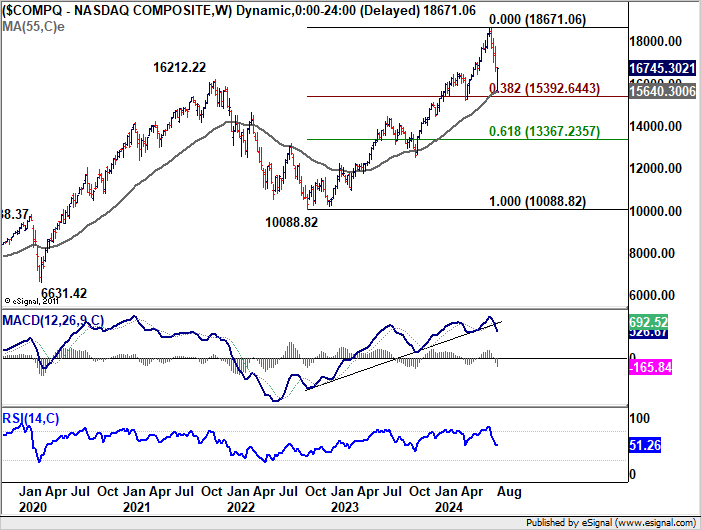

Technically, NASDAQ's recovery from last week's low at 15708.53 is so far corrective looking. Thus, near term risks stay on the downside. The key question is whether NASDAQ could defend the support zone between 55 W EMA (15640.28) and 38.2% retracement of 10207.47 to 18671.06 at 15437.96 on next week. Strong rebound from there, followed by firm break of 55 D EMA (now at 17250.48) will indicate that the correction from 18671.06 has completed, and keep the medium term up trend intact.

However, sustained break of the mentioned support zone will argue that a larger scale correction is already underway. Next downside target will be 61.8% retracement at 13367.23.

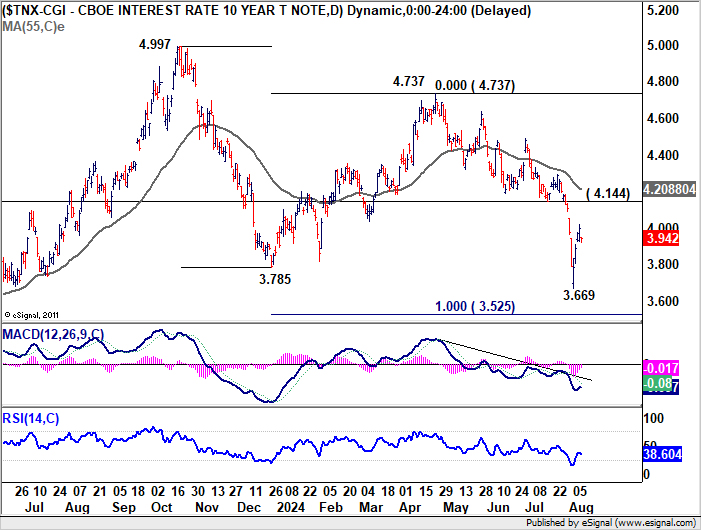

10-year yield dived through 3.785 support to resume the whole decline from 4.997. But it recovered strongly after hitting 3.669, and even breached 4.000 mark. But still, near term outlook will stay bearish as long as 4.144 support turned resistance holds. Below 3.669 will target 100% projection of 4.997 to 3.785 from 4.737 at 3.525, or even further to 38.2% retracement of 0.398 to 4.997 at 3.240.

As for Dollar index, despite last week's recovery, near term outlook will stay bearish as long as 103.65 support turned resistance holds. The key level is 100% projection of 106.51 to 103.99 from 106.13 at 102.05. Decisive break there, which is close to long term trend line support, could prompt downside acceleration through 102.35 support towards 100.61 low. Nevertheless, sustained break of 103.65 will bring stronger rebound towards 55 D EMA (now at 104.42), even as a corrective move.

Nikkei Stabilizes After Historical Plunge, DAX Faces Downside Risks

Japan was at the epicenter of the market turmoil globally. On Monday, Nikkei suffered a historic drop of -12.4%. However, the index managed to stabilize as the week progressed, even staging a strong rebound. Contributing to this recovery was BoJ Deputy Governor Shinichi Uchida, who helped soothe investor anxieties by downplaying the likelihood of an imminent rate hike. Uchida emphasized the necessity of keeping the current policy rate "for the time being," citing the "extremely volatile" market environment.

Technically, however, Nikkei hasn't even filled the gap left on Monday totally yet. The close below 55 W EMA is also a bearish sign. Risk remains on the downside for another fall. The key question is whether Nikkei could finally defend the long term channel support as seen in the weekly chart. Decisive break there will argue that fall from 42426.77 is a medium term down trend itself, rather than a corrective move. Nevertheless, break of 35880.14 gap resistance would at least bring stronger rebound for the near term.

For DAX, on the one hand, a head and shoulder top was clearly formed, which is a bearish signal. On the other hand, the downside target could be considered matched with the dive to 17623.97, after hitting 55 W EMA (now at 17241.89). Still risk will stay on the downside as long as 17951.17 support turned resistance holds. The fall from 18892.92 could extend to long term channel support (now at around 16600), or even to 38.2% retracement of 11862.84 to 18892.91 at 16207.42 before completion. Nevertheless, firm break of 17951.17 will argue that the correction is already over.

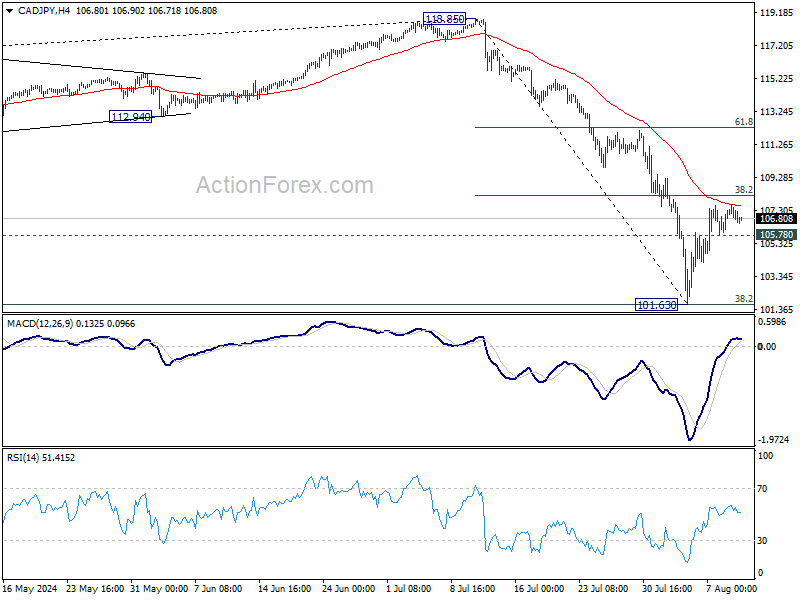

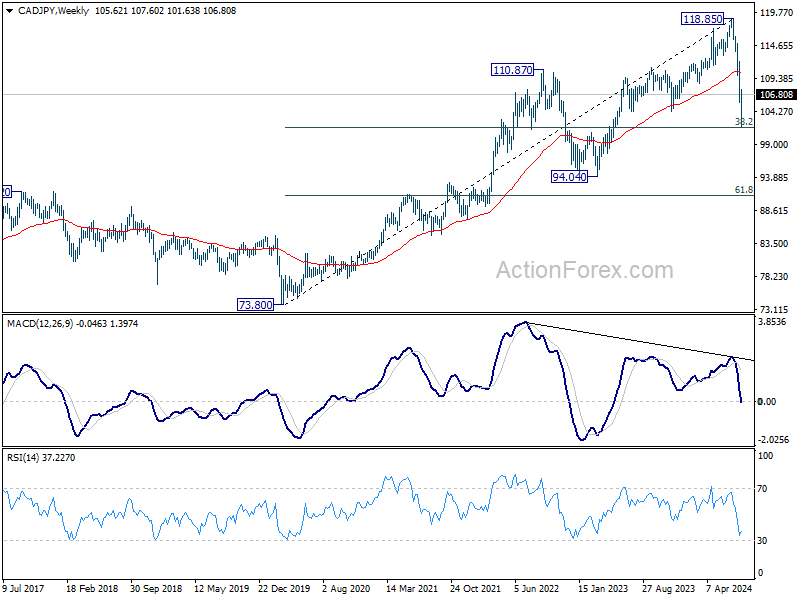

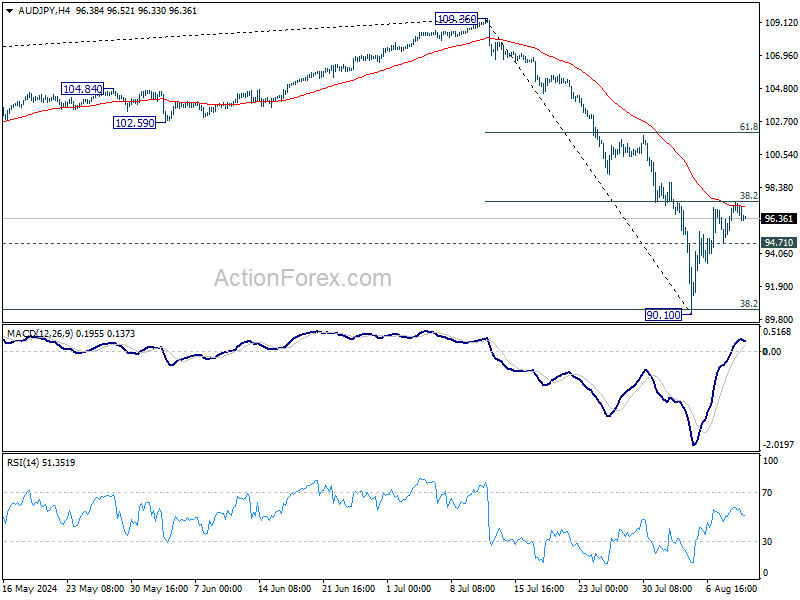

CAD/JPY and AUD/JPY Rebounds From Key Fibonacci Levels, But Bearish Risks Persist

Both CAD/JPY and AUD/JPY rebounded strongly after initial dives, getting strong support from long term fibonacci levels. But price actions of since then have so far been corrective. Thus, risk will stay on the downside for now.

CAD/JPY recovered after falling to 101.63, after touching 38.2% retracement of 73.80 (2020 low) to 118.85 at 101.64. However, upside is capped by 55 4H EMA (now at 107.57) as well as 38.2% retracement of 118.85 to 101.63 at 108.20. Near term outlook will remain bearish for now. Break of 105.78 minor support will argue that the corrective recovery is completed and bring retest of 101.63, with prospect of resuming the whole fall from 118.85. Nevertheless, firm break of 108.20 will bring stronger rebound to 61.8% retracement at 112.27, even as an extended corrective rise.

Similarly, AUD/JPY rebounded after hitting 90.01, breaching 38.2% retracement of 59.85 (2020 low) to 109.36 at 90.44. But upside is capped by 55 4H EMA (now at 97.10) as well as 38.2% retracement of 109.36 to 90.10 at 97.45. Near term outlook remains bearish for now. Break of 94.71 minor support will suggest that the recovery is finished and bring retest of 90.10, with risk of extending whole decline from 109.36. However, firm break of 94.5 will extend the rebound to 61.8% retracement at 102.22, even as an extended correcting rally.

EUR/CHF Weekly Outlook

EUR/CHF rebounded strongly after initial dive to 0.9209 last week. But upside is limited by 0.9476 support turned resistance so far. Near term outlook remains bearish for now. On the downside, break of 0.9354 minor support will turn bias back to the downside for retesting 0.9209 low first. On the upside, however, sustained break of 0.9476 will turn bias to the upside for strong rise back to 55 D EMA (now at 0.9606).

In the bigger picture, medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 0.9928 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 8/12 – 8/16

Monday, Aug 12, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 12:30 | CAD | Building Permits M/M Jun | 5.60% | -12.20% |

| 23:50 | JPY | PPI Y/Y Jul | 3.00% | 2.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 12:30 | CAD | Building Permits M/M Jun | |

| Forecast: 5.60% | Previous: -12.20% | ||

| 23:50 | JPY | PPI Y/Y Jul | |

| Forecast: 3.00% | Previous: 2.90% | ||

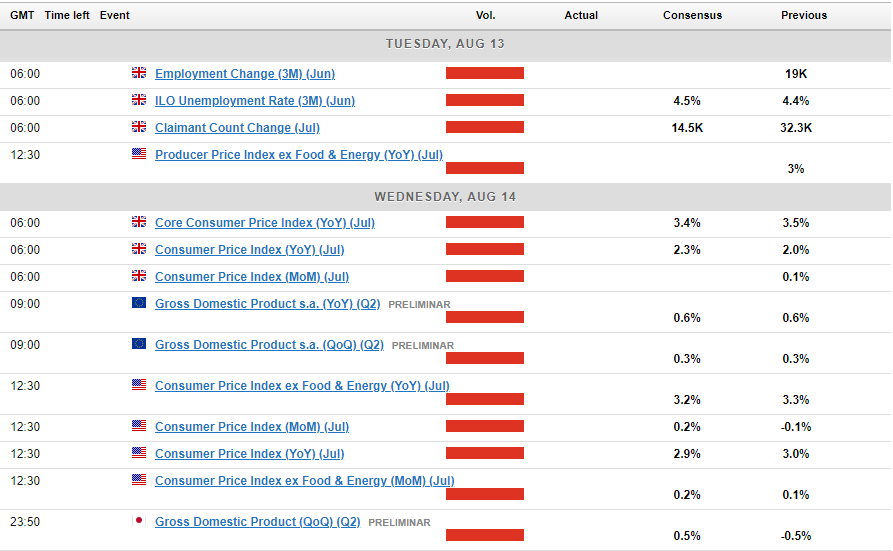

Tuesday, Aug 13, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Aug | -1.10% | |

| 01:30 | AUD | Wage Price Index Q/Q Q2 | 0.90% | 0.80% |

| 01:30 | AUD | NAB Business Conditions Jul | 4 | |

| 01:30 | AUD | NAB Business Confidence Jul | 4 | |

| 06:00 | JPY | Machine Tool Orders Y/Y Jul | 9.70% | |

| 06:00 | GBP | Claimant Count Change Jul | 14.5K | 32.3K |

| 06:00 | GBP | ILO Unemployment Rate (3M) Jun | 4.50% | 4.40% |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jun | 5.70% | |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jun | 4.60% | 5.70% |

| 09:00 | EUR | Germany ZEW Economic Sentiment Aug | 30.6 | 41.8 |

| 09:00 | EUR | Germany ZEW Current Situation Aug | -68.9 | |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Aug | 35.4 | 43.7 |

| 10:00 | USD | NFIB Business Optimism Index Jul | 91.7 | 91.5 |

| 12:30 | USD | PPI M/M Jul | 0.20% | 0.20% |

| 12:30 | USD | PPI Y/Y Jul | 2.60% | |

| 12:30 | USD | PPI ex Food & Energy M/M Jul | 0.20% | 0.40% |

| 12:30 | USD | PPI ex Food & Energy Y/Y Jul | 3% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | AUD | Westpac Consumer Confidence Aug | |

| Forecast: | Previous: -1.10% | ||

| 01:30 | AUD | Wage Price Index Q/Q Q2 | |

| Forecast: 0.90% | Previous: 0.80% | ||

| 01:30 | AUD | NAB Business Conditions Jul | |

| Forecast: | Previous: 4 | ||

| 01:30 | AUD | NAB Business Confidence Jul | |

| Forecast: | Previous: 4 | ||

| 06:00 | JPY | Machine Tool Orders Y/Y Jul | |

| Forecast: | Previous: 9.70% | ||

| 06:00 | GBP | Claimant Count Change Jul | |

| Forecast: 14.5K | Previous: 32.3K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Jun | |

| Forecast: 4.50% | Previous: 4.40% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Jun | |

| Forecast: | Previous: 5.70% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Jun | |

| Forecast: 4.60% | Previous: 5.70% | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Aug | |

| Forecast: 30.6 | Previous: 41.8 | ||

| 09:00 | EUR | Germany ZEW Current Situation Aug | |

| Forecast: | Previous: -68.9 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Aug | |

| Forecast: 35.4 | Previous: 43.7 | ||

| 10:00 | USD | NFIB Business Optimism Index Jul | |

| Forecast: 91.7 | Previous: 91.5 | ||

| 12:30 | USD | PPI M/M Jul | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 12:30 | USD | PPI Y/Y Jul | |

| Forecast: | Previous: 2.60% | ||

| 12:30 | USD | PPI ex Food & Energy M/M Jul | |

| Forecast: 0.20% | Previous: 0.40% | ||

| 12:30 | USD | PPI ex Food & Energy Y/Y Jul | |

| Forecast: | Previous: 3% | ||

Wednesday, Aug 14, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 02:00 | NZD | RBNZ Rate Decision | 5.50% | 5.50% |

| 03:00 | NZD | RBNZ Press Conference | ||

| 06:00 | GBP | CPI M/M Jul | 0.10% | |

| 06:00 | GBP | CPI Y/Y Jul | 2.30% | 2.00% |

| 06:00 | GBP | Core CPI Y/Y Jul | 3.40% | 3.50% |

| 06:00 | GBP | RPI M/M Jul | 0.20% | |

| 06:00 | GBP | RPI Y/Y Jul | 3.30% | 2.90% |

| 06:00 | GBP | PPI Input M/M Jul | -0.40% | -0.80% |

| 06:00 | GBP | PPI Input Y/Y Jul | -0.40% | |

| 06:00 | GBP | PPI Output M/M Jul | 0.20% | -0.30% |

| 06:00 | GBP | PPI Output Y/Y Jul | 1.40% | |

| 06:00 | GBP | PPI Core Output M/M Jul | 0.10% | |

| 06:00 | GBP | PPI Core Output Y/Y Jul | 1.10% | |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | 0.30% | 0.30% |

| 09:00 | EUR | Eurozone Employment Change Q/Q Q2 P | 0.20% | 0.30% |

| 09:00 | EUR | Eurozone Industrial Production M/M Jun | 0.70% | -0.60% |

| 12:30 | USD | CPI M/M Jul | 0.20% | -0.10% |

| 12:30 | USD | CPI Y/Y Jul | 3.00% | 3.00% |

| 12:30 | USD | CPI Core M/M Jul | 0.20% | 0.10% |

| 12:30 | USD | CPI Core Y/Y Jul | 3.20% | 3.30% |

| 14:30 | USD | Crude Oil Inventories | -3.7M | |

| 23:50 | JPY | GDP Q/Q Q2 P | 0.60% | -0.50% |

| 23:50 | JPY | GDP Deflator Y/Y Q2 P | 2.60% | 3.40% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 02:00 | NZD | RBNZ Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 03:00 | NZD | RBNZ Press Conference | |

| Forecast: | Previous: | ||

| 06:00 | GBP | CPI M/M Jul | |

| Forecast: | Previous: 0.10% | ||

| 06:00 | GBP | CPI Y/Y Jul | |

| Forecast: 2.30% | Previous: 2.00% | ||

| 06:00 | GBP | Core CPI Y/Y Jul | |

| Forecast: 3.40% | Previous: 3.50% | ||

| 06:00 | GBP | RPI M/M Jul | |

| Forecast: | Previous: 0.20% | ||

| 06:00 | GBP | RPI Y/Y Jul | |

| Forecast: 3.30% | Previous: 2.90% | ||

| 06:00 | GBP | PPI Input M/M Jul | |

| Forecast: -0.40% | Previous: -0.80% | ||

| 06:00 | GBP | PPI Input Y/Y Jul | |

| Forecast: | Previous: -0.40% | ||

| 06:00 | GBP | PPI Output M/M Jul | |

| Forecast: 0.20% | Previous: -0.30% | ||

| 06:00 | GBP | PPI Output Y/Y Jul | |

| Forecast: | Previous: 1.40% | ||

| 06:00 | GBP | PPI Core Output M/M Jul | |

| Forecast: | Previous: 0.10% | ||

| 06:00 | GBP | PPI Core Output Y/Y Jul | |

| Forecast: | Previous: 1.10% | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 09:00 | EUR | Eurozone Employment Change Q/Q Q2 P | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 09:00 | EUR | Eurozone Industrial Production M/M Jun | |

| Forecast: 0.70% | Previous: -0.60% | ||

| 12:30 | USD | CPI M/M Jul | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 12:30 | USD | CPI Y/Y Jul | |

| Forecast: 3.00% | Previous: 3.00% | ||

| 12:30 | USD | CPI Core M/M Jul | |

| Forecast: 0.20% | Previous: 0.10% | ||

| 12:30 | USD | CPI Core Y/Y Jul | |

| Forecast: 3.20% | Previous: 3.30% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -3.7M | ||

| 23:50 | JPY | GDP Q/Q Q2 P | |

| Forecast: 0.60% | Previous: -0.50% | ||

| 23:50 | JPY | GDP Deflator Y/Y Q2 P | |

| Forecast: 2.60% | Previous: 3.40% | ||

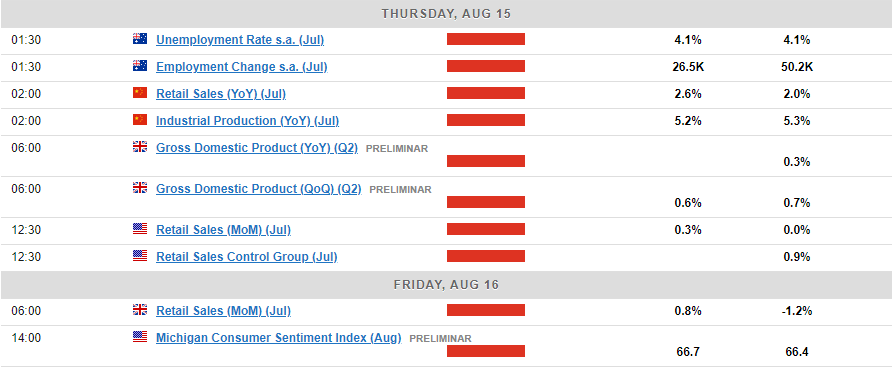

Thursday, Aug 15, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Aug | 4.30% | |

| 01:30 | AUD | Employment Change Jul | 26.5K | 50.2K |

| 01:30 | AUD | Unemployment Rate Jul | 4.10% | 4.10% |

| 02:00 | CNY | Industrial Production Y/Y Jul | 5.20% | 5.30% |

| 02:00 | CNY | Retail Sales Y/Y Jul | 2.60% | 2.00% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jul | 3.90% | 3.90% |

| 04:30 | JPY | Industrial Production M/M Jun F | -3.60% | -3.60% |

| 06:00 | GBP | GDP M/M Jun | 0.10% | 0.40% |

| 06:00 | GBP | GDP Q/Q Q2 P | 0.60% | 0.70% |

| 06:00 | GBP | Industrial Production M/M Jun | 0.10% | 0.20% |

| 06:00 | GBP | Industrial Production Y/Y Jun | 0.40% | |

| 06:00 | GBP | Manufacturing Production M/M Jun | 0.10% | 0.40% |

| 06:00 | GBP | Manufacturing Production Y/Y Jun | 0.60% | |

| 06:00 | GBP | Goods Trade Balance (GBP) Jun | -16.0B | -17.9B |

| 06:30 | CHF | Producer and Import Prices Y/Y Jul | 0.20% | -1.90% |

| 06:30 | CHF | Producer and Import Prices M/M Jul | 0% | |

| 12:30 | CAD | Wholesale Sales M/M Jun | -0.60% | -0.80% |

| 12:30 | USD | Initial Jobless Claims (Aug 9) | 239K | 233K |

| 12:30 | USD | Retail Sales M/M Jul | 0.30% | 0.00% |

| 12:30 | USD | Retail Sales ex Autos M/M Jul | 0.10% | 0.40% |

| 12:30 | USD | Import Price Index M/M Jul | 0% | 0% |

| 12:30 | USD | Empire State Manufacturing Index Aug | -5.9 | -6.6 |

| 12:30 | USD | Philadelphia Fed Survey Aug | 6.6 | 13.9 |

| 13:15 | USD | Industrial Production M/M Jul | 0.10% | 0.60% |

| 13:15 | USD | Capacity Utilization Jul | 78.6% | 78.8% |

| 14:00 | USD | Business Inventories Jun | 0.30% | 0.50% |

| 14:00 | USD | NAHB Housing Market Index Aug | 43 | 42 |

| 14:30 | USD | Natural Gas Storage | 21B | |

| 22:30 | NZD | Business NZ PMI Jul | 41.1 | |

| 22:45 | NZD | PPI Input Q/Q Q2 | 0.50% | 0.70% |

| 22:45 | NZD | PPI Output Q/Q Q2 | 0.60% | 0.90% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Consumer Inflation Expectations Aug | |

| Forecast: | Previous: 4.30% | ||

| 01:30 | AUD | Employment Change Jul | |

| Forecast: 26.5K | Previous: 50.2K | ||

| 01:30 | AUD | Unemployment Rate Jul | |

| Forecast: 4.10% | Previous: 4.10% | ||

| 02:00 | CNY | Industrial Production Y/Y Jul | |

| Forecast: 5.20% | Previous: 5.30% | ||

| 02:00 | CNY | Retail Sales Y/Y Jul | |

| Forecast: 2.60% | Previous: 2.00% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jul | |

| Forecast: 3.90% | Previous: 3.90% | ||

| 04:30 | JPY | Industrial Production M/M Jun F | |

| Forecast: -3.60% | Previous: -3.60% | ||

| 06:00 | GBP | GDP M/M Jun | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 06:00 | GBP | GDP Q/Q Q2 P | |

| Forecast: 0.60% | Previous: 0.70% | ||

| 06:00 | GBP | Industrial Production M/M Jun | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 06:00 | GBP | Industrial Production Y/Y Jun | |

| Forecast: | Previous: 0.40% | ||

| 06:00 | GBP | Manufacturing Production M/M Jun | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 06:00 | GBP | Manufacturing Production Y/Y Jun | |

| Forecast: | Previous: 0.60% | ||

| 06:00 | GBP | Goods Trade Balance (GBP) Jun | |

| Forecast: -16.0B | Previous: -17.9B | ||

| 06:30 | CHF | Producer and Import Prices Y/Y Jul | |

| Forecast: 0.20% | Previous: -1.90% | ||

| 06:30 | CHF | Producer and Import Prices M/M Jul | |

| Forecast: | Previous: 0% | ||

| 12:30 | CAD | Wholesale Sales M/M Jun | |

| Forecast: -0.60% | Previous: -0.80% | ||

| 12:30 | USD | Initial Jobless Claims (Aug 9) | |

| Forecast: 239K | Previous: 233K | ||

| 12:30 | USD | Retail Sales M/M Jul | |

| Forecast: 0.30% | Previous: 0.00% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Jul | |

| Forecast: 0.10% | Previous: 0.40% | ||

| 12:30 | USD | Import Price Index M/M Jul | |

| Forecast: 0% | Previous: 0% | ||

| 12:30 | USD | Empire State Manufacturing Index Aug | |

| Forecast: -5.9 | Previous: -6.6 | ||

| 12:30 | USD | Philadelphia Fed Survey Aug | |

| Forecast: 6.6 | Previous: 13.9 | ||

| 13:15 | USD | Industrial Production M/M Jul | |

| Forecast: 0.10% | Previous: 0.60% | ||

| 13:15 | USD | Capacity Utilization Jul | |

| Forecast: 78.6% | Previous: 78.8% | ||

| 14:00 | USD | Business Inventories Jun | |

| Forecast: 0.30% | Previous: 0.50% | ||

| 14:00 | USD | NAHB Housing Market Index Aug | |

| Forecast: 43 | Previous: 42 | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 21B | ||

| 22:30 | NZD | Business NZ PMI Jul | |

| Forecast: | Previous: 41.1 | ||

| 22:45 | NZD | PPI Input Q/Q Q2 | |

| Forecast: 0.50% | Previous: 0.70% | ||

| 22:45 | NZD | PPI Output Q/Q Q2 | |

| Forecast: 0.60% | Previous: 0.90% | ||

Friday, Aug 16, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Jun | 0.30% | -0.40% |

| 06:00 | GBP | Retail Sales M/M Jul | 0.80% | -1.20% |

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jun | 14.5B | 12.3B |

| 12:15 | CAD | Housing Starts Jul | 245K | 242K |

| 12:30 | CAD | Manufacturing Sales M/M Jun | -2.50% | 0.40% |

| 12:30 | USD | Building Permits M/M Jul | 1.44M | 1.45M |

| 12:30 | USD | Housing Starts M/M Jul | 1.34M | 1.35M |

| 14:00 | USD | Michigan Consumer Sentiment Index Aug P | 67.3 | 66.4 |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M Jun | |

| Forecast: 0.30% | Previous: -0.40% | ||

| 06:00 | GBP | Retail Sales M/M Jul | |

| Forecast: 0.80% | Previous: -1.20% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) Jun | |

| Forecast: 14.5B | Previous: 12.3B | ||

| 12:15 | CAD | Housing Starts Jul | |

| Forecast: 245K | Previous: 242K | ||

| 12:30 | CAD | Manufacturing Sales M/M Jun | |

| Forecast: -2.50% | Previous: 0.40% | ||

| 12:30 | USD | Building Permits M/M Jul | |

| Forecast: 1.44M | Previous: 1.45M | ||

| 12:30 | USD | Housing Starts M/M Jul | |

| Forecast: 1.34M | Previous: 1.35M | ||

| 14:00 | USD | Michigan Consumer Sentiment Index Aug P | |

| Forecast: 67.3 | Previous: 66.4 | ||

Markets Weekly Outlook – US CPI to Test Markets Following Tumultuous Week

- US equities rebounded from a selloff earlier in the week, ending slightly higher. However, caution remains due to upcoming economic data releases.

- The Japanese Yen is heading for its first losing week in six, impacted by a peak in short-position unwinding and dovish BoJ comments.

- The upcoming week features significant data releases, including US and UK inflation, Chinese economic figures, and the RBNZ interest rate decision. Markets are cautious due to recessionary fears and concerns about China’s economic recovery.

Week in Review: Tumultuous Week Comes to an End

A tumultuous week for markets is set to end on a positive note. US equities have bounced back from an early-week selloff and are trading slightly higher for the week as of now. However, traders are exercising caution with a slew of high-impact economic data releases on the horizon.

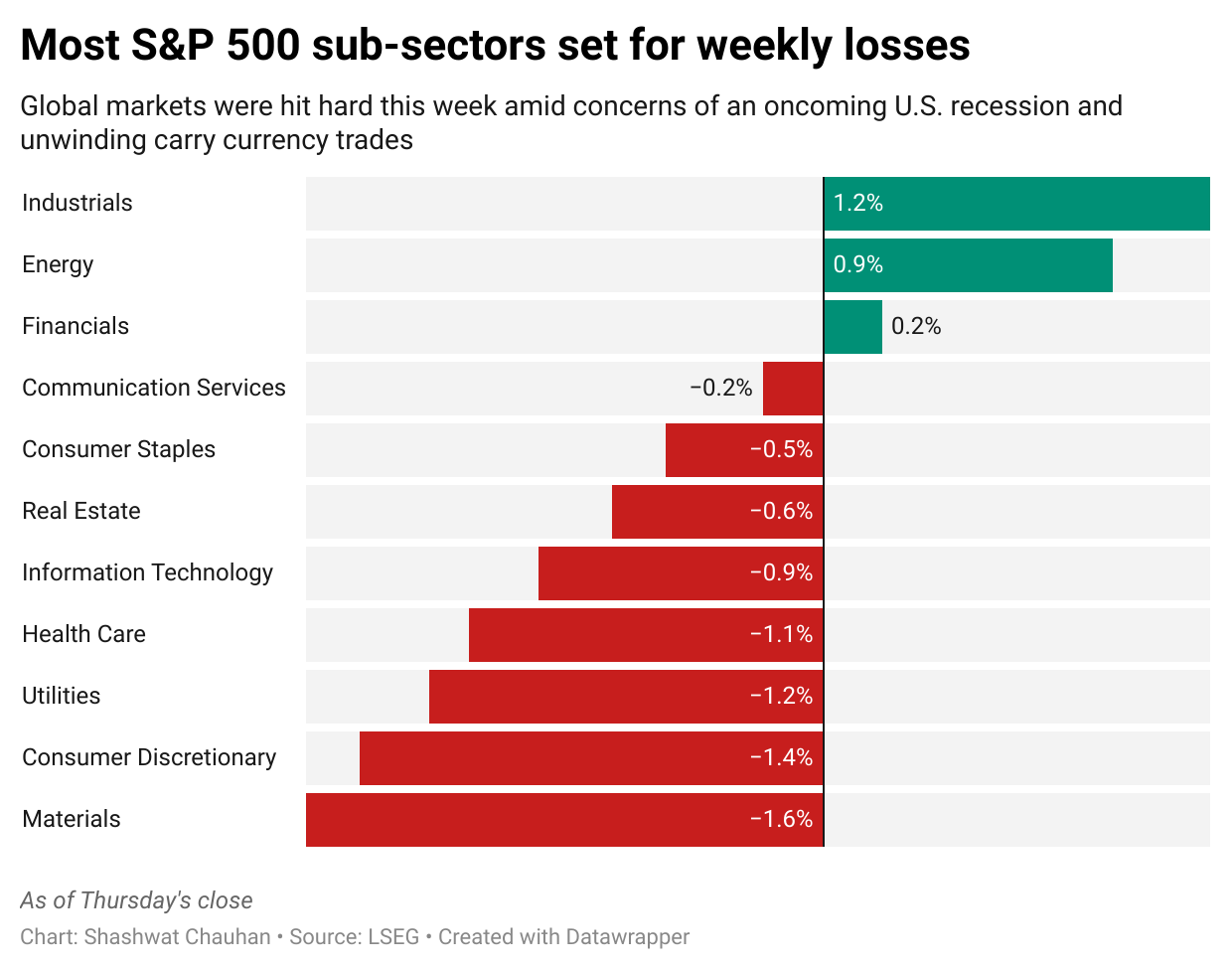

Although US indices have recovered, several sub-sectors within the S&P 500 are still poised for a weekly loss.

Source: LSEG

In the commodities sector, gold seems poised to end the week in the red but showed strong recovery towards the end of the week. Conversely, oil prices have had an impressive week, up 2.7% at the time of writing.

OPEC+ comments this week suggested that the group might postpone their planned October production increase if market conditions remain unstable. This news likely contributed to oil’s gains this week after four consecutive weeks of losses.

On the FX front, the Dollar Index is slightly down for the week at the time of writing. A robust recovery in the US Dollar during the latter part of the week wiped out gains seen by some of its G7 counterparts.

The Japanese Yen continues to be a point of interest and is on track for its first losing week in six. The unwinding of short positions seemed to peak on Monday, dragging USD/JPY to a low of 141.67. However, as sentiment improved and the unwinding phase concluded, the yen struggled to gain traction for the rest of the week.

This coupled with some dovish testimony from BoJ officials weighed further on the Japanese Yen.

The Week Ahead: Data Heavy Week to Test Markets

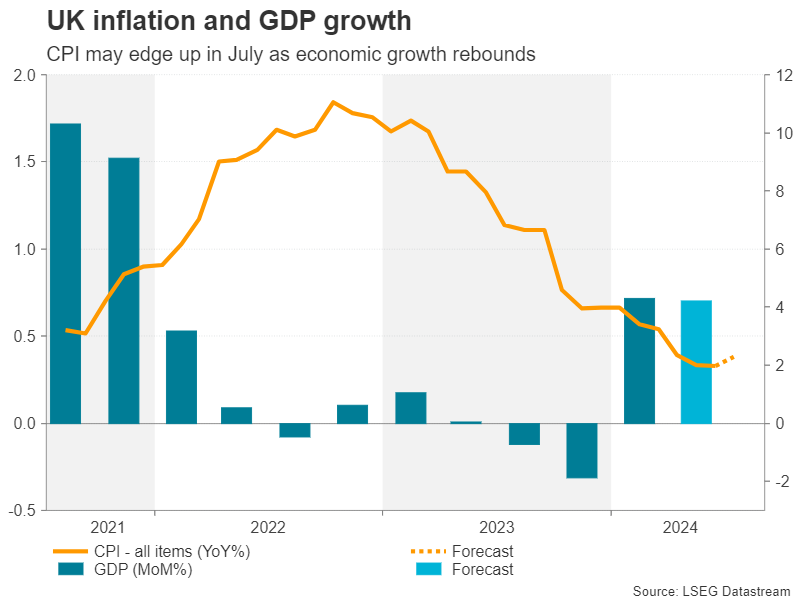

The upcoming week promises to be blockbuster with a host of high impact data releases. We have the US and UK inflation data prints coupled with data out of China and Japan. Last but not least we have the Reserve Bank of New Zealand (RBNZ) interest rate meeting.

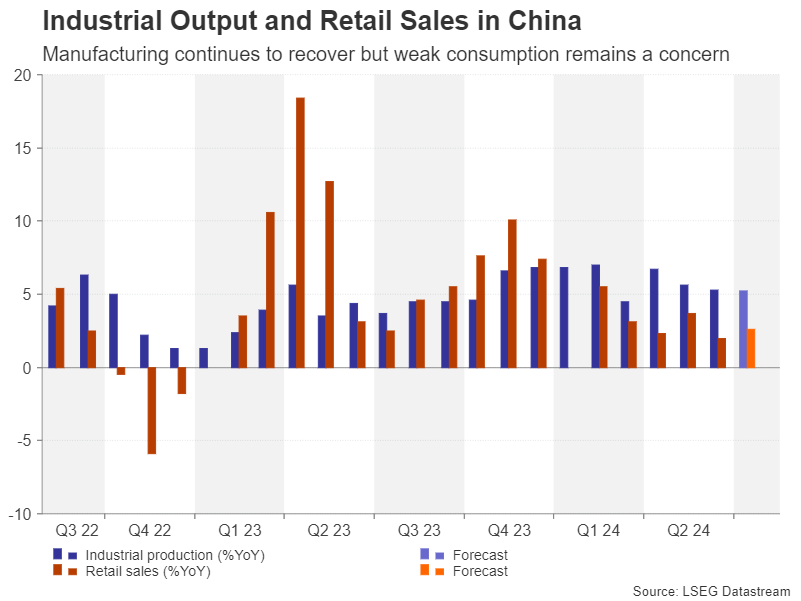

Markets remain cautious heading into the new week. Data will no doubt be scrutinized as recessionary fears have not fully abated yet. Chinese data in particular will be of particular interest given the slowdown and recession fears have been sparked somewhat by a slower than expected recovery from the world’s second largest economy.

Asia Pacific Markets

In Asia, China’s major economic data releases are scheduled for the coming week. On Thursday, the People’s Bank of China will set the Medium-Term Lending Facility (MLF) rate.

Additionally, China will release 70-city housing price data and key economic activity figures. A smaller decline in property prices and stabilization in tier-one or two cities would be a positive step in restoring confidence. Retail sales are expected to recover slightly after last month’s post-pandemic low, while industrial production and FAI may also stabilize this month.

Japan will release its 2Q24 GDP on Thursday, expected to rebound to 0.5% quarter-on-quarter seasonally-adjusted (slightly below the 0.6% market consensus). However, this is unlikely to fully offset the 0.7% contraction seen in 1Q24. June manufacturing activity was weaker than anticipated due to another auto safety issue, affecting auto-related sectors. On the positive side, household spending and facility investment should see improvement.

Following the comments by BoJ policymakers it will be interesting to gauge the market reaction to Japanese data as this will be the first set of key data following the rate hike.

Europe + UK + US

Looking to the Euro Area, the US and UK and the calendar comes back to life following a quiet week.

There is a host of UK high impact data which includes the employment data, UK CPI, GDP and Retail sales. The GBP continues to hold the high ground with positive data likely to keep the GBP elevated.

The US also delivers its July CPI data in the week ahead and given the repricing of Federal Reserve rate cuts will be of particular interest. The week wraps up with US retail sales and Michigan consumer sentiment data.

Q2 Euro Area GDP preliminary numbers will also come out this week. This is a key gauge for market participants to keep an eye on as the global growth slowdown weighs on the minds of traders.

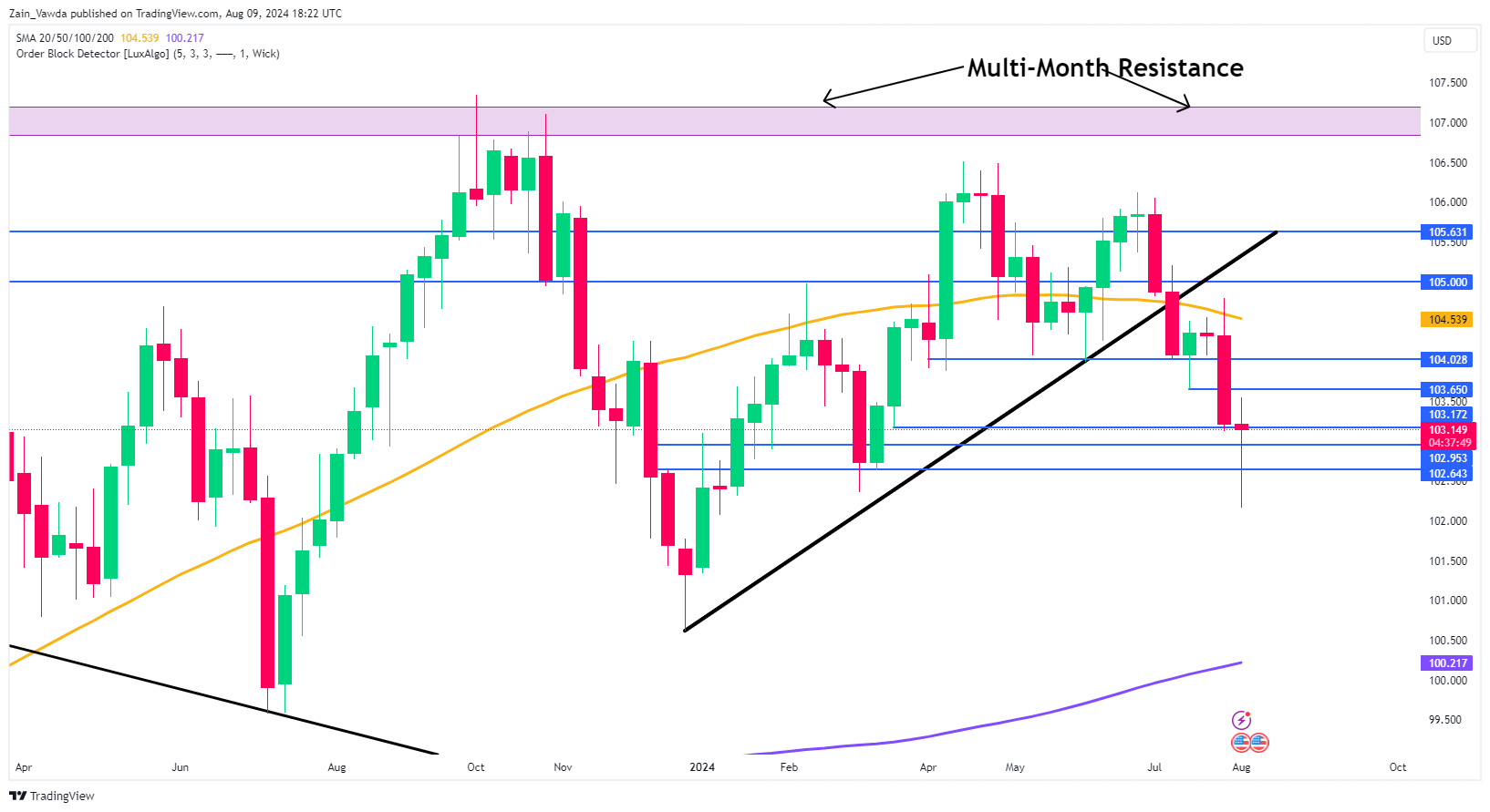

Chart of the Week

The chart of the week I’m focusing on is the US Dollar Index (DXY), which remains a significant force in the financial markets.

After an early week selloff, the DXY has rebounded to trade nearly flat as we head into next week. The substantial downside week is promising for bulls, but the DXY still faces downside risks.

Currently, the DXY is just below key resistance at 103.17, with the next point of interest around 103.65.

A downward move from here would need to break supports at 102.95 and 102.64 before this week’s lows at 100.64 come into play.

US Dollar Index (DXY) Weekly Chart – August 9, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support:

- 103.00

- 102.64

- 101.50

Resistance:

- 103.50

- 104.29

- 105.00

The Weekly Bottom Line: Bumps in the Road

U.S. Highlights

- Inflation and the labor market are cooling off, but the economy has not yet hit a wall. Despite what markets may be fearing.

- The ISM services survey showed broad based improvements in July, while falling longer term interest rates are easing financial conditions.

- Next week’s inflation report and the Jackson Hole summit in a couple of weeks are two big events to keep an eye on.

Canadian Highlights

- Canada’s labour market continues to bend, but not break. A slight decline in both employment and labour force growth has kept the unemployment rate steady.

- We have shifted our expectations for the path of interest rates, where we expect Bank of Canada to deliver three quarter-point cuts over the remainder of 2024.

- Trade data released this week is firming up expectations that economic growth may overshoot the Bank of Canada’s estimates in the second quarter, while also providing a strong hand off into the third quarter.

U.S. – Bumps in the Road

After last Friday’s disappointing payrolls report sent equities tumbling and bonds flying, markets have taken a bit of a breather this week. The U.S. 10-year treasury yield is back to 3.9%, within basis points of where it was last Thursday, while equities have retraced roughly half of their losses since Friday – although they are still well off their mid-July highs

The payrolls data set off alarm bells and traders piled into bets of impending rate cuts and a steep slowdown in economic activity. Fed funds futures are pricing 100 basis points of rate cuts from the Fed through the end of 2024. Importantly, with only three meetings to go, this suggests a 50-basis point cut could come as early as September.

We think this is a tad overdone. To be sure, rate relief is on the way, however our expectation is that the Fed will deliver three more cuts through December. The difference is slight but reflects the fact that we still see an economy that’s gradually gearing down, rather than one where the bottom is falling out.

For instance, take last week’s jobs report. Job growth slowed sharply to 114k jobs from 179k the month prior, with the services sector kicking its smallest addition of the post-pandemic recovery. On the face of it, the second consecutive month of decelerating job growth reflects waning momentum. However, job growth needed to cool to tame inflation and from this lens, the average of 170k jobs gained over the past three months, combined with a cooling in inflation, is a pace the Fed would be happy to accept.

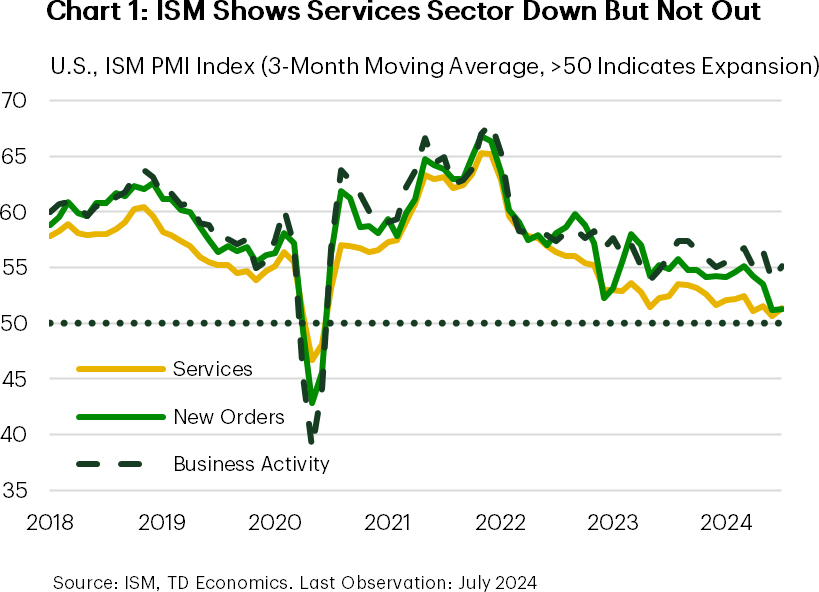

Beyond the labor market, there are signs that economic activity is holding up. This week the ISM services index surprised to the upside, showing the sector regained some momentum to continue expanding. The details of the report were solid with new orders, overall activity and even employment all showing gains (Chart 1).

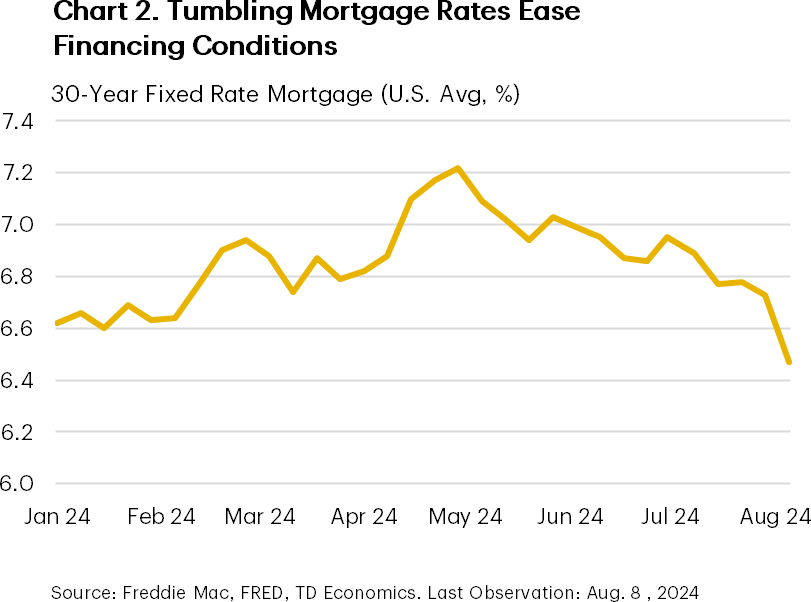

Moreover, falling bond yields are helping ease financial conditions. Thirty-year mortgage rates are down below 6.5%, from 6.9% a month ago (Chart 2). Data from the National Association of Realtors showed June’s pending home sales up nearly 5% month-on-month (m/m), and with a further drawdown in financing costs in July, further recovery in actual sales could be in the offing.

These indicators suggest an economy that continues to mosey along, slower than before, but not yet hitting a wall. And remember, the Fed remains data dependent, so for a sense of how the Fed will respond in September, two upcoming events will be in focus. First up, next week’s release of July’s Consumer Price Index (CPI). We are looking for a firming in core CPI (ex. food and energy) to 0.2% month-on-month. While this implies an annual figure of 3.2%, it would sink the three- and six-month percent changes in core CPI to roughly 1.6% and 2.9% annualized, respectively, comfortably extending the cooling in price gains.

The update on inflation then lays the groundwork for the next big event, the Fed’s Jackson Hole Economic Symposium on August 22-24th. Chairman Powell is slated to speak, so markets will be closely parsing his statements for any insights into the Fed’s read of recent events.

Canada – Keep Calm, Carry On

Canadian markets spent the holiday-shortened week digesting the rapid shift in market sentiment stemming from growth worries south of the border. Recent events in the U.S. and Japan have created volatile market conditions that have spilt over to Canadian markets. Yields whipsawed, with front-end yields rising 15 basis points, partially reversing the 30 bps rally the week prior. The Canadian dollar also caught a bid, up just over a tenth of a cent to 0.728/USD. Despite the external noise, we’d argue the economic outlook for Canada is stable and there isn’t a need to ring the alarm bells just yet.

With a soft U.S. payrolls print last week spurring knee-jerk reactions, Canada’s job market updates were being watched with an even closer eye. Like our southern counterparts, Canada disappointed against expectations, with virtually no job growth recorded in July. But unlike the past several months, labour force growth pulled back which helped keep the unemployment rate steady at 6.4%.Meanwhile, wages as measured by the Labour Force Survey are still growing at 5.0%, which will continue to be on the Bank of Canada’s (BoC) radar (Chart 1). The labour market has no doubt lost steam, but it is holding up relatively well and is evolving roughly in line with what we’d expect from past economic cycles.

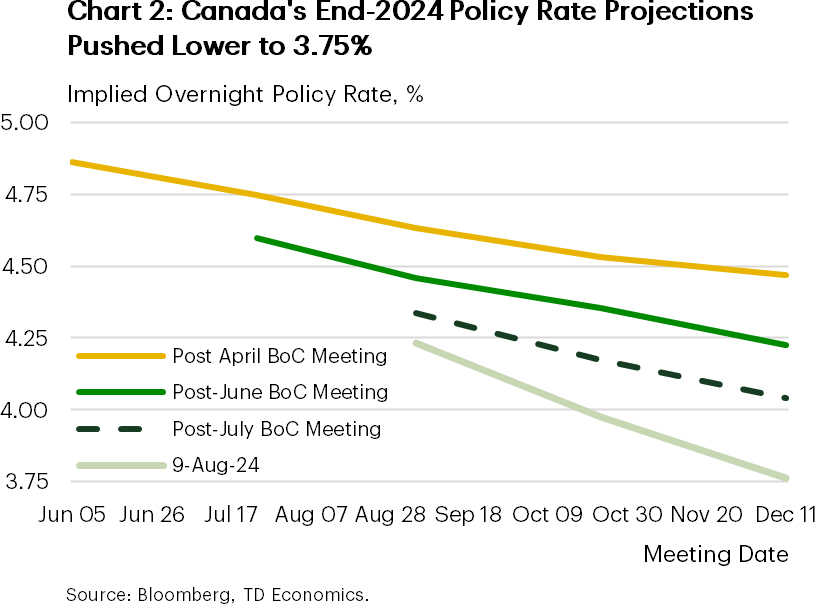

The Bank of Canada will use the labour data as a marker in their next policy decision. The Bank has firmly entered their rate easing cycle and so the question becomes how the path for policy rates looks over the rest of the year. Governor Macklem’s dovish tilt at last month’s meeting had markets re-jigging their rate cut expectations for the remaining three announcements this year, to now see Canada’s policy rate at 3.75% at year-end (Chart 2). This aligns with our thinking as it keeps interest rates on a slowly declining path and balances the objectives of supporting growth without reigniting inflation.

The BoC’s Summary of Deliberations also released this week reiterated an important shift in the BoC’s thinking from last meeting. New in their messaging was the emphasis on the downside risks to inflation via excess supply and how it has taken on an increased weight in monetary policy discussions. This is an important shift in sentiment, as it’s indicative of a central bank concerned that the still high level of the policy rate may be exerting too much slowing in the economy.

Economic growth in Canada’s economy is by no means advancing at breakneck speed, but we don’t foresee a deterioration–or a recession–on the horizon. Domestically, the Canadian consumer bounced back in the first quarter of this year with contributions from spending expected to remain in coming quarters. Further, Canada’s trade picture is firming up as the recently operational Trans Mountain Pipeline expansion boosts energy exports, a theme we expect to persist of the coming months. At this stage, the BoC has enough confidence to gradually deliver rate relief to the economy with a soft-landing scenario still being the likely outcome.

Weekly Economic & Financial Commentary: A Wild Week in a Data Desert

Summary

United States: A Wild Week in a Data Desert

- It was a very quiet week on the U.S. economic data front, but financial markets were anything but calm. Last week's run of weak U.S. data, capped by a troubling rise in the unemployment rate and a slowdown in nonfarm payroll growth, helped spark a wild week in global markets.

- Next week: CPI (Wed.), Retail Sales (Thu.), Industrial Production (Thu.)

International: Mixed Week for Foreign Central Banks, International Data

- Among this week's central bank announcements, Australia and India held rates steady, and hawkish comments suggest rate cuts are still some months away. Mexico's central bank cut rates 25 bps, given soft growth and despite elevated inflation, while we still see gradual easing going forward. In this week's economic figures, Japan's wage data were sturdy, while labor market data from Canada and New Zealand were mixed.

- Next week: U.K. CPI (Wed.), Japan GDP (Thu.), China Industrial Production and Retail Sales (Thu.)

Credit Market Insights: Households Are Feeling the Pinch

- The Q2 New York Fed Household Debt & Credit report signaled that even as households continue to borrow, debt has increased at a slower rate in recent quarters, suggesting consumers may be feeling the pinch of higher rates.

Topic of the Week: Have Lower Bond Yields Started the Easing Process Early?

- A monetary policy pivot looks to be forthcoming. A move down in long-term interest rates has raised hopes that the easing process may already be under way. Unfortunately, lower mortgage rates have yet to result in a meaningful pickup in the mortgage demand, one sector of the economy most likely to benefit from reduced rates.

Is the US Data that Bad to Justify a Rate Cut?

- The recent acute market reaction occurred due to increased recession fears

- Surprise indices point to a more balanced US economic situation

- Recessions tend to be caused by one-off major events

The recent market drop has been attributed to higher chances of a US recession

It has been a very volatile period in markets. The recent higher-than-expected rate hike by the BoJ caused a knee-jerk reaction in Japanese stock markets that led to the yen making significant gains across the board. Amidst this fragile environment, the Fed's choice to avoid a dovish shift did not probably sit well with equity investors who took advantage of the weak US labour market report to stage a strong correction in US stocks.

The increased fear of a US recession has been touted as the key reason for the recent market angst, prompting calls for aggressive rate cuts by the Fed. The market quickly priced in 125bps of total easing in 2024 with this level dropping to around 100bps at the time of writing. The market is currently assigning a 50% probability for a 50bps move at the September Fed gathering.

Is the recent data justifying the market's fear about recession? Or are equities just experiencing a long-due correction?

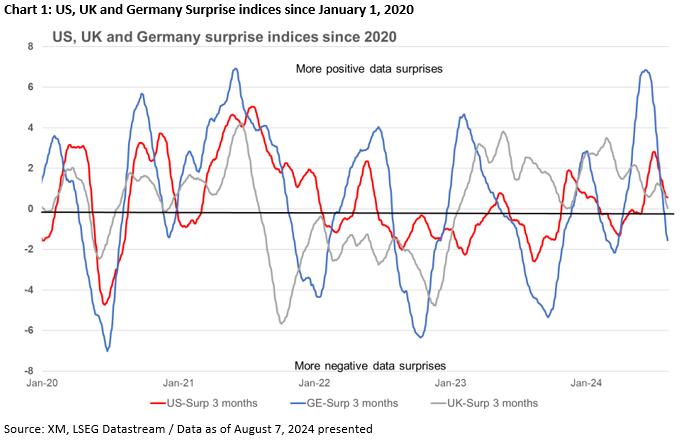

A quick look at the US surprise index

In an earlier special report, our custom-made surprise indices were presented. The intention was to (a) identify the current state of economic surprises in each region, (b) compare the different regions, and (c) examine whether these indices confirm or even lead to the performance of key financial assets.

Despite being still in an embryonic state, these surprise indices try to adequately present the current economic sentiment. As seen in Chart 1 below, the US surprise index, created using a 3-month rolling period of economic data releases, peaked in late June and has been dropping since.

This means that over the past three months data releases in the US have been weakening compared to their previous prints, and that data surprises have been more negative than positive. However, the index remains in positive territory, and it is still quite far from the 2020 low, which was caused by the outbreak of the COVID pandemic. Therefore, based on this surprise index the US economy is not exactly falling off a cliff, as Fed Daly very eloquently commented earlier this week.

Recessions tend to be caused by one-off events?

The last two recessions in the US coincided with significant one-off events that almost crashed the global economy. More specifically, the COVID pandemic in 2020 led to an abrupt drop in economic activity that immediately caused an acute risk-off reaction in markets. Similarly, the subprime mortgage crisis that commenced in 2007 led to the so-called "great recession" of 2007-2009, which eventually morphed into the euro area debt crisis.

Moving further back, the dot-com bubble bust that led to the 2001 slowdown could be, on the margin, compared with the current situation. But then again, a one-off event, the tragic September 11 events in the US, exacerbated the weakened economic momentum and forced the Fed to aggressively cut its interest rate with the government also announcing numerous tax breaks.

Another market crash could open the door to aggressive Fed rate cuts

With a US recession still viewed as unlikely, the market might be trying to force the Fed’s hand into aggressively cutting rates. The Fed remains focused in meeting its dual mandate of price stability and full employment, but it is also very attentive to financial stability issues.

Market participants are aware of the Fed’s sensitivity to stock market crashes, the famous "Fed-put". A market crash could be one of the few reasons that the Fed opts for a 50bps rate cut in September and keeps the door open to further action down the line, if needed.

Interestingly, the last time the Fed aggressively cut interest rates was in March 2020 when in two unscheduled meetings a total of 150bps of easing was announced, 50bps on March 3 and 100bps on March 15.

Putting everything together, the Fed’s choice to avoid a dovish shift at its late July gathering, partly due to the US economy performing adequately, might have contributed to the recent market reaction. By utilizing recession fears and the yen-driven market angst, certain investors might have tried to push the Fed into aggressive rate cuts. With the chances of a 50bps September rate cut dropping to around 50%, barring a major one-off event, certain market participants could be in for a disappointment in September.

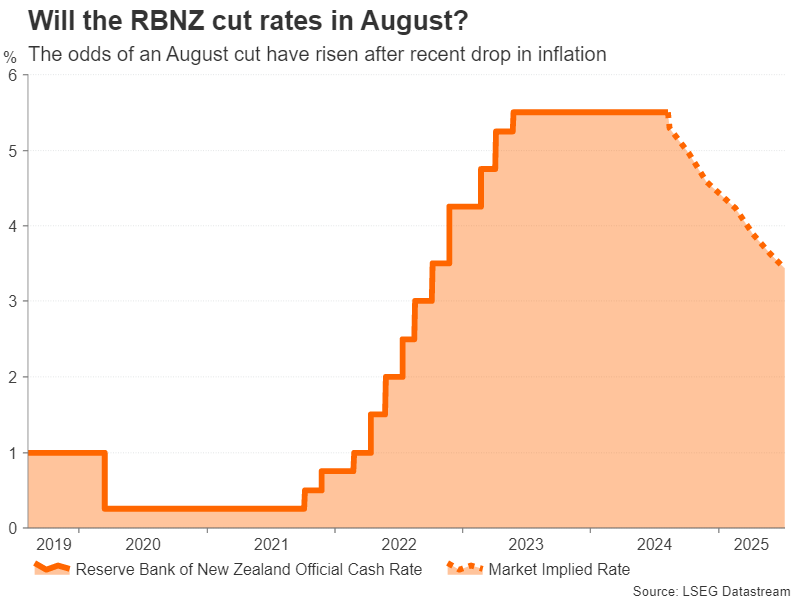

Week Ahead – US CPI to Test Market Nerves, RBNZ Might Cut Rates

- Market turmoil has eased, but will US CPI stir things up again?

- Crucial week for sterling as UK CPI, GDP and retail sales on the way

- The RBNZ is edging closer to a rate cut, but will it be next week?

- Japanese GDP, Australian jobs and Chinese data eyed too

US economy worries take front and centre

The panic about the US economy being on the verge of a recession has mostly eased but markets remain jittery. Investors see a real risk that the Fed’s delay in cutting rates has made a downturn inevitable. Sticky inflation is the main reason why the Fed has stayed this cautious. But inflationary pressures finally seem to be receding in a more sustainable manner.

Next week’s CPI report is expected to underscore this trend and in the absence of any surprises, the data may not do much in allaying the slowdown fears as the focus has shifted somewhat to the growth side of the story. But in the event that the inflation numbers shock either to the upside or downside, the ripple effects will certainly be more notable.

CPI to likely maintain downward trajectory

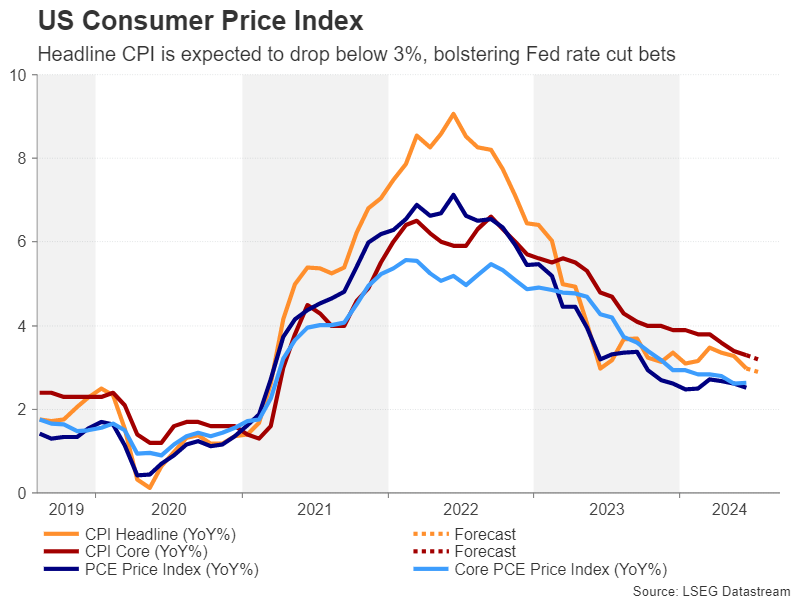

The headline rate of CPI is expected at 2.9% y/y in July, easing slightly from the prior 3.0%. The month-on-month figure is anticipated to have accelerated, however, from -0.1% to 0.2%. Core CPI is forecast to slow too on an annual basis from 3.3% to 3.2%, but inch up from 0.1% to 0.2% month-on-month.

A large upside surprise would be the worst outcome for the markets as it would mean the Fed won’t be able to slash rates very rapidly even as the economy is losing steam. On the other hand, a big miss would likely boost expectations that the Fed will cut rates by 50 basis points in September, cheering investors.

A busy US agenda

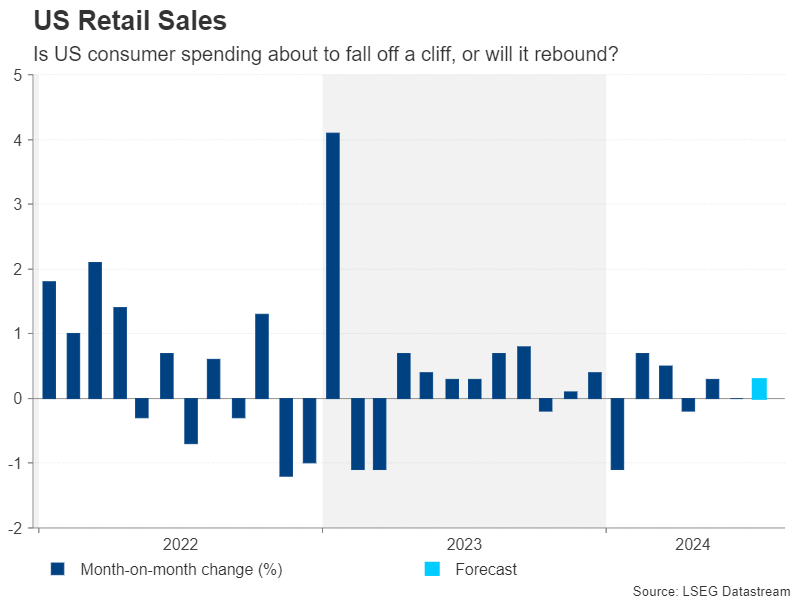

The CPI numbers are due on Wednesday and will be preceded by producer prices on Tuesday, while on Thursday, the spotlight will turn to retail sales. After flat growth in June, retail sales are forecast to have risen by 0.3% month-on-month in July, which may go some way in calming fears about a recession.

On Friday, the University of Michigan’s consumer sentiment survey will also be important, in particular, the inflation expectations for the next one and five years. Other releases will include the New York and Philly Fed’s manufacturing gauges, as well as industrial production for July, all out on Thursday, while on Friday, building permits and housing starts will attract some attention too.

If the upcoming data give a further green light to aggressive rate cuts, the US dollar could come under renewed pressure, having barely rebounded from the past week’s selloff.

Pound on the backfoot ahead of UK data flurry

The pound has retraced almost all its July gains, underperforming all other majors this month apart from the dollar. Although the Bank of England’s rate cut is to blame for some of this weakness, the riots across English cities have also been weighing on sterling as they’ve occurred just as investors had priced out political risks for the UK.

However, the focus over the next seven days will firmly be on the economy, starting with the labour market report on Tuesday. A somewhat cooler labour market has helped wage growth moderate to 5.7% y/y but ideally, BoE policymakers will need to see a further drop before being ready to lower rates again.

July CPI figures will follow on Wednesday and could be key to shaping rate cut expectations for the BoE’s September gathering as the odds for a second 25-bps reduction currently stand at around 30%. Headline inflation was unchanged at 2.0% in June – bang on the BoE’s target. But it probably edged up in July to 2.3% y/y, supporting the reasoning behind the hawkish cut at the August meeting.

Investors will also be keeping a close eye on services CPI, which like wages, remains elevated.

On Thursday, the UK will publish preliminary GDP readings for the second quarter. The economy is projected to have expanded by 0.7% q/q in Q2, maintaining the same pace as in Q1. Rounding up the weekly releases on Friday will be July retail sales.

Although the likelihood of a back-to-back rate cut in September is quite low, a broadly soft set of data could nevertheless push up market expectations, in a further setback for sterling.

Will the RBNZ join the rate-cut club?

The Reserve Bank of New Zealand meets on Wednesday for its latest policy decision. Economists are not anticipating any change but there is growing consensus among traders that the RBNZ will announce a 25-bps reduction in the cash rate. Easing expectations started to gain traction after the previous meeting when policymakers sounded upbeat about the prospect of inflation returning to the 1-3% target range in the second half of this year, which was later backed by the Q3 CPI report that showed inflation falling to 3.3%.

Further building the case for looser policy was the RBNZ’s own survey on inflation expectations that pointed to the lowest expectations in more than three years.

Subsequently, investors have ramped up their bets for an August cut to about 80% so should the RBNZ decide to proceed with one, the New Zealand dollar will probably not suffer huge losses unless policymakers signal that more are on the way.

Can the aussie extend its recovery?

With the RBNZ looking certain to begin reducing rates later this year if not at the August meeting, the RBA is increasingly becoming the odd one out. Governor Michelle Bullock has pushed back on market bets of a cut anytime soon, but investors still see a reasonable chance of a move by December.

Nonetheless, the RBA’s hawkish stance is supporting the Australian dollar’s rebound attempt against the greenback, although next week’s releases may pose a downside risk. The wage price index for the second quarter is due on Tuesday and the employment report for July is coming up on Thursday.

In addition to domestic indicators, aussie traders will also be watching China’s latest monthly data dump. The July readings for industrial production, retail sales and fixed asset investment are out on Thursday. Any disappointment, especially with retail sales, would add to concerns that China’s economy is stuck in the slow lane, possibly hurting the aussie.

Yen bulls look to Q2 GDP

Finally in Japan, second quarter GDP numbers are due on Thursday. The data will be vital for the Bank of Japan where there’s an ongoing debate about whether the economy is strong enough to withstand higher interest rates. Other releases will include corporate goods prices on Tuesday and machinery orders on Friday.

The yen rally is currently taking a breather after the impressive gains over the past month. However, a print that’s stronger than the expected 0.5% q/q could revive the bulls.

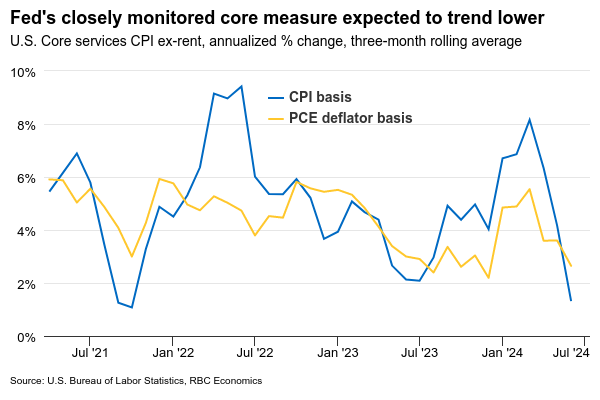

U.S. Inflation Likely Held Steady in July

All eyes will be on Wednesday’s U.S. inflation print after a larger-than-expected increase in the unemployment rate and softening in the manufacturing sector a week ago heightened concerns that the Federal Reserve may need to respond with more aggressive interest rate cuts than previously thought.

Economic data since then have somewhat calmed concerns with the U.S. services purchasing managers index pointing to further expansion and initial jobless claims edging lower in the past week. Still, we expect further signs of easing inflation in July. We forecast headline price growth held at 3% on an annual basis but with a second straight small 0.1% monthly increase in core (excluding food and energy) prices. That should reassure the Fed that those annual rates will continue to move lower.

In June, the Fed’s “supercore” (core services ex-rent) measure posted its lowest reading on a three-month annualized basis since October 2021 at 1.3%. The breadth of inflationary pressures has narrowed in recent months and the share of products seeing inflation above 5% has returned to pre-pandemic levels. Home rents continue to account for a disproportionate share of the remaining annual price growth. But, it is slowing as the impact of earlier easing in market rent increases eventually passes through to lease agreements.

U.S. economic growth (or inflation) numbers haven’t hit a level yet that would push Fed officials to panic. But, it is becoming increasingly difficult to justify interest rates more than 200 basis points above the Fed’s own estimate of the long-run “neutral” rate. Evidence is building that broader economic conditions have already normalized and inflation is more likely to drift lower. Our base case assumption is that the Fed will cut the fed funds target range by 25 basis points in September and risks of a larger cut are contingent on further downside in economic growth or inflation surprises.

Week ahead data watch

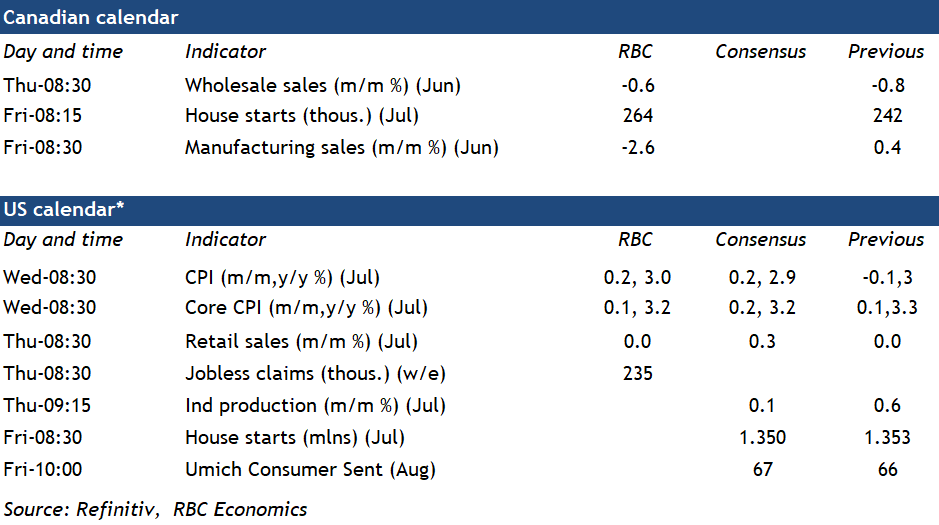

According to StatCan’s early indicator, core wholesales sales were down 0.6% in June. Much of that weakness came from the sales decline in the motor vehicle and motor vehicle parts and accessories subsector, as well as the food, beverage, and tobacco subsector.

We expect manufacturing sales to drop by 2.6% in June, in line with StatCan’s prelim estimates, driven by lower sales in the chemical product and transportation equipment subsectors.

Canadian housing starts likely came in at 264K in July. That would be up 9.2% from June to reverse the 8.8% decline the prior month. Building permits trended higher during recent months, with the three-month rolling average value increased from 257K in March to 286K in May.

U.S. retail sales are likely little changed from last month. Higher auto sales and a price-related sales growth at gas stations were offsetting by the decline in control sales.

Canada’s Job Market Softens Further in July

For the second straight month, Canadian employment was essentially unchanged (-2.8k), disappointing expectations for a modest 25k gain. Full-time positions rebounded (+62k), but were offset by sizeable part-time job losses (-64k).

The unemployment rate also remained unchanged at 6.4%, as a slight decline in the labour force (-0.1% month-on-month (m/m)) offset job losses. The decline in the labour force came despite continued growth in population (0.4% m/m), as the labour force participation rate continued to fall to 65% in July.

Although population aging has put downward pressure on the labour force participation rate, the most recent year-over-year decline in July 2024 largely reflected declines among people under the age of 65.

Looking across sectors, job gains were concentrated in the public sector (+41k). The private sector lost jobs in July (-42k). Wholesale and retail trade led the private sector in job losses (-44k), while finance, insurance and real estate (-15k) also shed jobs.

Unemployment rates for recent immigrants to Canada and youth continued to rise. The unemployment rates for immigrants who have landed in Canada within the last five years rose 3.1 percentage points to 12.6%. And it continues to be a cruel summer for students (aged 15 to 24), with the employment rate was 51.3% in July – the lowest since 1997 (outside of the pandemic 2020).

Lastly, total hours rebounded in July (1.0% m/m), leaving them up 1.9% over the past year. Wage growth cooled modestly to 5.2% year-on-year in July.

Key Implications

July's job market report was a bit of a mixed bag on the surface, but most trends are consistent with a labour market that continues to cool. Sure, full-time jobs rose, but over the past year part-time employment (+3.4%; +122,000) has grown at a faster pace than full-time employment (+1.4%; +224,000). Recent immigrants and youth are facing a particular deterioration in job market conditions.

The labour market is giving the OK for the Bank of Canada to continue its gradual quarter-point cut per rate announcement pace. We expect the Bank to cut interest rates three more times this year (see rates forecasts).