Sample Category Title

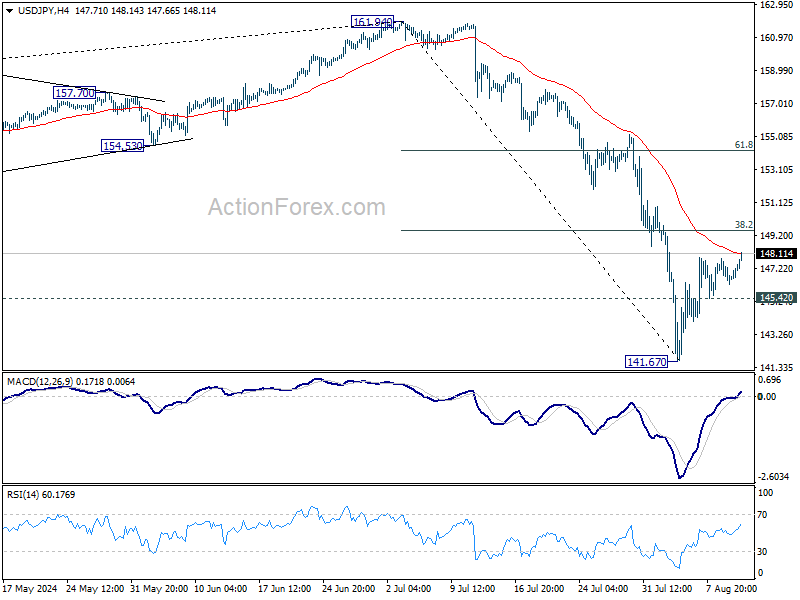

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.96; (P) 146.89; (R1) 147.49; More...

USD/JPY's rebound from 141.67 extends higher today but stays below 38.2% retracement of 161.94 to 141.67 at 149.41. Intraday bias stays neutral and outlook remains bearish. Below 145.42 minor support will turn bias to the downside for 141.67. Break there will resume the fall from 161.94 to 140.25 support next. Nevertheless, decisive break of 149.41 will bring stronger rally to 61.8% retracement at 154.19, even as a corrective move.

In the bigger picture, fall from 161.94 medium term is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.77) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

Yen and Swiss Franc Weaken in Quiet Markets as Focus Shifts to Australian Data

Yen and Swiss Franc weaken slightly in today's subdued trading environment. With the economic calendar offering little in terms of market-moving events during the European and US sessions, currency movements have been minimal. Meanwhile, Australian and New Zealand Dollars are showing modest strength, though most other major currencies are trading within narrow ranges. Other financial markets are similarly quiet, with European stock indexes and benchmark treasury yields in both Europe and US remaining stuck in tight ranges.

Attention is now turning to the upcoming Asian session, where some Australian economic data will be released. This includes Westpac consumer sentiment, NAB business confidence, the wage price index. Among these, wage growth will be closely watched, given its significance for domestic inflationary pressures. RBA has made it clear that it remains uncertain about the need for another rate hike, and Governor Michele Bullock has effectively ruled out the possibility of a rate cut this year. Should the wage growth data come in strong, it would likely solidify RBA's stance and diminish any speculation about rate cuts in the near future.

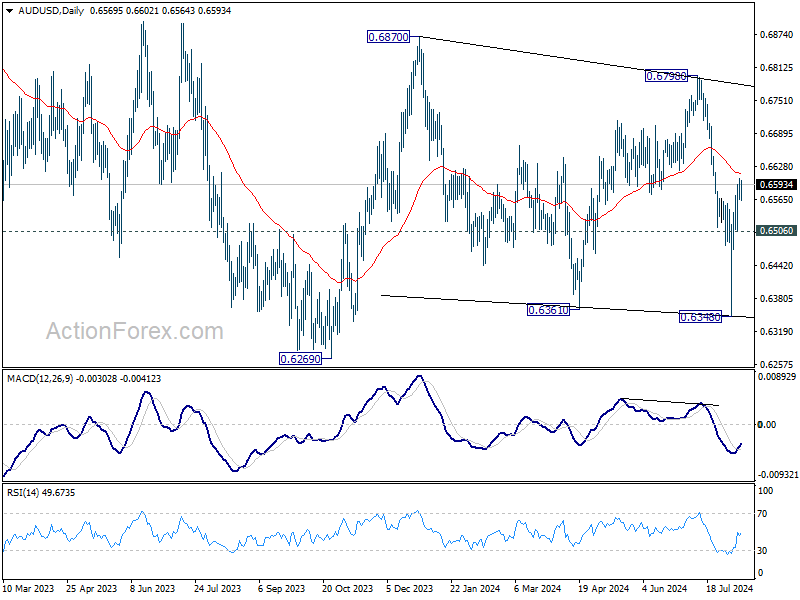

On the technical side, while AUD/USD's rebound from 0.6348 was slightly stronger than expected, it's starting to struggle as it approaches 55 D EMA. Rejection by the EMA, followed by break of 0.6505 support, will retain near term bearishness for another decline through 0.6340 to 0.6269 low. Nevertheless, sustained break of the EMA will pave the way back to 0.6798 resistance. Despite the current technical setup, the true driver of any substantial movement in AUD/USD is likely to come from the US CPI data scheduled for release on Wednesday.

In Europe, at the time of writing, FTSE is up 0.38%. DAX is up 0.12%. CAC is down -0.16%. UK 10-year yield is up 0.0012 at 3.950. Germany 10-year yield is up 0.016 at 2.246. Earlier in Asia, Japan was on holiday. Hong Kong HSI rose 0.56%. China Shanghai SSE rose 0.13%. Singapore Strait Times fell -0.81%.

OPEC downgrades oil demand growth estimates for 2024

OPEC downgraded its global oil demand forecast for 2024, now expecting an increase of 2.11 million barrels per day (bpd), slightly lower than the 2.25 million bpd projected last month. The organization also adjusted its demand growth estimate for next year, lowering it to 1.78 million bpd from the previous forecast of 1.85 million bpd.

These adjustments reflect the actual data received for Q1 of 2024, and in some cases, the Q2, along with ". OPEC noted that while the summer driving season got off to a slower start compared to the previous year, transport fuel demand is anticipated to remain robust, supported by healthy road and air mobility.

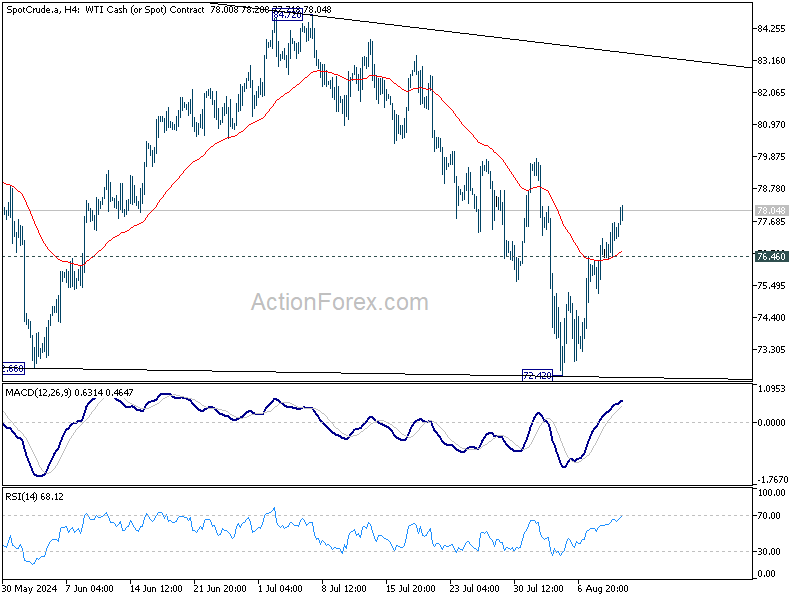

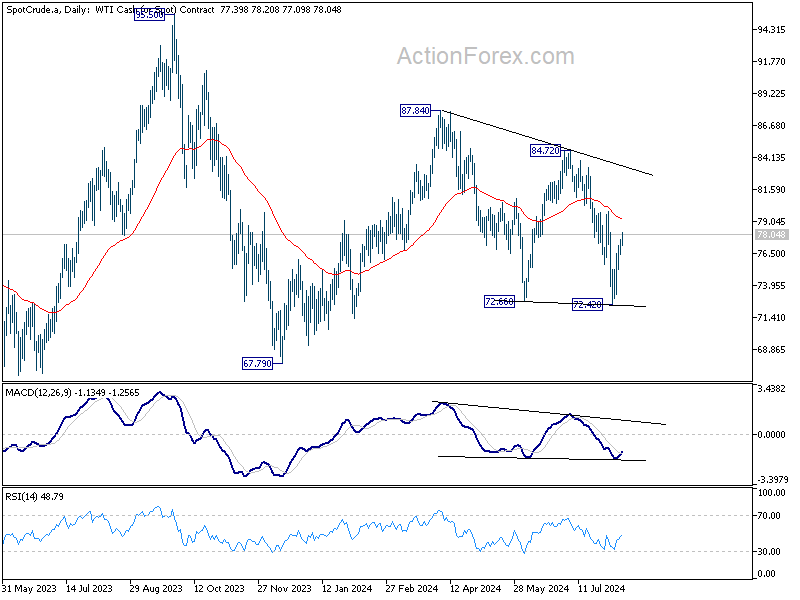

WTI oil shrugs off the downgrade and extends its near term rebound from 72.42. Technically, the strong break of 55 4H EMA suggests that fall from 84.72 has completed already. Further rise is now in favor as long as 76.46 support holds, towards 55 D EMA (now at 79.23). Firm break there will solidify this near term bullish case and target top of the medium term range between 84.72 and 87.84.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 145.96; (P) 146.89; (R1) 147.49; More...

USD/JPY's rebound from 141.67 extends higher today but stays below 38.2% retracement of 161.94 to 141.67 at 149.41. Intraday bias stays neutral and outlook remains bearish. Below 145.42 minor support will turn bias to the downside for 141.67. Break there will resume the fall from 161.94 to 140.25 support next. Nevertheless, decisive break of 149.41 will bring stronger rally to 61.8% retracement at 154.19, even as a corrective move.

In the bigger picture, fall from 161.94 medium term is seen as correcting whole up trend from 102.58 (2021 low). Deeper decline could be seen to 38.2% retracement of 102.58 to 161.94 at 139.26, which is close to 140.25 support. In any case, risk will stay on the downside as long as 55 W EMA (now at 149.77) holds. Nevertheless, firm break of 55 W EMA will suggest that the range for medium term corrective pattern is already set.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 12:30 | CAD | Building Permits M/M Jun | -13.90% | 5.60% | -12.20% | -12.70% |

OPEC downgrades oil demand growth estimates for 2024

OPEC downgraded its global oil demand forecast for 2024, now expecting an increase of 2.11 million barrels per day (bpd), slightly lower than the 2.25 million bpd projected last month. The organization also adjusted its demand growth estimate for next year, lowering it to 1.78 million bpd from the previous forecast of 1.85 million bpd.

These adjustments reflect the actual data received for Q1 of 2024, and in some cases, the Q2, along with ". OPEC noted that while the summer driving season got off to a slower start compared to the previous year, transport fuel demand is anticipated to remain robust, supported by healthy road and air mobility.

WTI oil shrugs off the downgrade and extends its near term rebound from 72.42. Technically, the strong break of 55 4H EMA suggests that fall from 84.72 has completed already. Further rise is now in favor as long as 76.46 support holds, towards 55 D EMA (now at 79.23). Firm break there will solidify this near term bullish case and target top of the medium term range between 84.72 and 87.84.

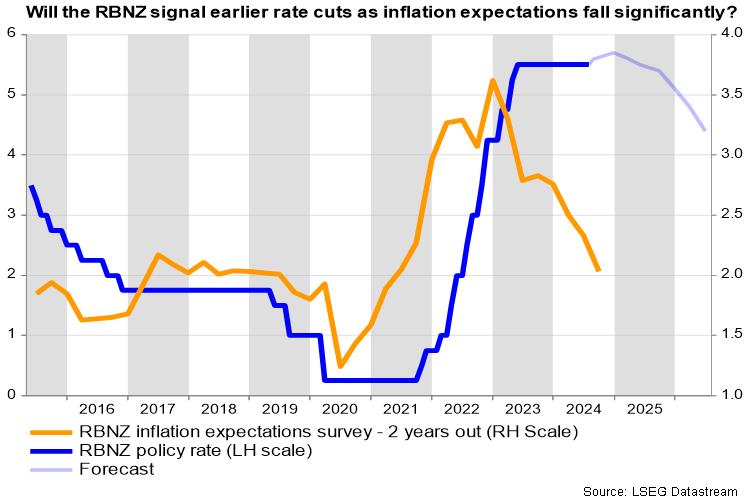

Will RBNZ Start Cutting Rates Sooner Than Later

- RBNZ could keep interest rates steady but signal easing sooner rather than later

- Economic picture shows signs of stress but no red flags yet

- NZDUSD approaches 0.6060-0.6080 resistance territory

NZ employment data sway rate cut bets

Q2 employment data from New Zealand exceeded the forecasts, leading to a reevaluation of rate cut expectations and a subsequent bullish movement in NZDUSD. However, the odds have since increased and now strongly indicate a 25bps rate reduction. Market pricing also implies two more similar rate reductions by year-end.

On the other hand, analysts believe that interest rates will remain steady at 5.5% and they might be right as inflation has yet to sustainably reach the RBNZ’s target of 1-3%, and strikingly is still hanging some distance above the 2.0% midpoint target. Non-tradable inflation, which includes housing and construction costs has barely slowed down, standing way higher at 5.4%.

Yet, a rate cut this month could be justified, or at least it could be a close call for lower interest rates to come in sooner rather than later. A survey conducted by the central bank showed inflation expectations from one- to ten-year timeframes falling markedly, with the two-year measure, which is closely monitored by the RBNZ, converging towards the 2.0% target from 2.33% previously. Opinions also showed optimism that the battle against inflation has been won.

Macro data raise the odds for a rate cut sooner than later

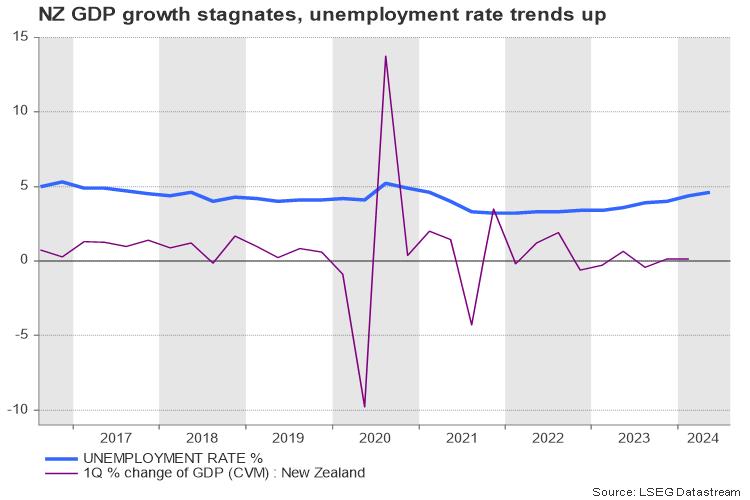

Separately, quarterly GDP data returned to growth in the three months to March, albeit at a pale pace of 0.2%, staying below pre-pandemic levels. Discouragingly, the manufacturing sector suffered the most since 2021 in July according to PMI data and the latest update from the services sector was disappointing as well.

As regards the labor market, despite the positive surprise in the Q2 figures, the unemployment rate continued to trend higher for the fifth consecutive quarter, climbing to the highest in three years. Additionally, although there was an unexpected quarterly rise in wage growth, the annual rate fell to its lowest point in two years at 3.6%, while working hours decreased by 1.2% q/q. By mid-2025, the RBNZ foresees a sustained rise in the unemployment rate to 5.1%.

Market reaction

The next inflation and employment update will be in October and November respectively, which makes someone wonder if the RBNZ has enough patience to wait till the end of the year before easing policy as talks for a bold 50bps rate reduction in September heat up in the US. One possible initial action for policymakers could be to modify their narrative of “higher for longer” stated in May’s statement and/or move up the timeline of rate cuts to 2024 from the previously projected March 2025.

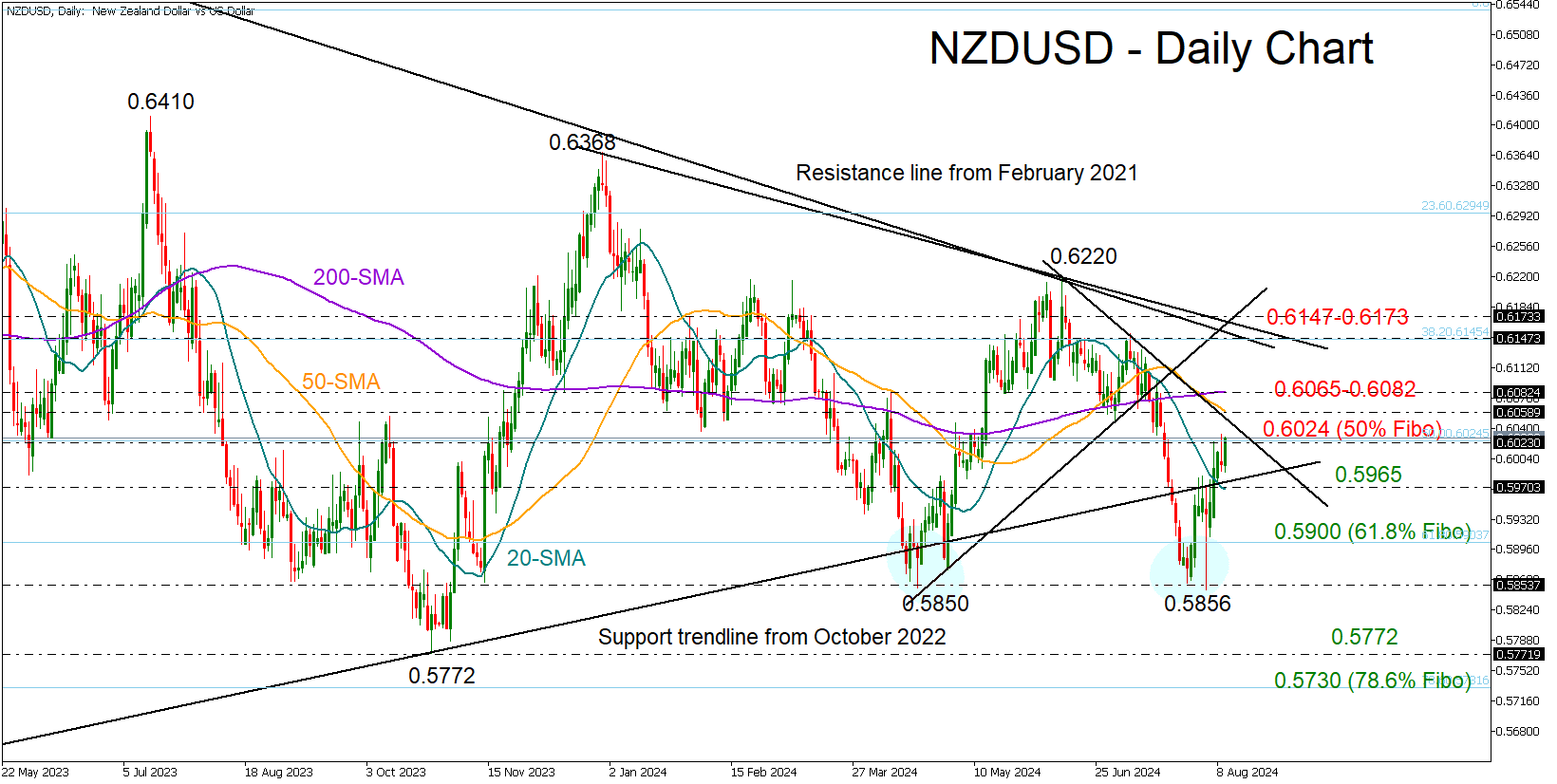

Steady interest rates or a 25bps rate cut accompanied by signals of more aggressive rate easing in the coming meetings could weigh on NZDUSD, pressing the pair towards 0.5900 if the 20-day simple moving average (SMA) proves fragile. Even lower the door would open for the double bottom area of 0.5850.

In the opposite scenario that the central bank maintains a hawkish tone due to the stickiness in non-tradable inflation, keeping interest rates steady for now and flagging fewer rate cuts by year-end than anticipated by investors, the pair could rise to re-challenge its 50- and 200-day SMAs within the 0.6060-6080 area. Even higher, the bulls might fight the critical resistance zone of 0.6147-0.6173.

Note that US CPI and retail sales data are also on the agenda this week and could fuel extra volatility in the markets.

NZD/USD Gains Momentum ahead of RBNZ Meeting

The New Zealand dollar is steadily rising against the US dollar, with the NZD/USD pair reaching 0.6014 as of Monday. The financial markets are gearing up for Wednesday’s Reserve Bank of New Zealand (RBNZ) meeting. Analysts widely anticipate that the RBNZ will maintain the official cash rate at 5.5% for the ninth consecutive time, reflecting ongoing concerns about the robustness of New Zealand’s economy.

Recent data releases have painted a mixed economic picture. The unemployment rate in New Zealand showed a less-than-expected increase in Q2, while inflation expectations dipped to a three-year low for Q3. These factors collectively strengthen the case for potential rate cuts, though it appears unlikely that the RBNZ will adjust rates downward in August, preferring to wait for cues from major global central banks.

Investor attention is also turning towards upcoming US inflation data, which could further influence global monetary policy expectations, particularly Federal Reserve expectations.

Despite challenges in July and August, the NZD has shown commendable resilience, suggesting potential for continued stability and barring significant external shocks.

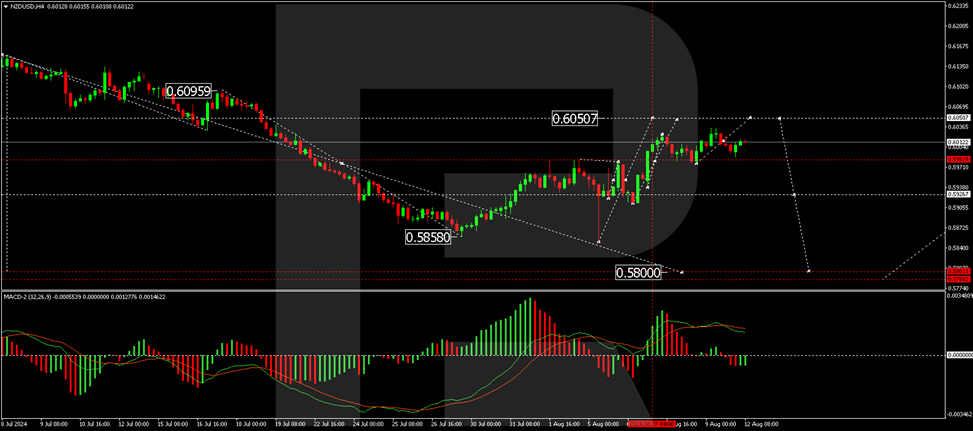

Technical analysis of NZD/USD

The NZD/USD pair is developing a consolidation range just above the 0.5983 level. We expect to see an extension of this range to 0.6050, considered a corrective move. The market will likely initiate a downward trend towards 0.5920 following this correction. A breach of this level could open the path to a further decline towards 0.5800. This bearish outlook is supported by the MACD indicator, which, although above zero, points downwards, indicating potential selling pressure.

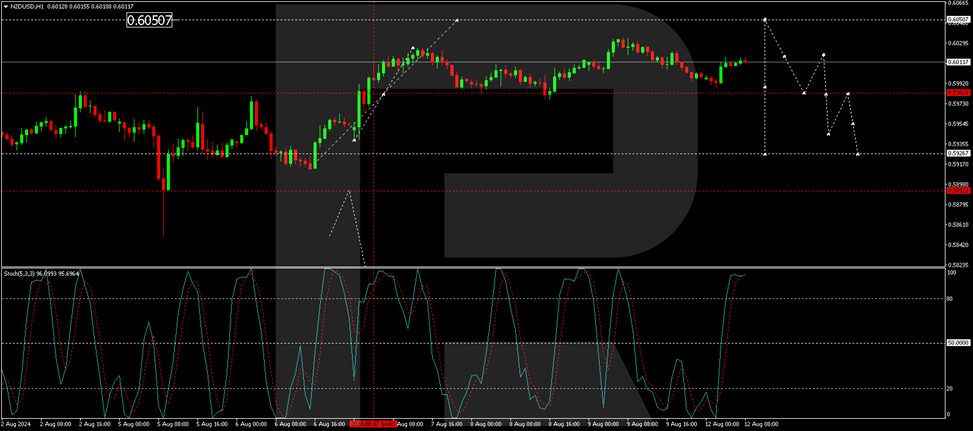

On the hourly chart, the NZD/USD is crafting the fifth segment of a growth wave aiming for 0.6050, considered a corrective rally. Upon reaching this level, we anticipate a reversal leading to a decrease towards 0.5983, potentially extending the downtrend to 0.5920. This bearish scenario is substantiated by the Stochastic oscillator, whose signal line is currently positioned azove 80 but shows signs of a forthcoming downturn.

Hang Seng Index: Medium-Term Bullish Trend Damaged

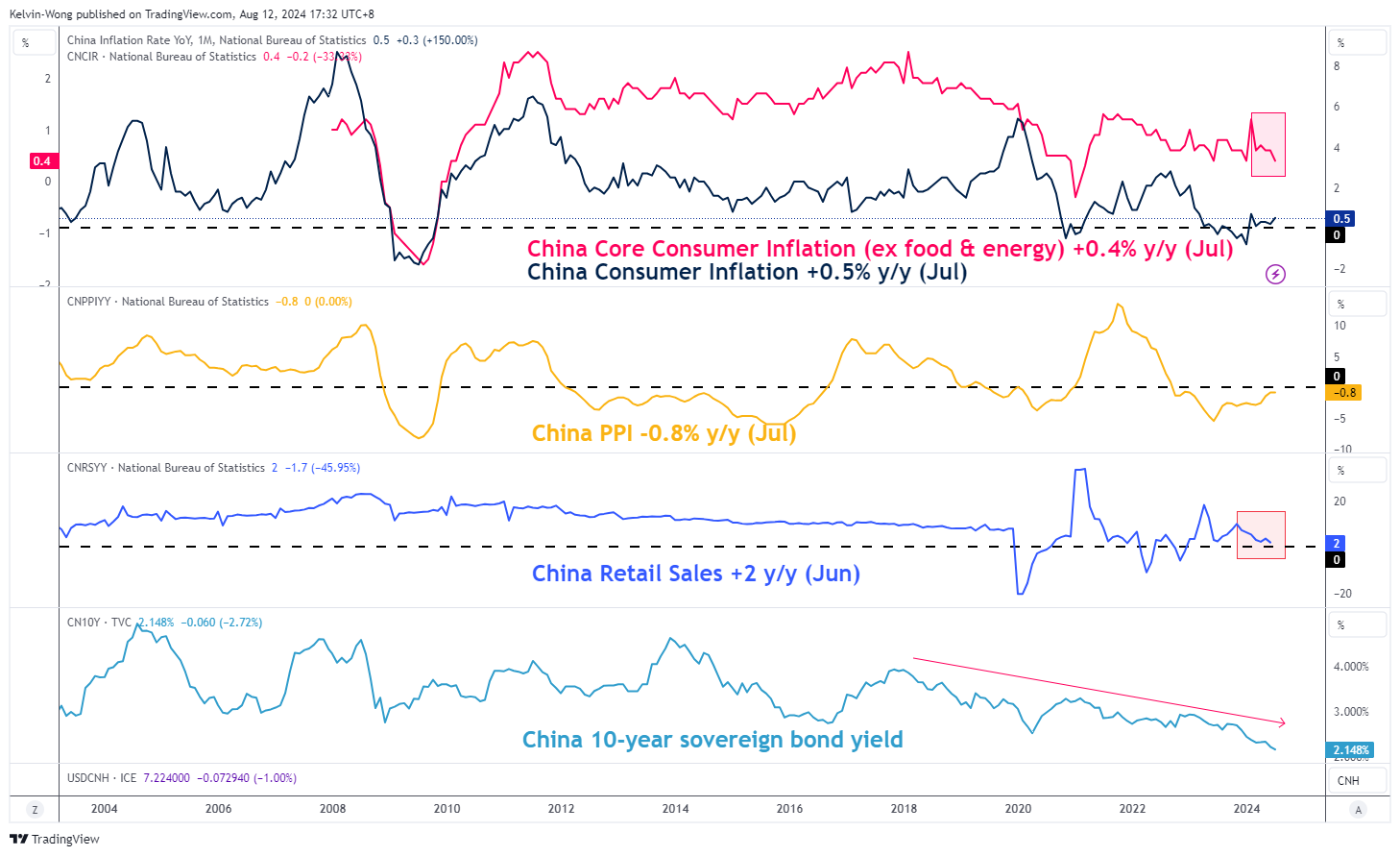

- China’s lacklustre core consumer inflation growth for July suggests the current pace of piecemeal stimulus measures is not sufficient to eradicate deflationary pressures.

- The “non-abating” deflationary risk scenario pushed the 10-year China sovereign bond yield to a record low of 2.12% last Monday, 05 August.

- The price actions of the Hang Seng Index have traded below its 50-day and 200-day moving averages.

This is a follow-up analysis of our prior report, “Hang Seng Index: Weak key China data & revival of Trumponomics dampen last week’s bullish tone” dated 15 July 2024.

Since our last publication, the price actions of the Hang Seng Index have dropped lower as expected; it shed by 8.7% in the past four weeks to print an intraday low of 16,441 on Monday, 5 August.

Overall, the Hang Seng Index has not been able the repeat its prior medium-term bullish feat seen from April to May this year where it rallied by 23% due to the lacklustre macro data out from China and the continuation rhetoric of boosting domestic consumption but without actual concrete forceful stimulus measures follow through from policymakers.

China’s inflationary growth still reeks of deflationary risk

Fig 1: China’s inflation data & 10-year sovereign bond yield trends as of July 2024 (Source: MacroMicro, click to enlarge chart)

Even though the latest China’s headline consumer inflation for July climbed to 0.5% y/y, exceeding expectations of 0.3% and 0.2% recorded in June, the uptick is likely to be driven by seasonal food inflation rather than an improvement in internal demand.

Severe weather conditions in the past months had hit supplies of fresh vegetables and eggs. Fresh vegetable prices climbed 3.3% y/y, after diving 7.3% in the previous month, while egg prices inched up 0.4%, after falling 3.9%.

Overall, the core consumer inflation rate that stripped out food and energy-related products inched down lower to 0.4% y/y in July from 0.6% in June, its fifth consecutive month of lacklustre inflationary growth since February print of 1.2% (see Fig 1).

The financial markets responded to the inherent “non-abating” deflationary risk by pushing the 10-year China sovereign bond yield to a record low of 2.15% in July and it sunk lower last Monday, 05 August to printing a fresh low of 2.12% before recovering to 2.20% at this time of the writing due to verbal and operational intervention by China central bank, PBoC as some rural banks have suspended trading in China sovereign bonds.

Bearish breakdown below 200-day MA triggers further potential downside pressure

Fig 2: Hang Seng Index medium-term trend as of 12 Aug 2024 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, the medium-term uptrend phase of the Hang Seng Index from its 22 January 2024 low has been damaged.

The bearish breakdown below the ascending channel support and thereafter its 200-day moving average on 2 August has skewed the probability of its medium-term trend towards the bearish camp (see Fig 2).

The next medium-term support to watch will be at 16,055 on the Hang Seng Index and a break below it exposes the long-term pivotal support of 14,600 (also the secular ascending trendline in place since the August 1998 low).

Only a clearance above 18,000 medium-term pivotal resistance negates the bearish tone for the next medium-term resistances to come in at 18,530 and 19,710.

News of the Week (August 12— August 16): NZDUSD Market Review

Focus on NZDUSD! Exciting trading possibilities are just around the corner.

The NZDUSD pair is usually called the "Kiwi,". It denotes the exchange rate between the New Zealand dollar and the US dollar. It is usually regarded as one significant indicator of the economic activities between New Zealand and the United States. Commodity prices, tourism, and the New Zealand trade balance drive the strength of the NZD. On the other side, the USD is driven by US indicators, Federal Reserve policies, and global risk sentiment. Relative strength in one or both can move the NZDUSD rate and indicate shifts in the economic health of these two nations.

New Zealand interest rate decision, August 14, 04:00 (GMT+2)

The interest rate of the Reserve Bank of New Zealand is expected to be at 5.50%. In reality, an unchanged rate would be considered favorable for economic stability, with no changes in investment or spending, which would further strengthen the NZD against the USD. If the rate is raised, it will result in a significant appreciation of the New Zealand dollar against the US dollar. This could indicate a more positive view on the economic outlook or inflationary concerns and lead to a rise in the NZDUSD exchange rate. An unexpected rate cut should be perceived as economic uncertainty. This will be followed by a weakening NZD and a fall in NZDUSD.

The Reserve Bank of New Zealand had its last meeting on July 10, and the interest rate remained unchanged. Nevertheless, NZDUSD experienced a sharp fall!

US Consumer Price Index (CPI) MoM, August 14, 14:30 (GMT+2)

The US CPI is expected to increase to 0.2% from the previous month’s -0.1%. If this forecast meets or exceeds expectations, indicating strong economic activity and potential inflationary pressures, the US dollar could strengthen as markets anticipate a possible rate hike by the Federal Reserve. Such a scenario usually results in a lower NZDUSD as a stronger US Dollar has a negative impact on the NZD. Alternatively, the USD might weaken if the CPI report falls below the anticipated 0.2%, suggesting less economic vigor than expected. A softening could boost the NZDUSD as confidence in the strength of the US economy weakens.

In the Daily timeframe, NZDUSD, which is in a long-term downtrend, has bounced off support and is consolidating near 38.2 Fibonacci resistance. Demarker rose above 0.300, breaking out of the oversold zone, although the overall sentiment remains exceptionally bearish.

- If the bulls push the price above 0.6000 resistance, the next target will be 0.6080 resistance, corresponding to 61.8 Fibonacci;

- A rebound from the resistance would take NZDUSD back to 0.5870 support;

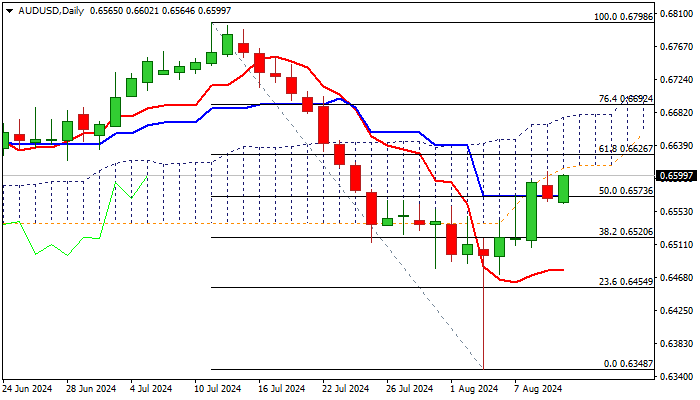

AUD/USD Outlook: Lifted by Fresh Risk Appetite, Retests Key Resistance Zone

AUDUSD advanced 0.5% in Asian / European trading on Monday, to completely reverse Friday’s drop and generate initial signal of bullish continuation.

Fresh strength cracked pivotal barriers at 0.6600 zone (converged 200/100DMA’s / base of rising daily cloud, where Friday’s action was strongly rejected.

Gains so far minimized signals of bull trap and recovery stall but need to register clear break of these barriers to open way for further recovery.

Otherwise, repeated upside failure may keep the price in extended consolidation or turn near-term structure into bearish mode on break below 10DMA (0.6538).

Daily studies show MA’s in mixed setup, north-heading momentum still in the negative territory and overbought stochastic, all contributing to unclear near term direction.

On the other hand, fundamentals are improving as revived risk appetite lifted Asian stocks and provided fresh support to risk sensitive Ausie dollar, which may play a key role and help the pair to clear pivotal barriers.

Sustained break higher to expose targets at 0.6626 (Fibo 61.8% of 0.6798/0.6348 descend) and 0.6679 (daily cloud top) in extension.

Broken Fibo 50%, reinforced by daily Kijun-sen (0.6573) offers immediate support, guarding pivotal 10DMA (0.6538).

Res: 0.6609; 0.6626; 0.6679; 0.6692.

Sup: 0.6573; 0.6564; 0.6538; 0.6520.

Australian Dollar Gains Ground, Eyes Wage Growth

The Australian dollar has started the week in positive territory. AUDUSD is trading at 0.6596 in the European session, up 0.41% on the day at the time of writing.

Australian dollar recovers as markets stabilize

The Australian dollar has quickly recovered from the recent turbulence which routed global stock markets. Last Monday, the Australian dollar fell as much as 2.4% but managed to pare most of the losses. As the markets have steadied, the risk-prone Aussie has improved by 1.5%. Still, there is uneasiness in the markets and if sentiment sinks, the Australian dollar could head lower.

On Tuesday Australia releases the wage price index for the second quarter. The market estimate stands at 0.9% q/q, compared to 0.8% in the first quarter. Annually, wage growth is expected to tick lower to 4.0%, compared to 4.1% in Q1. The RBA will monitoring the data carefully, as it remains concerned about a price-wage spiral.

The Reserve Bank of Australia held rates last week at 4.35% but remained hawkish, with Governor Bullock saying that she didn’t expect a rate cut for the next six months. Bullock said that policy makers had discussed a rate hike due to concerns of “persistently high inflation”.

The RBA could become an outlier among other central banks, which have already lowered rates or like the Federal Reserve, have signaled that rate cuts are coming soon. The message that rates could go higher has boosted the Australian dollar but there would be a cost as homeowners and businesses are straining under the weight of high interest rates. If inflation does rise more than expected, we are likely to see the RBA continue to hold rates for the next several months. The markets are more dovish and have widely priced in a rate cut in December.

AUD/USD Technical

- There is resistance at 0.6668 and 0.6765

- 0.6509 and 0.6412 are the next support levels

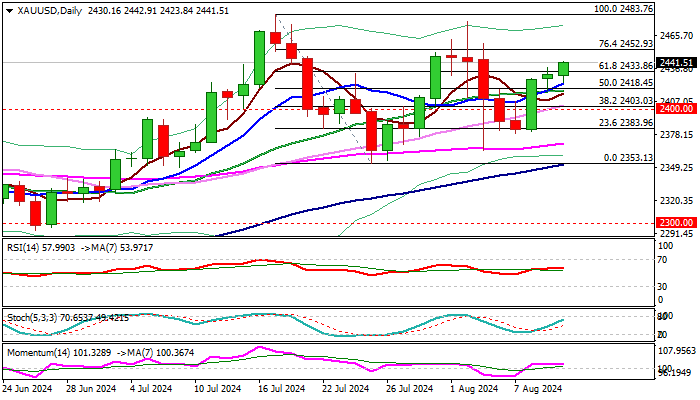

XAU/USD Outlook: Bulls Hold Grip Ahead of Key US Inflation Data

Gold remains at the front foot and edges higher in early Monday, extending recovery into third straight day.

The yellow metal regained ground after last week’s sharp fall, boosted by growing signals that the Fed may opt for 50 basis points rate hike in September.

Weak US economic data warn of worse than expected scenario, with last week’s talks of US economy entering recession (after Fed’s long-lasting calming signals of soft landing) sparking panic in the market.

Although the situation is calmer now, investors remain cautious.

Markets await release of US inflation report for July, which is expected to shed more light on Fed’s next steps on monetary policy.

The metal price is also supported by geopolitical tensions, which adds to overall positive outlook.

Technical studies on daily chart are in full bullish setup and contribute to positive picture, as fresh push higher on Monday broke above Fibo 61.8% of $2483/$2353 ($2433), with close above this level to add to bullish signals.

However, markets are likely to move at a slower pace ahead of release of US CPI data.

Next targets lay at $2452 (Fibo 76.4%), $2477 (Aug 2 spike high), guarding new all-time high at $2483.

Rising 10DMA ($2422) and broken Fibo 50%) mark solid supports which should keep the downside protected and maintain bullish structure.

Res: 2452; 2462; 2477; 2483.

Sup: 2433; 2422; 2418; 2403.