Sample Category Title

USD/JPY Maintains a Clear Range Ahead of Japanese CPI – FX Analysis

USD/JPY is often playing tricks on FX traders, and this time it is completely avoiding volatility after gigantic up-and-down moves.

The Currency pair is known for its erratic price action, highly affected by movements in rates, global trade, and inflation, as well as regional and geopolitical developments, all of which have been severely affected since the beginning of the US-Iran conflict.

Seen as a major safe-haven currency since the early 2000s, profiting from lower yields in times of panic, the JPY could not find any appeal during this conflict.

Even as stock markets initially sold off, risk-off assets and currencies failed to gain traction, with the US Dollar and WTI Crude drawing all the attention.

Believing the conflict would stay focused on the Middle East, a wider flight to safety was avoided.

But the economic damage to Europe, and in the case of today's USD/JPY outlook, Japan and Asia, is still heavy, and that led to massive rallies in the US Dollar against currencies from these regions.

You can see the strong correlation between USD/JPY and Oil movements in our recent analysis of the pair.

Add to this narrative a striking stall in inflation in Japan, which was the only path to justify a return to less accommodative policy, and Traders really found a natural terrain to race back to Japan shorts.

Recent Japanese CPI data – Courtesy of Trading Economics

The Japanese CPI, releasing tonight at 19:30 (ET), is expected to rebound, as supply-side inflationary pressures could once again slowly push Japanese consumer prices higher.

The Bank of Japan mentioned conflict-led inflation a few times but reportedly still leans toward a pause at the upcoming meeting, while hinting at a higher chance of a 25 bps hike in June to allow for further analysis of the war's impact.

So, unless CPI beats expectations by a lot, this pricing shouldn't change much.

With the second round of talks, delayed for almost a week and a half, set to resume tomorrow and continue throughout the weekend, this will be a decisive moment for the FX pair.

Forming a clear 2,000 pip hesitation range in recent action, traders are waiting to see if a proper peace solution is met (implying a break lower in the range) or if the war is to resume, which would add further chances to revisit 2026 highs (above 160.00).

Let's dive right into an intraday-timeframe analysis for the Gopher – more commonly named, USD/JPY.

USD/JPY Multi-Timeframe Analysis

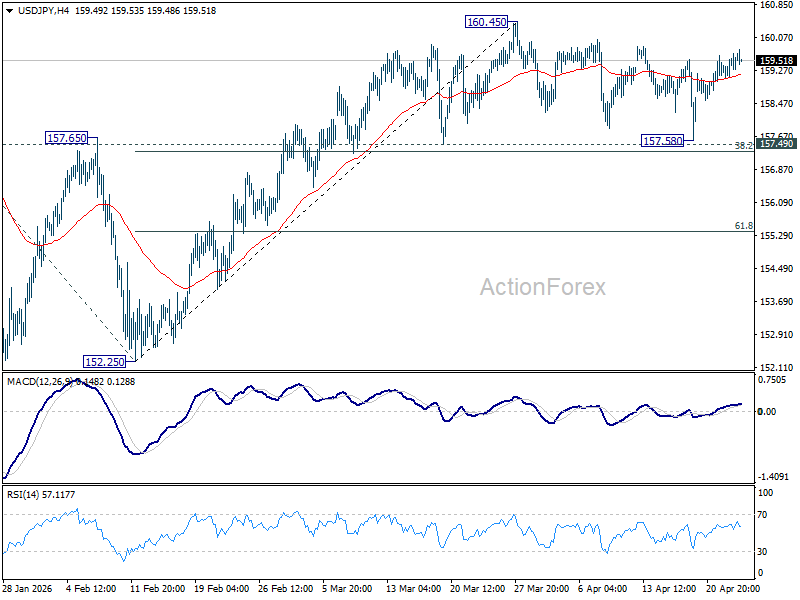

4H Chart

USD/JPY 4H Chart. April 23, 2026 – Source: TradingView

Instead of entering a corrective phase, as was forecasted by the break below key MAs and bull channel, USD/JPY maintained a clearly rangebound picture as the US Dollar completely stalled its correction.

Since reaching new 2026 highs on March 27, the pair has been stuck in a clear 2,000 pip range between 157.50 and 159.50 (+/- 100 pips).

While the consolidation is solid, as seen with the flattening 50 and 200 Moving Averages, traders will have to remain cautious as the narrative could change during the weekend.

Currently at the resistance, USD/JPY has more chances to reject lower, but any headlines regarding a compromised peace process would push for a breakout towards 160.50.

Let's take a closer look.

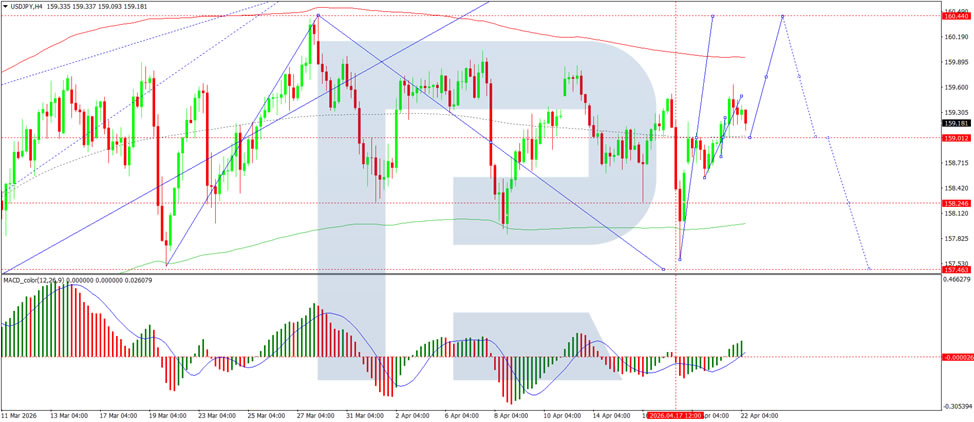

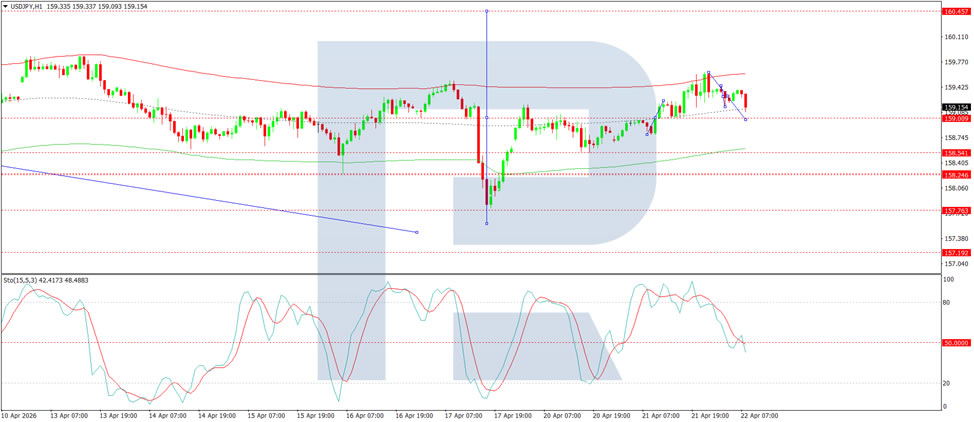

1H Chart and Technical Levels

USD/JPY 1H Chart. April 23, 2026 – Source: TradingView

As can be seen on the 1H timeframe, the range has seen swift up-and-down movement, tumbling to support last Friday and exploding back to retest resistance.

With today's North American session not expected to provide any meaningful change, traders should remain patient.

If the CPI data comes hotter, expect to see a drop below 159.43 (50-Hour MA) which could provide decent sell-stop entries – Extending below 158.80 should see bearish acceleration.

- Watch out if the action breaks 159.80

- The weekend break will provide high volatility movement on Monday, so watch your size ahead of the key developments.

Resistance levels

- 159.50 to 159.70 2026 Major Resistance (range highs)

- 159.78 daily highs

- April 2024 160.00 to 160.40 Major Resistance

- June Mini resistance 160.70 to 161.00

Support levels

- 159.43 (50-Hour MA)

- Mid-range pivot 158.75 bull above, bear below

- December highs Major Pivot 157.50 to 158.00 (range lows)

- 156.00 Pivotal Support

- 155.00 Mini-Support

Safe Trades!

Sunset Market Commentary

Markets

It’s a hard time these days for (economic) analysts and central bankers alike. Their assessment on the current state and the outlook for the economy is conditional to the (until now) unpredictable extent and outcome of the conflict in the Middle East. Hard data often/mostly are outdated at the time of publication. The monthly PMI surveys (and ISM’s in the US) in this context probably provide one of the better, more or less timely pointers on the reaction of a key group of economic agents, the purchasing managers. The outcome of the April EMU PMI was ‘as feared’. The EMU economy is heading toward stagflation. First, the ‘least worse part of the story’. The overall composite PMI declined more than expected from 50.7 to 48.6, the first sub-50 reading, separating growth from contraction, since December 2024, due to a sharp contraction in activity in the (mostly domestic) services sector (47.7). S&P global analyses that the decline in output was broad-based across the region. Interestingly (surprisingly?), activity in the manufacturing sector even improved (52.2 from 51.6, best level in 47 months). However, there is a ‘but’. ‘Some of the upturn reflected reports of customers seeking to secure purchases amid concerns over price rises and supply shortages’. In this respect, manufacturers also see suppliers' delivery times lengthen to the greatest extent since mid-2022. S&P calculated that the decline signals a 0.1% quarterly rate of GDP contraction at the start of Q2. For now the negative impact on employment was limited. Still, overall confidence on the year-ahead outlook, still at a 21 month high in February, in April dropped to lowest since end 2022. The picture regarding growth was far from inspiring. The story on prices is even more worrisome. Both input costs and output prices are rising at the sharpest rates in more than three years. S&P even sees the biggest surge in cost pressures since 2000 if one excludes Covid pandemic era. The rise in costs is also not only due to higher energy prices, but due a wider rise in commodity prices and a growing supply-demand mismatch.

The ‘one million dollar question’ of course is what this means of ECB policy. EMU yields this morning initially added a few bps with Brent oil north of the $100 barrier also adding to the inflationary woes, but for now there is no follow-through price action. EMU swap yields are little changed in a daily perspective. Even so, after reducing ECB rate hike expectations to 1 ½ 25 bps steps by year end on Friday, EMU money markets currently again see a near 90% chance of a June rate hike and more than one additional step by year end. US yields show similar small ‘changes’. US weekly jobless claims rose a slightly higher than expected 214k, but remain at a benign level. The US manufacturing PMI released at the time of finishing this report even improved (composite 52 from 50.3), but with little market impact. After recent rally, gains in (US) equities stall as headlines on the Iran conflict remains highly confusing (S&P 500 and Eurostoxx 50 ceding 0.1%). The dollar ‘enjoys’ a (still modest) safe haven bid (DXY 98.7, EUR/USD 1.169, USD/JPY 159.55).

News & Views

UK activity rose in April with the composite PMI improving to a two-month high of 52, corresponding with a 0.2% quarterly growth rate. This upturn, however, comes with a catch, S&P Global said. It’s reflecting in part a rush to secure purchases ahead of price rises and already-present supply shortages linked to the Iran war. This was most visible in the manufacturing gauge (53.6, 47-month high) but also in services (52, two-month high). Advanced purchasing temporarily lifted industrial orders books while services providers reported fragile demand conditions due to business uncertainty, higher inflationary pressures (transportation costs) and elevated borrowing costs. S&P said these survey details “hint strongly that this [growth] pace cannot be sustained should the crisis persist.” Private sector employment numbers decreased for the 19th month running, be it at the slowest pace since October 2025. Price pressures are strong with manufacturers recording a steep increase in their input prices. Services companies have seen input costs rise at the fastest pace since the survey begin almost 30 years ago on greater fuel costs and wages. This resulted in the sharpest output price increase since February 2023 with both sectors contributing. Optimism for the year ahead fell to its second-weakest since December 2022 on these increasing cost burdens. Despite this ‘better performance’ compared to EMU, UK gilts underperform Bunds with yields rising 1.0 (5-y)-3.5 (30-y) bps. Recent sterling outperformance against the euro slows (EUR/GBP little changed near 0.8665).

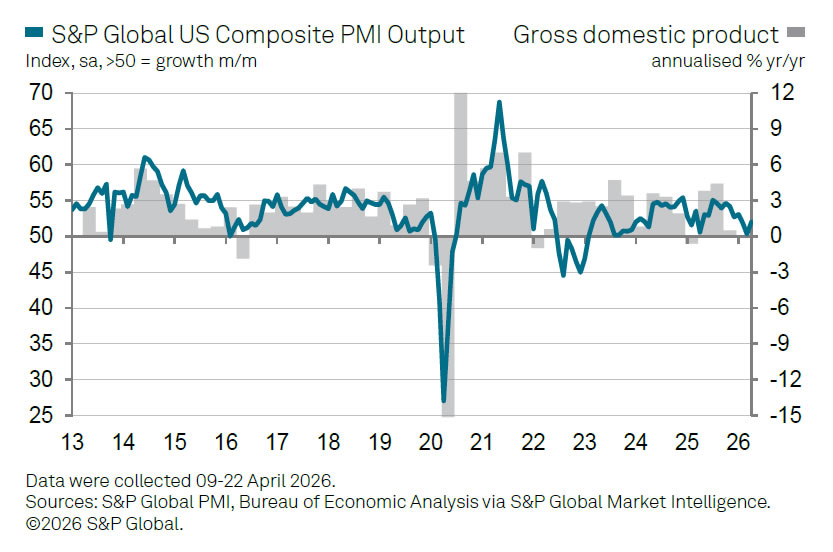

US PMI Signals Sub-1% GDP Growth as Inflation Pressures Intensify

US business activity picked up in April, with the Flash Composite PMI rising from 50.3 to 52.0, a three-month high. The improvement suggests the economy regained some momentum after near-stagnation in March, though the overall pace remains modest. The data is broadly consistent with the economy struggling to sustain annualized growth much above 1%, with the vast services sector acting as the principal drag despite a return to expansion.

Manufacturing led the economy. PMI rose from 52.3 to 54.0, while output jumped from 53.2 to 55.7, the strongest in four years. However, much of the strength appears precautionary. Firms reported “panic” and “emergency” buying of inputs, building inventories ahead of expected supply disruptions and price increases linked to the Middle East conflict and ongoing tariff pressures.

The services sector, by contrast, remains subdued. PMI edged up from 49.8 to 51.3, but demand growth is weak, with hesitancy in spending across travel, finance, and other services. Higher prices and the prospect of tighter financial conditions are acting as a drag on activity, keeping overall growth modest.

At the same time, inflation pressures are accelerating sharply. Input costs and output prices rose at the fastest pace since mid-2022, driven by energy, commodities, and rising wages.

| Indicator | Apr | Mar |

|---|---|---|

| PMI Composite | 52.0 | 50.3 |

| PMI Services | 51.3 | 49.8 |

| PMI Manufacturing | 54.0 | 52.3 |

| Manufacturing Output | 55.7 | 53.2 |

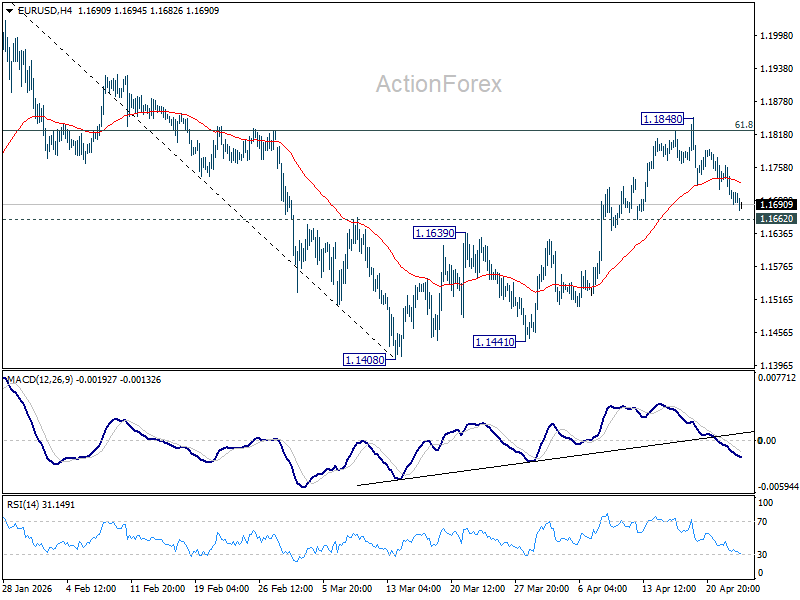

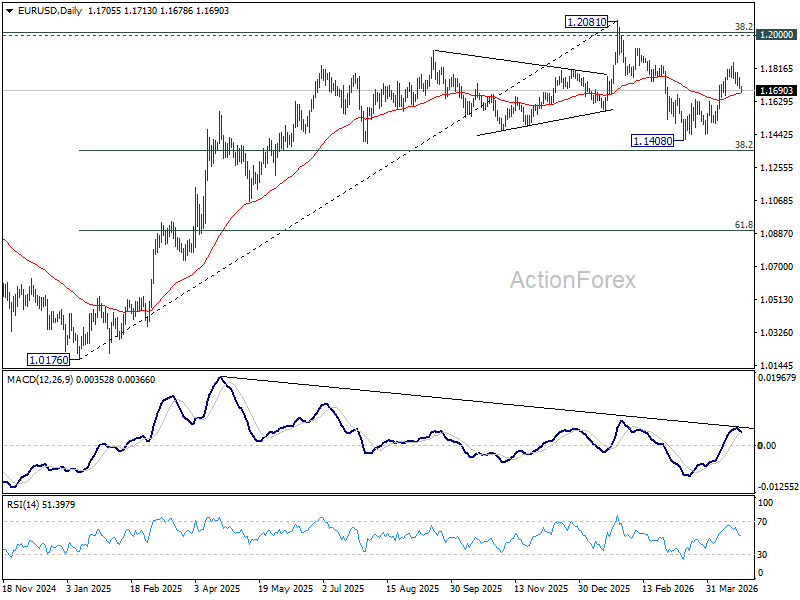

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.1684; (P) 1.1724; (R1) 1.1745; More….

No change in EUR/USD's outlook as it's staying above 1.1662 support. Intraday bias remains on the upside and further rise is still in favor. On the upside, sustained trading above 61.8% retracement of 1.2081 to 1.1408 at 1.1824 will pave the way to retest 1.2081 high. However, firm break of 1.1662 support will bring deeper decline back towards 1.1408 low instead.

In the bigger picture, the strong support from 38.2% retracement of 1.0176 to 1.2081 at 1.1353 suggests that the pullback from 1.2081 is more likely a corrective move. Strong support was also found in 55 W EMA (now at 1.1507). Focus is back on 1.2 key cluster resistance level. Decisive break there will carry long term bullish implications. Nevertheless, break of 1.1408 support will revive the case of medium term bearish trend reversal.

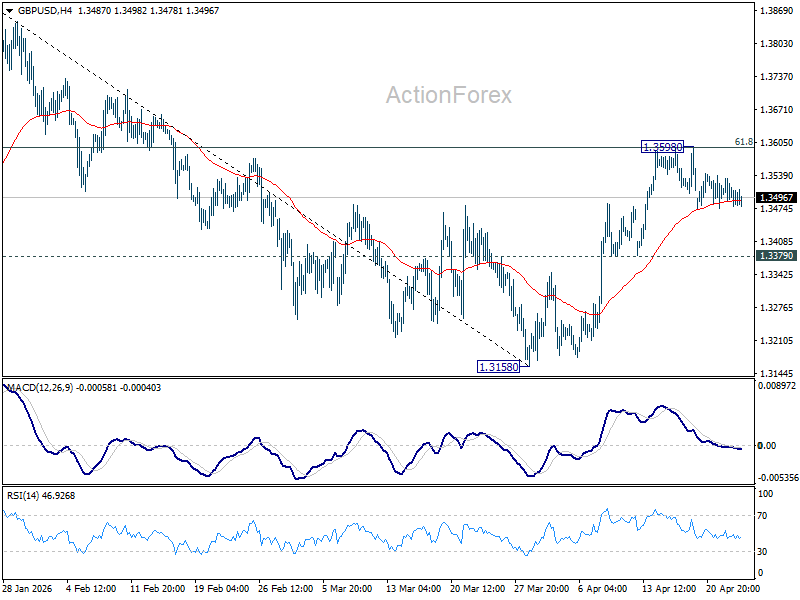

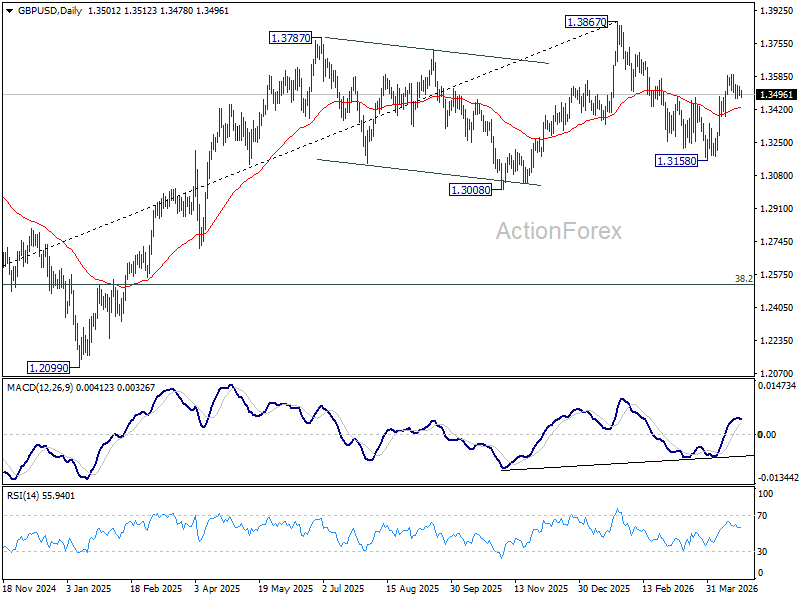

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.3484; (P) 1.3511; (R1) 1.3529; More...

No change in GBP/USD's outlook as it's still extending consolidations from 1.3598 and intraday bias remains neutral. With 1.3379 support intact, further rise is favor. On the upside, sustained break of 61.8% retracement of 1.3867 to 1.3158 at 1.3596 will pave the way to retest 1.3867 high. However, firm break of 1.3379 will bring deeper fall back to 1.3158 low instead.

In the bigger picture, current development suggests that price actions from 1.3867 are merely a corrective pattern within the broader up trend from 1.0351 (2022 low). With 1.3008 support intact, medium term bullishness is maintained and break of 1.3867 is back in favor for a later stage, towards 1.4248 key resistance (2021 high).

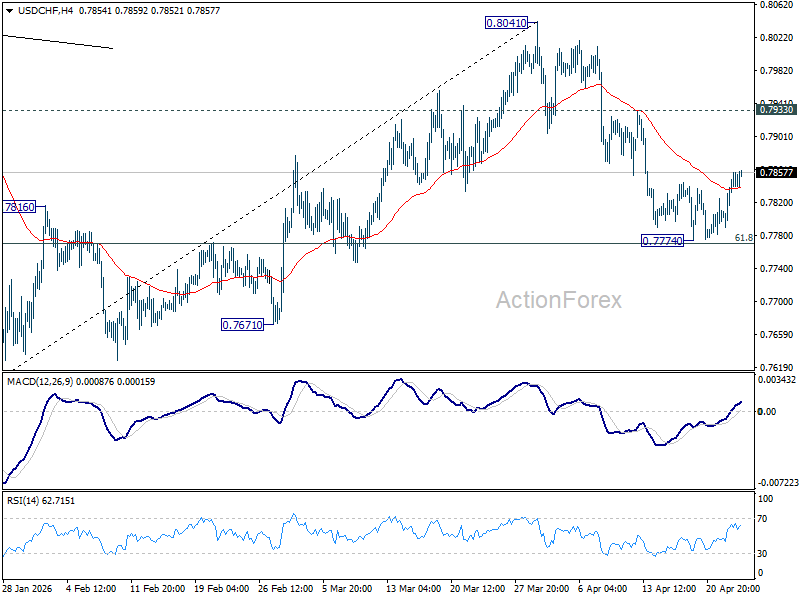

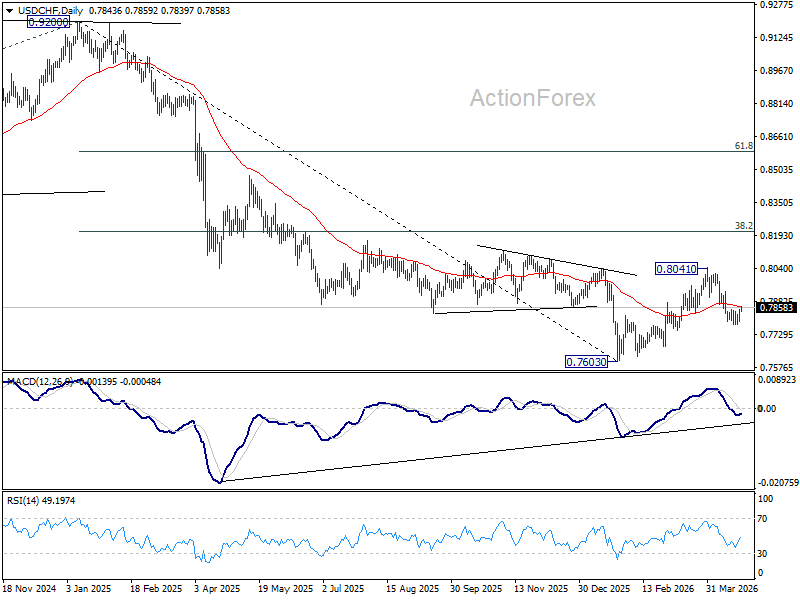

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.7808; (P) 0.7830; (R1) 0.7867; More….

USD/CHF recovers further today but stays well below 0.7933 resistance. Intraday bias remains neutral and further decline is expected. Sustained break of 61.8% retracement of 0.7603 to 0.8041 at 0.7770 will resume the decline from 0.8041 to retest 0.7603 low.

In the bigger picture, rebound from 0.7603 medium term bottom is seen as correcting the fall from 0.9200 only. Rejection by 55 W EMA (now at 0.8059) will affirm this bearish case, and setup down trend resumption to 100% projection of 1.0146 (2022 high) to 0.8332 from 0.9200 at 0.7382 at a later stage. Though, sustained break of 55 W EMA will suggest that it's probably correcting the larger scale down trend from 1.0146 (2022 high).

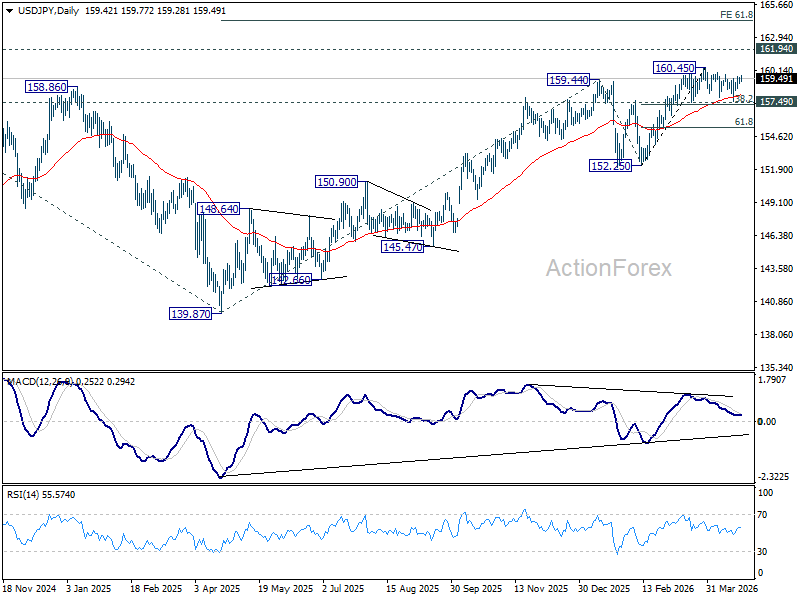

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.20; (P) 159.38; (R1) 159.66; More...

USD/JPY edged higher today, but remains bounded in established range below 160.45. Intraday bias remains neutral and more consolidations could still be seen. Further rise is expected with 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) intact. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.80) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

Global PMIs Diverge as Iran War Shock Spreads: Europe Contracts, UK Front-Loads, Australia Trapped, Japan Absorbs Costs

Global PMI data for April paints a clear picture: the Iran war shock is now feeding through the world economy, but not in a uniform way. Rising energy costs and supply disruptions are hitting all major regions, yet the transmission differs sharply depending on economic structure, demand conditions, and policy constraints. What emerges is not synchronized slowdown, but fragmented stagflation.

The common thread is unmistakable. Across Australia, Japan, the Eurozone and the UK, businesses are reporting surging input costs, longer delivery times, and a growing need to secure supplies ahead of further disruptions. Energy, shipping, and raw materials are the key drivers, with the Strait of Hormuz disruption acting as the central transmission channel. The result is a broad-based cost shock now pushing through supply chains globally.

Nowhere is the impact clearer than in the Eurozone. The Flash Composite PMI fell into contraction, driven by a sharp collapse in services, the weakest since the pandemic period. The region’s heavy reliance on imported energy makes it particularly vulnerable to the “Hormuz gap,” where supply disruption translates quickly into both higher prices and weaker demand. While manufacturing remains in expansion, this strength is largely artificial, driven by stockpiling rather than genuine demand. The Eurozone is already slipping into a stagflationary phase—falling growth alongside rising prices.

The UK is showing a different pattern, but one that may prove equally fragile. PMI data rebounded, With Manufacturing reaching a multi-year high. However, this strength is being driven by front-loaded demand, as firms rush to secure inputs before costs rise further. Price pressures have surged at rates not seen outside the pandemic, and supply delays are intensifying. Growth is being pulled forward, suggesting that the current expansion may not be sustainable.

Australia presents a classic policy trap. The Composite PMI returned to expansion, but manufacturing output remains in contraction, pointing to underlying weakness. At the same time, cost pressures have surged to the highest level in nearly four years. This creates a “nightmare scenario” for the Reserve Bank of Australia: growth is fragile, yet inflation is being pushed higher by external shocks, leaving limited room for policy flexibility.

Japan’s case is more nuanced but no less challenging. Manufacturing is surging, with PMI at 54.9 and output at multi-year highs, supported by export demand and precautionary production. However, services are slowing, and input costs are rising rapidly. The weak Yen is acting as a double-edged sword—boosting exports while sharply increasing the cost of imported energy and raw materials. Rather than broad inflation, Japan is experiencing a margin squeeze, with companies struggling to pass through rising costs.

| Economy | Growth Impact | Inflation Impact | Overall Risk |

|---|---|---|---|

| Eurozone | Sharp slowdown | Strong | Stagflation 🔴 |

| UK | Temporary rebound | Very strong | Delayed slowdown 🟠 |

| Australia | Fragile | Rising | Policy trap 🟠 |

| Japan | Mixed (exports up) | Imported inflation | Margin squeeze 🟡 |

Across all regions, a key feature is the role of stockpiling. Firms are accelerating purchases and building inventories in anticipation of further supply disruptions and price increases. This behavior is temporarily boosting manufacturing activity but is unlikely to be sustained. Once inventories are rebuilt or demand weakens, production could slow sharply.

Inflation dynamics are also shifting. This is no longer just an energy story. While oil remains the initial trigger, price increases are spreading across goods and services, reflecting both supply constraints and precautionary pricing behavior. The risk of second-round effects is rising, particularly in Europe and the UK, where cost pass-through is more immediate.

Central banks are now facing increasingly complex trade-offs. The European Central Bank is confronted with contraction and inflation simultaneously, limiting its policy options. The Bank of England and Reserve Bank of Australia are facing pressure to tighten policy even as growth shows signs of fragility. The Bank of Japan remains more cautious but is not immune to rising cost pressures.

The broader takeaway is clear. The oil shock from the Iran war is not producing a synchronized global slowdown, but a fragmented and uneven adjustment. Europe is already contracting, the UK is front-loading growth, Australia is caught in a policy trap, and Japan is absorbing the shock through costs.

Ultimately, this divergence is likely to define the next phase of the global cycle. Markets will increasingly differentiate between regions based on how they absorb the shock. The common factor remains oil—and as long as supply risks persist, the inflationary pressure will continue to shape both policy and market direction.

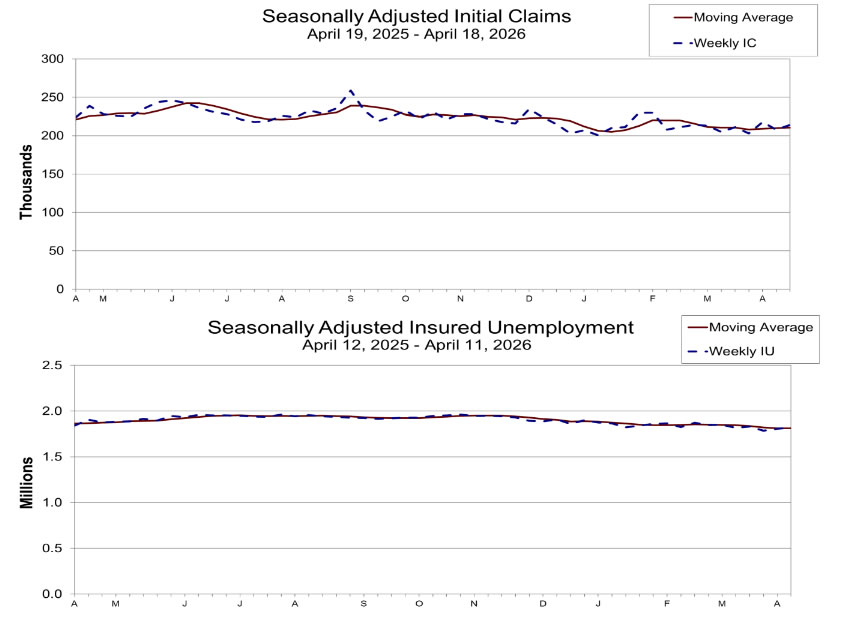

US Initial Unemployment Claims Edge Higher to 214k

US initial jobless claims ticked up by 6k to 214k in the week ending April 18, above expection of 210k. Four-week average also edged higher to 210.75k. Read More.

UK PMI Composite rises to 52.0 and Manufacturing Surges to 47-Month High

PMI data shows the UK economy rebounding, but inflation pressures are rising fast. The recovery may not last if the crisis drags on. Read More.

Eurozone PMI Composite Falls to 48.6, Signals -0.1% GDP Contraction in Q2

Eurozone PMI drops below 50 as war-driven energy costs hit services and push inflation higher, signaling -0.1% GDP contraction. Read More.

Japan PMI Composite Falls to Four-Month Low, Out Prices Hit Record

Manufacturing is driving Japan’s growth, but services are losing momentum and costs are rising fast. The divergence is becoming harder to ignore. Read More.

Australia Composite PMI Back in Expansion, Price Pressures Highest in Nearly Four Years

Australia PMI Composite returned to growth at 50.1 in April, led by services rebound. Manufacturing output weakened while rising fuel and shipping costs lifted inflation pressures to highest in nearly four years. Read More.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 159.20; (P) 159.38; (R1) 159.66; More...

USD/JPY edged higher today, but remains bounded in established range below 160.45. Intraday bias remains neutral and more consolidations could still be seen. Further rise is expected with 157.49 cluster support (38.2% retracement of 152.25 to 160.45 at 157.31) intact. On the upside break of 160.45 will target a retest on 161.94 high. However, firm break of 157.31/49 will bring deeper fall back to 61.8% retracement at 155.38 next.

In the bigger picture, outlook is unchanged that corrective pattern from 161.94 (2024 high) should have completed with three waves at 139.87. Larger up trend from 102.58 (2021 low) could be ready to resume through 161.94. This will remain the favored case as long as 55 W EMA (now at 153.80) holds. Firm break of 161.94 will pave the way to 61.8% projection of 102.58 to 161.94 from 139.87 at 176.75.

US Initial Unemployment Claims Edge Higher to 214k

US initial jobless claims ticked up by 6k to 214k in the week ending April 18, above expectation ion of 210k. Four-week average also edged higher to 210.75k.

Continuing claims rose by 12k to 1.821M in the week ending April 11, suggesting a modest increase in the number of people staying on unemployment benefits. Four-week moving average of continuing claims rose 1k to 1.812M.

EUR/USD Falls for Third Day as Geopolitics and Strong Dollar Dictate Terms

EUR/USD has declined steadily, falling to 1.1688 on Thursday. The US dollar has returned to ten-day highs amid a lack of progress in US-Iran peace talks, boosting demand for the currency as a safe-haven asset.

The Strait of Hormuz remains effectively closed. Tehran continues to control this strategically vital waterway, with reports indicating it has previously seized two vessels in the area. At the same time, the US blockade of Iranian ports persists, contributing to higher energy prices and increasing risk for inflation.

Meanwhile, US President Donald Trump stated that the current truce will remain in force indefinitely, as Washington awaits a new peace proposal from Iran.

Investors remain concerned about US inflation, reinforcing expectations that the Federal Reserve will keep interest rates unchanged for the remainder of the year. Earlier, Fed nominee Kevin Warsh emphasised the importance of maintaining the central bank's independence from the White House.

Market focus now shifts to weekly jobless claims and PMI data, which should provide further insight into the outlook for the US economy.

Technical Analysis

On the H4 chart, EUR/USD is trading within a consolidation range around 1.1736, currently extending down to 1.1693. The pair is likely to move lower towards 1.1680. The MACD indicator supports this scenario, with its signal line below zero and pointing firmly downwards, indicating sustained bearish momentum.

On the H1 chart, EUR/USD is developing a move lower towards 1.1680. A corrective rebound to 1.1711 may follow, before a further decline towards 1.1620. The Stochastic oscillator confirms this view, with its signal line below 20 and pointing firmly downwards, suggesting continued short-term downside pressure.

Conclusion

EUR/USD has declined for a third consecutive session amid geopolitical tensions and a stronger dollar. The lack of progress in US-Iran peace talks, combined with Tehran's control over the Strait of Hormuz and the ongoing US blockade of Iranian ports, has kept energy prices elevated and inflation risks in focus. Trump's indication that the truce will remain in place indefinitely, pending a new proposal from Iran, offers little immediate relief. With markets now pricing in no Fed rate cuts this year and key US data approaching, the euro remains under pressure. Technical signals suggest further downside towards 1.1680, and potentially to 1.1620 in the near term.