Sample Category Title

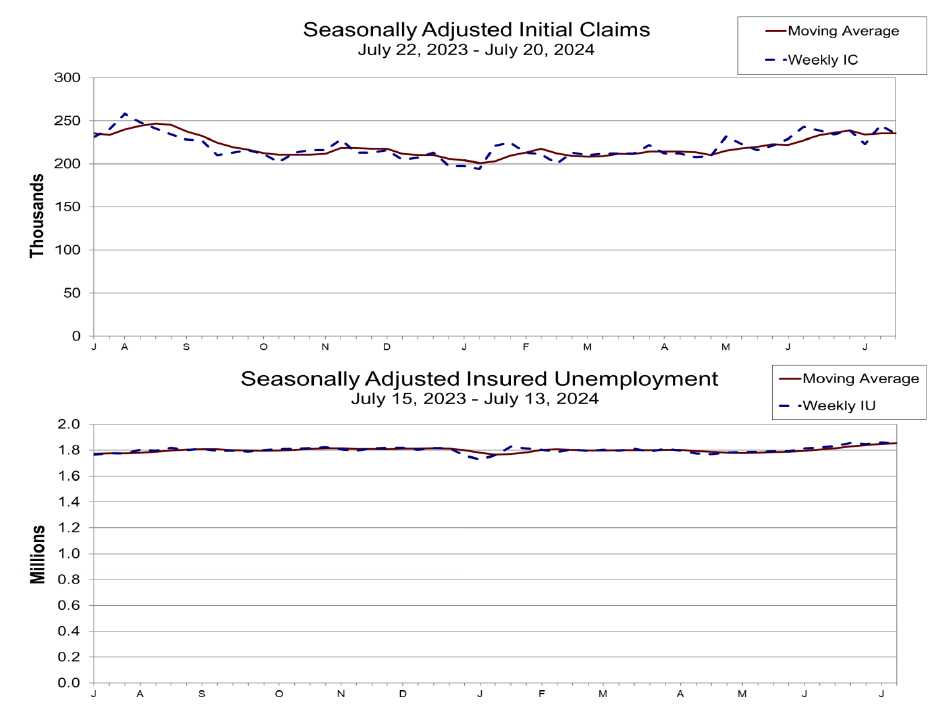

US initial jobless claims falls to 235k vs exp 238k

US initial jobless claims fell -10k to 235k in the week ending July 20, slightly below expectation of 238k. Four-week moving average of initial claims was relatively unchanged at 236k.

Continuing claims fell -9k to 1851k in the week ending July 13. Four-week moving average of continuing claims rose 5k to 1854k, highest since December 4, 2021.

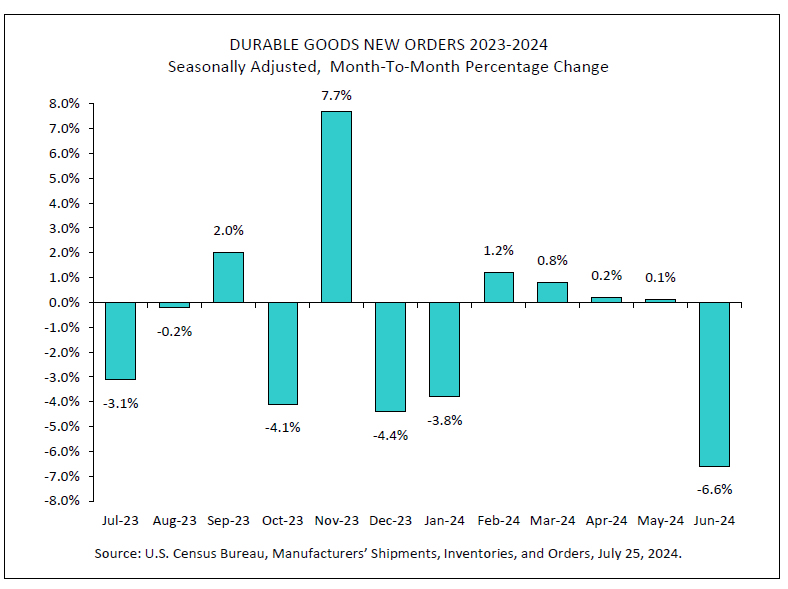

US durable goods orders falls -6.6% mom, but ex-transport orders up 0.4% mom

US durable goods orders fell sharply by -6.6% mom to USD 264.5 in June, much worse than expectation of 0.4% mom rise. However, ex-transportation orders rose 0.5% mom to USD 188.7B, above expectation of 0.2% mom. Ex-defense orders fell -7.0% mom to USD 247.6B. Transportation equipment drove the headline contraction and fell -20.5% mom to USD 75.8B.

US Q2 GDP grows 2.8% annualized, inflation pressures ease

The advance estimate of US GDP growth in Q2 2024 showed a robust 2.8% annualized increase, significantly exceeding the anticipated 2.0% and doubling Q1's pace of 1.4%.

This stronger-than-expected growth was driven by rises in consumer spending, private inventory investment, and nonresidential fixed investment. Notably, imports also increased, which are subtracted in the GDP calculation.

On the inflation front, GDP price index slowed from 3.1% to 2.3%, falling below the expected 2.6%. PCE price index also eased from 3.4% to 2.6%, and core PCE price index saw a notable decrease from 3.7% to 2.9%.

The sharp uptick in GDP growth, coupled with cooling inflation metrics, presents an optimistic economic outlook. Deceleration in price indexes suggests easing inflationary pressures, which would support rate cut by Fed in the coming months.

SPX 500: Further Weakness May Trigger Medium-Term Global Risk-off Event

- Market participants have started to question the earlier high earnings growth prospects placed on the “Magnificent 7” stocks.

- The past month of record low implied correlation among S&P 500 component stocks can increase the odds of a more pronounced spike in the VIX.

- The S&P 500 is at risk of shaping a medium-term (multi-week) corrective decline phase which may trigger a global risk-off scenario.

The mega-capitalization stocks have led yesterday’s rout in the US stock market where the Magnificent 7 cohort (Apple, Amazon, Microsoft, Nvidia, Tesla, Alphabet, and Meta) shed close to -US$760 billion loss in their combined market capitalization in a single day on Wednesday, 26 July 2024.

The Nasdaq 100 has the highest weightage of the “Magnificent 7” group of stocks among the major benchmark US stock indices, bled the most with a daily loss of -3.65%, its worst daily performance since 7 October 2022. This set of horrendous performance came after the bearish breakdown below its 19,520 key short-term pivotal support as highlighted in our previous report reinforced by a disappointment in the Q2 earnings results of Tesla and Alphabet.

The weakness inherent in the higher beta Nasdaq 100 has triggered a negative feedback loop into the broader S&P 500 that shed 2.32 %; its worst daily performance since 15 December 2022 after it notched 38 record closing highs this year and ended its best streak without a 2% decline since the Great Financial Crisis of 2007.

The current month-to-date outperformers as of 24 July, the Dow Jones Industrial Average (+1.88%), and Russell 2000 (+7.21%) that have benefitted from the bull steepening of the US Treasury yield curve (10-year minus 2-year) were not spared from yesterday’s mega-cap onslaught as both of them recorded daily losses of 1.25% and 2.13% respectively.

Implied low correlation and volatility may trigger further sell-off

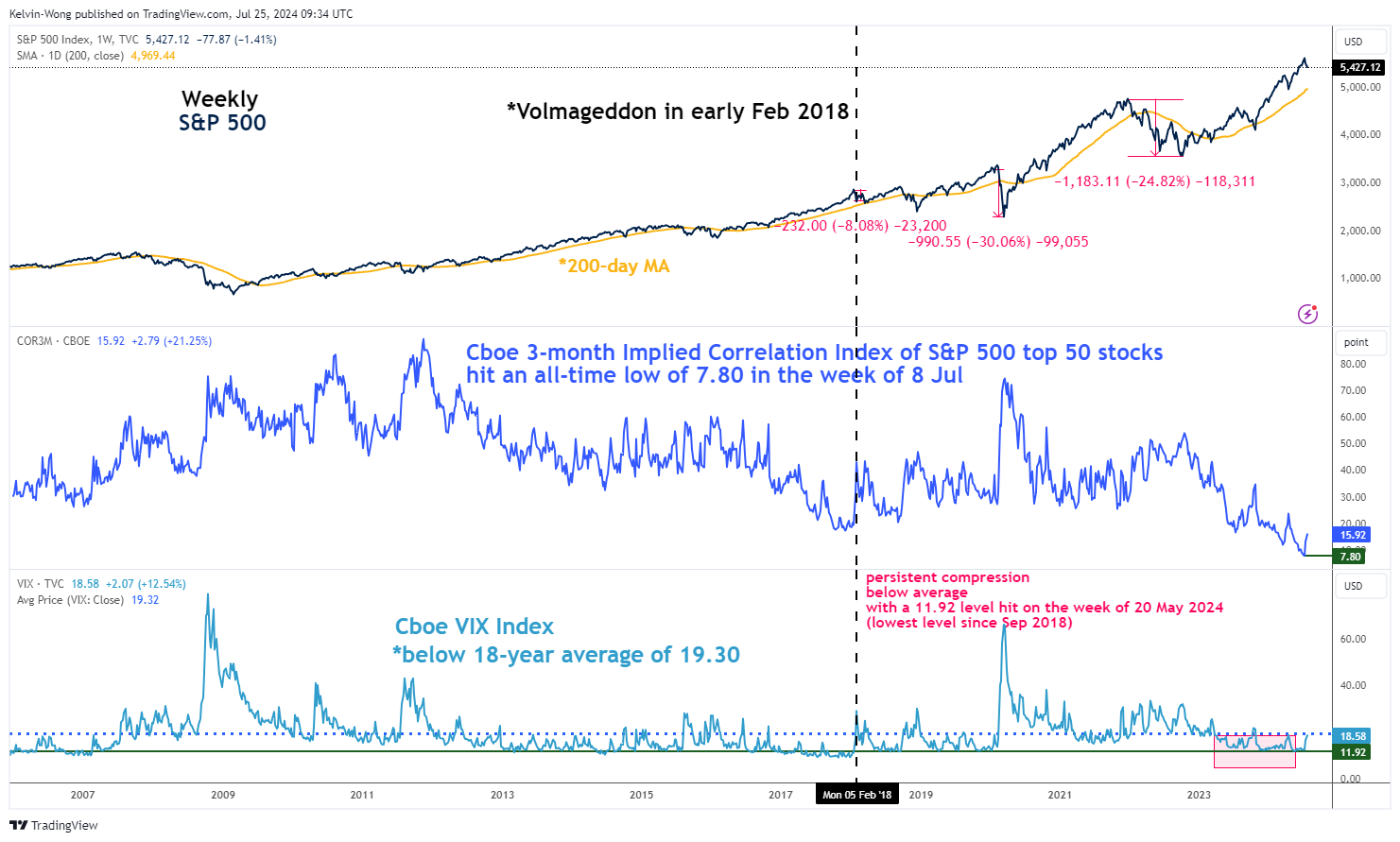

Fig 1: Cboe VIX & 3-month implied correlation index of S&P 500 constituents as of 24 Jul 2024 (Source: TradingView, click to enlarge chart)

Another interesting point to note is the recent plunge in the VIX (implied volatility of the S&P) to almost a six-year low of 11.92 on the week of 20 May 2024 which in turn has coincided with market participants’ perceptions of future low correlation readings (higher dispersion of returns on the average) among the US S&P 500 index constituents.

The Cboe 3-month Implied Correlation Index measures the 3-month expected correlation across the top 50 market capitalization-weighted S&P 500 constituents which have slipped to an all-time low reading of 7.80 on the week of 8 July 2024 as artificial intelligence optimism has led to outsized gains in the “Magnificent 7” excluding Tesla since the start of this year versus meagre gains seen from the other 494 component stocks of the S&P 500.

The persistent trend of lower “lows” seen in the Cboe 3-month Implied Correlation Index in the past three months has helped to depress the VIX which in turn created an artificial calm in the overall stock market that led to a higher degree of “complacent risk-on or seeking behaviour”. The VIX hit a level of 11.92 on the week of 20 May 2024; its lowest level since September 2018 and continued to remain compressed below its 18-year average of 19.30 till the first two weeks of July 2024 (see Fig 1).

Hence, if the earnings results and or outlook disappoint in next week’s earnings reports for other Magnificent 7 stocks (Amazon, Apple, Microsoft, and Meta), the VIX may see a further spike which is likely to trigger a medium-term corrective decline sequence in S&P 500 and triggered a negative feedback loop into other global stock indices.

S&P 500 at risk of breaking below its 50-day moving average

Fig 2: US SPX 500 medium-term & major trends as of 25 Jul 2024 (Source: TradingView, click to enlarge chart)

Based on the current price actions of the US SPX 500 CFD Index (a proxy of the S&P 500 E-mini futures), it is now looking vulnerable for a breakdown below its 50-day moving average and the lower boundary of its medium-term ascending channel from 27 October 2023 low.

In addition, the medium-term momentum condition has turned bearish as depicted by the latest reading on the daily RSI momentum indicator as it broke below the 50 level on Wednesday, 24 July, and has not reached its oversold region yet.

These observations suggest that the medium-term uptrend phase in place since the 27 October 2023 low has been damaged. A break below the intermediate support at 5,327 may reinforce a medium-term (multi-week) corrective decline phase to expose the next supports at 5,150 and 5,010 (also the 200-day moving average) in the first step (see Fig 2).

On the other hand, a clearance above 5,680 key medium-term pivotal resistance reinstates the bullish impulsive upmove sequence to see the next medium-term resistance coming in at 5,830/920.

GBP/USD Dips to 1.2850 Amid Growing BoE Rate Cut Speculation

- GBP/USD is declining due to speculation of a BoE rate cut and concerns about global growth.

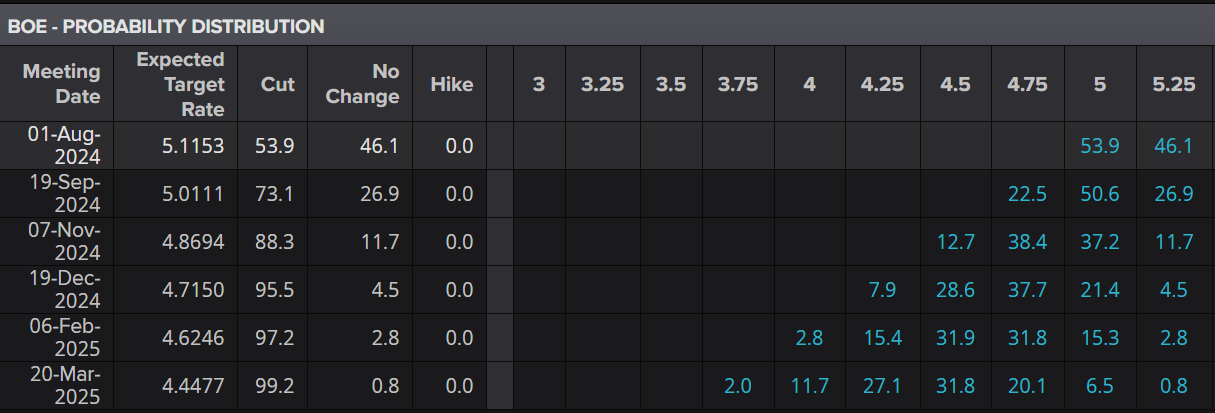

- Market participants are pricing in a 53% chance of rate cuts in August, but economists polled predict an 80% chance of a cut.

- Technically, GBP/USD has support at 1.2850 and resistance at 1.2950.

Cable has continued to edge toward support at the 1.2850 handle as high impact US data lies in wait. Market participants meanwhile have upped the probability of a rate cut by the Bank of England at next week’s meeting to 53%, and pricing in around 52bps of cuts in 2024. A Reuters poll conducted from July 18-24 revealed that over 80% of economists expect the Bank of England (BoE) to lower its key borrowing rates by 25 basis points (bps) to 5% in the August meeting. However, June’s poll indicated a higher expectation, with 97% of respondents anticipating a rate cut. In contrast, market participants are currently pricing in only a 53% chance of rate cuts in August.

BoE Rate Cut Probabilities

Source: LSEG

It appears that the pivot which drove US stocks lower toward the back end of last week may be affecting markets as a whole. We are seeing shifting sentiments and positioning by market participants as rate cut bets ramp up while concerns around global growth in H2 2024 continue to grow as well.

The UK business optimism index which is published by the Confederation of British Industry in its Industrial Trends Survey, is an average of 400 small, medium, and large manufacturing companies are surveyed each quarter. The index dropped significantly in Q3 to -9 compared to the print in Q2 which was a positive 9.

This is surprising given the optimism around rate cuts, but it could also be attributed to growing concerns about slower global growth in Q3 and Q4, alongside expectations of a rise in UK inflation during the same period.

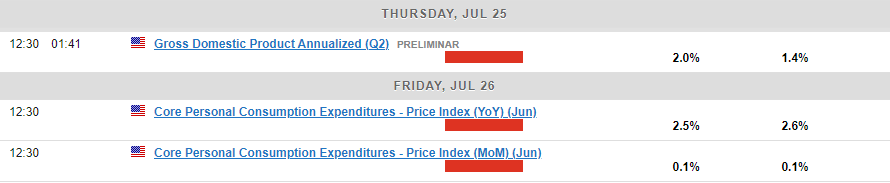

US Data Ahead

US GDP data expected later today may trigger some volatility in GBP/USD, with an anticipated print of 2%. However, I predict a 2.3-2.5% print, which should reassure Federal Reserve officials about the economy’s health. The impact on the US dollar could be two-fold, depending on market perception. A positive GDP reading could confirm economic strength and support expectations for rate cuts starting in September, potentially weakening the USD.

Conversely, a lower-than-expected GDP could heighten recession fears and reduce rate cut expectations, leading to short-term US dollar appreciation. Given recent market sensitivity to data, how this information is perceived will likely be crucial.

Technical Analysis

From a technical standpoint, GBP/USD has been steadily declining since peaking just above the psychological 1.3000 level.

Immediate support is at 1.2850, and a break below this may lead to a third test of the ascending trendline. On the Daily timeframe, price action and structure remain bullish, but a daily candle close below 1.26200 is needed to shift the overall trend.

For this to materialize, however, the pair must first navigate the 100 and 200-day moving averages, which are positioned at 1.2680 and 1.2622, respectively.

Alternatively, an upward move will encounter resistance at 1.2950 before the psychological 1.3000 level becomes significant again.

GBP/USD Chart, July 25, 2024

Source: TradingView (click to enlarge)

Support

- 1.2850

- 1.2680

- 1.2620

Resistance

- 1.2950

- 1.3000

- 1.3040

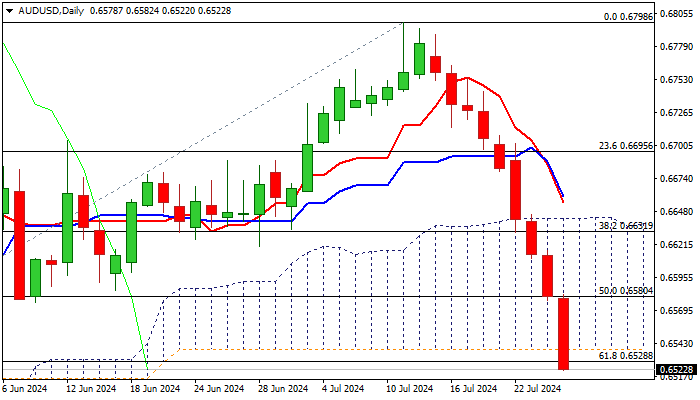

AUD/USD Outlook: Steep Downtrend Breaks Below the Base of Thick Daily Cloud

Steep fall extends into the ninth consecutive day and accelerated on Thursday (down 0.85% in Asian / European session), hitting the lowest levels since early May and being on track for the biggest weekly loss since mid-June 2023.

Break of 0.6580 pivot (200DMA/ 50% retracement of 0.6362/0.6798) accelerated existing downtrend through next key supports at 0.6538/28 (base of thick daily cloud / Fibo 61.8%) which generated another strong bearish signal, exposing targets at 0.6500 (psychological) and 0.6465 (Fibo 76.4%).

Bears are expected to firmly hold grip in persisting favorable conditions for Aussie dollar, though partial profit-taking should be anticipated in coming sessions as daily studies are strongly oversold.

Daily cloud base reverted to solid barrier (0.6538) which should ideally cap, while extended upticks should stall under 0.6580 to keep larger bears in play.

Res: 0.6528; 0.6538; 0.6580; 0.6605.

Sup: 0.6500; 0.6465; 0.6389; 0.6362.

Analysis of USD/JPY: Yen Strengthens by 5.5% Against US Dollar in 2 Weeks

On Thursday, 11 July, the USD/JPY exchange rate was above 161, and today it is below 153.

According to Reuters, this could be attributed to effective intervention by the Bank of Japan.

While intervention was anticipated when the yen weakened to extreme levels not seen since 1983, Tokyo authorities were cryptic in their comments, maintaining uncertainty, making it harder for investors to predict when and how they might intervene.

As indicated by today's USD/JPY chart:

→ The ascending trend channel (shown in black) that has been in place since 2023 is losing its relevance.

→ Red circles indicate pivotal points where significant price action occurred, helping to define the contours for a descending channel (shown in red).

→ The USD/JPY rate is near the lower boundary of the red channel. According to technical analysis, this boundary tends to act as support for the price – a bullish argument suggesting that the decline might slow down here.

Whether there will be a rebound from the lower line of the descending channel or the bears will manage to break through the 152 level (where the price found support in May) will largely depend on next week’s news: Tuesday will bring reports on inflation and unemployment in Japan, and Wednesday will see statements from the Bank of Japan regarding the interest rate.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

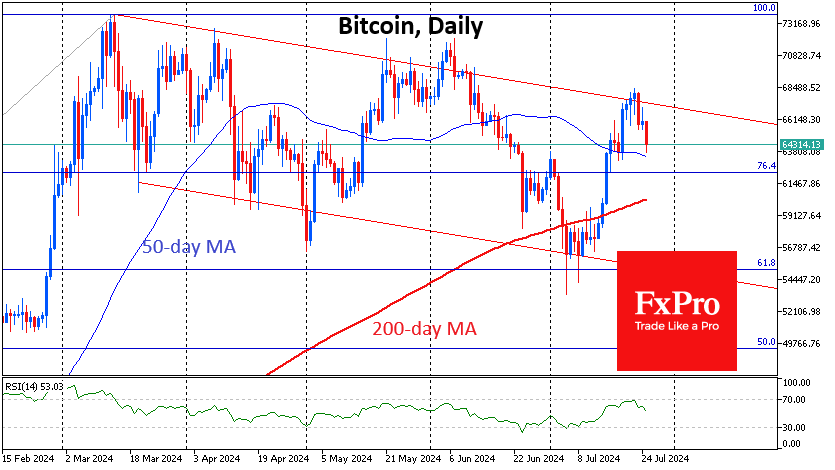

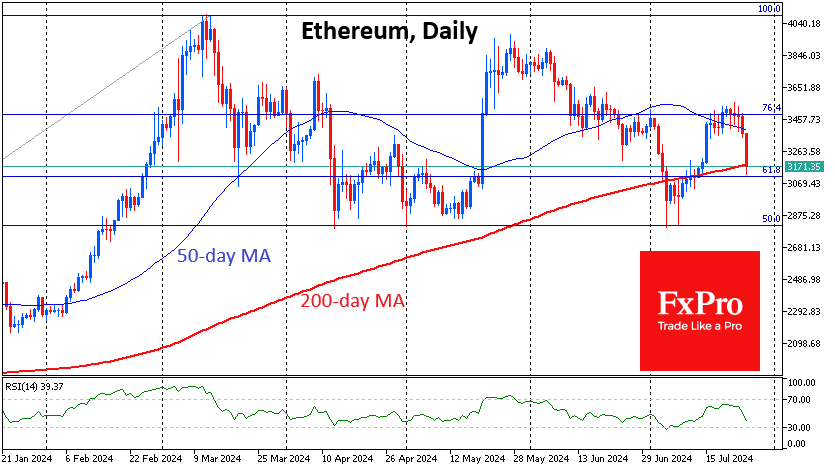

Stock Routs Undermine the Image of Ethereum ETF Launch

Market picture

The pressure on financial markets has spread to cryptocurrencies – the flip side of the long-desired easing of institutional access to the crypto market. The launch of the Ethereum ETF coincided with the most powerful drop in the Nasdaq index in months. The cryptocurrency market lost 3.5% in the last 24 hours, pulling back at one point to $2.3 trillion, its lowest in 10 days.

Bitcoin is down to $64.0K, once again approaching the 50-day MA where it consolidated for most of last week. There are small hopes that the first cryptocurrency will gain support near this level. However, this week could be just the beginning of a decline from the upper boundary of the BTCUSD downtrend channel. In this case, an important test of strength will be in the $60K area, where the 200-day MA and the significant milestone are held.

Ethereum is already testing the 200-day MA, having lost over 9% in less than 24 hours to 3150. In early July, the major altcoin steadily gained support after touching this curve. However, these purchases could be largely credited to the expectations of the ETF launch. Now, this speculative factor is out of play, multiplying sell-the-fact activity on top of global markets risk-off.

News background

News background

Spot Ethereum-ETF trading volume on the first day after listing totalled $1.08bn – that’s 23% of the bitcoin-ETF’s first day, with net inflows estimated by SoSoValue at $106.7m.

Creditors of bankrupt exchange Mt.Gox have started receiving Bitcoin and Bitcoin Cash transfers to accounts in Kraken. According to Arkham Intelligence, the exchange’s address no longer has assets.

The Hash Ribbons indicator gives a signal to buy Bitcoin. On 23 July, the indicator came out of “capitulation” for the first time in almost two months. Whenever this happens, an “explosive price rise” follows, noted analyst Mikybull.

Bitcoin investors can become EU citizens by investing €500,000 in the cryptocurrency through Portugal’s “golden visa” programme.

Italian car manufacturer Ferrari will start accepting cryptocurrencies as a payment method in Europe at the end of July. The decision follows the initiative’s successful launch in the US territory in the autumn of 2023.

According to a Europol report, bitcoin remains the most popular crypto asset among criminals despite the efforts of international law enforcement agencies and governments. The hype surrounding the Ordinals project and the launch of the bitcoin-ETF could trigger a new wave of cyber threats.

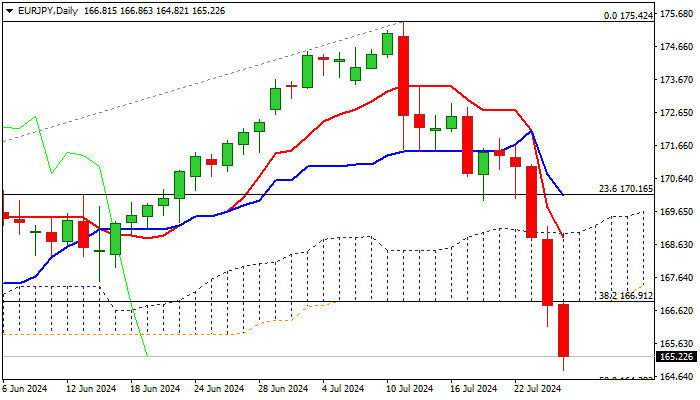

EUR/JPY Outlook: Falls to New Multi-Week Low After Break of Key Support

EURJPY extends steep fall into fifth straight day and hit 11-week low in early Thursday (down 1% in Asian session).

Recent interventions by Japan’s authorities boosted yen across the board and fresh strength gained strong momentum, suggesting that the currency could rise further.

Wednesday’s close below pivotal support at 166.91 (daily cloud base / Fibo 38.2% of 153.14/175.42 rally) generated strong bearish signal, which showed immediate result in fresh acceleration lower on Thursday.

Bears eye targets at 164.28 (50% retracement) and 163.91 (200 DMA) violation of which to unmask 161.65 (61.8% retracement) and psychological 160 in extension.

Meanwhile, bears may take a breather for consolidation, as daily studies are strongly oversold.

Upticks should be capped under broken pivot at 166.91, now acting as solid resistance, to keep bears in play and mark positioning for fresh push lower.

Markets shift focus towards next week’s BoJ monetary policy meeting (Wednesday) especially on the latest talks encouraging further rate hikes, which would provide fresh support to rising yen.

Res: 166.91; 167.78; 168.87; 169.01.

Sup: 164.28; 163.91; 163.01; 161.65.

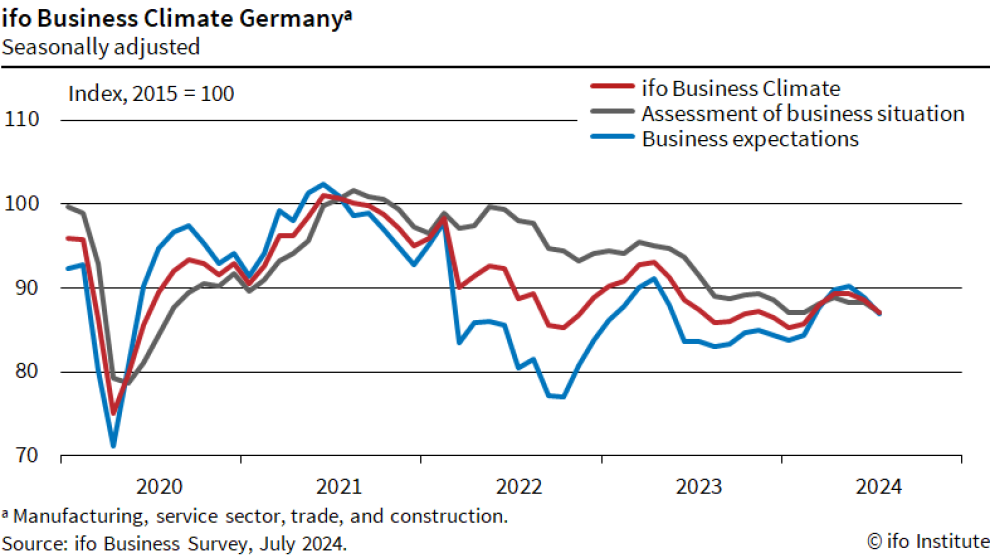

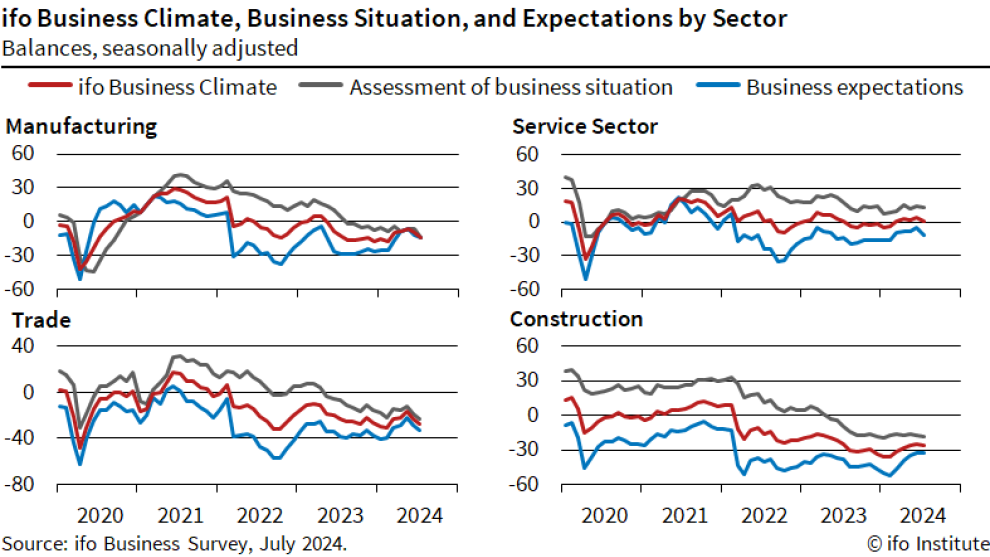

German Ifo falls to 87, economy stuck in crisis

Germany's Ifo Business Climate Index fell from 88.6 to 87.0 in July, missing expectations of 89.0. Current Assessment Index also dropped from 88.3 to 87.1, below the anticipated 88.5. Additionally, Expectations Index declined from 88.8 to 86.9, underperforming the forecast of 89.0.

Sector-wise, manufacturing index plunged from -9.3 to -14.1, indicating significant dissatisfaction among manufacturers. Services sector saw a decline from 4.2 to 0.7, while the trade sector fell from -23.6 to -27.8. Construction also showed a decrease, moving from -25.2 to -26.0.

Ifo noted that sentiment has "declined considerably," with companies expressing growing dissatisfaction with the current business situation. The level of skepticism regarding the coming months has increased notably. The German economy, as described by Ifo, is currently "stuck in crisis."