Sample Category Title

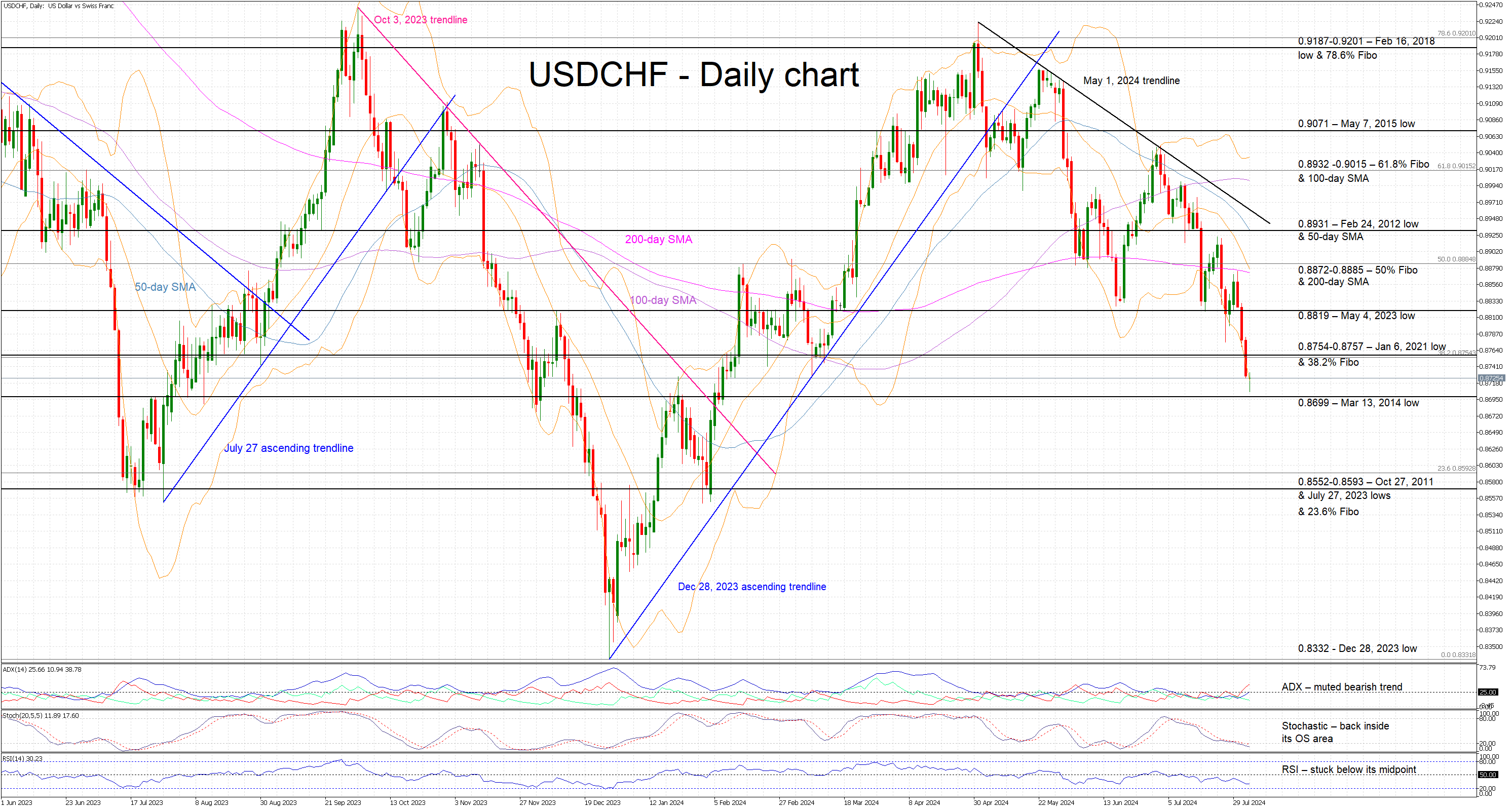

USDCHF Bearish Pressure Lingers

- USDCHF’s retreat continues with a new 6-month low recorded

- Downtrend from early May high is in place

- Momentum indicators acknowledge the bearish pressure

USDCHF is trading sideways today, a tad above the 0.8699 level and trying to record its fourth consecutive red candle since failing to break above the 200-day simple moving average (SMA). It has been a one-way move since the May 1 local peak with USDCHF actually registering a new 6-month low amidst a series of lower lows and lower highs.

Momentum indicators are mostly confirming the current bearish pressure. More specifically, the Average Directional Movement Index (ADX) is edging higher and tentatively signaling the presence of a muted bearish trend in USDCHF. Additionally, the RSI is moving lower again, far from its 50-midpoint and close to the December 2023 lows. More importantly, the stochastic oscillator has returned inside its oversold territory. There are some early signs of a bullish divergence forming but the current bearish move has to be completed first.

Should the bears remain hungry, they could try to break below the March 13, 2014 low and then have a go at pushing USDCHF even lower. The 0.8552-0.8593 range, which is defined by the October 27, 2011 low, the July 27, 2023 low and the 23.6% Fibonacci retracement of the October 21, 2022 – July 27, 2023 downtrend, stands in bears' way to test the 2024 lows.

On the flip side, the bulls will probably try to defend the 0.8699 level and then gradually set course for the 0.8754-0.8757 area that is populated by the January 6, 2021 low and the 38.2% Fibonacci retracement. Even higher, they could test the resistance set by the busy 0.8872-0.8885 region, assuming they successfully surpass the May 4, 2023 low at 0.8819.

To sum up, the ongoing bearish pressure has pushed USDCHF to a new multi-month low with the bulls desperately trying to stage a comeback.

Elliott Wave Intraday Analysis Expecting Nikkei (NKD) to Extend Lower

Short Term Elliott Wave in Nikkei (NKD) suggests the Index shows short term incomplete bearish sequence from 7.10.2024 high favoring further downside. Decline from 7.10.2024 is in progress as a double three Elliott Wave structure. Down from 7.10.2024 high, wave (W) ended at 37395. Rally in wave (X) ended at 39318 with internal subdivision as a zigzag structure. Up from wave (W), wave A ended at 38785 and wave B ended at 37395. Wave C higher ended at 39318 which completed wave (X) in higher degree.

The Index has turned lower in wave (Y) with internal subdivision as a zigzag structure. Down from wave (X), wave ((i)) ended at 37405 and wave ((ii)) ended at 38010. Wave ((iii)) lower ended at 36465 and wave ((iv)) ended at 36920. Final leg wave ((v)) ended at 36165 which completed wave A in higher degree. Wave B rally is in progress to correct cycle from 7.31.2024 high before it turns lower. Near term, while below 39318, expect rally to fail in 3, 7, or 11 swing for further downside. Potential target lower is 100% – 161.8% Fibonacci extension of wave (W). This area comes at 30932 – 34135 where buyers can appear for further upside or 3 waves rally at least.

Nikkei (NKD) 45 Minutes Elliott Wave Chart

NKD Elliott Wave Video

https://www.youtube.com/watch?v=_eVla6C-dVQ

Dollar Story a Nuanced One, UST Outperformance More Than Offset by Risk-off on Equity Markets

Markets

And the summer slide continues. Core bond yields yesterday dropped another 2.7-10.8 bps in the US & 4.9-7.8 bps in Germany. The front outperformed after a series of US economic data disappointed across the board. Weekly jobless claims rose to the highest in 11 months, Q2 unit labor costs eased sharply to 0.9% and the manufacturing ISM hit a YtD low of 46.8 with subseries such as new orders (47.4) and employment (43.4) suggesting little improvement going forward. The numbers came after the Fed on Wednesday paved the way for rate cuts soon (September). With the central bank’s “go”, the front-end of the curve is now adjusting towards the estimated terminal rate. Market expectations are currently around <3.25% by end 2026. That’s a huge shift from just a month ago (>3.75%) but it is a more realistic view assuming the Fed is headed towards neutral (+/- 3%). Long tenors join the trend lower as the recent slew of sub-par eco data makes markets ponder the risks of a sharper economic slowdown than they had expected thus far. That’s also being reflected in stock markets. Both US and European equities are under selling pressure lately. Yesterday’s 2% sell-off meant the lowest close in the EuroStoxx50 since mid-February. The S&P500 and Nasdaq wiped out post-Fed gains to close back around the July lows. European yields suffer from US spillovers while economic data (e.g. PMIs) on the bloc were not very convincing either. Here, too, money markets have come to entertain a more realistic idea of an ECB terminal rate just north of 2% instead of >2.5% one month ago. US payrolls are in focus today. We don’t think they’ll alter current market forces. The US 2-yr yield is currently hovering near the YtD lows of 4.11%. A break looks imminent in case of a further moderating labour market. 3.95-4% is then the next reference to watch. After breaking sub 4.03%, the next technical zone to watch in the US 10-yr is located at 3.78-3.81%. Unless a dramatic payrolls report sparks outright recessionary fears, we don’t assume these levels to appear on the screens today. The dollar story is a nuanced one. UST outperformance yesterday was more than offset by the risk-off on equity markets, pushing EUR/USD eventually below 1.08 again. Similar trading dynamics could play out today. The EUR/USD 1.07 zone acts as first meaningful support. EUR/GBP jumped to 0.847 yesterday. Risk sentiment was yesterday’s main driver of GBP, outplaying the BoE and is probably going to be key for GBP today too.

News & Views

The Czech central bank cut policy rates yesterday by 25 bps to 4.5%. In the policy statement published afterwards, it noted that it still sees inflationary pressures in the economy. A restrictive policy stance is still deemed necessary and as such further rate cuts are approached “with great caution”. Headline inflation is expected to average 2.2% this year and 2% in 2025. Core inflation will still be at 2.3% next year. Its policy is working though and the CNB sees the economy below potential amid weak domestic and external demand. Czech GDP is expected to grow by 1.2% this year and accelerate to 2.8% next year on a recovery of household consumption. The forecasts are made on the assumption of a further modest decline in interest rates to around 4% end 2024/early 2025. The Czech crown, which appreciated yesterday from a 2.5 year low in the wake of the decision, is seen around current levels (EUR/CZK 25.3) for the remainder of the year before appreciating gradually through 2025.

South Korean inflation rose 0.3% m/m and picked up on a yearly basis from 2.4% to 2.6% in July, snapping a cooling streak that was in place since February. Core inflation matched June’s 2.2% y/y, defying expectations for a slight easing to 2.1%. While the Bank of Korea blamed temporary factors for the uptick and sees inflation resuming the downtrend this month, it remains wary for easing policy from the current 3.5% level. It is awaiting evidence for inflation to cool as expected (and sustainably to the 2% target) while they are worried that a less restrictive stance would prompt an increase in household debt. The South Korean won slightly gains this morning to USD/KRW 1370.

Graphs

GE 10y yield

The ECB cut policy rates by 25 bps in June. Stubborn inflation (core, services) make follow-up moves less evident. Markets nevertheless price in two to three more cuts for 2024 as disappointing US and unconvincing EMU data rolled in, dragging the long end of the curve down. After breaking below 2.34%-2.4% eyes now turn to 2.12-2.16%.

US 10y yield

The Fed in its July meeting paved the way for a first cut in September. It turned attentive to risks to the both sides of its dual mandate as the economy is continuing to move better in to balance. There was no pushback against market pricing back then (75 bps cuts in 2024, 100 bps in 2025). The pivot weakened the technical picture in US yields with another batch of weak eco data pushing the 10-yr sub 4%.

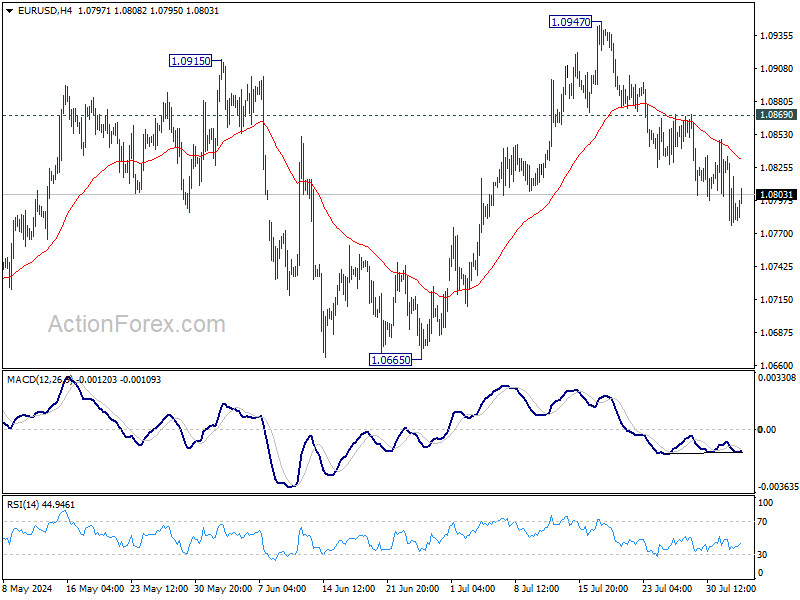

EUR/USD

EUR/USD tested the topside of the 1.06-1.09 range as the dollar lost interest rate support at stealth pace. A September rate cut is highly likely and markets increase bets on future easing on incoming weak US data. The risk-off these data trigger (sharper than expected slowdown?) offset the interest rate losses for USD. EUR/USD is moving south within the 1.07-1.09 range.

EUR/GBP

The Bank of England delivered a hawkish cut in August. Policy restrictiveness will be further unwound gradually and on a pace determined by a broad range of data. The strategy similar to the ECB’s balances out EUR/GBP in a monetary perspective. Risk-off proved a more important driver of GBP recently. We may see a return to the 0.85-0.86 sideways trading range that dominated 2024H1.

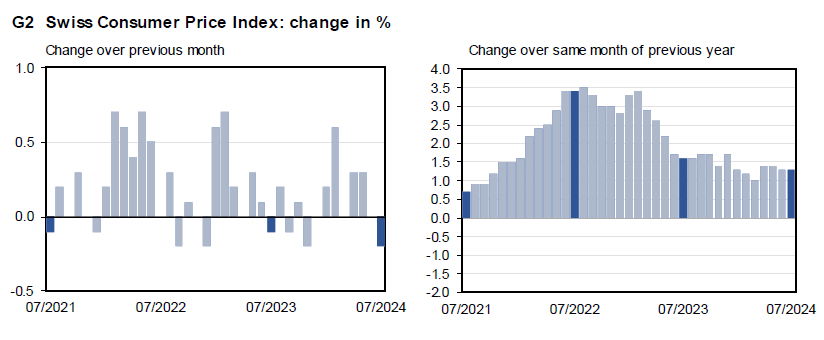

Swiss CPI at -0.2% mom, 1.3% yoy in Jul, matches expectations

Swiss CPI fell -0.2% mom in July, matched expectations. Core CPI (excluding fresh and seasonal products, energy and fuel) fell -0.3% mom. Domestic product prices rose 0.2% mom. Imported products prices fell -1.3% mom.

For the 12-month period, CPI was unchanged at 1.3% yoy, matched expectations. Core CPI was unchanged at 2.0% yoy. Domestic product prices growth was unchanged at 2.0% yoy. Import product prices growth deepened from -0.8% yoy to -1.0% yoy.

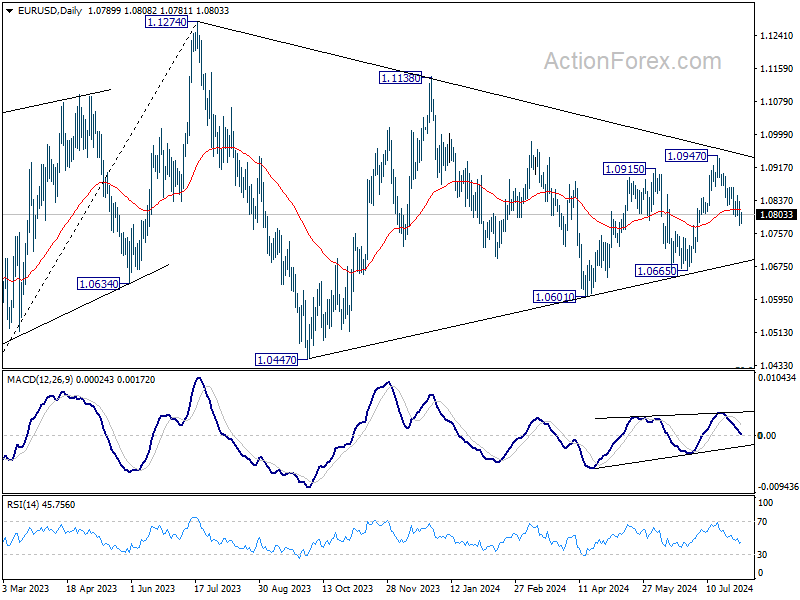

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0802; (P) 1.0826; (R1) 1.0849; More.....

Further decline is expected in EUR/USD as long as 1.0869 resistance holds. Current development suggests that rebound from 1.0601 has completed with three waves up to 1.0947. Deeper decline should be seen to 1.0665 support. Firm break there will target 1.0601 support next.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.

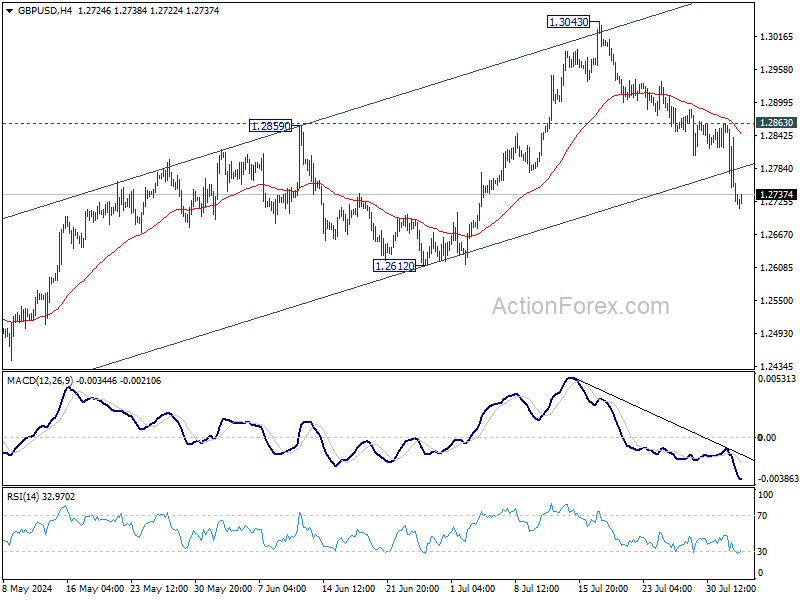

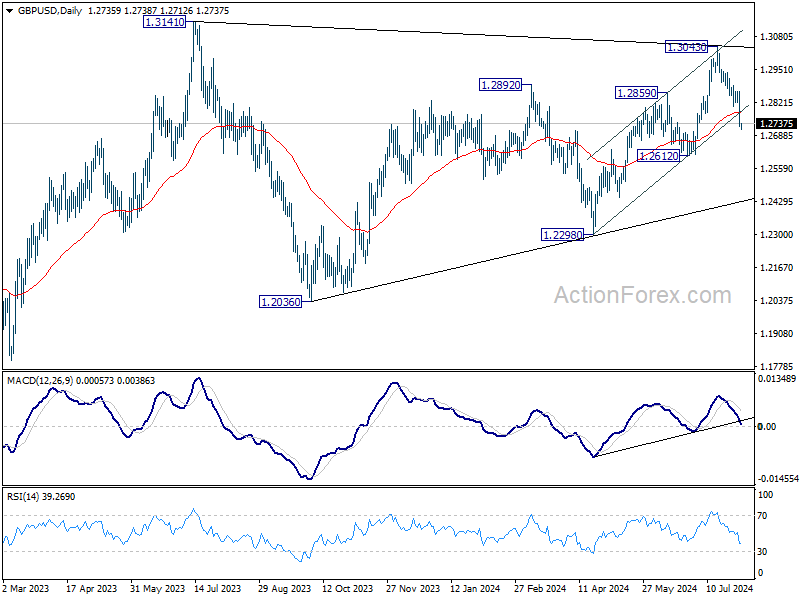

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2830; (P) 1.2847; (R1) 1.2873; More...

GBP/USD's fall from 1.3043 is in progress and intraday bias stays on the downside. Rise from 1.2298 could have completed at 1.3043 already. Deeper fall would be seen to 1.2612 support and below. On the upside, break of 1.2863 resistance is needed to indicate short term bottoming. Otherwise, outlook will stay bearish in case of recovery.

In the bigger picture, current development suggests that corrective pattern from 1.3141 is extending with fall from 1.3043 as another leg. Break of 1.2612 support would strengthen this case. But still, downside should be contained by 1.2036/2298 support zone. Rise from 1.0351 (2022 low) remains in favor to resume at a later stage.

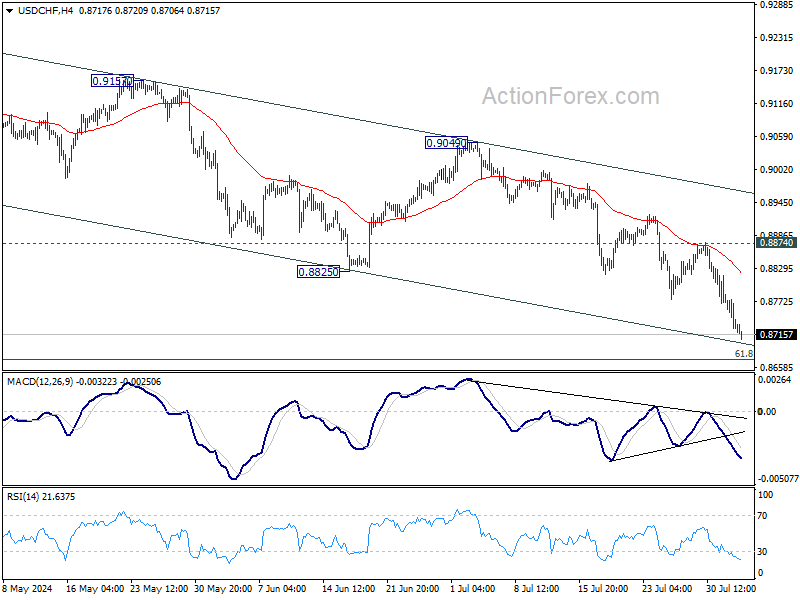

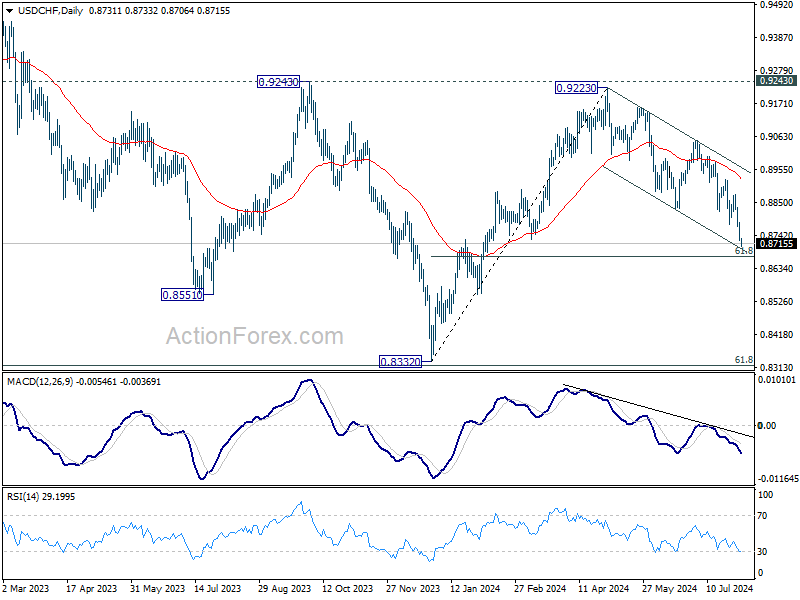

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8753; (P) 0.8797; (R1) 0.8823; More…

No change in USD/CHF's outlook as intraday bias stays on the downside. Current fall from 0.9223 is in progress for 61.8% retracement of 0.8332 to 0.9223 at 0.8672. Sustained break there will pave the way to retest 0.8332 low. For now, risk will stay on the downside as long as 0.8874 resistance holds, in case of recovery.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

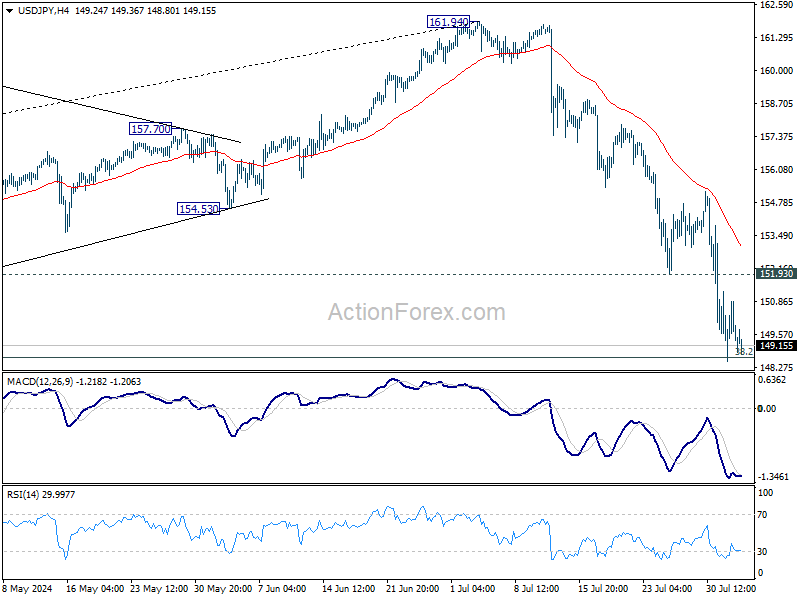

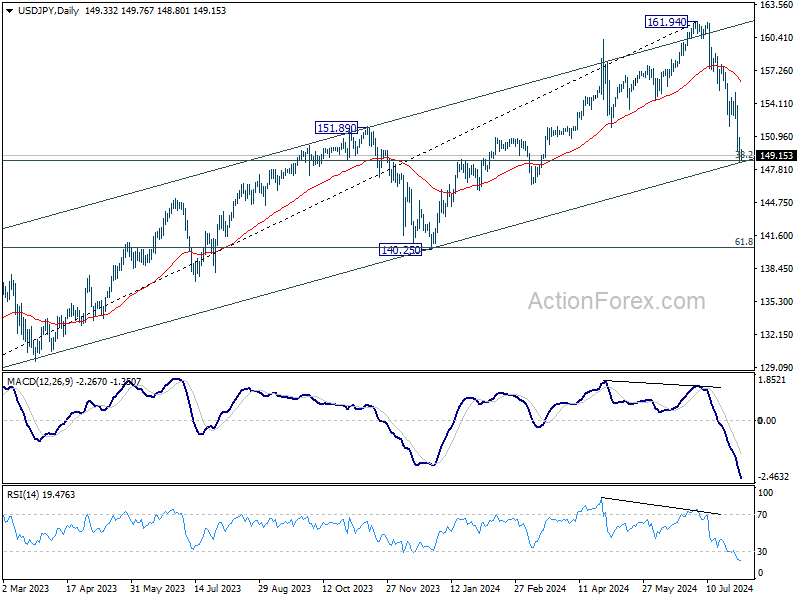

USD/JPY Daily Outlook

Daily Pivots: (S1) 148.42; (P) 151.16; (R1) 152.72; More...

No change in USD/JPY's outlook and intraday bias stays on the downside at this point. Strong support could be seen from 148.66 fibonacci level to bring consolidations. On the upside, above 151.93 support turned resistance will turn bias back to the upside for stronger recovery. Nevertheless, sustained break of 148.66 will pave the way to next support at 140.25.

In the bigger picture, considering the depth and momentum of the current decline, 161.94 should be a medium term top already. Fall from there is seen as correcting the whole rise from 127.20 (2023 low) at least. Next target is 38.2% retracement of 127.20 to 161.94 at 148.66. Decisive break there will pave the way to 140.25 support next. Risk will now stay on the downside as long as 55 D EMA (now at 156.14) holds, in case of rebound.

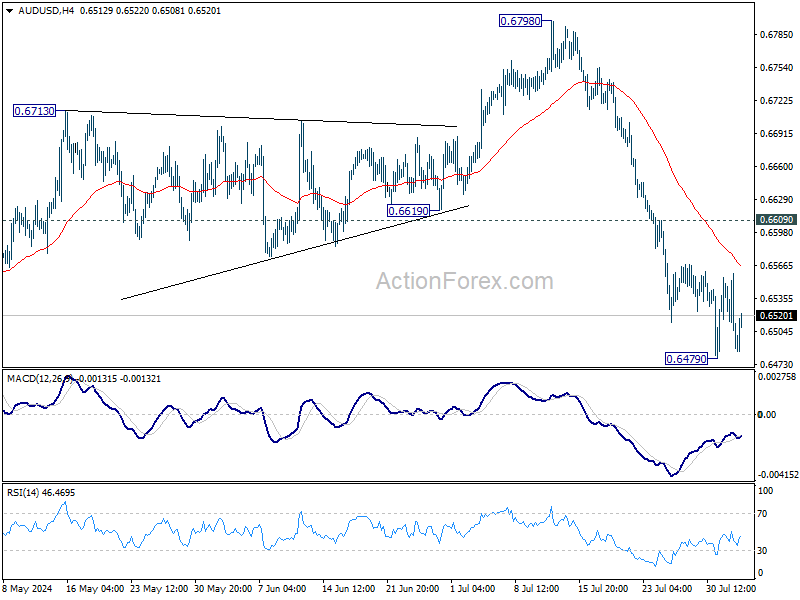

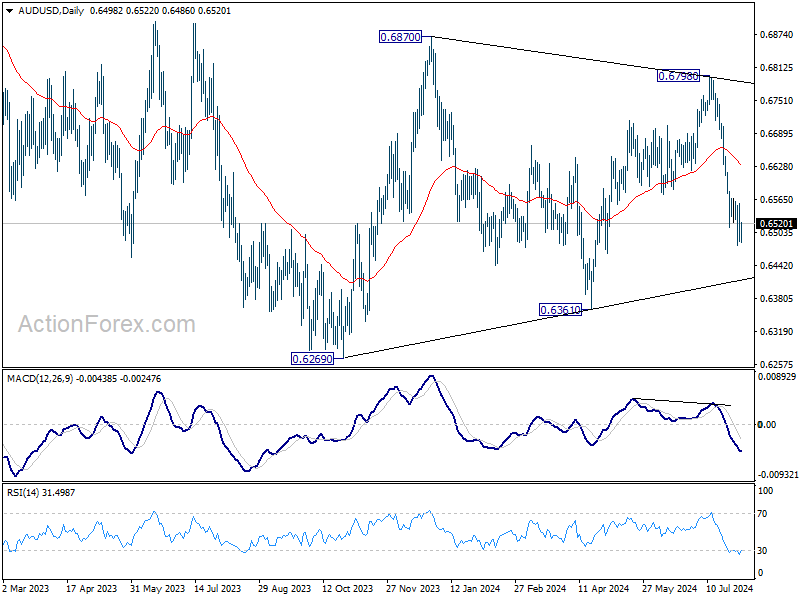

AUD/USD Daily Report

Daily Pivots: (S1) 0.6496; (P) 0.6526; (R1) 0.6572; More...

Intraday bias in AUD/USD remains neutral as consolidations continue above 0.6479 temporary low. Outlook will stay bearish as long as 0.6609 minor resistance holds, and further decline is expected. On the downside, break of 0.6479 will resume the fall from 0.6798 to 0.6361 support first. Firm break there will target 0.6269 low.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with fall from 0.6798 as another falling leg. Deeper fall could be seen to the lower side of the range between 0.6169/6361. But strong support should be seen there to contain downside. For now, risk will stay on the downside as long as 0.6798 resistance holds, in case of rebound.

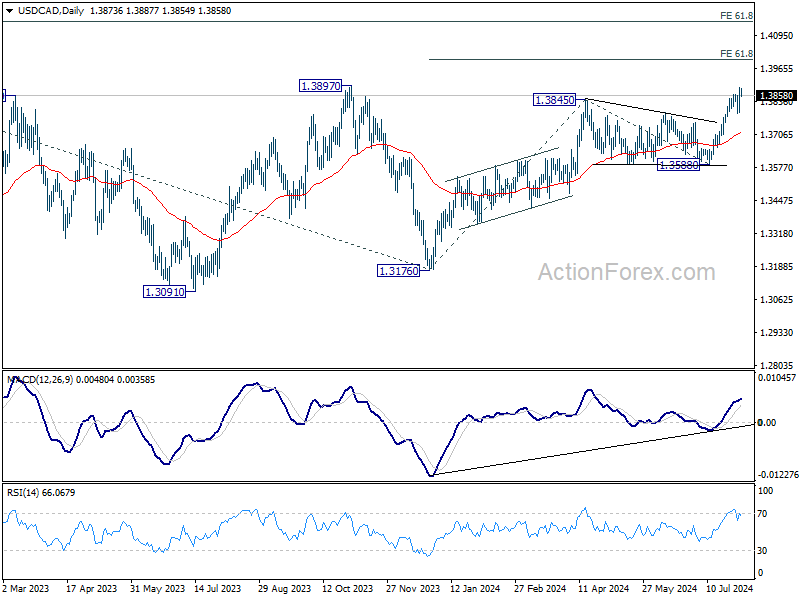

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3777; (P) 1.3818; (R1) 1.3849; More...

USD/CAD's rally resumed after brief consolidations and intraday bias is back on the upside. Current rise is part of the whole rally from 1.3176 and next target is 61.8% projection of 1.3176 to 1.3845 from 1.3588 at 1.4025. On the downside, break of 1.3786 support is needed to indicate short term topping. Otherwise, outlook will remain bullish in case of retreat.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.