Sample Category Title

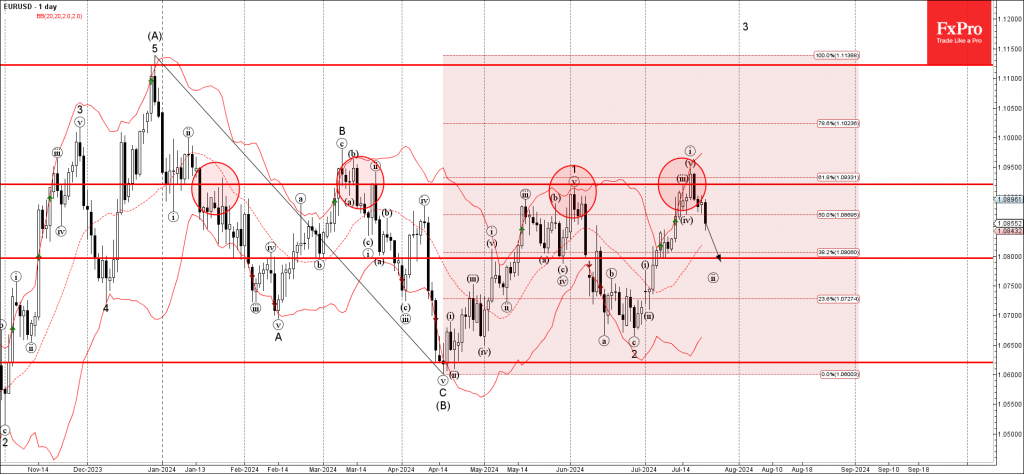

EURUSD Wave Analysis

- EURUSD reversed from resistance area

- Likely to fall to support level 1.0800

EURUSD currency pair recently reversed down from the resistance area set between the multi-month resistance level 1.0920 (which has been reversing the price from the start of this year), upper daily Bollinger Band and the 61.8% Fibonacci correction of the downward wave B from December.

The downward reversal from this resistance area created the daily Japanese candlesticks reversal pattern Bearish Engulfing – which started the active wave ii.

EURUSD currency pair can be expected to fall further to the next support level 1.0800 (target price for the completion of the active wave ii.

EUR/JPY Outlook: Collapses to Five-Week Low on BoJ Rate Hike Signals

EURJPY fell nearly 1% on Tuesday, as yen rose across the board on hawkish talks which may prompt BoJ for more rate hikes.

The pair broke below psychological 170 support, hitting the lowest levels in five weeks and cracked Fibo 76.4% retracement of 167.52/175.42 upleg.

Technical picture weakened further on daily chart, with daily close below 170 handle to add to negative stance.

Bears focus significant support at 169.00 (top of thick rising daily cloud), with penetration of cloud to open way for full retracement of 167.52/175.42 bull-leg.

Meanwhile, bears may face headwinds from daily cloud and pause for consolidation, with 170 level now acting as solid resistance which should ideally cap and keep intact next significant barrier at 170.54 (55DMA/broken Fibo 61.8%).

Res: 170.00; 170.54; 171.00; 171.47.

Sup: 169.00; 168.00; 167.52; 166.92.

Sunset Market Commentary

Markets

Another empty daily calendar left investors to their own devices with central bank meetings in Hungary (-25 bps to 6.75%, as expected) and Turkey (unchanged at 50%, cfr. infra) offering some distraction in non-core areas. That resulted in core bonds gaining ground after three days of losses. German Bunds outperformed US Treasuries this time around. Excluding the 2-yr yield (-10 bps due to a benchmark change), yields decline between 4 and 5.5 bps. ECB’s de Guindos was the latest to chip in after last week’s (uninspiring) policy meeting. The vice-president said the huge level of uncertainty warrants prudence when setting rates. He referred to the September meeting, which produces new forecast, as a “much more convenient month for taking decisions”. He noted that “All measures of underlying inflation are coming down” and that wages are slowing down as well. This will show up in services inflation (4.1% in June) eventually. US yield moves varied between -1.5 and -1.9 bps in technically insignificant trading. Stocks in Europe still eke out a gain to the tune of 0.4% but are off intraday highs. Wall Street opened little changed, awaiting the earnings release of tech bellwethers including Google parent Alphabet and Tesla as well as consumer discretionary giant LVMH after market.

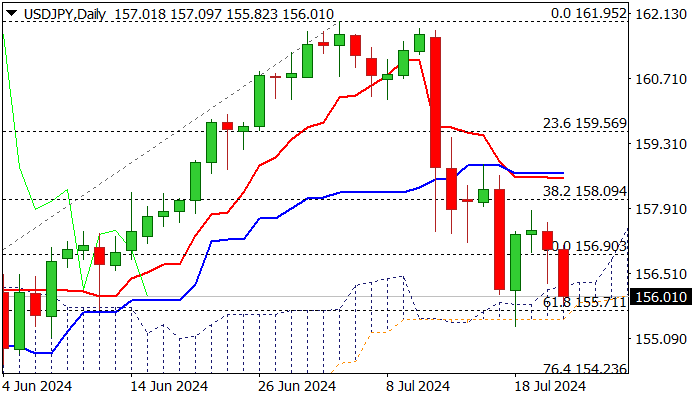

The Japanese yen for a second day straight takes the lead on currency markets. USD/JPY is on track for the lowest close around 156.1 since early June. EUR/JPY slipped through the 170 barrier and in doing so is testing the lower bound of the 2024 upward trading channel. The Norwegian krone lags G10 peers with oil prices extending the July correction to $81.65 (Brent) currently. The euro is weighed down by falling European/German yields. EUR/USD drops to 1.0854 from an open just south of 1.09. Sterling erases much of the losses incurred last week to trade around the levels seen just before the higher-than-expected CPI release. EUR/GBP is filling offers at 0.84.

News & Views

Vice governor Jan Fait of the Czech National Bank (CNB) in an interview indicated that the focus at the August 1 policy meeting will be on a 25 bps rate cut as the CNB is approaching the point of finetuning its policy. Even so, he didn’t also didn’t completely rule out another 50 bps step as inflation in June was again softer than expected (-0.3% M/M and 2.0% Y/Y). Frait sees room for the CNB to cut rates from 4.75% now to around 4.0% ‘give or take 25 bps’ at the end of the year. With respect to the economy, he indicated that household consumption, investment activity and demand for Czech exports are rather weak and not generating substantial demand-led inflationary pressures. A tight labour market is a good reason to proceed cautiously with monetary policy easing. He assess the koruna currently a bit weaker than fundaments imply. This is not a reason to be afraid to at least consider a 50 bps cut next week. With respect to the neutral rate, also Jan Frait sees this as probably being a bit higher than the 3.0% level currently used in the CNB model. The koruna today weakened further to EUR/CCZK 25.38 from 25.25 and is nearing the weakest levels YTD against the euro (25.52 mid-February).

The Central Bank of Turkey (CBRT) as expected kept its policy rate on hold at 50% for the fourth consecutive meeting. The CBRT welcomes the decline in the underlying trend of monthly inflation in June (headline 1.64% M/M and 71.60% Y/Y from 3.37% M/M and 75.45% in May). The CBRT expects a temporary uptick in July due to external factors (administered prices, taxes, food prices), but sees the underlying inflation to stay relatively limited. Domestic demand is slowing down but still at inflationary levels. In this respect, the MPC remains highly attentive to inflationary risks. The tight monetary stance will be maintained until a significant and sustained decline in the underlying trend of monthly inflation is observed, and inflation expectations converge to the projected forecast range. A tight monetary stance is expected to bring down the underlying trend of monthly inflation through moderation in domestic demand, a real appreciation in Turkish lira and improving inflation expectations. The CBRT adds that the monetary transmission mechanism will continue to be supported via additional macroprudential measures, while sterilization will be implemented effectively by enriching the toolset whenever needed. The lira extends recent tentative gains trading near EUR/TRY 35.74.

Graphs

EUR/HUF: forint ends appreciation streak after central bank banks on slower-than-expected inflation by cutting rates to 6.75%

USD/JPY on track for lowest close since early June. JPY against EUR is testing lower bound of upward trading range.

EUR/TRY: “decisive” monetary policy stance, including an unchanged 50% policy rate, is not bringing the lira much support

European 2-yr swap yield struggles near recent lows, trying to keep the 3% clean

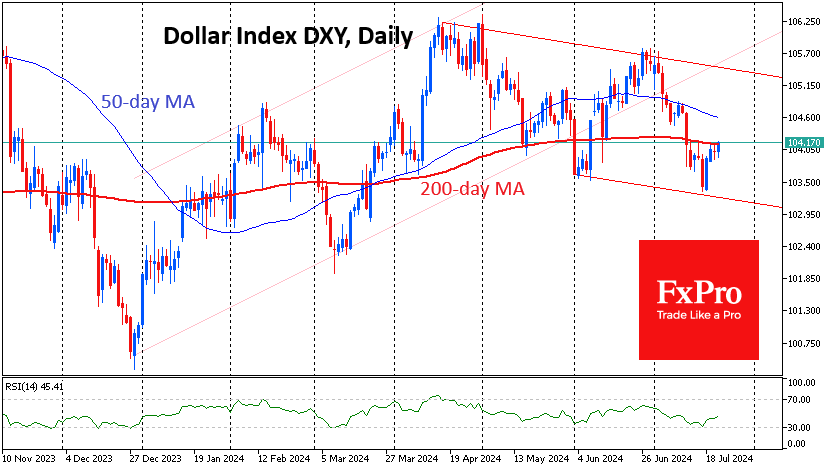

Dollar Bears Paused, Breaking the Uptrend

Last week, the dollar index regained some of its losses from the previous four weeks, but technically, it looks like short-term profit-taking by sellers before a new downward momentum.

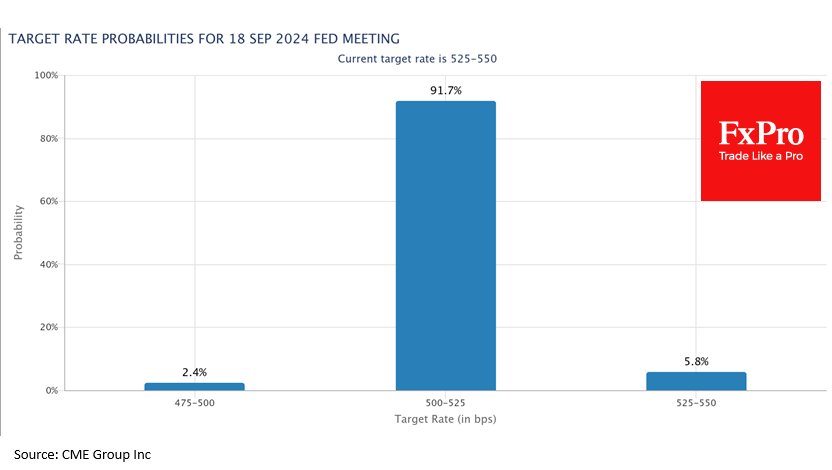

The US dollar has been under pressure since late June as the Fed noted progress in reducing inflation. Money markets readily accepted this signal, giving a 94% probability of a rate cut in September versus 66% a month earlier and just 46% about two months ago. These changes are causing short-term bond yields to fall, reducing interest in the dollar.

Changes in expectations have taken about 2% away from the dollar over the past month. But on this downward path, the DXY has taken several technical levels, showing increasing signs of moving into a downward trend.

Sustained pressure on the dollar since early July has knocked it out of the upward channel formed by the lows of December and March and the highs of February and April. Moreover, a descending corridor is formed, with the upper boundary passing through the peaks of April and June and the lower boundary passing through the lows of June and July.

At last week’s lows, DXY has stepped up from the lower boundary of the trading range, removing some of the local oversold conditions.

For the past ten days, the rise in the Dollar Index has encountered resistance near the 200-day moving average. The 50-day moving average is pointing downwards and threatens to form a “death cross” — a meaningful bear sign — next month.

Thus, the latest bounce looks like cautious profit-taking, with no signs of buying enthusiasm on the downturn.

If the 200-day resistance proves impossible for the bulls, the dollar index may turn down towards the intermediate target at 102.3 (-1.7% from the current level) in the March lows. More important now looks to be the 101 (-2.9%) area, where several of last year’s lows are centred. Taking this support would effectively break the dollar bull run in 2021–2022, sending the DXY into the 90-92 area.

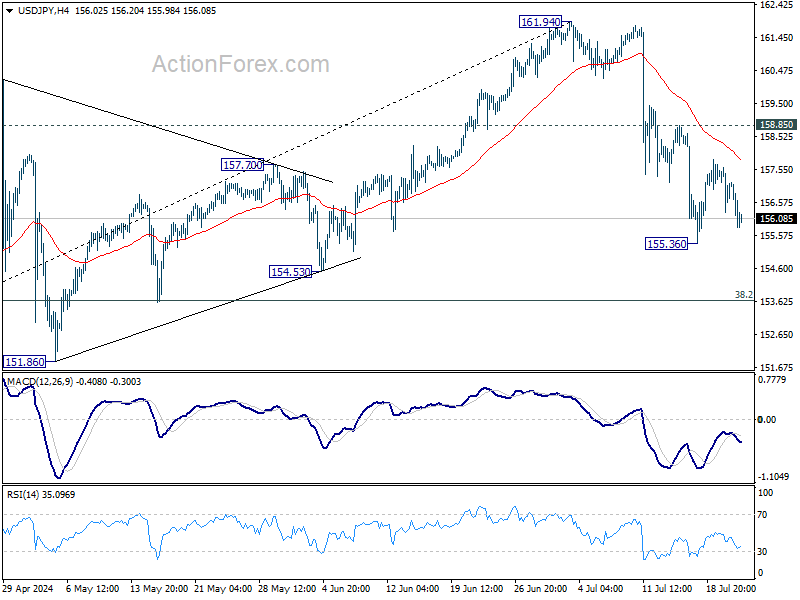

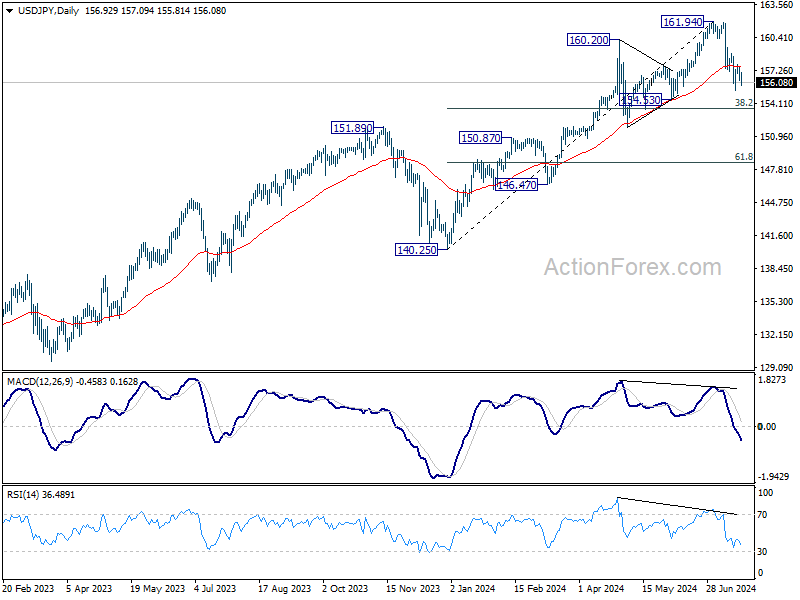

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 156.37; (P) 156.99; (R1) 157.69; More...

No change in USD/JPY's outlook as range trading continues. Intraday bias stays neutral and further decline is expected with 158.85 resistance intact. Below 155.36 will target 38.2% retracement of 140.25 to 161.94 at 153.65. On the upside, above 158.85 resistance will turn bias back to the upside for stronger rebound instead.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

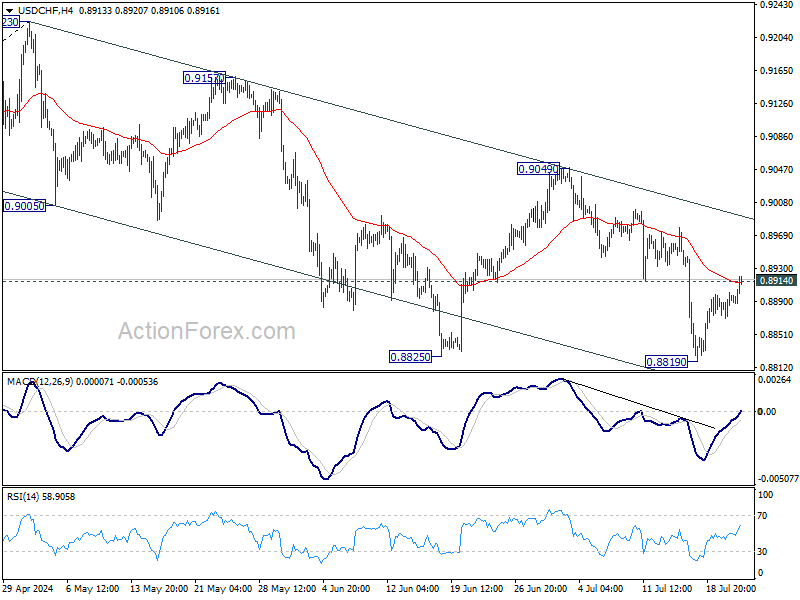

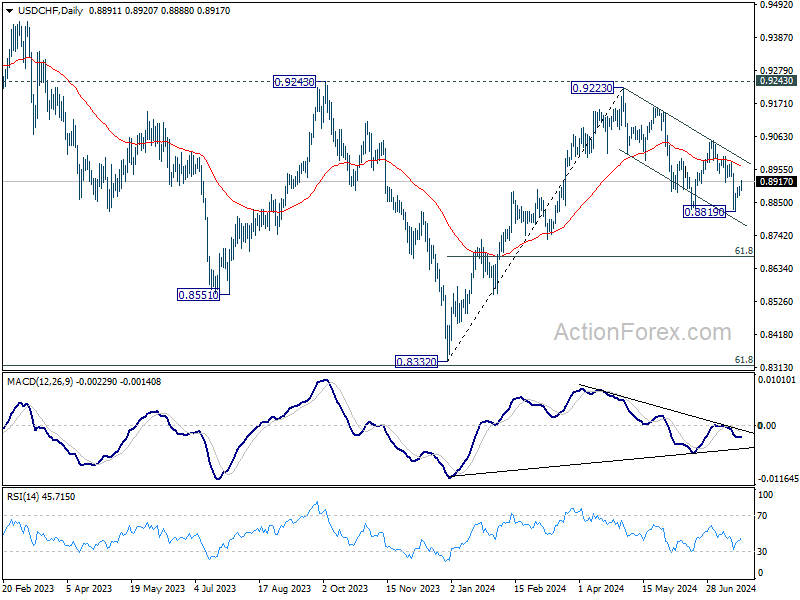

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8878; (P) 0.8890; (R1) 0.8909; More…

Intraday bias in USD/CHF is back on the upside with break of 0.8914 support turned resistance. Further rally should be seen to 55 D EMA (now at 0.8967) and possibly above. But still, break of 0.9049 resistance is needed to confirm that fall from 0.9223 has completed. Otherwise, risk will stay on the downside for another fall at a later stage.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

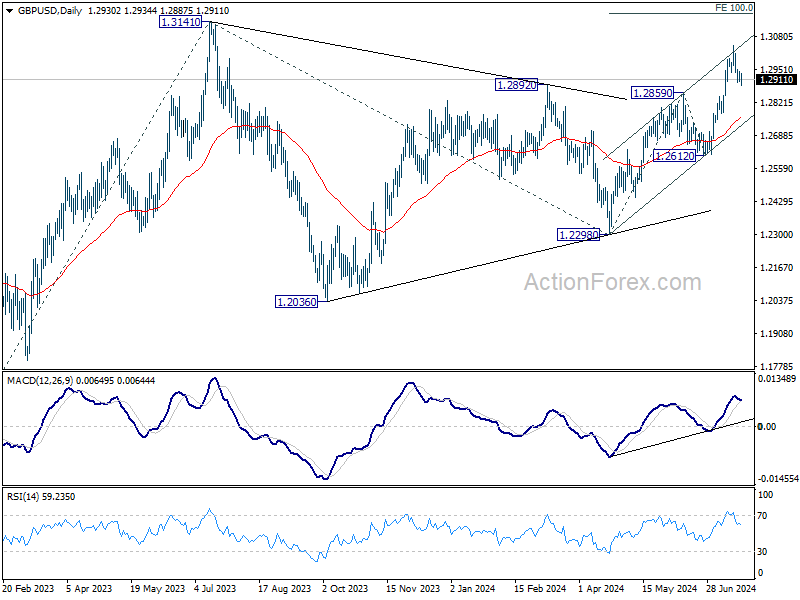

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2912; (P) 1.2927; (R1) 1.2949; More...

GBP/USD is still holding above 1.2859 resistance turned support and intraday bias remains neutral. Further rally is expected for now. Break of 1.3043 will resume the rise from 1.2298 and target 100% projection of 1.2298 to 1.2859 from 1.2612 at 1.3173, which is slightly above 1.3141 key medium term resistance. However, firm break of 1.2859 will turn bias to the downside for deeper decline.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.

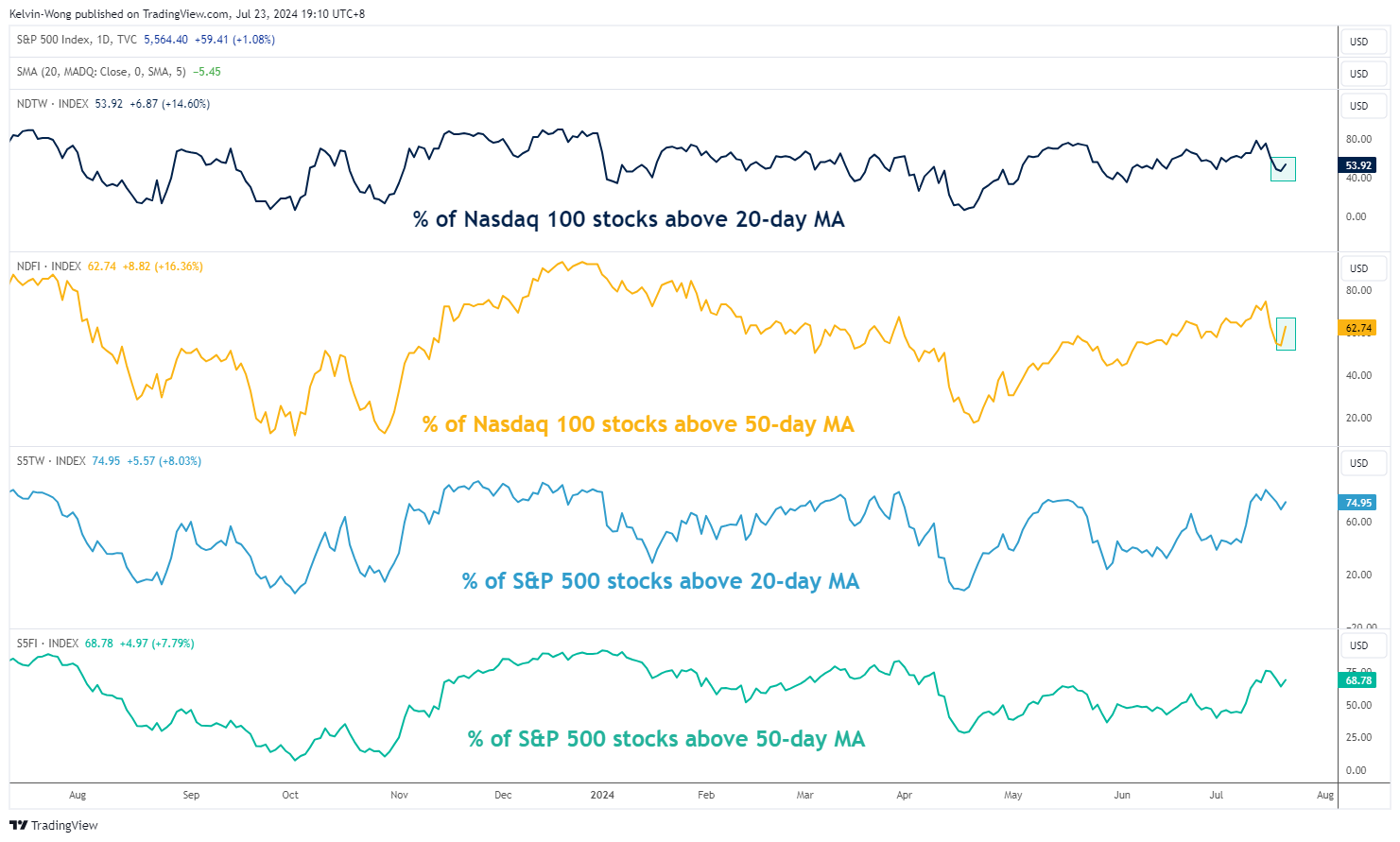

Nasdaq 100: Potential Bullish Reversal Looms Ahead of Alphabet and Tesla Earnings Results

- Market breadth indicators (% of component stocks above 20-day & 50-day moving averages) have increased to above 50%.

- Short-term bullish momentum condition sighted at the retest of its 50-day moving average.

- Watch the 19,520 key short-term support ahead of a risk event; the earnings results of Alphabet & Tesla after today’s US session close.

In the past two weeks, the Nasdaq 100 CFD (a proxy of Nasdaq 100 E-mini futures) has staged a decline of 6.2% from its all-time intraday high of 20,792 printed on 11 July to an intraday low of 19,501on last Friday, 19 July.

Also, it underperformed the value-oriented Dow Jones Industrial Average (+1.5%) and small-caps Russell 2000 (+4.7%) over the same period primarily driven by the bull steepening of the US Treasury yield curve (10-year minus 2-year).

In the lens of the technical analysis, the Nasdaq 100 CFD may have reached an inflection point for a potential bullish reversal ahead of the release of Tesla and Alphabet Q2 earnings results after the close of today, 23 July US session.

The price actions of Tesla and Alphabet are likely to have a significant impact on the Nasdaq 100 because both are in the top 10 component stocks of the Nasdaq 100; ranked 7th and 8th respectively in terms of market capitalization.

Market breadth has improved

Fig 1: Market breadth indicators of Nasdaq 100 and S&P 500 as of 22 Jul 2024 (Source: Trading View, click to enlarge chart)

After a recent slide to around 50% from 12 July to 19 July on the percentage of Nasdaq 100 components stocks trading above their respective 20-day and 50-day moving averages, these two market breadth indicators have managed to improve on Monday, 22 July where both hit above the 50% mark again (see Fig 1).

The percentage of Nasdaq 100 component stocks above their 20-day moving averages increased from 47% on Friday, 19 July to 54% on Monday, 22 July.

In addition, the percentage of Nasdaq 100 component stocks above their 50-day moving averages jump more significantly from 54% on Friday, 19 July to 63% on Monday, 22 July.

These current positive market breadth observations suggest the short and medium-term uptrend phases of the Nasdaq 100 remain intact.

Short-term bullish momentum condition sighted

Fig 2: Nasdaq 100 CFD short-term trend as of 23 Jul 2024 (Source: Trading View, click to enlarge chart)

After a bullish divergence condition sighted on the hourly RSI momentum indicator on Friday, 19 July, the price actions of the Nasdaq 100 CFD have a positive follow-through right at its 50-day moving average and its medium-term ascending trendline from 19 April 2023 low.

These short-term positive price actions suggest a potential bullish reversal scenario if the 19,520 pivotal support holds (see Fig 2).

The next near-term resistance zone to watch will be at 20,060/20,210 (also the 20-day moving average) and a clearance above it increases the odds of another impulsive upmove sequence to retest the current all-time high area at 20,710 before the medium-term pivotal resistance comes in at 20,900.

On the other hand, a break below 19,520 invalidates the bullish reversal scenario for a deeper multi-week corrective decline to expose to the near-term supports at 19,115 and 18,950 in the first step.

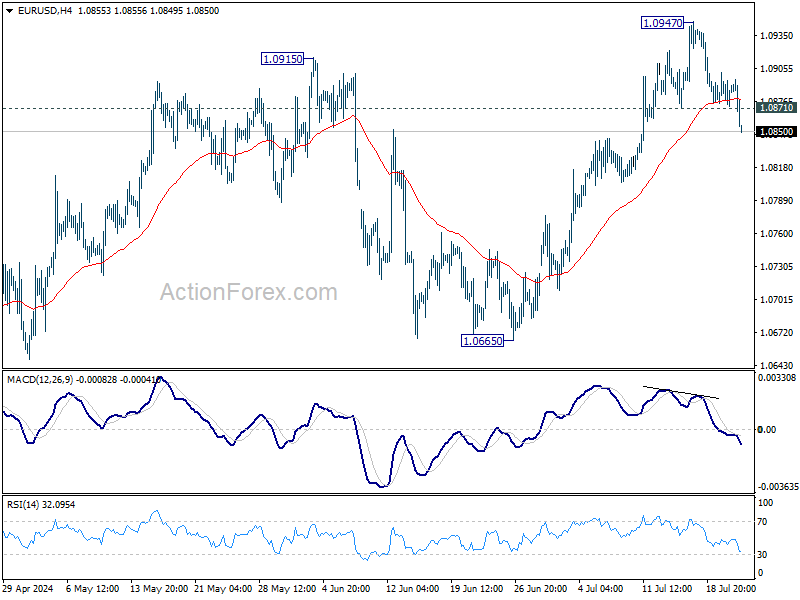

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0875; (P) 1.0889; (R1) 1.0905; More.....

EUR/USD's break of 1.0871 support suggests that a short term top was already formed at 1.0947, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for 55 D EMA (now at 1.0810). Sustained break there will argue that whole rebound from 1.0601 has completed with three waves up to 1.0947, and target 1.0601/0665 support zone. For now, risk will stay on the downside as long as 1.0947 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.