Sample Category Title

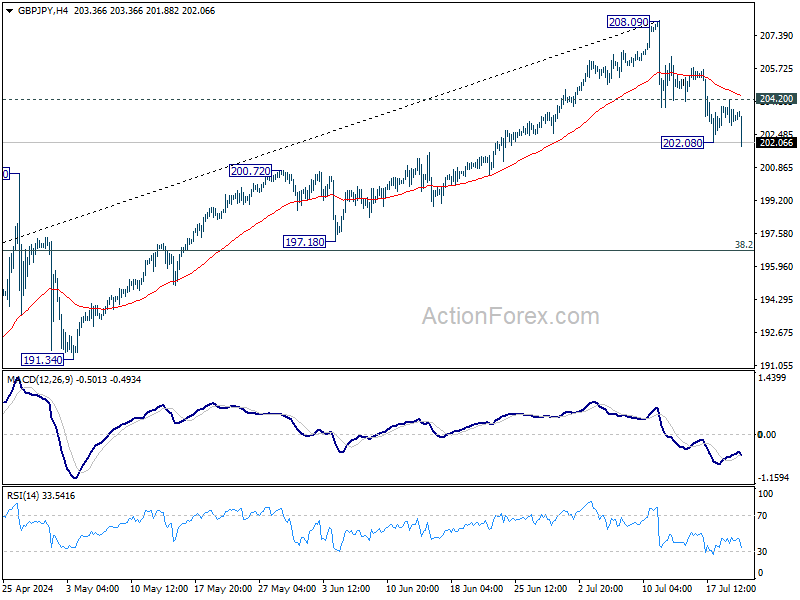

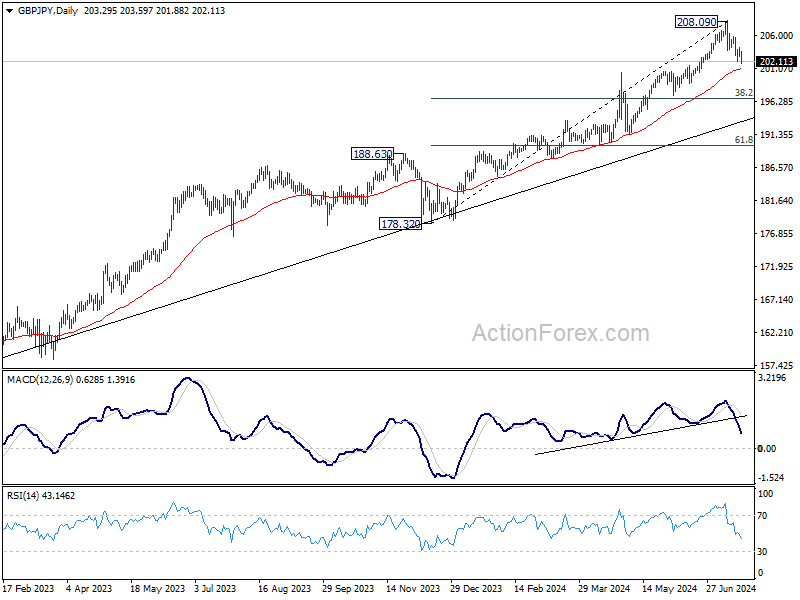

GBP/JPY Daily Outlook

Daily Pivots: (S1) 202.75; (P) 203.47; (R1) 203.97; More...

Intraday bias in GBP/JPY is back on the downside with breach of 20208 temporary low. Fall from 208.09 is resuming, as a correction to whole rise from 178.32. Next target is 55 D EMA (now at 201.02). Sustained break there will target 38.2% retracement of 178.32 to 208.09 at 196.71. Nevertheless, break of 204.20 resistance will retain near term bullishness and bring retest of 208.09 high.

In the bigger picture, medium term outlook will stay bullish as long as 188.63 resistance turned support holds. Long term up trend remains in favor to continue through 208.09 at a later stage. However, firm break of 188.63 will be a strong sign of bearish trend reversal.

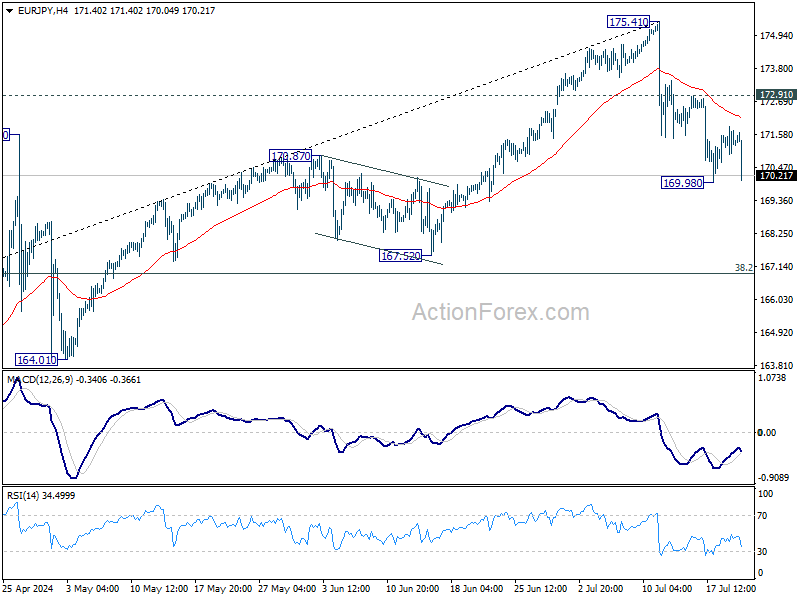

EUR/JPY Daily Outlook

Daily Pivots: (S1) 170.95; (P) 171.33; (R1) 171.73; More...

EUR/JPY is staying above 169.98 despite today's fall. Intraday bias remains neutral first, and further decline is expected as long as 172.91 resistance holds. Below 169.98 will target 38.2% retracement of 153.15 to 175.41 at 166.90, as a correction to whole rise from 153.15. On the upside, though, break of 172.91 resistance will revive near term bullishness and bring retest of 175.41 high.

In the bigger picture, medium term outlook will stay bullish as long as 164.29 resistance turned support holds. Long term up trend is still in favor to continue through 175.41 at a later stage. However, firm break of 164.29 will be a strong sign of bearish trend reversal.

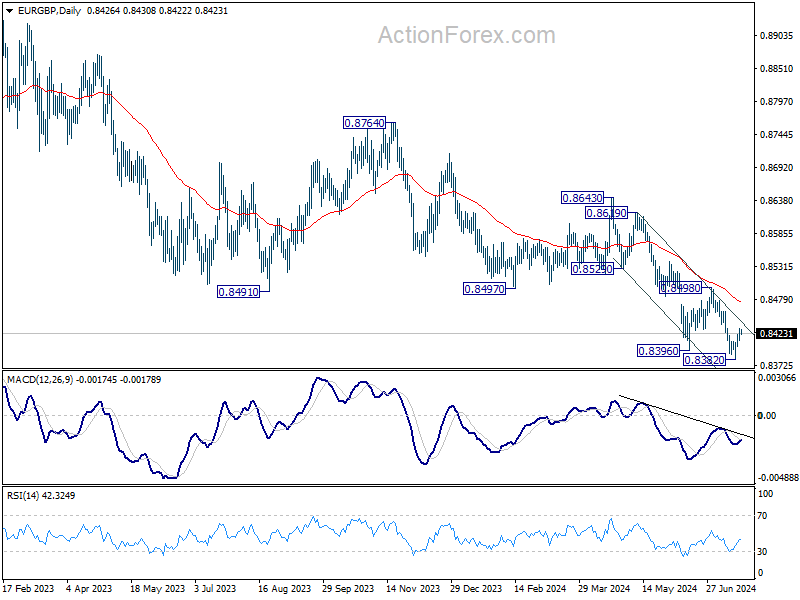

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8413; (P) 0.8423; (R1) 0.8438; More....

Intraday bias in EUR/GBP stays mildly on the upside as stronger rebound could be seen in EUR/GBP to 55 D EMA (now at 0.8473). Nevertheless, outlook will stay bearish as long as 0.8498 resistance holds, and larger down trend should resume through 0.8382 at a later stage.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 key support (2022 low). For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

Biden Leaving Election Races Dominates Headlines

Markets

Markets and several economic sectors Friday morning faced some jitters due to an IT outage linked to problems with an security update by CrowdStrike. It added to a risk-off tone at the final session of the week. Major US and EMU equity indices lost slightly less than 1.0% (S&P 500 -0.71%, Eurostoxx 50 -0.88%). Post Thursday’s ECB meeting, several ECB members brought some nuances to the message of Chair Lagarde that the ECB remains in a data-dependent approach and that everything stays open for the September meeting. The likes of ECB Muller and Rehn held to a strict data-dependent approach with no precommitment on the timing of further easing. Others (Simkus, Villeroy) took the approach of supporting current market pricing of 25 bps steps in September and December. German yields added between 1.9 bps (2-y) and 4.0 bps (30-y). US yields showed some further bottoming, rising between 4.7 bps (5-y) and 2.5 bps (30-y). Markets apparently concluded that enough Fed easing is discounted after recent softer than expected US (inflation) data. The focus now turns to the July 31 FOMC meeting. The dollar gained further ground after Thursday’s rebound. DXY further left the week lows near 103.65 behind to close 104.4, halting the unfolding of a potential double top formation. EUR/USD failed to holds the 1.09 barrier (close 1.0882). Sterling (close EUR/GBP 0.843) underperformed the dollar and the euro as poor UK retail sales keep the debate open whether or not the BOE will be in a position to already cut interest rates at the August 1 meeting.

US President Biden leaving the US election races dominates the new/market headlines this morning. Still, markets don’t draw any firm conclusions yet. The news as such isn’t enough to abruptly close the Trump trade that at some occasions was build out recently (higher LT-yields, a stronger dollar and uncertainty in equity sectors that might be affected by a more protectionist US trade policy). US yields are declining slightly marginally (< 3 bps). The dollar tentatively lost some ground at the open in Asia, but most of this initially reaction is already undone at the time of writing (EUR/USD 1.0885, DXY 104.33). The yen slightly outperforms (USD/JPY 157.15). Today (and tomorrow) the eco calendar in the US and EMU is thin. Later this week, the July PMI’s (US and EMU), the first reading of the US Q2 GDP (including price deflators) and the ‘real start’ of the earnings season have market moving potential. (US) yields bottomed (2-y 4.40% area, 10-y support 4.15%/4.20%). We see further consolidation going into next week Fed meeting. The dollar also shows signs of bottoming, but the move for now isn’t impressive either. EUR/USD 1.0948/81 is first resistance/USD support which we don’t expect to be broken easily short-term.

News & Views

The Chinese central bank (PBOC) lowered its seven-day reverse repo rate by 10 bps to 1.7% this morning. The move was unexpected given that it left the one-year lending facility (MLF) benchmark rate unchanged at 2.5% last week. The PBOC over the previous weeks signaled a shift towards making the seven-day rate the future reference. Today’s decision eroding the importance of the MLF rate further seems to back that. The fundamental impact of a 10 bps cut at a time where interest rates are already at their lowest in decades is likely to be limited. It does shape expectations for more easing , but the PBOC is walking a tightrope in creating easy monetary conditions to support the economy vs. fueling a stampede towards government bonds and adding to the downward pressure on the CNY, both of which concern the government in terms of financial stability risks. China’s 10-yr yield indeed eased a few bps after the announcement while USD/CNY gapped to the nine-month highs around 7.273 at the open.

UK Treasury ministers from the incoming Labour government are seen as preparing the public opinion for a tough autumn Budget and possible tax increases. Chancellor Reeves said yesterday she wanted to “level” with the public about the fiscal “mess”. Ministers last week handed to Treasury their assessment of the spending commitments they have inherited from the Tories, including the fiscal holes that need to be filled. One of the problems that arose early is how to find the billions to fund a 5.5% pay increase for about 1.9mn public sector workers. Cabinet Office minister Pat McFadden meanwhile similarly told ministers to urgently identify (financial) problems in their departments, adding to the idea the new government is seeking a political and public base for what is undoubtedly going to be a strict Budget..

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. Meanwhile, much of the save haven bids were reversed after the (first round in) the French elections. The 2.34%-2.4% support zone looks solid.

US 10y yield

The Fed indicated that it needs more evidence to lower its policy rate. June dots suggested one move in 2024 and four next year. Disappointing ISM and back-to-back downward CPI surprises put the US money market back on (at least) two rate cuts this year (September/December). The US 10-yr yield tests the recent lows and the downside of the downward trend channel in the 4.2% area.

EUR/USD

EUR/USD is testing the topside of the 1.06-1.09 range as the dollar loses interest rate support at stealth pace. Markets consider a September rate cut a done deal and only need confirmation from high-ranked Fed officials. In the meantime, the euro got rid of the (French) political risk premium. Risks of a topside break are high, bringing the psychologic 1.10 and the December 2023 top at 1.1139 on the radar.

EUR/GBP

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. Labour has yet to reveal its policy plans after securing a landslide election victory. EUR/GBP 0.84 support is being tested.

US Will Reveal Its Latest GDP Update

Joe Biden threw in the towel and announced that he quits the presidential race this weekend. He endorsed Vice President Kamara Harris to take his place. Harris said that she will do anything in her power to beat Trump, she got the support from Bill and Hillary Clinton while Trump said that Harris will be an easier bite for him than Biden himself. Even though Biden’s goodbye reshuffled the cards for the November election, it didn’t materially change the expected outcome… yet. We don’t know if Harris could secure her party’s nomination and gather enough momentum in the polls to beat Trump. The early polls show that Harris is a favourite to become the new Democrat nominee, but that Donald Trump is still expected to win the November’s presidential election. The Trump trade could lose some steam but will probably not get reversed if Harris doesn't make a material difference in the polls quickly.

The latter expectation was reflected with a brief post-announcement selloff and a rebound in Bitcoin. The US dollar is slightly softer across the board. Stock futures in Europe and the US are in the green while the Treasuries show muted reaction with small gains at the beginning of a new week, after a cyberattack - the largest IT shortage of the world history – came on Friday as a cherry on top of a week marked by increasing worries about the AI spending and worsening global trade relations in case of a Trump victory.

While Friday’s digital worldwide chaos was not a hack - on the contrary was caused by an update from a cybersecurity firm called CrowdStrike that triggered an 11% selloff of its shares - it sure showed to what extent many IT systems around the world are concentrated in the hands of a few providers and how seriously world-wide activity could be paralyzed in case of a hack. Although the Friday’s attack came as a threat to CrowdStrike’s reputation, it boosted the price of competitor stocks like Palo Alto Networks and SentinelOne.

But the week started looking unappetizing in Asia. Equities in Australia and China fell despite a surprise rate cut announcement from the People’s Bank of China (PBoC). The PBoC pulled its rates to new record lows to boost economic growth and give support to the troubled property sector. Xi Jinping revealed plans to improve the finances of the highly indebted local governments. But in vain. Last week’s communist party meeting in China didn’t bring big changes to the policy. There was no news of fresh stimulus. Consequently, investors didn’t want to extend exposure to Chinese equities this Monday. The CSI 300 is being offered near the 50-DMA, erasing a part of last week’s losses that were built on hope that we would hear fresh stimulus measures to make a difference.

The week also started on a meagre note for the technology stocks in Taiwan. TSM kicked off the week with a 3% fall after last week erased more than 3.5% from the technology-heavy Nasdaq stocks in the US. The S&P500 fell nearly 2% over the week, while the Russell 2000 printed a 1.50% advance despite erasing more of the earlier gains on Friday.

The week ahead

This week, the economic calendar will be light in the US. On Thursday, the US will reveal its latest GDP update, expected to show a rebound to 1.9% in the Q2 from 1.4% printed in Q1. Then, the core PCE index, the Federal Reserve’s (Fed) favourite gauge of inflation, will tell on Friday whether the price pressures further eased as the economic growth slightly improved. A better growth combined to softer inflation would be the best possible outcome for the Fed and the Fedwatchers as it would mean that the Fed is getting closer to abating inflation without sending the US economy into recession. That should echo positively across stock and bond markets and could potentially slow a tech-led selloff in major indices. But the earnings will certainly matter more this week than the economic data. Two of the 7 Magnificent Seven companies in the US are due to report their Q2 earnings this week. Both Tesla and Google will reveal how well they did in the Q2.

Inside AI

Google's earnings will be crucial for interpreting the future of AI. Recall that last earnings season, the focus was on whether the significant AI spending by Big Tech companies—which benefited AI tool providers like semiconductor and data center companies—would start bearing fruit for data-rich companies like Google and Meta, potentially shifting the AI rally from AI tool providers to those heavily investing in AI. The answer was no. On the contrary, Meta announced it needed to increase its AI spending to reach profitability. This earnings season, we will again look for any positive impact of substantial AI investments on big data holders like Google and Meta. We'll assess if the concerns about the profitability of huge AI investments are valid. Given the uncertainty, Big Tech earnings could either lead to further profit-taking or slow down the bleeding. The risk this quarter is that even outstanding results from companies like Nvidia may not sustain AI euphoria if those heavily invested in AI tools can't demonstrate to their investors that these investments are worthwhile.

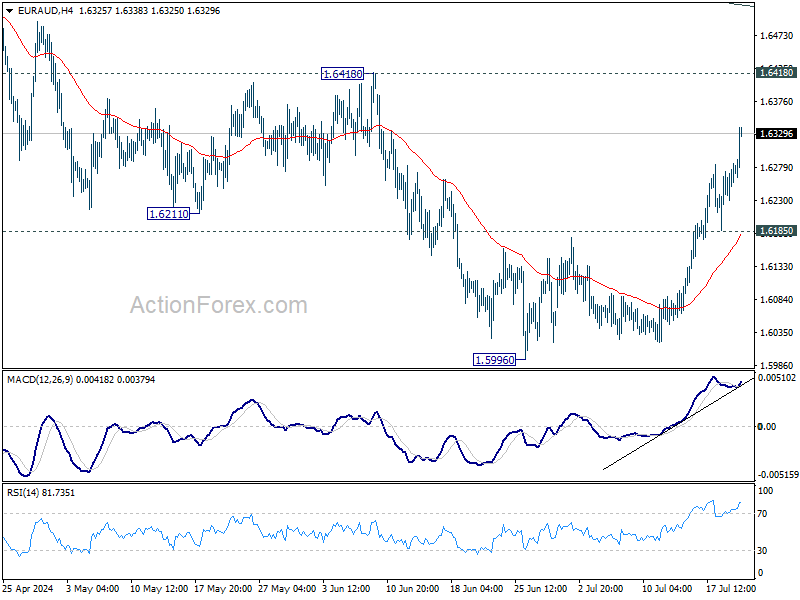

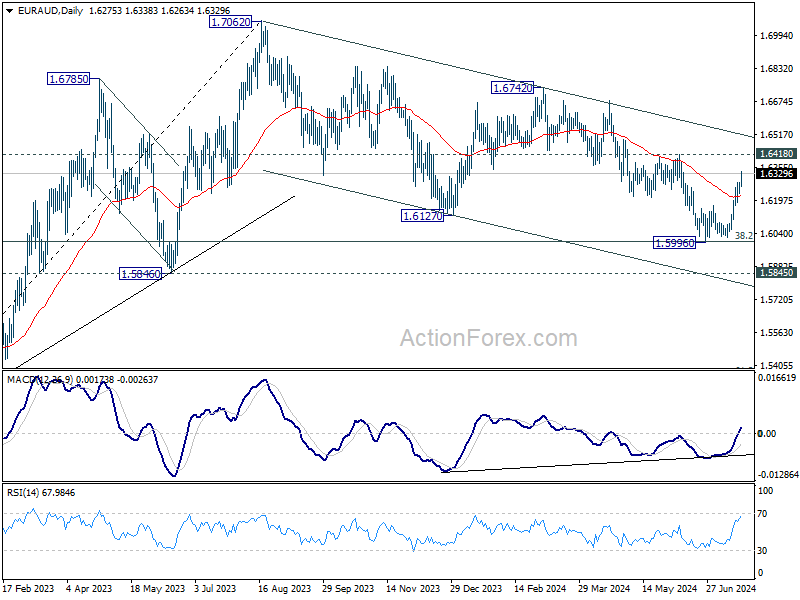

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6250; (P) 1.6270; (R1) 1.6308; More...

Intraday bias in EUR/AUD is back on the upside as rebound from 1.5996 resumed after brief retreat. Current development suggest that 1.0762 has completed with three waves down to 1.6000 fibonacci support. Further rise should be seen to 1.6418 resistance first. Firm break there will solidify this bullish case and target 1.6742 resistance next. On the downside, though, break of 1.6185 support will dampen this bullish view and bring retest of 1.5996 instead.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.6148 resistance will argue that the correction has completed, and the up trend is ready to resume through 1.7062.

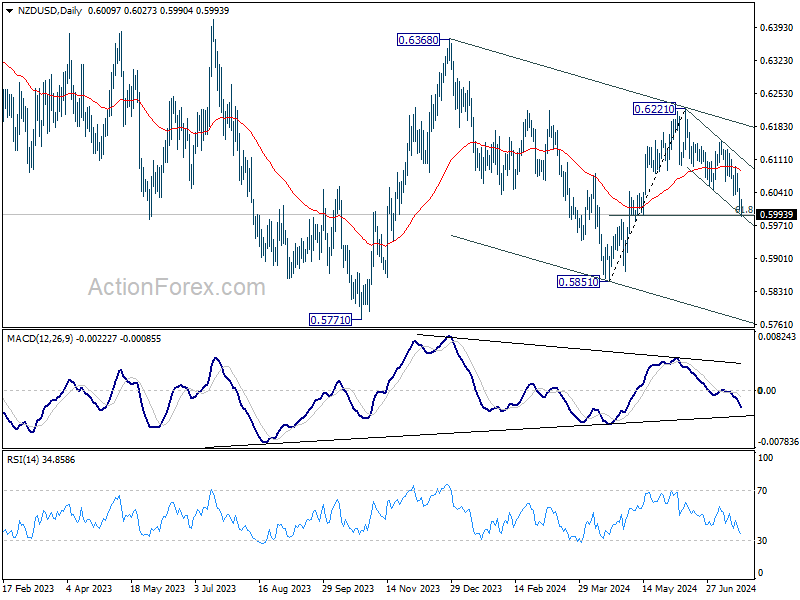

Aussie Leads Decline in Commodity Currencies; Risk Aversion Dominates Following China’s Rate Cut

Australian Dollar leads other commodity currencies lower in Asian session today, reflecting a broader risk-off sentiment in the markets. The market's risk-off sentiment is further emphasized by the strength of Yen and Swiss Franc, currencies typically favored during periods of uncertainty.

Nikkei has slipped below the 40k mark, while China's Shanghai SSE is down over -1%. This negative mood should be primarily driven by the unexpected rate cut by China's central bank, signaling deepening economic troubles in the country.

Some analysts have speculated that market reactions could be influenced by US President Joe Biden's announcement to withdraw from the presidential race. However, Biden's exit was largely anticipated and should have already been digested by the markets. The more pressing question now is whether Vice President Kamala Harris will step in to compete against Donald Trump,or if another contender will emerge.

In the currency markets, New Zealand Dollar and Canadian Dollar are trailing the Australian Dollar in losses. On the other hand, Japanese Yen and Swiss Franc are emerging as the strongest performers, reflecting a typical risk-aversion picture. Dollar, Euro, and British Pound are trading in the middle, showing no clear advantage over each other.

Technically, NZD/USD is now pressing 61.8% retracement of 0.5851 to 0.6221 at 0.5992. Sustained break of 0.5992 will argue that fall from 0.6221 is likely resuming the decline from 0.6368, which is the third leg of the whole down trend from 0.6537 (2023 high). In this bearish case, NZD/USD should tumbles through 0.5851 support to 0.5771 low and possibly below. This will remain the favored case as long as 55 D EMA (now at 0.6086) holds.

In Asia, at the time of writing, Nikkei is down -1.31%. Hong Kong HSI is up 0.79%. China Shanghai SSE is down -1.10%. Singapore Strait Times is down -0.13%. Japan 10-year JGB yield is up 0.0098 at 1.057.

China's surprise rate cut lifts USD/CNH

In a surprised move, China's PBoC today announced its first reduction in a key short-term policy rate in nearly a year, following weaker-than-expected economic growth in Q2. The economy expanded at its slowest pace in over a year, prompting the central bank to lower the seven-day reverse repo rate from 1.8% to 1.7%. PBOC emphasized that these rate cuts are part of its strategy to "strengthen counter-cyclical adjustments to better support the real economy."

Following closely on PBOC's announcement, Chinese banks adjusted their main benchmark lending rates, marking the first such adjustment since August 2023. The one-year loan prime rate was reduced to 3.35% from 3.45%. The five-year rate, which is crucial for mortgages, dropped to 3.85% from 3.95%.

In response to these developments, USD/CHN extends the recovery from 7.2597 following the news. Technically, current development suggests that pull back from 7.3111 has already completed, and larger rise from 7.0870 is probably ready to resume. Break of 7.3111 will target 100% projection of 7.0870 to 7.2827 from 7.1648 at 7.3605, which is slightly below 7.3745 (2023 high). This will remain the favored case as long as 7.2597 support holds.

New Zealand's goods exports falls -0.1% yoy, imports down significantly by -13% yoy

In June, New Zealand's overall goods exports slightly declining by -0.1% yoy, a reduction of NZD 7.4m, totaling NZD 6.2B. Conversely, goods imports experienced a more significant decrease, falling -13% yoy or NZD 821m, resulting in total imports of NZD 5.5B. This led to a trade surplus of NZD 699m, surpassing expectations of NZD 294m.

Examining trade movements by country, exports to major partners showed mixed results. China saw a decrease of NZD 142m in exports, a -9.1% yoy drop, while exports to Australia also fell by NZD 74m or -9.2% yoy. In contrast, exports to the US and the EU increased by NZD 91m (12% yoy) and NZD 129m (34% yoy) respectively. Japan's exports marginally decreased by NZD 4.1m or -1.1% yoy.

On the import front, China and the EU recorded increases of NZD 11m (0.9% yoy) and NZD 33m (3.3% yoy) respectively. However, imports from Australia, the US, and South Korea saw significant declines, with reductions of NZD 69m (-10% yoy), NZD 49m (-8.4% yoy), and NZD 54m (-14% yoy) respectively.

BoC rate cut and US GDP advance headline light economic week

BoC's rate decision is the major highlight in a relatively light economic week. It's widely expected that BoC will lower its overnight interest rate by 25bps to 4.50%. Going forward, a recent Reuters survey shows that a slim majority of economists, 16 out of 30, expect BoC to cut rates twice more this year, in October and December, bringing the rate to 4.00%. Ten economists predict just one more cut to 4.25%, while four expect a total of three additional cuts to 3.75%.

The median forecast is for a total of four rate cuts this year, including the previous cut in June, the upcoming one this week, and further cuts in October and December. This aligns with the forecasts from all five major Canadian banks. However, the eventual rate path will depend on how the sticky core inflation and wage growth evolve in Canada.

On the data front, US Q2 GDP advance release is another significant event. Growth is expected to bounce back from the lowest rate since 2022 in Q1. However, any lower-than-expected momentum would solidify market expectations that Fed is on track for two rate cuts this year. Additionally, the US will release durable goods orders and PCE inflation data, with the latter expected to mirror the latest CPI report, indicating further disinflation.

Other notable economic data releases this week include PMIs from major economies, Germany's Gfk consumer sentiment, and Ifo business climate index. Japan's Tokyo CPI is also on the docket.

Here are some highlights for the week:

- Monday: New Zealand trade balance; China rate decision.

- Tuesday: Eurozone consumer confidence; US existing home sale.

- Wednesday: Australia PMIs; Japan PMIs; Germany Gfk consumer sentiment; Eurozone PMIs; UK PMIs; Canada new housing price index, BoC rate decision; US goods trade balance, PMIs, new home sales.

- Thursday: Japan corporate service price index; Germany Ifo business climate; Eurozone M3 money supply; US Q2 GDP advance, jobless claims, durable goods, orders.

- Friday: Japan Tokyo CPI; US personal income and spending, PCE inflation.

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6250; (P) 1.6270; (R1) 1.6308; More...

Intraday bias in EUR/AUD is back on the upside as rebound from 1.5996 resumed after brief retreat. Current development suggest that 1.0762 has completed with three waves down to 1.6000 fibonacci support. Further rise should be seen to 1.6418 resistance first. Firm break there will solidify this bullish case and target 1.6742 resistance next. On the downside, though, break of 1.6185 support will dampen this bullish view and bring retest of 1.5996 instead.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.6148 resistance will argue that the correction has completed, and the up trend is ready to resume through 1.7062.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jun | 699M | 294M | 204M | 54M |

| 01:15 | CNY | 1-Y Loan Prime Rate | 3.35% | 3.45% | 3.45% | |

| 01:15 | CNY | 5-Y Loan Prime Rate | 3.85% | 3.95% | 3.95% |

China’s surprise rate cut lifts USD/CNH

In a surprised move, China's PBoC today announced its first reduction in a key short-term policy rate in nearly a year, following weaker-than-expected economic growth in Q2. The economy expanded at its slowest pace in over a year, prompting the central bank to lower the seven-day reverse repo rate from 1.8% to 1.7%. PBOC emphasized that these rate cuts are part of its strategy to "strengthen counter-cyclical adjustments to better support the real economy."

Following closely on PBOC's announcement, Chinese banks adjusted their main benchmark lending rates, marking the first such adjustment since August 2023. The one-year loan prime rate was reduced to 3.35% from 3.45%. The five-year rate, which is crucial for mortgages, dropped to 3.85% from 3.95%.

In response to these developments, USD/CHN extends the recovery from 7.2597 following the news. Technically, current development suggests that pull back from 7.3111 has already completed, and larger rise from 7.0870 is probably ready to resume. Break of 7.3111 will target 100% projection of 7.0870 to 7.2827 from 7.1648 at 7.3605, which is slightly below 7.3745 (2023 high). This will remain the favored case as long as 7.2597 support holds.

New Zealand’s goods exports falls -0.1% yoy, imports down significantly by -13% yoy

In June, New Zealand's overall goods exports slightly declining by -0.1% yoy, a reduction of NZD 7.4m, totaling NZD 6.2B. Conversely, goods imports experienced a more significant decrease, falling -13% yoy or NZD 821m, resulting in total imports of NZD 5.5B. This led to a trade surplus of NZD 699m, surpassing expectations of NZD 294m.

Examining trade movements by country, exports to major partners showed mixed results. China saw a decrease of NZD 142m in exports, a -9.1% yoy drop, while exports to Australia also fell by NZD 74m or -9.2% yoy. In contrast, exports to the US and the EU increased by NZD 91m (12% yoy) and NZD 129m (34% yoy) respectively. Japan's exports marginally decreased by NZD 4.1m or -1.1% yoy.

On the import front, China and the EU recorded increases of NZD 11m (0.9% yoy) and NZD 33m (3.3% yoy) respectively. However, imports from Australia, the US, and South Korea saw significant declines, with reductions of NZD 69m (-10% yoy), NZD 49m (-8.4% yoy), and NZD 54m (-14% yoy) respectively.

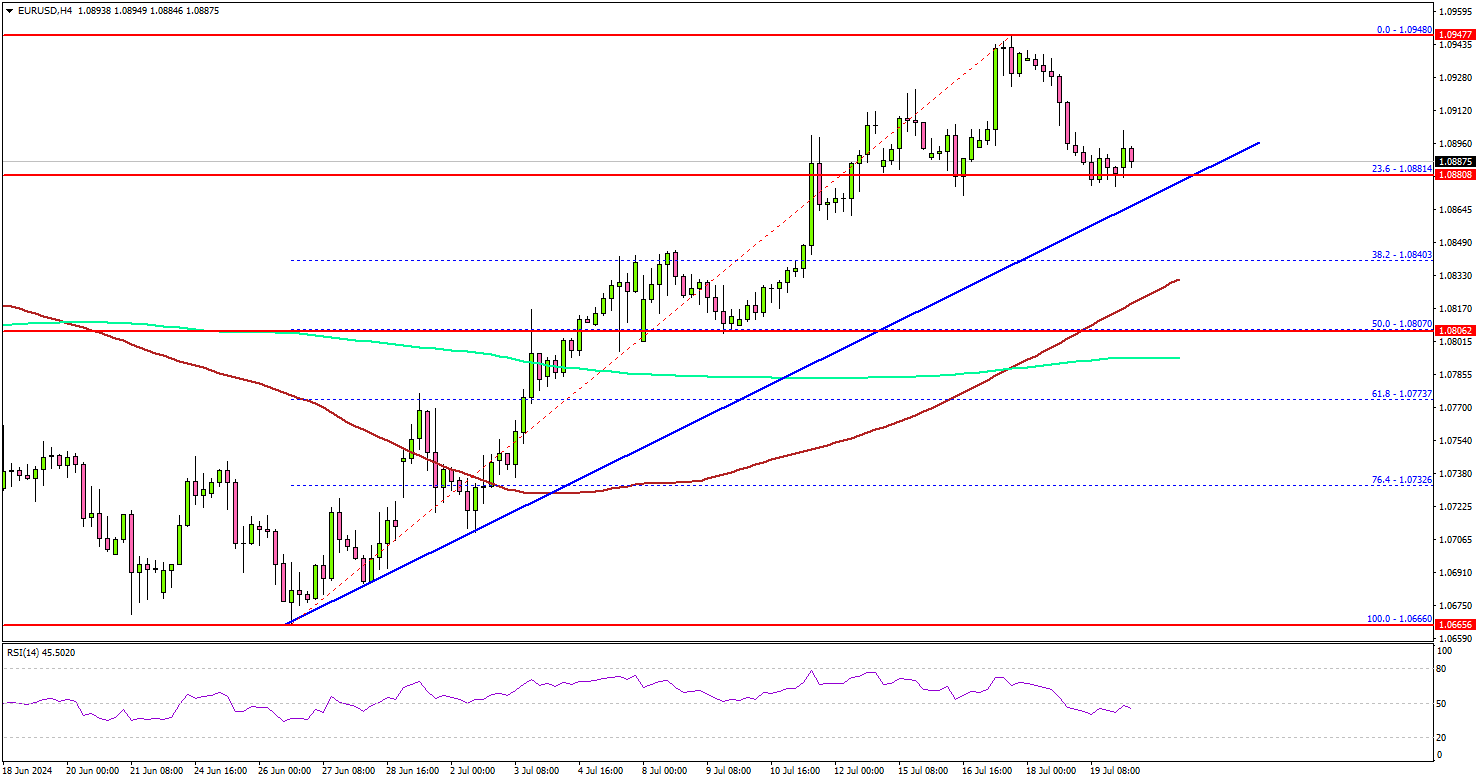

EUR/USD Remains Supported For More Upsides Above 1.0880

Key Highlights

- EUR/USD started a steady increase and surpassed the 1.0910 resistance.

- A key bullish trend line is forming with support at 1.0870 on the 4-hour chart.

- GBP/USD is correcting gains from the 1.3050 resistance zone.

- Oil prices extended losses and declined below the $80.50 level.

EUR/USD Technical Analysis

The Euro remained in a positive zone above the 1.0850 level against the US Dollar. EUR/USD climbed above the 1.0910 resistance to move into a bullish zone.

Looking at the 4-hour chart, the pair tested the 1.0950 level, and settled above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour). The pair tested the 1.0950 resistance zone and is currently correcting gains.

There was a drop below the 1.0910 level. The pair is now testing the 23.6% Fib retracement level of the upward move from the 1.0660 swing low to the 1.0948 high.

There is also a key bullish trend line forming with support at 1.0870 on the same chart. If there is a fresh increase, the pair could face resistance near the 1.0910 level. The next resistance sits at 1.0920. The main hurdle sits at 1.0950.

A clear move above the 1.0950 resistance might send it toward the 1.0980 level. Any more gains might open the doors for a test of the 1.1050 zone in the coming days.

Immediate support is near the 1.0870 level and the trend line. The next major support is near the 1.0850 level. A downside break and close below the 1.0850 support zone could open the doors for more losses. In the stated case, EUR/USD might decline toward the 1.0820 level.

Looking at Oil, there was a fresh bearish reaction and the bears were able to push the price below the $80.50 level.

Economic Releases

- Eurogroup Meeting.

- German Buba Monthly Report.