Sample Category Title

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2884; (P) 1.2911; (R1) 1.2935; More...

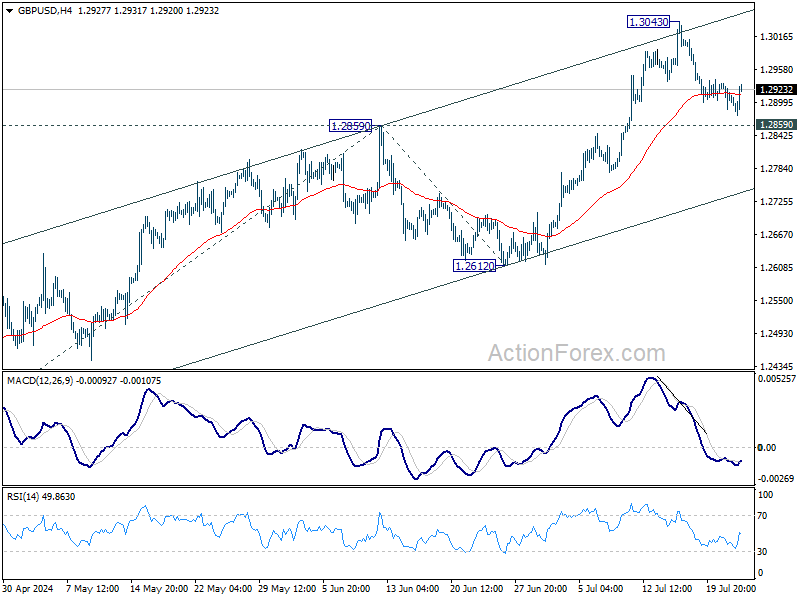

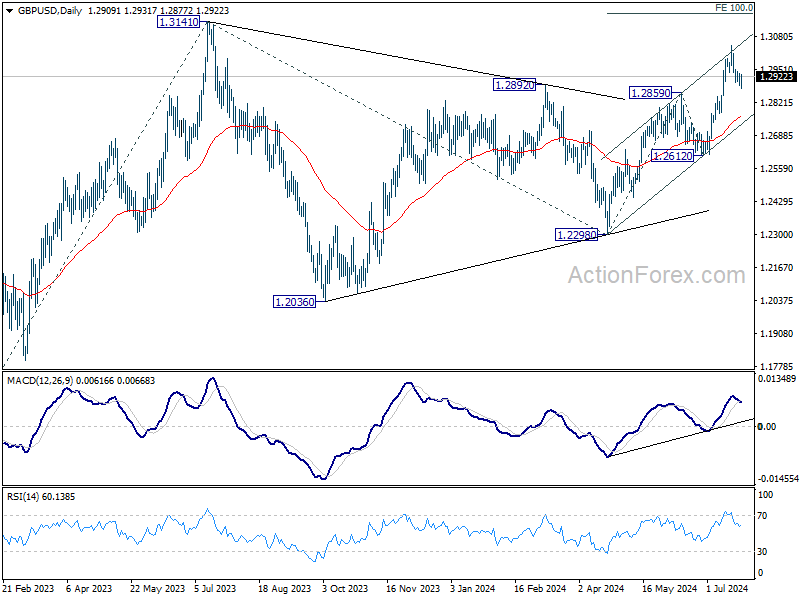

Range trading continues in GBP/USD and intraday bias stays neutral. Further rally is expected for with 1.2859 resistance turned support intact. Break of 1.3043 will resume the rise from 1.2298 and target 100% projection of 1.2298 to 1.2859 from 1.2612 at 1.3173, which is slightly above 1.3141 key medium term resistance. However, firm break of 1.2859 will turn bias to the downside for deeper decline.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.

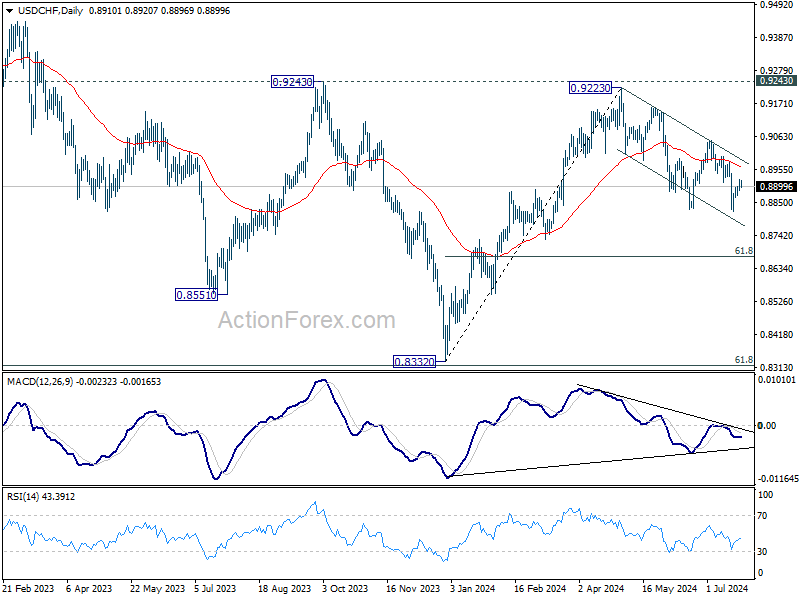

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8891; (P) 0.8908; (R1) 0.8930; More…

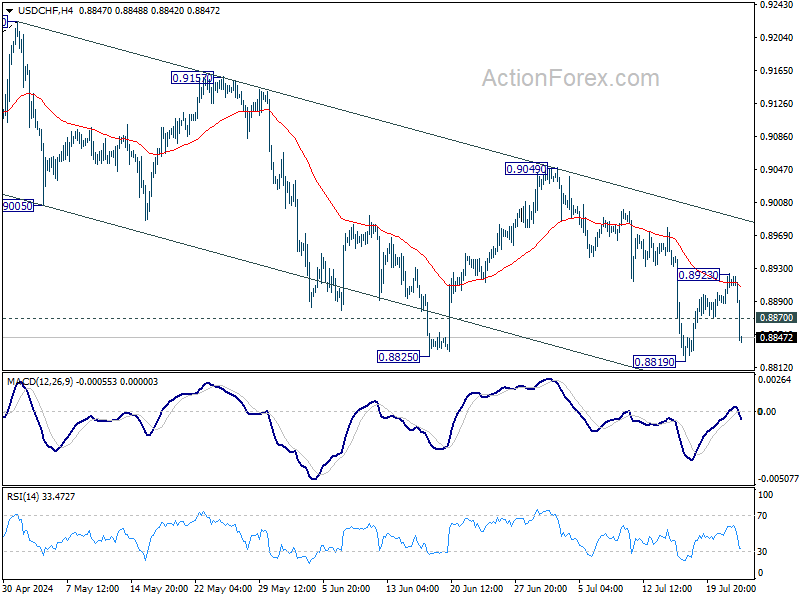

USD/CHF's sharp decline suggests that recovery from 0.8819 has completed at 0.8923, after rejection by 55 4H EMA. Intraday bias is back on the downside for 0.8819. Firm break there will resume whole fall from 0.9223. Next target is 61.8% retracement of 0.8332 to 0.9223 at 0.8672. For now, risk will stay on the downside as long as 0.8923 resistance holds.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

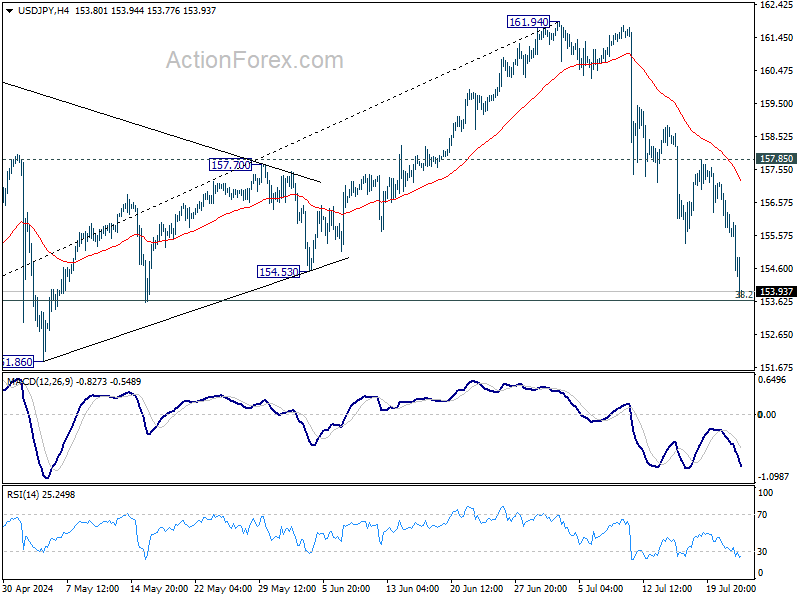

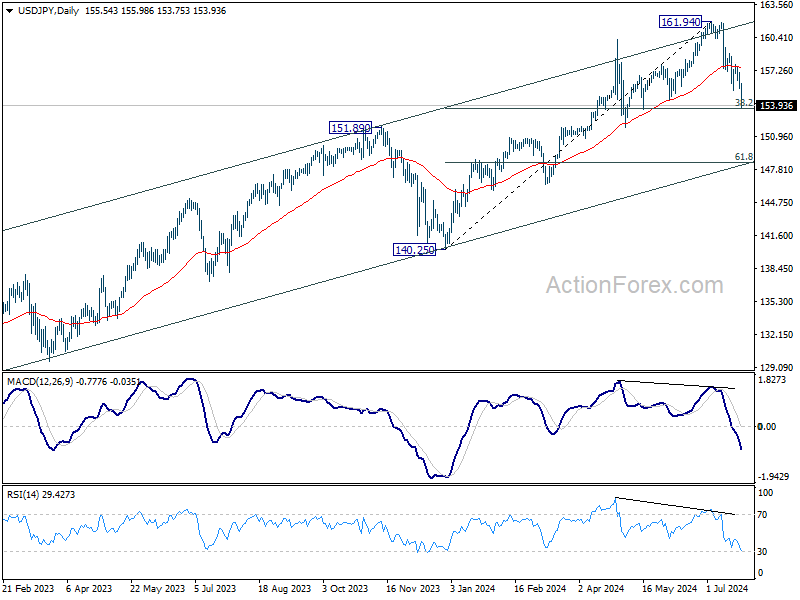

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.06; (P) 156.08; (R1) 156.60; More...

Intraday bias in USD/JPY remains on the downside with focus on 38.2% retracement of 140.25 to 161.94 at 153.65. Some support could be seen there to bring rebound, at least on first attempt. But risk will stay on the downside as long as 157.85 resistance holds, even in case of strong recovery. Sustained break of 153.65 would pave the way to 61.8% retracement at 148.53.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

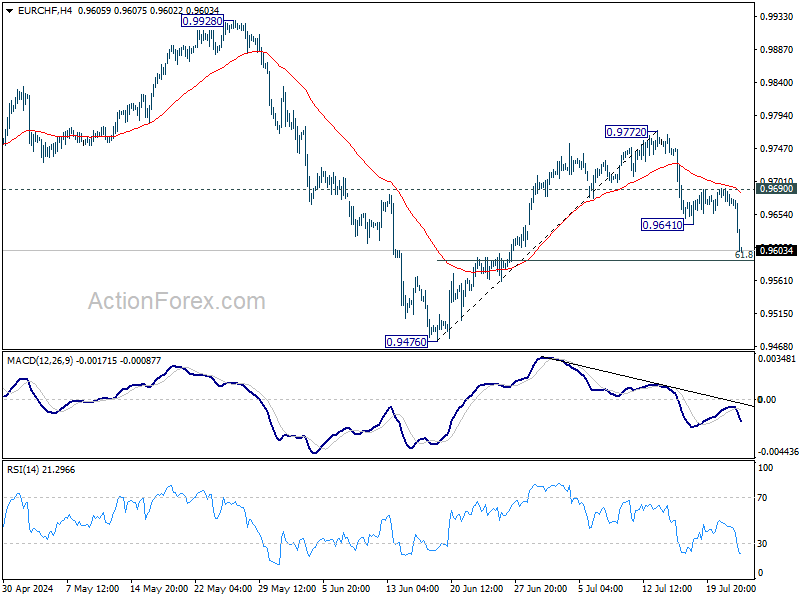

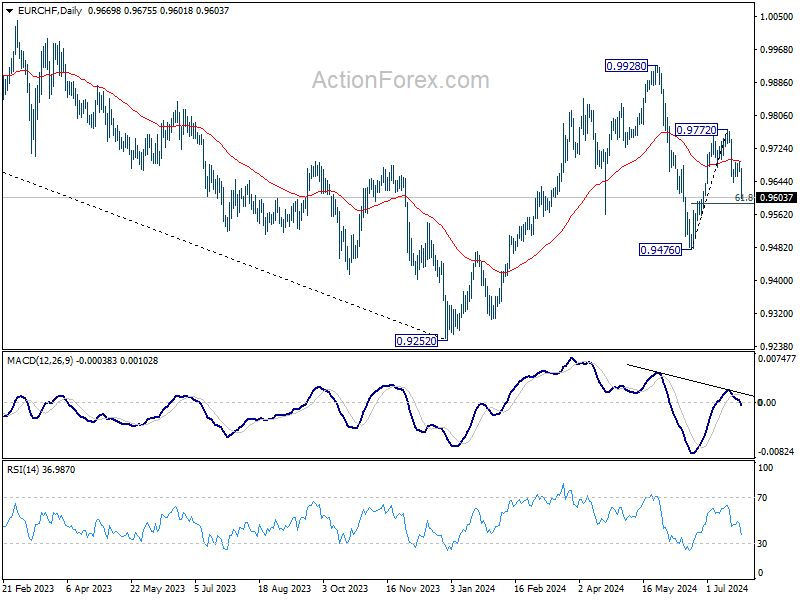

EUR/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9665; (P) 0.9678; (R1) 0.9688; More....

EUR/CHF's fall from 0.9772 resumed by breaking through 0.9641 support and intraday bias is back on the downside. Next target is 61.8% retracement of 0.9476 to 0.9772 at 0.9589. Sustained break there will target 0.9476 low. For now, risk will stay on the downside as long as 0.9690 resistance holds, in case of recovery.

In the bigger picture, rebound from 0.9252 medium term bottom might not be completed yet. But even in case of resumption, strong resistance could emerge from 1.0095 to limit upside. Medium term outlook will be neutral at best as long as 1.0094 structural resistance holds. Meanwhile, break of 0.9476 will bring retest of 0.9252 low.

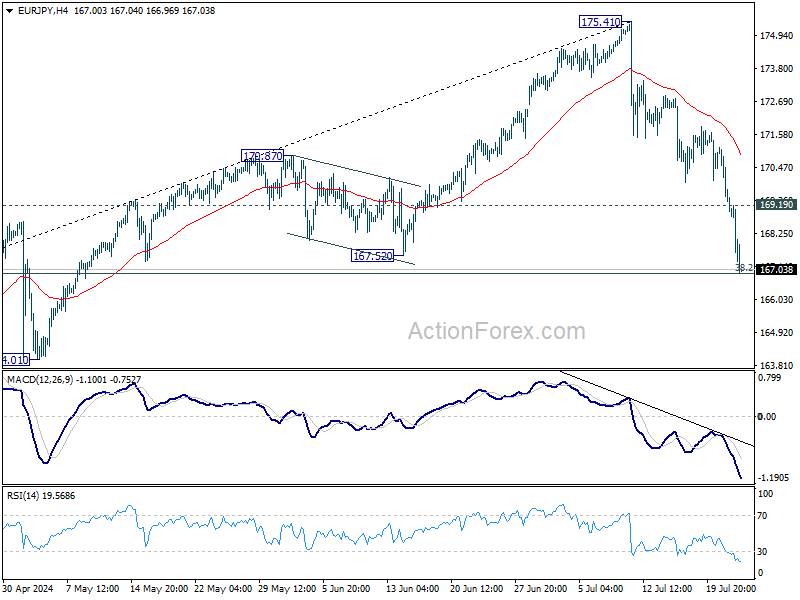

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 168.13; (P) 169.61; (R1) 170.38; More...

EUR/JPY's fall from 175.41 accelerates lower today and it's now pressing 38.2% retracement of 153.15 to 175.41 at 166.90. Some support could be seen from this fibonacci level, and break of 169.19 minor resistance will turn intraday bias neutral first. However, decisive break of 166.90 will pave the way to medium term channel support (now at 165.46).

In the bigger picture, medium term outlook will stay bullish as long as 164.29 resistance turned support holds. Long term up trend is still in favor to continue through 175.41 at a later stage. However, firm break of 164.29 will be a strong sign of bearish trend reversal.

Euro Slips After Weak PMI Data, Yen Extends Gains on BoJ Speculations

Yen continues to dominate the forex markets today, with speculation heating up ahead of next week's BoJ meeting. According to a Reuters report, unnamed sources have confirmed that a rate hike will be debated at the meeting. However, the decision is expected to be a "close call," described as a "judgment call" on whether to "act now or later this year." It is also believed that BoJ will unveil a plan to roughly halve its bond purchases in the coming years, continuing its steady withdrawal from massive monetary stimulus.

Meanwhile, Euro is under pressure following disappointing PMI data, which showed significant deterioration in the manufacturing sector while services growth remained moderate only. This data should justify a September ECB rate cut, although inflation data might complicate further cuts beyond that. On the other hand, Sterling is supported by solid PMI figures, bolstering the stance of BoE hawks against a rate cut in August.

Overall in the currency markets, Swiss Franc is the second strongest for the day, trailing the Yen, with support from buying against Euro. Sterling follows as the third strongest. New Zealand Dollar is currently the worst performer, followed closely by Australian Dollar and then Euro. Dollar and Canadian Dollar are positioned in the middle, with the latter awaiting BoC rate cut later in the session.

Technically, the medium term bearish case for Nikkei continues to build up with today's break of 55 D EMA, as well as trend line support. A medium term top is likely in place at 42426.77 on bearish divergence condition in D MACD. Fall from there could be correcting the whole five-wave rally from 25661.89. Deeper decline would be seen to 37950.19 support first, and firm break there will solidify this case. Next medium term target would be 38.2% retracement of 25661.89 to 42426.77 at 36022.58. The depth of Nikkei correction could be used to verify the depth of USD/JPY's based on their close correlation.

In Europe, at the time of writing, FTSE is down -0.08%. DAX is down -0.75%. CAC is down -1.03%. UK 10-year yield is up 0.013 at 4.141. Germany 10-year yield is down -0.004 at 2.439. Earlier in Asia, Nikkei fell -1.11%. Hong Kong HSI fell -0.91%. China Shanghai SSE fell -0.46%. Singapore Strait Times fell -0.01%. Japan 10-year JGB yield rose 0.0144 to 1.078.

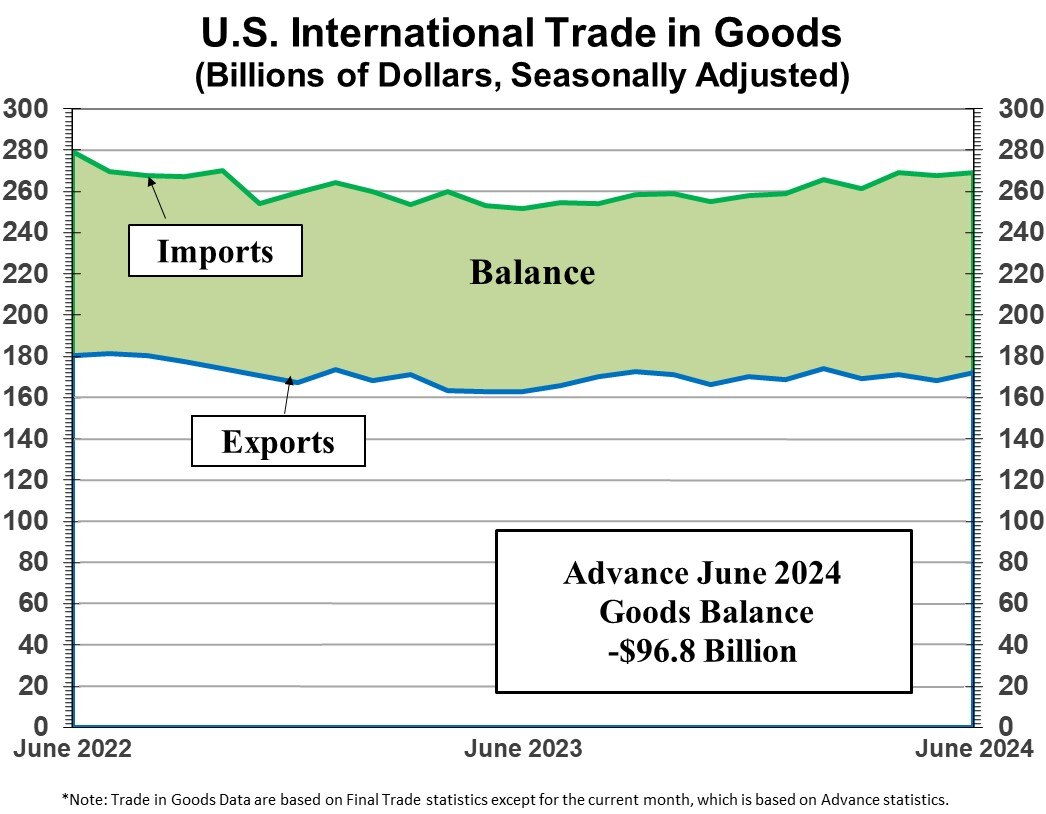

US goods exports rises 5.7% yoy, imports rises 6.9% yoy

US goods exports rose 5.7% yoy to 172.32B in June. Goods imports rose 6.9% yoy to USD 269.16B. Trade balance reported USD -96.84B, versus expectation of USD -98.0B.

Wholesale inventories rose 0.2% mom to USD 903.3B. Retail inventories rose 0.7% mom to USD 802.1B.

UK manufacturing PMI hits 24-month high, encouraging start to H2

UK PMI data for July reveals a promising start to the second half of the year. PMI Manufacturing rose to 51.8, exceeding expectations of 51.1 and marking a 24-month high. PMI Services also increased slightly from 52.1 to 52.4, though just below the forecast of 52.5. The overall PMI Composite index improved from 52.3 to 52.7.

Chris Williamson, Chief Business Economist at S&P Global Market Intelligence, noted, "The flash PMI survey data for July signal an 'encouraging start' to the second half of the year, with output, order books, and employment all growing at faster rates amid rebounding business confidence, while price pressures moderated."

Post-election business sentiment has surged, with increased demand and hiring in both manufacturing and services sectors. Despite the slowest price rise in three and a half years, suggesting potential for a summer rate cut, caution remains.

"Policymakers will likely take a cautious approach to loosening policy amid signs of inflationary pressures pivoting away from services towards manufacturing, where Red Sea shipping delays and higher freight prices are adding to costs again," Williamson added. The renewed hiring trend could also sustain wage pressures, keeping inflation somewhat persistent.

Eurozone PMI composite hits 5-month low at 50.1, ECB's post-September rate cut path uncertain

Economic activity in Eurozone weakened in July, with PMI Manufacturing dipping from 45.8 to 45.6, a seven-month low, and missing expectations of 46.3. PMI Services also declined from 52.8 to 51.9, below the anticipated 52.9, marking a four-month low. Consequently, PMI Composite fell from 50.9 to 50.1, a five-month low.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that the Eurozone economy "barely moved" in July. He highlighted that the manufacturing sector "deteriorated significantly," offsetting "moderate growth" in the services sector.

While current growth data might justify a September rate cut by ECB, inflation data complicates this decision. De la Rubia noted that input prices in the services sector rose faster, and selling prices remained steady. Manufacturing input prices, which had fallen for over a year, have increased for two consecutive months. Output prices only marginally decreased.

De la Rubia added "Our conclusion is that while a September rate cut will most probably be exercised, it will be much trickier to follow this path in the months thereafter, unless the downturn morphs into a deep recession."

German Gfk consumer sentiment improves to -18.4, driven by income expectations

Germany's Gfk Consumer Sentiment for August rose to -18.4, surpassing expectations of -21.1, and marking an improvement from July's -21.6.

In July, economic expectations jumped from 2.5 to 9.8, and income expectations surged from 8.2 to 19.7, reaching their highest level since October 2021. Willingness to buy also improved, rising from -13.0 to -8.4, while willingness to save slightly decreased from 8.2 to 8.0.

Rolf Buerkl, consumer expert at NIM, attributed this upswing primarily to Germans' increased income expectations. He also noted that the euphoria from the European Football Championship likely contributed to the positive sentiment.

However, Buerkl cautioned that it remains to be seen whether this effect is sustainable or just a "short-term flare-up." He warned that if this good mood fades quickly, the path out of low consumption could be "long and demanding."

Australia's PMI composite dips to 50.8, no major slowdown with continued inflation pressures

Australia's PMI Manufacturing saw a marginal improvement in July, rising slightly from 47.2 to 47.4. Conversely, PMI Services dropped to a six-month low, moving from 51.2 to 50.8. PMI Composite also decreased from 50.7 to 50.2, the lowest in six months.

Warren Hogan, Chief Economic Advisor at Judo Bank, highlighted that despite a further moderation in the composite output index, "there are no signs of a significant slowdown in Australian business activity in 2024." He noted that while manufacturing continues to struggle, services sector is still experiencing better activity compared to the end of 2023.

Hogan also mentioned that the impact of recent tax cuts and cost-of-living support measures has yet to fully manifest in the business conditions and should positively affect consumer spending in future months. Insights from the upcoming final PMIs for July and the reports for August are expected to provide a clearer picture of these effects.

Despite softer activity levels, inflation pressures have not eased significantly. The services sector saw a notable increase in input costs, which rose four points to 63.3—the highest since November 2023. In contrast, manufacturing input costs rose only slightly and are near their lowest in four years. The composite output price index nudged up to 54.1 in July, indicating a small increase but suggesting that inflation is likely stabilizing around an annualized rate of 4% as of mid-2024.

Japan's PMI services surges to 53.9 while manufacturing back in contraction

Japan's PMI Manufacturing declined from 50.0 to 49.2, underperforming against expectations of 50.5, indicating contraction. In contrast, PMI Services experienced a robust increase, rising sharply from 49.4 to 53.9, signaling a strong expansion and the highest activity level in three months. PMI Composite also rose from 49.7 to 52.6.

Usama Bhatti, Economist at S&P Global Market Intelligence, stating the reading was "indicative of solid growth," driven primarily by the services sector. Manufacturing saw a "renewed reduction in output," though the decline was marginal.

Additionally, the PMI report highlighted increasing operational challenges, with a "renewed increase in capacity pressures" across the private sector. For the first time in three months, there was a rise in the level of outstanding business, suggesting that firms are facing more backlog in their operations.

The report also underscored persistent cost pressures, particularly in manufacturing, where input prices rose sharply, marking the steepest increase since April 2023.

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 168.13; (P) 169.61; (R1) 170.38; More...

EUR/JPY's fall from 175.41 accelerates lower today and it's now pressing 38.2% retracement of 153.15 to 175.41 at 166.90. Some support could be seen from this fibonacci level, and break of 169.19 minor resistance will turn intraday bias neutral first. However, decisive break of 166.90 will pave the way to medium term channel support (now at 165.46).

In the bigger picture, medium term outlook will stay bullish as long as 164.29 resistance turned support holds. Long term up trend is still in favor to continue through 175.41 at a later stage. However, firm break of 164.29 will be a strong sign of bearish trend reversal.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:00 | AUD | Manufacturing PMI Jul P | 47.4 | 47.2 | ||

| 23:00 | AUD | Services PMI Jul P | 50.8 | 51.2 | ||

| 00:30 | JPY | Manufacturing PMI Jul P | 49.2 | 50.5 | 50 | |

| 00:30 | JPY | Services PMI Jul P | 53.9 | 49.4 | ||

| 06:00 | EUR | Germany GfK Consumer Confidence Aug | -18.4 | -21.1 | -21.8 | -21.6 |

| 07:15 | EUR | France Manufacturing PMI Jul P | 44.1 | 45.9 | 45.4 | |

| 07:15 | EUR | France Services PMI Jul P | 50.7 | 49.7 | 49.6 | |

| 07:30 | EUR | Germany Manufacturing PMI Jul P | 42.6 | 44.5 | 43.5 | |

| 07:30 | EUR | Germany Services PMI Jul P | 52 | 53.5 | 53.1 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jul P | 45.6 | 46.3 | 45.8 | |

| 08:00 | EUR | Eurozone Services PMI Jul P | 51.9 | 52.9 | 52.8 | |

| 08:30 | GBP | Manufacturing PMI Jul P | 51.8 | 51.1 | 50.9 | |

| 08:30 | GBP | Services PMI Jul P | 52.4 | 52.5 | 52.1 | |

| 12:30 | CAD | New Housing Price Index M/M Jun | -0.20% | 0.10% | 0.20% | |

| 12:30 | USD | Goods Trade Balance (USD) Jun P | -96.8B | -98.0B | -99.4B | -99.4B |

| 12:30 | USD | Wholesale Inventories Jun P | 0.20% | 0.50% | 0.60% | |

| 13:45 | CAD | BoC Interest Rate Decision | 4.50% | 4.75% | ||

| 13:45 | USD | Manufacturing PMI Jul P | 51.5 | 51.6 | ||

| 13:45 | USD | Services PMI Jul P | 54.5 | 55.3 | ||

| 14:00 | USD | New Home Sales M/M Jun | 643K | 619K | ||

| 14:30 | CAD | BoC Press Conference | ||||

| 14:30 | USD | Crude Oil Inventories | -2.6M | -4.9M |

US goods exports rises 5.7% yoy, imports rises 6.9% yoy

US goods exports rose 5.7% yoy to 172.32B in June. Goods imports rose 6.9% yoy to USD 269.16B. Trade balance reported USD -96.84B, versus expectation of USD -98.0B.

Wholesale inventories rose 0.2% mom to USD 903.3B. Retail inventories rose 0.7% mom to USD 802.1B.

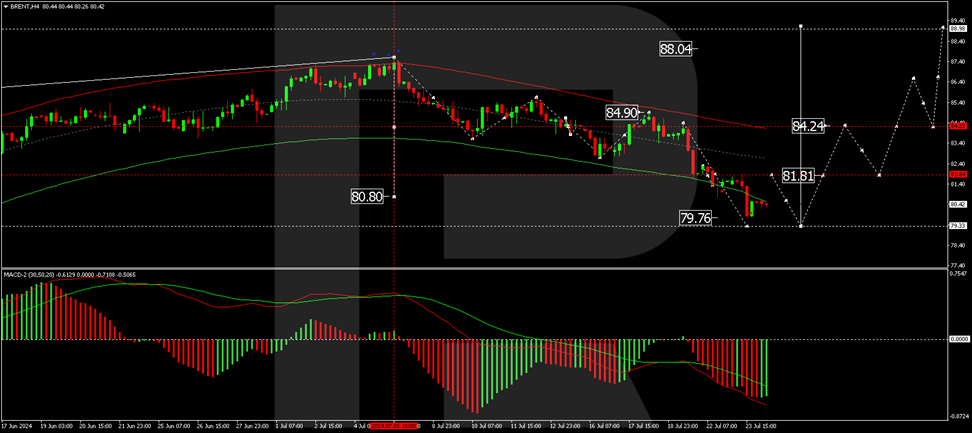

Brent Oil Prices Decline Amid Inventory Reductions and Middle East Optimism

Brent crude oil prices have continued their downward trajectory, reaching 81.14 USD per barrel as of Wednesday. This marks the fifth consecutive session of decline, primarily influenced by significant reductions in US oil inventories. The latest data from the API indicates a decrease of 3.9 million barrels, surpassing the forecasted reduction of 2.5 million barrels and marking the fourth consecutive week without a correction.

Concurrently, developments in the Middle East are also impacting oil prices. There is emerging optimism regarding ceasefire negotiations between Israel and Hamas, which has helped alleviate some geopolitical pressures on oil prices. Additionally, concerns about potential disruptions in oil supplies due to forest fires in Canada influence market dynamics, albeit helping to stabilise prices momentarily.

The strength of the US dollar continues to make commodities less attractive, as a stronger dollar typically reduces the purchasing power of other currencies in the commodities market.

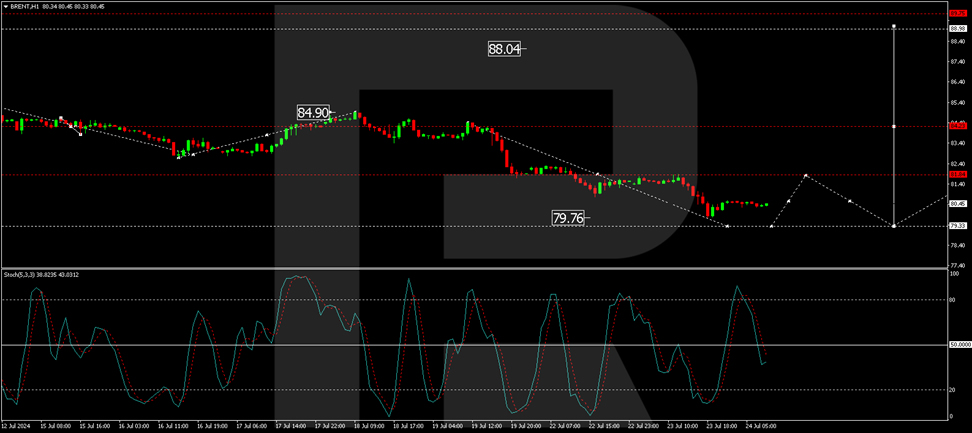

Technical analysis of Brent

Brent oil is forming a consolidation range around the 80.80 USD level with an extension down to 79.76 USD. A further decline to 79.33 USD may occur. If the price exits this range on the upside, we might see the initiation of a growth wave targeting 84.24 USD. The MACD indicator supports this scenario, showing potential for new growth as it prepares at the lows.

The market has established a consolidation range around the 81.84 USD level. The target level of 79.76 USD has been reached with a downward exit. We anticipate a new consolidation range forming at these lows, potentially followed by another decline to 79.33 USD. If the price exits the range upward, a rebound to 81.44 USD could occur. The Stochastic oscillator, currently below the 50 level and heading towards 20, supports this potential downward movement.

Investors and market analysts must closely monitor these developments, as any significant changes in US monetary policy or geopolitical events could further influence oil prices.

ETHUSD Trades Flat After ETF Debut

- ETHUSD has been rangebound in the past few sessions

- Spot ETF launch did not trigger much volatility

- Momentum indicators remain positively tilted

ETHUSD (Ethereum) has experienced a strong rally in July, breaking above its 50-day simple moving average (SMA). However, the leading altcoin has been trading sideways for more than a week now, even though the short-term oscillators have been hovering deep in their positive zones.

If the price extends its recent upleg, the recent resistance region of 3,560 could curb initial upside attempts. Higher, the April resistance of 3,710 could prove to be the next barricade for the bulls to overcome. A break above that zone could open the door for the May peak of 3,974.

Alternatively, should the recent range break to the downside, the price could challenge the June support of 3,360. Failing to halt there, Ethereum could descend towards the June low of 3,235, a region that also provided support back in March and April. Even lower, the March low of 3,055 could provide downside protection.

In brief, the much-anticipated spot Ether ETF debut in the US did not manage to put an end to ETHUSD’s choppy trading in the near term. Nevertheless, the short-term picture will remain bullish as long as the price holds above its 50-day SMA.

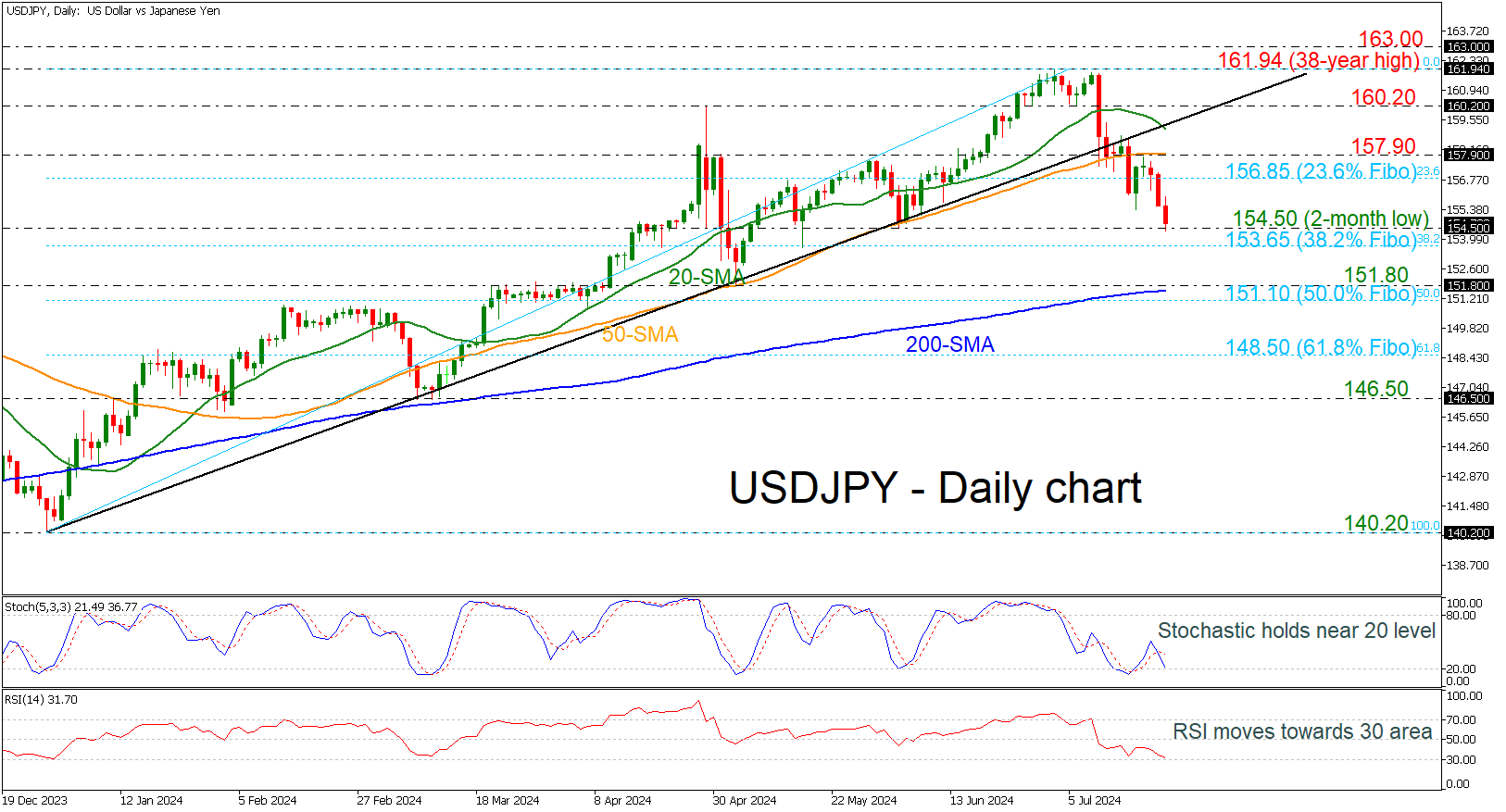

USDJPY Edges Lower Near 2-month Low

- USDJPY holds beneath diagonal line

- Stochastics and RSI suggest more bearish moves

USDJPY tumbled to a new two-month low of 154.50 following a significant pullback from the long-term ascending trend line and the 50-day simple moving average (SMA) near 157.90. The stochastic oscillator created a bearish crossover, diving to just above the oversold region, while the RSI is also pointing downwards near the 30 level.

Further losses may drive the pair towards the 38.2% Fibonacci retracement level of the up leg from 140.20 to 161.94 at 153.65, before challenging the 200-day SMA around the 151.80 support. Slightly lower, the 50.0% Fibonacci of 151.10 may act as a turning point for traders.

On the other hand, a potential rebound off 154.50 could take investors higher again, resting near the 23.6% Fibonacci of 156.85 ahead of the 50-day SMA at 157.90. A climb back above the ascending trend line could endorse the scenario for bullish actions again, hitting 160.20.

In brief, USDJPY has been in a bearish correction since the climb to a 38-year high on July 3, and any closing sessions beneath the 200-day SMA could switch the long-term outlook to negative.