Sample Category Title

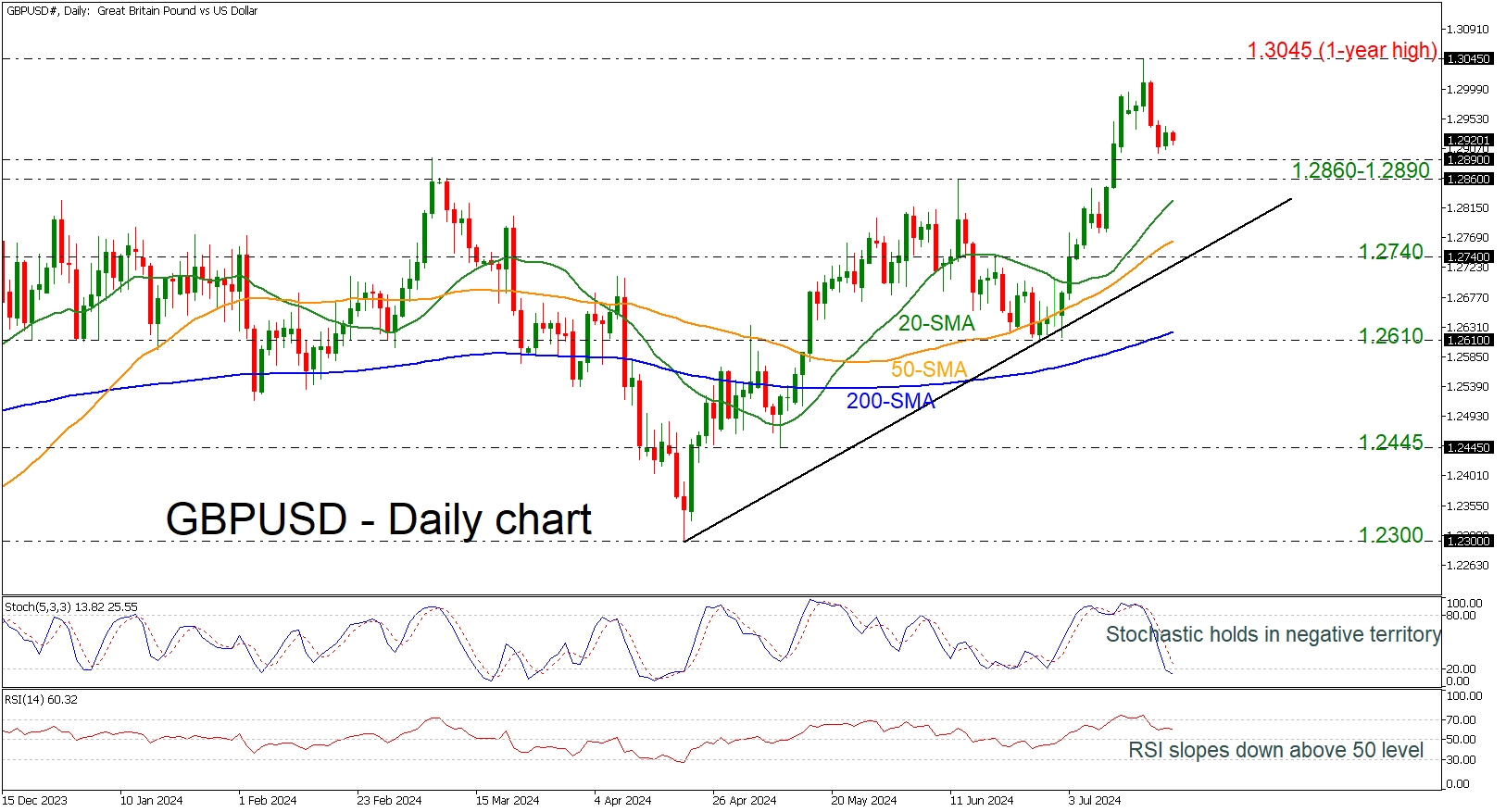

GBPUSD Holds Well Below the 1-year High

- GBPUSD eases but remains above uptrend line

- Stochastics and RSI suggest more losses

GBPUSD is retreating after a strong rally towards the one-year high of 1.3045. The technical oscillators also confirm the bearish retracement. The stochastic is diving into oversold territory, while the RSI is pointing slightly down above the 50 level.

If the dive continues, immediate support could come from the 1.2860–1.2890 region, ahead of the 20-day simple moving average (SMA) at 1.2825. Steeper declines could pave the way for a retest of the 50-day SMA at 1.2760 and the ascending trend line near 1.2740.

In a positive scenario, a rebound from 1.2890 may take the price higher again, testing the previous peak at 1.3045. More upside pressures could push the market to its peak of 1.3140 in July 2023.

Summarizing, GBPUSD has been exhibiting a bullish tendency since April 22, and only a closing session beneath the 200-day SMA could change this outlook.

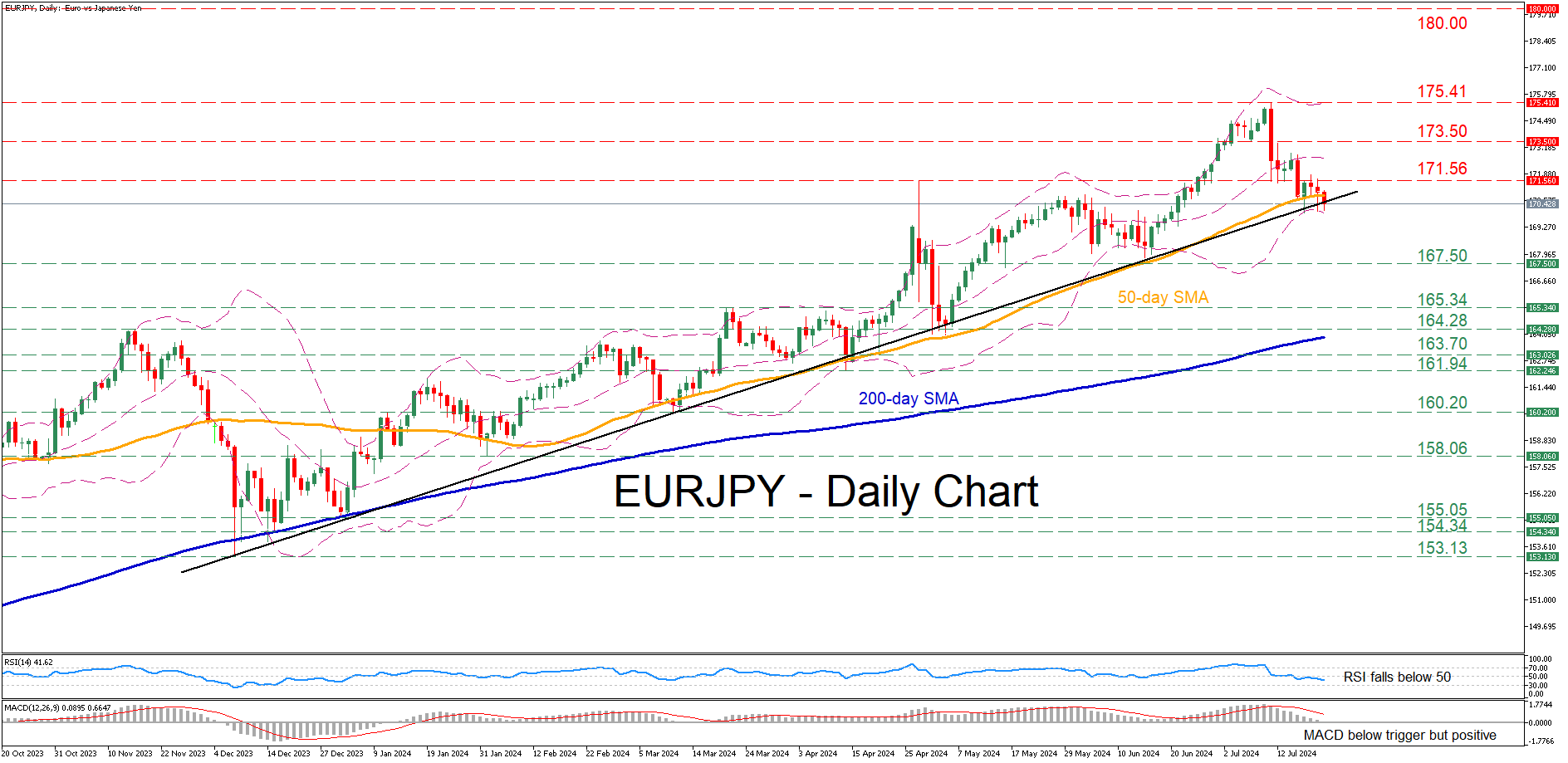

EURJPY Extends Pullback from 32-year High

- EURJPY jumped to its highest since January 1992 on July 11

- But is trending lower since then due to Japanese intervention

- Oscillators deteriorate significantly, suggesting bearish bias

EURJPY has been in an uptrend since the beginning of the year, storming to a fresh 32-year peak of 175.41. Nevertheless, the pair experienced a pullback following a currency intervention from Japan, with the retreat extending towards the 50-day simple moving average (SMA) and ascending trendline in place since December 2023.

Should bearish pressures persist and the pair violate the upward sloping trendline, the June support of 167.50 could act as the first line of defence. A break below that zone could trigger a retreat towards 165.34 or 164.28, two previous resistance regions that could serve as support in the future.

On the flipside, if the price edges back higher, the April high of 171.56 may prevent initial advances. Higher, the pair could meet resistance at 173.50 ahead of its 32-year peak of 175.41. Conquering this barricade, the bulls could then attack the 180.00 psychological level.

In brief, EURJPY has been undergoing a steady correction following its 32-year peak of 175.41, with the pair currently challenging a crucial technical zone. Hence, a break below the fortified region that includes the 50-day SMA and ascending trendline could further deteriorate the technical picture.

Outcome of Expected Contest Between Trump and Harris Too Early To Call

Markets

US President Biden stepping out of the presidential election race dominated press/market headlines yesterday. Still, the direct impact on global trading was modest after all. For now, the outcome of an expected contest between Donald Trump and Kamala Harris is too early to call. It is even more difficult to assess the concrete impact of post-election policy both the economy and a fortiori what it might mean for (global) markets trading. Equities had a good start to the new week (S&P +1.08%, Nasdaq +1.58%, EuroStoxx 50 +1.45%). However, coming on the back of a rather forceful correction last week and with investors looking forward to the earnings’ season, it’s unclear how much of this rebound was due to the political developments in the US. US and European yields extended last week’s bottoming out process. US yields rose marginally between 0.6 bps (2-y) and 2.5 bps (30-y). With an inaugural September 25 bps Fed rate cut almost fully discounted and more than one additional step priced for the end of the year, markets currently see no reason anticipate an even more aggressive Fed U-turn compared to the June dots (one 25 bps step this year). For that to happen, more soft US data and/or more concrete Fed guidance is probably needed. Bunds underperformed Treasury with German yields rising between 4.6 bps (2-y) and 1.5 bps (30-y). Markets are adapting to the message from last week’s ECB press conference that everything is open with respect to an additional ECB rate cut in September. Despite a (small) loss of relative interest rate support and a risk-on sentiment, the dollar only lost modest ground (DXY 104.30 from 104.39 on Friday, EUR/USD 1.0891 from 1.0882). The yen again marginally outperformed (close USD/JPY 157 area). Sterling showed signs of bottoming after a correction last week supported by tentatively higher UK yields (2-y + 5.9 bps). EUR/GBP closed at 0.842.

Asian markets (ex-China) this morning show a mild risk-on in the wake of yesterday’s WS rebound. The yen extends its rebound (USD/JPY 156.4). EUR/USD is going nowhere. US yields decline marginally (+/- 1 bp).

Eco data in the US (Richmond Fed manufacturing index, existing home sales) and E(M)U (EC consumer confidence) only are of intraday significance, at best. ECB’s Lane will speak. Equity investors will keep a close eye at earnings of Alphabet & Tesla. We assume more technical inspired trading with the preliminary PMI’s (tomorrow) and the first estimate of US GDP (including price deflators) on Thursday further shaping market expectations going into next week’s Fed, BOJ and BoE policy meetings. For now, we expect recent lows in US and EMU yields to hold. The dollar shows no clear trend. In other countries, the Central bank of Turkey (CBRT) and the National Bank of Hungary (MNB) will announce policy decisions today. The CBRT is expected to keep the policy rate unchanged at 50% but might take additional measures to reduce excess liquidity. Comments from MNB vice governor Virag last week suggested that there is still room for some guarded easing as inflation is still cooling (3.7% in June) and as the forint continues to hold up rather well. We expected an MNB rate cut from 7.0% to 6.75%.

News & Views

Car manufacturers and dealers in the US are increasingly cutting prices in an attempt to offset demand dented by high interest rates and to clear inventories at pre-pandemic levels. Auto data provider Motor Intelligence said that incentive packages, which include cash backs, low interest rates and price cuts, rose 53% y/y in June. Their efforts have been showing up in US inflation figures with the cost of new and used vehicles having fallen by 0.2% and 1.5% m/m respectively. The report adds to evidence that the Fed’s restrictive monetary policy is increasingly weighing on consumer demand, especially for big-ticket items.

Top Japanese lawmaker Toshimitsu Motegi is calling upon the Bank of Japan to more clearly reveal its monetary policy normalization intentions. Motegi is Secretary-General of the ruling Liberal Democratic Party (LDP) and shared growing frustrations among party members that the BoJ’s snail pace, even with inflation above target, is hurting the yen and biting in Japanese consumer’s purchasing power. Motegi’s remarks are closely watched. He’s seen as a possible contender with good odds in the September LDP leadership race. The outcome of the race ultimately determines who will be prime minister of Japan. The Bank of Japan is meeting July 31.

Graphs

GE 10y yield

The ECB cut its key policy rates by 25 bps at the June policy meeting. A more bumpy inflation path in H2 2024, the EMU economy gradually regaining traction and the Fed’s higher for longer US strategy make follow-up moves difficult. Markets are coming to terms with that. Meanwhile, much of the save haven bids were reversed after the (first round in) the French elections. The 2.34%-2.4% support zone looks solid.

US 10y yield

The Fed indicated that it needs more evidence to lower its policy rate. June dots suggested one move in 2024 and four next year. Disappointing ISM and back-to-back downward CPI surprises put the US money market back on (at least) two rate cuts this year (September/December). The US 10-yr yield tests the recent lows and the downside of the downward trend channel in the 4.2% area.

EUR/USD

EUR/USD is testing the topside of the 1.06-1.09 range as the dollar loses interest rate support at stealth pace. Markets consider a September rate cut a done deal and only need confirmation from high-ranked Fed officials. In the meantime, the euro got rid of the (French) political risk premium. Risks of a topside break have increased, bringing the psychologic 1.10 and the December 2023 top at 1.1139 on the radar.

EUR/GBP

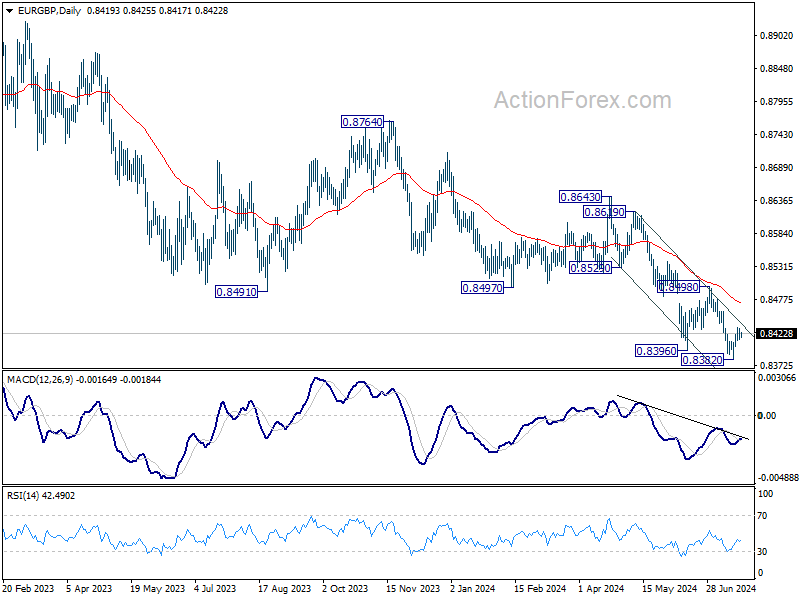

Debate at the BOE is focused at the timing of rate cuts. May headline inflation returned to 2%, but core measures weren’t in line with inflation sustainably returning to target any time soon. Still some BoE members at the June meeting appeared moving closer to a rate cut. Labour has yet to reveal its policy plans after securing a landslide election victory. EUR/GBP 0.84 support is being tested.

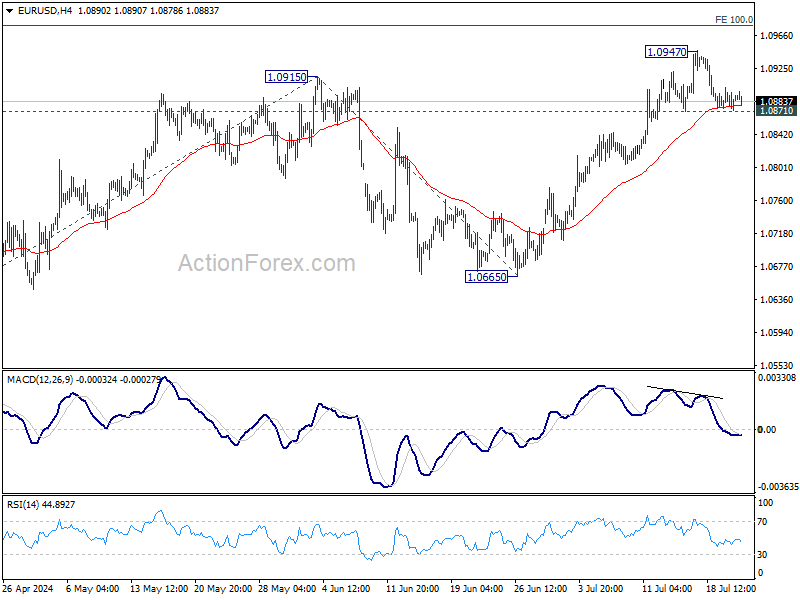

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0875; (P) 1.0889; (R1) 1.0905; More....

Intraday bias in EUR/USD remains neutral and further rise is in favor as long as 1.0871 minor support holds. Break of 1.0947 will target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. However, firm break of 1.0871 will turn bias to the downside for deeper fall to 55 D EMA (now at 1.0810) and possibly below.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

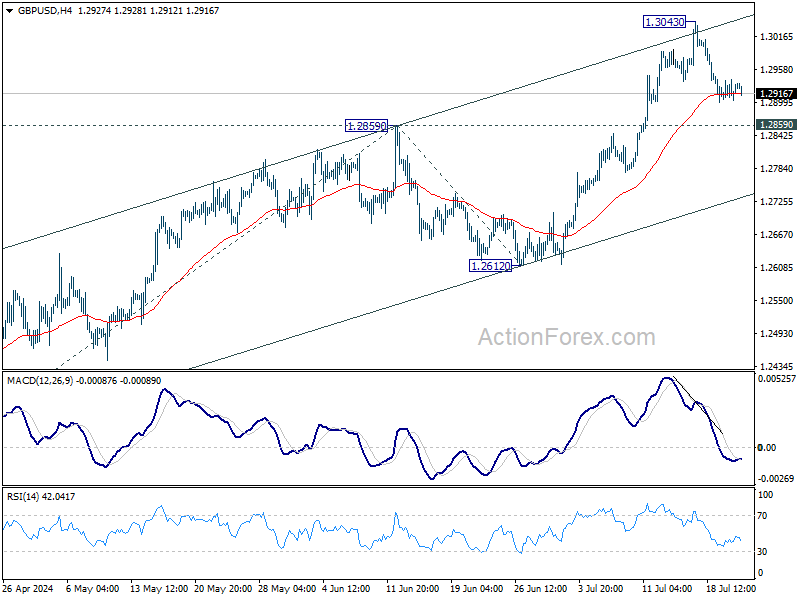

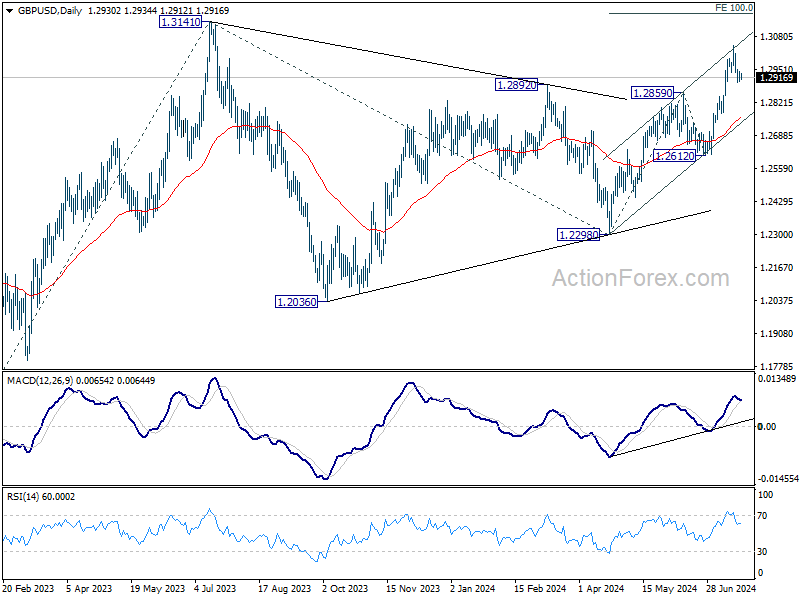

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2912; (P) 1.2927; (R1) 1.2949; More...

GBP/USD is extending consolidation from 1.3043 and intraday bias remains neutral. Downside should be contained by 1.2859 resistance turned support to bring another rally. Break of 1.3043 will resume the rise from 1.2298 and target 100% projection of 1.2298 to 1.2859 from 1.2612 at 1.3173, which is slightly above 1.3141 key medium term resistance. However, firm break of 1.2859 will turn bias to the downside for deeper decline.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.

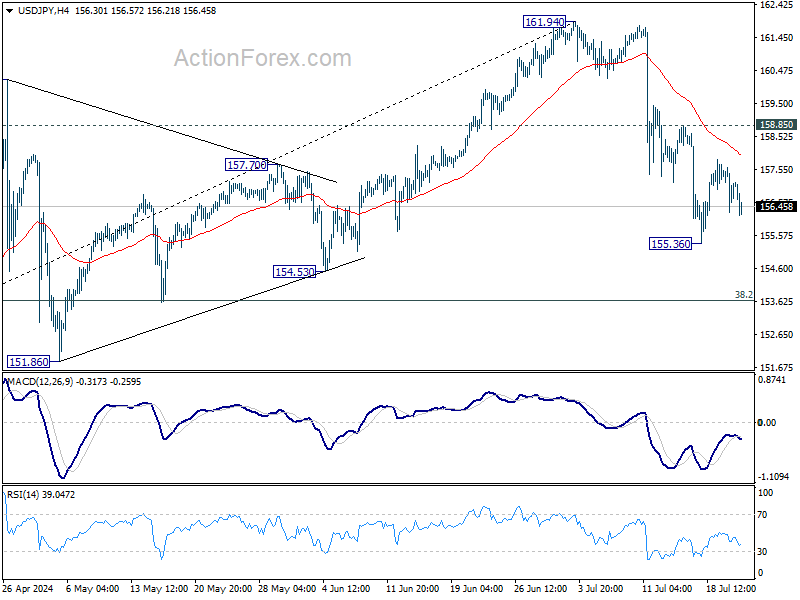

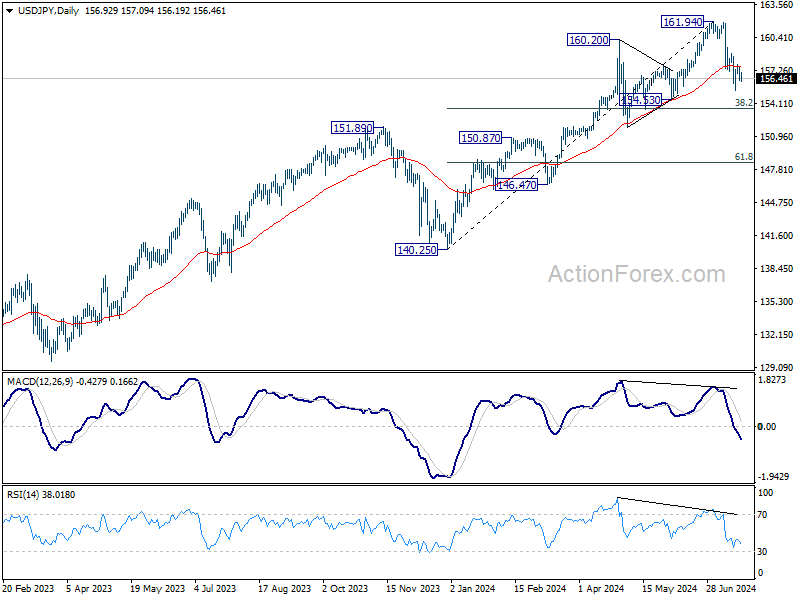

USD/JPY Daily Outlook

Daily Pivots: (S1) 156.37; (P) 156.99; (R1) 157.69; More...

Intraday bias in USD/JPY remains neutral as range trading continues above 155.36. Further decline is expected with 158.85 resistance intact. Below 155.36 will target 38.2% retracement of 140.25 to 161.94 at 153.65. On the upside, above 158.85 resistance will turn bias back to the upside for stronger rebound instead.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

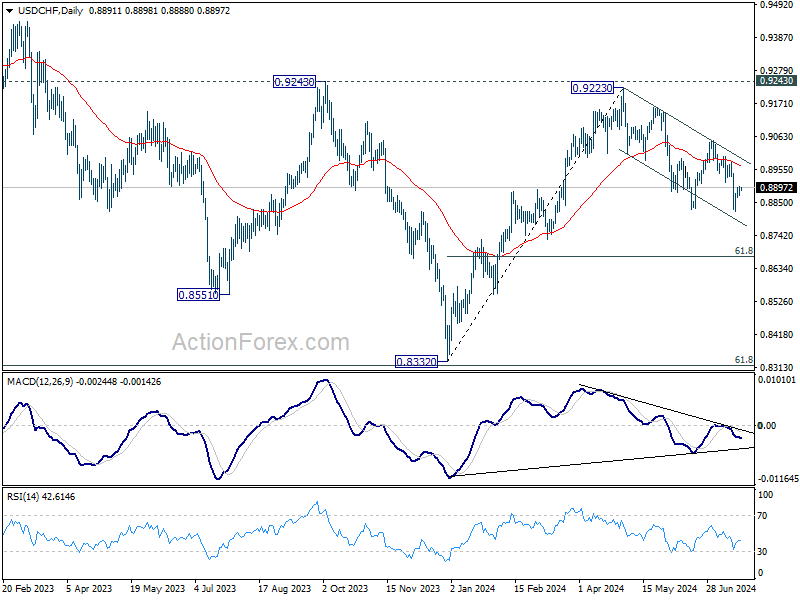

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8878; (P) 0.8890; (R1) 0.8909; More…

Intraday bias in USD/CHF remains neutral first as range trading continues above 0.8819. Further decline is in favor as long as 0.8914 support turned resistance holds. Break of 0.8819 will target 61.8% retracement of 0.8332 to 0.9223 at 0.8672 next. However, break of 0.8914 will turn bias back to the upside for stronger rebound instead.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

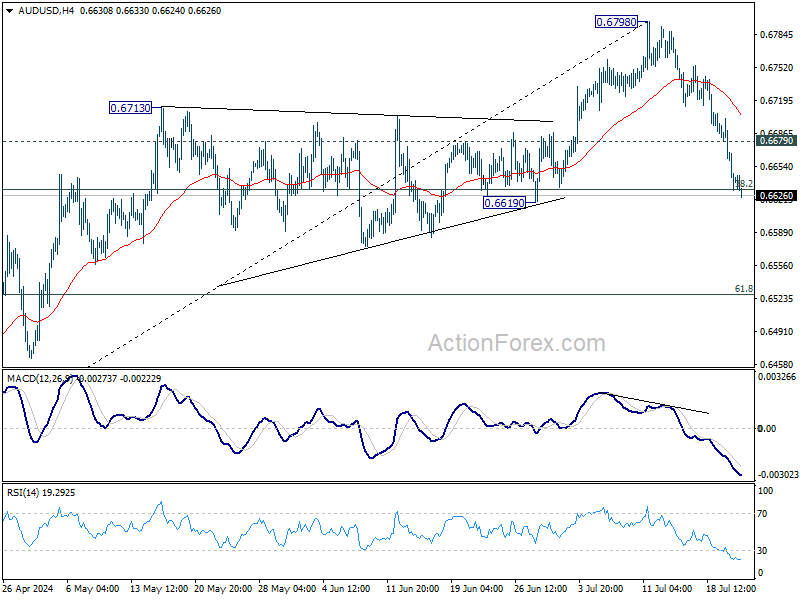

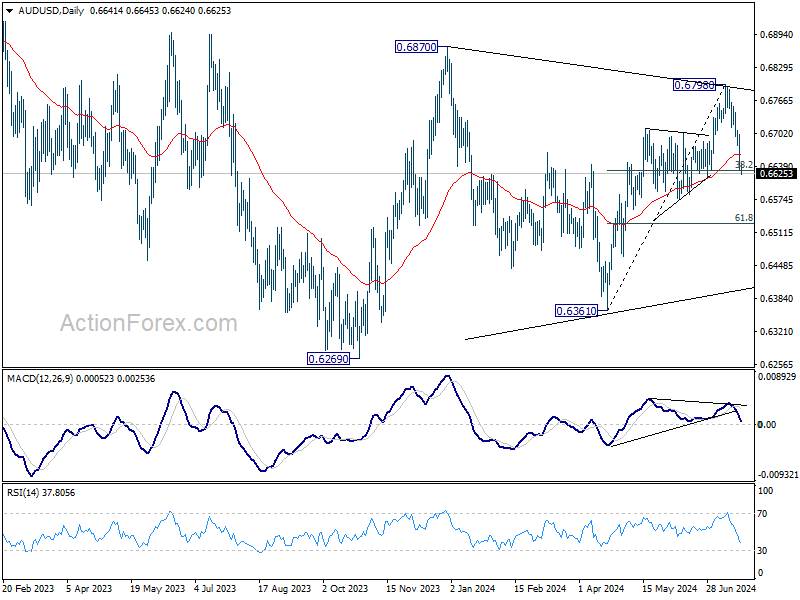

AUD/USD Daily Report

Daily Pivots: (S1) 0.6615; (P) 0.6658; (R1) 0.6686; More...

Intraday bias in AUD/USD as fall from 0.6798 continues to accelerate lower. Sustained trading below 38.2% retracement of 0.6361 to 0.6798 at 0.6631 will raise the chance of near term bearish reversal. Next target will be 61.8% retracement at 0.6528. On the upside, above 0.6679 minor resistance will turn intraday bias neutral first.

In the bigger picture, overall, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern, which is still extending. Break of 0.66870 resistance will extend the rising leg from 0.6269 towards 0.7156 (2023 high). However, break firm break of 0.6619 support will argue that another falling leg has started back towards lower side of the range between 0.6169/6361.

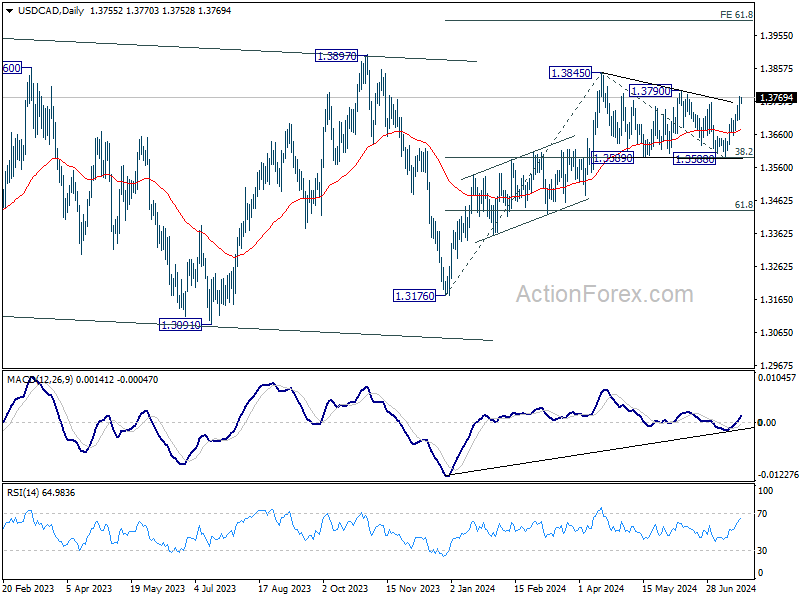

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3716; (P) 1.3746; (R1) 1.3786; More...

Intraday bias in USD/CAD stays on the upside and outlook is unchanged. Corrective pattern from 1.3845 might have completed with three waves to 1.3588, after hitting 38.2% retracement of 1.3716 to 1.3845 at 1.3589. Further rise should be seen to 1.3790 resistance first. Firm break there will likely resume whole rally from 1.3176 to 61.8% projection of 1.3176 to 1.3845 from 1.3588 at 1.4025. Nevertheless, break of 1.3704 minor support will dampen this bearish case.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

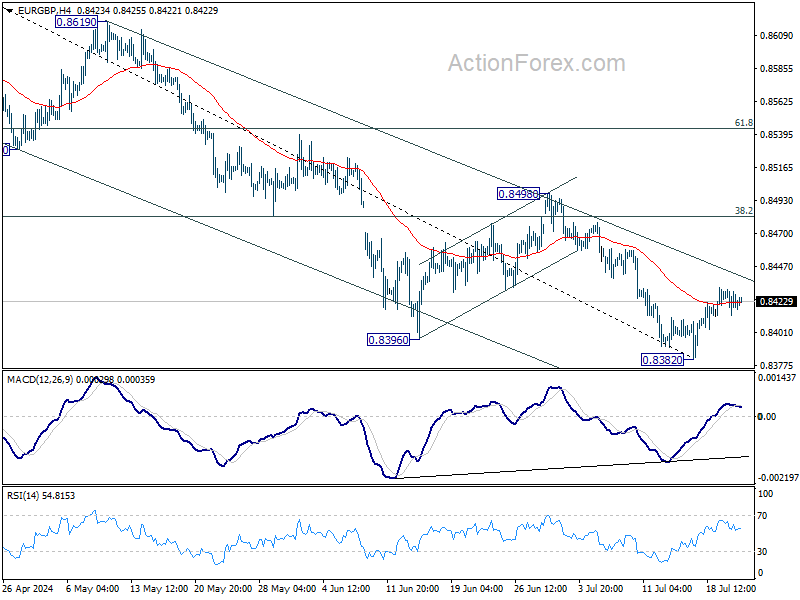

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8413; (P) 0.8422; (R1) 0.8431; More....

Intraday bias in EUR/GBP is turned neutral again with 4H MACD crossed below signal line. While rebound from 0.8382 could extend higher, outlook will stay bearish as long as 0.8498 resistance holds. Larger down trend should resume through 0.8382 at a later stage.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 key support (2022 low). For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.