Sample Category Title

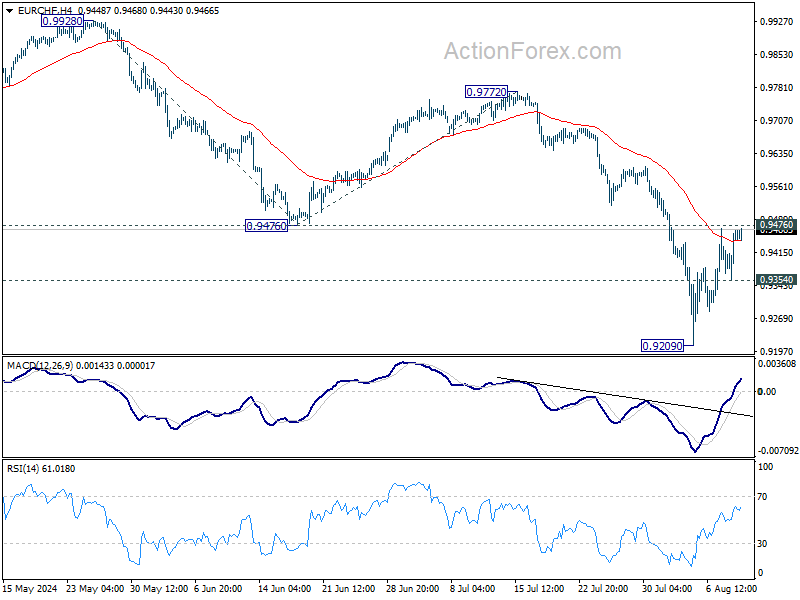

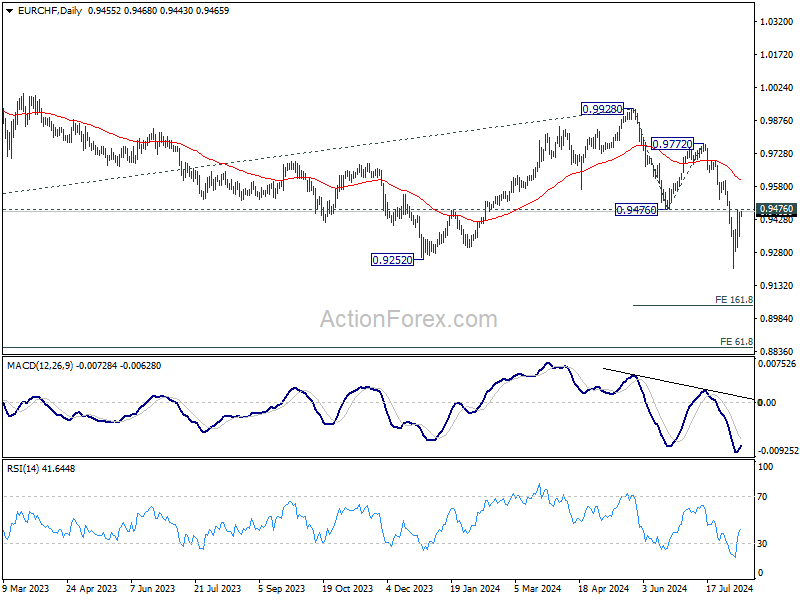

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9390; (P) 0.9428; (R1) 0.9500; More....

Intraday bias in EUR/CHF remains neutral and further decline is expected with 0.9476 support turned resistance intact. On the downside, below 0.9354 minor support will bring retest of 0.9209 first. Firm break there will resume larger fall from 0.9928 to 161.8% projection of 0.9928 to 0.94767 from 0.9772 at 0.9041 next. However, sustained break of 0.9476 will turn bias back to the upside for stronger rebound.

In the bigger picture, current downside acceleration argues that medium term corrective pattern from 0.9407 (2022 low) might have completed with three waves to 0.9928. Decisive break of 0.9252 (2023 low) will confirm long term down trend resumption. Next target will be 61.8% projection of 1.1149 to 0.9407 from 0.9928 at 0.8851. For now, outlook will stay bearish as long as 0.9928 resistance holds, even in case of strong rebound.

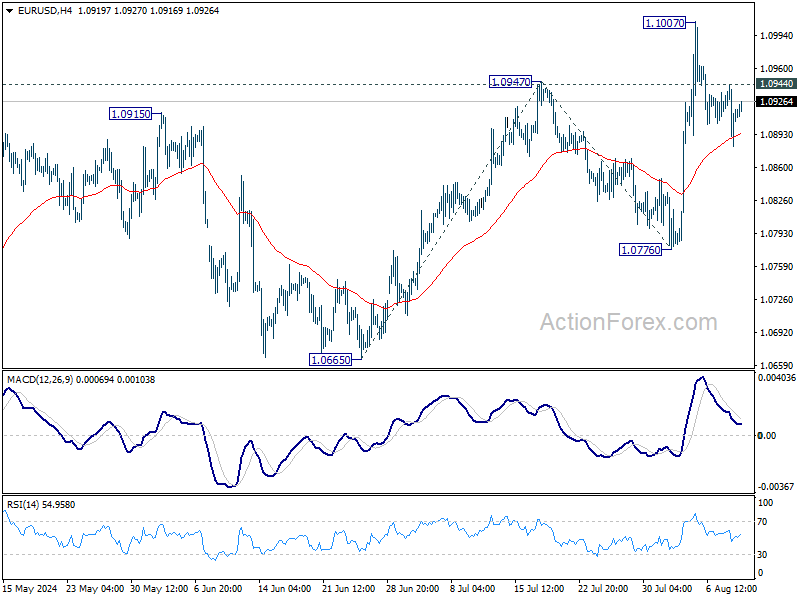

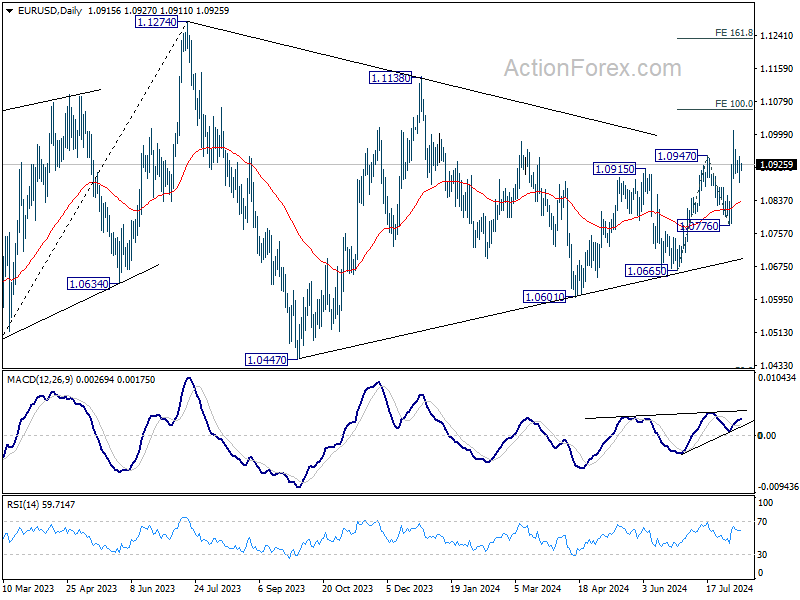

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0886; (P) 1.0915; (R1) 1.0949; More.....

Intraday bias in EUR/USD remains neutral first and outlook is unchanged. While deeper retreat cannot be ruled out, downside should be contained well above 1.0776 support. On the upside, above 1.0944 minor resistance will bring retest of 1.1007 first. Further break there will resume recent rally from 1.0665 to 100% projection of 1.0665 to 1.0947 from 1.0776 at 1.1056 next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0776 support will extend the correction with another falling leg back towards 1.0447 support.

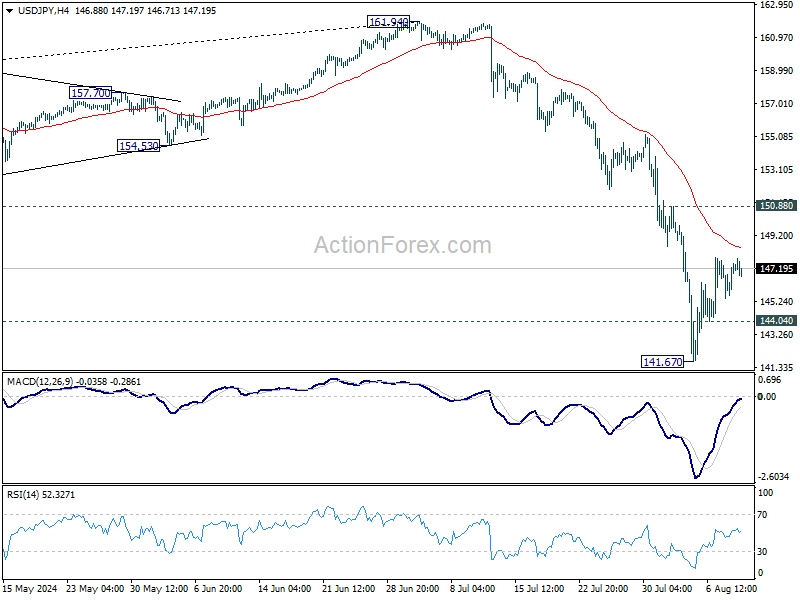

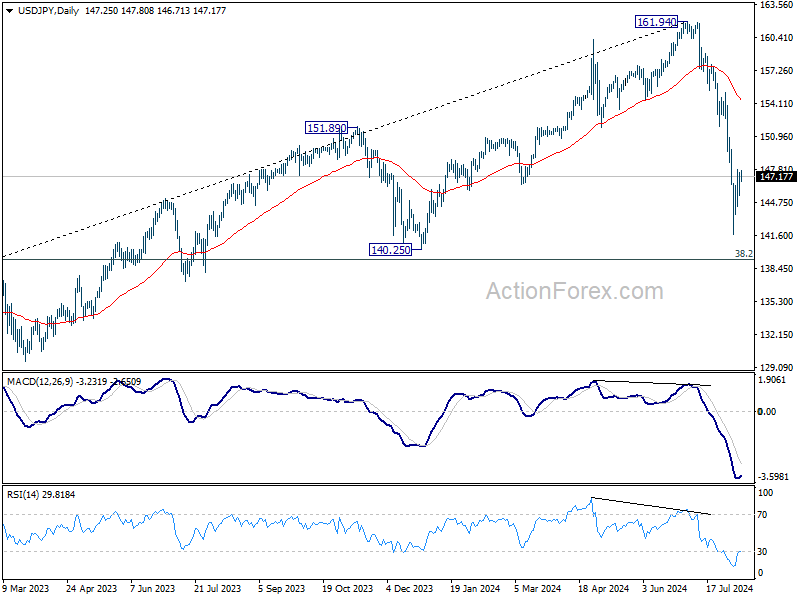

USD/JPY Daily Outlook

Daily Pivots: (S1) 145.96; (P) 146.76; (R1) 148.07; More...

Intraday bias in USD/JPY remains neutral and outlook is unchanged. While further rise cannot be ruled out, outlook will stay bearish as long as 150.88 resistance holds. On the downside, below 144.04 minor support will bring retest of 141.67 first. Break there will resume the fall from 161.94 to 140.25 support next.

In the bigger picture, the strong break of 55 W EMA (now at 149.98) argue that fall from 161.94 medium term is correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.83) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

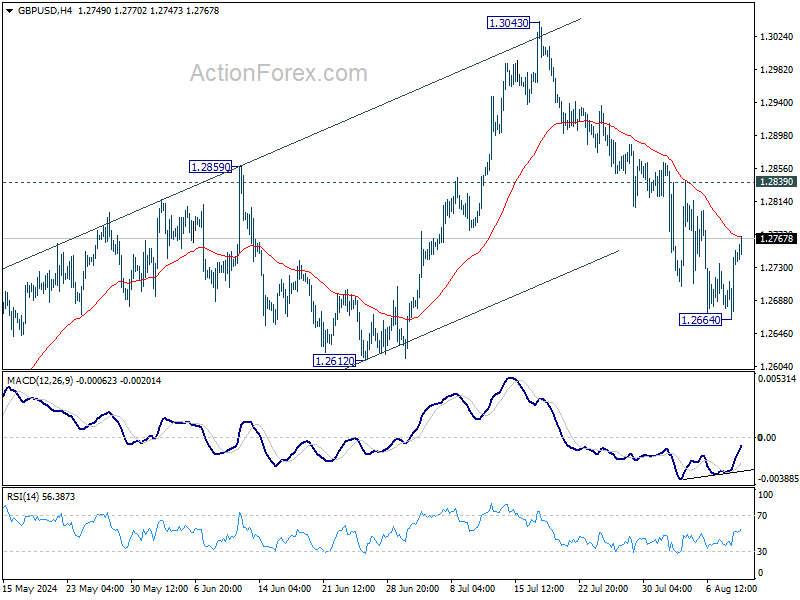

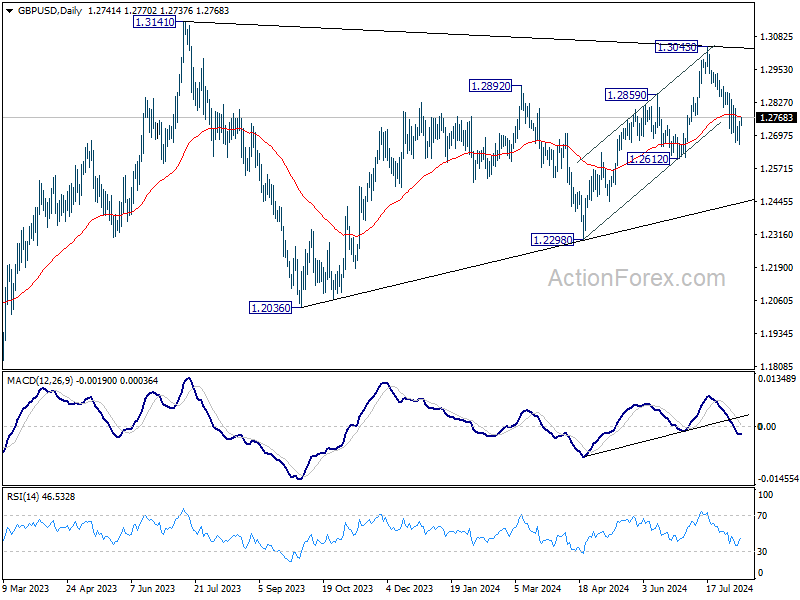

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2693; (P) 1.2722; (R1) 1.2780; More...

Intraday bias in GBP/USD is turned neutral first with current recovery. Another fall is in favor as long as 1.2839 resistance holds. Below 1.2664 will target 1.2612 support. Decisive break there should confirm that rise from 1.2298 has completed, and target this support next. However, break of 1.2839 resistance will argue that the pull back from 1.3043 has completed and turn bias back to the upside.

In the bigger picture, current development suggests that corrective pattern from 1.3141 is extending with fall from 1.3043 as another leg. Break of 1.2612 support would strengthen this case. But still, downside should be contained by 1.2036/2298 support zone even in case of deep decline. Rise from 1.0351 (2022 low) remains in favor to resume at a later stage.

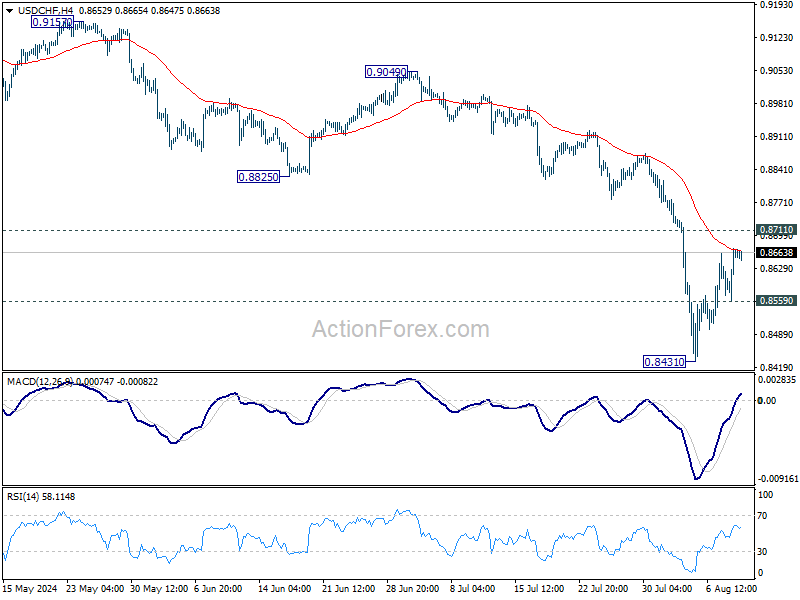

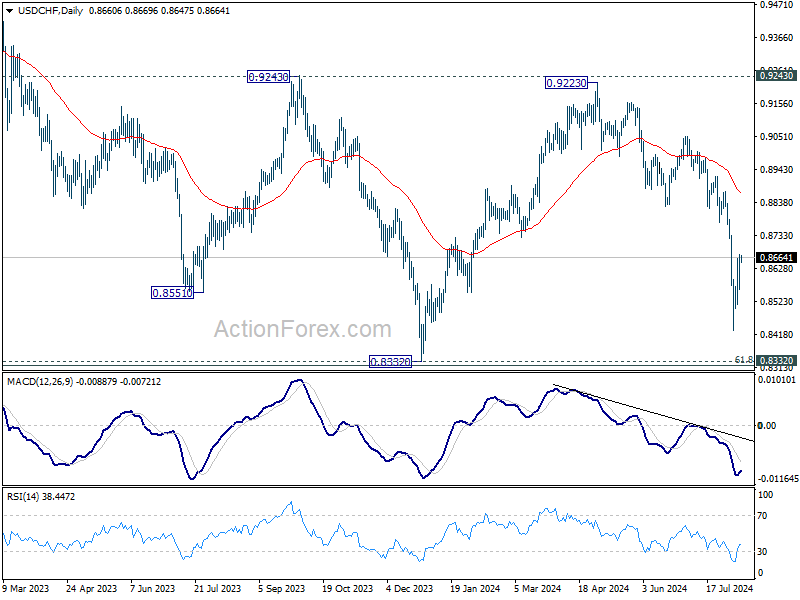

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8593; (P) 0.8634; (R1) 0.8707; More…

While USD/CHF's recovery from 0.8431 extends but upside is limited below 0.8711 resistance. Intraday bias remains neutral and further decline is still expected. On the downside, below 0.8559 minor support will bring retest of 0.8431 first. Break there will resume the fall from 0.9223 to retest 0.8332 low. However, sustained break of 0.8711 will turn bias back to the upside for stronger rebound.

In the bigger picture, price actions from 0.8332 (2023 low) are currently seen as a medium term corrective pattern, with fall from 0.9223 as the second leg. Strong support could be seen from 0.8332 to bring rebound. Yet, overall outlook will continue to stay bearish as long as 0.9243 resistance holds. Firm break of 0.8332, however, will resume larger down trend from 1.0146 (2022 high).

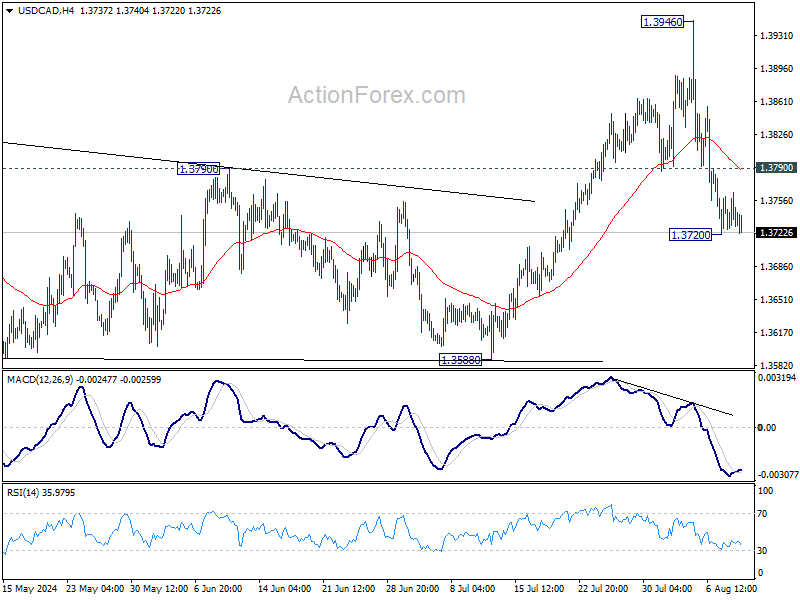

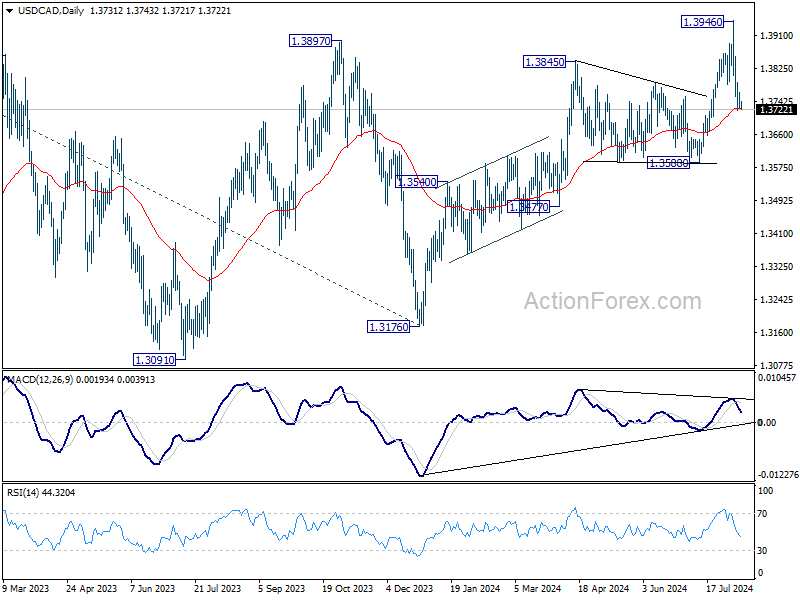

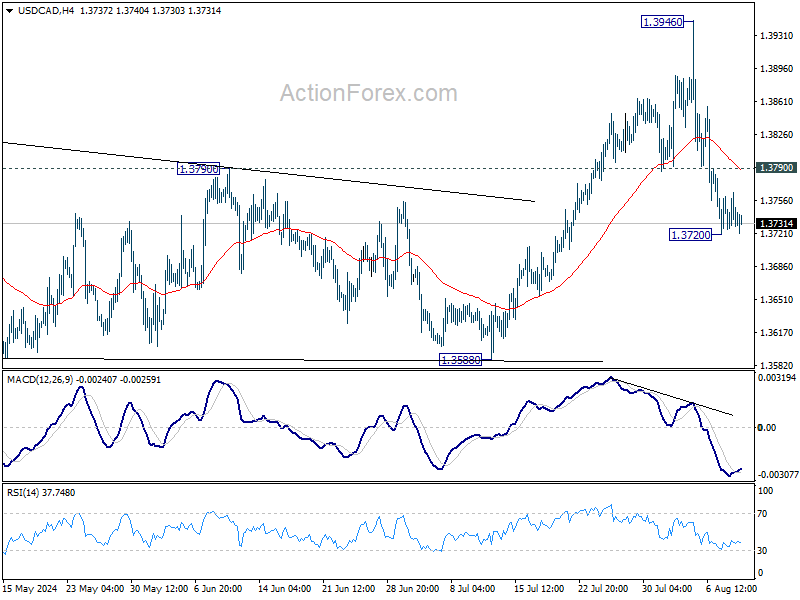

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3719; (P) 1.3742; (R1) 1.3759; More...

Intraday bias in USD/CAD is turned neutral first with current recovery. But further fall is expected as long as 1.3790 resistance holds. Break of 1.3720 and sustained trading below 55 D EMA (now at 1.3726) would dampen the original bullish outlook and bring deeper fall to 1.3588 support. On the upside, above 1.3790 minor resistance will bring retest of 1.3946 instead.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.

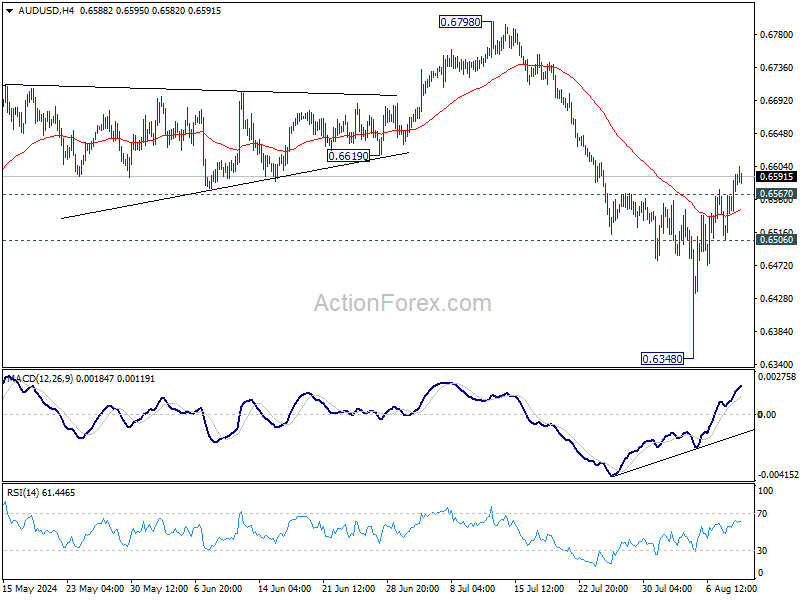

AUD/USD Daily Report

Daily Pivots: (S1) 0.6535; (P) 0.6565; (R1) 0.6622; More...

AUD/USD's break of 0.6567 resistance confirms short term bottoming at 0.6348 and stronger rebound is underway. Intraday bias is back on the upside for 55 D EMA (now at 0.6614). Sustained break there will target 0.6798 resistance. On the downside, break of 0.6506 minor support will turn bias back to the downside for retesting 0.6348 instead.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with fall from 0.6798 as another falling leg. Deeper fall could be seen to the lower side of the range between 0.6169/6361. But strong support should be seen there to contain downside. For now, risk will stay on the downside as long as 55 D EMA (now at 0.6614) holds, in case of rebound.

US Stock Rebound Fails to Boost Asian Markets, Focus on Canadian Jobs Data

The US stock market rebounded notably overnight, with all three major indexes closing higher. However, this positive momentum didn't carry over to the Asian session, where major markets are trading mixed. Despite the gains in the US, the price actions this week still appear more corrective than not, indicating that selling pressure has only temporarily eased rather than fully dissipated. With no major US events scheduled for today, this consolidative mood is likely to persist, potentially extending until next week's CPI release.

In the currency markets, Australian Dollar is currently the strongest performer for the week, followed by New Zealand Dollar and Canadian Dollar. On the other hand, Swiss Franc is the weakest, with British Pound and Japanese Yen also lagging. Euro and Dollar are positioned in the middle.

Today's focus will be on Canadian employment data. Earlier this week, BoC's July meeting minutes revealed concerns among some members that further labor market weakness could delay the rebound in consumption, exerting downward pressure on both growth and inflation. Such developments might push the BoC to consider normalizing interest rates from the current restrictive levels to a more neutral stance.

Technically, USD/CAD is worth some attention today. Fall from 1.3946 slowed after hitting 1.3720, as seen in 4H MACD. Rebound from current level, followed by break of 1.3790 minor resistance will suggest that the corrective pullback is over, and kept the rise from 1.3716 intact. However, downside re-acceleration from there would indicate that deeper correction is underway, probably through 1.3588 support.

In Asia, at the time of writing, Nikkei is down -0.65%. Hong Kong HSI is up 1.41%. China Shanghai SSE is down -0.01%. Singapore Strait Times is up 0.37%. Japan 10-year JGB yield is up 0.0276 at 0.860. Overnight, DOW rose 1.76%. S&P 500 rose 2.30%. NASDAQ rose 2.87%. 10-year yield rose 0.029 to 3.997.

Fed's Barkin: Disinflation trend positive, economy offers time for deliberate rate decisions

Richmond Fed President Tom Barkin expressed optimism about the ongoing disinflation trend during a virtual event overnight.

Barkin noted that recent data has been encouraging, both in overall levels and across various inflation components, stating that "all the elements of inflation seem to be settling down." He remains "relatively hopeful" that this trend will persist.

Barkin also highlighted that the current economic environment provides some leeway to assess whether the economy is gradually normalizing, which would allow for a steady and deliberate approach to rate adjustments. He pointed out the importance of determining if further aggressive action is necessary, depending on how the economy evolves.

Goolsbee: Fed's focus on economy, not stock market or elections

Chicago Fed President Austan Goolsbee reiterated concerns about the current stance of monetary policy in a Fox interview, warning that maintaining high borrowing costs, even as inflation declines, could further tighten financial conditions and potentially harm the labor market. Goolsbee stressed the importance of balancing monetary policy to avoid unnecessary damage to employment.

He also made it clear that Fed's decisions are driven solely by economic considerations, not by the stock market or political factors. Goolsbee stated, "The Fed's out of the election business. The Fed is in the economic business," emphasizing that the focus remains on maximizing employment and stabilizing prices.

Fed's Schmid: Further labor market cooling needed before rate cut

Kansas City Fed President Jeff Schmid acknowledged that while inflation is nearing the Fed's 2% target, currently at around 2.5%, "we are still not quite there."

Nevertheless, "if inflation continues to come in low, my confidence will grow that we are on track to meet the price stability part of our mandate, and it will be appropriate to adjust the stance of policy," Schmid said at a bankers' event overnight.

Despite fears sparked by a weak jobs report, Schmid pushed back against the notion that Fed would need to take aggressive action to avoid a recession. He described the economy as resilient, with strong consumer demand and a labor market that, although cooling, remains "quite healthy."

Schmid noted that Fed's current policy stance "is not that restrictive" and suggested that further cooling in the labor market may be necessary to achieve additional declines in inflation.

China's CPI rises to 0.5% in Jul, driven by surging food prices

China's CPI rose by 0.5% yoy in July, up from June's 0.2% yoy surpassing expectations of 0.4% yoy and marking the highest increase since February. This uptick was driven in part by a significant 20.4% yoy surge in pork prices, the highest since December 2022. Core CPI, which excludes food and energy prices, saw a slower rise of 0.4% yoy, down from 0.6% yoy in June.

On a month-over-month basis, CPI rebounded with a 0.5% increase, reversing the -0.2% decline seen in June and exceeding expectation of 0.3% rise. The rise in food prices, driven by high temperatures and heavy rainfall in some regions, contributed significantly to this monthly growth, according to NBS statistician Dong Lijuan.

Meanwhile, China's PPI as unchanged at -0.8% yoy, slightly better than the expected -0.9%.

Looking ahead

Germany CPI final and Swiss SECO consumer climate will be released in European session. Canada employment data is the main focus later in the day.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6535; (P) 0.6565; (R1) 0.6622; More...

AUD/USD's break of 0.6567 resistance confirms short term bottoming at 0.6348 and stronger rebound is underway. Intraday bias is back on the upside for 55 D EMA (now at 0.6614). Sustained break there will target 0.6798 resistance. On the downside, break of 0.6506 minor support will turn bias back to the downside for retesting 0.6348 instead.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with fall from 0.6798 as another falling leg. Deeper fall could be seen to the lower side of the range between 0.6169/6361. But strong support should be seen there to contain downside. For now, risk will stay on the downside as long as 55 D EMA (now at 0.6614) holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 01:30 | CNY | CPI Y/Y Jul | 0.50% | 0.40% | 0.20% | |

| 01:30 | CNY | PPI Y/Y Jul | -0.80% | -0.90% | -0.80% | |

| 06:00 | EUR | Germany CPI M/M Jul F | 0.30% | 0.30% | ||

| 06:00 | EUR | Germany CPI Y/Y Jul F | 2.30% | 2.30% | ||

| 07:00 | CHF | SECO Consumer Climate Q3 | -36 | -37 | ||

| 12:30 | CAD | Net Change in Employment Jul | 26.9K | -1.4K | ||

| 12:30 | CAD | Unemployment Rate Jul | 6.50% | 6.40% |

Cliff Notes: Varied Assessments of Risk

Key insights from the week that was.

Following a tumultuous start to the week for global markets after a disappointing US employment print (see below), the RBA made clear their views on the risks the Australian economy faces. The RBA’s decision to leave the cash rate unchanged at 4.35% was not the focus for markets, even though the probability of such an outcome was being extensively debated not too long ago. Rather, participants quickly turned to the RBA’s updated assessment of the economy, epitomised by the judgement that “there is more excess demand in the economy and the labour market than previously thought”. Given the RBA’s forecasts for economic growth, trimmed mean inflation and the unemployment rate were only revised at the margin, the foundation of the Board’s reassessment is seemingly model-based estimates of the balance between the level of demand and supply which, in the RBA’s words, have “considerable uncertainty”.

The main takeaway from the RBA’s perspective is that this imbalance is “resulting in persistent inflation”, leading Governor Bullock in a speech the following day to assert that the Board “will not hesitate to raise rates” should there be upside risks around the inflation outlook. Regarding rate cuts, Governor Bullock’s press conference following the decision was forthright, telegraphing that the scenario of a rate-cut by year-end, as per current market pricing, “does not align with [the Board’s] thinking”.

As detailed by Chief Economist Luci Ellis following these developments, we have revised our RBA view, with the first cash rate cut now expected in February 2025 instead of November 2024 – uncertainty around the narrow path to target pointing to a higher hurdle before the Board can be confident in inflation’s deceleration. We still anticipate rate cuts to ensue at a measured pace of 25bps per quarter through to Q4 2025, albeit now to a slightly higher terminal rate of 3.35%.

In the US at the end of last week, non-farm payrolls disappointed, rising 114k (consensus 175k). The prior two months were also revised down by a cumulative 29k. Arguably more unnerving for markets, the unemployment rate rose 0.2ppts to 4.3%, triggering the ‘Sahm Rule’. This indicator states that a recession has started once the three-month moving average of the unemployment rate is 0.5ppts above the lowest three-month average of the past 12 months. This evidence of deteriorating labour market conditions kept participants on guard throughout the week.

FOMC members Goolsbee and Barkin sought to steady sentiment by emphasising that one month's data does not constitute a trend. However, Goolsbee also made it clear he believed policy was materially restrictive and the longer it remains that way, the more policymakers' focus has to turn to the employment side of the mandate. Helping the FOMC’s case by pointing to the resilience of the US economy, the ISM services PMI bounced in July to 51.4, supported by gains in all but two sub-indices in the month. Of particular note, the employment index rose 5pts, breaking a five-month run of contractionary reads. Cheered by the market late in the week, initial jobless claims fell last week and remain near historic lows, providing further support for the view that US employment might be stalling, but there is no evidence of significant aggregate job loss across the economy.

While not a focus for the market, responses to the July Senior Loan Officer Survey were cautious but benign for the growth trend, with "tighter standards and basically unchanged demand for commercial and industrial (C&I) loans" in Q2 and "tighter standards and weaker demand for all commercial real estate (CRE) loan categories". For households, banks reported "basically unchanged lending standards and weaker demand across all categories of residential real estate (RRE) loans and lending standards and demand unchanged for home-equity loans. Demand was unchanged for credit cards, but weakened for other forms of consumer credit.

As US inflation continues to come down and with downside risks growing, there is reason for the FOMC to cut decisively into year end and through early-2025. That said, we remain confident in the underlying health of the US economy and believe the FOMC will too, resulting in a more muted easing cycle than the market currently expects. We continue to expect the first cut to be 25bps in September, but now expect another 25bp cut at each of the meetings through November 2024 to March 2025. One cut per quarter from the June quarter 2025 will leave the fed funds rate at 3.375% end-2025. That is the same terminal rate as we had previously, but it will be reached six months earlier. As long as the labour market remains in good health, which we expect, lower interest rates will boost demand into 2025 and ease banks’ concerns over the outlook.

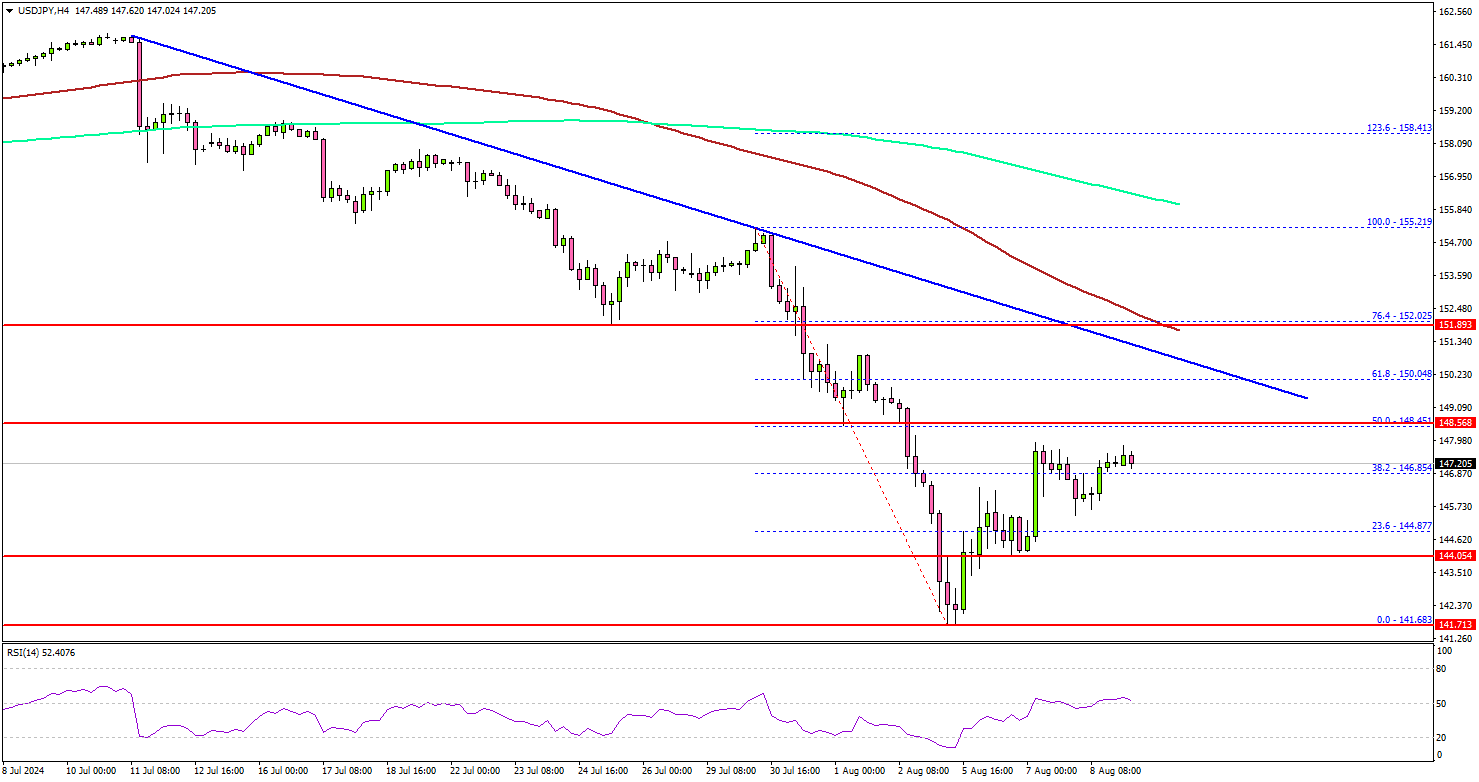

USD/JPY In An Uphill Battle: Can It Push Higher?

Key Highlights

- USD/JPY is attempting a fresh increase from the 141.65 support zone.

- A major bearish trend line is forming with resistance at 150.00 on the 4-hour chart.

- Oil prices might struggle to climb above the $76.60 resistance.

- EUR/USD corrected gains but the bulls seem to be active above 1.0850.

USD/JPY Technical Analysis

The US Dollar started a major decline from well above 155.00 against the Japanese Yen. USD/JPY even declined below 145.00 before the bulls appeared.

Looking at the 4-hour chart, the pair settled below the 150.00 level, the 200 simple moving average (green, 4-hour), and the 100 simple moving average (red, 4-hour). A low was formed near 141.68 before the pair started a recovery wave.

There was a move above the 145.00 level. The pair cleared the 38.2% Fib retracement of the downward move from the 155.21 swing high to the 141.68 low.

Immediate resistance sits near the 148.50 level or the 50% Fib retracement of the downward move from the 155.21 swing high to the 141.68 low. The next resistance sits at 150.00. There is also a major bearish trend line forming with resistance at 150.00 on the same chart.

A clear move above 150.00 could open the door to more gains. In the stated case, the pair could rise and test 152.00 or the 100 simple moving average (red, 4-hour).

Immediate support is near the 145.80 level. The next major support is near the 144.00 level. A downside break and close below the 144.00 support zone could open the doors for more losses. In the stated case, USD/JPY might decline toward the 142.00 level.

Looking at Oil, the price started a recovery wave above the $74.50 level but the bears might remain active near the $76.60 level.

Economic Releases

- Canada’s employment Change payrolls for July 2024 – Forecast 22.5K, versus -1.4K previous.

- Canada’s Unemployment Rate April 2024 - Forecast 6.5%, versus 6.4% previous.