Sample Category Title

WTI Oil Outlook: Bears Taking a Breather After 4.3% Weekly Drop

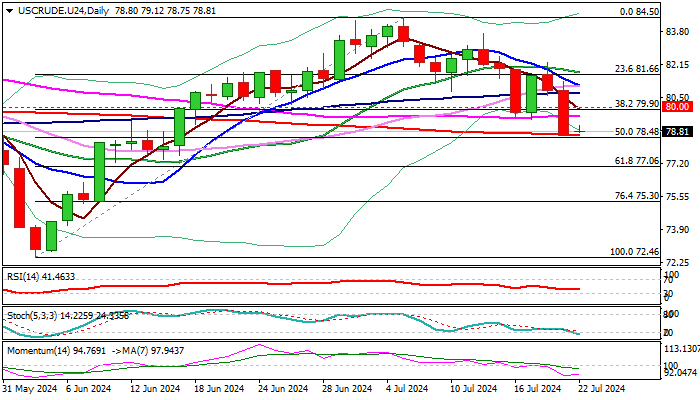

WTI oil price is holding within a narrow consolidation in early Monday, following sharp acceleration lower on Friday (down 2.8% for the day) and weekly loss of 4.3% (the biggest weekly drop since the last week of April.

Oil closed below $80 on Friday, for the first time in five weeks, with near-term action being weighed by large Friday’s and weekly bearish candles.

Friday’s drop was contained by 200DMA ($78.62), with oversold conditions on daily chart, prompting traders for a partial profit-taking.

Oil price was pressured by weaker than expected economic data from China which fueled fears about lower demand from the world’s second largest economy.

Market’s focus is shifting on Fed amid growing expectations that the US central bank would give firmer signals of the timing of the start of monetary policy easing cycle, during the policy meeting on July 30/31, with September seen as possible time to begin cutting interest rates.

Technical picture on daily chart is predominantly bearish, with corrective upticks to be ideally capped by psychological $80 barrier (also daily cloud top) to keep bears in play for further weakness below pivots at $78.62/48 (200DMA / 50% retracement of $72.46/$84.50).

Caution on break above $80 which would sideline immediate bears, but stronger acceleration higher and regain of $81.60/$82.00 zone will be required to revive bulls.

Res: 79.55; 80.00; 80.84; 81.16.

Sup: 78.62; 78.48; 77.06; 76.13.

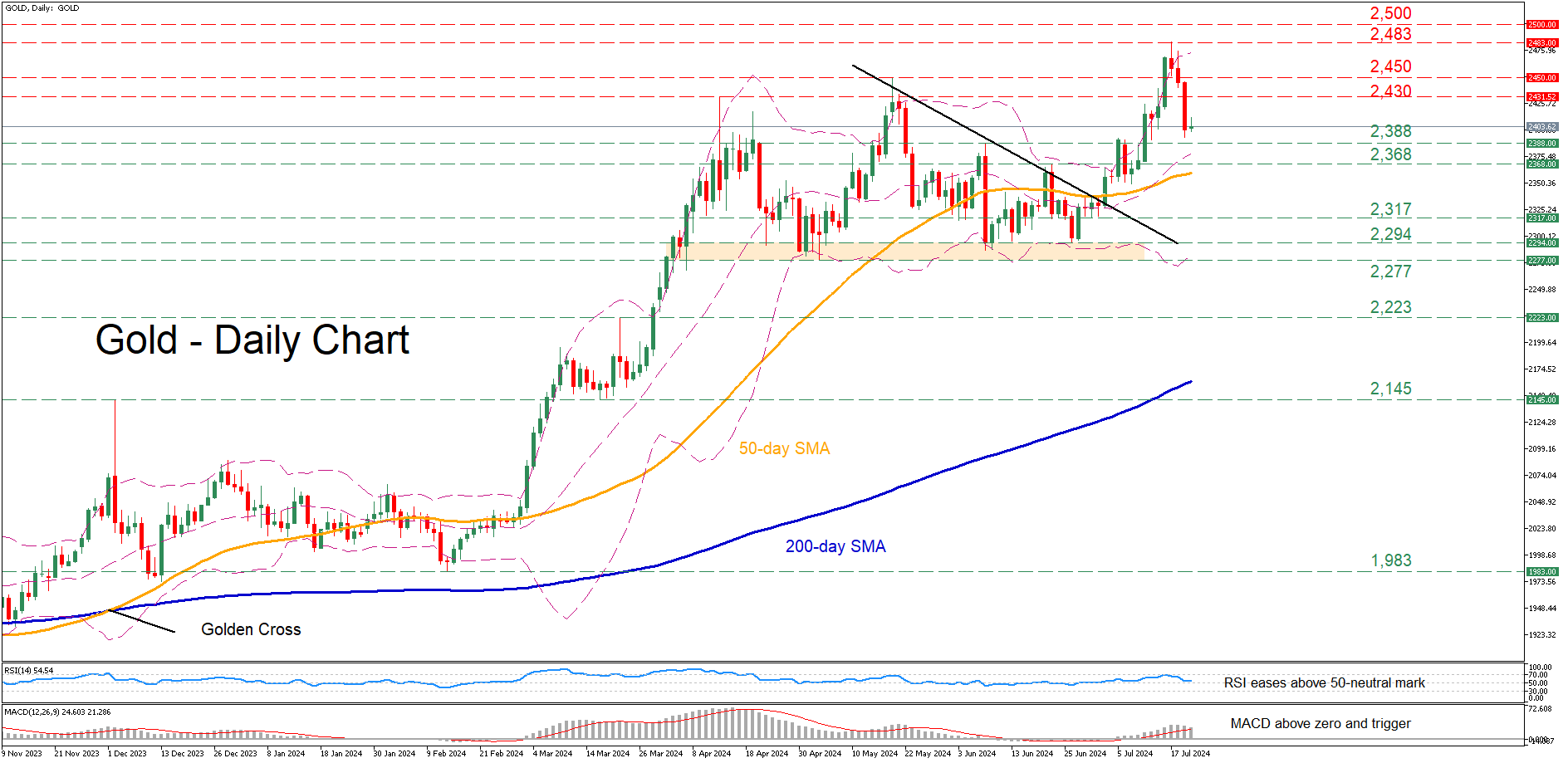

Gold Declines Sharply from All-time High

- Gold jumped to its highest level ever on July 17

- But reversed lower due to reaching overbought conditions

- Despite latest weakness, oscillators remain positively tilted

Gold had been in a steady uptrend since late May, which led to a fresh all-time high of 2,483 last week. However, the pair quickly corrected lower as the momentum indicators warned of an overstretched advance.

Should the pullback extend, the price could inch lower towards two previous resistance zones of 2,388 and 2,368, which could now serve as support. Further declines could then stall at 2,317, a region that held its ground both in June and July. Even lower, bullion might face the 2,294-2,277 range, defined by the May and June lows.

On the flipside, if the bulls attempt to strike back, immediate resistance could be found at the April high of 2,430. Surpassing that hurdle, gold might attempt to revisit its May high of 2,450. A violation of that zone could set the stage for the recent record peak of 2,483.

In brief, gold has been undergoing a pullback after its trip to all-time highs came to an end. Should the bears keep the pedal to the metal, the 50-day simple moving average (SMA) might quickly come under scrutiny.

Market Analysis: GBP/USD Trims Gains While USD/CAD Rallies

GBP/USD started a pullback from the 1.3050 zone. USD/CAD is rising and might aim for more gains above the 1.3735 resistance.

Important Takeaways for GBP/USD and USD/CAD Analysis Today

- The British Pound started a downside correction from the 1.3050 resistance zone.

- There is a key bearish trend line forming with resistance at 1.2940 on the hourly chart of GBP/USD at FXOpen.

- USD/CAD is showing positive signs above the 1.3700 support zone.

- There is a major bullish trend line forming with support at 1.3720 on the hourly chart at FXOpen.

GBP/USD Technical Analysis

On the hourly chart of GBP/USD at FXOpen, the pair struggled to continue higher above the 1.3050 resistance zone. The British Pound started a downside correction and traded below the 1.3010 support zone against the US Dollar.

The pair even traded below 1.2970 and the 50-hour simple moving average. Finally, the bulls appeared near the 1.2900 level. A low was formed at 1.2900 and the pair is now consolidating losses below the 23.6% Fib retracement level of the downward move from the 1.3044 swing high to the 1.2900 low.

Immediate resistance on the upside is near a key bearish trend line at 1.2940. The first major resistance is near the 1.2970 zone and the 50% Fib retracement level of the downward move from the 1.3044 swing high to the 1.2900 low.

The main hurdle sits at 1.3010. A close above the 1.3010 resistance might spark a steady upward move. The next major resistance is near the 1.3050 zone. Any more gains could lead the pair toward the 1.3120 resistance in the near term.

Initial support on the GBP/USD chart sits at 1.2900. The next major support sits at 1.2880, below which there is a risk of another sharp decline. In the stated case, the pair could drop toward 1.2840.

USD/CAD Technical Analysis

On the hourly chart of USD/CAD at FXOpen, the pair formed a strong support base above the 1.3660 level. The US Dollar started a fresh increase above the 1.3680 resistance against the Canadian Dollar.

The bulls pushed the pair above the 1.3700 and 1.3720 levels. The pair cleared the 50-hour simple moving average and climbed above 1.3735. A high was formed at 1.3747 and the pair recently corrected some gains.

There was a move below the 23.6% Fib retracement level of the upward move from the 1.3670 swing low to the 1.3747 high. Initial support is near a major bullish trend line at 1.3720.

The next major support is near 1.3700 or the 50% Fib retracement level of the upward move from the 1.3670 swing low to the 1.3747 high on the same USD/CAD chart. The main support sits near the 1.3660 zone.

A downside break below the 1.3660 level could push the pair further lower. The next major support is near the 1.3625 support zone, below which the pair might visit 1.3550.

If there is another increase, the pair might face resistance near the 1.3735 level. A clear upside break above 1.3735 could start another steady increase. The next major resistance is the 1.3750 level.

A close above the 1.3750 level might send the pair toward the 1.3785 level. Any more gains could open the doors for a test of the 1.3820 level.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

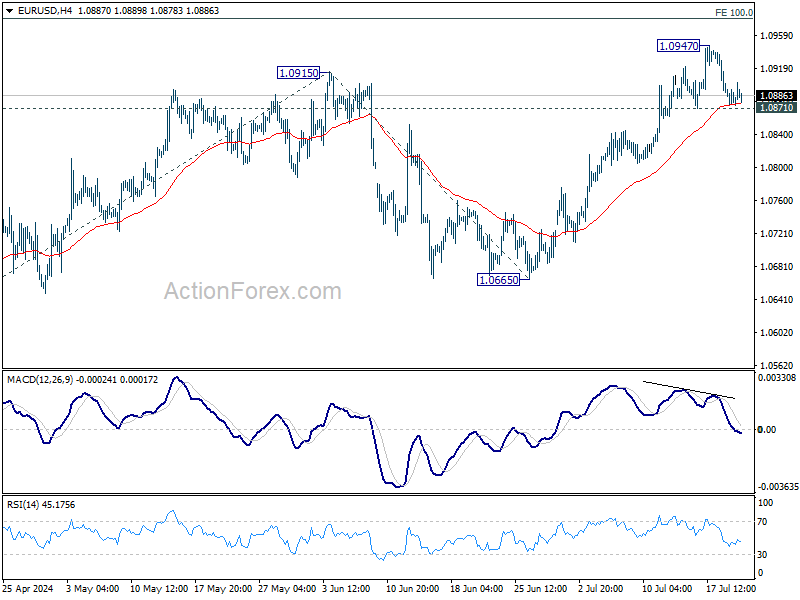

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0870; (P) 1.0889; (R1) 1.0903; More....

Intraday bias in EUR/USD stays neutral and further rise is in favor as long as 1.0871 minor support holds. Break of 1.0947 will target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. However, firm break of 1.0871 will turn bias to the downside for deeper fall to 55 D EMA (now at 1.0809) and possibly below.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

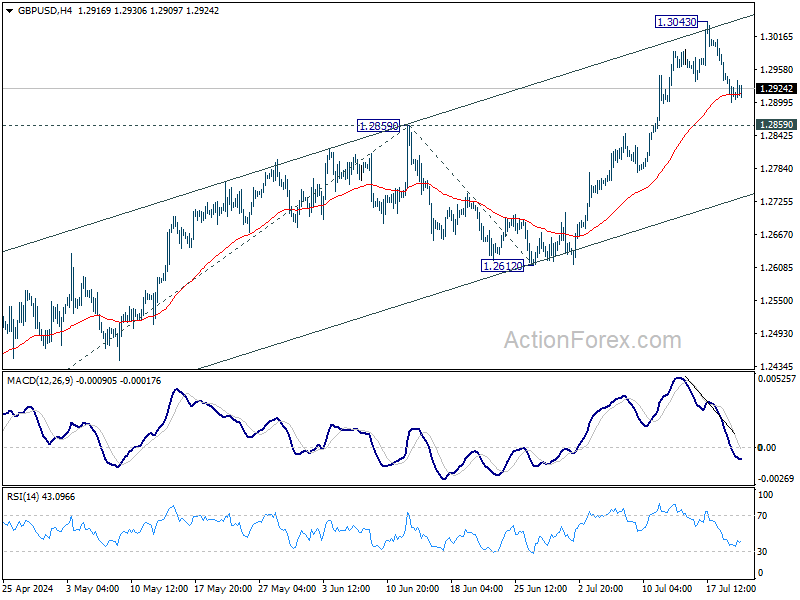

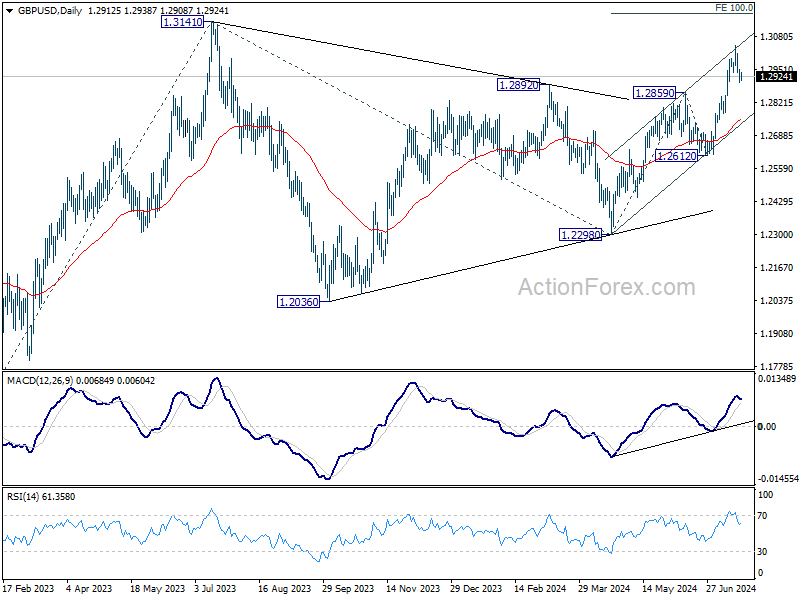

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2886; (P) 1.2930; (R1) 1.2958; More...

Intraday bias in GBP/USD remains neutral first. Downside of consolidations should be contained by 1.2859 resistance turned support to bring another rally. Break of 1.3043 will resume the rise from 1.2298 and target 100% projection of 1.2298 to 1.2859 from 1.2612 at 1.3173, which is slightly above 1.3141 key medium term resistance. However, firm break of 1.2859 will turn bias to the downside for deeper decline.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.

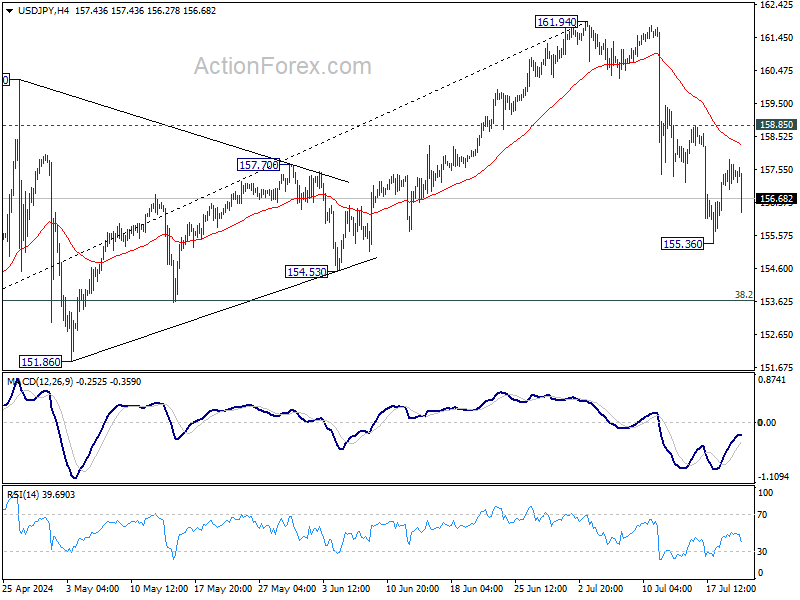

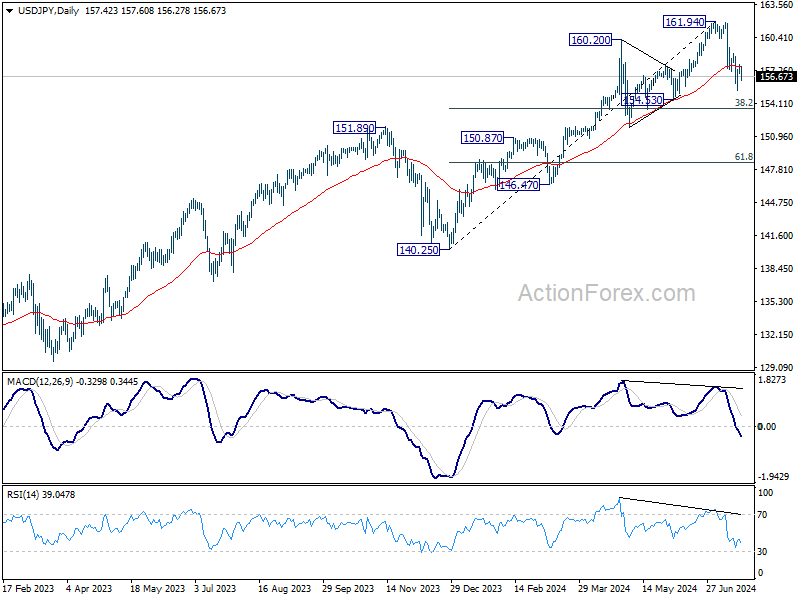

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.02; (P) 157.38; (R1) 157.78; More...

Intraday bias in USD/JPY stays neutral and further decline is expected with 158.85 resistance intact. Below 155.36 will target 38.2% retracement of 140.25 to 161.94 at 153.65. On the upside, above 158.85 resistance will turn bias back to the upside for stronger rebound instead.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

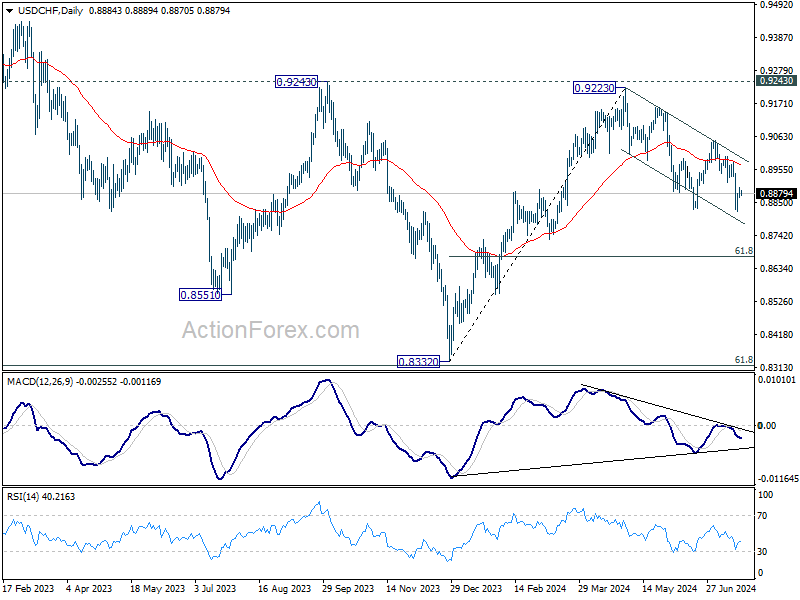

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8867; (P) 0.8884; (R1) 0.8908; More…

Intraday bias in USD/CHF remains neutral at this point. Further decline is in favor as long as 0.8914 support turned resistance holds. Break of 0.8819 will target 61.8% retracement of 0.8332 to 0.9223 at 0.8672 next. However, break of 0.8914 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

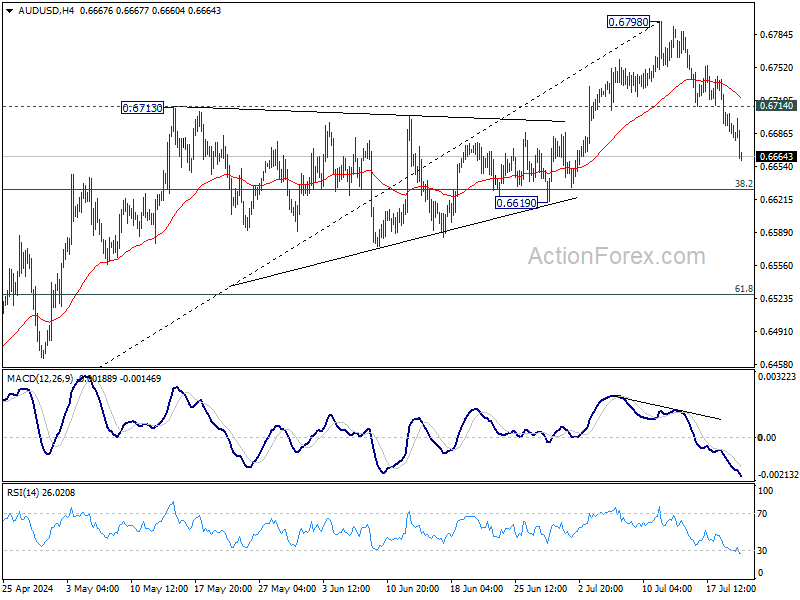

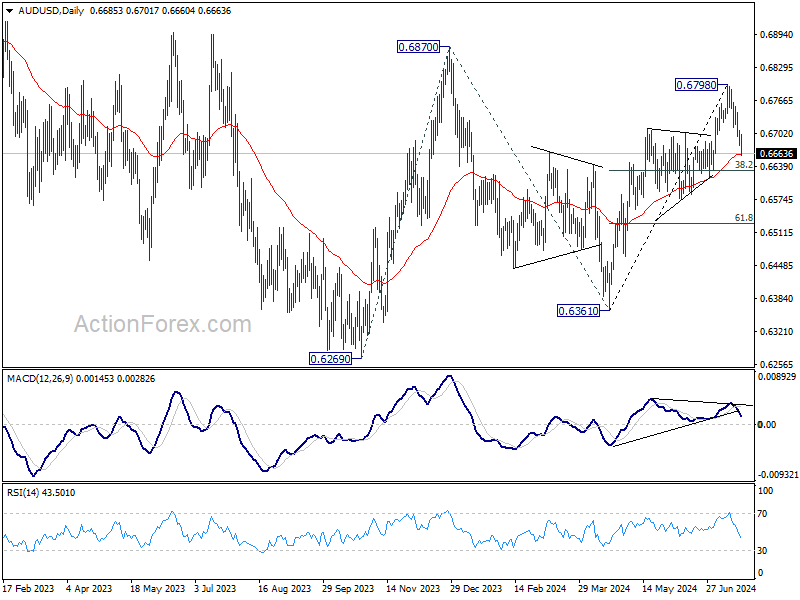

AUD/USD Daily Report

Daily Pivots: (S1) 0.6672; (P) 0.6693; (R1) 0.6707; More...

Intraday bias in AUD/USD remains on the downside. Fall from 0.6798 short term top is in progress for 38.2% retracement of 0.6361 to 0.6798 at 0.6631. Strong support would be seen there to bring rebound. On the upside, above 0.6714 minor resistance will turn bias back to the upside for retesting 0.6798. However, sustained break of 0.6631 will bring deeper fall to 61.8% retracement at 0.6528 instead.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg. Break of 0.6870 will target 100% projection of 0.6269 to 0.6870 from 0.6361 at 0.6962.

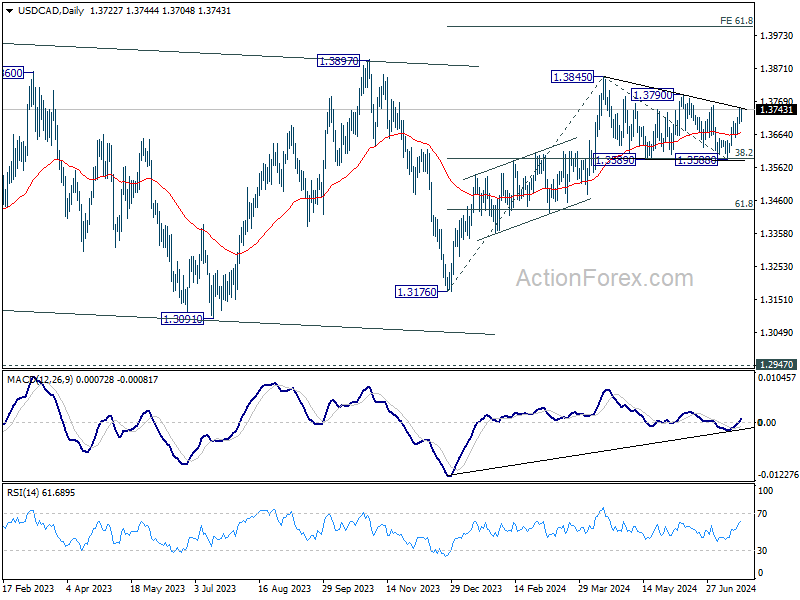

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3703; (P) 1.3725; (R1) 1.3752; More...

Intraday bias in USD/CAD remains on the upside for the moment. Corrective pattern from 1.3845 might have completed with three waves to 1.3588, after hitting 38.2% retracement of 1.3716 to 1.3845 at 1.3589. Further rise should be seen to 1.3790 resistance first. Firm break there will likely resume whole rally from 1.3176 to 61.8% projection of 1.3176 to 1.3845 from 1.3588 at 1.4025. Nevertheless, break of 1.3670 minor support will dampen this bearish case.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

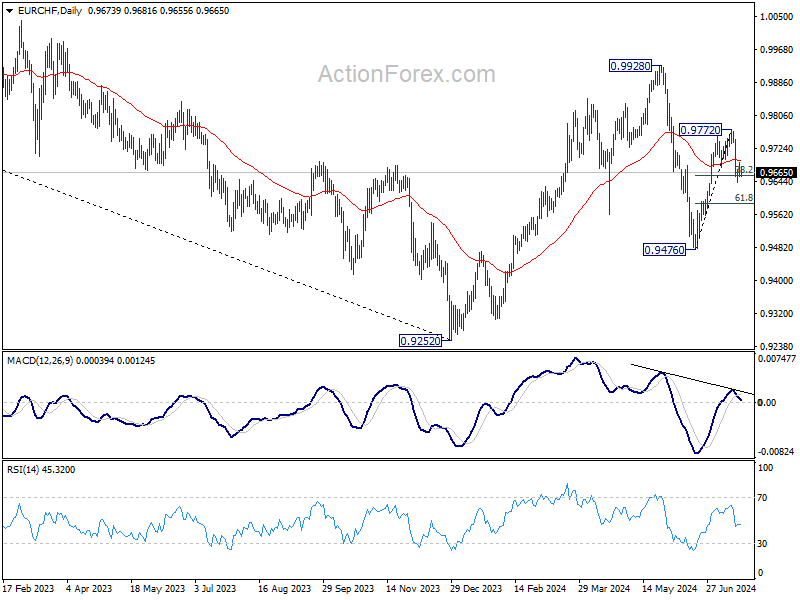

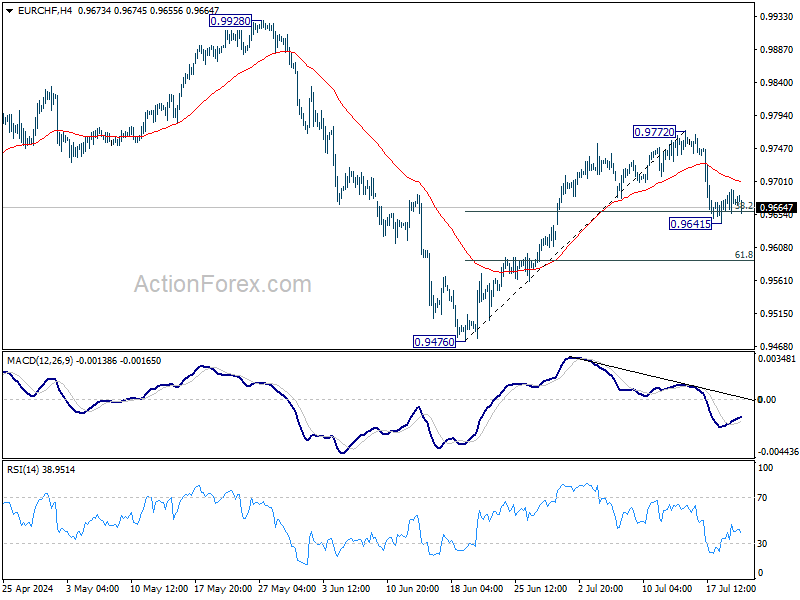

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9644; (P) 0.9668; (R1) 0.9698; More....

Intraday bias in EUR/CHF stays neutral for the moment. Strong bounce from current level will maintain near term bullishness. Break of 0.9972 will resume the rally from 0.9772. However, firm break of 38.2% retracement of 0.9476 to 0.9772 at 0.9659 will extend the fall from 0.9772 to 61.8% retracement at 0.9589 and possibly below.

In the bigger picture, rebound from 0.9252 medium term bottom might not be completed yet. But even in case of resumption, strong resistance could emerge from 1.0095 to limit upside. Medium term outlook will be neutral at best as long as 1.0094 structural resistance holds. Meanwhile, break of 0.9476 will bring retest of 0.9252 low.