Sample Category Title

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0875; (P) 1.0889; (R1) 1.0905; More.....

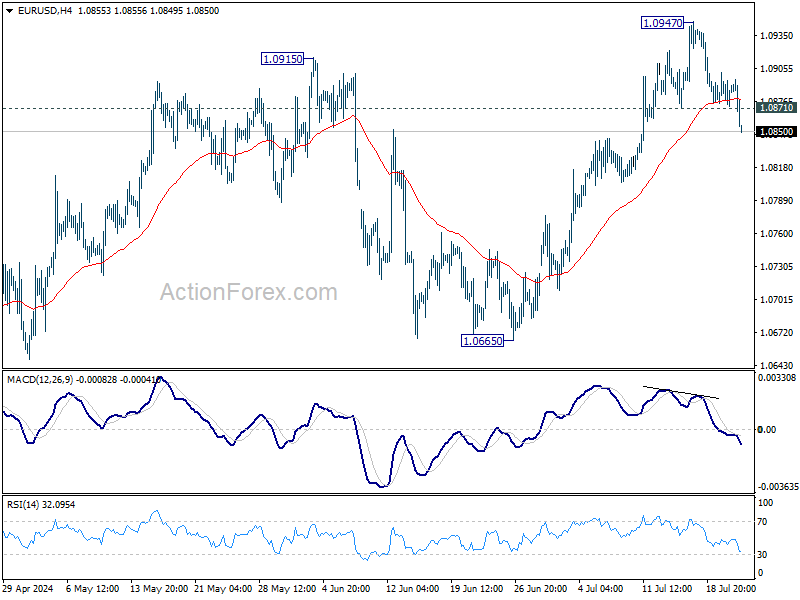

EUR/USD's break of 1.0871 support suggests that a short term top was already formed at 1.0947, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for 55 D EMA (now at 1.0810). Sustained break there will argue that whole rebound from 1.0601 has completed with three waves up to 1.0947, and target 1.0601/0665 support zone. For now, risk will stay on the downside as long as 1.0947 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.

Yen Holds Strong While Dollar Begins to Flex Its Muscles

Japanese Yen continues to stand out as the strongest currency, in another day with a lackluster economic calendar. However, it's Dollar that's capturing market interest as markets enter into US session, where it has shown notable gains against major counterparts like Euro and Swiss Franc. Break of near term levels in both EUR/USD and USD/CHF suggests that the greenback's near term rebound might extend further.

A key question now is whether the "Trump Trade" has returned, in particular particularly after Kamala Harris has solidified her position as the Democratic presidential nominee by securing necessary party and public support. The prospect of Donald Trump returning to the presidency and implementing his characteristic trade and tax policies could lead to stronger economic growth and higher inflation. These factors are expected to moderate Fed's easing cycle, thereby supporting a stronger Dollar.

In the broader currency spectrum, Dollar's momentum places it just behind Yen in terms of strength, followed by Canadian Dollar. At the other end, Australian Dollar languishes as the weakest, closely followed by New Zealand Dollar and then Euro. British Pound and Swiss Franc are positioned in the middle.

Technically, AUD/JPY's fall from 109.36 resumed this week and accelerates to as low as 103.21 so far. Current development suggests that it's now correcting whole rise from 86.04. Near term outlook will stay bearish as long as 105.76 resistance holds. Deeper fall should be seen to 38.2% retracement of 86.04 to 109.36 at 100.45. But strong support should be seen above 99.32 resistance turned support to bring rebound.

In Europe, at the time of writing, FTSE is down -0.28%. DAX is up 0.84%. CAC is down -0.17%. UK 10-year yield is down -0.0221 at 4.142. Germany 10-year yield is down -0.049 at 2.449. Earlier in Asia, Nikkei fell -0.01%. Hong Kong HSI fell -0.94%. China Shanghai SSE fell -1.65%. Singapore Strait Times rose 0.70%. Japan 10-year JGB yield rose 0.0181 to 1.063.

ECB's de Guindos: Sep economic projections key for policy reassessment

In an interview with Spanish news agency Europa Press, ECB Vice President Luis de Guindos emphasized the significance of new macroeconomic projections in September, together with another two months of data on inflation and underlying inflation. These projections and data will help ECB reassess its monetary policy stance more effectively.

De Guindos stressed the importance of having more confidence that inflation will reach ECB's target of 2% by the end of 2025, calling it the "key question." He acknowledged the high level of uncertainty, stating that ECB must be "prudent" when making decisions.

He predicted that inflation will remain "around current levels until the end of the year" and observed that all measures of underlying inflation are declining. He added, "The disinflation process will continue from the start of next year."

De Guindos also pointed out that wages are "starting to slow down," and firms expect wage increases to moderate, particularly from 2025 onward. This moderation in wage increases is expected to lead to a reduction in services inflation, helping ECB achieve its 2% inflation target by the end of next year.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0875; (P) 1.0889; (R1) 1.0905; More.....

EUR/USD's break of 1.0871 support suggests that a short term top was already formed at 1.0947, on bearish divergence condition in 4H MACD. Intraday bias is back on the downside for 55 D EMA (now at 1.0810). Sustained break there will argue that whole rebound from 1.0601 has completed with three waves up to 1.0947, and target 1.0601/0665 support zone. For now, risk will stay on the downside as long as 1.0947 resistance holds, in case of recovery.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). However, break of 1.0665 support will extend the correction with another falling leg back towards 1.0447 support.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 14:00 | USD | Existing Home Sales Jun | 4.00M | 4.11M | ||

| 14:00 | EUR | Eurozone Consumer Confidence Jul P | -13 | -14 |

EUR and GBP Retreat from Key Levels

Financial and currency markets are experiencing one shock after another. The steady decline in US inflation, a potential Fed rate cut, and the current US president’s exit from the election race have led to sharp fluctuations in almost all currency pairs. Last week:

- The GBP/USD pair traded above the psychological level of 1.3000;

- USD/JPY sellers pushed the price below 156.00;

- The EUR/USD currency pair updated its May highs of the current year at 1.0920. Currently, we are observing corrective pullbacks from recent impulses. The news coming out this week will provide more clues about the development of current trends.

GBP/USD

Technical analysis of the GBP/USD pair indicates the possibility of a continued upward movement if the range of 1.2900-1.2880 remains as support. However, at the end of last week, a "bearish engulfing" pattern was formed on the daily timeframe, which, if fully realised, could lead to a test of 1.2860-1.2800. The following news could affect the pair’s pricing:

- Today at 17:00 (GMT+3) - US existing home sales data for June;

- Tomorrow at 11:30 (GMT+3) - UK services PMI release.

EUR/USD

Technical analysis of the EUR/USD pair indicates the likelihood of resuming an upward movement if the price continues to trade above 1.0870-1.0850. At the same time, the possibility of a deeper downward correction cannot be ruled out, as a "bearish tweezer" pattern has formed on the daily timeframe. If the price goes below 1.0870, the decline may continue towards 1.0820-1.0800. The following events could reinforce current trends:

- Today at 10:00 (GMT+3) - speech by European Central Bank representative Philip Lane;

- Today at 17:00 (GMT+3) - Eurozone consumer confidence index release;

- Tomorrow at 11:00 (GMT+3) - Eurozone manufacturing PMI release for the current month.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

Analysis of XAU/USD: Gold Price Falls for 4 Consecutive Days

As shown on the XAU/USD chart, Monday, 22 July marked the fourth consecutive day of declining gold prices. The change from the historical peak reached on Wednesday is around -3.5%.

Bearish sentiment is driven by:

→ Market participants' assessment of prospects due to the change of the Democratic Party's presidential candidate in the US.

→ Caution in anticipation of economic news. On Thursday at 15:30 GMT+3, US GDP data will be released. On Friday at the same time, the Core PCE Price Index data will be published.

Market participants may also be influenced by the psychological level of $2500.

Can the Gold Price Fall Further?

Technical analysis of the XAU/USD chart provides valuable insights:

→ In June, the gold price was within the range of 2290-2385. The rise to July's peak corresponds to a target calculated by the range height: 2385 + (2385 - 2290) = 2480;

→ After reaching a record on 17 July, the price failed to hold above the May peak, which is a bearish sign;

→ The XAU/USD chart shows increasing support points for a descending channel (shown in red), which may form a corrective movement within a broader upward trend (shown in blue).

Bulls may take advantage of the gold price being near the support block of 2365-2385, which is formed by:

→ The former resistance at 2385;

→ The median lines of the blue and red channels.

However, if we see a weak rebound from this block, it may indicate that the gold price is indeed in a corrective phase.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

FTSE 100 Consolidates, S&P 500 Faces Critical Test, Earnings Ahead

- The FTSE 100 is currently consolidating, trading within a range, with the possibility of a significant breakout.

- Glencore and Anglo American experiencing declines while Compass reports strong revenue growth.

- The S&P 500 faces a critical resistance level that could shift market momentum, with Alphabet and Tesla’s earnings reports expected to influence investor sentiment.

FTSE 100

The FTSE 100 has entered a period of consolidation following the UK election, posting a modest gain of approximately 0.29% for July. Year-to-date (YTD), the FTSE 100 has delivered a steady, though not spectacular, performance with gains around 6%.

The start of this week has seen some notable movements, particularly in the mining sector. Miner and commodities trader Glencore (GLEN.L) fell as much as 2.4% this morning, leading the losses on the FTSE 100. This decline followed an HSBC analyst downgrade, which reduced Glencore’s price target from 455p to 435p and Anglo American’s (AAL.L) price target to 2300p due to the temporary closure of GEMCO’s operations.

As a result, Glencore is down about 8% YTD, while Anglo American remains up approximately 11.5% YTD.

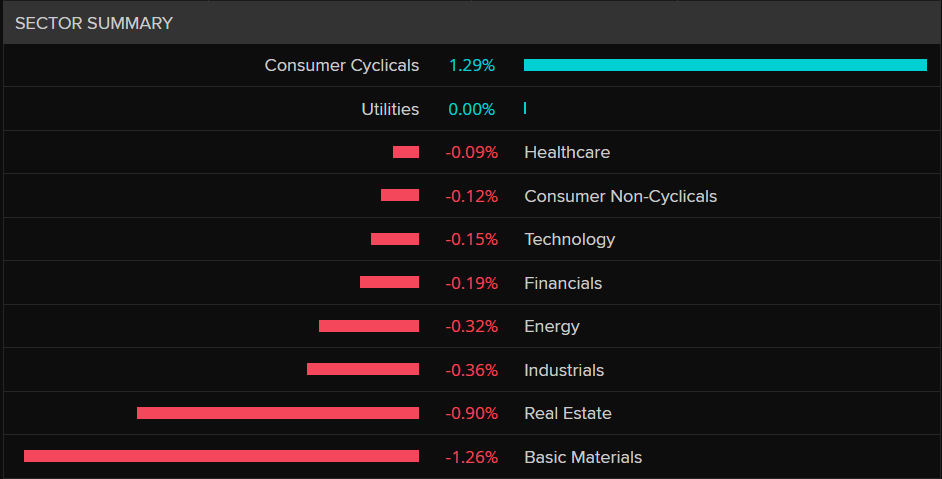

Sector Performance, FTSE 100, July 23, 2024

Source: LSEG

The standout performer today has been contract caterer Compass (CPG.L), which reported a 10% rise in revenue and highlighted strong industry trends. The only downside noted by Compass was the strength of the GBP, which has been near multi-month highs. The company’s stock is up 4.88% on the day, leading the day’s gainers.

FTSE 100 Daily Chart, July 23, 2024

Source: TradingView.com (click to enlarge)

Since the UK election, the FTSE 100 has been trading within a range, consolidating between the support level at 8117 and the resistance level at 8273. Recent price movements have been erratic, with lower highs and higher lows indicating market indecision.

The longer prices remain in a range or wedge pattern, the more intense the eventual breakout is likely to be. For intraday trading, immediate resistance is at 8240, followed by the top of the wedge pattern near the 8273 mark.

On the downside, initial support is at 8187, with further support at the lower end of the wedge pattern and the 8117 level.

S&P 500: Earnings Heats Up, Tesla (TSLA.O) and Alphabet (GOOGL.O) After Market Close Today

The S&P 500 and the Nasdaq 100 are heading into a significant week following last week’s tech selloff. Earnings reports from major tech companies begin today, with Alphabet (GOOGL.O) and Tesla (TSLA.O) both releasing their results after market close (PMC).

What can we expect from Alphabet?

Alphabet is expected to report earnings of $1.85 per share for the second quarter, which is slightly lower than the $1.89 per share from the previous quarter but still a 28% increase compared to the same quarter last year.

Total revenue is projected to be $84.3 billion, marking a 4% increase from the first quarter and a 13% rise compared to the same period last year.

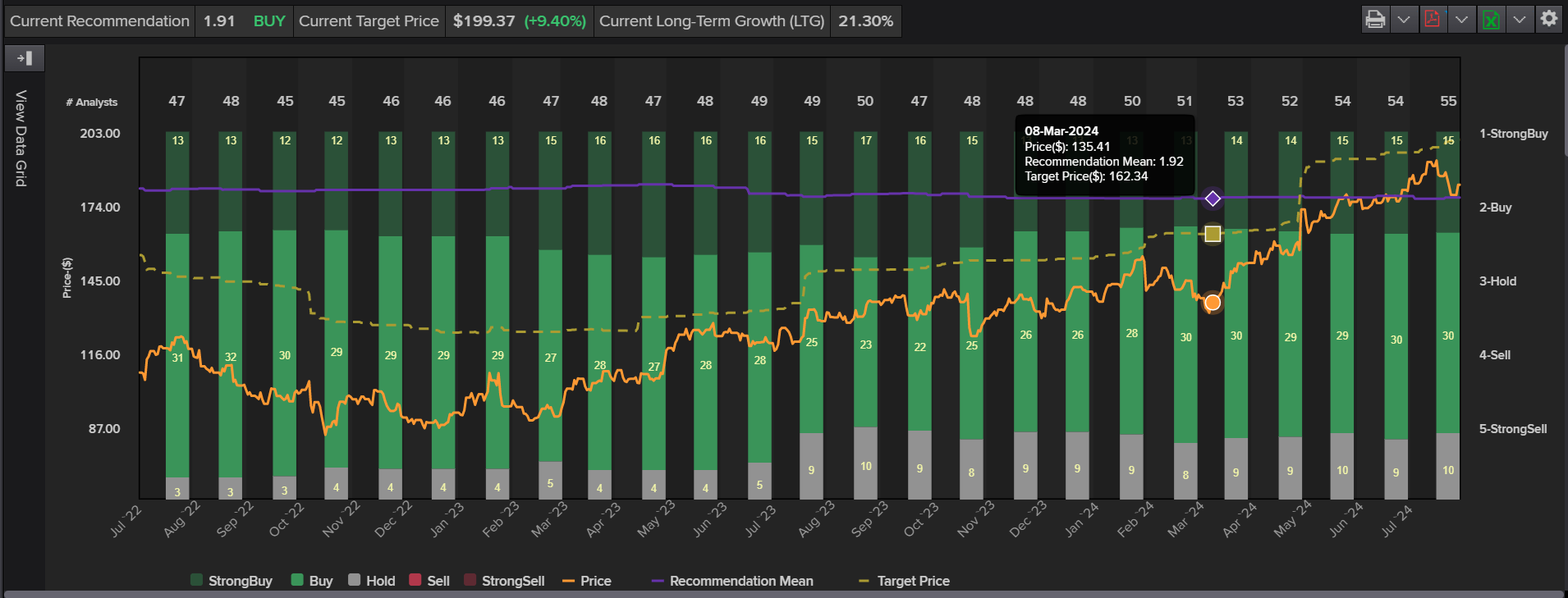

The Graph below depicts the Price Target average by various institutions around the world.

*The Chart below is based on a average estimates by analysts who have set a price target around $199.37. The current price of Alphabet shares are around the $181, which means analyst are eyeing further gains of around 10% for Alphabet moving forward.

Source: LSEG

Markets seem slightly more cautious due to the recent sector rotation, which has favored smaller stocks and benefited the Russell 2000 index.

For now, US election uncertainty is taking a backseat as it appears that current Vice President Kamala Harris will secure enough votes for the Democratic party nomination. This development seems to have alleviated concerns among market participants regarding a potential challenger to Donald Trump.

S&P 500 Daily Chart, July 23, 2024

Source: TradingView.com (click to enlarge)

The S&P 500 is approaching a crucial resistance level that could shift market momentum and encourage bullish sentiment. After rebounding from the ascending trendline and moving higher again, the resistance zone around 5575 will be critical.

If a four-hour candle closes above 5575, it could pave the way for further gains. The next key level to watch is around 5600, followed by the recent highs near 5660.

Gold Outlook: Pullback from New Record High Runs Out of Steam Ahead of Key US Data

Gold price edges higher in European trading on Monday, after Monday’s Doji candle signaled that pullback from new record high ($2483) might be running out of steam.

Pullback was contained by solid supports at $2390 zone (daily Kijun-sen / 50% retracement of $2293/$2483 upleg), with oversold conditions on daily chart and indicators predominantly in bullish setup, contributing to initial signal of an end of corrective phase.

However, fundamentals are expected to play the key role in defining metal’s near term direction, with US Q2 GDP and June PCE data, being in focus.

Investors will be looking for more information about the condition of the US economy, as well as signals about timing of start of Fed’s rate cuts from inflation numbers.

Lift above daily Tenkan-sen ($2427) is seen as minimum requirement for recovery to generate firmer bullish signal and spark further recovery.

Otherwise, the price may hold in extended consolidation with risk of fresh attempts through $2390 pivot, though larger bullish bias will remain while the price stays above daily cloud top ($2363).

Res: 2411; 2421; 2427; 2445.

Sup: 2388; 2366; 2363; 2352.

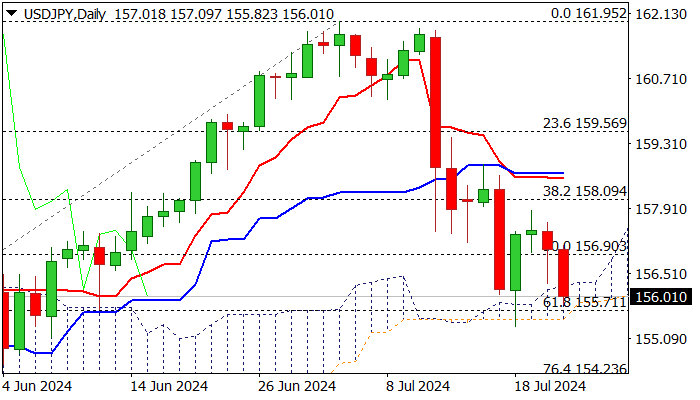

USD/JPY: Bears Retest Key Near-Term Support

USDJPY fell 0.7% in Asia on Tuesday after comments from Japanese official added pressure on the central bank for more rate hikes to further boost strengthening yen.

The latest comments further improved yen’s sentiment, though most analysts expect BoJ to keep rates unchanged in the next policy meeting.

Fresh weakness is pressuring key supports at 155.70 zone (daily cloud base / Fibo 61.8% of 151.85/161.95 upleg) where a bear trap has formed on last week’s strong downside rejection.

Reaction at daily cloud base (cloud is spanned between 155.87 and 156.30 and will thicken in coming days) will be key for near term direction.

Sustained break below cloud base and nearby July 18 low / 100DMA (155.35) would generate strong bearish signal and open way for deeper correction towards targets at 154.23/ 153.60.

Weakening daily studies (strong negative momentum / MA’s in bearish setup) support the notion, but risk of another downside rejection still exists.

Upticks should be ideally capped by converged 10/55DMA’s (157.81) to keep bears intact.

Only lift and close above daily Tenkan-sen / Kijun-sen (158.56/65) would sideline bears and signal formation of a higher base.

Res: 156.30; 156.83; 157.81; 158.56.

Sup: 155.71; 155.35; 155.00; 154.54.

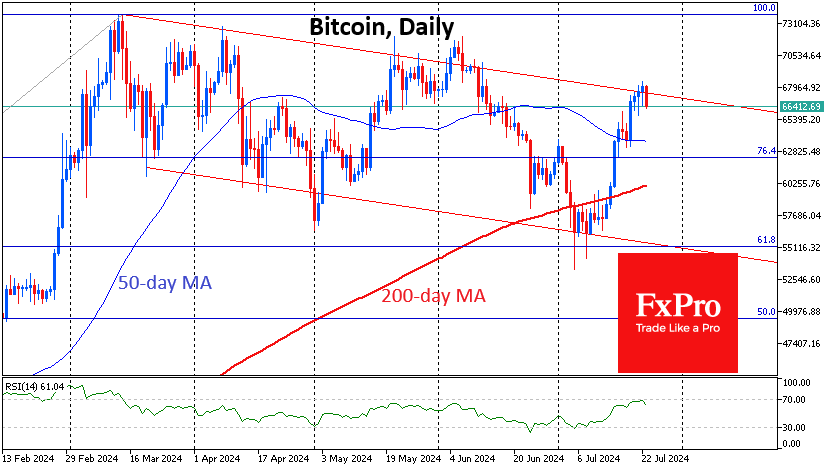

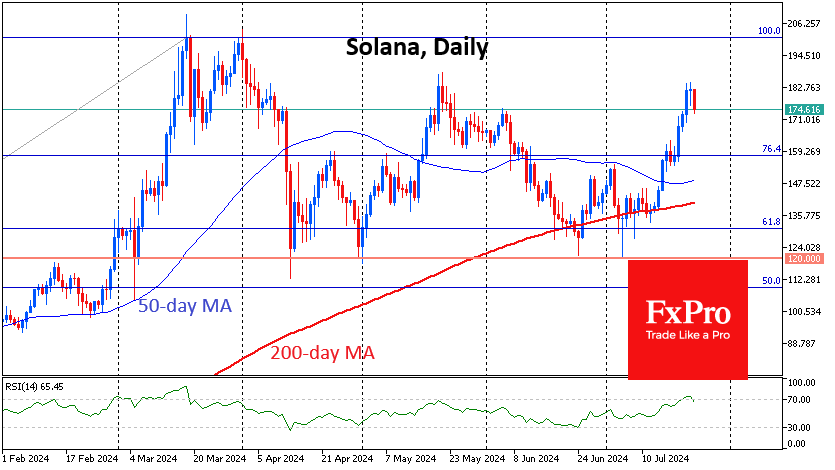

Crypto: Tactical Retreat from the Peak

Market picture

The cryptocurrency market lost 2% of its capitalisation in 24 hours to $2.41 trillion. However, this is a pullback from a high base. This tug-of-war between bulls and bears points to the importance of the current situation. Bitcoin and Ethereum are losing just over 1% each, while most altcoins are losing significantly more, ranging from 2.5% (BNB, Solana) to 3.5% (Dogecoin, Toncoin). The positive exception is XRP, which has maintained its 1.2% gain, although it has retreated 4% from its late-afternoon peak on Monday.

Bitcoin remains within a broad downward range for now, pressured by news of a new series of BTC transfers to exchanges from Mt. Gox. The previous actions did not lead to an extreme sell-off but kept the price from rising. The big question is how deep buyers’ pockets will be, given recent reports from Bloomberg citing RSM Global that the UK may sell 61,245 BTC ($4B) confiscated in 2018. The constant overhang of selling forms a series of lower price peaks.

Solana formed a peak above $180 earlier in the week, roughly reaching the levels of the May highs. In the short term, on a daily time frame, the RSI has moved out of the overbought territory, indicating the potential start of a correction. Looking at the medium-term outlook, Solana is behaving more confidently than many altcoins after strong support at 61.8% and the 200-day average in June and July.

News background

According to CoinShares, crypto fund investments rose by $1.353B last week after inflows of $1.439B a week earlier; the figure is up for the third consecutive week. Bitcoin investments increased by $1.277B, Ethereum by $45M, and Solana by $10M.

CryptoQuant noted that the market has seen a decrease in selling pressure from large investors as the price of the first cryptocurrency has consolidated near $67K. Meanwhile, realised gains for BTC holders are ‘minimal compared to March or May’.

BRN notes that Ethereum options have seen a sharp rise in implied volatility (IV). This suggests the risk of a wave of selling after the ETF launch to the $2800-3100 range, with a gradual recovery after that.

The ETF Store believes applications to launch ETFs based on a basket of assets, including Bitcoin, Ethereum, and Solana, will emerge in the next few months. According to Bloomberg, the SEC could register the Solana-ETF in mid-March 2025.

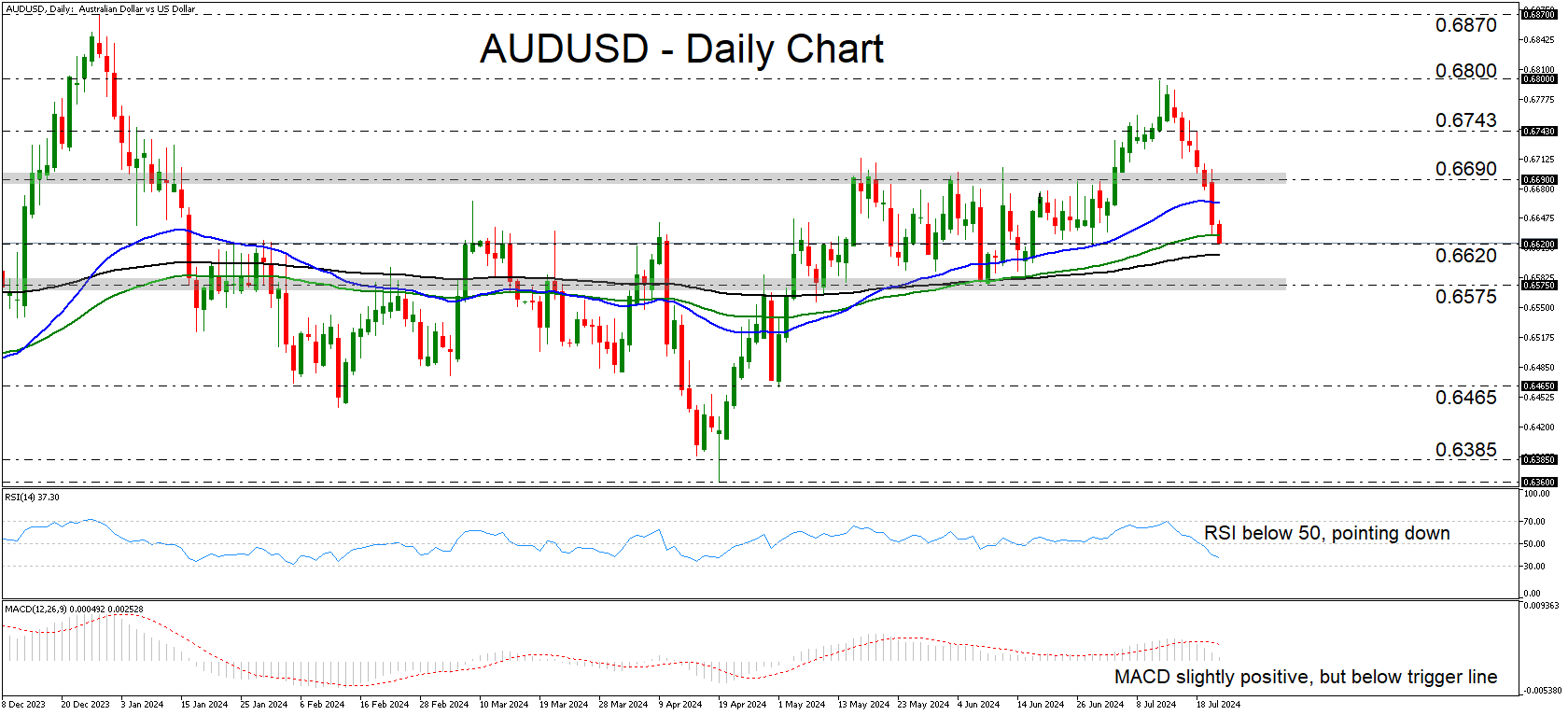

AUDUSD Tumbles Below Key 0.6690 Zone

- AUDUSD falls back within a range

- RSI and MACD support further declines

- Dip below 0.6575 could carry larger bearish implications

- Rebound above 0.6690 may invite more bulls.

AUDUSD has been trading in a free-fall mode since July 15, while yesterday, the bears cleared the key barrier of 0.6690. Now, the pair is back within the sideways range that contained most of the price action between May 3 and July 3. As long as the pair remains within that range, the outlook could be considered neutral.

The RSI is lying below 50, pointing down, while the MACD, although still slightly positive, it is running below its trigger line. Both indicators suggest that the tumble may continue for a while longer, perhaps until the lower bound of the range, at around 0.6575.

For the picture to start being considered bearish, the price may need to fall below that barrier. Such a move may encourage more sellers to jump into the action and perhaps drive the battel towards the 0.6465 zone, marked as support by the low of May 1.

On the upside, a decisive rebound back above the range’s upper end, at around 0.6690 may allow advances towards the high of July 18 at 0.6743, the break of which could carry extensions towards the peak of July 11, at 0.6800.

To recap, AUDUSD has been tumbling since July 15, returning within the sideways range between 0.6575 and 0.6690. For the outlook to be considered bearish, the price may need to fall below the range’s lower end.

ECB’s de Guindos: Sep economic projections key for policy reassessment

In an interview with Spanish news agency Europa Press, ECB Vice President Luis de Guindos emphasized the significance of new macroeconomic projections in September, together with another two months of data on inflation and underlying inflation. These projections and data will help ECB reassess its monetary policy stance more effectively.

De Guindos stressed the importance of having more confidence that inflation will reach ECB's target of 2% by the end of 2025, calling it the "key question." He acknowledged the high level of uncertainty, stating that ECB must be "prudent" when making decisions.

He predicted that inflation will remain "around current levels until the end of the year" and observed that all measures of underlying inflation are declining. He added, "The disinflation process will continue from the start of next year."

De Guindos also pointed out that wages are "starting to slow down," and firms expect wage increases to moderate, particularly from 2025 onward. This moderation in wage increases is expected to lead to a reduction in services inflation, helping ECB achieve its 2% inflation target by the end of next year.