Sample Category Title

Canada’s July Employment Report Will Confirm a Weaker Labour Market

The Canadian jobs report for July next Friday is expected to show more softening in the labour market.

Employment gains have already slowed substantially into the summer, and we expect July will be no exception with 15,000 new jobs added. Against a still rapidly rising population, the unemployment rate will likely have ticked higher again to 6.5% in July, from 6.4% in June. In comparison, it was at 5.6% in early 2020 just before the pandemic, and dropped below 5% during the post-pandemic labour crunch in the summer of 2022.

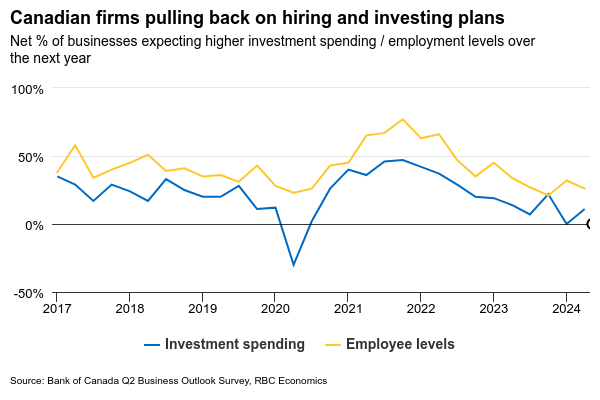

Overall, forward-looking indicators are showing little signs of recovery in hiring demand. Job openings in Canada have continued to decline in recent months, and businesses surveyed in the Q2 Bank of Canada outlook survey again reported lacklustre intentions to hire and invest over the next year.

Whereas employment growth has slowed, wage growth data from the labour force report has still been holding up at high levels. That contradicts data from elsewhere including the SEPH survey that has shown a more pronounced slowing in wage growth. In addition, business expectations on wage growth have also moderated substantially alongside the pull back in hiring demand, according to the Bank of Canada Business Outlook Survey. Overall, we expect wage growth to trend lower and don’t think it will fuel future inflation. That should quell the BoC’s concerns while it continues to cut interest rates.

Week ahead data watch

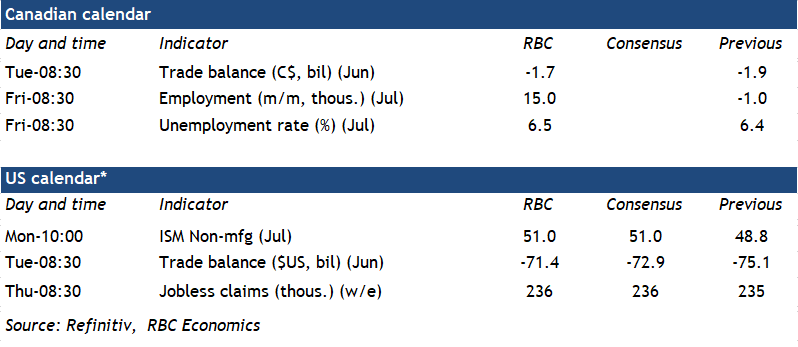

We expect Canadian goods exports dipped 0.4% in June, and imports dropped by a slightly bigger 0.6% to leave the trade deficit narrower at $1.7 billion. Details should show a decline in motor vehicle shipments. That coupled with a drop in oil prices are expected to have contributed to the slowdown in trade flows.

U.S. advance economic indicators showed the goods deficit narrowed by US$2.5 billion in June, as higher export growth (2.5%) outpaced growth in import (0.7%). The increase in exports was broad-based, led by food and beverages. Higher imports were supported by industrial supply, more than offsetting a decline in auto imports.

USD/JPY Outlook: Falls Further on Weaker than Expected NFP Numbers

USDJPY fell sharply (down 1% in immediate reaction to US jobs data) after US NFP dipped well below expectations in July (114K vs 176K f/c), while June’s figure was revised down to 179K from initial 206K.

Unemployment unexpectedly rose to 4.3% in July from 4.1% June / consensus, while average earnings rose by 0.2% last month vs 0.3% in June and identical forecast.

Weaker than expected labor data, with significant drop in Nonfarm payrolls, added to negative outlook, boosted the latest dovish signals from Fed and strongly boosted expectations for 50bp cut in September (against initial 25 bp) and lifted projections for cuts in 2024 to 110 bp.

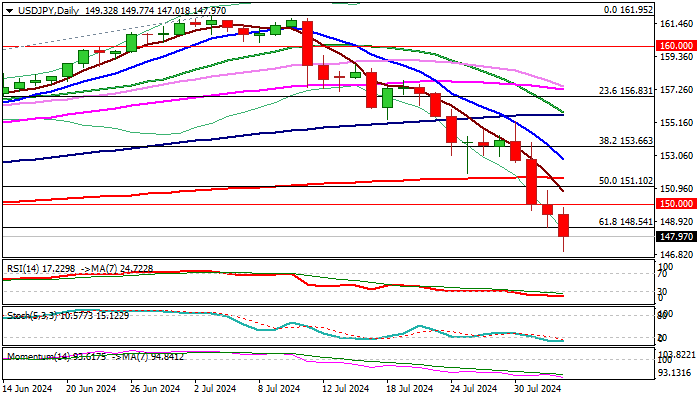

The pair extended further below broken 150 mark and broke below pivotal Fibo support at 148.54 (61.8% of 140.25/161.95 to hit the lowest since mid-March (147.01) in post-NFP acceleration, with weekly close below 150 to confirm negative signal.

Bears eye immediate target at 146.48 (Mar 8/11 higher base) and may extend towards 145.37 (Fibo 76.4%), with consolidation likely to precede as daily studies are oversold.

Upticks should be ideally capped under 150 level (reverted to resistance), guarding 200DMA (151.65).

Res: 148.54; 150.00; 150.80; 151.65.

Sup: 147.01; 146.48; 145.89; 145.37.

July Employment: That Was Sahm Jobs Reports

Summary

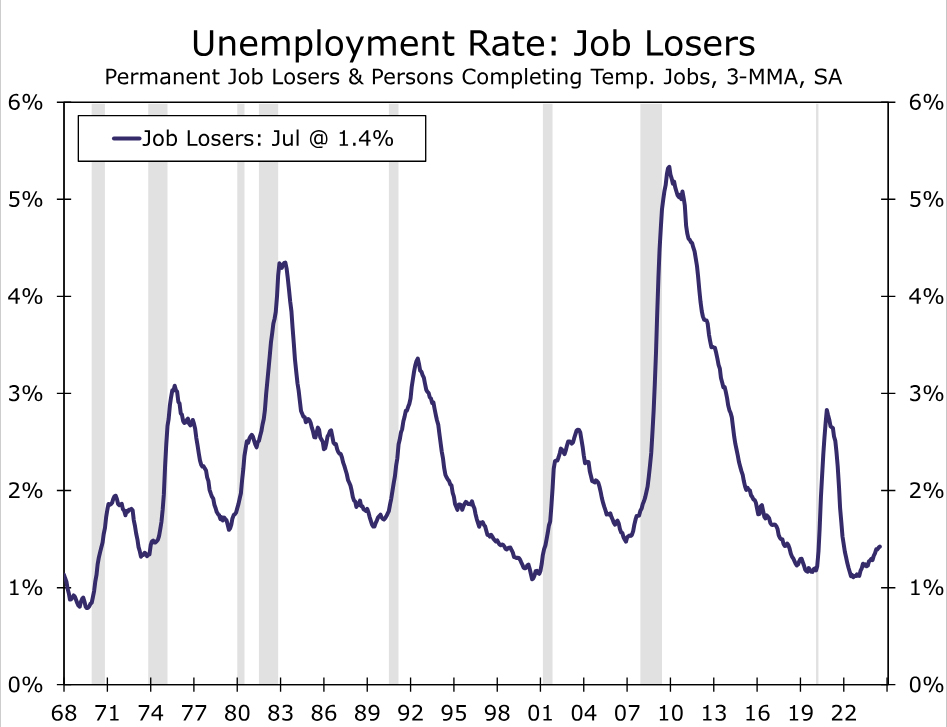

The ongoing deterioration in the jobs market was on full display in the July Employment report. Nonfarm payrolls posted the second smallest gain in 3.5 years with an increase of 114K, average hourly earnings growth eased to 3.6% year-over-year and the unemployment rate jumped to 4.3% from 4.1% in June. The landfall of Hurricane Beryl at the start of the survey week looks to have had no significant impact on the change in payrolls or the increase in the unemployment rate.

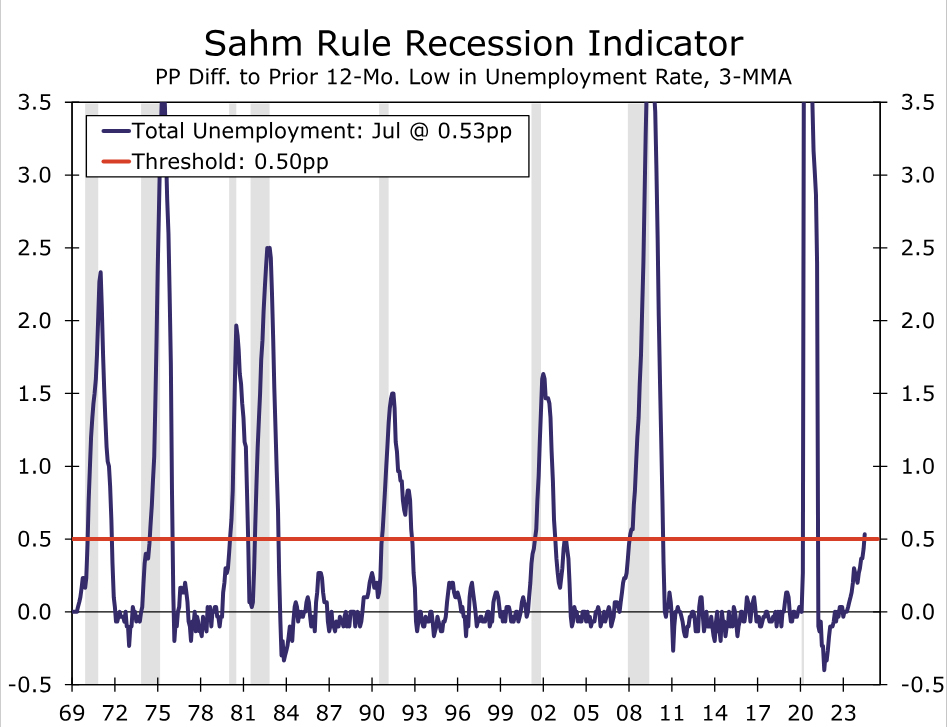

The increase in the unemployment rate now puts it over the 0.5 point Sahm Rule threshold that has historically been associated with the economy being in a recession. The rise in unemployment due to labor force entrants over the past year suggests the current increase may not be the sure-fire sign of a downturn it has been in the past. However, the significant rise in job losers over the past year underscores genuine weakening in labor market conditions that are quickly raising the risk of recession. We expect the Fed to begin reducing its policy rate in September as a result, with the possibility of a 50 bps cut at least on the table after today's report.

The Beginning of the End?

The ongoing deterioration in the jobs market was on full display in the July Employment report. Nonfarm payrolls expanded by just 114K, well below consensus expectations for a 175K gain and close to the smallest monthly gain this cycle. Revisions were minimal relative to the last two months' downward adjustment of 111K, but were once again negative with the net change the prior two months lowered by 29K. Over the past three months, payrolls have expanded at an average monthly pace of 170K, down from 267K in the first quarter and 251K in 2023.

The BLS reported that the landfall of Hurricane Beryl at the start of the survey had no discernable effect on the collection of data for the survey period. It furthermore looks to have had no significant impact on the change in payrolls. To be removed from the payroll count in July, workers would have had to miss the entire pay period that overlapped with the survey week. Individuals paid bi-weekly or semi-monthly who worked the first week of the month therefore would still have been counted as employed. The 27% of workers who are paid weekly were more likely to miss work the entire payroll period covering the survey week, yet industries with a relatively high share of workers paid weekly such as construction, manufacturing and trade & transportation saw payrolls pick up slightly over the month.

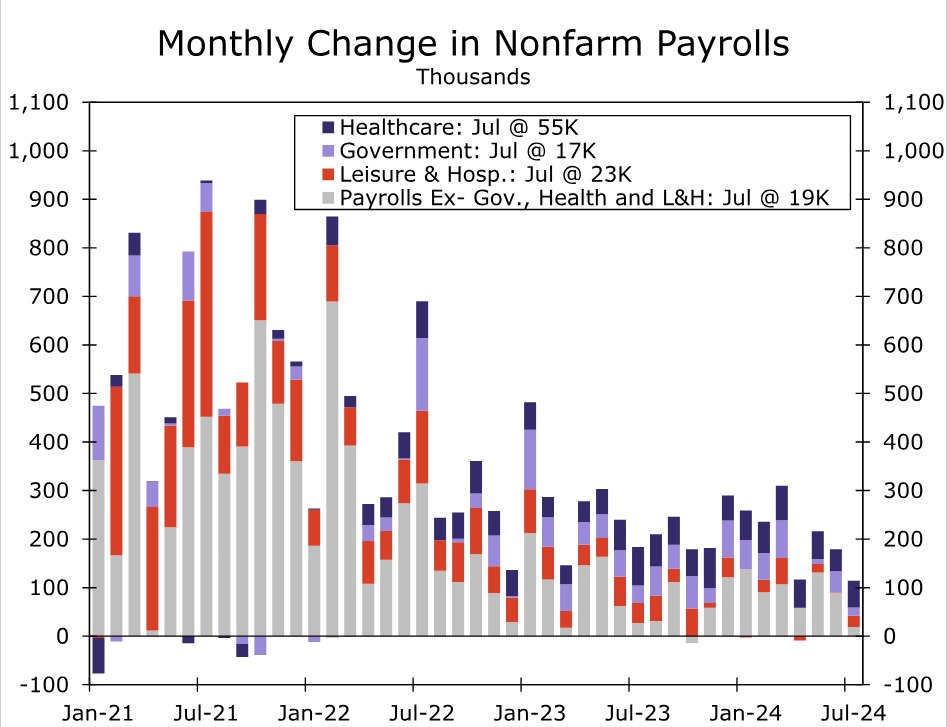

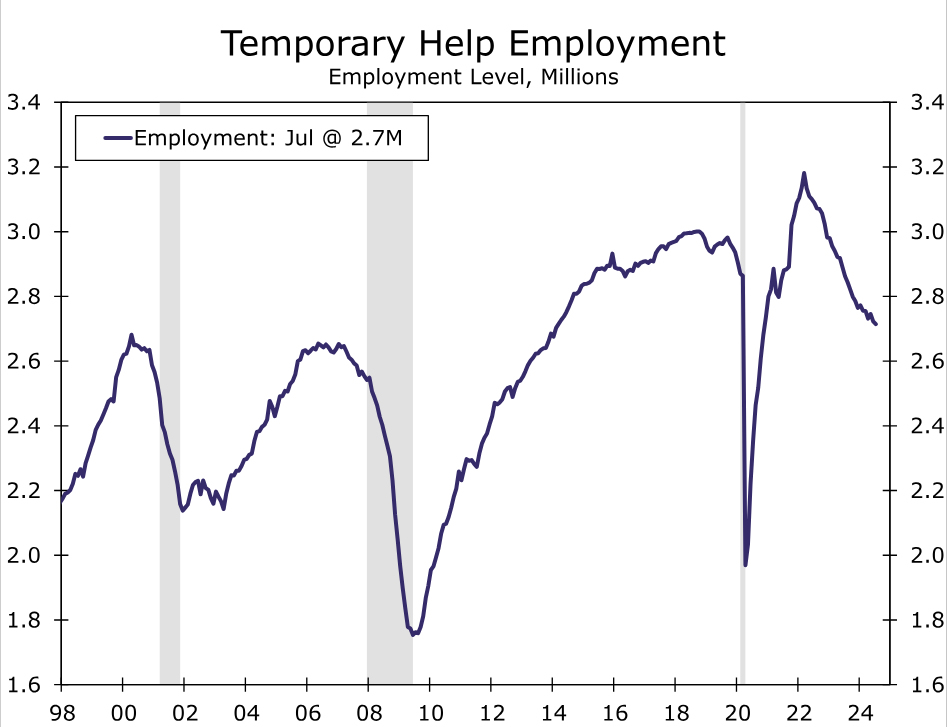

Nevertheless, hiring outside of healthcare (+55K)—and to a lesser extent government (+17K) and leisure & hospitality (+23K)—continues to look feeble (chart). Employment in white-collar jobs like information, financial services and professional & business services all fell in July. Meantime, temporary employment declined for the 26th time in 28 months and is now 242K below its 2019 average.

The separate Household Survey showed some disruption to work in July, with the number of individuals with a job but not at work due to bad weather surging 14-times above July's historical average. However, workers absent from their jobs due to bad weather are counted as employed in the Household Survey whether they are paid for the time away or not.

This means the jump in the unemployment rate to 4.3% from 4.1% in June cannot be explained away by the hurricane. The increase in unemployment from 3.5% this time last year is more concerning because the unemployment rate tends to vacillate little throughout the business cycle. Rising unemployment can set off a negative feedback loop between income, spending and hiring. This dynamic has put a spotlight on the “Sahm Rule,” which highlights the historical pattern that the unemployment rate has never risen 0.5 points above its prior 12-month low (when measured on a three-month average basis) without the economy being in a recession.

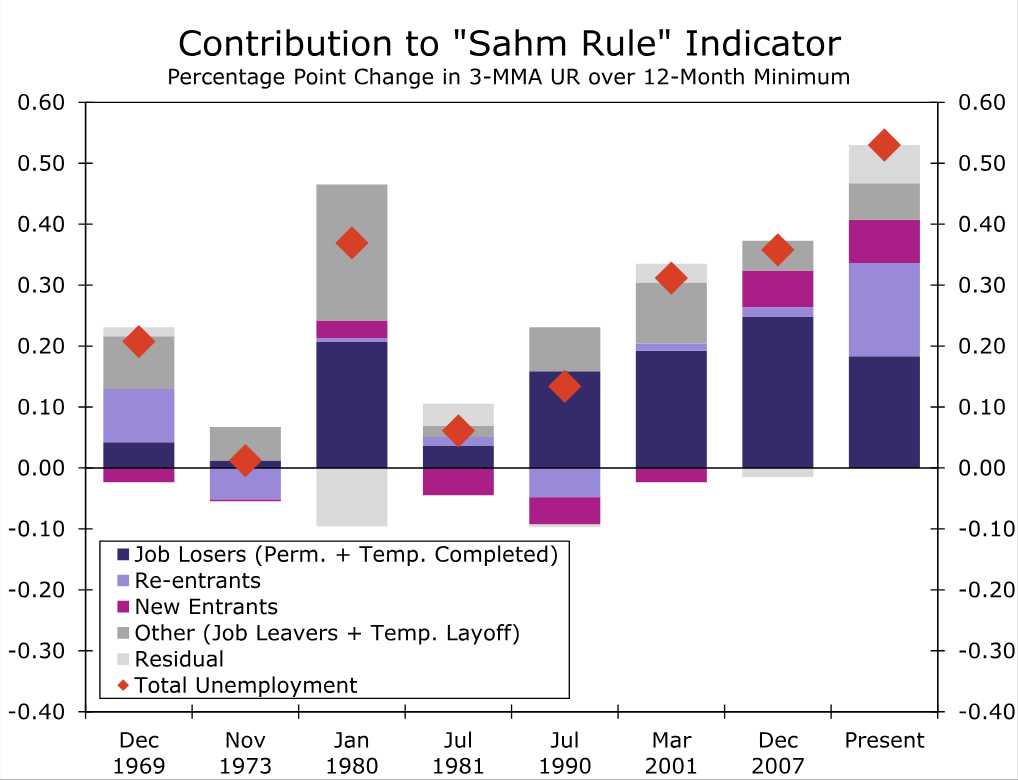

July's unemployment rate reading has pushed the Sahm Rule indicator to 0.53, above its 0.5 point threshold. As we discussed in a recent report, the increase in unemployment has been driven more by entrants into the labor force than at the start of prior recessions. In July, new and re-entrants accounted for 22 bps of the rise in the Sahm Rule indicator over the past year, more than its contribution in the first month of each of the past seven recessions (2020 excluded, chart). This increase in unemployment for the “right” reasons suggests that the crossing of the 0.5 point threshold may not be the sure-fire sign of recession that it has been in the past. That said, unemployment due to a permanent job loss or completion of temporary work has also risen significantly over the past year, including another increase in July (chart). This increase for the "wrong" reasons underscores that even if the threshold for a recession might be somewhat higher this cycle, there has nevertheless been a clear deterioration in labor market conditions.

The looser labor market is having the intended effect of reducing inflation pressures. Average hourly earnings increased 0.2% in July, bringing the year-over-year change down to a three-year low of 3.6%. The moderation adds to other evidence released this week that labor costs are no longer a threat to inflation, including the Employment Cost Index, the Fed's preferred gauge of compensation costs, slipping to an annualized rate of 3.7% in Q2 and unit labor costs now running comfortably below 2%.

Time to Get a Move On

The July jobs report offers the latest indication that the exceptional jobs market that followed the unique circumstances of the pandemic looks to have come to an end. Demand for new workers continues to fade, as evidenced by the downward trend in job openings, small business hiring plans and temporary help employment. Workers have taken notice, with perceptions of job availability and the share of employees quitting their jobs falling to cycle lows. The weakening trend in hiring, unemployment and job switching over the past year puts conditions on par with the late 2010s. While the labor market remains in decent shape in an absolute sense, further softening would be hard to attribute to “normalization” and instead would be consistent without outright weakness in our view.

We expect the FOMC to begin dialing back the current level of policy restriction soon. Although inflation has not yet returned to the Fed's 2% target, the cooler jobs market points to inflation pressures continuing to recede. Our forecast remains for the FOMC to reduce the fed funds rate beginning in September by 25 bps at every other meeting through 2025, although growing risks to the employment side of the Fed's mandate suggest a 50 bps cut in September could also be on the table as more and/or a faster pace of rate cuts look increasingly warranted.

Week Ahead – RBA and BoJ Summary of Opinions Take Center Stage

- RBA decides on policy as hike bets disappear

- BoJ Summary of Opinions awaited for more hike hints

- After Fed, dollar turns to ISM non-mfg PMI

- New Zealand and Canada jobs data also on tap

Will the RBA turn dovish?

Following the BoJ, the Fed, and the BoE decisions this week, the central bank torch will next be passed to the RBA, which announces its decision on Tuesday.

At its latest meeting, this Bank kept its benchmark rate unchanged at 4.35%, but there was a discussion on whether to raise it by another 25bps due to inflation easing more slowly than previously expected.

After the meeting, the monthly y/y CPI rate for May rose to 4.00% from 3.60%, intensifying expectations for another quarter-point hike by the end of the year, while the employment report pointed to more-than-expected job gains in June.

However, the inflation data for the whole of Q2 revealed that, although headline inflation rose to 3.8% y/y from 3.6%, the more closely watched underlying metrics eased. Combined with the increasing worries about the performance of the Chinese economy, this prompted investors to erase their hike bets and start penciling in more basis points worth of reductions. Currently, a 25bps reduction by December is fully priced in.

Having said all that though, even if the RBA sounds more dovish at this gathering, it is unlikely to make a 180-degree spin and start communicating a rate cut. They may opt for a more neutral stance and signal that they want more evidence that inflation is back on a downward path. Something like that may disappoint market participants expecting hints about a potential rate cut, allowing the aussie to recover some of its recently lost ground.

Could BoJ summary add more fuel to the yen’s engines?

On Thursday, the BoJ releases the Summary of Opinions from this week’s meeting, where officials decided to raise interest rates by 15bps, at a time when market participants were assigning a slightly more than 50% chance for a 10bps move. Officials also agreed to gradually taper the pace of their monthly bond purchases, aiming to take it down to around 3 trillion yen by April 2026.

This allowed the yen to extend its latest rally that was probably initiated by a risk-off environment and the unwinding of profitable carry trades. Should the Summary of Opinions reveal that policymakers are willing to further raise interest rates before the turn of the year, the yen may stay on the front foot, despite the rally already appearing overstretched.

ISM non-mfg PMI eyed as traders ramp up Fed cut bets

In the US, the Fed was the only central bank to keep interest rates untouched this week, with Chair Powell noting that “a rate cut could be on the table at the September meeting.” Officials also highlighted the progress of inflation towards their objective, prompting market participants to add some more basis points worth of rate reductions by the end of the year. Although a September rate cut was already fully priced in ahead of the decision, investors are now considering the case of three quarter-point reductions by December as a done deal.

Next week, on Monday, dollar traders may turn their eyes to the ISM non-manufacturing PMI for July for further clues on how the world’s largest economy is faring. The prices charged subindex may attract special attention as it could serve as an early indication of whether inflation continued its downward trajectory. The employment index could also be monitored due to the latest softness in the labor market.

New Zealand and Canada jobs data also on the agenda

The New Zealand and Canadian employment data are also on next week’s agenda. The former is scheduled for Wednesday and the latter for Friday.

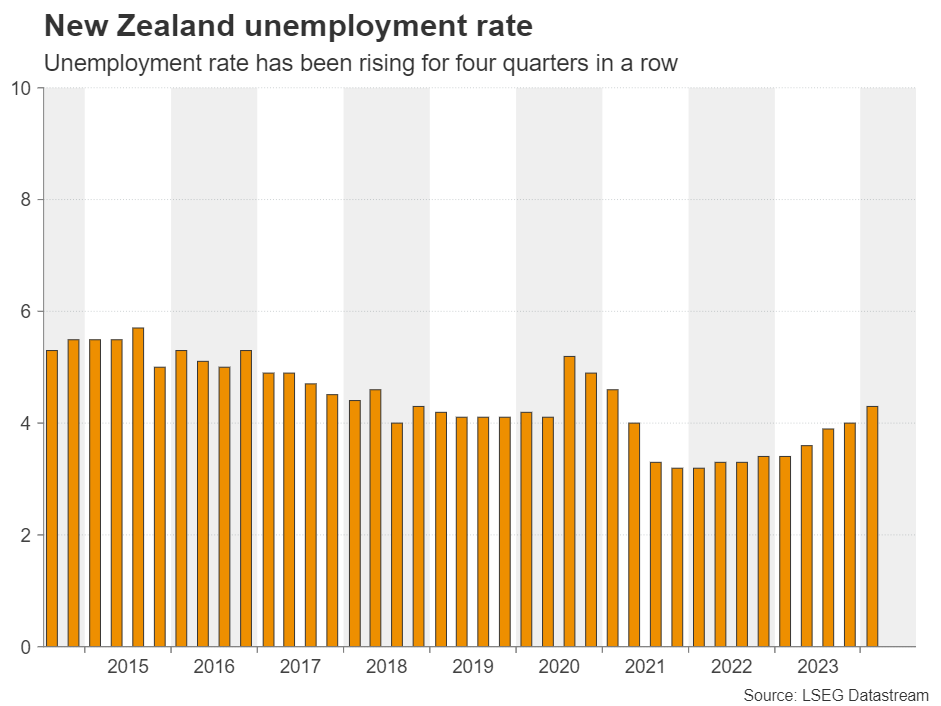

Getting the ball rolling with New Zealand, at its July decision, the RBNZ made a dovish U-turn after keeping the door to a rate hike open in May, saying that it expects headline inflation to return within its 1-3% target range in the second half of this year.

A few days later, the inflation data for Q2 revealed that the headline CPI dropped to 3.3% y/y from 4.0%, corroborating the notion that this Bank may start lowering interest rates soon. Money markets suggest that investors are anticipating more than two quarter-point reductions this year, with the probability of the first being delivered in August now resting at around 35%. Should the jobs data reveal that the unemployment rate rose for the fifth consecutive quarter, that probability could go even higher, thereby exerting more pressure on the already wounded kiwi.

Passing the ball to Canada, the BoC has been one of the most dovish major central banks, already cutting interest rates twice and signaling that more reductions may be on the way. Investors are nearly convinced that a third consecutive 25bps cut will be delivered in September and a soft employment report may seal the deal.

Besides their domestic data, the aussie and the kiwi may well be impacted by the Chinese trade and CPI data for July on Thursday and Friday respectively. Anything adding to concerns about the performance of the world’s second largest economy may weigh on both risk-linked currencies.

On the earnings front, Disney announces its results on Wednesday before the market opens.

Sunset Market Commentary

Markets

Markets are trembling. US payrolls missed expectations by a significant margin as employment only grew by 114k (175k consensus). Last month’s reading was revised down by about 30k. The unemployment rate unexpectedly rose to 4.3%, the highest since Oct 2021, and hourly earnings only rose by 0.2% m/m (3.6% y/y). It’s a big disappointment across the board that followed on a long streak of weak(er) data, including yesterday’s, and adds to a growing sense of the US economy & labour market rapidly losing momentum. The Fed on Wednesday stopped short of announcing a September rate cut but markets fear policymakers are behind the curve. US money markets sharply rose easing bets with more than 100 bps of cuts priced in for 2024 alone. That implies at least one 50 bps rate cut, something Powell just two days ago said they were not considering. He did keep the door ajar: "If we see something that looks like a more significant downturn [in the labour market], that would be something that we would have the intention of responding to." US yields at some point dropped a whopping 30 bps at the front before cutting losses to a still-massive 19 bps. The 2-yr yield tanked to the lowest level since June 2023 (3.95%) with technically little in the way to 3.55% (March 2023 low, regional banking crisis). The 10-yr (-12 bps, 3.85%) tested the YtD/December 2023 at 3.81%. A break paves the way for a return to 3.64%-3.66%/3.50%. Bund yields got caught in the slipstream, dropping between 4.6 and 10 bps in a similar curve shift. The 2-yr is attacking the YtD low at 2.35%, the 10-yr lost support at 2.20% and has intermediate support at 2.08% as a final hurdle ahead of the 1.89% December 2023 low. Stocks sold off in Europe (-2.2%) as well as in the US. Risk aversion and earning misses by the likes of Intel and Amazon makes the Nasdaq go belly up. The tech-heavy index (-2.5%) loses support at 1700. The S&P500 (-1.6%) gaps below 5400 support. The VIX volatility index rises to the highest level since October 2023. Unlike yesterday, the dollar is unable to offset the interest rate support losses through the vulnerable market climate. It is losing against peers with EUR/USD jumping towards the 1.09 barrier, DXY falling off a cliff to 103.43 in the biggest move in 9 months and USD/JPY hitting the lowest level since mid-March at 147.6. EUR/GBP heavily tested the 0.85 barrier but for now is not pushing through. Sterling does gain against a weak dollar with GBP/USD reversing about 75% of yesterday’s decline (1.282).

News & Views

Huang Yiping, a key advisor to the Chinese central bank, was unusually vocal on what he believes are insufficient policies to get the economy steamrolling again. Huang said that authorities should change their focus from investment and exports to domestic consumption. He suggested offering cash handouts as well as take a looser stance vs fiscal health (e.g. by dropping the 3% budget deficit rule). Huang proposed an inflation target of 2 to 3% for the central bank instead of regarding 3% implicitly as a ceiling. Huang suggested the central bank adopt the aggressive policies taken by the likes of the Fed and ECB to prop up the economy. But the PBOC is wary to do so, given that it is also tasked with preserving currency stability. USD/CNY by mid-July hit an 8-month high around 7.28. The pair witnessed some sharp swings over the past few days, including a dollar-driven sharp drop to 7.18 currently.

Swiss inflation eased by 0.2% m/m in July. The yearly figure came in at 1.3%, matching the June reading. Both numbers were exactly as expected. The core gauge (ex. fresh and seasonal products & energy) was unchanged too, at 1.1%. Swiss Statistics said that package holidays, air travel and clothing saw prices falling, while the costs of hotels and fruit and vegetables rose. The Swiss National Bank was among the first to cut rates in March of this year. It did so again in June, to 1.25%. With inflation steady and within the target range of 0-2%, the SNB is expected to deliver a third cut in September. It doesn’t need to worry about a weak CHF – as it did back in May – as the recent sharp risk-off triggered some major safe haven flows towards the currency. EUR/CHF went from the 0.975 area mid-July to 0.94 earlier today. Barring a brief episode at the start of this year, that’s the strongest CHF level in decades.

Graphs

Vix volatility index jumps to highest since October last year amid market tremors

US 2-yr yield slides to lowest level since June 2023 as markets fear Fed is behind the curve

EUR/CHF: Swiss franc enjoyed strong safe haven flows in recent days. With stable inflation, SNB seems ready to cut again in September

Nasdaq opens below 17k support barrier on fears the economy is slowing down faster than expected

Swiss Franc Jumps After Soft US Job Numbers

The Swiss franc has posted sharp gains in the North American session on Friday. USD/CHF is currently trading at 0.8754, up 0.86% on the day. The Swiss franc is on a roll and is trading at its highest level since the end of January.

Swiss inflation declined 0.2%, in line with expectations

Switzerland’s inflation rate declined 0.2% m/min July, after no change in June and in line with the market estimate. Yearly, inflation remained at unchanged at 1.3% and matched the market estimate. This was the first decline in eight months. The core rate was also unchanged at 1.3%.

Inflation remains comfortably within the Swiss National Bank’s target range of between 0% and 2%. Inflation is much lower than in most of the other major economies but the central bank remains vigilant and in March it was the first major central bank to lower interest rates in a surprise move. The SNB cut a second time in June which lowered the cash rate to 1.25%.

SNB chair Thomas Jordan said after the second cut that the Bank lowered rates because of lower inflation and the strong Swiss franc. The SNB meets next in September and there is a strong possibility of another rate cut, as inflation remains on a downswing and the Swiss franc has soared 5.8% against the US dollar since May 1. Some US data has indicated the economy is weakening and investors have moved funds to safe haven assets like the Swiss franc.

US nonfarm payrolls slide below expectations

US nonfarm payrolls slipped badly in July, falling to 114 thousand. This was down from the revised 179 thousand in June and below the market estimate of 175 thousand. The unemployment rate rose to 4.3%, up from 4.1% which was also the market estimate. As well, wage growth fell in July from a revised 3.8% y/y to 3.6%, and monthly from 0.3% to 0.2%. Both wage growth readings missed the market estimate. In the aftermath of the employment report, the US dollar has retreated against most of the major currencies.

The weak employment numbers point to a US labour market which is cooling down and will raise expectations for a historic rate cut in September. The Federal Reserve has signaled that it could lower rates at the September meeting if inflation continues to move lower.

USD/CHF Technical

- USD/CHF has pushed below support at 0.8699. Below, there is support at 0.8621

- There is resistance at 0.8768 and 0.8846

US: Job Market Continued to Cool in July, Markets Up Ante on Rate Cuts

Non-farm employment rose by 114k in July, considerably below the consensus forecast calling for a larger gain of 175k. Job gains in the two prior months were revised a bit lower, subtracting a combined 29k from the previously reported figures.

Private payrolls rose 97k, with most of the gains concentrated in health care & social assistance (+64k), construction (+25k) and leisure & hospitality (+23k). Government hiring slowed, but still added 17k jobs last month.

In the household survey, the labor force surged by 420k, while civilian employment rose by a more modest 67k – pushing the unemployment rate higher by 0.2 percentage points to 4.3%. Meanwhile, the labor force participation rate edged higher by 0.1 percentage points to 62.7%.

Average hourly earnings (AHE) rose by a modest 0.2% month-on-month (m/m) – a modest deceleration from June's 0.3% gain. On a twelve-month basis, AHE ticked down to 3.6% (from 3.8% in June) – the slowest pace of wage growth in over three years.

Key Implications

The July employment report certainly came in on the softer side. Not only did payroll growth come in handily below expectations, but revisions to months prior showed a little less hiring momentum in the second quarter and the unemployment rate also continued to edge higher. This is consistent with other labor metrics including quit and hire rates, as well as the ratio of job openings to unemployed which are all at or below pre-pandemic levels. The softening in labor market fundamentals has been evident across a number of wage metrics, which are all quickly closing in on an annualized pace of growth that is more consistent with 2% inflation (after adjusting for productivity).

Given the softening in labor market fundamentals, a September cut is almost a guarantee. The labor market is no longer adding to inflationary pressures and waiting much longer risks pushing recent normalization dynamics too far in the other direction. Following the release of this morning's report, the 2-Year Treasury slipped by over 20 basis points (bps) and markets have moved to price in over 100 bps of easing by year-end.

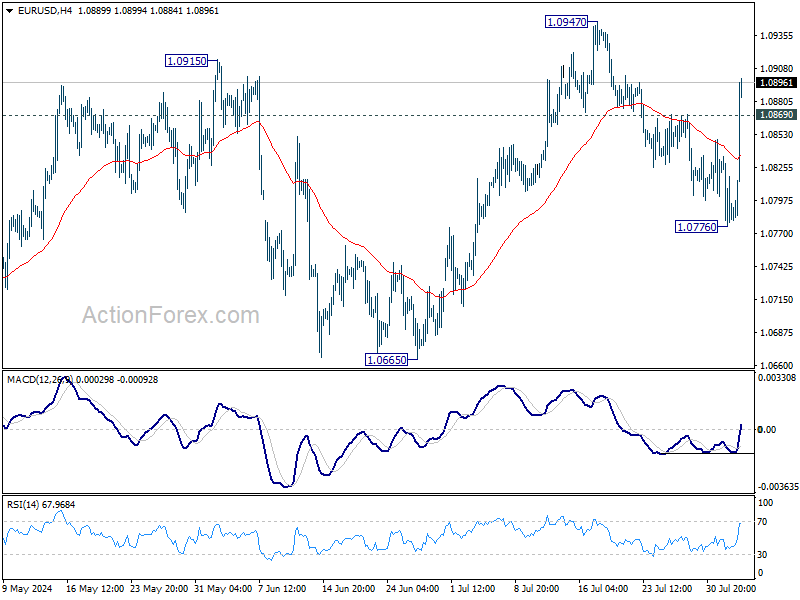

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0802; (P) 1.0826; (R1) 1.0849; More.....

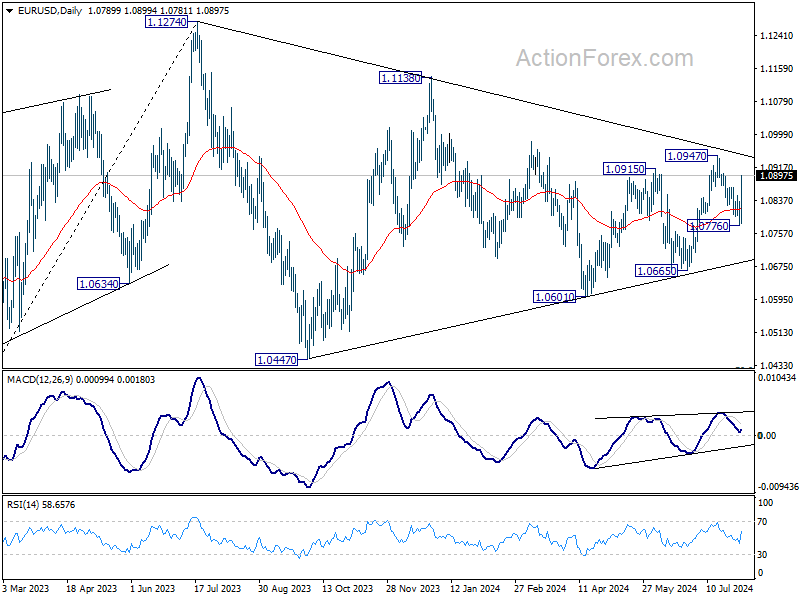

EUR/USD's strong rebound and break of 1.0869 resistance suggests that pullback from 1.0947 has completed as a correction a 1.0776. More importantly, rise from 1.0601 is probably still in progress. Intraday bias is back on the upside for retesting 1.0947 first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.

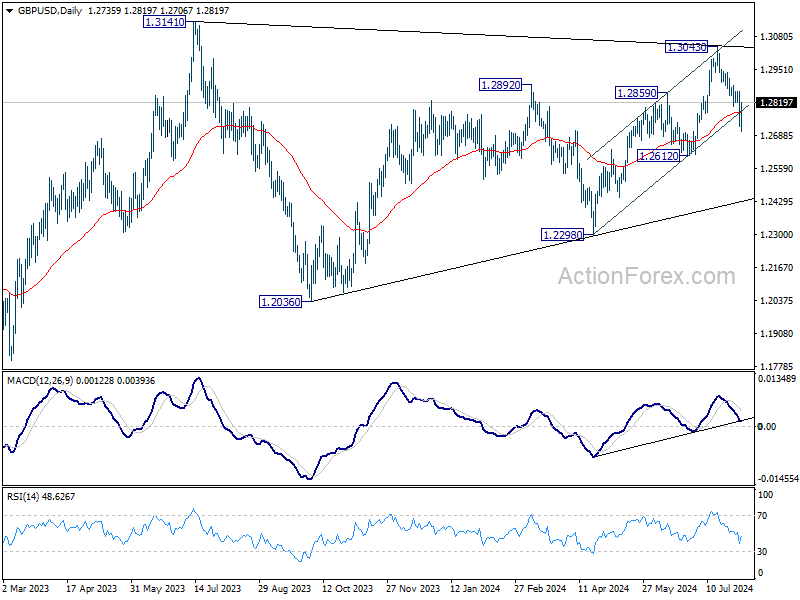

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2830; (P) 1.2847; (R1) 1.2873; More...

Intraday bias in GBP/USD is turned neutral first with current strong recovery. Another fall will remain in favor as long as 1.2863 resistance holds. Below 1.2706 will target 1.2612 support. However, firm break of 1.2863 will suggest that the pullback from 1.3043 has completed as a correction. Intraday bias will be turned back to the upside for retesting 1.3043 instead.

In the bigger picture, current development suggests that corrective pattern from 1.3141 is extending with fall from 1.3043 as another leg. Break of 1.2612 support would strengthen this case. But still, downside should be contained by 1.2036/2298 support zone. Rise from 1.0351 (2022 low) remains in favor to resume at a later stage.

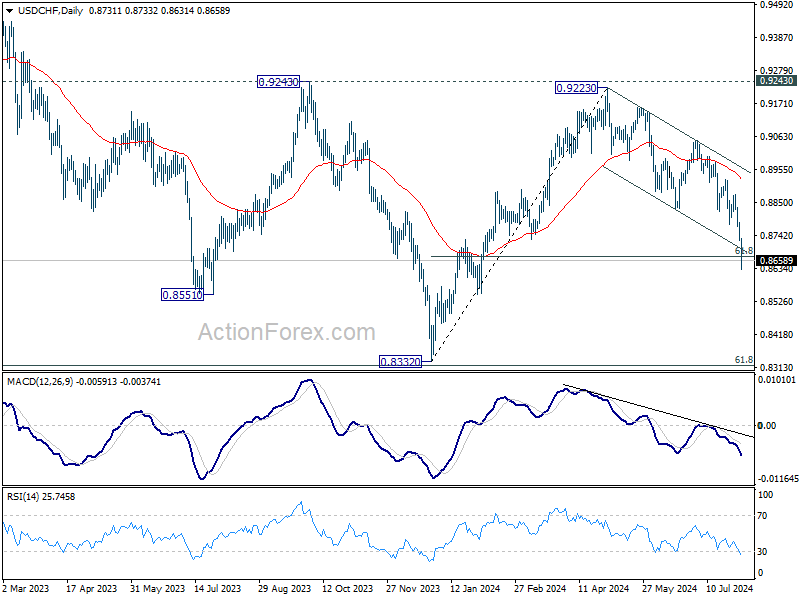

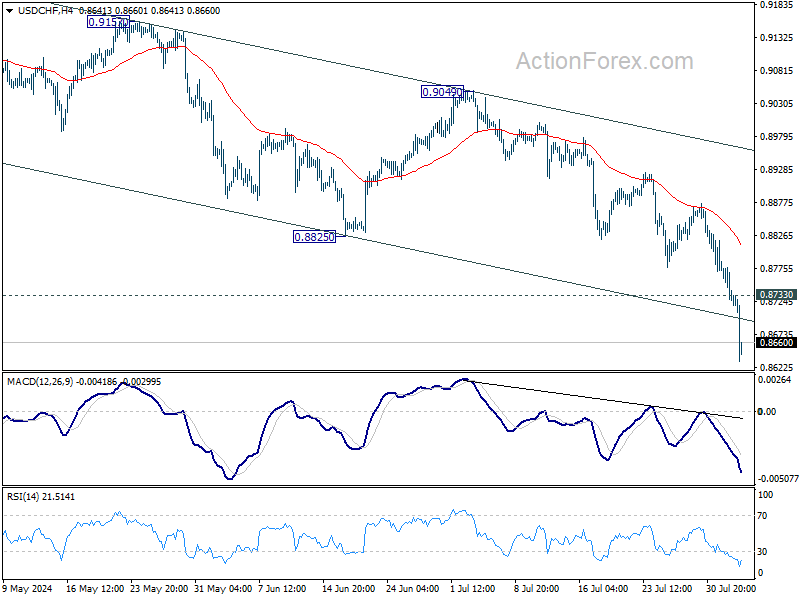

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8753; (P) 0.8797; (R1) 0.8823; More…

USD/CHF's decline from 0.9223 continues today and break of near term falling channel support indicates downside acceleration. Intraday bias stays on the downside. Sustained trading below 61.8% retracement of 0.8332 to 0.9223 at 0.8672 will pave the way to retest 0.8332 low. On the upside, above 0.8733 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.