Sample Category Title

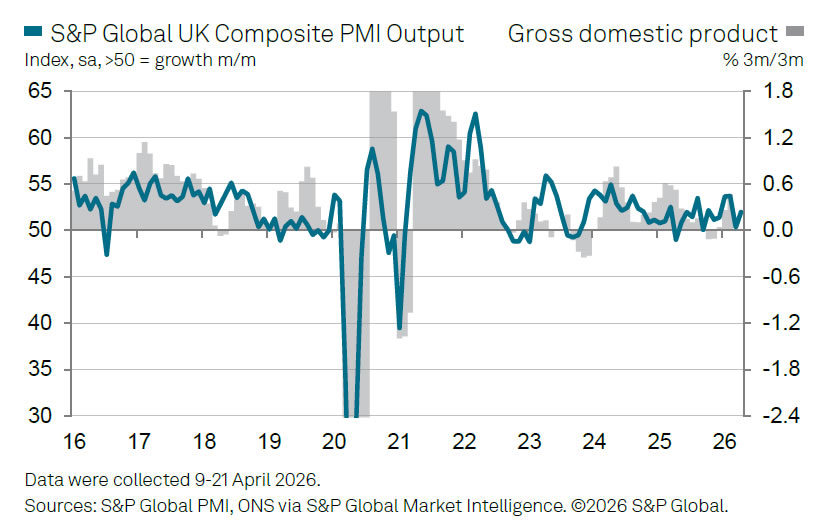

UK PMI Composite rises to 52.0 and Manufacturing Surges to 47-Month High

UK business activity picked up in April, with the Flash PMI Composite rising from 50.3 to 52.0, a two-month high. Services activity rose from 50.5 to 52.0. Manufacturing PMI jumped from 51.0 to 53.6, the highest level in nearly four years, with output returning to expansion at 51.8, up from 49.2. However, much of this strength appears to be driven by front-loaded demand, as firms rush to secure inputs and build inventories ahead of expected supply disruptions.

That urgency is being fueled by rising costs. Price pressures have surged at one of the fastest rates outside of the pandemic period, driven not only by higher energy prices but also broader supply concerns. Supply chain delays have also intensified, reaching levels rarely seen outside crisis periods, adding further upward pressure to prices.

The survey underscores the increasingly difficult trade-off facing the Bank of England. The sharp spike in price pressures is likely to intensify calls for further rate hikes to contain inflation. However, policymakers cannot ignore the growing signs of fragility in demand and confidence.

While April’s PMI points to a modest rebound from March, consistent with around 0.2% quarterly growth, the underlying details—softening employment, weaker sentiment, and supply-driven activity—suggest that this pace may prove short-lived if the crisis persists.

| Indicator | Apr | Mar |

|---|---|---|

| PMI Composite | 52.0 | 50.3 |

| PMI Services | 52.0 | 50.5 |

| PMI Manufacturing | 53.6 | 51.0 |

| Manufacturing Output | 51.8 | 49.2 |

| GDP Signal | ~0.2% qoq | Flat |

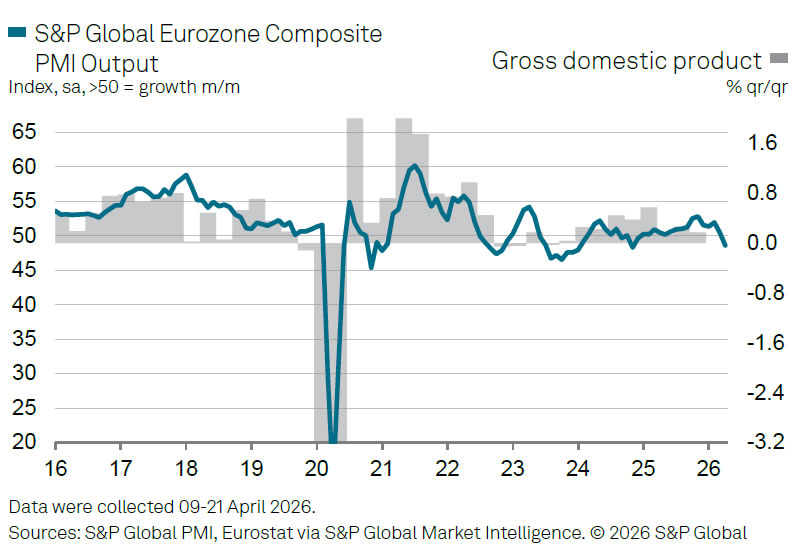

Eurozone PMI Composite Falls to 48.6, Signals -0.1% GDP Contraction in Q2

Eurozone business activity slipped back into contraction in April, with the Flash Composite PMI dropping from 50.7 to 48.6, a 17-month low. The downturn was driven primarily by a sharp deterioration in the services sector, where activity fell from 50.2 to 47.4, the weakest level in over five years.

The services slump highlights the growing impact of the Middle East conflict on the broader economy. Rising energy costs and supply disruptions are weighing heavily on demand, pushing activity down at a pace not seen since the pandemic period. The data suggests the Eurozone is already entering a mild contraction, with GDP expected to shrink slightly by -0.1% in the second quarter.

In contrast, manufacturing continues to show resilience. Output edged up from 52.0 to 52.2, while the headline PMI rose to from 51.6 52.2, the highest in nearly four years. However, this strength appears less encouraging beneath the surface. Much of the growth is being driven by "stock building" as firms rush to secure inputs ahead of further price increases and supply shortages.

Price pressures are intensifying sharply. Input costs and output prices have surged at the fastest rates since 2000 outside of the pandemic, reflecting higher energy prices and broader commodity inflation.

| Indicator | Apr | Mar |

|---|---|---|

| PMI Composite | 48.6 | 50.7 |

| PMI Services | 47.4 | 50.2 |

| Manufacturing PMI | 52.2 | 51.6 |

| Manufacturing Output | 52.2 | 52.0 |

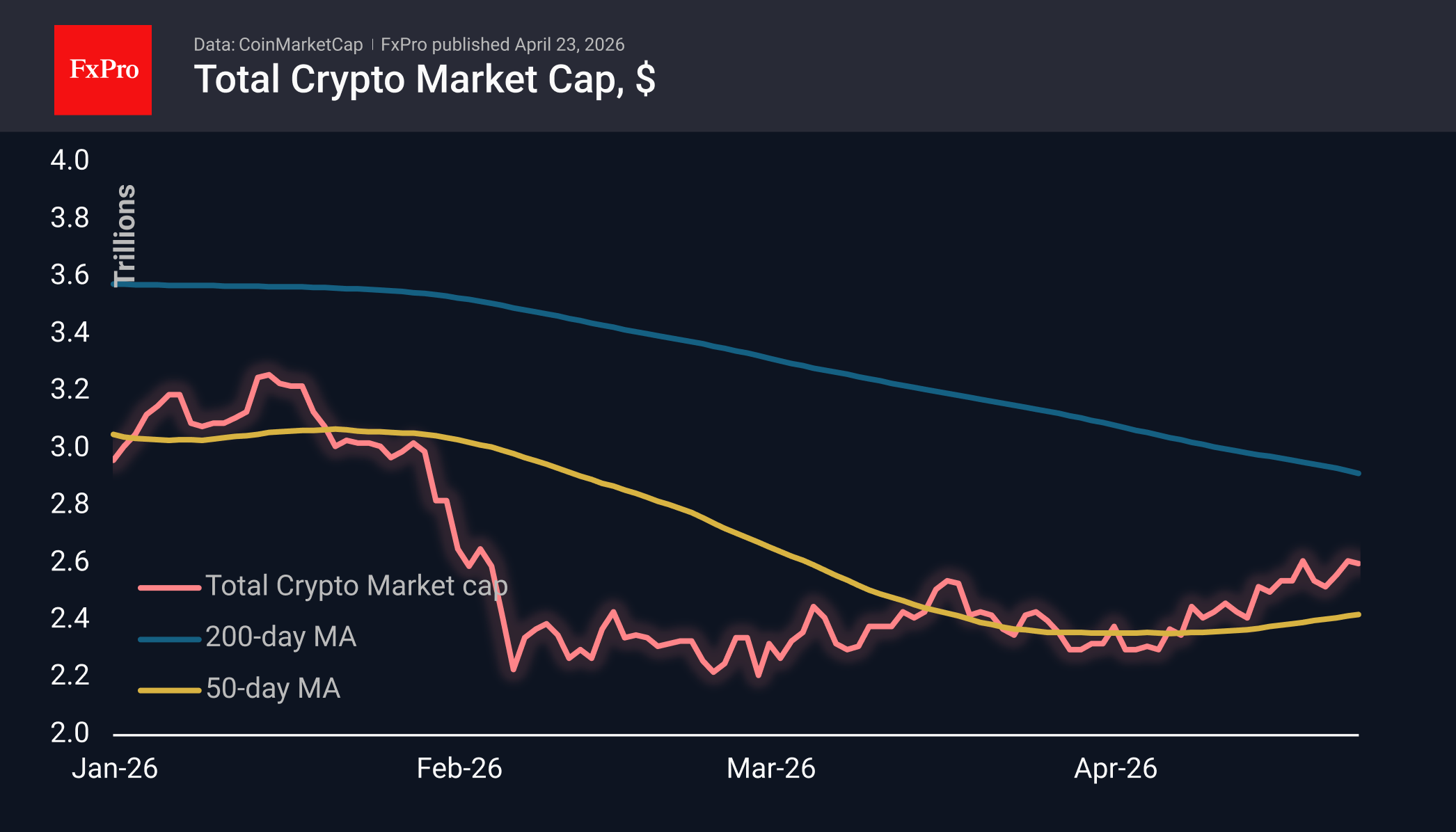

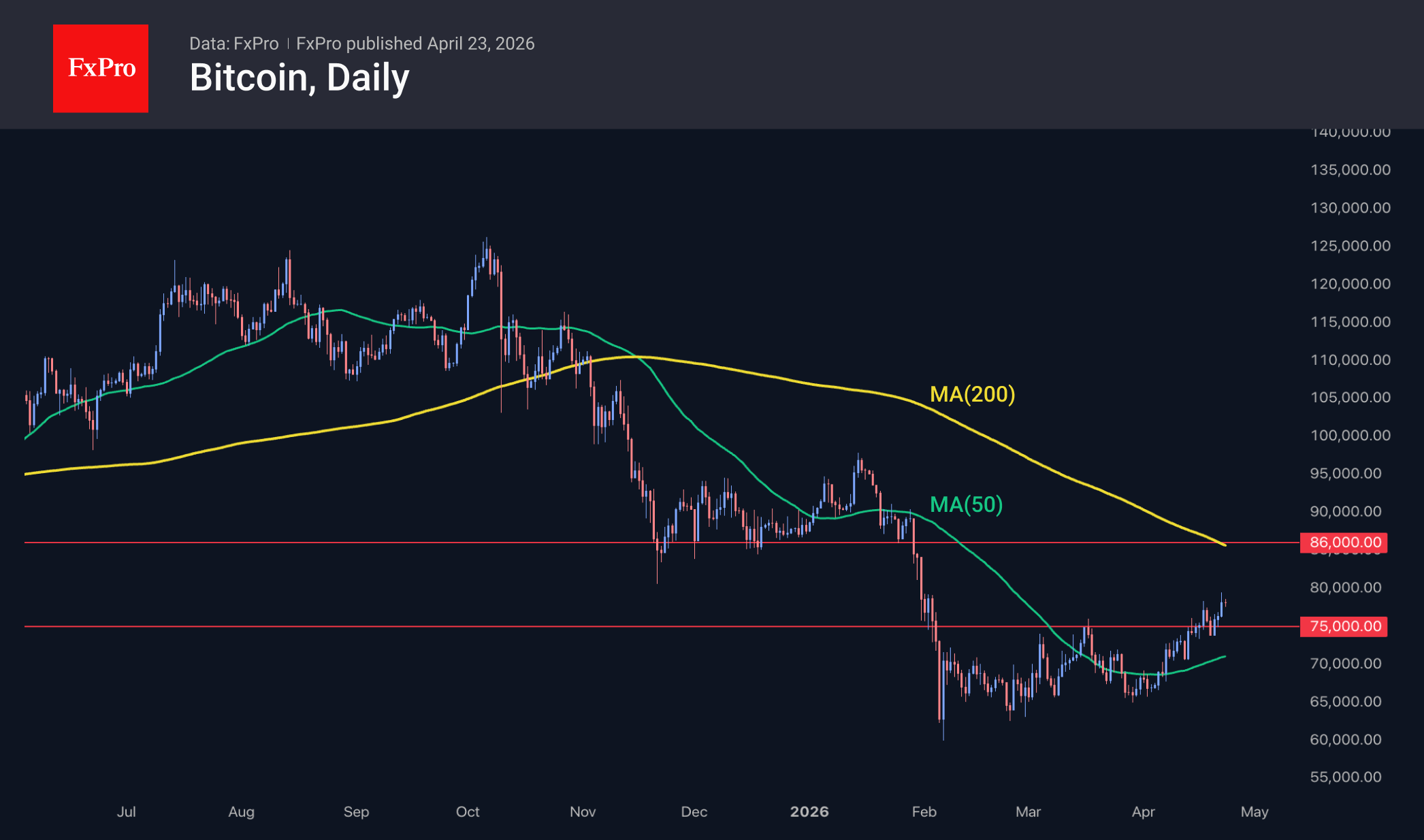

Crypto Market Pauses as Bitcoin Holds Firm

Market Overview

The crypto market capitalisation has fallen by 0.8% over the past 24 hours to $2.6 trillion, driven by pressure on altcoins, while Bitcoin has been pulling the market upwards, a relatively unusual situation. Leading the day’s gains with fairly modest figures were Bitcoin (+0.4%), Hedera (0%) and Aptos (0%). The corrective pullback is more pronounced, with losses of 5% for Dash, 4.9% for Theta and 4.8% for Basic Attention Token.

Sentiment continues to improve rapidly, with the corresponding index rising to 46 — a high not seen in over three months.

On Wednesday evening, Bitcoin briefly exceeded $79K, confirming our view of relatively weak resistance in the $75–86K range. This was the positive side of the close correlation with traditional financial markets. The flip side of this correlation was a pause in growth as key indices pulled back from all-time highs, causing the leading cryptocurrency to retreat to the $78K range.

News Background

The Volo liquid staking protocol on the Sui blockchain lost $3.5 million due to a hack. According to estimates by Memento Research, April was the worst month for the decentralised finance (DeFi) sector in terms of losses. The largest incidents involved the Drift and Kelp protocols, with combined losses approaching $600 million.

Within a few days of the Kelp hack, users withdrew $15.1 billion from the Aave lending protocol, notes EmberCN. Aave, the largest decentralised lending protocol, found itself at the centre of a systemic DeFi crisis after hackers used it to withdraw funds stolen from Kelp.

Tron founder Justin Sun has filed a lawsuit in a California federal court against Donald Trump’s family crypto platform, World Liberty Financial, claiming that his WLFI tokens were frozen without cause and threatened with destruction.

New York has sued crypto exchanges Coinbase and Gemini over contracts on the prediction market that violate gambling laws. The lawsuit follows several similar proceedings in other states. There is a possibility that the case will reach the US Supreme Court.

Trump’s nominee for Fed chair, Kevin Warsh, expressed support for cryptocurrencies during his testimony before the US Senate. According to him, digital assets “have already become an integral part of the US financial services industry”.

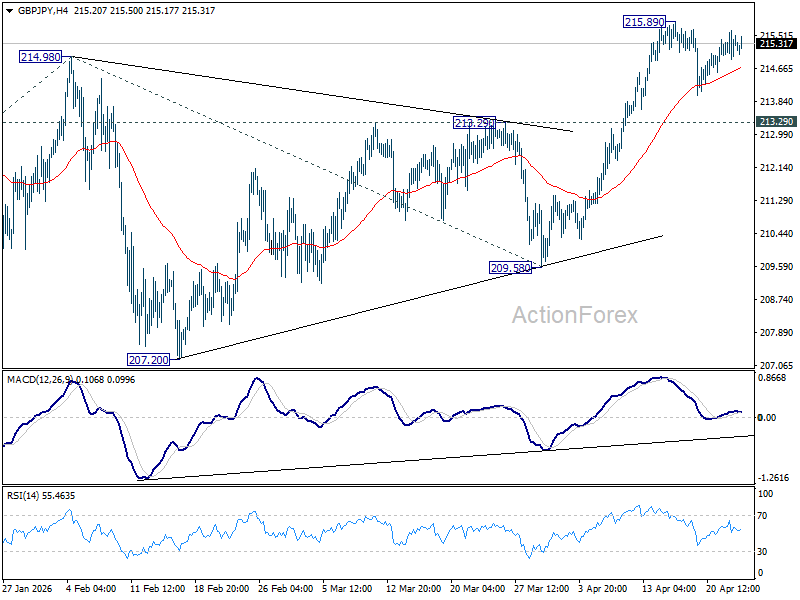

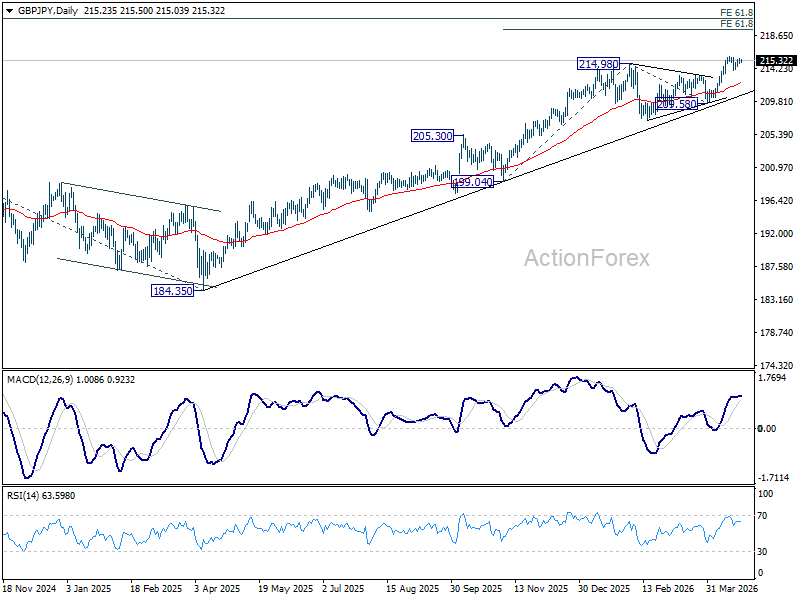

GBP/JPY Daily Outlook

Daily Pivots: (S1) 214.96; (P) 215.31; (R1) 215.71; More...

GBP/JPY is still extending consolidations below 215.89 and intraday bias remains neutral. Further rise is expected as long as 213.29 resistance turned support holds. Firm break of 215.89 will resume larger up trend to 61.8% projection of 199.04 to 214.98 from 209.58 at 219.43.

In the bigger picture, up trend from 123.94 (2020 low) is still in progress. Firm break of 214.98 will target 61.8% projection of 148.93 (2022 low) to 208.09 (2024 high) from 184.35 at 220.90. This will remain the favored case as long as 55 W EMA (now at 204.83) holds, even in case of another deep pullback.

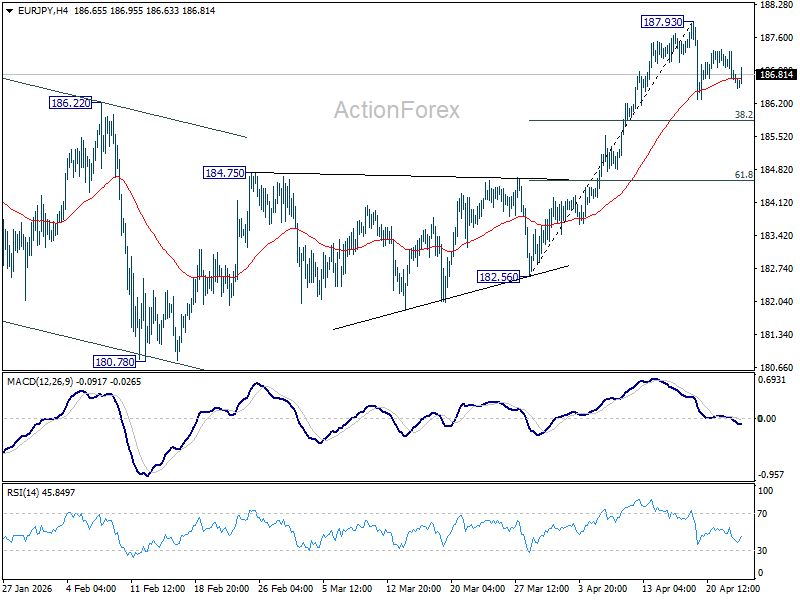

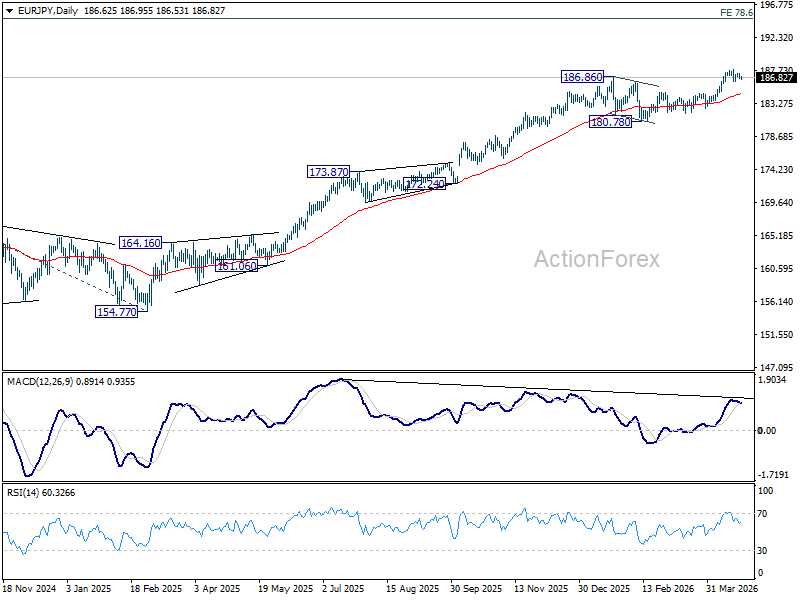

EUR/JPY Daily Outlook

Daily Pivots: (S1) 186.46; (P) 186.90; (R1) 187.14; More...

Intraday bias in EUR/JPY stays neutral as consolidations continue below 187.93. Another fall might be seen to 38.2% retracement of 182.56 to 187.93 at 185.87. But strong support would be seen there to bring rebound. On the upside, though, break of 187.93 will resume larger up trend.

In the bigger picture, up trend from 114.42 (2020 low) is in progress Next target is 78.6% projection of 124.37 (2022 low) to 175.41 (2025 high) from 154.77 at 194.88 next. For now, medium term outlook will stay bullish as long as 180.78 support holds, even in case of deeper pullback.

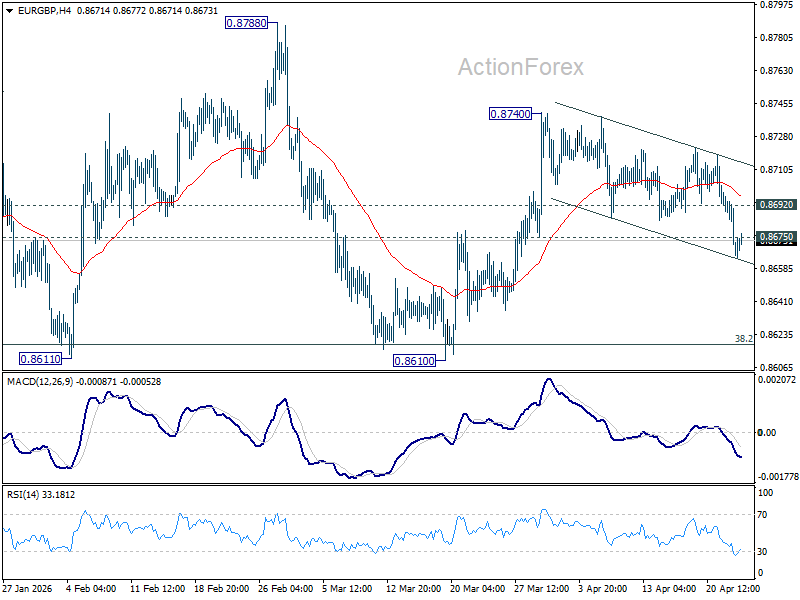

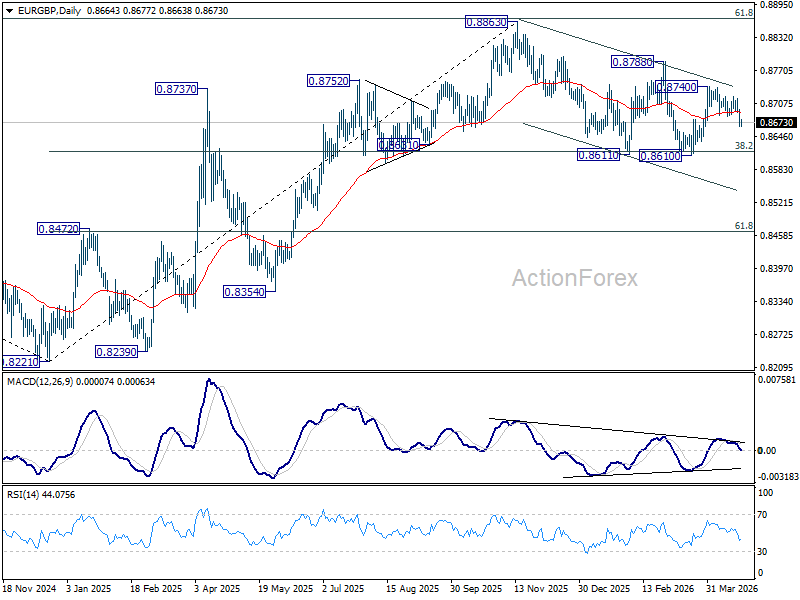

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8657; (P) 0.8680; (R1) 0.8693; More…

Intraday bias in EUR/GBP is back on the downside with break of 0.8675 support. Rebound from 0.8610 could have completed at 0.8740 already. Deeper fall would be seen back to retest 0.8610 low. On the paused, above 0.8692 minor resistance will turn intraday bias neutral again first.

In the bigger picture, strong support was seen again from 38.2% retracement of 0.8821 to 0.8863 at 0.8618. Break of 0.8788 resistance will argue that larger rise from 0.8221 might be ready to resume through 0.8863 (2025 high). Nevertheless, sustained trading below 0.8618 should confirm bearish reversal, and bring deeper fall to 61.8% retracement at 0.8466 at least.

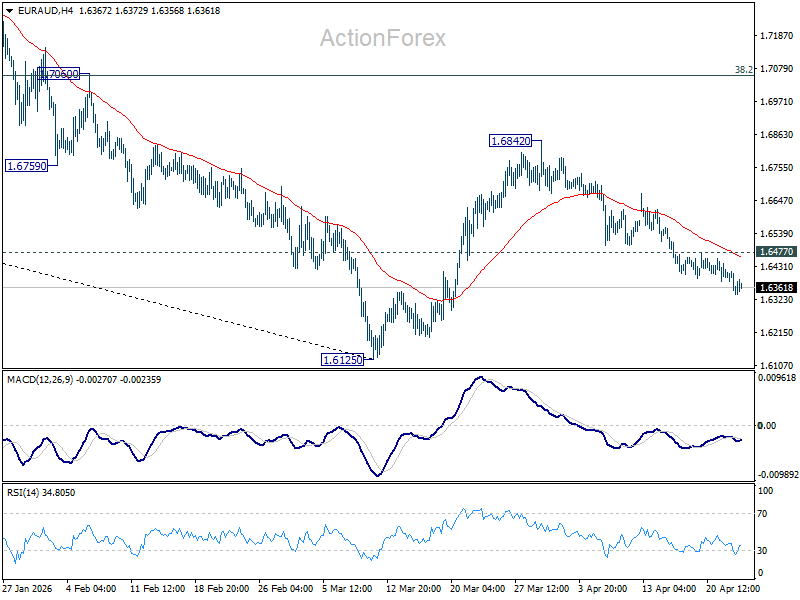

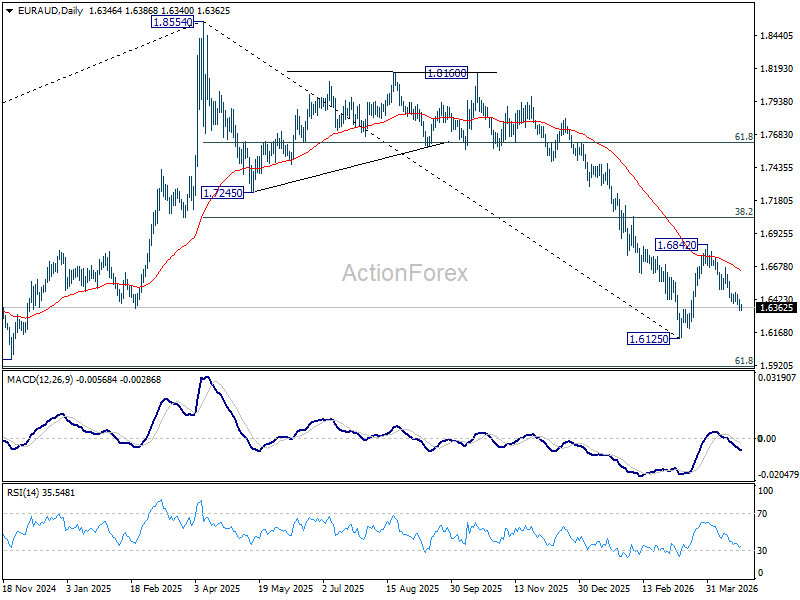

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6318; (P) 1.6378; (R1) 1.6412; More...

EUR/AUD's fall from 1.6842 is in progress and intraday bias remains neutral. Deeper decline should be seen to retest 1.6125 low. Firm break there will resume whole down trend from 1.8554 to 1.5913 fibonacci level next. On the upside, above 1.6477 minor resistance will turn intraday bias neutral first.

In the bigger picture, fall from 1.8554 (2025 high) is in progress and deeper decline should be seen to 61.8% retracement of 1.4281 to 1.8554 at 1.5913, which is slightly below 1.5963 structural support. Decisive break there will pave the way back to 1.4281 (2022 low). For now, risk will stay on the downside as long as 55 W EMA (now at 1.7131) holds, even in case of strong rebound.

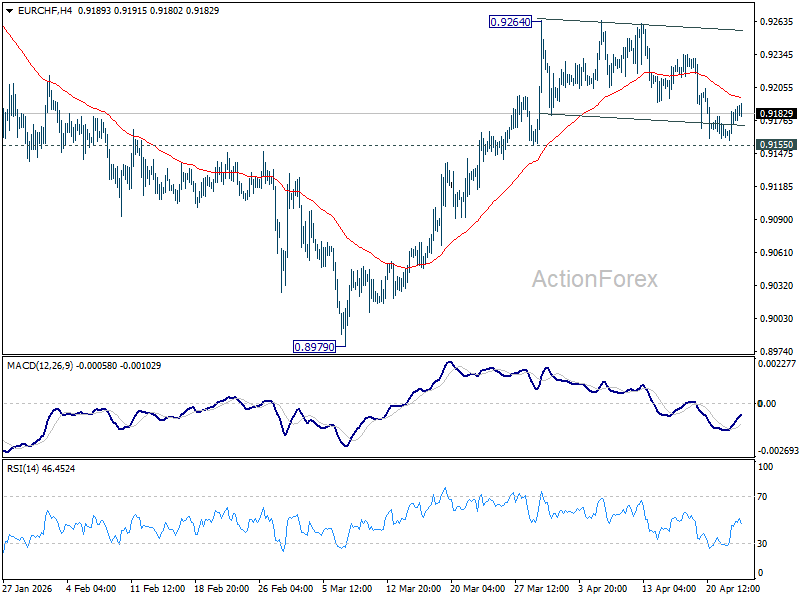

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9166; (P) 0.9179; (R1) 0.9198; More....

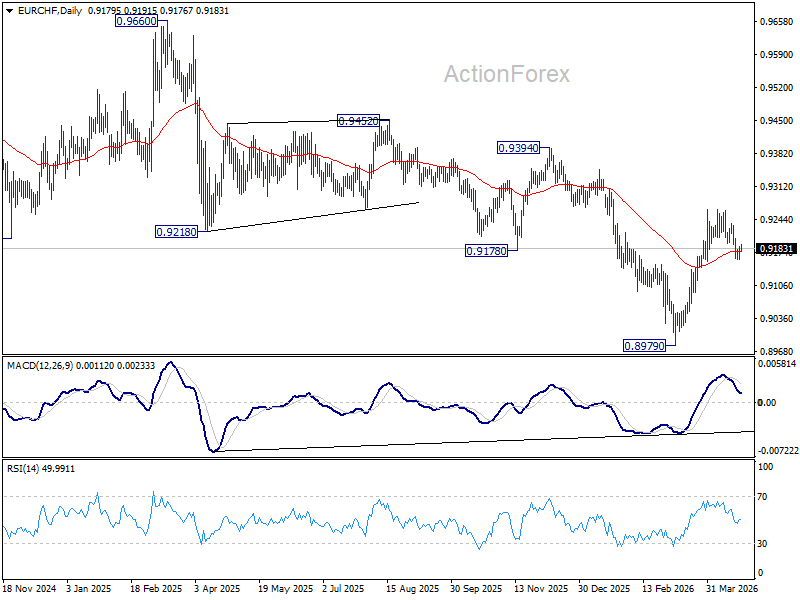

No change in EUR/CHF and intraday bias remains neutral. More consolidations could be seen below 0.9264. Further rise is in favor with 0.9155 support intact. Firm break of 0.9264 will resume the rise from 0.8979 to 0.9394 resistance next. However, break of 0.9155 will turn bias back to the downside for deeper pullback.

In the bigger picture, considering bullish convergence condition in W MACD, a medium term bottom should be in place at 0.8979. Sustained trading above 55 W EMA (now at 0.9280) will add more credence to this case. Further break of 0.9394 resistance will pave the way to 0.9660 resistance next. However rejection by the 55 W EMA will set up another fall through 0.8979 low at a later stage.

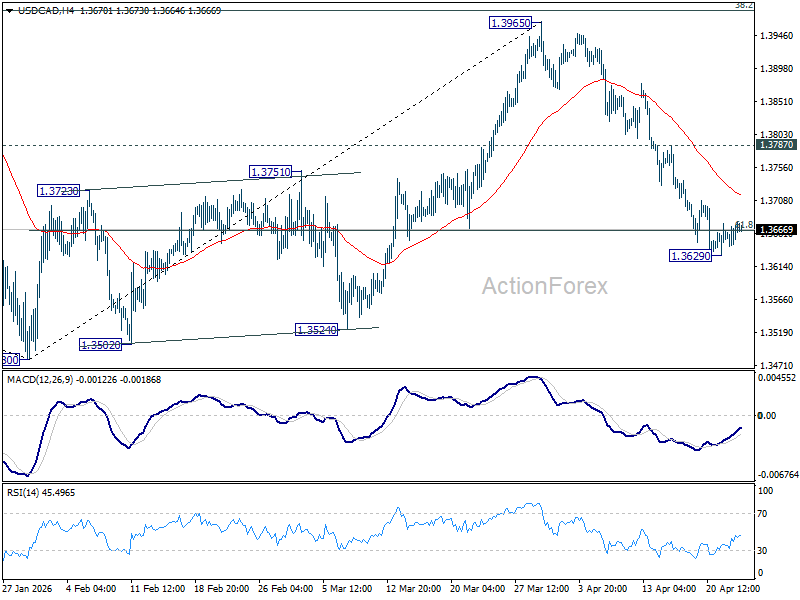

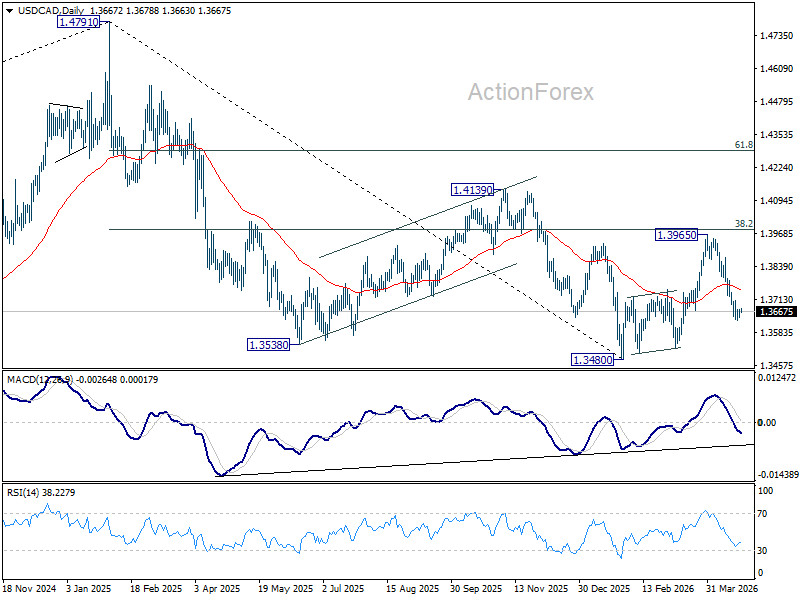

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3652; (P) 1.3663; (R1) 1.3684; More...

Intraday bias in USD/CAD is turned neutral again with current recovery. Further fall is in favor as long as 1.3787 resistance holds. Sustained trading below 61.8% retracement of 1.3480 to 1.3965 at 1.3665 will pave the way to retest 1.3480 low. However, firm break of 1.3787 will bring stronger rebound back to retest 1.3965 resistance.

In the bigger picture, price actions from 1.4791 are seen as a corrective pattern to the whole up trend from 1.2005 (2021 low). Deeper fall could be seen, as the pattern extends, to 61.8% retracement of 1.2005 to 1.4791 at 1.3069. However, decisive break of 38.2% retracement of 1.4791 to 1.3480 at 1.3981 will argue that the correction has completed with three waves down to 1.3480 already. Further break of 1.4139 will confirm and bring retest of 1.4791 high.

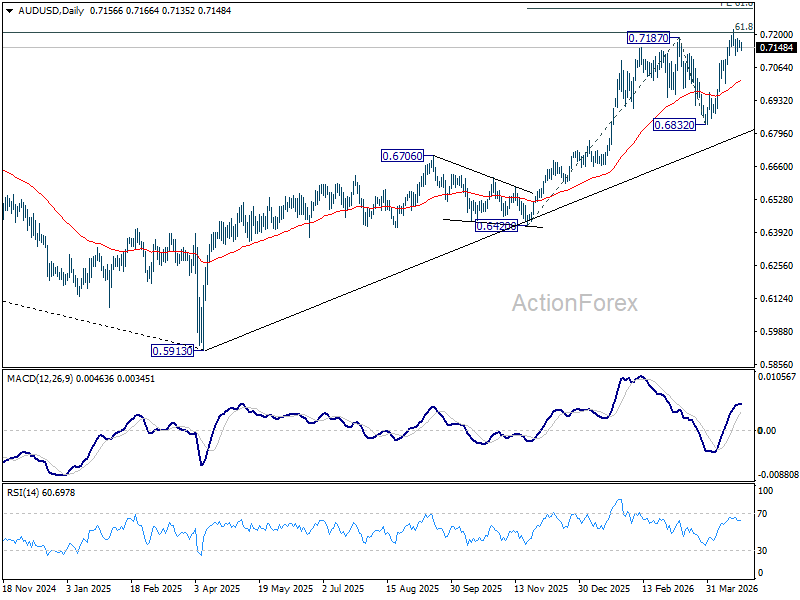

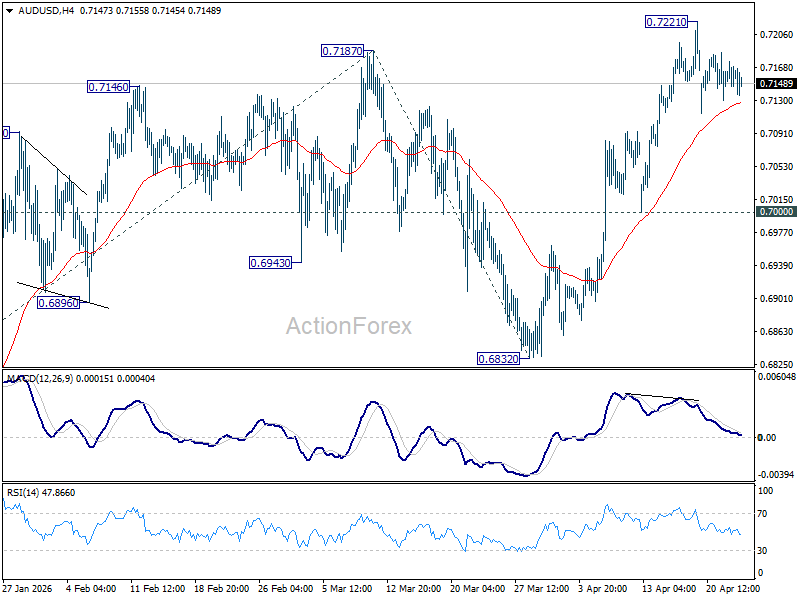

AUD/USD Daily Report

Daily Pivots: (S1) 0.7145; (P) 0.7161; (R1) 0.7175; More...

Intraday bias in AUD/USD remains neutral and more consolidations would be seen below 0.7221 temporary top. In case of deeper retreat, downside should be contained above 0.7000 support to bring rebound. On the upside, above 0.7221 will extend the larger up trend to 61.8% projection of 0.6420 to 0.7187 from 0.6832 at 0.7306. However, break of 0.7000 will bring deeper fall back to 0.6832 support instead.

In the bigger picture, rise from 0.5913 (2024 low) is still in progress. Decisive break of 61.8% retracement of 0.8006 to 0.5913 at 0.7206 will solidify the case that it's already reversing the down trend from 0.8006 (2021 high). Further rally should then be seen to retest 0.8006. For now, outlook will remain bullish as long as 0.6832 support holds, in case of pullback.