Sample Category Title

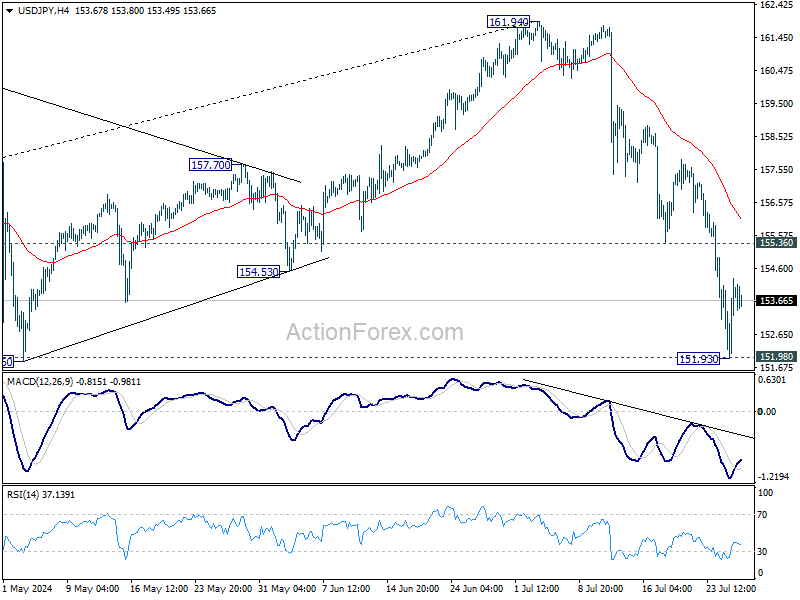

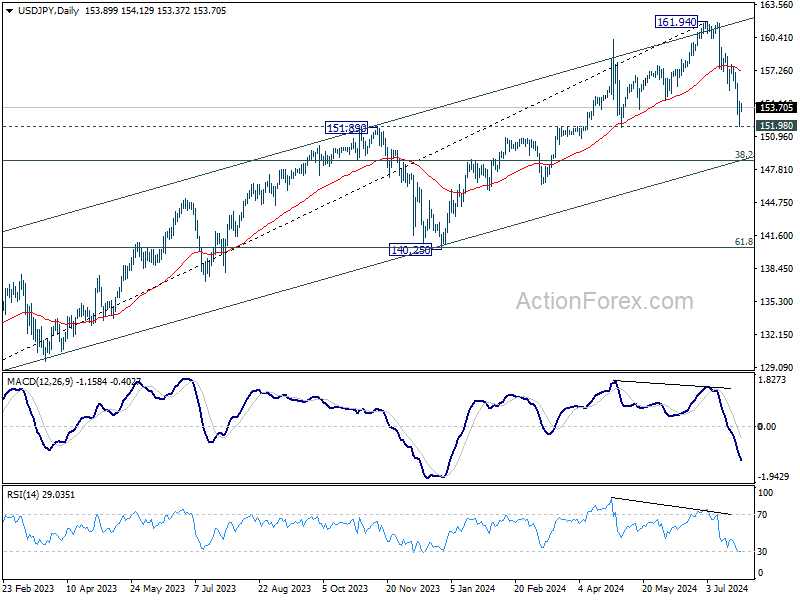

USD/JPY Daily Outlook

Daily Pivots: (S1) 152.48; (P) 153.40; (R1) 154.86; More...

Intraday bias in USD/JPY stays neutral for consolidations above 151.93 temporary low. Risk will stay on the downside as long as 155.36 support turned resistance holds. Decisive break of 151.89 resistance turned support will argue that large scale correction is underway to 148.66 fibonacci level. Nevertheless, break of 155.36 will turn bias back to the upside for stronger rebound.

In the bigger picture, considering the depth and momentum of the current decline, 161.94 should be a medium term top already. Fall from there is seen as correcting the whole rise from 127.20 (2023 low) at least. Break of 151.89 will pave the way to 38.2% retracement of 127.20 to 161.94 at 148.66. Risk will now stay on the downside as long as 55 D EMA (now at 157.25) holds, in case of rebound.

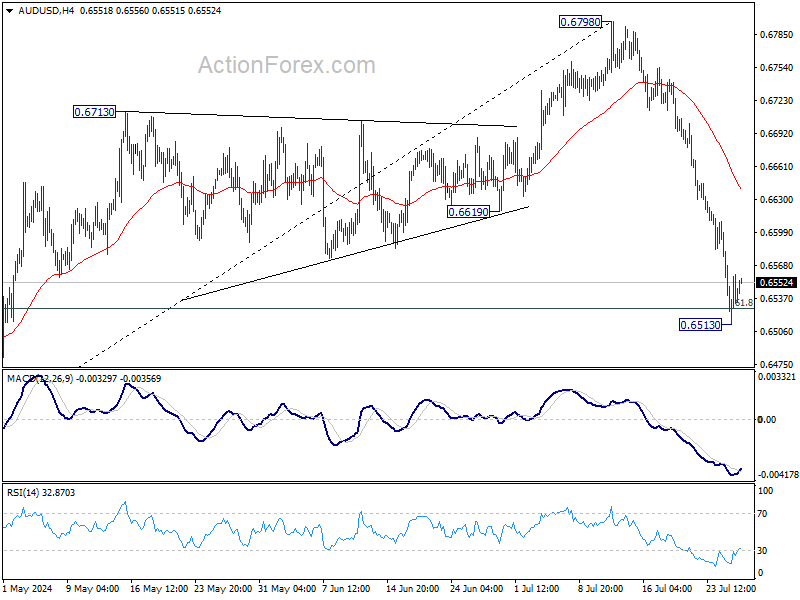

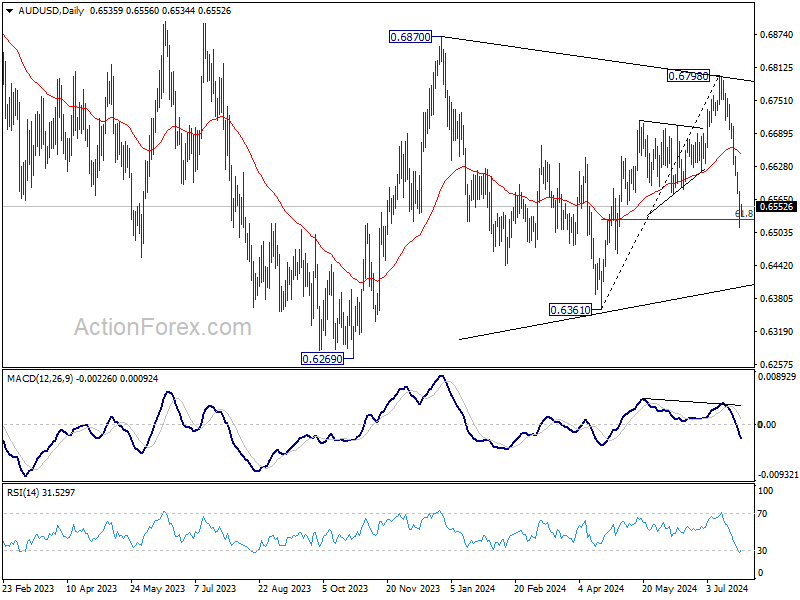

AUD/USD Daily Report

Daily Pivots: (S1) 0.6507; (P) 0.6545; (R1) 0.6576; More...

A temporary low should be in place at 0.6513 with current recovery. Intraday bias is turned neutral for consolidations. Further decline is expected as long as 55 4H EMA (now at 0.6639) holds. Sustained break of 61.8% retracement of 0.6361 to 0.6798 at 0.6528 will pave the way back to 1.6361 support next.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, with fall from 0.6798 as another falling leg. Deeper fall could be seen to the lower side of the range between 0.6169/6361. But strong support should be seen there to contain downside. For now, risk will stay on the downside as long as 0.6798 resistance holds, in case of rebound.

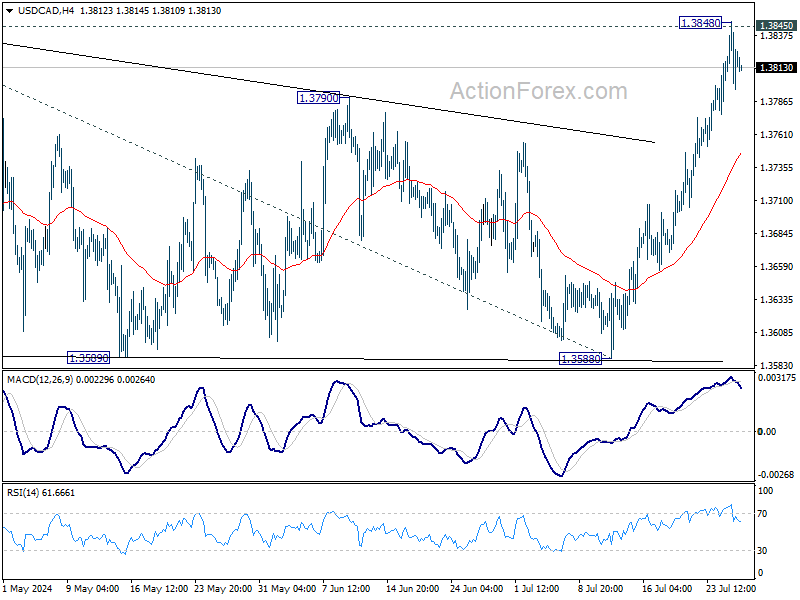

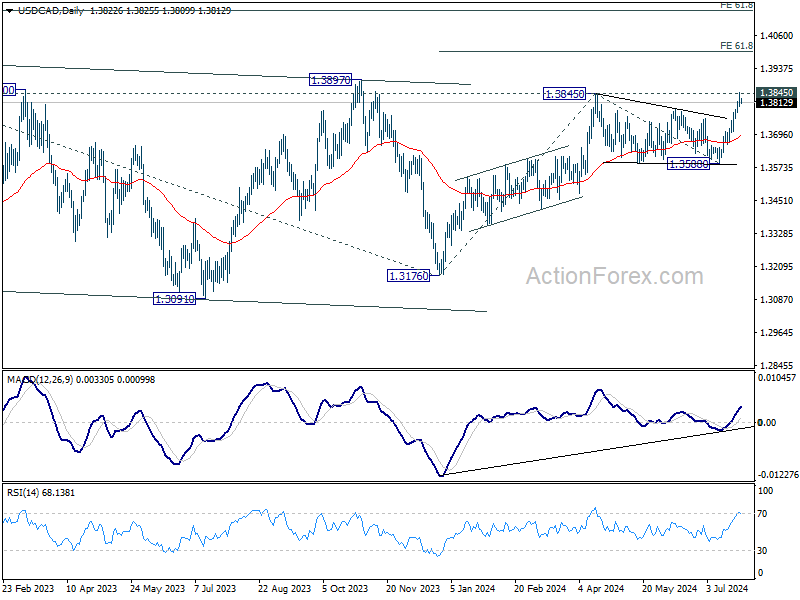

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3798; (P) 1.3824; (R1) 1.3850; More...

A temporary top should be in place at 1.3848 with current retreat. Intraday bias in USD/CAD is turned neutral for consolidations. Downside of retreat should be contained by 55 4H EMA (now at 1.3745) to bring another rally. On the upside, decisive break of 1.3845 high will resume whole rally from 1.3176. Next target is 61.8% projection of 1.3176 to 1.3845 from 1.3588 at 1.4025.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern, that might have completed at 1.3176 (2023 low) already. Firm break of 1.3976 will confirm resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149. This will be the favored case as long as 1.3588 support holds, in case of pullback.

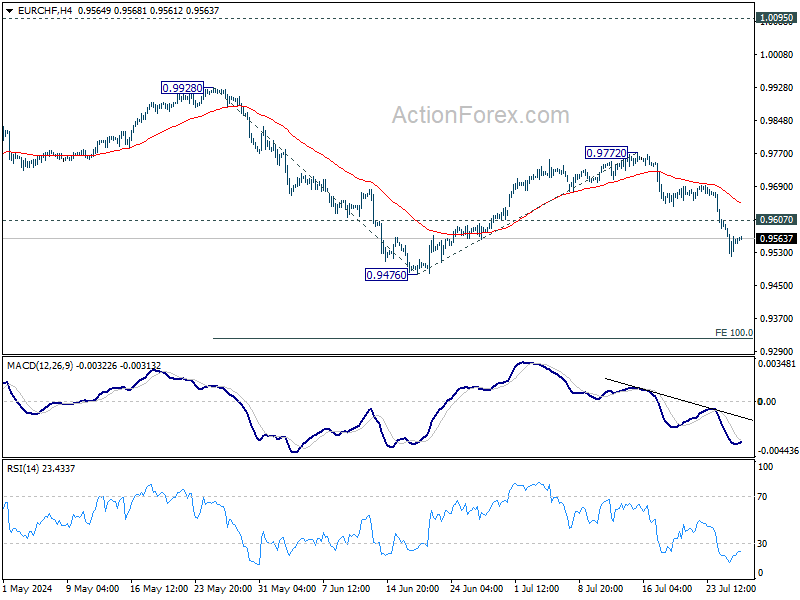

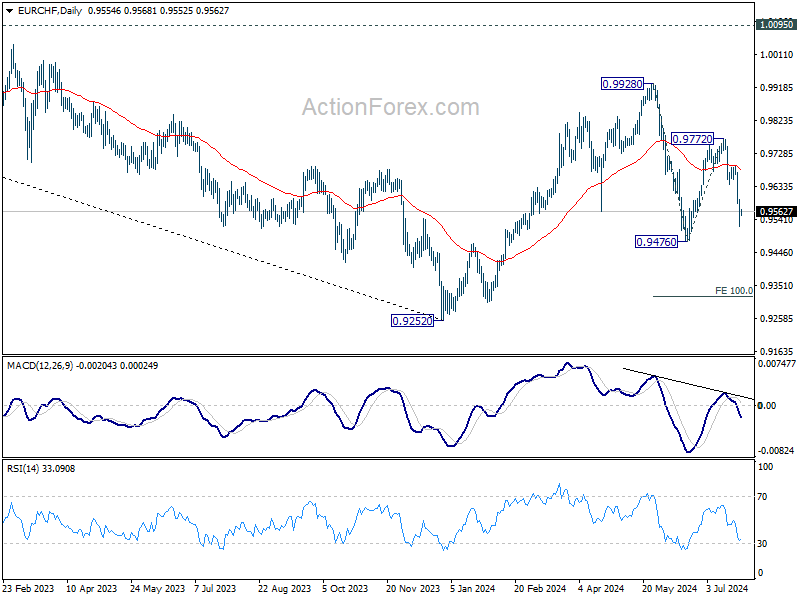

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9516; (P) 0.9566; (R1) 0.9612; More....

Intraday bias in EUR/CHF remains on the downside for retesting 0.9476 low. Firm break there will resume whole fall from 0.9928 to 100% projection of 0.9928 to 0.94767 from 0.9772 at 0.9320. On the upside, above 0.9607 minor resistance will turn intraday bias neutral first.

In the bigger picture, with 1.0095 key medium term resistance intact, price actions from 0.9252 (2023 low) are seen as a corrective pattern. Fall from 0.9928 might be the second leg and break of 0.9476 would bring deeper fall to retest 0.9252 low. But strong support should be seen there to extend the corrective pattern with another rising leg. In case, medium term outlook will be neutral at best as long as 1.0095 structural resistance holds.

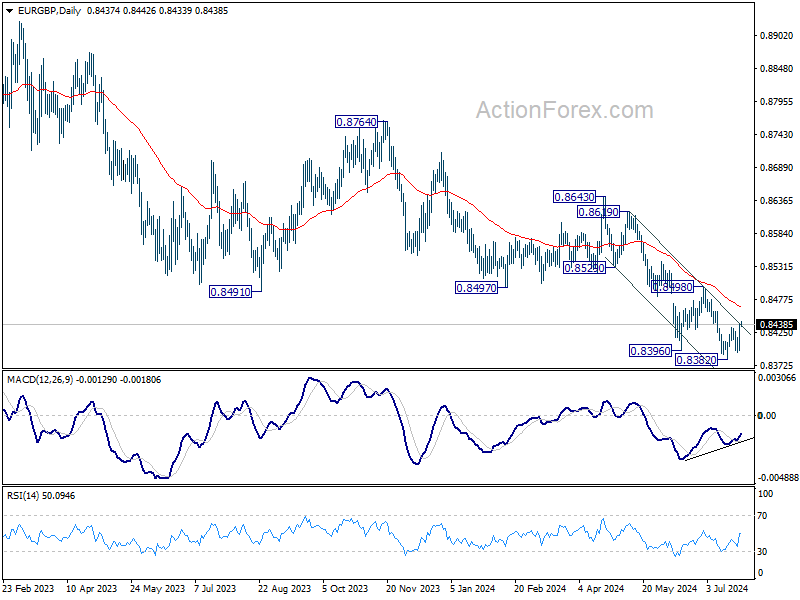

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8411; (P) 0.8425; (R1) 0.8455; More....

Intraday bias in EUR/GBP remains neutral for the moment and outlook stays bearish as long as 0.8498 resistance holds. Larger down trend should resume through 0.8382 at a later stage.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 key support (2022 low). For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

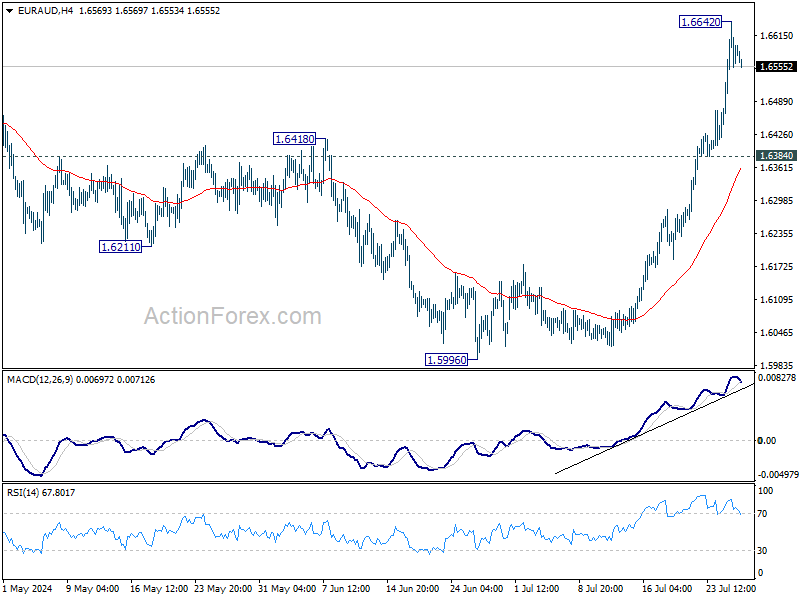

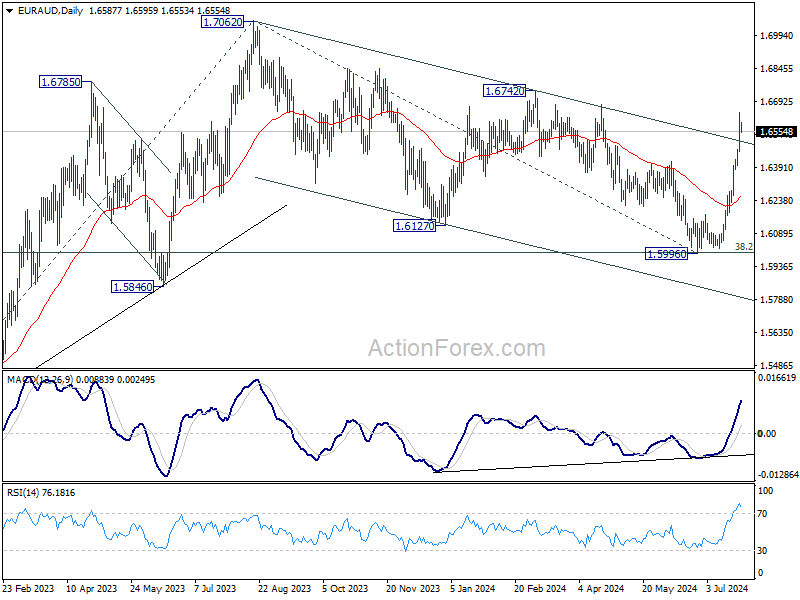

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6477; (P) 1.6560; (R1) 1.6672; More...

A temporary top should be in place at 1.6642 with current retreat. Intraday bias in EUR/AUD is turned neutral for consolidations. Outlook will stay bullish as long as 1.6384 support holds. Above 1.6642 will resume the rise from 1.5996 to retest 1.6742 resistance. Decisive break there will argue that larger up trend is ready to resume and target 1.7062 high next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) and could have completed after hitting 38.2% retracement of 1.4281 to 1.7062 at 1.6000. On resumption next target will be 61.8% projection of 1.4281 to 1.7062 from 1.5996 at 1.7715. This will now remain the favored case as long as 55 D EMA (now at 1.6263) holds.

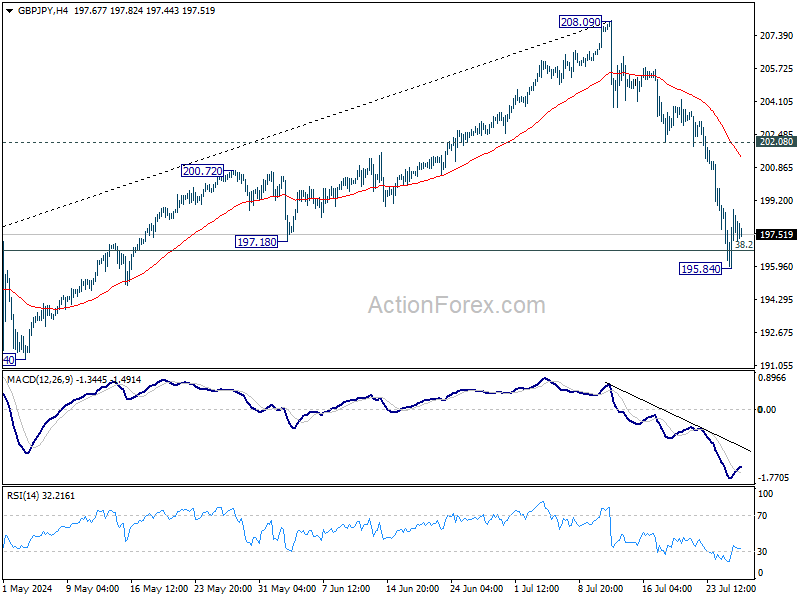

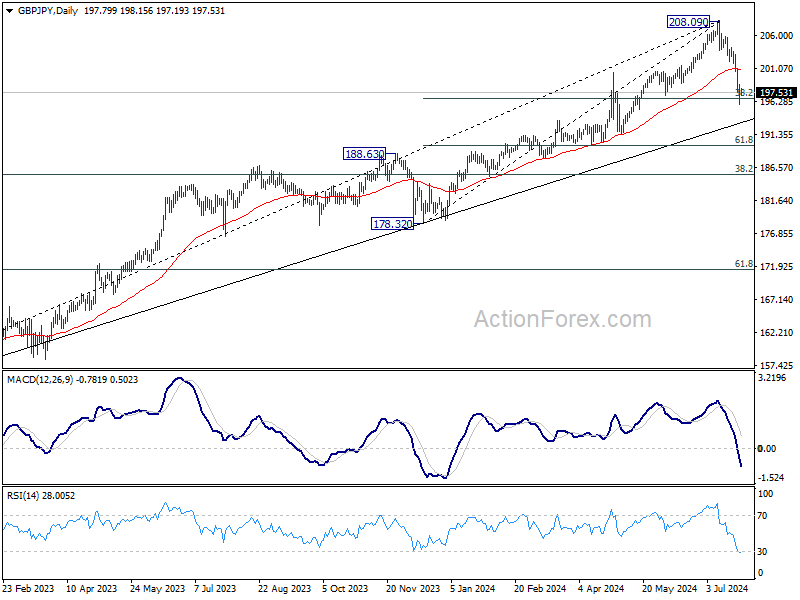

GBP/JPY Daily Outlook

Daily Pivots: (S1) 196.14; (P) 197.55; (R1) 199.22; More...

A temporary low should be formed at 195.84 and intraday bias in GBP/JPY is turned neutral for consolidations. Risk will stay on the downside as long as 202.08 support turned resistance holds. Sustained trading below 38.2% retracement of 178.32 to 208.09 at 196.71 will argue that larger scale correction is under way to 185.49 fibonacci level.

In the bigger picture, considering bearish divergence condition in W MACD, 208.09 might be a medium term top and fall from there could already be correcting whole up trend from 148.93 (2022 low). Risk will now stay on the downside as long as 55 D EMA (now at 201.00). Sustained break of 196.71 will pave the way to 38.2% retracement of 148.93 to 208.09 at 185.49.

Rotation Continues, But Europe Doesn’t Benefit

We went from ‘the Federal Reserve (Fed) could hardly cut in September’ to ‘it would be a mistake not to cut in July or September’ (source: Mohammad El Erian’s Linkedin feed) in a blink of an eye. Everything seems upside down since last week. The Big Tech stocks that have been rallying relentlessly since the beginning of 2023 are hit hard by rapid outflows as worries regarding the AI spending and the realization that it may take time to see the benefits of this massive spending push investors to take a part of their profits and walk away.

Walk away where?! Walk away toward the treasuries and government bonds with the expectation that the Fed and other central banks will either start or continue cutting their rates, and walk away toward the smaller and cyclical pockets of the equity markets. In this context, we’ve been seeing the lower S&P500 and Nasdaq countered by a rise in economically sensitive sectors since about two weeks now. And diving into the S&P500, around 300 of the stocks in there actually gained yesterday, US crude rebounded after testing the $77pb support and the Rusell 2000 stocks rallied 1.26% – reinforcing the rotation trend – from tech to non-tech - after the latest growth update showed that the US economy not only secured a 2% growth but grew at an impressive pace of 2.8% last quarter – double the first quarter number which had seen the growth rate fall to 1.4%. Consumer spending grew 2.3% and helped keeping the US economy on a strong path – although the savings are melting and credit card debt is rising to levels not seen in a decade. Core PCE prices eased from 3.7% to 2.9% during the quarter. And although the easing in prices was not as much as analysts expected, the Fed rate cut expectations didn’t really got hurt by the strong numbers as again, it’s now thought by some big names that not cutting rates in one of the two next meetings would be a policy mistake for the Fed. I personally think that cutting rates next week would be a mistake too, given the still-strong inflation and unbelievable growth numbers. Presently, activity on Fed funds futures don’t show a meaningful bet for a July cut; the probability of a cut next week is given less than 7%.

We have one more important data to go before next week’s decision: the core PCE index, the Fed’s favourite gauge of inflation. That number is expected to show a slight slowdown from 2.6% to 2.5%, although we may see a certain quickening in the monthly figure. But all in all, if not catastrophic, the Fed will probably hint that a rate cut is coming in fall, when they meet next week. The US 2-year yield shortly fell to 4.34% despite the strong GDP read, the 10-year yield sit on 4.25% and the US dollar index hovered around the 200-DMA as the economic picture wasn’t as sunny as in the US elsewhere. On the contrary, weak French and Germany business surveys came to complete the cloudy picture painted by PMI surveys printed earlier in the week. And the earnings from European companies are less than enchanting, preventing the European stocks from benefiting from the sector rotation in the US. Kering- which is the house of luxury brands including Gucci and Balenciaga – dropped 7.5% after warning that its profit is set to tumble in Q2 and pulled LVMH, Hermes and Burberry down with. And note that Hermes couldn’t escape the luxury selloff even after announcing that its own sales jumped… Stellantis fell more than 7% after revealing that their earnings plunged in the H1 and Nestle dropped 5% after downgrading its sales outlook for the year. All in all, the earnings didn’t look great. If we do an overall summary, around 40 of MSCI Europe stocks released earnings this far, and only half of them have beaten analyst forecasts. So the Stoxx 600 really looks toppish right now. The weak economic data and meagre earnings boost the European Central Bank (ECB) rate cut expectations for September, but I don’t know if the ECB alone could cheer up investors. The EURUSD found support near the 1.0825 despite unpleasant news and data. But the sticky US growth limits the Fed’s rate cut potential, hence could also limit the euro’s upside potential against the greenback.

Elsewhere, the USDJPY tipped a toe below the 152 yesterday and on rising expectation that the Bank of Japan (BoJ) could hike its policy rate next week. But the BoJ is not the Fed, or the ECB. Just because the market expects a rate hike doesn’t mean it will actually happen. The BoJ could easily disappoint those anticipating a hike next week, delivering a blow to long yen positions.

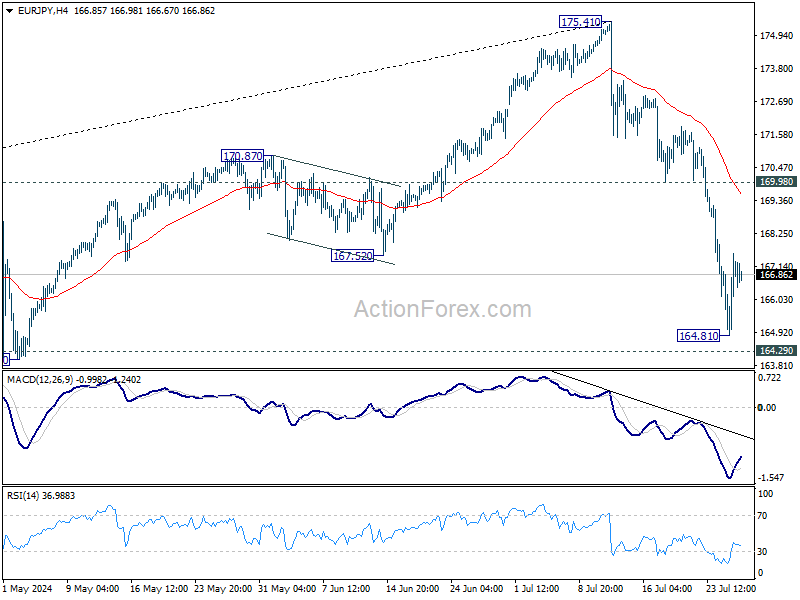

EUR/JPY Daily Outlook

Daily Pivots: (S1) 165.33; (P) 166.46; (R1) 168.09; More...

A temporary low should be in place at 164.81 with current recovery. Intraday bias in EUR/JPY is turned neutral first. But risk will stay on the downside as long as 169.98 support turned resistance holds. On the downside, decisive break of 164.29 support turned resistance will indicate that larger scale correction is underway for 155.91 fibonacci level.

In the bigger picture, immediate focus is now on 164.29 resistance turned support. Strong rebound from there will retain medium term bullishness for resuming the up trend through 175.41 at a later stage. However, decisive break of 164.29 will indicate that fall from 175.41 is at least correcting the rise from 124.73, with risk of bearish trend reversal. Deeper decline would be seen to 38.2% retracement of 124.37 to 175.41 at 155.91.

Calmer Markets Shift Focus to US PCE Inflation Data

The forex markets have calmed down considerably in Asian session after a week of significant wild ride. Despite the pause, the risk-averse sentiment persists. Yen, which has led the charge this week, is starting to take a breather. It remains the runaway leader, followed by Swiss Franc and then Dollar. Meanwhile, New Zealand Dollar has overtaken Australian Dollar as the worst performer, with Canadian Dollar trailing as a distant third. Euro and Sterling are trading in the middle of the pack, with Euro showing a slight edge.

Today's spotlight is on US PCE inflation report. Both the headline and core PCE are anticipated to decrease to 2.5% in June, mirroring the CPI report's indication of ongoing disinflation. A 25bps rate cut by Fed in September is fully priced in by the markets. The primary question has shifted to whether Fed will implement two or three rate cuts this year. Fed fund futures currently suggest there is a 60% chance that the federal funds rate will end the year at 4.50-4.75%, a reduction of 0.75% from the current level.

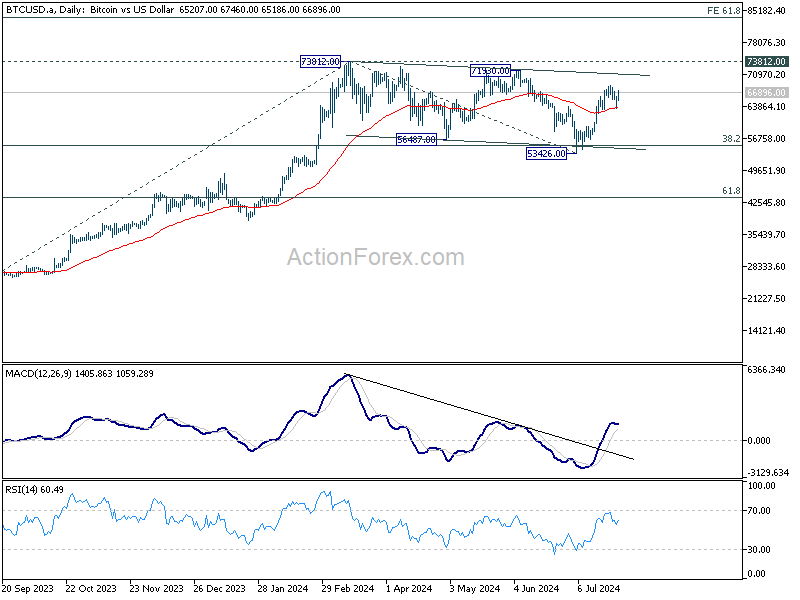

Technically, Bitcoin rebounded notably after dipping to 63421 earlier in the week. The strong support from 55 D EMA so far is keeping the bullish case alive. That is, consolidation from 73812 has completed with three waves down to 53426. Larger up trend is ready to resume towards 61.8% projection of 24896 to 73812 from 53426 at 83686. Let's see how it goes.

In Asia, at the time of writing, Nikkei is up 0.02%. Hong Kong HSI is up 0.01%. China Shanghai SSE is down -0.24%. Singapore Strait Times is down -0.01%. Japan 10-year JGB yield is down -0.014 at 1.060. Overnight, DOW rose 0.20%. S&P 500 fell -0.51%. NASDAQ fell -0.93%. 10-year yield fell -0.030 to 4.256.

Tokyo CPI core rises, but core-core falls; BoJ rate hike uncertainty persists

Japan's Tokyo CPI core (excluding food) increased from 2.1% yoy to 2.2% yoy in July, aligning with market expectations. This marks the third consecutive month of re-acceleration following a dip to 1.6% yoy in April. The primary driver of this uptick was energy prices, with electricity costs soaring by 19.7% yoy due to the termination of government utility subsidies.

However, other inflation measures showed a slowdown. CPI core-core (excluding food and energy) dropped from 1.8% yoy to 1.5% yoy. Additionally, services inflation decreased from 0.9% yoy to 0.5% yoy, while headline CPI fell slightly from 2.3% yoy to 2.2% yoy.

The increase in core inflation maintains the possibility of a BoJ rate hike next week. However, the current data is not sufficiently conclusive to confirm this outcome. Swap markets indicate a 38% probability of a 15bps hike. A Bloomberg survey reveals that 30% of BoJ watchers anticipate a hike, with 90% viewing it as a potential risk.

Looking ahead

Main focus ahead is US personal income and spending, and PCE inflation.

EUR/JPY Daily Outlook

Daily Pivots: (S1) 165.33; (P) 166.46; (R1) 168.09; More...

A temporary low should be in place at 164.81 with current recovery. Intraday bias in EUR/JPY is turned neutral first. But risk will stay on the downside as long as 169.98 support turned resistance holds. On the downside, decisive break of 164.29 support turned resistance will indicate that larger scale correction is underway for 155.91 fibonacci level.

In the bigger picture, immediate focus is now on 164.29 resistance turned support. Strong rebound from there will retain medium term bullishness for resuming the up trend through 175.41 at a later stage. However, decisive break of 164.29 will indicate that fall from 175.41 is at least correcting the rise from 124.73, with risk of bearish trend reversal. Deeper decline would be seen to 38.2% retracement of 124.37 to 175.41 at 155.91.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:30 | JPY | Tokyo CPI Y/Y Jul | 2.20% | 2.30% | ||

| 23:30 | JPY | Tokyo CPI Core Y/Y Jul | 2.20% | 2.20% | 2.10% | |

| 23:30 | JPY | Tokyo CPI Core-Core Y/Y Jul | 1.50% | 1.80% | ||

| 12:30 | USD | Personal Income M/M Jun | 0.40% | 0.50% | ||

| 12:30 | USD | Personal Spending Jun | 0.30% | 0.20% | ||

| 12:30 | USD | PCE Price Index M/M Jun | 0.10% | 0.00% | ||

| 12:30 | USD | PCE Price Index Y/Y Jun | 2.50% | 2.60% | ||

| 12:30 | USD | Core PCE Price Index M/M Jun | 0.20% | 0.10% | ||

| 12:30 | USD | Core PCE Price Index Y/Y Jun | 2.50% | 2.60% | ||

| 14:00 | USD | Michigan Consumer Sentiment Jul F | 66 | 66 |