Sample Category Title

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 157.02; (P) 157.38; (R1) 157.78; More...

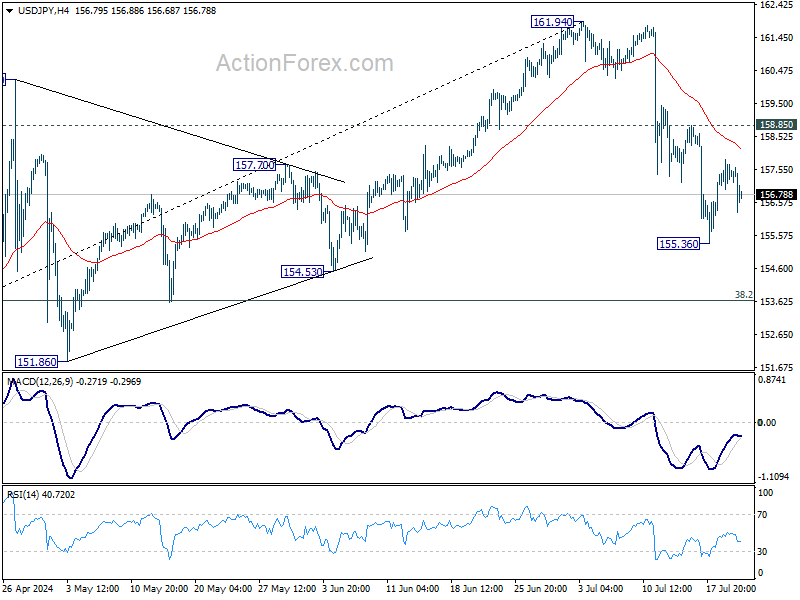

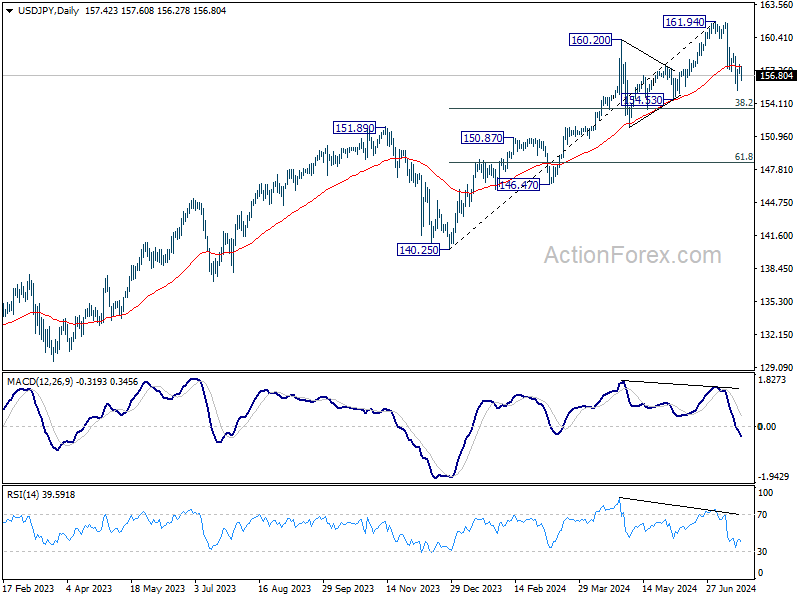

USD/JPY is staying in range above 155.36 temporary low and intraday bias remains neutral. Further decline is expected with 158.85 resistance intact. Below 155.36 will target 38.2% retracement of 140.25 to 161.94 at 153.65. On the upside, above 158.85 resistance will turn bias back to the upside for stronger rebound instead.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6672; (P) 0.6693; (R1) 0.6707; More...

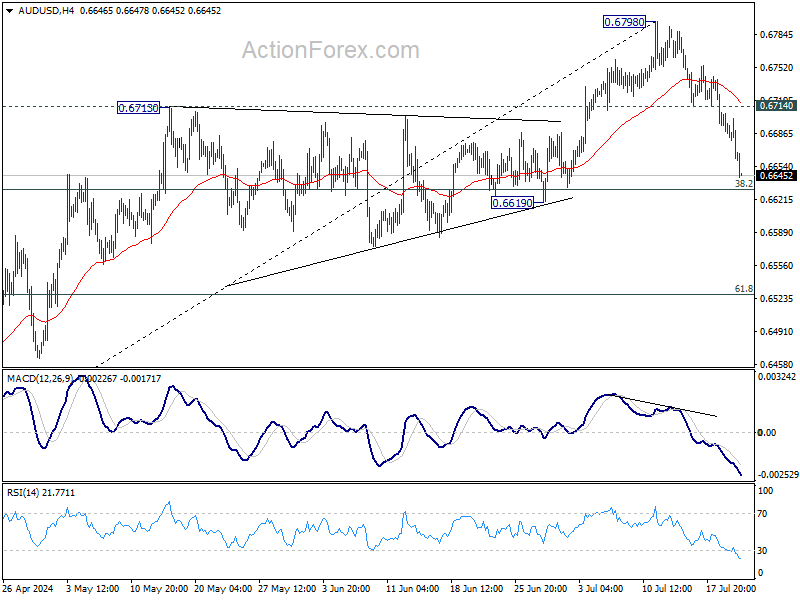

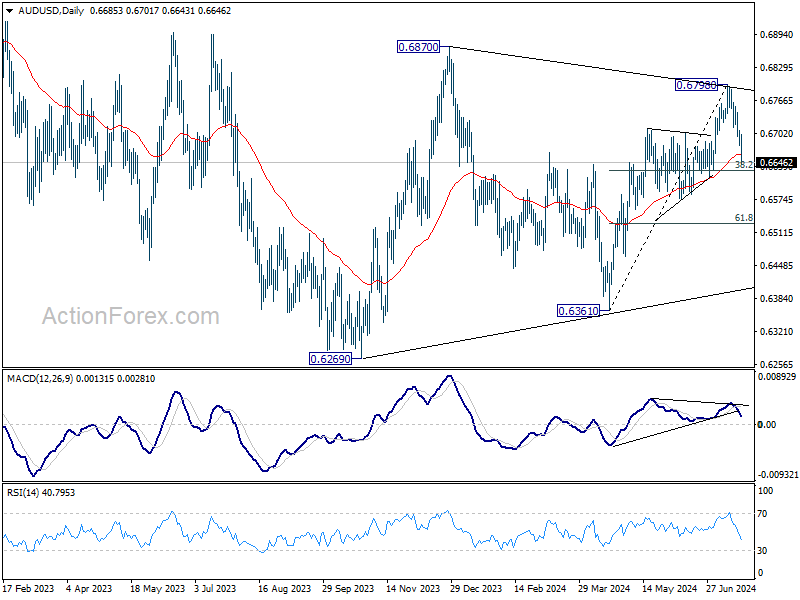

AUD/USD's fall from 0.6798 accelerates lower today and intraday bias stays on the downside for 38.2% retracement of 0.6361 to 0.6798 at 0.6631. Strong support could be seen there to bring rebound, and break of 0.6714 resistance will turn bias back to the upside for retesting 0.6798. However, sustained break of 0.6631 will bring deeper fall to 61.8% retracement at 0.6528 instead.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective patter, which is still extending. Break of 0.66870 resistance will extend the rising leg from 0.6269 towards 0.7156 (2023 high). However, break firm break of 0.6619 support will argue that another falling leg has started back towards lower side of the range between 0.6169/6361.

Aussie’s Selloff Deepens as Copper Prices Plunge

Australian Dollar continues to lead the decline among commodity currencies today, with the selloff appearing to accelerate. Despite stabilization in risk sentiment in Europe where major indexes are trading positively, and US futures, particularly NASDAQ, pointing to a stronger open, overall sentiment remains vulnerable. This fragility is largely due to political uncertainty in the US following Joe Biden's withdrawal from the presidential election race. Additionally, several high-profile earnings reports are set to be released this week, which could further influence market dynamics.

Contributing to Australian Dollar's woes is the continued decline in Copper prices. Copper just had its worst week since 2022, as the highly anticipated Plenum in China ended with significant disappointment among investors, offering no substantial plan to revive the beleaguered economy. Today's unexpected rate cut by the People's Bank of China serves as a stark reminder that economic troubles in the region persist.

Technically, Copper is now pressing 61.8% projection of 5.1650 to 4.3133 from 4.6839 at 4.1575. Decisive break there could trigger downside acceleration to 100% projection at 3.3058 next.

Overall in the currency markets, Yen is currently the strongest for the day, followed by Sterling and Swiss Franc. Dollar and Euro are positioned in the middle. However, Dollar, Euro, Sterling, and Swiss Franc are all trading within last week's ranges against each other, indicating that their relative positions could easily shift.

In Europe, at the time of writing, FTSE is up 0.91%. DAX is up 1.56%. CAC is up 1.45%. UK 10-year yield is down -0.0074 at 4.121. Germany 10-year yield is down -0.0013 at 2.457. Earlier in Asia, Nikkei fell -1.16%. Hong Kong HSI rose 1.25%. China Shanghai SSE fell -0.61%. Singapore Strait Times fell -0.30%. Japan 10-year JGB yield rose 0.0181 to 1.065.

Bundesbank urges prudence: further rate reductions must be judiciously evaluated

Bundesbank's latest monthly report indicates that while some factors are bolstering the economy, they are simultaneously complicating efforts to bring inflation down to target.

"The labor markets are still operating at high capacity, wage growth is brisk, and prices are rising strongly, particularly in the service sector," the report stated.

Bundesbank highlighted that "inflationary risks also predominate on the supply side." Services inflation is expected to decline only modestly in the coming months, with the overall price index likely to fluctuate around current levels.

Given these conditions, the Bundesbank advised that "possible further interest rate cuts should therefore be carefully considered in light of current data."

Bundesbank anticipates the economy to "strengthen somewhat" in the Q3. Private consumption is expected to "pick up a little more speed" driven by strongly rising wages, falling inflation, and a robust labor market, which should continue to support consumer spending.

However, the report also cautioned that industrial activity is likely to improve "only hesitantly" due to weak demand, which could result in GDP growth for Q3 falling slightly short of the expectations from June forecast.

ECB's Kazimir: Two more rate cuts this year not guaranteed

In an op-ed published today, ECB Governing Council member Peter Kazimir addressed market expectations for two additional rate cuts before the end of the year. He stated that while these market bets are "not entirely misplaced," they should not be considered a "given or a baseline scenario."

Kazimir highlighted that inflation is "on track" to return to the target but cautioned, "we are clearly not there yet." He emphasized the persistent risks of inflationary pressures due to various domestic and global factors. "There is still a non-negligible risk of inflationary pressures re-emerging," he noted.

"There is no need to rush our decisions," Kazimir added, advising a measured approach. "Enjoy the summer lull and wait for the much-anticipated September 'health check.' The upcoming data, combined with fresh forecasts, will set the stage for any necessary decisions."

China's surprise rate cut

In a surprised move, China's PBoC today announced its first reduction in a key short-term policy rate in nearly a year, following weaker-than-expected economic growth in Q2. The economy expanded at its slowest pace in over a year, prompting the central bank to lower the seven-day reverse repo rate from 1.8% to 1.7%. PBOC emphasized that these rate cuts are part of its strategy to "strengthen counter-cyclical adjustments to better support the real economy."

Following closely on PBOC's announcement, Chinese banks adjusted their main benchmark lending rates, marking the first such adjustment since August 2023. The one-year loan prime rate was reduced to 3.35% from 3.45%. The five-year rate, which is crucial for mortgages, dropped to 3.85% from 3.95%.

New Zealand's goods exports falls -0.1% yoy, imports down significantly by -13% yoy

In June, New Zealand's overall goods exports slightly declining by -0.1% yoy, a reduction of NZD 7.4m, totaling NZD 6.2B. Conversely, goods imports experienced a more significant decrease, falling -13% yoy or NZD 821m, resulting in total imports of NZD 5.5B. This led to a trade surplus of NZD 699m, surpassing expectations of NZD 294m.

Examining trade movements by country, exports to major partners showed mixed results. China saw a decrease of NZD 142m in exports, a -9.1% yoy drop, while exports to Australia also fell by NZD 74m or -9.2% yoy. In contrast, exports to the US and the EU increased by NZD 91m (12% yoy) and NZD 129m (34% yoy) respectively. Japan's exports marginally decreased by NZD 4.1m or -1.1% yoy.

On the import front, China and the EU recorded increases of NZD 11m (0.9% yoy) and NZD 33m (3.3% yoy) respectively. However, imports from Australia, the US, and South Korea saw significant declines, with reductions of NZD 69m (-10% yoy), NZD 49m (-8.4% yoy), and NZD 54m (-14% yoy) respectively.

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6672; (P) 0.6693; (R1) 0.6707; More...

AUD/USD's fall from 0.6798 accelerates lower today and intraday bias stays on the downside for 38.2% retracement of 0.6361 to 0.6798 at 0.6631. Strong support could be seen there to bring rebound, and break of 0.6714 resistance will turn bias back to the upside for retesting 0.6798. However, sustained break of 0.6631 will bring deeper fall to 61.8% retracement at 0.6528 instead.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective patter, which is still extending. Break of 0.66870 resistance will extend the rising leg from 0.6269 towards 0.7156 (2023 high). However, break firm break of 0.6619 support will argue that another falling leg has started back towards lower side of the range between 0.6169/6361.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Trade Balance (NZD) Jun | 699M | 294M | 204M | 54M |

| 01:15 | CNY | 1-Y Loan Prime Rate | 3.35% | 3.45% | 3.45% | |

| 01:15 | CNY | 5-Y Loan Prime Rate | 3.85% | 3.95% | 3.95% |

Bundesbank urges prudence: further rate reductions must be judiciously evaluated

Bundesbank's latest monthly report indicates that while some factors are bolstering the economy, they are simultaneously complicating efforts to bring inflation down to target.

"The labor markets are still operating at high capacity, wage growth is brisk, and prices are rising strongly, particularly in the service sector," the report stated.

Bundesbank highlighted that "inflationary risks also predominate on the supply side." Services inflation is expected to decline only modestly in the coming months, with the overall price index likely to fluctuate around current levels.

Given these conditions, the Bundesbank advised that "possible further interest rate cuts should therefore be carefully considered in light of current data."

Bundesbank anticipates the economy to "strengthen somewhat" in the Q3. Private consumption is expected to "pick up a little more speed" driven by strongly rising wages, falling inflation, and a robust labor market, which should continue to support consumer spending.

However, the report also cautioned that industrial activity is likely to improve "only hesitantly" due to weak demand, which could result in GDP growth for Q3 falling slightly short of the expectations from June forecast.

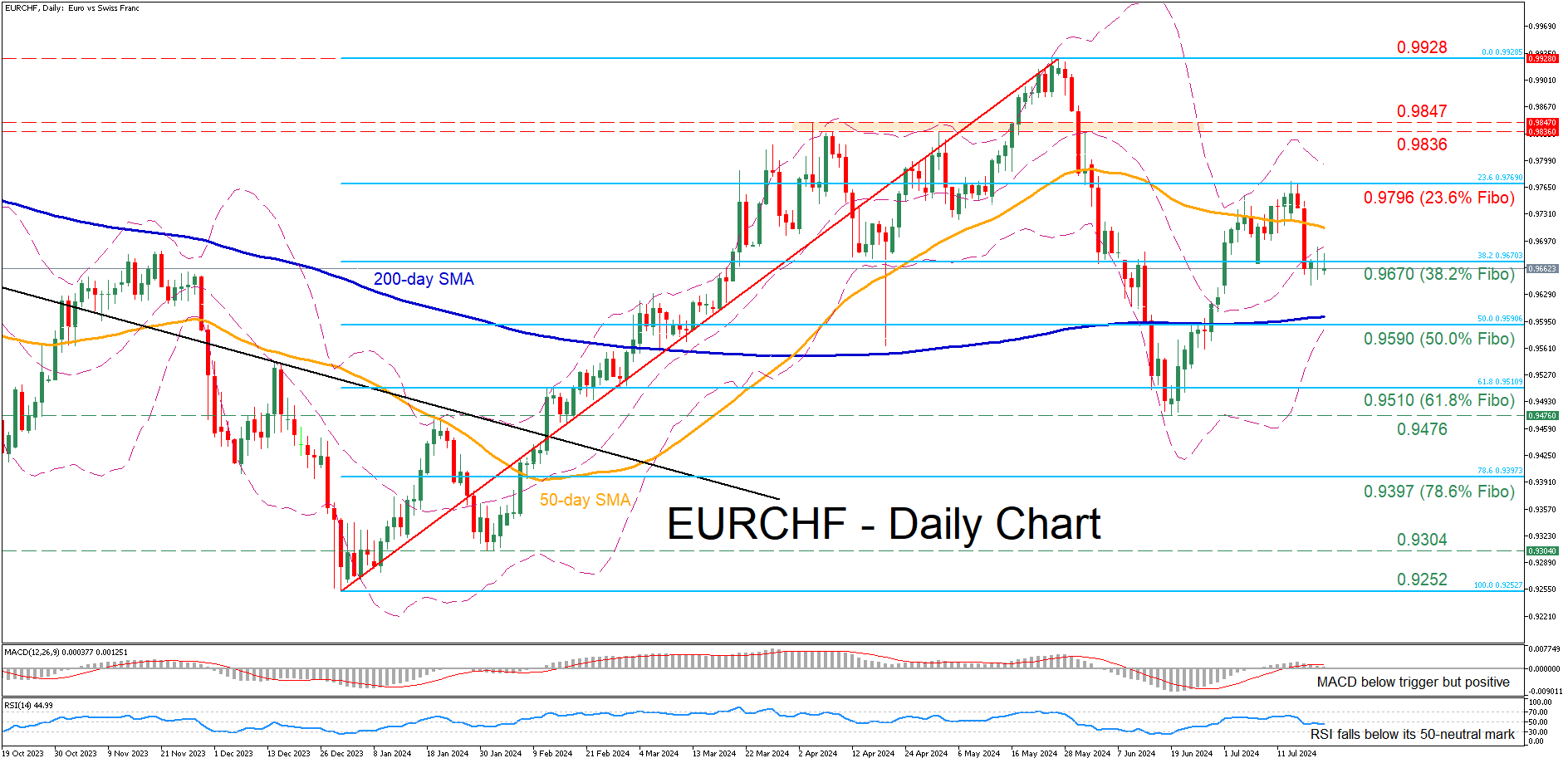

EURCHF Hovers Around 38.2% Fibo

- EURCHF spikes lower following rejection at 23.6% Fibo

- Price trades sideways after break below 50-day SMA

- Momentum indicators are neutral-to-negative

EURCHF has been staging a solid recovery since mid-June, advancing to its highest level in more than a month last Monday. However, the pair experienced a strong pullback following its rejection around 0.9796, which is the 23.6% Fibonacci retracement of the 0.9252-0.9928 upleg.

Should the negative bias persist, the bears could attempt to send the price below the 38.2% Fibo of 0.9670. Lower, the pair’s retreat could pause at the 50.0% Fibo of 0.9590, which lies very close to the 200-day SMA. In case of a downside violation, additional support could be found at the 61.8% Fibo of 0.9510.

On the flipside, if the price erases this latest slump, the 23.6% Fibo of 0.9796 could prove to be a tough barrier for the bulls to overcome. Further upside attempts could meet resistance at the 0.9836-0.9847 range, defined by the May resistance zone and the April peak. Surpassing that hurdle, the pair could revisit its 2024 peak of 0.9928.

Overall, EURCHF has been trading sideways in the past few sessions following an aggressive spike to the downside, which sent the pair below its 50-day SMA. For the bulls to regain confidence for a continuation of the latest uptrend, the pair needs to reclaim its short-term SMA.

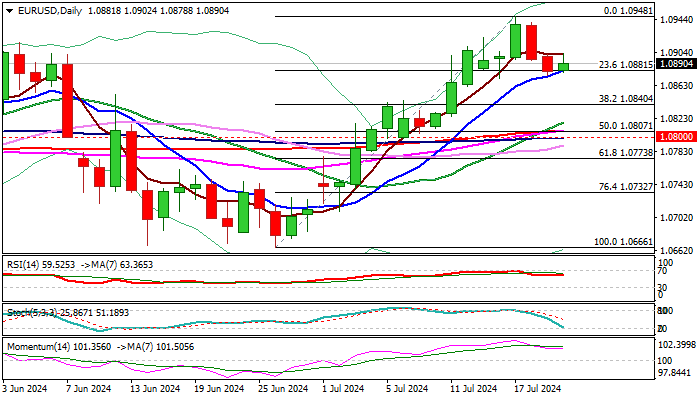

EUR/USD Outlook: Correction So Far Limited But Risk of Deeper Pullback Still Exists

EURUSD edges higher in European trading on Monday as bears are taking a breather after a two-day pullback from a multi-week high (1.0948).

Rising 10DMA and Fibo 23.6% of 1.0666/1.0948 (1.0881) contained dips for now, signaling a scenario of shallow correction before larger bulls regain control.

Talks about possible start of easing monetary policy as early as September add to positive outlook for the single currency, as daily studies keep strong positive momentum and MA’s remain in bullish setup.

However, weekly bull trap above 1.0933 Fibo barrier and weekly Doji candle with long upper shadow, warn that bulls might be running out of steam and deeper pullback cannot be ruled out.

Sustained break of 10 DMA / Fibo support to activate such scenario and expose next supports at 1.0840/07 (Fibo 38.2% / 50% / 200DMA).

Conversely, ability to hold above 1.0881support would keep near-term bias with bulls, with extension and close above 1.09 zone to generate initial signal of reversal and formation of a higher low.

Res: 1.0902; 1.0922; 1.0948; 1.0964.

Sup: 1.0881; 1.0840; 1.0807; 1.0788.

News of the Week (July 22—26): USDCNH Review

The USDCNH pair represents the exchange rate between the US dollar and the Chinese yuan. Factors influencing the US dollar include Federal Reserve policies, inflation rates, and the overall health of the US economy. In contrast, the Chinese yuan is affected by China’s monetary policies, economic growth metrics, and regulatory changes impacting capital flows. Movements in this currency pair can provide insights into shifts in economic policies, trade balances, and broader geopolitical tensions between the USA and China.

US Existing Home Sales, July 23, 16:00 (GMT+2)

The forthcoming release of US existing home sales predicted to decline to 4 million from 4.11 million, serves as a critical economic indicator. If the actual sales figures exceed expectations, suggesting a more robust housing market than anticipated, it could enhance investor confidence in the US economy. A strong real estate sector often correlates with broader economic strength, potentially boosting the US dollar and consequently driving the USDCNH pair higher. However, if the figures are lower than forecast, indicating a sluggish housing market, it could undermine confidence in the economic recovery, leading to a depreciation of the dollar against the yuan and a drop in the USDCNH rate.

CB Leading Index m/m, July 25, 15:00 (GMT+2)

The CB Leading Index from China measures economic activity and is forecasted to show a reduced contraction of -0.3%, an improvement over the previous -0.5%. If the index outperforms expectations by showing minimal contraction or unexpected growth, it would indicate an improving outlook for China's economy. A more robust Chinese economy usually bolsters the yuan, potentially lowering the USDCNH exchange rate as the yuan appreciates against the dollar. Conversely, a greater-than-expected decline in the index would suggest a sharper slowdown, potentially weakening the yuan. In such a case, the USDCNH pair might rise as the dollar strengthens relative to a faltering yuan, reflecting increased concerns over China's economic trajectory.

In the Daily timeframe, USDCNH is in a long-term uptrend. After a minor correction, the price fell to the 61.8 Fibonacci support, testing the MA50. Despite the long-term rise, Momentum fell below 100.0, which requires considering two possible scenarios.

- If the bears push the price below MA50 and 7.2600, the drop will be to 7.2000;

- However, a rebound from support would bring USDCNH back to resistance at 7.3100;

USD/JPY: Another Potential Relief Rally Leg Looms for JPY

- A potential uptick in Japan’s core-core CPI led by PPI may increase the odds of a BoJ’s interest rate hike in September.

- Republican presidential nominee Donald Trump’s betting odds have slipped after US President Biden decided to bow out of the US Presidential Election race.

- A resurgence of Trumponomics that may be challenged which in turn may lead to a US dollar mixed-bag to negative environment in the short term.

- Another daily close below 156.50 on the USD/JPY may trigger a multi-week corrective decline sequence.

Since the publication of our last analysis, the USD/JPY has indeed shaped the expected decline in the following two weeks; it declined by 538 pips/-3.35% to print an intraday low of 155.37 on Thursday, 18 July 2024 before it closed higher at 157.36 by the end of the US session that held above its key medium-term support at 156.50.

Two key catalysts for the recent weakness seen in the USD/JPY (Japanese yen strength revival); firstly, it has been the increased odds of a more dovish US Federal Reserve expectations to kickstart in the September FOMC meeting after a slew of soft key US economic data in terms of spending and inflationary trends.

Secondly, in an earlier Bloomberg interview with Republican US Presidential candidate Donald Trump published on Tuesday, 16 July, Trump implied that he favored a weaker US dollar against the Japanese yen and Chinese yuan (due to US exports losing competitiveness) despite the medium-term fundamental impact of the FX market is likely still a US dollar strength narrative as policies of Trumponomics of higher tax cuts yield a wider US budget deficit, in turn, drives up longer-term US Treasury yields which is US dollar positive.

Let’s now discuss the current factors (fundamentals, politics, and technical) that may support another leg of JPY strength at least in the short term.

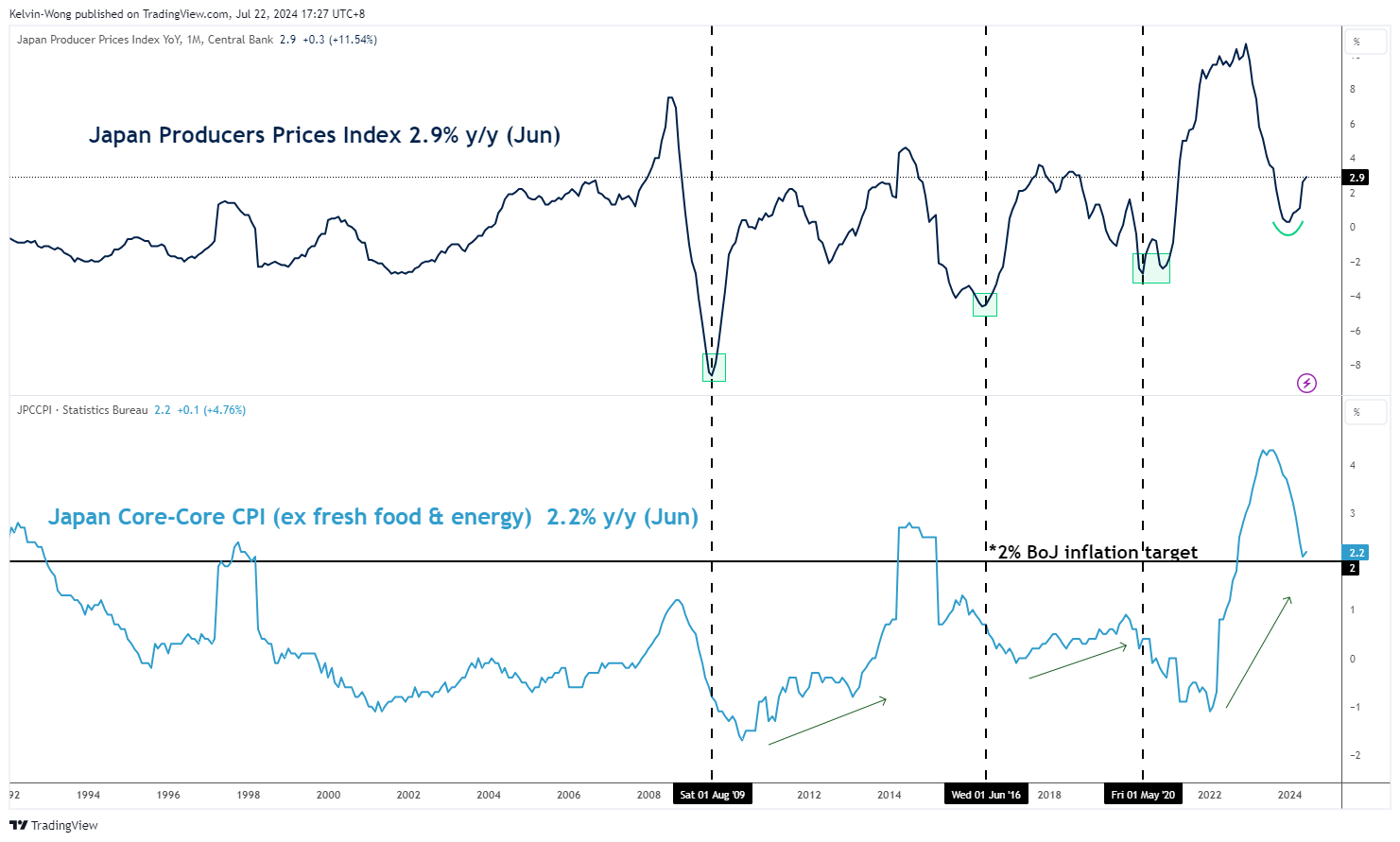

Japan’s consumer inflation deceleration trend has started to stall

Fig 1: Monthly Japan’s PPI & CPI trends (y/y) as of Jun 2024 (Source: TradingView, click to enlarge chart)

Japan’s nationwide core-core CPI (excluding fresh food and energy) has inched slightly higher in June to 2.2% y/y from 2.1% y/y in May (see Fig 1).

An interesting observation to highlight in terms of Japan’s producer prices index (manufacturers input costs) leading correlation with Japan’s core-core inflationary trend.

Based on the past three periods in August 2009, June 2016, and May 2020, the producer prices index (PPI) bottomed out first before core-core CPI trended higher, and the recent PPI has started to inch higher for six consecutive months to hit 2.9% y/y in June which suggests that the deceleration trend of Japan’s core-core CPI from its August 2023 reading of 4.3% y/y may have hit an inflection level in June and could follow the current upward bias trend of PPI.

A further uptick in core-core CPI above Bank of Japan (BoJ) inflation target of 2% is likely to set the stage for another potential interest rate hike in September after it enacted the first rate hike in March after 17 years, and such a signal or guidance may come in the upcoming 31 July monetary policy decision via a potential announcement of a further reduction in the purchase of 10-year Japanese Government Bonds (JGB).

Overall, a further potential reduction in the yield premium gap between US Treasuries and JGBs may support a further strengthening of the JPY.

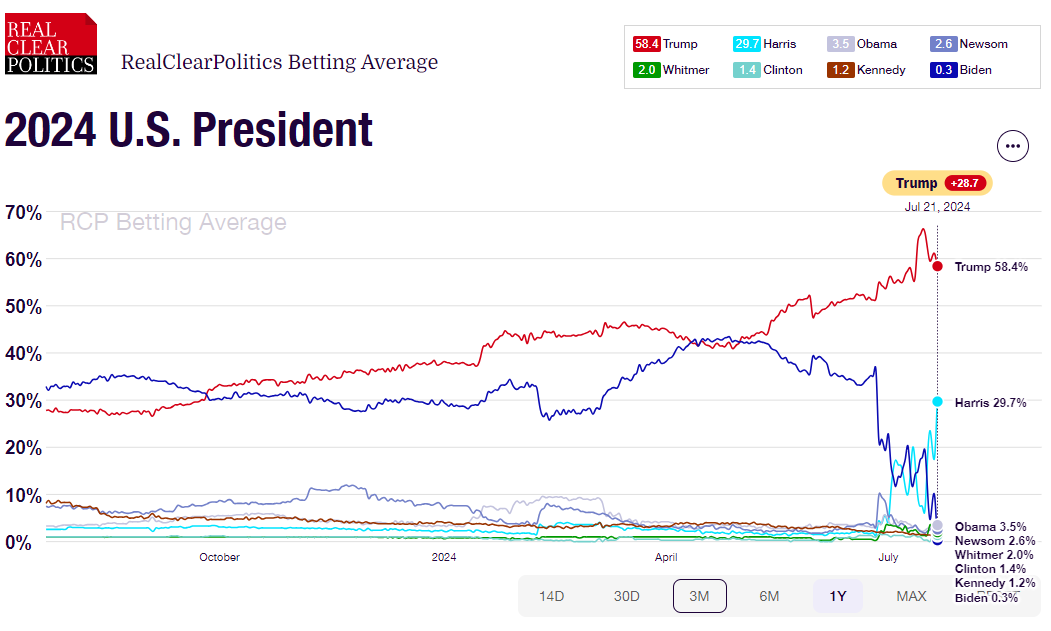

Trump’s chances of winning the US presidency have slipped

Fig 2: Average betting odds of 2024 US Presidential Election result of 21 Jul 2024 (Source: Real Clear Politics, click to enlarge chart)

So far, several prominent Democrats and will-be presidential nominee contenders have thrown in their support to endorse Harris as their preferred choice to face off against Trump as reported by various media outlets, such as Bill and Hillary Clinton, California Governor Gavin Newsom, and all 50 Democrat party state chairs.

The latest average betting odds on the 2024 US Presidential Elections result compiled by Real Clear Politics as of 21 July has indicated Republican presidential nominee, Trump has slipped to 58% from a significantly high level of 66% on 15 July (after the failed assassination attempt). Meanwhile, the odds for Democrat Harris have increased to 30% significantly from 7% over the same period.

Hence, betting markets suggest Trump’s margin of winning has been reduced which may be US dollar negative as the odds of the passage of Trumponomics policies have inched down as well.

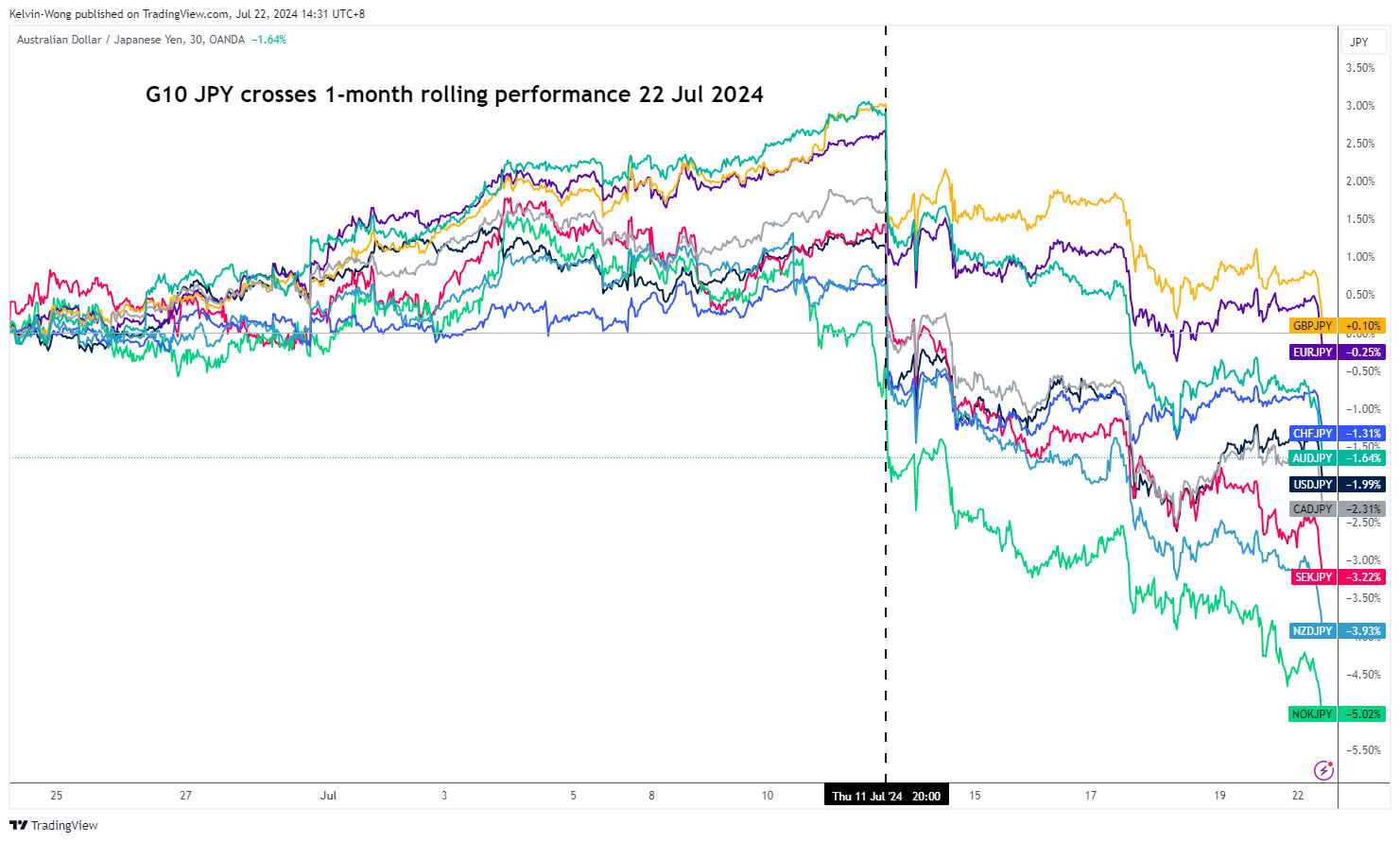

More bearish medium-term technical conditions sighted

Fig 3: 1-month of rolling performances of G-10 JPY crosses as of 22 Jul 2024 (Source: TradingView, click to enlarge chart)

Fig 4:USD/JPY medium-term & major trend phases as of 22 Jul 2024 (Source: TradingView, click to enlarge chart)

After a bearish divergence condition sighted on the daily RSI momentum indicator on 3 July, there has been another negative price action following through on the USD/JPY.

It has staged a bearish breakdown below its 50-day moving average, the first time since 8 March 2024, and the lower boundary of the medium-term ascending channel in place since the 28 December 2023 swing low.

These negative observations suggest that USD/JPY may be on the brink of a potential multi-week corrective decline phase if its price action has another daily close below 156.50 that exposes the next medium-term pivotal support at 151.70 (also the 200-day moving average) (see Fig 4).

On the other hand, a clearance above 162.40 sees the continuation of the impulsive upmove sequence for the next medium-term resistances to come in at 164.20/164.90 and 167.10 next.

ECB’s Kazimir: Two more rate cuts this year not guaranteed

In an op-ed published today, ECB Governing Council member Peter Kazimir addressed market expectations for two additional rate cuts before the end of the year. He stated that while these market bets are "not entirely misplaced," they should not be considered a "given or a baseline scenario."

Kazimir highlighted that inflation is "on track" to return to the target but cautioned, "we are clearly not there yet." He emphasized the persistent risks of inflationary pressures due to various domestic and global factors. "There is still a non-negligible risk of inflationary pressures re-emerging," he noted.

"There is no need to rush our decisions," Kazimir added, advising a measured approach. "Enjoy the summer lull and wait for the much-anticipated September 'health check.' The upcoming data, combined with fresh forecasts, will set the stage for any necessary decisions."

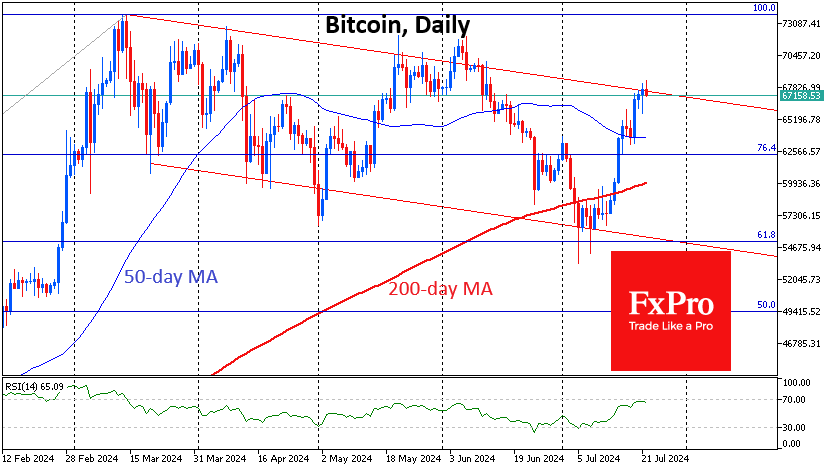

Crypto Rests After Another Rise

Market picture

The cryptocurrency market is near 6-week highs, with capitalisation near $2.44 trillion, adding 0.5% in the last 24 hours. A wait-and-see attitude and some profit-taking replaced active buying in the last three days starting Friday. Judging by the dynamics, the market prefers to stand still, waiting for new signals, which may be statements from politicians or important economic data scheduled for the second half of the week.

Bitcoin is trading near $67.2K, losing 0.7% since the beginning of the day. Growth has lost traction near the upper boundary of the descending channel resistance. Here, the first cryptocurrency may linger for a few days, staying within the pattern of the last five months. Prior to that, on Friday, the 50-day moving average served as an important support and launching pad for the latest growth momentum.

Bitcoin will need to overcome $71K to confirm the break of the downward consolidation, which we believe will be in the next few days. Also, during this retreat, there may be a new attempt to drag the price back below the 50-day MA (now near $63.7K).

News background

As a result of another recalculation, the mining difficulty of the first cryptocurrency increased by 3.21% – to 82.05T – after three weeks of decline. The average hashrate for the period since the previous value change was 646.59 EH/s.

The Chicago Board Options Exchange (CBOE) said the first five spot Ethereum-ETFs in the US will launch in just a few days – on 23 July. The SEC approved the launch of such funds on 23 May, but companies had to agree to a Form S-1 filing with the regulator before listing.

Binance CEO Richard Teng said Spot Ethereum-ETFs will provide stable and significant capital inflows over time. He also said product inflows are unlikely to be massive initially.

According to CryptoQuant, crypto whales with balances of 1,000 BTC or more bought 1.45 million coins worth $94 billion in 2024, with their total crypto wallet holdings growing to 1.8 million BTC. Meanwhile, investors continue to add 100,000 bitcoins to their wallets each week.

Julien Bittel, head of macroeconomic research at financial publication Global Macro Investor, said Bitcoin could reach $140K-$190K over the next twelve months. He pointed out the compression of the “Bollinger Bands” on the weekly chart, which has only been seen twice, in April 2016 and July 2023, and then led to a significant rise.

Speculation has begun on social media about a reserve bitcoin fund in the United States, which presidential candidate Donald Trump will allegedly announce at the Bitcoin 2024 conference in Nashville, which will be held from 25 to 27 July. It is expected that the basis for the US Bitcoin reserves will be the confiscated cryptocurrency in the amount of more than 213,000 BTC.