Sample Category Title

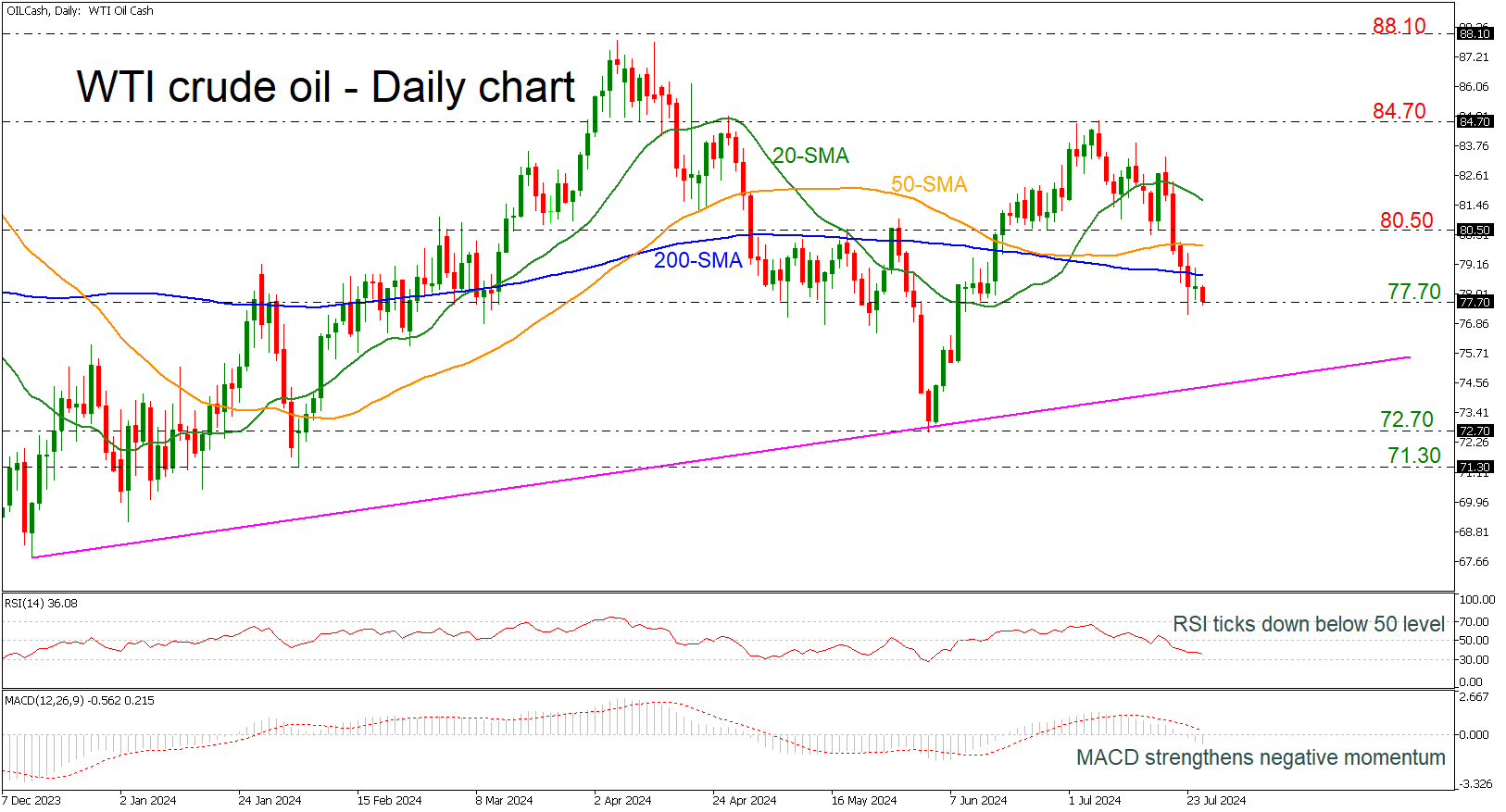

WTI Crude Oil Creates Bearish Wave

- WTI crude oil tests 77.70 support

- Price holds beneath SMAs

- RSI and MACD indicate more losses

WTI crude oil futures have been in a bearish movement after the pullback off the 84.70 resistance level. It has since slipped below the simple moving averages (SMAs) in the daily timeframe and the market is currently testing the 77.70 support level before diving towards the long-term ascending trend line near 74.80. A successful break beneath this region could open the door for more losses until the 72.70 barricade.

The technical oscillators are confirming the recent bearish movement in price. The RSI is heading south beneath the neutral threshold of 50, while the MACD is extending its bearish structure below its trigger and zero lines.

Alternatively, a climb above the 200- and 50-day SMAs could allow traders to reach the 80.50 resistance level before resting near the 20-day SMA at 81.64. Above them, the 84.70 resistance is waiting to act as a turning point again.

In summary, oil prices look bearish in the near term; however, the bigger picture is still bullish as long as they are standing above the uptrend line.

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0821; (P) 1.0844; (R1) 1.0861; More.....

Intraday bias in EUR/USD stays mildly on the downside for the moment. Fall from 1.0947 short term top should extend to 55 D EMA (now at 1.0813). Sustained break there will argue that whole rebound from 1.0601 has completed with three waves up to 1.0947, and target 1.0601/0665 support zone. On the upside, above 1.0896 minor resistance will turn intraday bias neutral first. But, risk will stay on the downside as long as 1.0947 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.

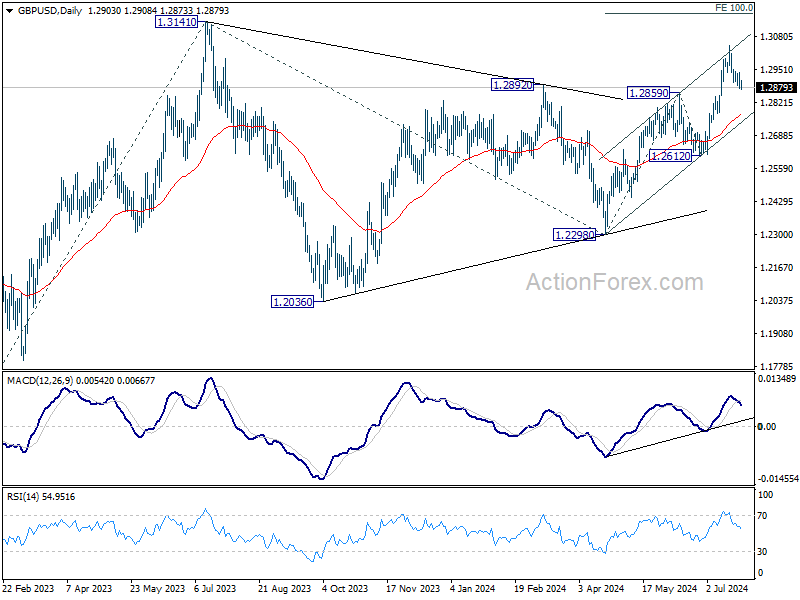

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2877; (P) 1.2907; (R1) 1.2938; More...

No change in GBP/USD's as range trading continues. Intraday bias remains neutral. Further rally is expected with 1.2859 resistance turned support intact. Break of 1.3043 will resume the rise from 1.2298 and target 100% projection of 1.2298 to 1.2859 from 1.2612 at 1.3173, which is slightly above 1.3141 key medium term resistance. However, firm break of 1.2859 will turn bias to the downside for deeper decline.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.

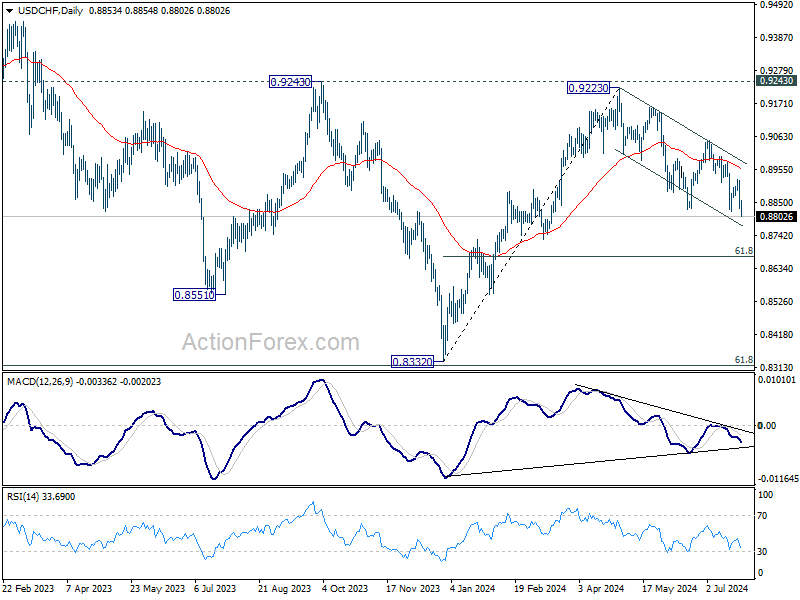

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8813; (P) 0.8868; (R1) 0.8907; More…

USD/CHF's fall from 0.9223 resumed by breaking 0.8819 support. Intraday bias stays on the downside for 61.8% retracement of 0.8332 to 0.9223 at 0.8672. For now, risk will stay on the downside as long as 0.8923 resistance holds, in case of recovery.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

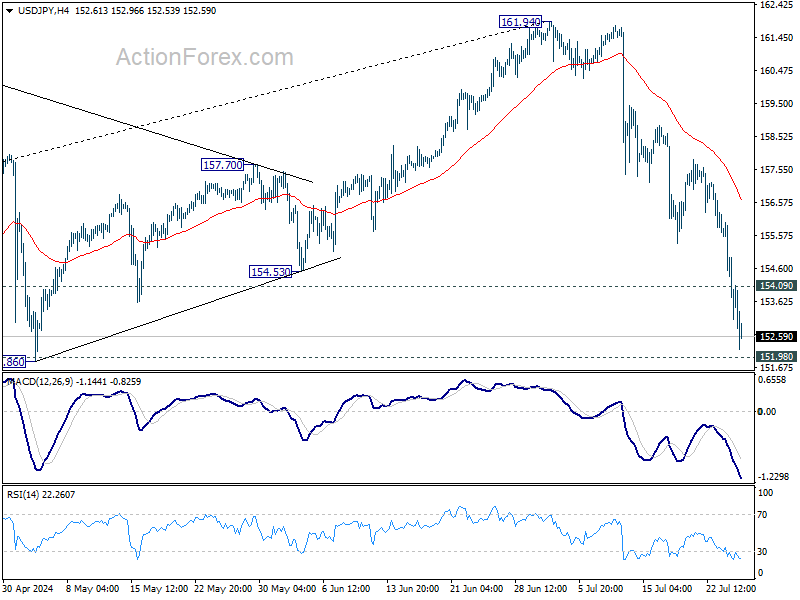

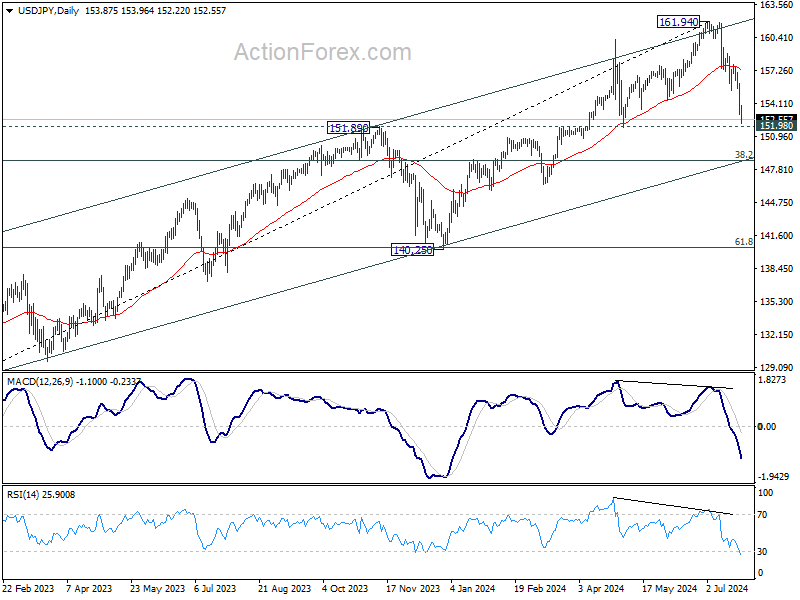

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.68; (P) 154.33; (R1) 155.56; More...

USD/JPY's fall from 161.94 continues today and there is no sign of bottoming. Intraday bias remains on the downside for 151.89 resistance turned support. Decisive break there will argue that large scale correction is underway to 148.66 fibonacci level. On the upside, above 154.09 minor resistance will turn intraday bias neutral first.

In the bigger picture, considering the depth and momentum of the current decline, 161.94 should be a medium term top already. Fall from there is seen as correcting the whole rise from 127.20 (2023 low) at least. Break of 151.89 will pave the way to 38.2% retracement of 127.20 to 161.94 at 148.66. Risk will now stay on the downside as long as 55 D EMA (now at 157.25) holds, in case of rebound.

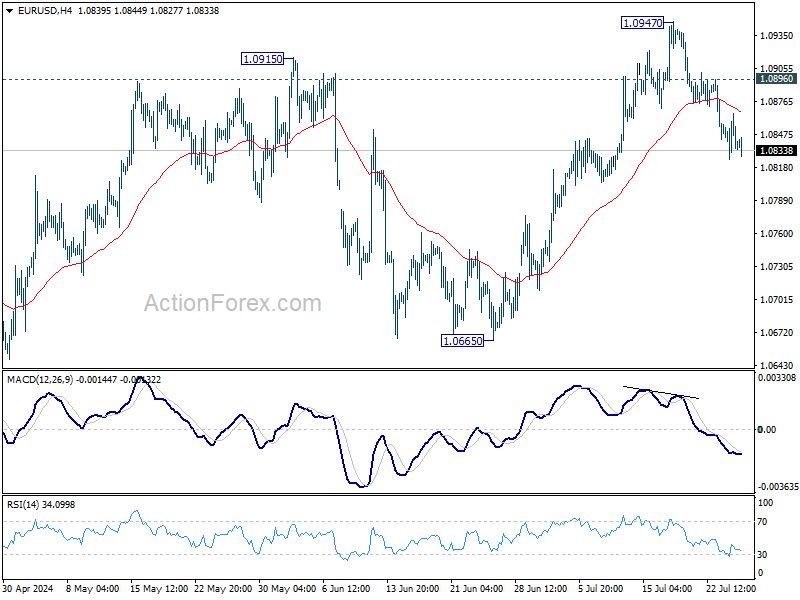

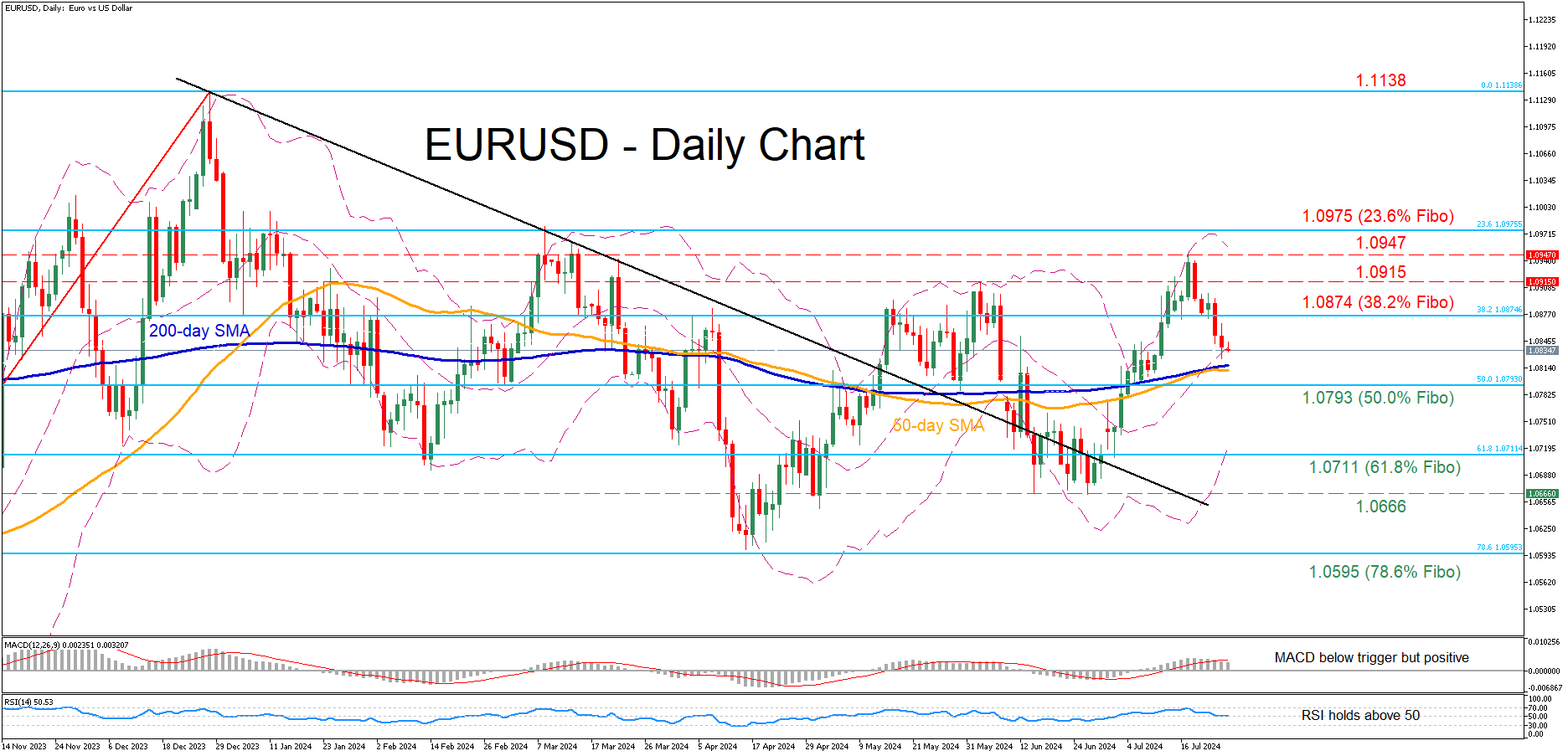

EURUSD Pulls Back Towards Converging SMAs

- EURUSD retraces lower after hitting 4-month high

- The bears eye converging 50- and 200-day SMAs

- Oscillators deteriorate but remain in positive zones

EURUSD had been rising steadily following its bullish breakout from a downward sloping trendline in early July, posting a fresh four-month peak of 1.0947 last week. However, the pair has been experiencing a correction since then, with the price approaching the converging 50- and 200-day simple moving averages (SMAs).

Should the retreat extend further and the pair break below its SMAs, initial support could be found at 1.0793, which is the 50.0% Fibonacci retracement of the 1.0447-1.1138 upleg. Lower, the 61.8% Fibo of 1.0711 might act as the next line of defense. Failing to halt there, the pair may then decline towards the June bottom of 1.0666.

Alternatively, if the price reverses back higher, the 38.2% Fibo of 1.0874 could prevent initial upside attempts. A violation of that hurdle could pave the way for the June peak of 1.0915 ahead of the recent four-month high of 1.0947. Claiming the latter barricade, the bulls could attack the 23.6% Fibo of 1.0975.

In brief, EURUSD has come under selling pressure after posting a fresh four-month high last week. Should the pullback extend further, the pair’s next crucial battle will probably take place around the converging 50- and 200-day SMAs.

Markets Gradually Moving to a Scenario of Fed Cutting Cumulative 75 bps This Year

Markets

Market focus yesterday initially was on the PMI releases. Later sentiment turned sharply risk-off even as there was no outright link between both storylines. EMU PMI’s (50.1 from 50.9) indicated that activity came to an almost standstill at the start of Q3. This triggered a further dis-inversion/steepening of the EMU/German curve, even as costs/price pressures remain high. The 2-y German yield declined 6.0 bps while long-term yields rose (30-y +2.5 bps). PMI’s in the UK (composite 52.7 from 52.3) and the US (55.0 from 54.8) were better than expected, but yield markets in both countries joined the broader steepening trend. In the US, poor new homes sales also was seen as a pointer that a restrictive monetary policy was weighing on activity that might force the Fed to cut rates rather soon. US 2-y yield declined about 3 bps while the 30-y rose 5.8 bps. Markets are gradually moving to a scenario of the Fed cutting its policy rate by a cumulative 75 bps this year, starting in September. Next to the data, sentiment was further shaped by an outright risk-off positioning after disappointing earnings from some US tech bellwethers. The S&P 500 lost 2.31%. Nasdaq tumbled 3.64%. In this context, one could expect a strong USD, but this wasn’t really the case. The DXY index even declined marginally (104.39), mainly due to sharp outperformance of the yen (USD/JPY close 153.89 from 155.6). The EUR/USD also limited the damage from the poor PMI’s (close 1.084). Remarkable, a new test of the EUR/GBP 0.84 also didn’t succeed, despite a better UK PMI’s, especially compared to the EMU.

Yesterday’s WS risk-off also dominates Asian trading (e.g Nikkei -3.25%). US yields extend their decline. The yen continues its sharp ascent. (USD/JPY 152.7). Later today, the calendar contains German IFO confidence, the first estimate of the Q2 US GDP (including price deflators), US weekly jobless claims and US durable goods orders. Consensus expects annualized Q/Q growth at 2.0% (from 1.4%). We even see an upward risk. Question remains whether a solid growth figure will be enough to change recent market drive pushing for ‘frontloaded’ Fed rate cuts. The US 2-y yield currently is at risk of falling below the 4.40% support. Recently markets were more sensitive to negative rather than positive news. In this respect weaker claims of durable goods orders and a risk-off sentiment also still have to role to play. With respect the FX impact of a risk-off correction, we also look out on the battle for the preferred safe haven between the yen and the dollar. At least for now the former remains in pole position. EUR/USD also shows ‘remarkable’ resilience with next support near 1.08 (50% retracement/early July lows).

News & Views

The Bank of Canada cut its policy rate from 4.75% to 4.5% yesterday. New forecasts showed that excess supply in the economy has increased. Household spending, including both consumer purchases and housing, has been weak and there are signs of slack in the labour market. GDP is expected to grow 1.2% this year, 2.1% in 2025 and 2.4% in 2026. CPI eased to 2.7% in June after increasing in May while the central bank’s preferred measures of core inflation have been below 3% for several months. Additionally, the breadth of price increases is now near its historical norm. The BoC forecasts core inflation to slow further to around 2.5% in 2024H2 and ease gradually through 2025. The path of headline CPI may be bumpy, temporarily dropping below core measures before returning sustainably to the 2% target in H2 2025. The BoC did not offer concrete hints on future cuts other than saying they will be guided by incoming information. Money markets upped their bets for another two rate cuts this year following the one yesterday (97% discounted). The Canadian swap curve turned less inverse with losses at the front of as much as 8.6 bps. These were partially inspired by the general risk-off move though. The Loonie extended the mid-July losing streak which coincided with a sharp oil correction as well. USD/CAD (1.382) is nearing the April highs of 1.3846.

China lowered the rate on its one-year policy loans this morning. The decision was unexpected and unusually large (20 bps, to 2.30%). This first reduction in a year followed Monday’s cut of the 7-day repo rate, which is now transforming into the new reference rate. But just like Monday’s reduction, there’s doubt whether it’ll really move a needle for China’s ailing economy. Demand for the policy loans is low given its high cost relative to market rates, which have come down sharply over the past months. China’s yuan nevertheless strengthened against the US dollar this morning for a second day straight. The move is at least as much inspired by the USD/JPY cross rate though. USD/CNY dropped from 7.2755 at the open yesterday to 7.2518 currently.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. Meanwhile, much of the save haven bids were reversed after the (first round in) the French elections. The 2.34%-2.4% support zone looks solid.

US 10y yield

The Fed indicated that it needs more evidence to lower its policy rate. June dots suggested one move in 2024 and four next year. Disappointing ISM and back-to-back downward CPI surprises put the US money market back on (at least) two rate cuts this year (September/December). The US 10-yr yield tests the recent lows and the downside of the downward trend channel in the 4.2% area.

EUR/USD

EUR/USD is testing the topside of the 1.06-1.09 range as the dollar loses interest rate support at stealth pace. Markets consider a September rate cut a done deal and only need confirmation from high-ranked Fed officials. In the meantime, the euro got rid of the (French) political risk premium. EUR/USD recently evolved back to a more neutral positioning.

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. Labour has yet to reveal its policy plans after securing a landslide election victory. EUR/GBP 0.84 support is being tested.

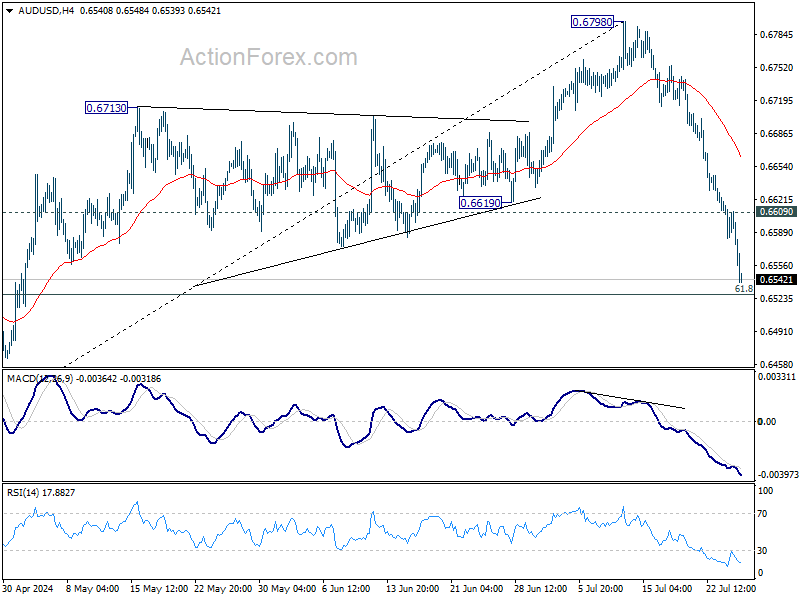

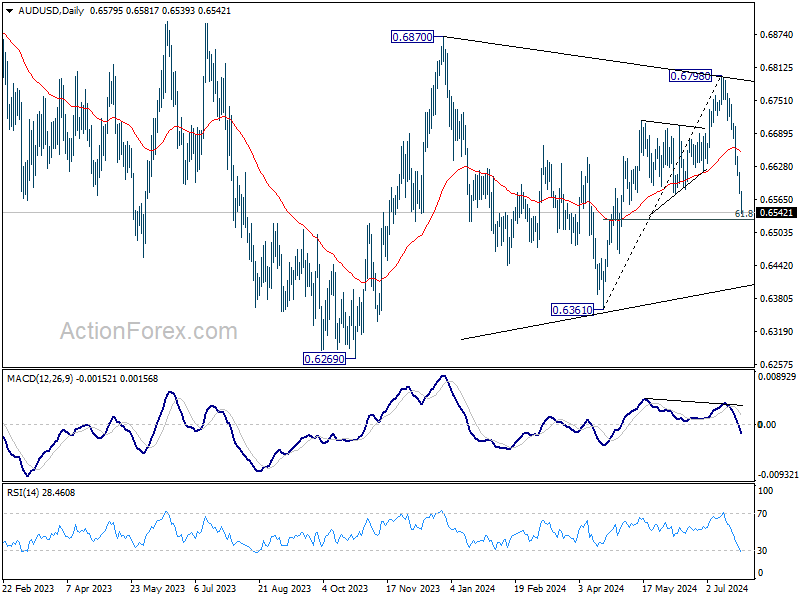

AUD/USD Daily Report

Daily Pivots: (S1) 0.6566; (P) 0.6593; (R1) 0.6608; More...

AUD/USD's fall from 0.6798 accelerates lower today and there is no sign of bottoming. Intraday bias stays on the downside for 61.8% retracement of 0.6361 to 0.6798 at 0.6528. Sustained break there will pave the way back to 1.6361 support next. On the upside, above 0.6609 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another fall.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with fall from 0.6798 as another falling leg. Deeper fall could be seen to the lower side of the range between 0.6169/6361. But strong support should be seen there to contain downside. For now, risk will stay on the downside as long as 0.6798 resistance holds, in case of rebound.

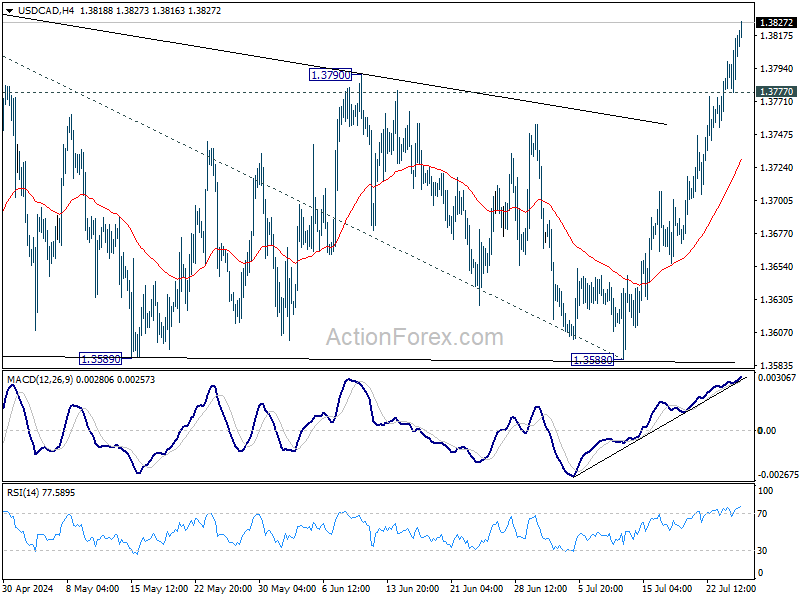

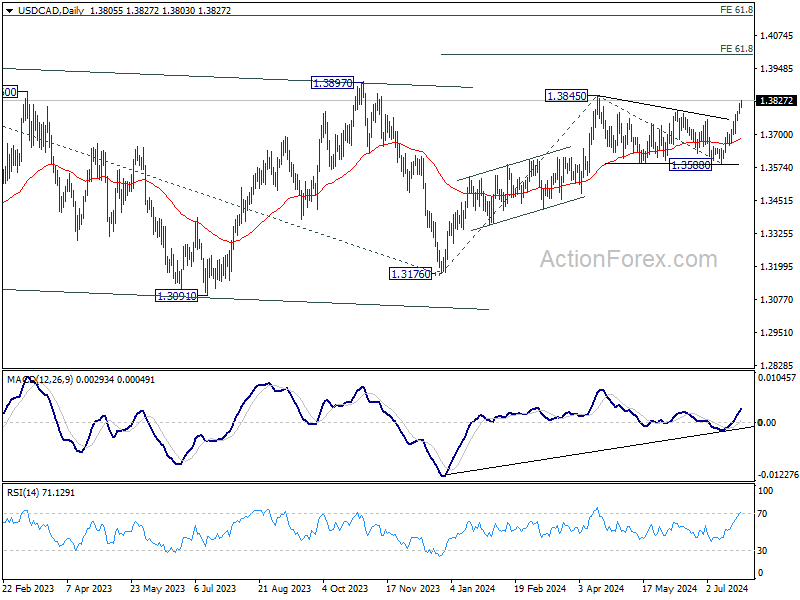

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3786; (P) 1.3801; (R1) 1.3824; More...

Intraday bias in USD/CAD remains on the upside for retesting 1.3845 high. Decisive break there will resume whole rally from 1.3176. Next target is 61.8% projection of 1.3176 to 1.3845 from 1.3588 at 1.4025. On the downside, below 1.3777 minor support will turn intraday bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.

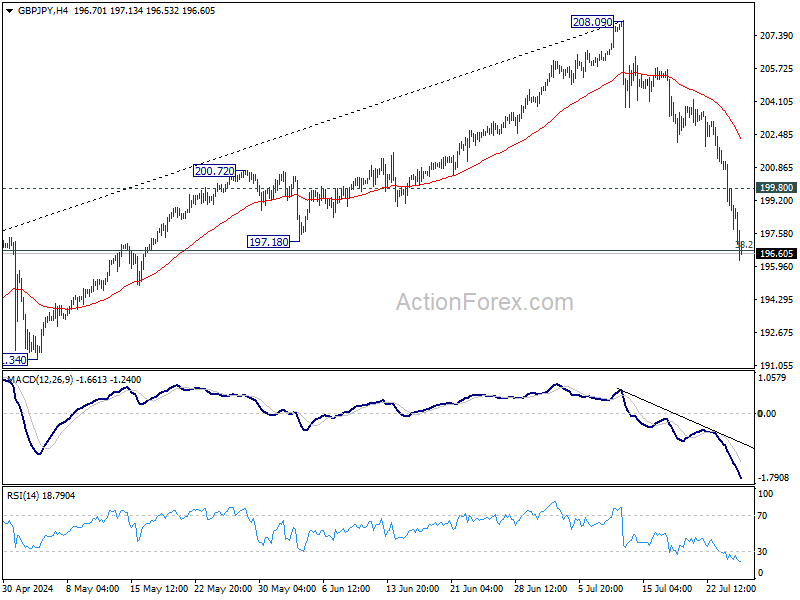

GBP/JPY Daily Outlook

Daily Pivots: (S1) 197.22; (P) 199.20; (R1) 200.63; More...

There is no sign of bottoming in GBP/JPY yet as fall from 208.09 continues today. Intraday bias stays on the downside. Sustained trading below 38.2% retracement of 178.32 to 208.09 at 196.71 will argue that larger scale correction is under way to 185.49 fibonacci level. On the upside, above 199.80 minor resistance will turn intraday bias neutral first.

In the bigger picture, considering bearish divergence condition in W MACD, 208.09 might be a medium term top and fall from there could already be correcting whole up trend from 148.93 (2022 low). Risk will now stay on the downside as long as 55 D EMA (now at 201.00). Sustained break of 196.71 will pave the way to 38.2% retracement of 148.93 to 208.09 at 185.49.