Sample Category Title

Weaker China GDP Dampens Sentiment; ECB and Global Inflation Data Highlight the Week

Asian markets began the week with a cautious tone, as weaker-than-expected GDP growth from China dampened investor sentiment, even though the selloff in stocks has been limited. Today's set of data, coupled with recent weak PMI readings, points to broader deceleration in China's recovery momentum, as both consumer and business sentiment are struggling. Markets are now keenly awaiting the Third Plenum in Beijing this week, hoping for new measures to stimulate the economy.

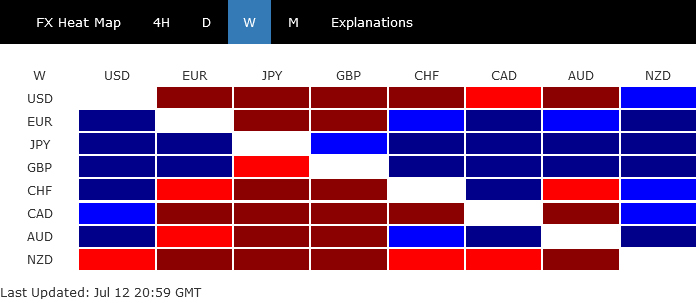

In the currency markets, Dollar is attempting to recover from last week's losses, although there hasn't been a clear follow-through in buying yet. Yen remains firm, also lacking strong follow-through buying, while Sterling ranks as the third strongest currency of the day at this point. Conversely, New Zealand Dollar continues to decline, driven lower by disappointing services data that strengthen the case for an earlier RBNZ rate cut. Canadian and Australian Dollars are also softer, while Euro and Swiss Franc are trading in the middle.

Technically, AUD/CAD's uptrend from 0.8562 is still in progress. Near term outlook will remain bullish as long as 0.9172 support holds. Next target is 100% projection of 0.8562 to 0.9063 from 0.8779 at 0.9280. Decisive break there could prompt further upside acceleration to 161.8% projection at 0.9590. The next move would hinge on this week's CPI from Canada and employment data from Australia.

In Asia, Japan is on holiday. Hong Kong HSI is down -1.27%. China Shanghai SSE is up 0.01. Singapore Strait Times is up 0.02%.

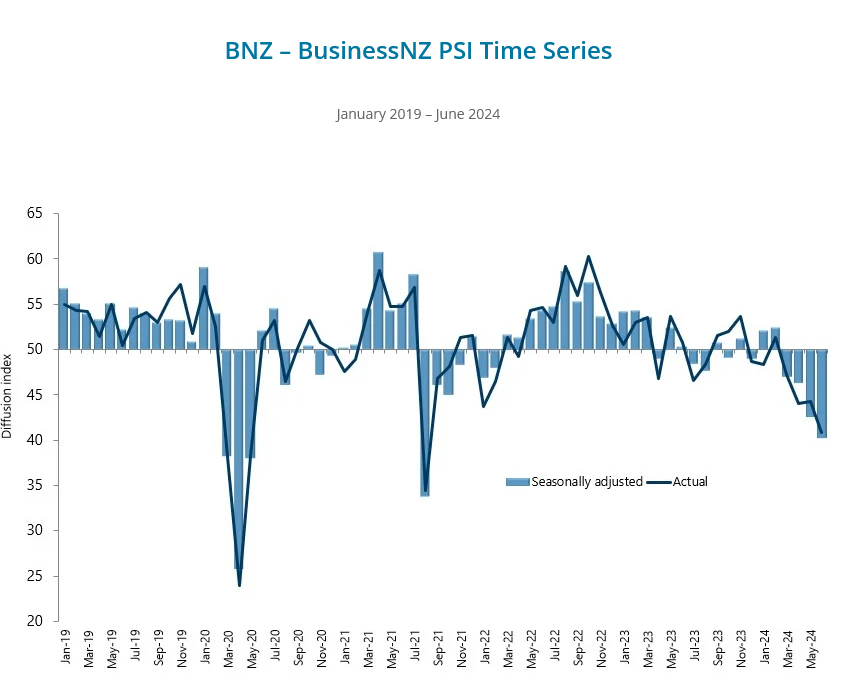

NZ BNZ services falls to 40.2, weakness accelerating

New Zealand BusinessNZ Performance of Services Index fell from 42.6 to 40.2 in June, marking the lowest level for the sector outside a COVID lockdown month since the survey began in 2007.

BusinessNZ chief executive Kirk Hope noted that after a poor May result, June's figures "simply got worse". Activity/Sales dropped to 35.6 and New Orders/Business fell to 38.3, both hitting record lows for non-lockdown months. Employment decreased to 45.6, the lowest since February 2022, while Supplier Deliveries declined to 41.6, the lowest since March 2022.

Negative comments rose to 67.0% in June, up from 65.4% in May and 66.3% in April, with respondents citing recessionary pressures.

BNZ Senior Economist Doug Steel observed, "The Performance of Services Index has been well below average for more than a year. Moreover, the weakness appears to be accelerating."

China's Q2 GDP growth slows to 4.7% amid weak domestic demand

China's GDP grew 4.7% yoy in Q2, down from 5.3% in Q1 and missing expectations of 5.1%. For the first half of the year, GDP growth stood at 5% year-on-year.

The National Bureau of Statistics noted, "The current external environment is complicated, while domestic demand remains insufficient. We still need to consolidate the foundation for economic recovery."

June's industrial production increased by 5.3% yoy, exceeding expectations of 5.0% yoy. However, retail sales grew only 2.0% yoy, well below the forecasted 3.3% yoy.

Fixed asset investment in the first six months rose by 3.9% ytd yoy, meeting expectations. Property investment saw a -10.1% yoy decline, consistent with May's fall. Additionally, home sales by floor area dropped by -19.0% yoy.

BoE's Dhingra advocates for rate normalization now

In a podcast today, BoE MPC member Swati Dhingra emphasized that "now is the time" to start normalizing interest rates and to "stop squeezing living standards" as the central bank has been doing to curb inflation.

Dhingra pointed out that demand in the UK is too weak for inflation to surge again, noting that inflation returned to 2% in May. She stated, "I don't see some kind of consumption boom and if we're going to start moderating from the very high level of interest rate that we are at now... it is going to take some time for that to happen, for us to moderate it as well as for that to then feed into the real economy."

Known as a dove within the MPC, Dhingra has consistently voted since February to cut the Bank Rate from its 16-year high of 5.25%.

ECB to hold and more global inflation data awaited

This week, financial markets are set to focus on ECB's monetary policy decision and a wave of crucial global inflation reports.

ECB is widely expected to keep its deposit rate at 3.75% and its main refinancing rate at 4.25%. President Christine Lagarde is anticipated to maintain the central bank's data-dependent, meeting-by-meeting approach. While she is likely to assure that further policy easing is underway, the central bank wouldn't commit to any forward guidance.

A Reuters poll conducted between July 4-11 indicated that 69 out of 85 economists predict ECB will cut the deposit rate twice more this year, in September and December, bringing it down to 3.25% by the end of the year. Additionally, nearly two-thirds of respondents believe the end-2024 deposit rate is more likely to be higher than their current expectations, suggesting that there is risk that ECB might opt for fewer cuts.

Global inflation data will also dominate the headlines this week, with CPI reports due from Canada, New Zealand, the UK, and Japan.

In Canada, BoC the chance of another rate cut by BoC on July 14 increased following weaker-than-expected June job data, which showed unemployment rising by 0.2% to 6.4%. Any downside surprises in the June CPI data could solidify this dovish case.

RBNZ left rates unchanged last week but surprisingly indicated that policy restriction "will be tempered" as inflation declines. Sharper-than-expected slowdown in Q2 CPI could bring forward the anticipated timing of the first rate cut from February next year to this November.

In the UK, hopes for an August BoE rate cut were dashed by hawkish comments from Chief Economist Huw Pill. Nonetheless, the decision will still hinge on the inflation outlook. Known hawk Catherine Mann cautioned that May's CPI hitting 2% was just a "touch and go". But this view will need backup from the upcoming June CPI release.

Meanwhile, in Japan, BoJ is expected to outline plans to taper its bond purchases at its late July meeting, though opinions vary on the extent of the reduction. Governor Kazuo Ueda has indicated that a rate hike is possible, but the recent strong rebound in Yen, allegedly due to intervention, adds complexity to the decision. But after all, the set of core and core-core CPI data would need to go up in June, rather than down, for BoJ to act again on interest rate.

Other key data to watch this week include retail sales figures from Canada, the US, and the UK, employment data from the UK and Australia, and German ZEW economic sentiment index.

Here are some highlights for the week:

- Monday: New Zealand BusinessNZ services index; China GDP, industrial production, retail sales, fixed asset investment; Swiss PPI; Eurozone industrial production; Canada manufacturing sales, wholesale sales; US Empire State manufacturing.

- Tuesday: Japan tertiary industry index; Eurozone trade balance; Germany ZEW; Canada housing starts, CPI; US retail sales, import prices, business inventories, NAHB housing index.

- Wednesday: New Zealand CPI; UK CPI, PPI; Eurozone CPI final; US building permits, housing starts, industrial production, Fed's Beige Book report.

- Thursday: Japan trade balance; Australia employment; Swiss trade balance; UK employment; ECB rate decision; US jobless claims.

- Friday: UK Gfk consumer confidence; Japan CPI; Germany PPI; UK retail sales, public sector net borrowing; Eurozone current account; Canada retail sales, IPPI and RMPI.

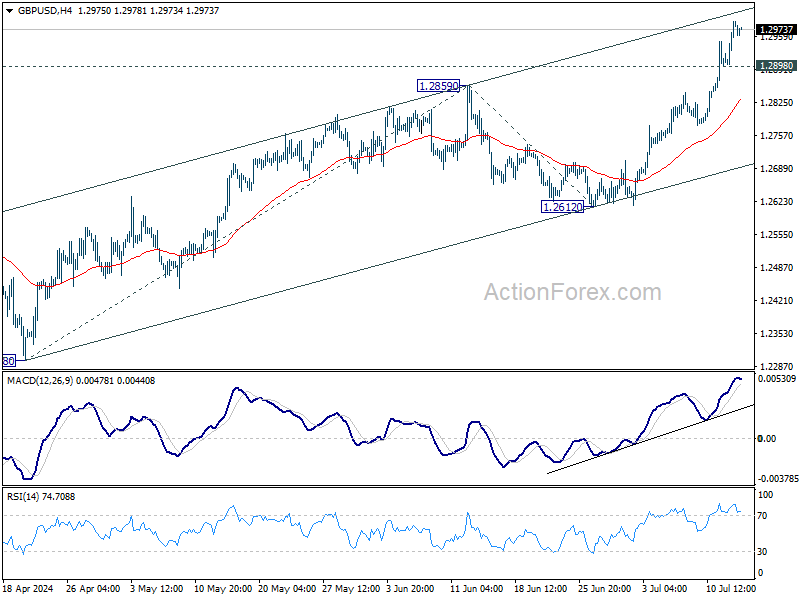

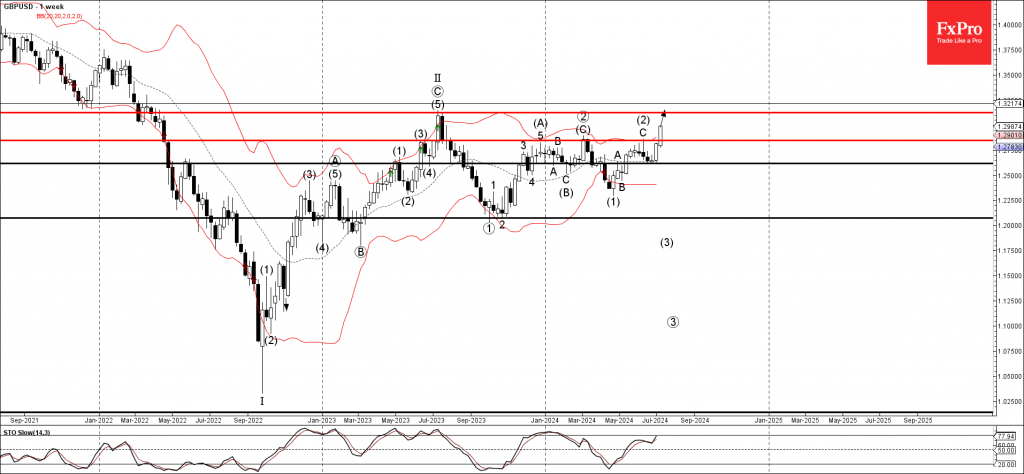

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2930; (P) 1.2960; (R1) 1.3019; More...

Intraday bias in GBP/USD remains on the upside despite current retreat. Rise fro 1.2298 is in progress for 100% projection of 1.2298 to 1.2859 from 1.2612 at 1.3173, which is slightly above 1.3141 key medium term resistance. On the downside, below 1.2898 minor support will turn bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Jun | 40.2 | 43 | 42.6 | |

| 23:01 | GBP | Rightmove House Price Index M/M Jul | -0.40% | 0.00% | ||

| 02:00 | CNY | GDP Y/Y Q2 | 4.70% | 5.10% | 5.30% | |

| 02:00 | CNY | Industrial Production Y/Y Jun | 5.30% | 5.00% | 5.60% | |

| 02:00 | CNY | Retail Sales Y/Y Jun | 2.00% | 3.30% | 3.70% | |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jun | 3.90% | 3.90% | 4.00% | |

| 06:00 | EUR | Germany Retail Sales M/M May | 0.00% | -1.20% | ||

| 06:30 | CHF | PPI M/M Jun | 0.10% | -0.30% | ||

| 06:30 | CHF | PPI Y/Y Jun | -1.80% | |||

| 09:00 | EUR | Eurozone Industrial Production M/M May | -1.00% | -0.10% | ||

| 12:30 | USD | Empire State Manufacturing Index Jul | -8 | -6 | ||

| 12:30 | CAD | Manufacturing Sales M/M May | 0.20% | 1.10% | ||

| 12:30 | CAD | Wholesale Sales M/M May | 2.00% | 2.40% | ||

| 14:30 | CAD | BoC Business Outlook Survey |

China’s Q2 GDP growth slows to 4.7% amid weak domestic demand

China's GDP grew 4.7% yoy in Q2, down from 5.3% in Q1 and missing expectations of 5.1%. For the first half of the year, GDP growth stood at 5% year-on-year.

The National Bureau of Statistics noted, "The current external environment is complicated, while domestic demand remains insufficient. We still need to consolidate the foundation for economic recovery."

June's industrial production increased by 5.3% yoy, exceeding expectations of 5.0% yoy. However, retail sales grew only 2.0% yoy, well below the forecasted 3.3% yoy.

Fixed asset investment in the first six months rose by 3.9% ytd yoy, meeting expectations. Property investment saw a -10.1% yoy decline, consistent with May's fall. Additionally, home sales by floor area dropped by -19.0% yoy.

NZ BNZ services falls to 40.2, weakness accelerating

New Zealand BusinessNZ Performance of Services Index fell from 42.6 to 40.2 in June, marking the lowest level for the sector outside a COVID lockdown month since the survey began in 2007.

BusinessNZ chief executive Kirk Hope noted that after a poor May result, June's figures "simply got worse". Activity/Sales dropped to 35.6 and New Orders/Business fell to 38.3, both hitting record lows for non-lockdown months. Employment decreased to 45.6, the lowest since February 2022, while Supplier Deliveries declined to 41.6, the lowest since March 2022.

Negative comments rose to 67.0% in June, up from 65.4% in May and 66.3% in April, with respondents citing recessionary pressures.

BNZ Senior Economist Doug Steel observed, "The Performance of Services Index has been well below average for more than a year. Moreover, the weakness appears to be accelerating."

BoE’s Dhingra advocates for rate normalization now

In a podcast today, BoE MPC member Swati Dhingra emphasized that "now is the time" to start normalizing interest rates and to "stop squeezing living standards" as the central bank has been doing to curb inflation.

Dhingra pointed out that demand in the UK is too weak for inflation to surge again, noting that inflation returned to 2% in May. She stated, "I don't see some kind of consumption boom and if we're going to start moderating from the very high level of interest rate that we are at now... it is going to take some time for that to happen, for us to moderate it as well as for that to then feed into the real economy."

Known as a dove within the MPC, Dhingra has consistently voted since February to cut the Bank Rate from its 16-year high of 5.25%.

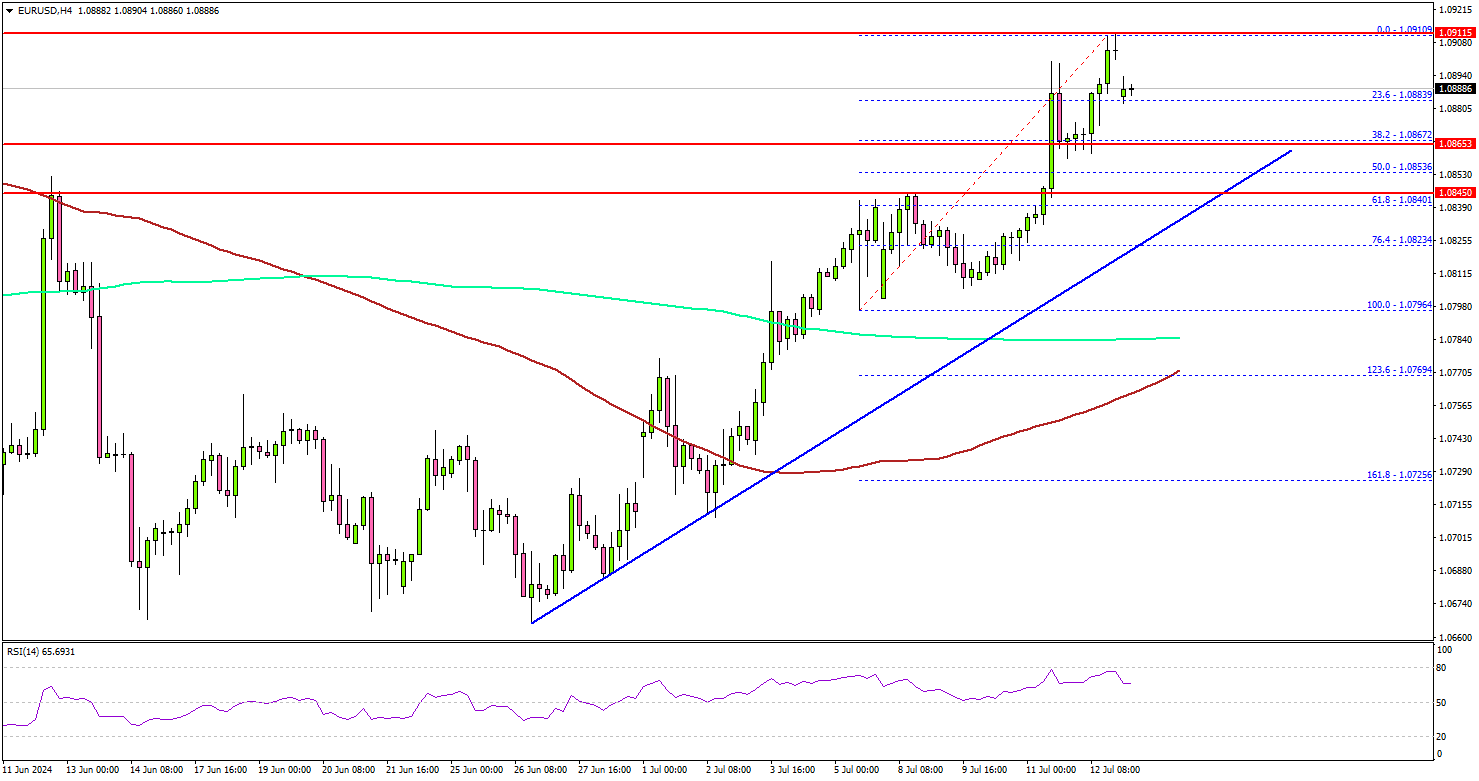

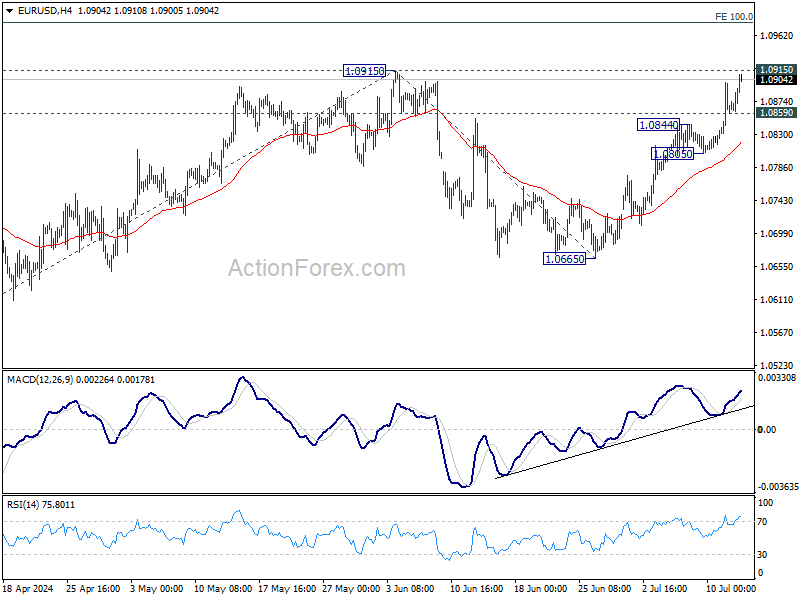

EUR/USD Consolidates Gains, Are Dips Supported?

Key Highlights

- EUR/USD rallied above the 1.0820 resistance zone.

- A key bullish trend line is forming with support at 1.0850 on the 4-hour chart.

- GBP/USD gained bullish momentum and almost tested the 1.3000 resistance.

- Gold prices are now consolidating near the $2,400 zone.

EUR/USD Technical Analysis

The Euro started a steady increase above the 1.0800 level against the US Dollar. EUR/USD cleared the 1.0820 and 1.0850 resistance levels to enter a positive zone.

Looking at the 4-hour chart, the pair settled above the 1.0850 level, the 100 simple moving average (red, 4-hour), and the 200 simple moving average (green, 4-hour). The pair even spiked above the 1.0900 level and tested the 1.0910-1.0920 resistance zone.

It is now consolidating gains near the 1.0880 zone. If there is a fresh increase, the pair could face resistance near the 1.0910 level. The next resistance sits at 1.0920.

The main hurdle sits at 1.0950. A clear move above the 1.0950 resistance might send it toward the 1.1000 level. Any more gains might open the doors for a test of the 1.1050 zone in the coming days.

Immediate support is near the 1.0880 level. The next major support is near the 1.0850 level. There is also a key bullish trend line forming with support at 1.0850 on the same chart. A downside break and close below the 1.0850 support zone could open the doors for more losses.

Looking at Gold, the price gained bullish momentum above the $2,400 level and the bulls seem to be in control above the $2,380 level.

Economic Releases

- NY Empire State Manufacturing Index for July 2024 – Forecast -6.0, versus -6.0 previous.

GBPUSD Wave Analysis

- GBPUSD under bullish pressure

- Likely to rise to resistance level 1.3120

GBPUSD currency pair is under bullish pressure after the earlier breakout of the resistance level 1.2850, which has been reversing the pair from 2023.

The breakout of the resistance level 1.2850 results from the simultaneously strongly bullish sterling sentiment and the equally weak USD sentiment.

GBPUSD can be expected to rise further to the next round resistance level 1.3120 (former multi-month high from the middle of 2023).

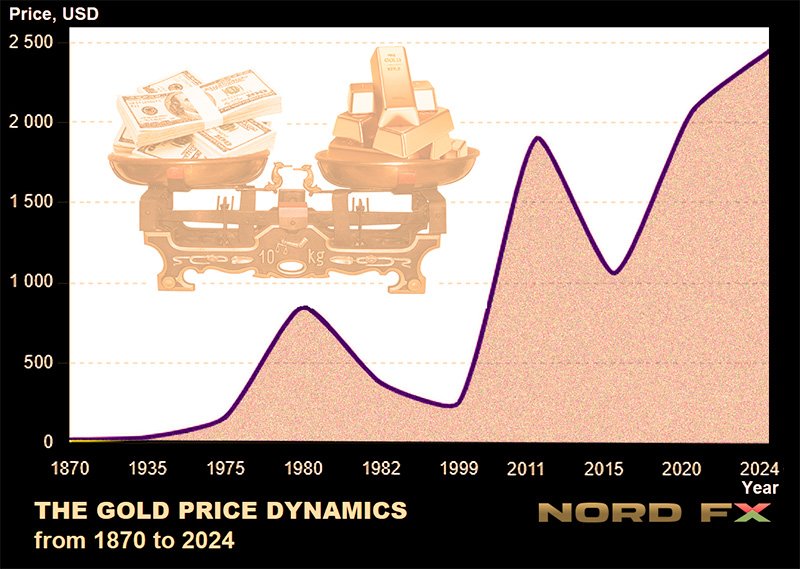

Gold as an Investment: Detailed Analysis and Price Forecasts for 2025-2050

Since ancient times, gold has remained a crucial element of global economies. Its unique properties have made it not only valuable as jewellery but also a reliable means of preserving wealth. Today, this metal constitutes a significant part of both investor portfolios and central bank reserves. This review analyses the dynamics and reasons for changes in the price of gold and presents forecasts from leading banks and experts regarding the XAU/USD pair in the medium- and long-term perspectives.

Gold Price: From Ancient Times to the 20th Century

Ancient Times. Gold mining and usage began in the 4th millennium BC. One of the first civilizations to actively use this metal was ancient Egypt, where it was mined from around 2000 BC. The importance of gold in ancient Egypt is hard to overestimate – it was considered "the flesh of the gods" and used in all aspects of life, from religious ceremonies to burial rites, in making vessels and statuettes, jewellery, and home decor, as well as a means of payment. Gold's resistance to corrosion made it a symbol of immortality and strength.

Exact data on the value of gold in ancient civilizations is hard to find, but it is known to have been one of the most valuable commodities, used not only for trade but also for wealth storage. For example, in Babylon in 1600 BC, one talent of gold (about 30.3 kg) was worth approximately 10 talents of silver (about 303 kg).

In the late 8th century BC, in Asia Minor, gold was first used as coinage. The first pure gold coins with stamped images are attributed to the Lydian King Croesus. They were of irregular shape and often minted only on one side.

Antiquity. In antiquity, gold continued to play a key role in the economy and culture. The Greeks mined gold in various places, including the region of Troy, where, according to myth, the deposit was a gift from the god Zeus. For the ancient Greeks, gold symbolized purity and nobility and was used to create unique artworks and jewellery.

In classical Athens (5th century BC), one gold drachma was worth about 12 silver drachmas. During the time of Alexander the Great (4th century BC) and the subsequent Hellenistic kingdoms, the gold-to-silver ratio varied but generally stayed within the range of 1:10 to 1:12. (Interestingly, this ratio has now grown to about 1:80). Alexander the Great issued gold staters weighing about 8.6 grams, highly valued coins often used for large international transactions.

Middle Ages. In the Middle Ages, gold remained a vital element of the economy. In the Byzantine Empire, the solidus gold coin, weighing 4.5 grams, was used for international trade. In medieval Europe, gold also played a significant role, especially after the discovery of large gold deposits in Africa. In 1252, the gold florin was introduced in Florence and used throughout Europe. In England, the gold sovereign appeared in 1489.

What could one buy with such a coin? In England in the 11th-12th centuries, a sovereign could purchase a small piece of land about one acre or a part of a farm. In the 13th century, a gold coin could buy several heads of cattle, such as two cows or several sheep.

Gold was also used to acquire weapons or armour. For example, a good quality sword might cost about one coin. One gold coin could also pay for a skilled craftsman's work for several months. For instance, such money could order the construction or repair of a house. Additionally, it could buy a large amount of food, such as a year's supply of bread for a family.

Modern Times. During the Age of Exploration, gold came to the forefront again. After the discovery of America, Spanish conquistadors brought vast quantities of gold to Europe. In the 17th-18th centuries, gold became the basis for the formation of monetary systems in Europe. By 1800, the price of one troy ounce of gold (31.1 grams) in Britain was about £4.25. Therefore, one troy ounce of this metal could buy a small plot of land in some rural areas or pay rent for housing for 8 months. It could also order the tailoring of four men's suits or pay for elementary school education for several years.

19th Century. The 19th century was marked by the Gold Rush, especially in California and Australia. This led to a significant increase in gold production and, consequently, a relative decrease in its price. In 1870, the price of one troy ounce of gold was about $20. Starting in 1879, the US monetary system was based on the so-called "gold standard," which tied the amount of paper money to the country's gold reserves, and $20 could always be exchanged for a troy ounce of this precious metal. This price level remained until the early 20th century.

20th Century: $20 – $850 – $250

1934. It had been 55 years since the adoption of the "gold standard" when, during the Great Depression, US President Franklin D. Roosevelt enacted the "Gold Reserve Act." According to this document, private ownership of gold was declared illegal, and all precious metals had to be sold to the US Treasury. A year later, after all the gold had been transferred from private ownership to the state, Roosevelt raised its price by 70% to $35 per troy ounce, allowing him to print the corresponding amount of paper money.

For the next four decades, gold prices remained stable at around $35 until 1971, when another US President, Richard Nixon, decided to abandon the "gold standard" altogether, delinking the dollar from gold. This decision can be considered a turning point in the history of the modern world economy. Gold ceased to be money and began to be traded on the open market at a floating exchange rate. This completely freed the US government's hands, allowing it to print infinite amounts of fiat currency, and the price of precious metals to grow exponentially.

By the end of 1973, the price of precious metals had already reached $97 per ounce and continued to rise amid economic instability and inflation, reaching $161 in 1975 and $307 in 1979. Just a year later, amid high inflation and political instability (including the Soviet invasion of Afghanistan and the Iranian revolution), XAU/USD reached a record level of $850 .

1982. After reaching this peak, there was a rollback to $376 in 1982, linked to rising interest rates in the US and stabilizing economic conditions. Political and economic changes in the world, such as the end of the Cold War and the development of global financial markets, stabilized the gold market, and until the mid-1990s, XAU/USD traded in the range of $350-$400. By 1999, the price had fallen to $252 per ounce, due to rising stock markets, low inflation, and decreased demand for gold as a safe-haven asset.

First Quarter of the 21st Century: From $280 to $2450

2000s. At the beginning of the 2000s, the price of gold was about $280 per troy ounce. However, it began to rise following the dot-com bubble burst and sharply increased during the global financial crisis, reaching $869 in 2008. This growth was driven by economic instability, falling stock markets, declining confidence in the dollar, and increased demand for gold from investors seeking safe-haven assets. By the end of 2010, the gold price continued to rise, reaching $1421. In September 2011, it reached a record level of $1900 per ounce. This rise was due to the European debt crisis and concerns about global economic instability. However, the dollar began to strengthen, inflation expectations fell, and stock markets rose, leading XAU/USD to turn south, falling to $1060 by the end of 2015.

After this, another reversal occurred, and the pair headed north again. In 2020, the price reached a new record level of $2067. The primary driver here was the COVID-19 pandemic, which prompted massive monetary stimulus measures (QE) by governments and central banks, primarily the US Federal Reserve. The historical maximum to date was reached in May 2024 at $2450, aided by geopolitical instability in the Middle East, Russia's military invasion of Ukraine, and expectations of interest rate cuts by the Federal Reserve, ECB, and other leading central banks.

Why Gold?

Mid-2024. Before moving on to gold price forecasts, let's answer the question: what exactly makes this yellow metal valuable?

Firstly, note its physical and chemical properties. Gold is chemically inert, resistant to corrosion, and does not rust or tarnish over time, making it an ideal asset for value storage. It has an attractive appearance and lustre that does not fade over time, making it popular for making jewellery and luxury items. It is also relatively rare in the Earth's crust. Limited availability makes it valuable since demand always exceeds supply.

Next, follow the economic factors, which are perhaps more important in the modern world. Gold is traditionally used as a means of preserving capital. We have already mentioned that in times of economic instability and geopolitical tension, investors often turn to gold to protect their savings from depreciation. Naturally, in such a situation, its price is influenced by the level of inflation and related monetary policies of central banks, including interest rate changes and quantitative easing (QE) or tightening (QT) programmes.

Investors use gold to diversify their portfolios and reduce risks. Gold has high liquidity, allowing it to be quickly and easily converted into cash or goods and services worldwide. This makes it attractive not only for investors but also for central banks, which hold significant gold reserves as part of their international reserves. This helps them maintain national currency stability and serves as a guarantee in case of financial crises. For example, the Federal Reserve holds nearly 70% of its foreign reserves in gold.

Forecasts for the Second Half of 2024 and 2025

Gold price forecasts for the end of 2024 and 2025 vary, but most analysts from leading global banks and agencies agree that its price will rise. UBS strategists predict an increase to $2500 per ounce. J.P. Morgan also targets $2500 in the medium term, provided the Federal Reserve cuts rates and economic instability persists.

Goldman Sachs has revised its forecasts and expects the price to reach $2700 per ounce in 2025. Bank of America economists initially forecasted $2400 for 2024 but also revised their forecast upwards to $3000 by 2025. The primary condition for growth, according to the bank, is the start of active rate cuts by the US Federal Reserve, which will attract investors to gold as a safe-haven asset.

Citi specialists agree with this figure. "The most likely scenario in which an ounce of gold rises to $3000," they write in an analytical note, "besides the Federal Reserve rate cut, is the rapid acceleration of the current but slow trend – the de-dollarization of central banks in developing economies, which will undermine confidence in the US dollar."

Rosenberg Research analysts also mention a figure of $3000. The consulting agency Yardeni Research does not rule out that due to a possible new wave of inflation, XAU/USD could rise to $3500 by the end of next year. The super-bullish forecast was given by TheDailyGold Premium magazine editor Jordan Roy-Byrne. Based on the "Cup and Handle" model, he stated that a breakout is coming, and with it a new cyclical bull market. "The current measured target for gold," writes Roy-Byrne, "is $3000, and its logarithmic target is somewhere between $3745 and $4080."

Forecasts to 2050

Most major banks and financial data providers typically offer only short- and medium-term forecasts. The main reason is that markets can be very volatile, and small changes in supply or demand factors and external events can lead to unexpected price fluctuations, casting doubt on prediction accuracy.

Despite this, there are different scenarios and long-term price forecasts for gold for 2030-50. Economist Charlie Morris, in his work "Rational Case for Gold by 2030," forecasts a price of $7000 per ounce. Another specialist, David Harper, predicted that the price of gold could reach $6800 by 2040. This scenario, according to Harper, describes reasonable growth with a return rate of about 7.2% per year.

Regarding a 25-year horizon, Josep Peñuelas, a research professor at the Centre for Ecological Research in Barcelona, warned that by 2050, the world might run out of key metals, including gold. However, other futurist theories are more optimistic. According to renowned investor and writer Robert Kiyosaki, gold has existed since time immemorial and, being "God's money," is likely to become the primary form of currency in the future. In his book "Fake," Kiyosaki argues that ultimately, gold, along with bitcoins, could destroy paper currencies and become the foundation of the global financial system.

Dollar Plummets as Markets Brace for Double or Even Triple Fed Rate Cuts This Year

Dollar weakened broadly last weeks market expectations on Fed's policy path shifted dramatically. The June US CPI report continued the narrative painted by the previous week's Non-Farm Payroll data, both suggesting further cooling in economic activity and easing price pressures. These developments have firmly positioned a September Federal Reserve rate cut as a near certainty in the minds of traders, with additional expectations for another reduction in December. Some aggressive market participants are even betting on an additional reduction in November. This shift in sentiment also boosted US stocks to new record highs and hammered treasury yields.

However, despite its significant movement, Dollar was only the second worst performer, with the New Zealand Dollar taking the bottom spot. Kiwi plunged following the surprisingly dovish statement from RBNZ, which accompanied their decision to hold interest rates unchanged. The hint of future monetary easing has markets betting on a rate cut by RBNZ as early as November. Meanwhile, Canadian Dollar was the third worst performer.

Conversely, Japanese Yen emerged as the week's star performer, buoyed by what appeared to be a strategically timed market intervention by Japan. The next move for Yen will depend on whether market participants join in to further boost its value, a development that might hinge on BoJ's meeting later this month.

Meanwhile, British Pound secured its position as the second strongest performer, rallying after expectations for an August rate cut by BoE were dashed by comments from a top BoE official and stronger-than-expected UK economic data. Euro ranked third in performance, while Aussie and Swiss Franc ended mixed in the middle.

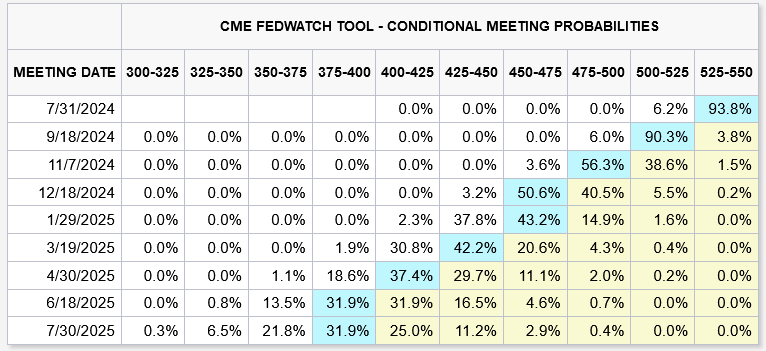

Odds of Three Fed Rate Cuts in 2024 Now a Toss-Up

US stock markets were on a high, with even laggard DOW reaching a new intraday record, following earlier surges by S&P 500 and NASDAQ. The upbeat sentiment among investors was largely driven by optimism that Fed is on track for rate cut, and this expectation was further solidified by US June CPI data.

The CPI report showed further slowdown in both headline and core inflation rates, suggesting that the "last mile" of disinflationary process in the US might be less daunting than previously feared. This positive development should bolster Fed policymakers' confidence to consider lowering interest rates sooner.

In light of these developments, fed fund futures now indicate 94% chance of a 25bps rate cut in September, bringing federal funds rate down to 5.00-5.25%. By year-end, there's also 94% chance of two total rate cuts, lowering the rate to 4.75-5.00%.

More importantly, there's around 60% chance of seeing two rate cuts by November meeting, reducing the rate to 4.75-5.00%. Furthermore, there's 54% probability of three cuts by year-end, bringing the rate down to 4.50-4.75%.

This suggests that some market participants are aggressively betting on back-to-back rate cuts in September, November, and December. This speculation has dialed back the clock to March, with close probabilities between two and three rate cuts this year.

Technically, S&P 500 surged to new record high at 5655.56. But it appears to be struggling slightly facing 61.8% projection of 4103.78 to 5263.95 from 4953.56 at 5670.55.

For now, further rally is expected as long 5523.64 resistance turned support holds. Firm break of 5670.66 will pave the way to 100% projection at 6113.73. This is where the real test lies with 100% projection of 2191.86 to 4818.62 from 3491.58 nearby.

Meanwhile, firm break of 5523.64 will bring consolidations first, before the up trend resumes.

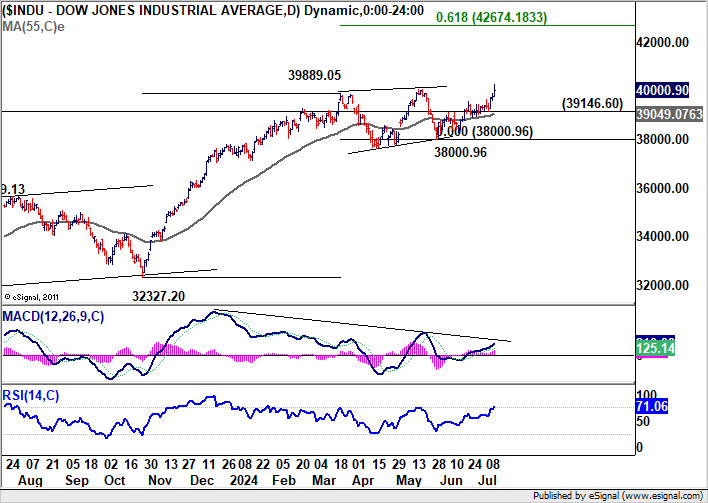

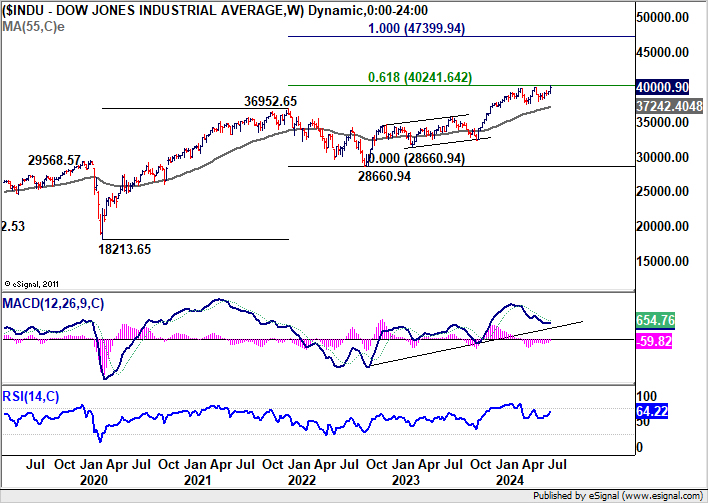

DOW's last breakout suggests that long term up trend is resuming. Further rise is expected as long as 39146.60 support holds. Sustained trading above 40000 handle will pave the way to 61.8% projection of 3237.20 to 39889.05 from 38000.96 at 42674.18.

Also, it should be emphasized that 40k handle is critical as it's also close to 61.8% projection of 18213.65 to 36952.65 from 28660.94 at 40241.64. Decisive break there could prompt medium term upside acceleration towards 100% projection at 47399.94.

Nevertheless, break of 39146.60 support will delay the bullish case.

Yields Fall and Dollar Weakens Amid Changing Fed Expectations

US 10-year yield fell notably last week along with the development in Fed expectations. Technically, outlook is unchanged that fall from 4.737 is the third leg of the pattern from 4.997 and it's still in progress. Further decline is expected as long as 55 D EMA (now at 4.352) holds.

Sustained break of 55 W EMA 55 W EMA (now at 4.189) could prompt downside acceleration in TNX, and extend the fall from 4.737 to 3.785, or even further to 100% projection of 4.997 to 3.785 from 4.737 in the medium term.

However, there is a notable counterargument to this bearish outlook, linked to steepening yield curve. This steepening is reflective of market concerns that re-election of Donald Trump could lead to policies that might increase the risk premium on longer-maturity Treasuries. In this case, TNX's decline could be floored to a certain extent.

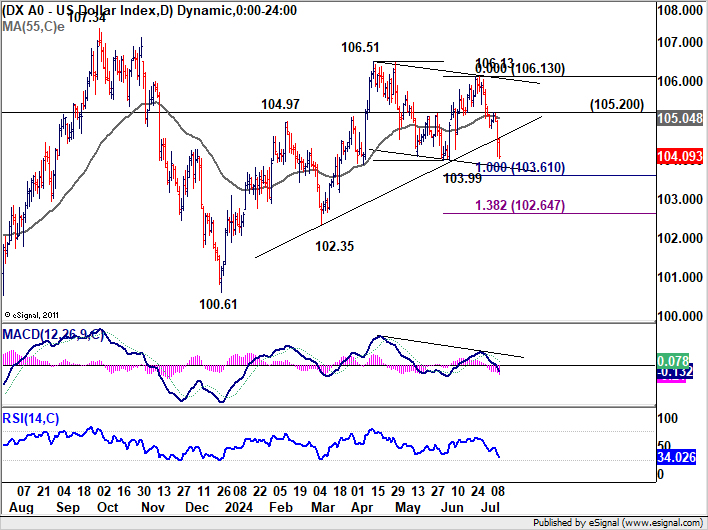

The bearish case in Dollar index is starting to build up with a close below 55 W EMA (now at 103.40). Deeper decline is expected as long as 105.20 support holds, to 100% projection of 106.51 to 103.99 from 106.13 at 103.61. Break there will target 138.2% projection at 102.64 next.

More importantly, sustained trading below 55 W EMA will strengthen the case that whole rise from 100.61 has already finished at 106.51. That would open up deeper fall through 102.35 to retest 100.61 support next.

Yen Jumps on Suspected Intervention; Market Awaits BoJ's Next Steps

Yen also dominated financial headlines, with its largest daily rally since late 2022, allegedly driven by unconfirmed market intervention from Japan. The timing of this intervention was notably strategic, occurring just after US CPI release, which had already exerted significant downward pressure on the greenback. Reports from BoJ accounts suggest that approximately JPY 3.5T may have been deployed in these efforts to buoy Yen.

Despite this surge, the yen's rebound was limited as market participants seemed hesitant to join to drive the currency higher. The focus now shifts to BoJ's meeting at the end of July. The financial community are divided over BoJ's next move: Some economists argue that market interventions increase the likelihood of a rate hike, viewing it as a necessary follow-up to governmental actions. Others believe that the easing pressure on Yen makes a rate hike less probable.

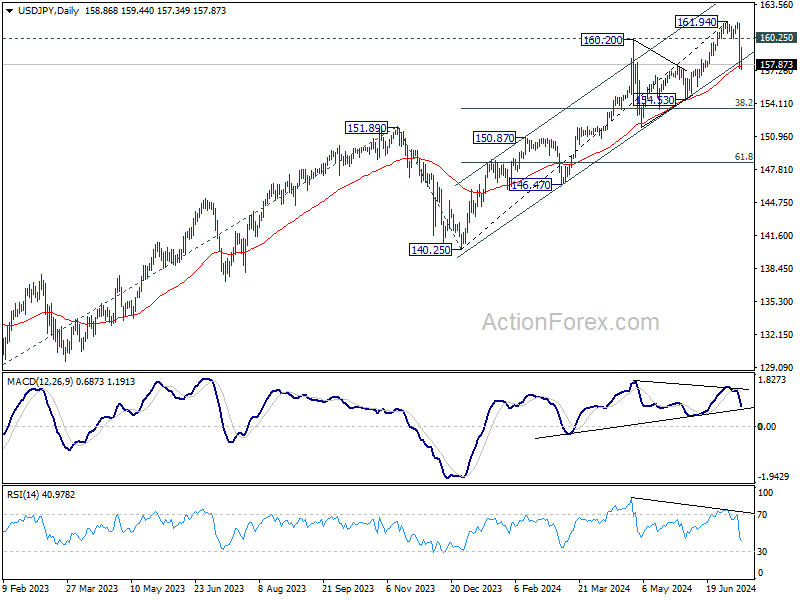

Technically, further decline is expected in USD/JPY as long as 160.25 support turned resistance holds. Considering bearish divergence condition in D MACD, fall from 161.94 might be correcting the whole five-wave rally from 140.25 already.

Sustained trading below 55 D EMA (now at 157.34) will strengthen this bearish case and send USD/JPY further lower to 38.2% retracement of 140.25 to 161.94 at 163.65. But strong support should emerge there to bring rebound, as set the range for medium term consolidations.

Nikkei, on the other hand, suffered with Yen's strong rebound. The Japanese index had it biggest daily drop of the year just after hitting new record above 42k. As long as 40746.89 support holds, there is still prospect of extending the record rally to 61.8% projection of 35038.28 to 41087.75 from 37950.19 at 44469.76. However, firm break of 40746.89 will bring deeper pull back to 55 D EMA (now at 39407.32). The depth of Nikkei's correct in this bearish case, would depend on that of USD/JPY too.

Sterling Stands Strong on Diminished Hopes for Aug BoE Rate Cut

Sterling stood out as one of the best performers again last week. There was a prevailing sentiment among investors that BoE might cut rates in August, especially after the general election. However, these hopes were tempered following remarks from BoE's Chief Economist, Huw Pill. Pill hinted a preference for maintaining interest rate at 5.25%, citing persistent wage growth and inflation within the services sector as key concerns. His cautious stance was further reinforced by stronger than expected UK GDP data for May. Consequently, the likelihood of an August BoE rate cut, previously priced into the market at around 60%, has tumbled to approximately 50%.

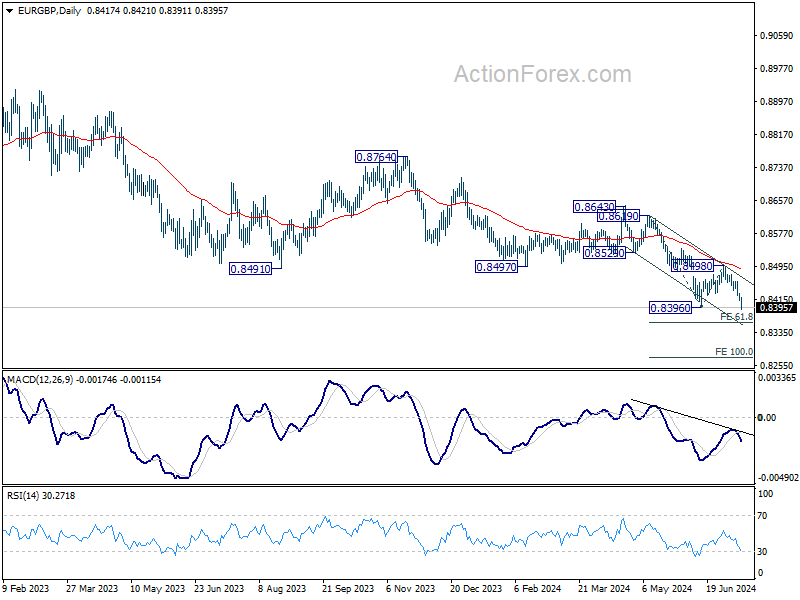

EUR/GBP's breach of 0.8396 support suggests that medium term down trend is ready to resume. Further decline would be seen to 61.8% projection of 0.8619 to 0.8396 from 0.8498 at 0.8360. Firm break there could prompt downside acceleration to 100% projection at 0.8275.

GBP/CHF's strong rebound from 1.1216 continued last week towards 1.1675 resistance. Firm break there would confirm resumption of whole rise from 1.0634. Next near term target is 61.8% projection of 1.0634 to 1.1675 from 1.1216 at 1.1859.

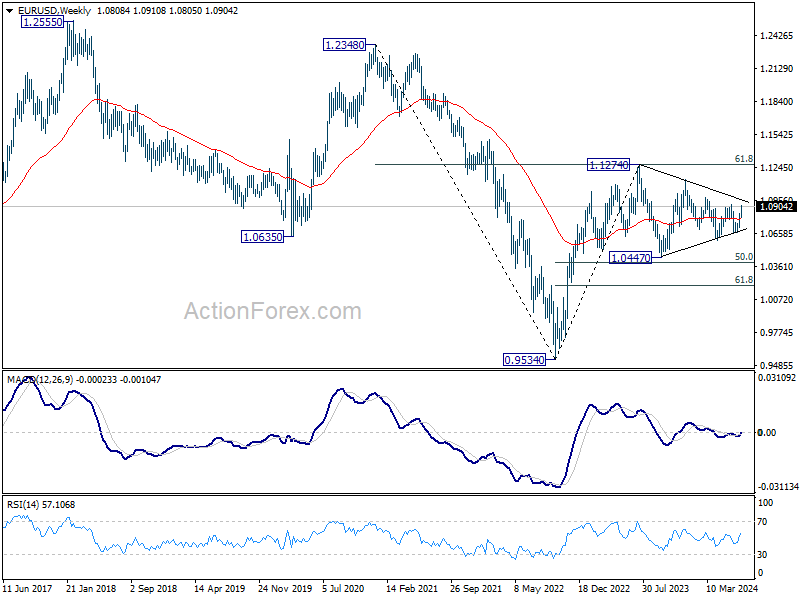

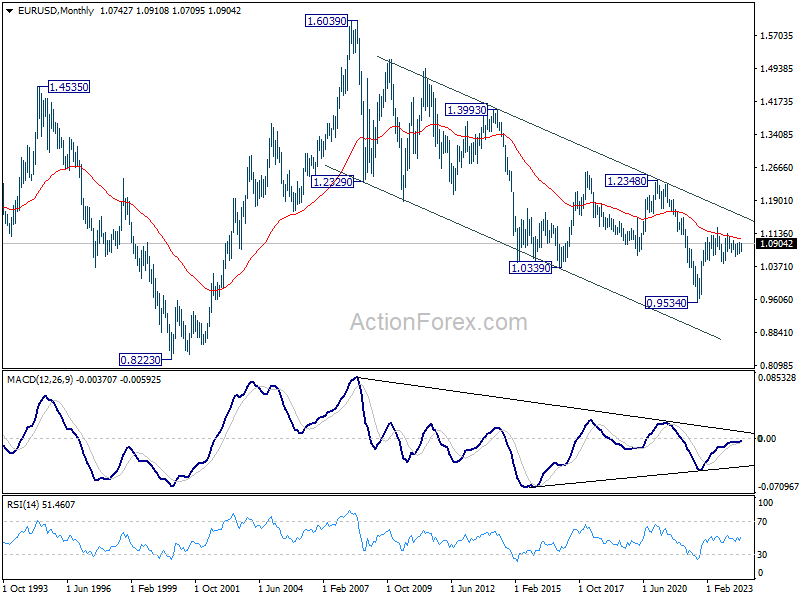

EUR/USD Weekly Outlook

EUR/USD's rally continued last week and hit as high as 1.0910. Initial bias stays on the upside this week. Firm break of 1.0915 will resume howl rise from 1.0601 to 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. On the downside, below 1.0859 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

In the long term picture, a long term bottom is in place at 0.9534 (2022 low). Sustained break of 55 M EMA (now at 1.1046) will raise the chance of long term reversal. But even in this case, firm break of 1.2348 structural resistance is needed to confirm. Rejection by 55 M EMA will maintain bearishness for extend the down trend from 1.6039 (2008 high) through 0.9534 at a later stage.

EUR/USD Weekly Outlook

EUR/USD's rally continued last week and hit as high as 1.0910. Initial bias stays on the upside this week. Firm break of 1.0915 will resume howl rise from 1.0601 to 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. On the downside, below 1.0859 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

In the long term picture, a long term bottom is in place at 0.9534 (2022 low). Sustained break of 55 M EMA (now at 1.1046) will raise the chance of long term reversal. But even in this case, firm break of 1.2348 structural resistance is needed to confirm. Rejection by 55 M EMA will maintain bearishness for extend the down trend from 1.6039 (2008 high) through 0.9534 at a later stage.