Sample Category Title

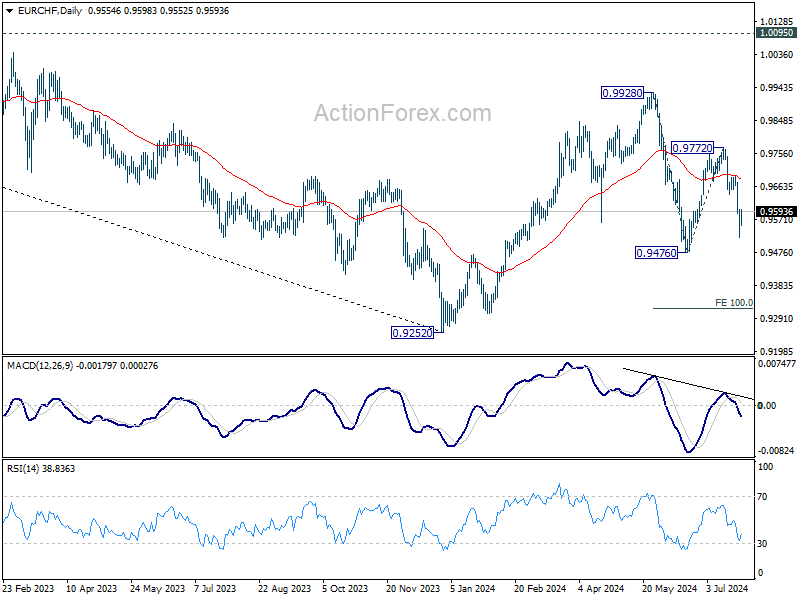

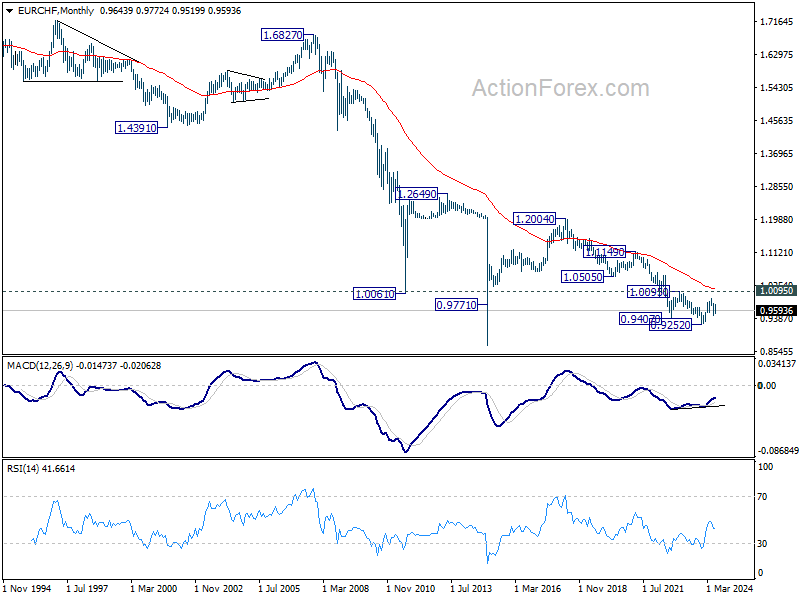

EUR/CHF Weekly Outlook

EUR/CHF's fall from 0.9772 extended to 0.9519 last week but recovered since then. Initial bias is turned neutral this week for consolidations first. Further decline is expected as long as 0.9641 support turned resistance holds. Rebound from 0.9476 should have completed as a corrective move at 0.9772. Below 0.9519 will bring retest of 0.9476. Firm break there will resume whole fall from 0.9928 to 100% projection of 0.9928 to 0.94767 from 0.9772 at 0.9320.

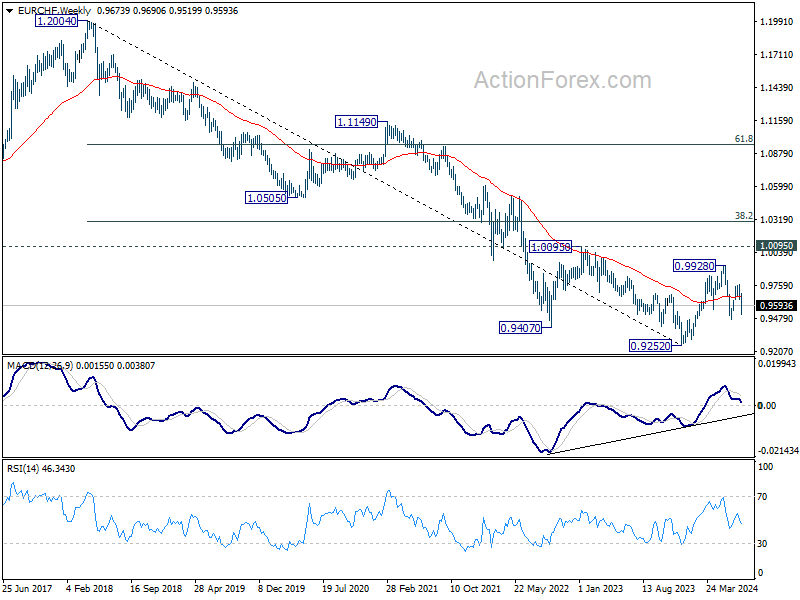

In the bigger picture, with 1.0095 key medium term resistance intact, price actions from 0.9252 (2023 low) are seen as a corrective pattern. Fall from 0.9928 might be the second leg and break of 0.9476 would bring deeper decline to retest 0.9252 low. But strong support should be seen there to extend the corrective pattern with another rising leg. In any case, medium term outlook will be neutral at best as long as 1.0095 structural resistance holds.

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

Summary 7/29 – 8/2

Monday, Jul 29, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 08:30 | GBP | M4 Money Supply M/M Jun | -0.10% | |

| 08:30 | GBP | Mortgage Approvals Jun | 60K | 60K |

| 23:30 | JPY | Unemployment Rate Jun | 2.60% | 2.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 08:30 | GBP | M4 Money Supply M/M Jun | |

| Forecast: | Previous: -0.10% | ||

| 08:30 | GBP | Mortgage Approvals Jun | |

| Forecast: 60K | Previous: 60K | ||

| 23:30 | JPY | Unemployment Rate Jun | |

| Forecast: 2.60% | Previous: 2.60% | ||

Tuesday, Jul 30, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Building Permits M/M Jun | -2.30% | 5.50% |

| 06:45 | EUR | France Consumer Spending M/M Jun | -0.40% | 1.50% |

| 05:30 | EUR | France GDP Q/Q Q2 P | 0.20% | 0.20% |

| 07:00 | CHF | KOF Leading Indicator Jul | 102.6 | 102.7 |

| 08:00 | EUR | Italy GDP Q/Q Q2 P | 0.20% | 0.30% |

| 08:00 | EUR | Germany GDP Q/Q Q2 P | 0.10% | 0.20% |

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | 0.20% | 0.30% |

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jul | 95.9 | |

| 09:00 | EUR | Eurozone Industrial Confidence Jul | -10.1 | |

| 09:00 | EUR | Eurozone Services Sentiment Jul | 6.5 | |

| 09:00 | EUR | Eurozone Consumer Confidence Jul F | -13 | -13 |

| 12:00 | EUR | Germany CPI M/M Jul P | 0.30% | 0.10% |

| 12:00 | EUR | Germany CPI Y/Y Jul P | 2.20% | 2.20% |

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y May | 7.40% | 7.20% |

| 13:00 | USD | Housing Price Index M/M May | 0.20% | 0.20% |

| 14:00 | USD | Consumer Confidence Jul | 99.8 | 100.4 |

| 22:45 | NZD | Building Permits M/M Jun | -1.70% | |

| 23:50 | JPY | Industrial Production M/M Jun P | -4.20% | 3.60% |

| 23:50 | JPY | Retail Trade Y/Y Jun | 3.30% | 2.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Building Permits M/M Jun | |

| Forecast: -2.30% | Previous: 5.50% | ||

| 06:45 | EUR | France Consumer Spending M/M Jun | |

| Forecast: -0.40% | Previous: 1.50% | ||

| 05:30 | EUR | France GDP Q/Q Q2 P | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 07:00 | CHF | KOF Leading Indicator Jul | |

| Forecast: 102.6 | Previous: 102.7 | ||

| 08:00 | EUR | Italy GDP Q/Q Q2 P | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 08:00 | EUR | Germany GDP Q/Q Q2 P | |

| Forecast: 0.10% | Previous: 0.20% | ||

| 09:00 | EUR | Eurozone GDP Q/Q Q2 P | |

| Forecast: 0.20% | Previous: 0.30% | ||

| 09:00 | EUR | Eurozone Economic Sentiment Indicator Jul | |

| Forecast: | Previous: 95.9 | ||

| 09:00 | EUR | Eurozone Industrial Confidence Jul | |

| Forecast: | Previous: -10.1 | ||

| 09:00 | EUR | Eurozone Services Sentiment Jul | |

| Forecast: | Previous: 6.5 | ||

| 09:00 | EUR | Eurozone Consumer Confidence Jul F | |

| Forecast: -13 | Previous: -13 | ||

| 12:00 | EUR | Germany CPI M/M Jul P | |

| Forecast: 0.30% | Previous: 0.10% | ||

| 12:00 | EUR | Germany CPI Y/Y Jul P | |

| Forecast: 2.20% | Previous: 2.20% | ||

| 13:00 | USD | S&P/CS Composite-20 HPI Y/Y May | |

| Forecast: 7.40% | Previous: 7.20% | ||

| 13:00 | USD | Housing Price Index M/M May | |

| Forecast: 0.20% | Previous: 0.20% | ||

| 14:00 | USD | Consumer Confidence Jul | |

| Forecast: 99.8 | Previous: 100.4 | ||

| 22:45 | NZD | Building Permits M/M Jun | |

| Forecast: | Previous: -1.70% | ||

| 23:50 | JPY | Industrial Production M/M Jun P | |

| Forecast: -4.20% | Previous: 3.60% | ||

| 23:50 | JPY | Retail Trade Y/Y Jun | |

| Forecast: 3.30% | Previous: 2.80% | ||

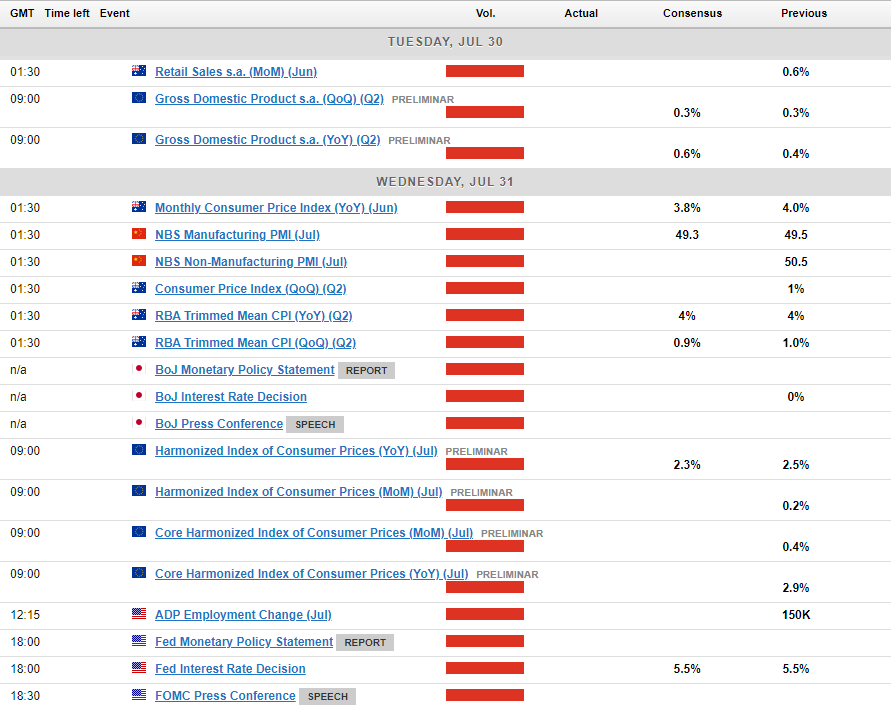

Wednesday, Jul 31, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| JPY | BoJ Interest Rate Decision | 0.10% | ||

| 01:00 | NZD | ANZ Business Confidence Jul | 6.1 | |

| 01:30 | AUD | Monthly CPI Y/Y Jun | 3.80% | 4.00% |

| 01:30 | AUD | CPI Q/Q Q2 | 1.00% | 1.00% |

| 01:30 | AUD | CPI Y/Y Q2 | 3.60% | |

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q2 | 0.90% | 1.00% |

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q2 | 4.00% | 4.00% |

| 01:30 | AUD | Retail Sales M/M Jun | 0.30% | 0.60% |

| 01:30 | AUD | Private Sector Credit M/M Jun | 0.40% | |

| 01:30 | CNY | NBS Manufacturing PMI Jul | 49.3 | 49.5 |

| 01:30 | CNY | NBS Non-Manufacturing PMI Jul | 50.2 | 50.5 |

| 03:00 | JPY | BoJ Outlook Report Q2 | ||

| 05:00 | JPY | Annualized Housing Starts Jun | 0.813M | |

| 05:00 | JPY | Housing Starts Y/Y Jun | -2.00% | -5.30% |

| 05:00 | JPY | Construction Orders Y/Y Jun | 2.10% | |

| 05:00 | JPY | Consumer Confidence Index Jul | 36.4 | |

| 06:00 | EUR | Germany Import Price Index M/M Jun | 0.10% | 0.00% |

| 07:55 | EUR | Germany Unemployment Change Jul | 16K | 19K |

| 07:55 | EUR | Germany Unemployment Rate Jul | 6.00% | 6.00% |

| 08:00 | CHF | UBS Economic Expectations Jul | 17.5 | |

| 09:00 | EUR | Eurozone CPI Y/Y Jul P | 2.40% | 2.50% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul P | 2.80% | 2.90% |

| 12:15 | USD | ADP Employment Change Jul | 166K | 150K |

| 12:30 | USD | Employment Cost Index Q2 | 1.00% | 1.20% |

| 12:30 | CAD | GDP M/M May | 0.10% | 0.30% |

| 13:45 | USD | Chicago PMI Jul | 44.1 | 47.4 |

| 14:00 | USD | Pending Home Sales M/M Jun | 1.60% | -2.10% |

| 14:30 | USD | Crude Oil Inventories | -3.7M | |

| 18:00 | USD | Fed Interest Rate Decision | 5.50% | 5.50% |

| 18:30 | USD | FOMC Press Conference |

| GMT | Ccy | Events | |

|---|---|---|---|

| JPY | BoJ Interest Rate Decision | ||

| Forecast: | Previous: 0.10% | ||

| 01:00 | NZD | ANZ Business Confidence Jul | |

| Forecast: | Previous: 6.1 | ||

| 01:30 | AUD | Monthly CPI Y/Y Jun | |

| Forecast: 3.80% | Previous: 4.00% | ||

| 01:30 | AUD | CPI Q/Q Q2 | |

| Forecast: 1.00% | Previous: 1.00% | ||

| 01:30 | AUD | CPI Y/Y Q2 | |

| Forecast: | Previous: 3.60% | ||

| 01:30 | AUD | RBA Trimmed Mean CPI Q/Q Q2 | |

| Forecast: 0.90% | Previous: 1.00% | ||

| 01:30 | AUD | RBA Trimmed Mean CPI Y/Y Q2 | |

| Forecast: 4.00% | Previous: 4.00% | ||

| 01:30 | AUD | Retail Sales M/M Jun | |

| Forecast: 0.30% | Previous: 0.60% | ||

| 01:30 | AUD | Private Sector Credit M/M Jun | |

| Forecast: | Previous: 0.40% | ||

| 01:30 | CNY | NBS Manufacturing PMI Jul | |

| Forecast: 49.3 | Previous: 49.5 | ||

| 01:30 | CNY | NBS Non-Manufacturing PMI Jul | |

| Forecast: 50.2 | Previous: 50.5 | ||

| 03:00 | JPY | BoJ Outlook Report Q2 | |

| Forecast: | Previous: | ||

| 05:00 | JPY | Annualized Housing Starts Jun | |

| Forecast: | Previous: 0.813M | ||

| 05:00 | JPY | Housing Starts Y/Y Jun | |

| Forecast: -2.00% | Previous: -5.30% | ||

| 05:00 | JPY | Construction Orders Y/Y Jun | |

| Forecast: | Previous: 2.10% | ||

| 05:00 | JPY | Consumer Confidence Index Jul | |

| Forecast: | Previous: 36.4 | ||

| 06:00 | EUR | Germany Import Price Index M/M Jun | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 07:55 | EUR | Germany Unemployment Change Jul | |

| Forecast: 16K | Previous: 19K | ||

| 07:55 | EUR | Germany Unemployment Rate Jul | |

| Forecast: 6.00% | Previous: 6.00% | ||

| 08:00 | CHF | UBS Economic Expectations Jul | |

| Forecast: | Previous: 17.5 | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jul P | |

| Forecast: 2.40% | Previous: 2.50% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jul P | |

| Forecast: 2.80% | Previous: 2.90% | ||

| 12:15 | USD | ADP Employment Change Jul | |

| Forecast: 166K | Previous: 150K | ||

| 12:30 | USD | Employment Cost Index Q2 | |

| Forecast: 1.00% | Previous: 1.20% | ||

| 12:30 | CAD | GDP M/M May | |

| Forecast: 0.10% | Previous: 0.30% | ||

| 13:45 | USD | Chicago PMI Jul | |

| Forecast: 44.1 | Previous: 47.4 | ||

| 14:00 | USD | Pending Home Sales M/M Jun | |

| Forecast: 1.60% | Previous: -2.10% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -3.7M | ||

| 18:00 | USD | Fed Interest Rate Decision | |

| Forecast: 5.50% | Previous: 5.50% | ||

| 18:30 | USD | FOMC Press Conference | |

| Forecast: | Previous: | ||

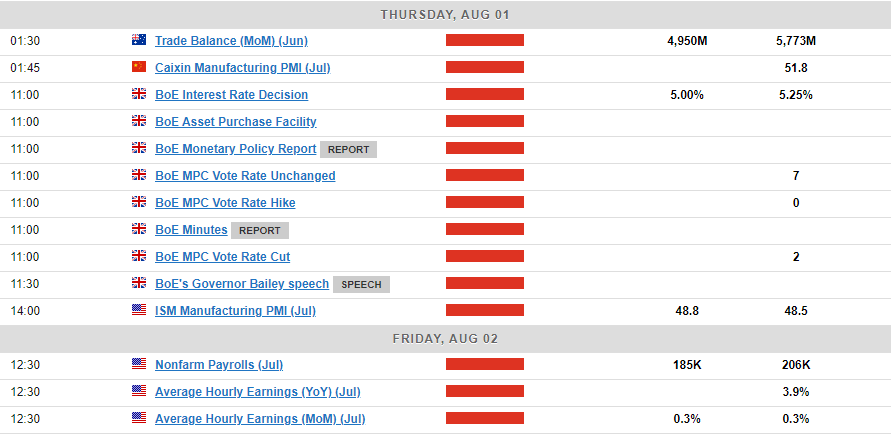

Thursday, Aug 1, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Jul F | 49.2 | 49.2 |

| 01:30 | AUD | Trade Balance (AUD) Jun | 4.95B | 5.77B |

| 01:30 | AUD | Import Price Index Q/Q Q2 | -0.70% | -1.80% |

| 01:45 | CNY | Caixin Manufacturing PMI Jul | 51.6 | 51.8 |

| 07:45 | EUR | Italy Manufacturing PMI Jul | 46.2 | 45.7 |

| 07:50 | EUR | France Manufacturing PMI Jul F | 44.1 | 44.1 |

| 07:55 | EUR | Germany Manufacturing PMI Jul F | 42.6 | 42.6 |

| 08:00 | EUR | Italy Unemployment Jun | 6.80% | 6.80% |

| 08:00 | EUR | ECB Economic Bulletin | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jul F | 45.6 | 45.6 |

| 08:30 | GBP | Manufacturing PMI Jul F | 51.8 | 51.8 |

| 09:00 | EUR | Eurozone Unemployment Rate Jun | 6.40% | 6.40% |

| 11:00 | GBP | BoE Interest Rate Decision | 5.00% | 5.25% |

| 11:00 | GBP | MPC Official Bank Rate Votes | 0--6--3 | 0--2--7 |

| 11:30 | USD | Challenger Job Cuts Y/Y Jul | 19.80% | |

| 12:30 | USD | Initial Jobless Claims (Jul 26) | 239K | 235K |

| 12:30 | USD | Nonfarm Productivity Q2 P | 1.50% | 0.20% |

| 12:30 | USD | Unit Labor Costs Q2 P | 1.60% | 4.00% |

| 13:30 | CAD | Manufacturing PMI Jul | 49.3 | |

| 13:45 | USD | Manufacturing PMI Jul F | 49.5 | 49.5 |

| 14:00 | USD | ISM Manufacturing PMI Jul | 48.8 | 48.5 |

| 14:00 | USD | ISM Manufacturing Prices Paid Jul | 52.5 | 52.1 |

| 14:00 | USD | ISM Manufacturing Employment Index Jul | 49.3 | |

| 14:00 | USD | Construction Spending M/M Jun | 0.20% | -0.10% |

| 14:30 | USD | Natural Gas Storage | 22B | |

| 23:50 | JPY | Monetary Base Y/Y Jul | 0.90% | 0.60% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 00:30 | JPY | Manufacturing PMI Jul F | |

| Forecast: 49.2 | Previous: 49.2 | ||

| 01:30 | AUD | Trade Balance (AUD) Jun | |

| Forecast: 4.95B | Previous: 5.77B | ||

| 01:30 | AUD | Import Price Index Q/Q Q2 | |

| Forecast: -0.70% | Previous: -1.80% | ||

| 01:45 | CNY | Caixin Manufacturing PMI Jul | |

| Forecast: 51.6 | Previous: 51.8 | ||

| 07:45 | EUR | Italy Manufacturing PMI Jul | |

| Forecast: 46.2 | Previous: 45.7 | ||

| 07:50 | EUR | France Manufacturing PMI Jul F | |

| Forecast: 44.1 | Previous: 44.1 | ||

| 07:55 | EUR | Germany Manufacturing PMI Jul F | |

| Forecast: 42.6 | Previous: 42.6 | ||

| 08:00 | EUR | Italy Unemployment Jun | |

| Forecast: 6.80% | Previous: 6.80% | ||

| 08:00 | EUR | ECB Economic Bulletin | |

| Forecast: | Previous: | ||

| 08:00 | EUR | Eurozone Manufacturing PMI Jul F | |

| Forecast: 45.6 | Previous: 45.6 | ||

| 08:30 | GBP | Manufacturing PMI Jul F | |

| Forecast: 51.8 | Previous: 51.8 | ||

| 09:00 | EUR | Eurozone Unemployment Rate Jun | |

| Forecast: 6.40% | Previous: 6.40% | ||

| 11:00 | GBP | BoE Interest Rate Decision | |

| Forecast: 5.00% | Previous: 5.25% | ||

| 11:00 | GBP | MPC Official Bank Rate Votes | |

| Forecast: 0--6--3 | Previous: 0--2--7 | ||

| 11:30 | USD | Challenger Job Cuts Y/Y Jul | |

| Forecast: | Previous: 19.80% | ||

| 12:30 | USD | Initial Jobless Claims (Jul 26) | |

| Forecast: 239K | Previous: 235K | ||

| 12:30 | USD | Nonfarm Productivity Q2 P | |

| Forecast: 1.50% | Previous: 0.20% | ||

| 12:30 | USD | Unit Labor Costs Q2 P | |

| Forecast: 1.60% | Previous: 4.00% | ||

| 13:30 | CAD | Manufacturing PMI Jul | |

| Forecast: | Previous: 49.3 | ||

| 13:45 | USD | Manufacturing PMI Jul F | |

| Forecast: 49.5 | Previous: 49.5 | ||

| 14:00 | USD | ISM Manufacturing PMI Jul | |

| Forecast: 48.8 | Previous: 48.5 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jul | |

| Forecast: 52.5 | Previous: 52.1 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jul | |

| Forecast: | Previous: 49.3 | ||

| 14:00 | USD | Construction Spending M/M Jun | |

| Forecast: 0.20% | Previous: -0.10% | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: | Previous: 22B | ||

| 23:50 | JPY | Monetary Base Y/Y Jul | |

| Forecast: 0.90% | Previous: 0.60% | ||

Friday, Aug 2, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | PPI Q/Q Q2 | 1.00% | 0.90% |

| 01:30 | AUD | PPI Y/Y Q2 | 4.30% | |

| 06:30 | CHF | CPI M/M Jul | -0.20% | 0.00% |

| 06:30 | CHF | CPI Y/Y Jul | 1.30% | |

| 06:45 | EUR | France Industrial Output M/M Jun | 0.90% | -2.10% |

| 07:30 | CHF | Manufacturing PMI Jul | 44.6 | 43.9 |

| 08:00 | EUR | Italy Industrial Output M/M Jun | -0.20% | 0.50% |

| 09:00 | EUR | Italy Retail Sales M/M Jun | 0.20% | 0.40% |

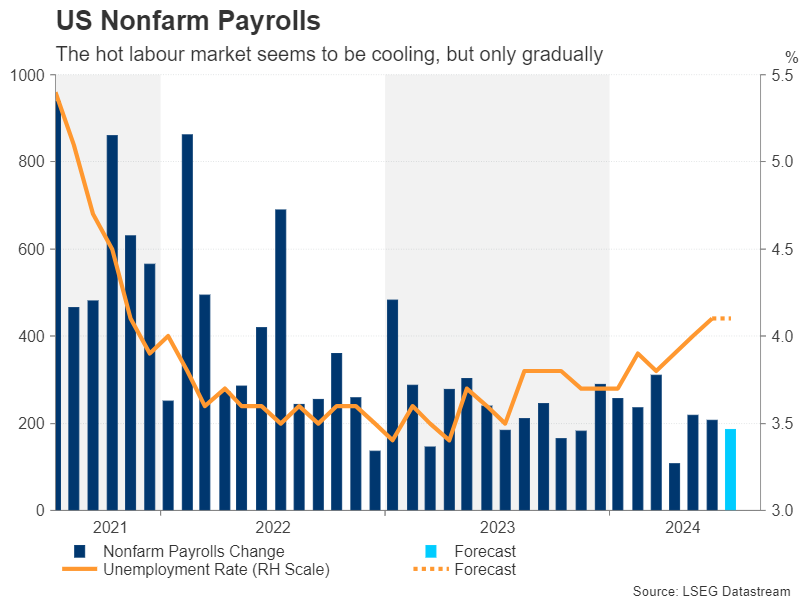

| 12:30 | USD | Nonfarm Payrolls Jul | 185K | 206K |

| 12:30 | USD | Unemployment Rate Jul | 4.10% | 4.10% |

| 12:30 | USD | Average Hourly Earnings M/M Jul | 0.30% | 0.30% |

| 14:00 | USD | Factory Orders M/M Jun | 0.50% | -0.50% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | PPI Q/Q Q2 | |

| Forecast: 1.00% | Previous: 0.90% | ||

| 01:30 | AUD | PPI Y/Y Q2 | |

| Forecast: | Previous: 4.30% | ||

| 06:30 | CHF | CPI M/M Jul | |

| Forecast: -0.20% | Previous: 0.00% | ||

| 06:30 | CHF | CPI Y/Y Jul | |

| Forecast: | Previous: 1.30% | ||

| 06:45 | EUR | France Industrial Output M/M Jun | |

| Forecast: 0.90% | Previous: -2.10% | ||

| 07:30 | CHF | Manufacturing PMI Jul | |

| Forecast: 44.6 | Previous: 43.9 | ||

| 08:00 | EUR | Italy Industrial Output M/M Jun | |

| Forecast: -0.20% | Previous: 0.50% | ||

| 09:00 | EUR | Italy Retail Sales M/M Jun | |

| Forecast: 0.20% | Previous: 0.40% | ||

| 12:30 | USD | Nonfarm Payrolls Jul | |

| Forecast: 185K | Previous: 206K | ||

| 12:30 | USD | Unemployment Rate Jul | |

| Forecast: 4.10% | Previous: 4.10% | ||

| 12:30 | USD | Average Hourly Earnings M/M Jul | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 14:00 | USD | Factory Orders M/M Jun | |

| Forecast: 0.50% | Previous: -0.50% | ||

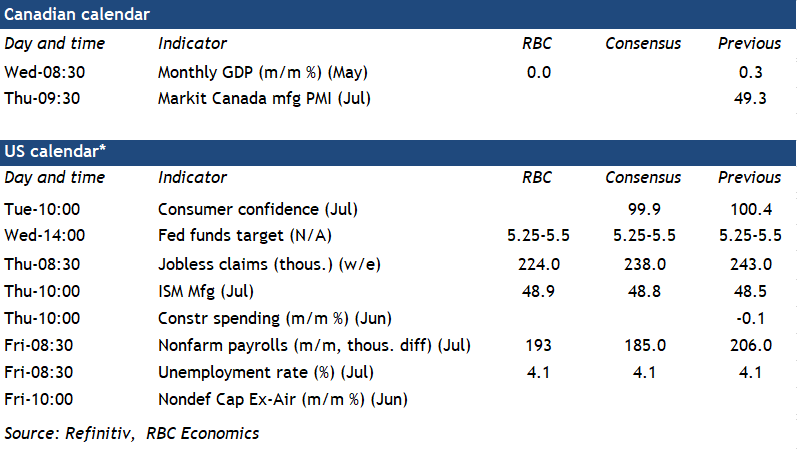

Markets Weekly Outlook: Central Banks and US Earnings. Will BoJ Hike Rates?

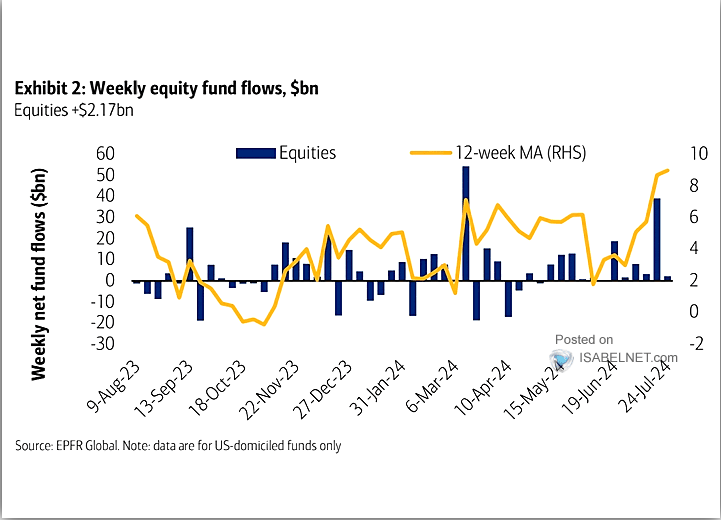

- Global markets experienced a volatile week, influenced by a tech selloff, China growth concerns, and anticipation of central bank decisions and US earnings reports

- Despite the volatility and tech led selloff, US equity funds saw inflows.

- Central bank meetings, particularly the FOMC and BoJ, and US NFP data will be key drivers of market sentiment in the coming week.

Week in Review: Sentiment Overshadows US Earnings and Data

A tumultuous week for global markets fraught with risk, volatility and a whole lot of opportunity is drawing to a close. The tech selloff in US Megacap tech stocks accelerated in the early part of the week, compounded by concerns around growth in China. A rally on Friday by the SPX and Nasdaq 100 was led by a rebound in tech stocks with Meta, Microsoft and Amazon leading the way.

Despite the concerns around Big tech stocks US equity funds still experienced inflows of around $2.17 billion for the week, according to Bank of America research

Source: EPFR Global, US Domiciled Funds Only

Elsewhere Gold prices recovered late in the week as well after dipping as low as 2353.10 on Thursday to trade at 2388.25 at the time of writing. Oil prices also appear to have found support with Brent posting a weekly low just above the psychological $80 a barrel mark.

Market moves this week have baffled many and that is understandable. US data for the first time this year appears to be overshadowed by other factors which have been driving markets.

The lackluster reaction to the US GDP and PCE prints further highlight this recent phenomenon. It would appear that the effects of the tech sell-off, early positioning for the US election, and the unwinding of carry trades have created significant market movements that overshadow US economic data.

Whether these factors will overshadow a host of economic data events due next week, remains to be seen.

The Week Ahead: Central Bank Meetings and NFP to Dominate

US

Looking ahead to next week, there is a lot happening globally which could have an impact on financial markets. Market participants will pay attention to the FOMC meeting but it remains too soon in the eyes of many to expect a rate cut..

The NFP and jobs report on Friday may have a bigger impact on the US dollar next week. Depending on the rhetoric from Federal Reserve Chair Jerome Powell the data could be an important cog in whether the Fed cut rates in September as expected.

Europe + UK

The Euro Area will report its preliminary inflation numbers on Wednesday as market participants eye further cuts from the European Central Bank. A soft inflation print will go some to solidifying the belief that more cuts are on the way and could see the Euro fall further.

The UK and the Bank of England (BoE) will definitely be in the spotlight next week. As one analyst put it, next week’s BoE decision is just too close to call. Looking overall at the UK which has somewhat outperformed expectation in 2024, there is a growing possibility of a cut next week.

The UK inflation story is looking better despite some recent upside surprises in services. An excellent way of looking at it, two members of the nine-person committee have already begun voting for rate cuts. Two or possibly three others hold the opposite view and are clearly resistant to cuts. This leaves four or five members in the middle, who seem undecided.

June’s meeting indicated that some, perhaps most, of these officials believed the decision was finely balanced. However, since the general election was called in late May, we’ve heard very little from these policymakers.

This lack of commentary makes it difficult to predict Thursday’s meeting with confidence. Nonetheless, we continue to maintain our long-held base case that a rate cut will occur in August.

Asia Pacific Markets

The most anticipated event next week is the Bank of Japan (BoJ) policy meeting. The reason…rumors that the central bank will unveil a plan to halve its bond buying and may even debate a 15bps rate hike.

This news brought a lot of volatility and strength to the Japanese Yen this week. The economy has returned to a recovery trajectory following an unexpected contraction in the first quarter of 2024, and solid wage growth in May should bolster the central bank’s confidence.

The key for me is wage growth, a key gauge punted by Governor Ueda since he assumed office. The positive increases in wages coupled with an announcement this week of a new minimum wage cap are signs that the economy may be about ready for a rate hike.

Inflationary pressure continues to plague the RBA and Australian consumers, something which RBA Governor Bullock acknowledged recently. The Governor seems to support the idea that domestic demand is too strong to permit inflation to decrease at an acceptable rate. Another uptick in inflation is likely to see rate hike bets ramp up for the RBA’s August meeting.

The US Earnings season continues next week with some heavy hitters on the agenda. Microsoft will release results after market close on Tuesday, followed by Meta on Wednesday and Apple and Amazon on Thursday. Significant volatility could materialize particularly in the S&P 500 and Nasdaq 100.

Chart of the Week

The chart of the week that I will be focusing on is the Nasdaq 100. Last week’s selloff continued, pushing the Nasdaq 100 below the ascending trendline before bouncing off the 100-day moving average (MA) on Friday.

Currently, the daily candle appears likely to close as a bullish engulfing candle, suggesting potential further recovery next week. However, a retest and rejection of the trendline could lead to new lows next week, depending on earnings reports and overall market sentiment.

For the Nasdaq to reach support at 18,400 and potentially lower levels, a break and daily candle close below the 100-day MA are necessary, with the 200-day MA resting at 17,656.

On the upside, resistance lies at the trendline, and a break above this level could bring 19,480 into focus, followed by the psychological barrier at 20,000.

Nasdaq 100 Daily Chart – June 28, 2024

Source:TradingView.Com (click to enlarge)

Key Levels to Consider:

Support:

- 18757

- 18400

- 17656

Resistance:

- 19247

- 19500

- 20000

- 20400

The Weekly Bottom Line: All Eyes on Next Week’s Fed Meeting

U.S. Highlights

- The U.S. economy accelerated in the second quarter, growing by 2.8% (annualized), up from 1.4% in the first quarter.

- At the same time, inflation cooled to 2.5% year-on-year (y/y) in June, as measured by the personal consumption expenditure deflator. However, the Fed’s preferred inflation metric, core PCE, was unchanged relative to May.

- High interest rates continued to burden the housing market in June, as existing home sales fell 5.4% month-on-month.

Canadian Highlights

- The Bank of Canada lowered its policy rate by a second straight 25 basis points, taking the overnight rate to 4.50%.

- The Bank’s communications took a dovish turn, pushing forecasters to bump up their expectations for the pace of future rate cuts.

- Economic projections in the updated Monetary Policy Report (MPR) suggest that Canada’s economy will achieve a soft-landing.

U.S. – All Eyes on Next Week’s Fed Meeting

With the second half of the year now well under way, data this week showed a fairly Goldilocks outcome for the U.S. economy. Growth momentum coming out of the first half of the year was broadly favorable, while at the same time, inflationary pressures are cooling. In financial markets, company earnings reports out this week were mixed on aggregate, with weakness among the large tech firms dragging the S&P 500 down by 0.9% on the week as of the time of writing. U.S. Treasury yields also fell modestly on Friday’s PCE inflation report as markets wait to hear from the Federal Reserve next week.

Starting the week off on Tuesday, June housing data showed that existing home sales fell sharply to end the second quarter, fully retracing the uptick seen in the first quarter. However, this has not translated into material price adjustments, as the median home sales price in June was only a half-step off its all-time high seen in the month prior. With expectations growing for lower interest rates in the second half of the year, it’s possible that some buyers are biding their time.

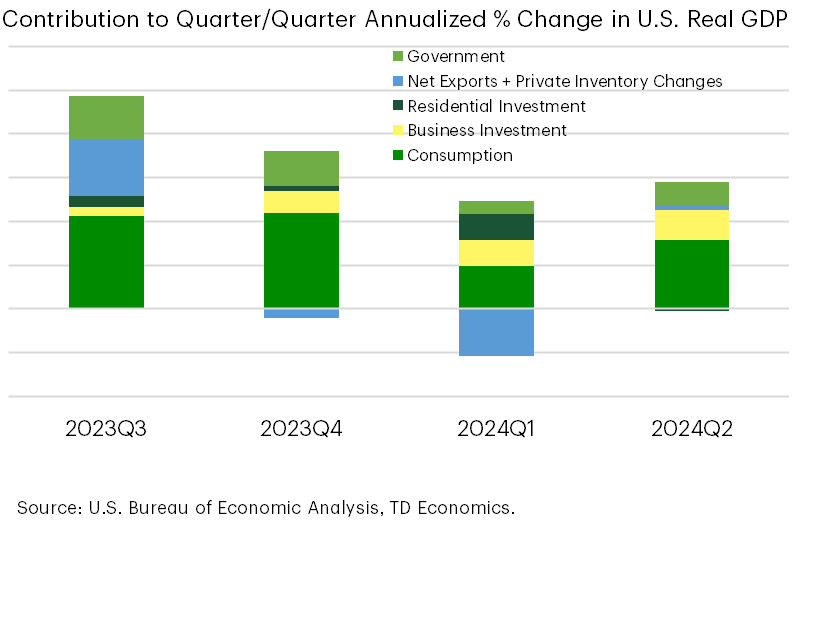

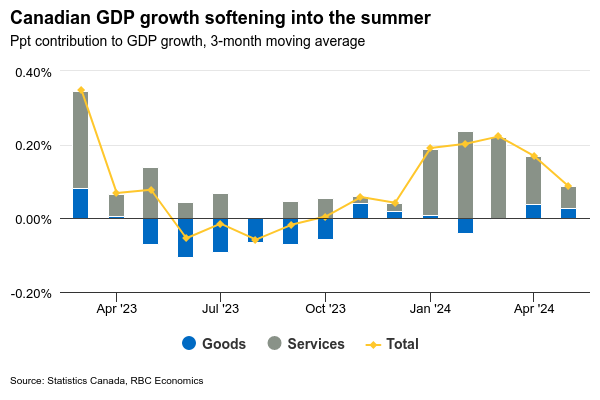

The decline in the housing market shaved a marginal amount off real GDP growth in the second quarter, but solid growth in consumption, business investment, and government spending pushed the quarterly annualized growth rate to 2.8%, up from 1.4% in the first quarter (Chart 1). Growth in final sales to private domestic purchasers (excluding government spending and private inventory adjustments) was unchanged relative to the first quarter, as stronger consumption was offset by weakness in the housing market. Looking ahead, we expect that growth will moderate through the second half of the year but remain near the long-run average as the Federal Reserve begins to lower rates in the coming months.

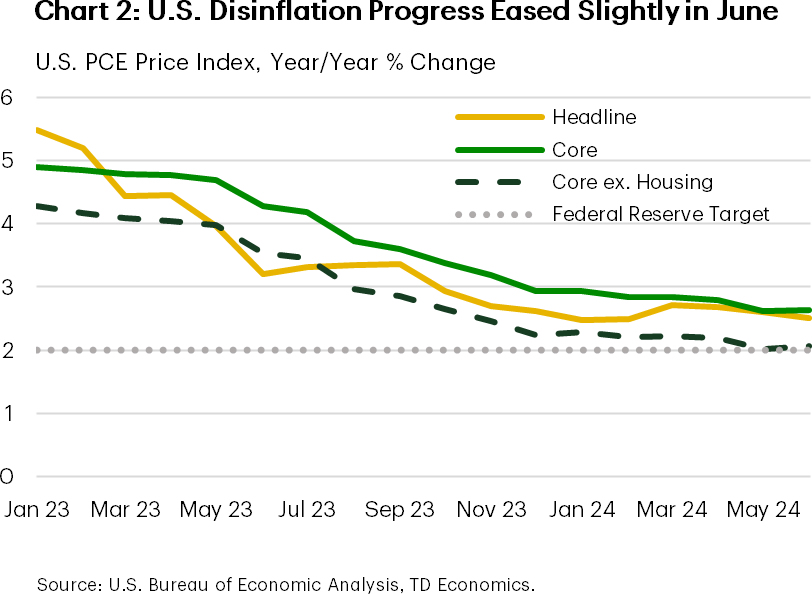

To that end, inflation data released on Friday was slightly mixed on aggregate. Although headline PCE inflation declined modestly, core PCE inflation on a year-on-year basis was unchanged owing to a marginal acceleration in core PCE ex. housing, which offset a deceleration in housing inflation. Nevertheless, with housing inflation expected to continue to moderate moving forward and annual core PCE ex. housing inflation still in-line with the Fed’s 2% target (Chart 2), this report will not likely sway the Fed’s confidence about disinflation progress to a great degree.

Looking ahead, on the one-year anniversary of the last time the Fed hiked rates, Chair Powell is expected to begin opening the door to the possibility of a near-term pivot to rate cuts during his press conference next week. Financial markets have fully priced in the first cut occurring in just under two months at the September meeting, with an additional 2-3 cuts expected by year-end. However, overall guidance from the Fed next week is expected to emphasize caution and flexibility. Given the flare up in inflation in the first quarter, the Fed is going to want to be quite confident that inflation will continue to move in the right direction. On the other side of the Fed’s dual mandate, the second-last employment report before the September meeting, out next Friday, will also be monitored closely to determine whether the deceleration in job growth in the second quarter carried into the third.

Canada – Who Let the Doves Out?

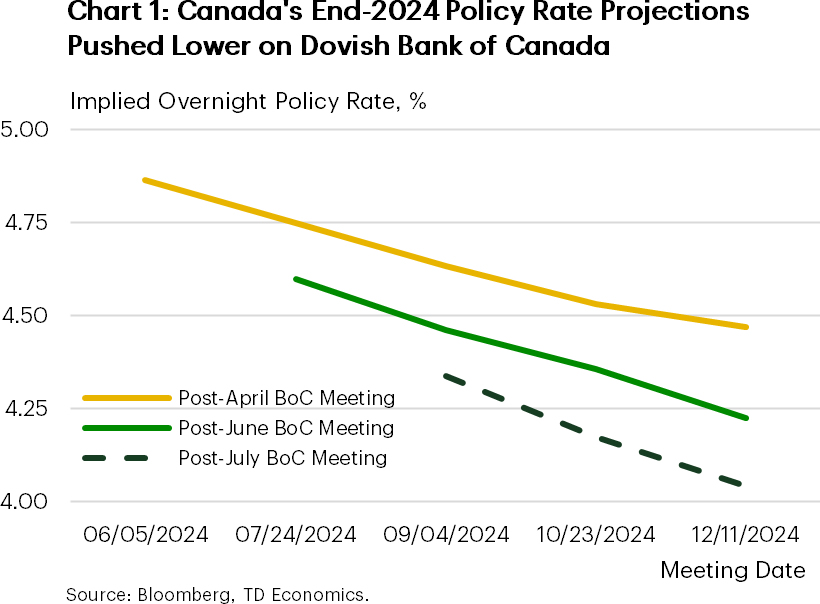

The Bank of Canada (BoC) forged ahead with a second consecutive interest rate cut this week, bringing its policy rate down by 25 basis points (bps) to 4.50%. The move was widely expected and confirms that the BoC has now firmly entered into their rate easing cycle. The path forward is more uncertain, but the meeting’s dovish tilt suggests that the Bank is not hesitant to push rates lower in the near-term. As a result of the decision and communications, markets are pricing a 75% probability of an interest rate cut in September, and fully pricing in a 4.00% policy rate (two cuts) by the end of the year (Chart 1). Yields bull steepened with short-end rates falling around 10 bps on the week, while the CAD settled half a cent lower to 0.7240/USD.

The message is clear: “If inflation continues to ease broadly in line with our forecast, it is reasonable to expect further cuts in our policy interest rate.” New in the BoC’s messaging was the emphasis on the downside inflation risks via excess supply and its increased weight in monetary policy discussions. This is an important shift in sentiment, as it’s indicative of a central bank concerned about needing a less restrictive rate environment to limit potential economic weakness.

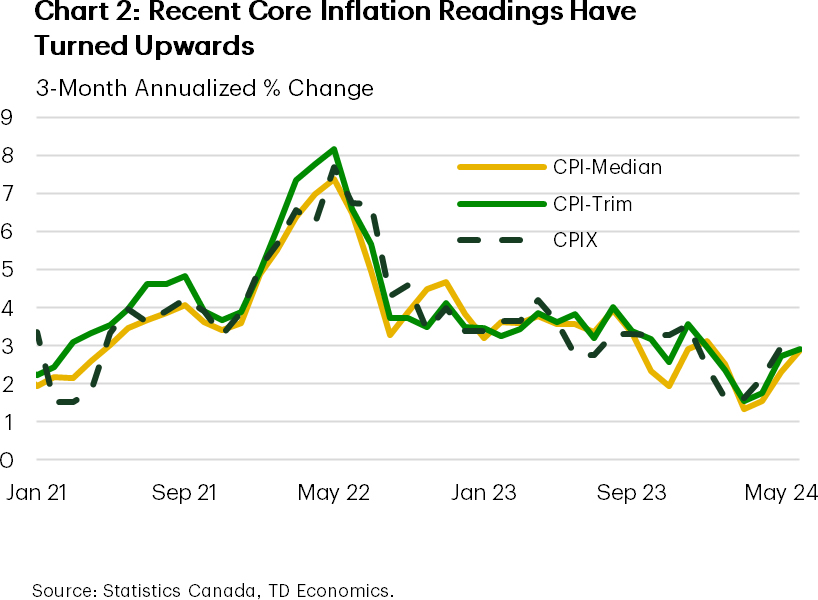

For the Bank’s part, they continue to acknowledge the progress on inflation, and we wouldn’t disagree. Headline inflation has registered under 3% year-on-year (y/y) for six consecutive months and the breadth of price increases across CPI components is near its historical average. However, while core measures have also softened within the Bank’s target range, we continue to flag that near-term growth rates for the BoC’s preferred core measures have accelerated.

Economic forecast updates in the Monetary Policy Report were modest compared to April’s issue but continue to highlight a soft-landing scenario for the economy. Despite shaving 2024 annual GDP growth to 1.2%–due to a weaker first half of the year—growth projections ratchet up to north of 2% for 2025 and 2026.

The buildup of slack in the labour market is of particular interest for the inflation projection. The BoC appears to have some reservations about whether the federal government will hit its target to rein in non-permanent resident growth by 2027. The BoC’s expectation for relatively stronger population growth in an economy with an already normalized job vacancy rate suggests the labour market is expected to loosen further. With wage sensitive services prices powering inflation, an expectation of growing excess supply in the labour market would help contain the recent uptick in core prices.

The BoC’s next interest rate announcement is on September 4th. Governor Macklem reiterated their data-dependent decision making, balancing the upside pressures from shelter and other services against ongoing excess supply. While the labour market has undoubtedly softened, if the recent uptick in core inflation is sustained, it could be the fly in the ointment for the BoC.

Weekly Economic & Financial Commentary: Wake Me Up When September Ends

Summary

United States: Economic Resilience or Reticence?

- The U.S. economy defied expectations in the second quarter, expanding at a 2.8% annualized pace. Despite the upside surprise, we still see enough softening in inflation and signs of stress to warrant a rate cut in September.

- Next week: ECI (Wed.), ISM Manuf. (Thu.), Employment (Fri.)

International: Bank of Canada Doubles Down on Monetary Easing

- The Bank of Canada (BoC) cut its policy rate 25 bps to 4.50% this week, following on from its initial rate cut in June. The accompanying statement was dovish in tone, suggesting that further rate cuts will be forthcoming in the months ahead. This week's sentiment surveys for July showed a strengthening in the U.K. manufacturing and services PMIs, but a moderate softening in the Eurozone PMIs.

- Next week: Eurozone CPI (Wed.), BoJ Policy Announcement (Thu.), BoE Policy Rate (Thu.)

Interest Rate Watch: Wake Me Up When September Ends

- The only change we expect out of next week's monetary policy meeting is for the FOMC to signal rate cuts are coming as early as its next meeting in September. Inflation progress resumed in Q2, and the labor market is softening—both developments position for Fed easing.

Credit Market Insights: Small Businesses Are Feeling the Pinch

- The NFIB Small Business Optimism Index remains lower than its historical average even at its highest level this year. With tight credit standards and high interest rate loans, we forecast some modest relief may only be from the Fed later this year.

Topic of the Week: U.S. Presidential Election Update

- The U.S presidential election took yet another historic turn this week, when President Biden announced that he will not seek re-election this November and subsequently endorsed Vice President Kamala Harris. While it is hard to say anything with certainty, it strikes us as likely a potential Harris administration, should it come to pass, would support many of the same economic policy positions of the current Biden administration.

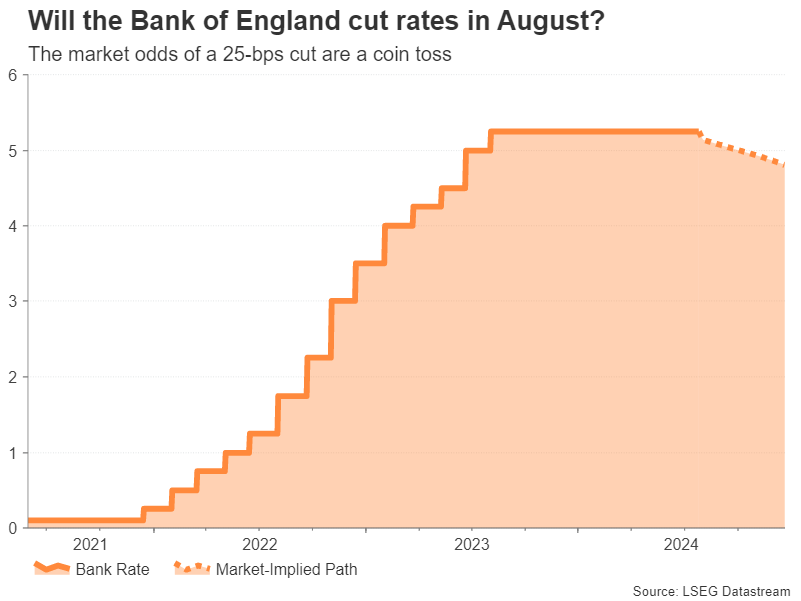

Bank of England Preview – A Dovish Hold; Limited EUR/GBP Downside Potential

- We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 1 August. We stress that it is a very close call not least due to the very limited amount of communication from the MPC over the past months.

- Overall, we expect the BoE to deliver a dovish twist to its forward guidance priming markets for a forthcoming start to a cutting cycle.

- We expect EUR/GBP to drop upon announcement but that the dovish communication in the statement and press conference will limit the downside potential.

We expect the Bank of England (BoE) to keep the Bank Rate unchanged at 5.25% on 1 August. Consensus expects a 25bp cut to 5.00% and markets currently price -12bp for the meeting. We expect the vote split to be very tight with the majority voting for an unchanged decision. The close call is further amplified by new member Clare Lombardelli (replacing Ben Broadbent) joining the committee for her first meeting. Note, this meeting will include updated projections and a press conference following the release of the statement.

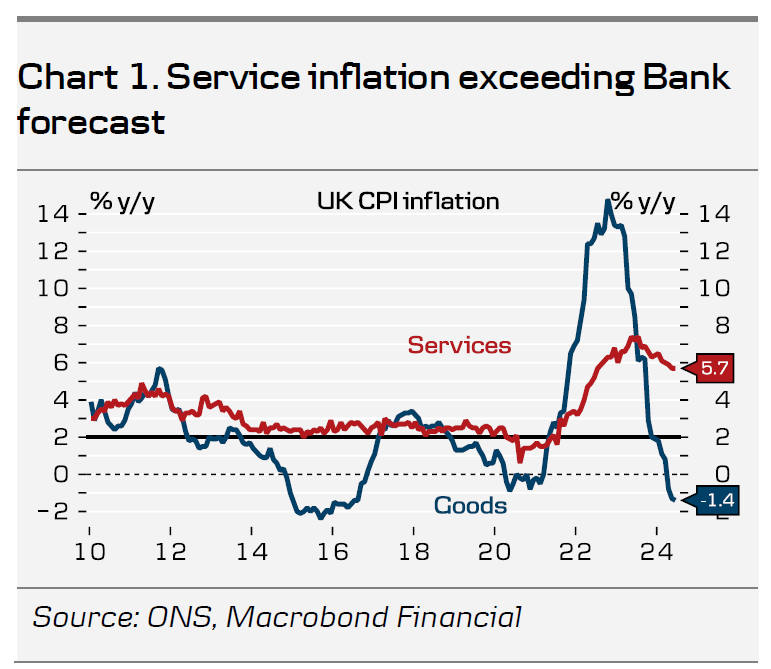

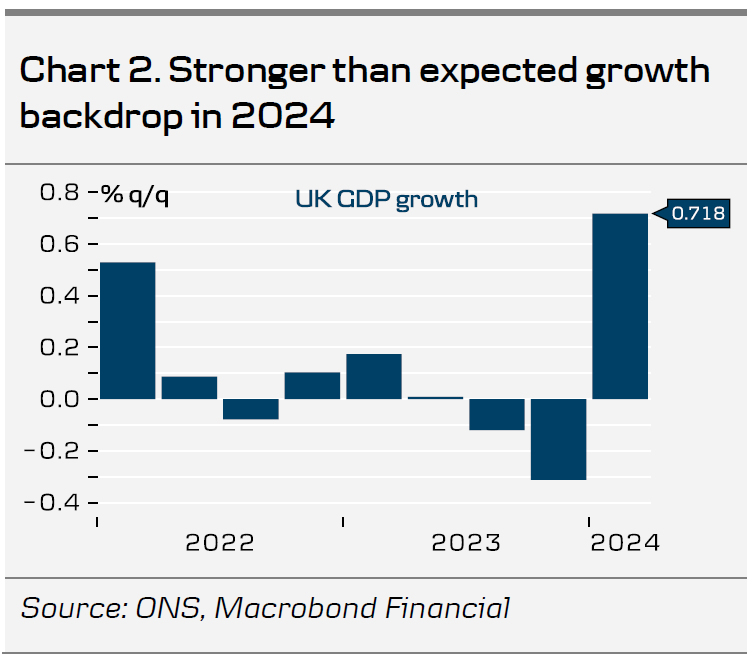

Overall, we expect the MPC to add a dovish twist to its previous guidance, priming the markets for a forthcoming start to a cutting cycle. We expect them to retain much of its wording in terms of forward guidance, repeating that "monetary policy could remain restrictive even if Bank Rate were to be reduced, given that it was starting from an already restrictive level and that "the policy decision at this meeting was finely balanced" for some members. Since the last monetary policy decision in May, data has overall been stronger than expected across both inflation, activity and partly labour markets. Activity picked up in Q1 with the economy growing 0.7% q/q (vs BoE forecast of 0.4%) underpinned by a recovery in real wages. Service inflation remained elevated in Q2 at 5.8% y/y (vs BoE forecast of 5.3%) with underlying momentum still strong. The labour market continues its gradual loosening, but wage growth remains elevated leaving a small upside risk to the BoEs Q2 forecast underpinned by the recent rise in the National Living Wage.

Given the UK general election, communication from the MPC has been very limited over the past months. Notably, Pill delivered hawkish commentary noting that "services price inflation and wage growth continue to point to an uncomfortable strength in those underlying inflation dynamics" and that indicators "have hinted towards some upside risk to my assessment of inflation persistence". In a notoriously divided committee, Bailey and Pill have voted in unison at every meeting since Pill joined the MPC in 2021.

BoE call. We expect the BoE to deliver the first cut of 25bp in September. Subsequently, we expect quarterly cuts through 2024 and 2025. Markets are pricing 50bp for the remainder of the year with the first 25bp cut fully priced by November.

FX. In our base case of a dovish "unchanged" decision, we expect EUR/GBP to drop upon announcement but that the dovish communication in the statement and press conference will limit the downside potential. We expect EUR/GBP to continue its recent move lower driven by indicators pointing to a continued (modest) rebound in the global manufacturing cycle, tight credit spreads and low FX volatility. The key risk is policy action from the BoE.

Week Ahead – BoJ, Fed and BoE Meetings: A Hike, a Hold and a Cut?

- A trio of central bank decisions coming up from the BoJ, Fed and BoE

- One might hike, one might stand pat and the other cut rates

- ECB to also be in focus as Eurozone flash GDP and CPI data are due

- Week will culminate with crucial US jobs report

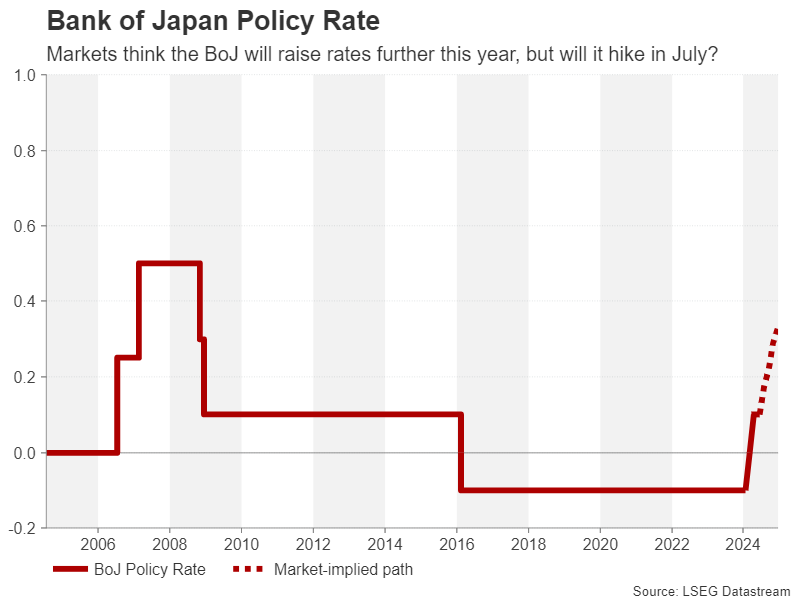

BoJ expected to taper; will it hike too?

The Bank of Japan has barely left the headlines lately. Whether it’s speculation about rate hikes, the constant hints about bond tapering or suspicions of intervention in foreign exchange markets, Governor Ueda has certainly been making his mark since taking over.

Next week’s gathering on July 30-31 looks set to give the bank more prime airtime as policymakers have already flagged that a decision will be made at this meeting on how much to reduce bond purchases by. Reuters has reported that the current monthly purchases of six trillion yen could be halved in the coming years based on what sources have said.

However, there is less clarity about the likelihood of a rate hike as policymakers do not appear to have made up their minds yet on the precise timing of one even though most agree that further increases will be necessary this year. Investors on their part have upped their bets of a July move and a 10-basis-point hike is now about two-thirds priced in. Hence, there’s a lot of room for disappointment if the bank keeps rates unchanged.

The sluggish economy and concerns about weak consumer demand could justify the need for caution, particularly when inflation, whilst above target, is far from being rampant. Moreover, the yen’s impressive rebound in July has potentially provided policymakers some breathing space on the urgency of rate hikes.

However, even if there are no major surprises on Wednesday and the only announcement is the expected decision on scaling back bond purchases, it’s unlikely that policymakers would risk sounding dovish as this could derail the yen’s recovery. The bank’s latest outlook report may offer some additional clues on the future policy course in such a scenario. Nevertheless, given the scale of the yen’s rally, a hawkish hold could still trigger some profit taking in yen crosses.

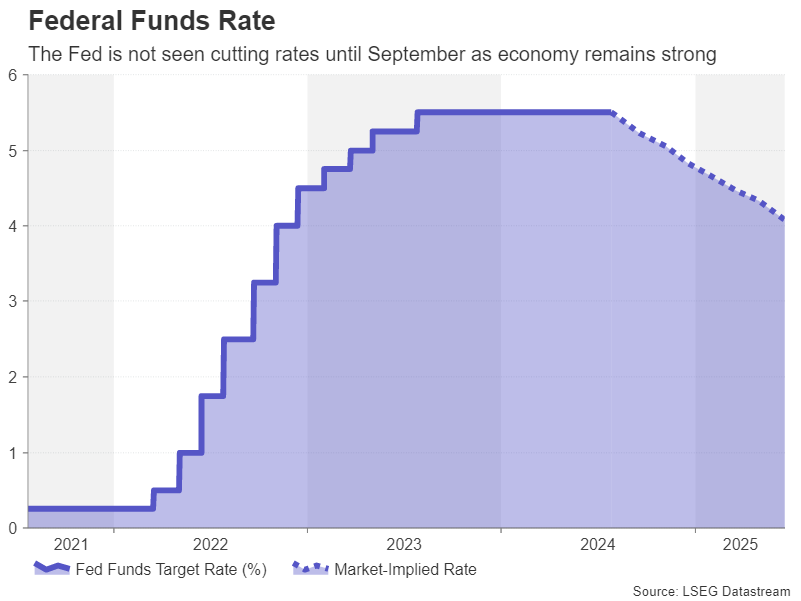

No Fed rate cut in July

The Federal Reserve will announce its decision a few hours after the BoJ on Wednesday. Out of the three central banks, the Fed is the least likely to announce any policy change. If there was a remote possibility of a surprise cut, those odds were slashed even more after the stronger-than-expected GDP reading for the second quarter.

The US economy is displaying only mild signs of a slowdown and the same is true for the labour market. This backdrop has made it difficult for Fed officials to say with certainty that inflation is on a sustained path towards 2%. However, their most recent remarks indicate growing confidence that the target is within reach and the policy statement will likely be tweaked to reflect this, signalling a dovish tilt.

July NFP to keep Powell in check

Yet, Jay Powell will probably stop short of mentioning a specific timeframe for when the Fed will start its easing cycle so the downside risks to the US dollar from the meeting are limited. With the July nonfarm payrolls report due just a couple of days later on Friday, Powell will not want to risk pre-committing to a rate cut in case the data surprises to the upside.

After rising by 206k, the American labour market is projected to have added another 185k jobs in June. The unemployment rate is forecast to have remained steady at 4.1% and average hourly earnings growth is also anticipated to have maintained a similar pace to May month-on-month.

Weaker-than-expected jobs numbers could go some way in boosting sentiment on Wall Street but hurt the dollar, as it would reinforce the aggressive rate cut bets, while another strong print could exacerbate the current selloff in equities.

Investors will get the chance to pore over plenty of other data as well over the coming week, including the consumer confidence index and JOLTS job openings on Tuesday, the ADP employment report, Chicago PMI and pending homes sales on Wednesday, and of course the ISM manufacturing PMI on Thursday.

Will the BoE take the plunge and cut?

The Bank of England will round up next week’s central bank decisions and even though the UK election uncertainty has been removed, it’s unclear what the outcome will be on Thursday as a tight vote looms. After a few setbacks, inflation in the UK has fallen sharply this year, hitting the bank’s 2% target in the past two months. But BoE policymakers remain concerned about the still high services inflation and the very slow decline in wage growth.

The latest commentary suggests there is no unanimity within the MPC on whether or not to cut rates in August and market opinion is split 50-50 too. But there have been subtle hints from policymakers that rates don’t need to stay as high as the current 5.25% to maintain restrictive policy so the odds are tilted somewhat towards a 25-bps reduction.

What may ultimately sway MPC members’ minds is the bank’s updated quarterly projections. If they decide to start easing, it will likely be a close call and be communicated as a hawkish cut amid the persisting upside risks to inflation. So, despite a cut not being fully priced in, the pound may not necessarily slide much on the news.

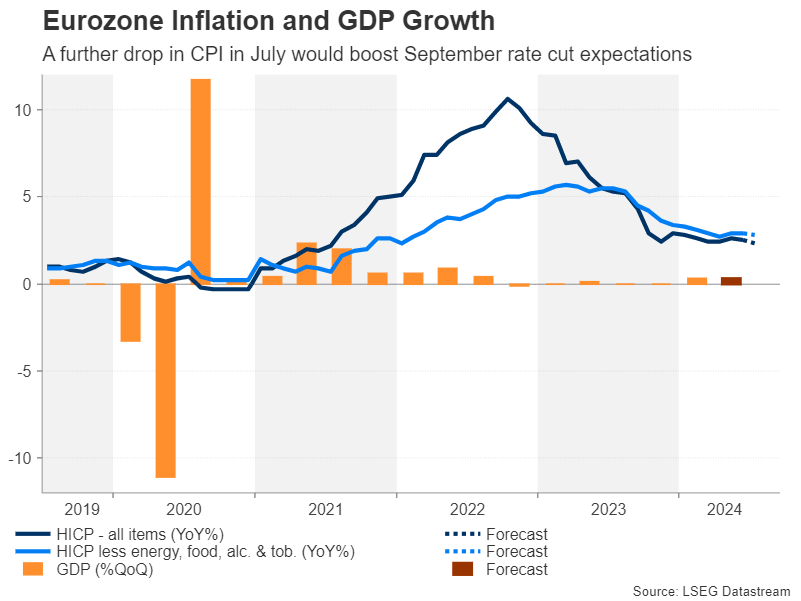

Eurozone CPI eyed as economic rebound falters

Over in the continent, the Eurozone’s economic recovery appears to have hit a roadblock. But figures out on Tuesday are expected to show that for the three-month period to June, GDP expanded by a respectable 0.3% q/q, pushing the annual growth rate up to 0.6%.

For the European Central Bank, the more up-to-date PMI surveys, which deteriorated further in July, will likely take precedence, especially for the doves who favour another rate cut in September. Wednesday’s flash CPI estimates will therefore be more significant for investors.

There was relief in the June report when headline inflation fell back to 2.5% y/y and there could be more good news for July. The harmonized index of consumer prices is projected to ease further to 2.3% y/y in July, coming within short distance of the ECB’s 2% goal.

The impact of such a drop will be lessened if there isn’t a similar decline in the underlying measures of inflation. Thus, for the euro to come under significant pressure against the dollar, there will have to be progress in core inflation too.

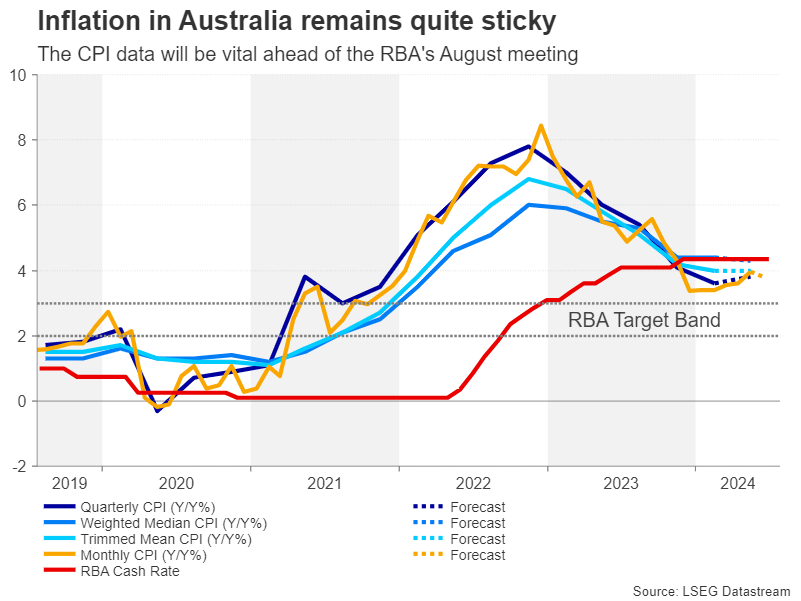

Australian CPI might pave way for RBA hike

It will be an unusually busy period for Australian data next week, with releases ranging from retail sales to trade. The highlight, though, will be Wednesday’s quarterly CPI readings.

Inflation in Australia has bucked the global trend and has been edging higher all year, reaching 4.0% y/y in May in the monthly measure. The Reserve Bank of Australia has been hesitant about raising interest rates again, but the more reliable and complete quarterly numbers may just convince policymakers that further tightening is needed. And with the next meeting coming up on August 6, the timing couldn’t be better.

The latest risk-off episode in the markets has been devastating for the Australian dollar so a hotter-than-expected set of CPI figures could provide the currency with a much-needed boost. Also on aussie traders’ radar will be Chinese manufacturing PMIs out on Wednesday and Thursday, amid the ongoing pessimism about China’s economy.

Canadian GDP Growth to Slow, U.S. Fed to Stand Pat

The week ahead is a busy one on the data calendar with the release of Canada’s gross domestic product for May and the U.S. Federal Reserve’s decision on interest rates on Wednesday, followed by U.S. payroll employment data on Friday.

Canadian GDP data should continue to point to a weakening economy in Q2. We expect momentum faded in May with output growth unchanged after a stronger 0.3% increase in April. That’s slightly more pessimistic than Statistics Canada’s preliminary estimate for a 0.1% increase, but more in line with early industry readings that flagged a decline in wholesale and retail sales. In June, GDP growth likely weakened further, dipping to an outright contraction. Total hours worked fell by 0.6%, and manufacturing sales contracted by 2.6%. Overall, those monthly readings should leave the Q2 quarterly GDP at an annualized 1.5% from Q1. That’s in line with our tracking of 1.4% and the Bank of Canada’s forecast of 1.5% in their latest July Monetary Policy Report and should point to another decline in output per-capita in Q2 once the increase in population is accounted for.

In the U.S., we expect no change in key interest rate from the Fed’s meeting next Wednesday. Chairman Jerome Powell had refrained from giving any guidance on future policy moves in the last few meetings and other speaking engagements. Instead, he has focused on the central bank’s assessment that employment and inflation risks are moving into a better balance—but just not to the point that would spur interest rate cuts. There is the risk of a slightly more dovish lean, given the progress with consumer price index readings in the summer alongside normalization in the labour market backdrop. The core PCE price index in the U.S. dropped to an annualized 2.9% in Q2 from 3.7% in Q1, in line with slowing in CPI data in May and June. Labour market conditions have softened, with employment growth trending broadly lower and the unemployment rate edging higher – although both to levels that would still be considered historically robust. We expect Friday’s U.S. labour market data will show another 193,000 increase in employment in July, and the unemployment rate staying at 4.1%.

Week ahead data watch

Sunset Market Commentary

Markets

Markets finally took a breather this morning after recent sharp risk-off repositioning especially in equities and interest rates. However, it doesn’t feel as if a sharp, sustained countermove is already in store. Initial ‘gains’ in yields, gradually evaporated. Equities are rebounding about 0.75% (Eurostoxx50 & S&P500) but one has the feeling that some kind of sell-on-upticks dynamics could still kick in. Investors are pondering the chances of a ‘global’ economic slowdown and the impact of any subsequent monetary policy response/easing. At least for now, markets clearly see little reason to profoundly scale back recent pricing of the start of a genuine (Fed) easing cycle in a not that distant future (September) with policy normalization to continue in Q4. Regarding the data, sentiment today was challenged by the publication of July US income and spending data and the release of the closely watched price deflators. June personal income was weaker than expected (0.2% vs 0.4% expected) and the July figure was downwardly revised. Spending (0.3% from upwardly revised 0.4 M/M in May) and the price deflators (headline 0.1% M/M and 2.5% Y/Y from 2.6%, core 0.2% M/M and 2.6% Y/Y) were very close to expectations. The reaction post the release showed that south remains the path of the least resistance for US yields. From a marginal rise just before the release, US yields currently again decline between 5.5 bps (5-y) and 4.0 bps (30-y), building on recent steepening trend. The 2-y yield (4.38%) struggles to avoid a close below the 4.40% support. German bunds slightly underperform Treasuries but yields also reversed an early modest rise with yields again ceding 3.0 bps (2-y) to 1.0 bp (30-y). The EMU 2-y swap also fails to regain the 3.0% mark (2.95%). Still, in the monthly ECB expectations survey, EMU consumers at least only see a gradually further easing of inflation (cf infra). Uncertainty on global growth also prevents any meaningful rebound in in the oil price (Brent $ 81.5 p/b).

On FX markets, the dollar still shows an unconvincing momentum. DXY declines marginally (104.26). USD/JPY initially tried to regain some further ground, but the rebound was blocked after the release of the US data (currently 153.9). EUR/USD gains marginally (1.0865). Some calm returned for hard-beaten mostly smaller & often commodity related currencies (NZD, AUD, CAD NOK, SEK) but the rebound if any mostly remains technically insignificant. The Aussie dollar (AUD/USD 0.6563) and the Norwegian krone (EUR/NOK 11.91) look best positioned for some bottoming out process. The Swiss franc (EUR/CHF 0.9584) makes a small step backward as the safe haven bid eases. UK yields also extend their decline going into next week’s BoE policy meeting (2-y -3.3 bps,10-y -5.5 bps). Sterling holds yesterday’s loss with EUR/GBP trading near 0.844. The test of the key 0.84/0.8383 support is again rejected.

News & Views

The ECB’s consumer inflation survey showed their expectations for price increases have remained unchanged. The one-year ahead gauge matched last month’s 2.8% reading, which was the lowest since September 2021. The medium-term indicator (three years forward) came in at an unaltered 2.3% and both measures remained below the perceived past inflation rate (from 4.9% to 4.5%). European consumers anticipate nominal incomes to grow at a slightly quicker pace than in May (1.4% from 1.2%) while spending over the next 12 months is seen rising by 3.3%. Their expectations for growth turned more negative, from -0.8% to -0.9% but the unemployment rate was seen slightly lower over the same period, from 10.7% to 10.6% - a series low. In June consumers expected the price of their home to increase by 2.7% over the next 12 months, which was slightly higher than in May (2.6%), and mortgage rates of 4.8% (vs 4.9% in May).

Norwegian retail sales were came in sub-par in June. Turnover dropped a whopping 5.1% m/m, the sharpest monthly drop since August 2021, to be -3% lower y/y. All categories except for sales of ICT equipment dropped significantly but, despite the size, is no reason for concern. This month’s decline followed an exceptionally strong month of May, which saw an upward revision to 4.7% m/m (from 3.2%). On a quarterly basis, sales were nevertheless up 1% compared to Q1 of this year. The Norwegian krone appreciated slightly today (EUR/NOK 11.90) but that move is at least partially inspired by a less sour/improved market sentiment compared to the previous days/weeks.

Graphs

UK 2-yr yield drops to lowest level in more than a year as markets ponder chance of BoE rate cut next week.

Brent oil struggles as markets see risk to global demand due to mediocre growth.

US 10-y yield still testing the 4.20% support area as markets prepare for genuine (Fed) easing cycle.

EUR/CHF: franc rebound taking a breather as risk-off eases (for now).

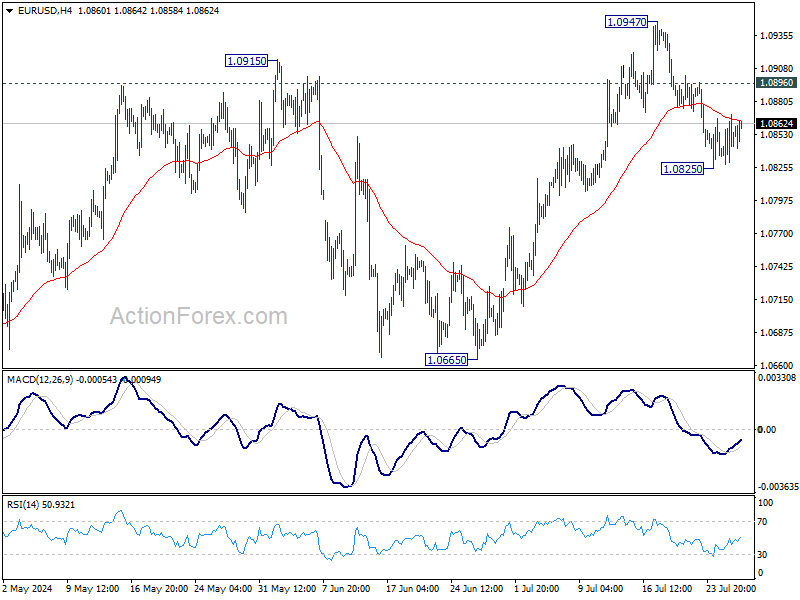

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0825; (P) 1.0848; (R1) 1.0867; More.....

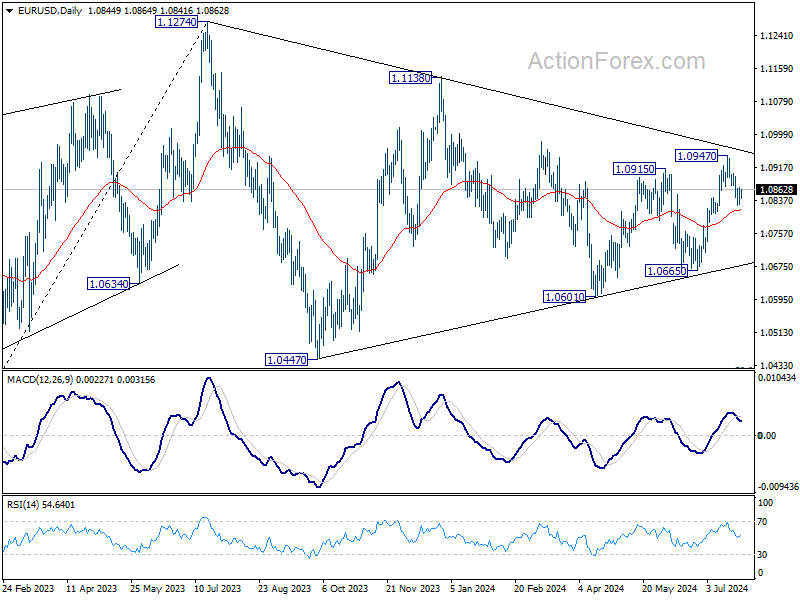

Intraday bias in EUR/USD remains neutral at this point. Deeper fall is in favor as long as 1.0896 minor resistance holds. Below 1.0825 will target 55 D EMA (now at 1.0813). Sustained break there will argue that whole rebound from 1.0601 has completed with three waves up to 1.0947, and target 1.0601/0665 support zone. Nevertheless, break of 1.0896 will bring retest of 1.0947 resistance instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.