Sample Category Title

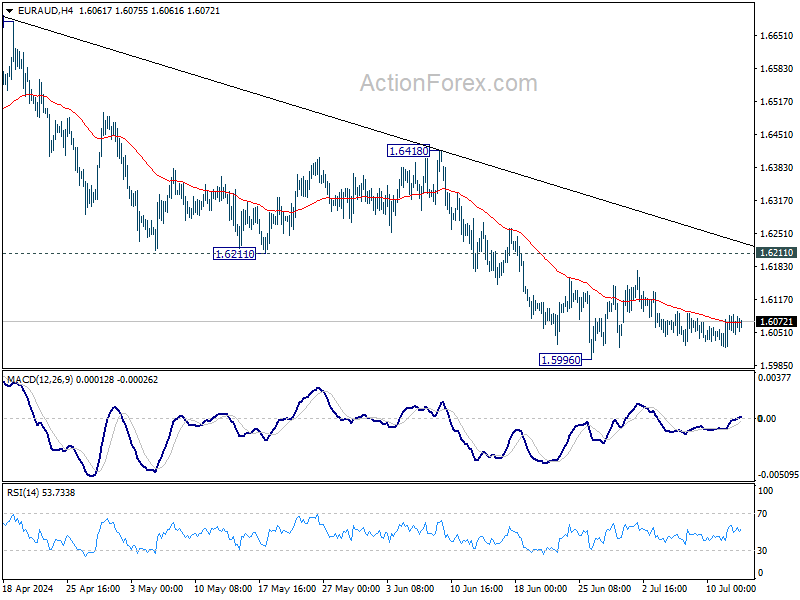

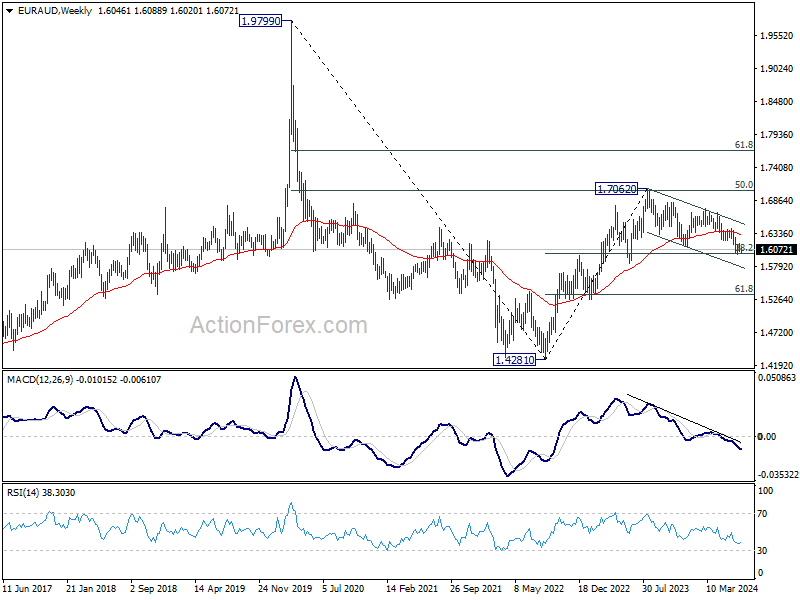

EUR/AUD Weekly Outlook

EUR/AUD's consolidation from 1.5996 continued last week and outlook is unchanged. Initial bias stays neutral this week first. While another recovery cannot be ruled out, further decline is expected as long as 1.6211 resistance holds. Break of 1.5996 will resume larger fall to 1.5846 support next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.6148 resistance will argue that the correction has completed.

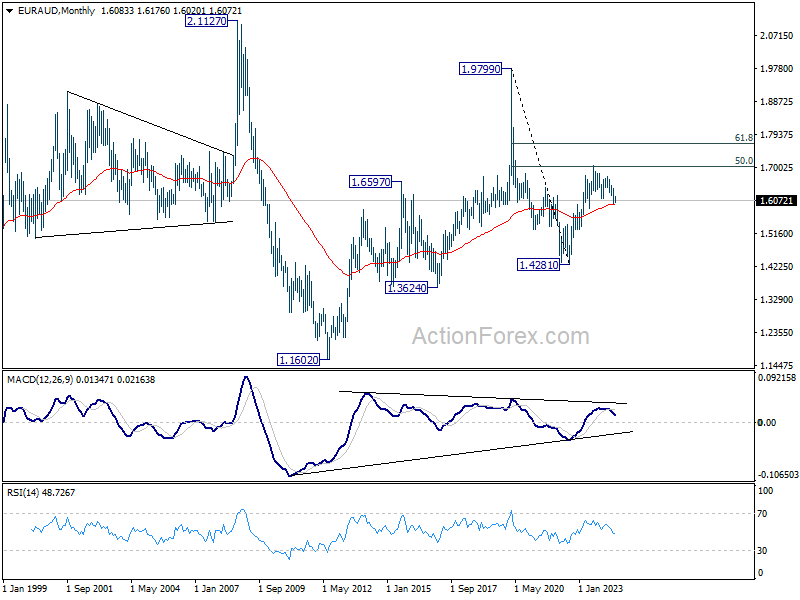

In the longer term picture, price actions from 1.9799 (2020 high) are seen as a long term decline at the same scale as the rise from 1.1602 (2012 low). Rebound from 1.4281 is seen as the second leg. As long as 55 M EMA (now at 1.5970) holds, this second leg could still extend higher. However, sustained trading below 55 M EMA will open up the bearish case for extending the decline through 1.4281 low.

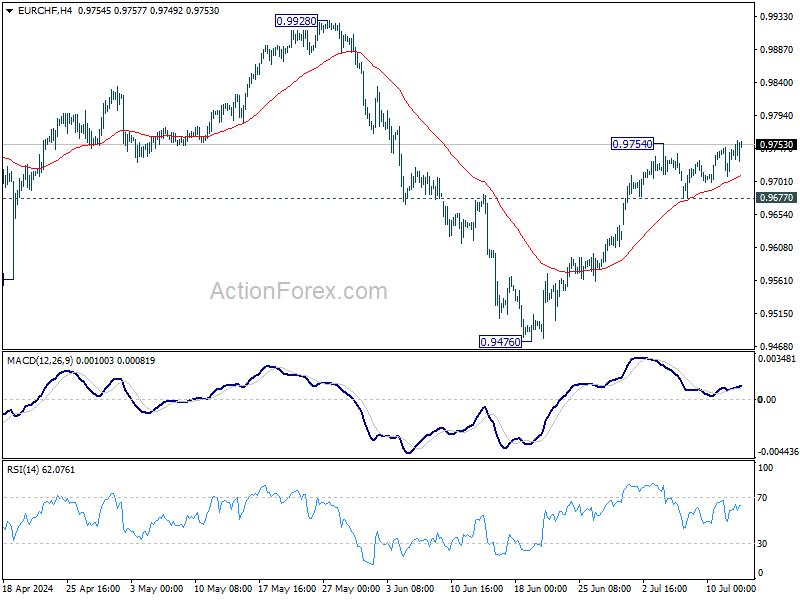

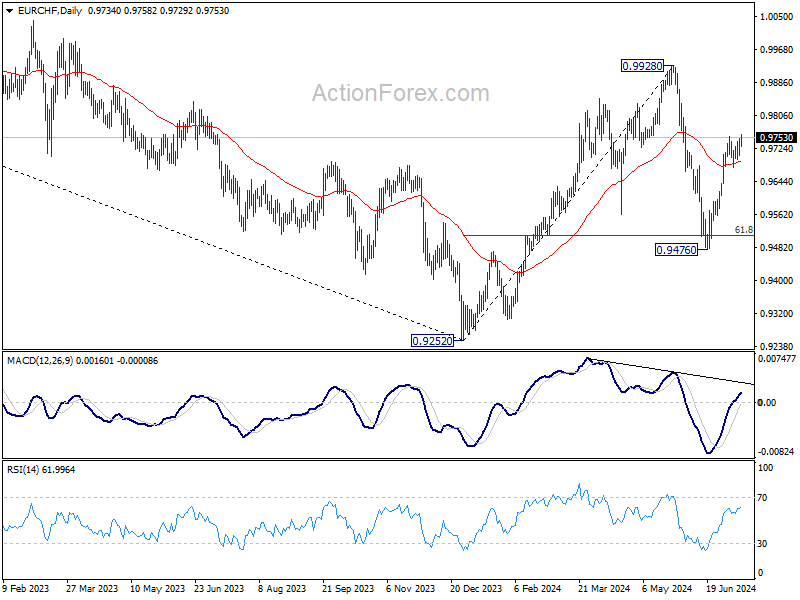

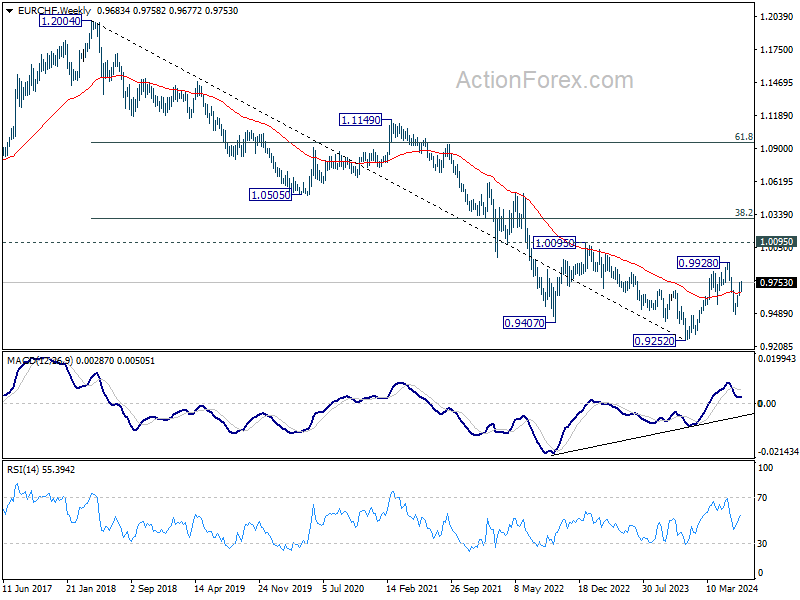

EUR/CHF Weekly Outlook

EUR/CHF's late breach of 0.9754 resistance last week suggests that rise from 0.9476 is resuming. Initial bias is back on the upside this week. Further rally would be seen to retest 0.9928 high. On the downside, however, break of 0.9677 will turn bias to the downside for deeper pullback.

In the bigger picture, rebound from 0.9252 medium term bottom might not be completed yet. But even in case of resumption, strong resistance could emerge from 1.0095 to limit upside. Medium term outlook will be neutral at best as long as 1.0094 structural resistance holds. Meanwhile, break of 0.9476 will bring retest of 0.9252 low.

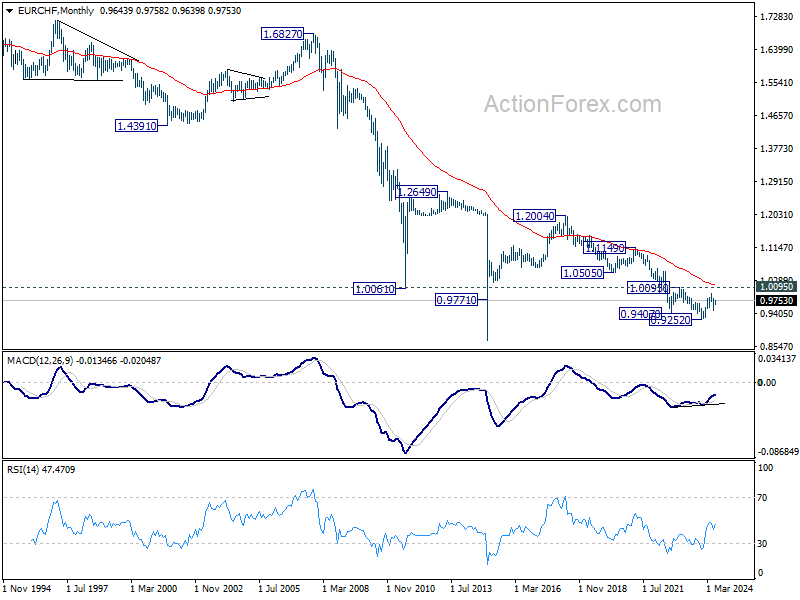

In the long term picture, fall from 1.2004 (2018 high) is part of the multi-decade down trend. Firm break of 1.0095 resistance is needed to be the first sign of long term bottoming. Otherwise, outlook will remain bearish.

The Week Ahead – ECB Spotlight as Fed Rate Speculations Drive Market Shifts

- US inflation data caused a significant selloff in US mega-cap tech stocks and a shift towards riskier areas of the market.

- The ECB interest rate decision is expected to bring no change, but the bank lending survey may shed light on the impact of higher rates on the economy.

- In the UK, inflation data is due on Wednesday, and while headline CPI dipped below 2% in June, it is expected to rise again in the second half of the year.

- In the US, the market will be quiet, with a speech by Fed Chair Powell being the most notable event.

Week in Review: Rate cut bets weigh on tech stocks as US inflation cools

Another week is over and market participants will undoubtedly have plenty of mixed feelings. The highlight of the week came on Thursday when US inflation data data was lower than expected, which has helped boost the confidence of individual FOMC members that inflation is on track to reach the Federal Reserve’s 2% target.

The headline CPI fell by 0.1% month-on-month instead of rising by 0.1% as predicted, while core CPI increased by 0.1% MoM compared to the 0.2% forecast. Additionally, initial jobless claims dropped by 17,000 to 222,000 and continuing claims remained stable. However, the low CPI number is the main focus, causing the 10-year Treasury yield to fall below 4.20% for the first time since late March.

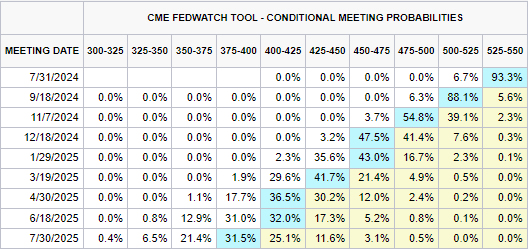

US Interest Rate probabilities have doubled over the past month with market participants now pricing in a 80%+ chance of a rate cut in September and a 60% chance of a cut in November. A stark contrast to two weeks ago and the most recent Fed meeting.

Source: CME Fedwatch Tool

US PPI data released on Friday showed an increase across the board. Market participants hoping for relief were disappointed, as any hopes of a modest US Dollar recovery were dashed by the preliminary Michigan consumer sentiment report. Lower-than-expected consumer sentiment and softer inflation expectations were enough to maintain selling pressure on the US Dollar heading into the weekend.

The most intriguing development following the inflation data release was a significant selloff in US mega-cap tech stocks. The inflation data prompted a notable shift towards riskier areas of the market, with the Russell 2000 emerging as the top performer.

Additionally, another noteworthy development that underscores concerns about the concentration of the S&P 500 in the ‘magnificent 7’ is that the index lost around 0.8% for the day, despite approximately 400 companies ending the day in the green.

The Russell 2000 surged 3.6%, marking its best day in 2024. Homebuilders soared, and banks saw gains ahead of the upcoming earnings season. Given that earnings season is upon us, this could play a crucial role in determining whether the rotation to more smaller stocks will be sustainable or prove to be short-lived.

The Week Ahead – EU, US and ASIA

Europe + UK

The week ahead brings the European Central Bank (ECB) interest rate decision with market participants expecting no change from the ECB. It would seem that the ECB bank Lending Survey may be more important as it sheds light on the impact higher rates are having on the economy.

In the UK we have inflation data due on Wednesday. Headline CPI dipped slightly below 2% in June, but this is likely the lowest point. Expect it to rise again in the second half of the year, settling between 2-2.5%. Services inflation is a bigger concern for the Bank of England and has been more persistent than expected. We anticipate some minor progress in this area as well. Much of the recent unexpected increase is due to price hikes at the start of the financial year, which the Bank of England believes is likely just noise, not a significant trend.

ASIA PACIFIC

In the Asia Pacific region, the most significant data release next week comes from China on Monday. This includes retail sales, industrial production, and GDP growth data, which will capture the attention of market participants. There is still some uncertainty regarding the Chinese economy, and recent data from the world’s second-largest economy has not alleviated these concerns. Weak data could negatively impact commodity-dependent currencies such as the Australian and New Zealand dollars, as well as the South African Rand.

US

In the US, market participants get a reprieve as we have a quiet week on the calendar. Among the most notable events will be a speech by Fed Chair Powell. It will be interesting to hear what the Fed Chair has to say following the CPI and PPI data and whether the PPI print may weigh on any decisions at the Fed upcoming meetings.

Chart of the Week

The chart I will be focusing on this week is the US Dollar Index (DXY). Following softer inflation data in the US, the DXY has broken through the psychological level of 105.00. The DXY also completed a break of the ascending trendline and both the 100 and 200-day MAs.

Price is resting at the 104.00 support handle heading into next week. I think the big question on the lips of market participants is whether this move will be sustainable. The lack of data next week from the US means the speech by Fed Chair Powell could be key in determining the US Dollar Indexes next move.

Continued weakness in the DXY will likely benefit US Dollar denominated currency pairs as well as commodities like Gold and Silver.

DXY Daily Chart – July 12, 2024

Source:TradingView.Com (click to enlarge)

The Weekly Bottom Line: U.S. – Inflation Cooling

U.S. Highlights

- U.S. inflation eased by more than expected in the month of June, raising the likelihood of a September rate cut.

- Small business confidence continued to edge higher in June, though several forward-looking indicators suggests some softening in the months ahead.

- Eyes will be on Chair Powell’s appearance in DC next week for a reaction to this week’s CPI data.

Canadian Highlights

- Taking the lead from the U.S., Canadian yields took a dive this week as a softer-than-expected U.S. CPI report raised the odds of the Federal Reserve easing its policy rate earlier than previously expected.

- Home sales picked up in June, although benchmark home price growth remained subdued – a welcome sign for consumer inflation.

- CPI will be next week’s headliner. Core inflation likely eased, but not enough to fully support a July rate cut.

U.S. – Inflation Cooling

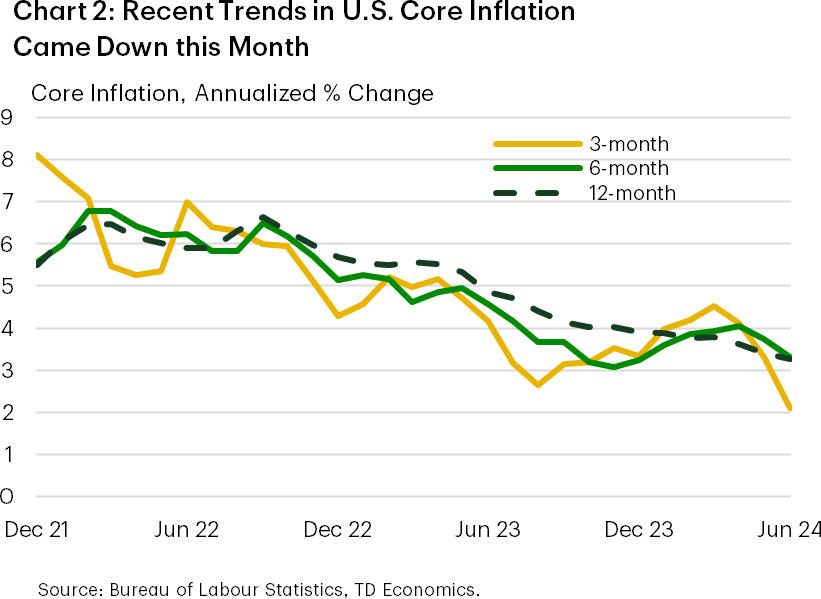

Federal Reserve Governor Lisa Cook said on Wednesday this week that the “soft landing” was starting to line up in U.S. data, a statement that, while intended to be backward-looking, may have been an unexpected act of prescience. A day later, the CPI report for June was released and as we wrote in our commentary yesterday, the report was exactly what the FOMC was looking for. The pace of inflation eased for both headline and core, as shown in Chart 1.

Defying expectations for modest gain of 0.1% from the previous month, headline CPI declined 0.1%. Core prices increased by a ‘soft’ 0.1%, compared to the 0.4% monthly gain averaged in the first 3 months of the year. By almost all measures, this is perhaps the most promising CPI report the FOMC has seen since it stopped raising interest rates just under a year ago. In Chart 2, we can see how how much this release brings down recent trends in CPI. The possibility of a September rate cut was already live, especially as concerns have been mounting over how quickly the labor market has been cooling– now we expect it to be at the forefront of the Fed’s decision-making.

Aside from the CPI report, it was a fairly light week for U.S. data. We did see the release of the NFIB Small Business Optimism Index, which generally painted a still upbeat picture for small businesses. However, there were hints of soft landing throughout the release, including a further easing in the share of firms planning to raise prices and further evidence that the labor market is cooling, with hiring intentions remaining handily below pre-pandemic levels.

We already mentioned Governor Lisa Cook’s speech which signaled, even before the last release of the CPI data, that prices, labor markets, and economic activity were evolving constructively in the eyes of the Fed. Chairman Powell offered a similar observation in his testimony to the Senate Committee on Banking, Housing, and Urban Affairs the day before. The Fed chairman made the point in his testimony that they see risks to the Fed’s dual mandate as more balanced than earlier this year when inflation had turned meaningfully higher. More balanced risks means the Federal Reserve will not delay rate cuts too long for fear of cooling the economy and the labor market too much.

Next week, attention will shift to the June readings of retail sales and housing starts as investors try and gauge to what extent domestic activity has slowed alongside the recent cooling in the labor market. We also look ahead to Chairman Powell’s appearance at the Economic Club of Washington on Monday, which is the first time we will hear from a voting FOMC member following this week’s inflation data. With the trend on inflation lower, and a number of employment metrics showing increasing slack building in the labor market, Powell will likely use next week’s appearance to start priming markets for a September cut.

Canada – Calm Before the Storm

Even with no week-shortening holiday to blame it on, there was a paucity of major Canadian economic data this week. Instead, Canadian markets were left to take their cues from developments elsewhere. In oil markets, prices were flat, as an improved summer demand backdrop faced off with easing supply concerns. Elsewhere, the benchmark 10-year bond yield followed its U.S. counterpart lower, after a soft U.S. CPI inflation print raised the expectation that the Federal Reserve could be getting closer to cutting its policy rate. This same factor also helped propel a gain in the TSX this week. Meanwhile, the Canadian dollar was broadly unchanged during the week and has been range-bound for nearly 2 years.

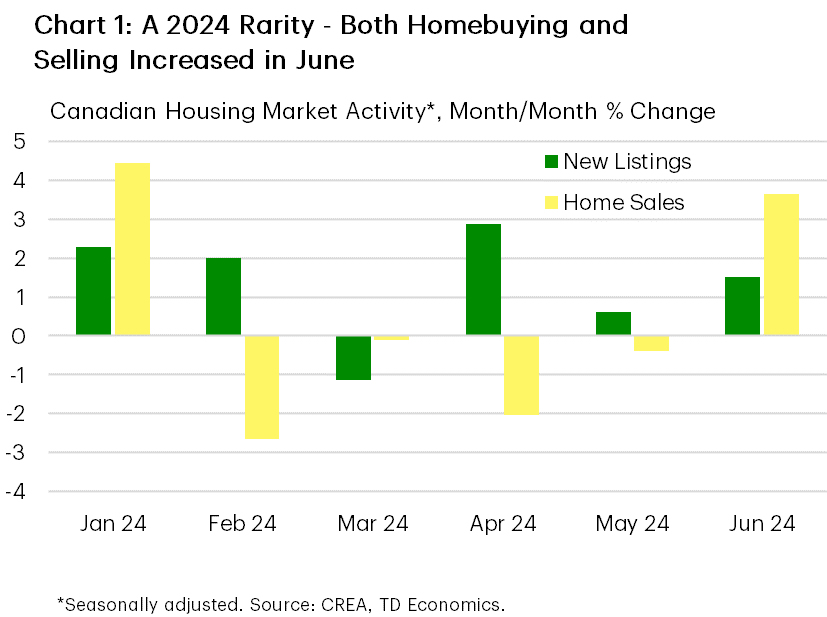

The week did offer a look at how Canadian housing markets performed in June and as it turns out, both buyers and sellers were more active, although sales levels remained low (Chart 1). A drop in interest rates during the month likely played some role in enticing buyers back into the market. Listings also picked up, posting their 5th increase in 6 months and offering buyers more choice. For their part, the Bank of Canada was likely pleased with the report, as overall economic growth was boosted by rising home sales. What’s more, the mild performance in benchmark prices suggests that the underlying trend in home price inflation remains subdued – a meaningful development for the CPI.

The real data fireworks come next week, with the Bank of Canada’s Business Outlook Survey (BoS) and Survey of Consumer Expectations on Monday and the June CPI report on Tuesday. Markets will also receive a pulse-check on the consumer via the retail trade report on Friday. On the latter, Statcan’s preliminary estimate suggests that retail spending dropped 0.6% month-on-month in May, offering some contrast to the gain shown in TD’s internal credit and debit card data. However, these same metrics point to a spending slowdown in June. A key takeaway from the prior BoS was that 2-year inflation expectations continued to decline while firms’ pricing behaviour further normalized in the first quarter. We’ll be looking for a continuation of these trends in the second quarter report. Economic growth indicators are also part of the Survey, but we’ve had plenty of other data showing the Canadian economy’s resilience in Q2, including decent job gains in the first two months of the quarter, an above-trend GDP growth print in April, and a preliminary estimate showing another monthly gain in May.

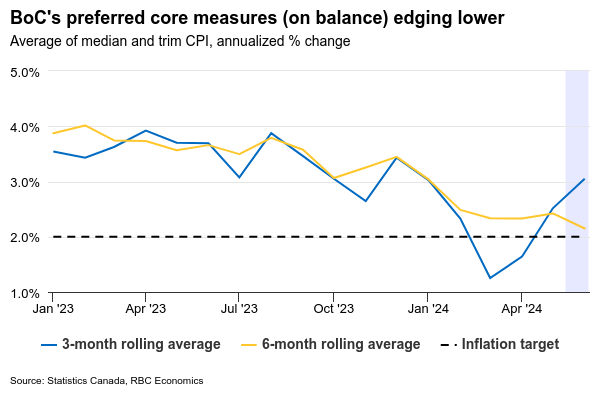

However, the inflation report will be the marquee print of the week. We expect that the average of the Bank of Canada’s preferred core inflation measures dipped to 2.8% year-on-year from 2.9% in May (Chart 2). If it materializes, this result would obviously be an improvement, although probably wouldn’t be enough to tip the scales in favour of a July rate cut. Indeed, the Bank’s next move is likely to come in September, which is when markets have the next rate cut fully priced-in.

Weekly Economic & Financial Commentary: Balanced Risks Drive the FOMC Closer to a September Rate Cut

Summary

United States: Fed’s Challenge: Making Sure Fire Is Out vs. Water Damage

- We learned this week that CPI declined in June and core prices rose at the slowest clip since early 2021. With the inflation target in sight, Fed policymakers are taking stock of deteriorating labor market dynamics and souring consumer sentiment as they weigh the outlook for rates.

- Next week: Retail sales (Tues.), Housing Starts (Wed.), Industrial Production (Wed.)

International: Some Encouraging Signs in Japanese Wage Growth and U.K. Economic Recovery

- This week, some underlying measures of pay growth in Japan bested expectations, potentially reflecting the historically high wage hikes agreed to in this year's spring wage negotiations; we view this as consistent with further Bank of Japan policy normalization this year and into next. In the U.K., monthly GDP figures revealed an ongoing economic recovery.

- Next week: China GDP (Mon.), Canada CPI (Tue.), European Central Bank Policy Rate (Thu.)

Interest Rate Watch: Balanced Risks Drive the FOMC Closer to a September Rate Cut

- Since January, the FOMC's post-meeting statement has signaled that neither further hikes were likely nor were rate cuts near. In Congressional testimony this week, however, Chair Powell's comments suggested that the FOMC is getting closer to exiting its holding pattern and preparing to descend.

Credit Market Insights: Interest Expense Getting to Consumers

- Consumer credit has downshifted thus far in 2024, as mounting personal interest expenses have increased the cost of carrying these debts. Revolving credit, which is primarily composed of credit cards, has driven much of this deceleration.

Topic of the Week: "Elevated Inflation Is Not the Only Risk We Face" – Jerome Powell

- Given the material cooling in the labor market over the past year, further deterioration may look less like a welcome “normalization” and more like unexpected weakening to the Fed. We highlighted several cracks in the labor market earlier this year, and six months later, the widespread signs of negative momentum in these worry spots persist.

June Inflation Report and BOS Survey Set the Stage for BoC’s Next Rate Cut

The Bank of Canada’s quarterly Business Outlook Survey (BOS) and June’s inflation data will be the last major data releases before the BoC’s next interest rate announcement on July 24. We expect a slowdown in inflation after an upside surprise in May and for the BOS to look soft enough to justify a second consecutive 25 basis point interest rate cut from the BoC at that meeting.

Headline consumer price index growth is expected to slow to 2.7% year-over-year after a surprisingly higher 2.9% reading in May. Energy price growth slowed on lower gasoline prices in June and food price increases have also been edging lower. Stripping out volatile food and energy components, inflation should come in at 3%, little changed from the prior month. But, the BoC will focus on growth in the preferred “core” measures, which provide more insights into broader underlying price growth trends. The closely watched three-month average of monthly increases will likely tick higher for both the median and trim CPI measures as a very small monthly increase in March falls out of that calculation, but the six-month average should hold around the 2% inflation target given earlier downside surprises.

The Q2 BOS will also be closely watched for further confirmation that the economic backdrop is continuing to soften in a way that would raise the central bank’s confidence about inflation pressures easing. The BoC’s governing council is particularly focused on indicators of the supply and demand balance in the economy, corporate pricing behaviour, inflation expectations, and wage growth. We expect all to show further improvement in the survey. Business responses’ will be reviewed for whether global shipping disruptions (and a jump higher in container shipping costs) are feeding through to increased costs. However, falling per capita gross domestic product and rising unemployment should mean that expected wage growth and inflation continue to slow. Corporate pricing behaviour has been normalizing with the frequency and size of price adjustments edging slowly back towards pre-pandemic levels.

Week ahead data watch

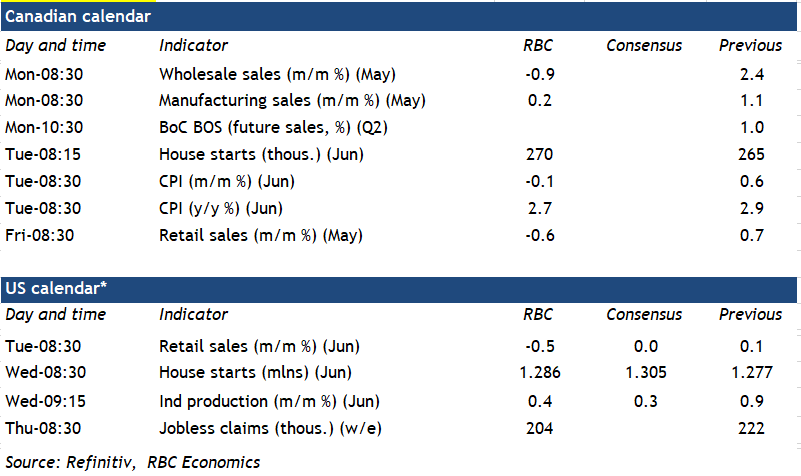

Canadian manufacturing sales likely edged up 0.2% in May, according to Statistics Canada’s flash estimate, down from 1.1% sales growth in April and primarily driven by higher sales in aerospace products and parts industry group as well as the food product subsector.

We expect Canadian core wholesale sales (excluding petroleum, products, and other hydrocarbons and excluding oilseed and grain) to drop by 0.9%, with sales in motor vehicles, parts and accessories seeing the largest decline.

Canadian housing starts likely increased by 270,000 in June, up 2.1% from last month after a 9.7% jump in April.

We look for a 0.6% decline in May Canadian retail sales, in line with StatCan’s advance indicator. Much of the slowdown came from lower auto sales during that month (-3.7% seasonally adjusted), as well as a price-related sales decline at gas stations (-3.2%).

U.S. retail sales likely edged lower 0.5% in June, given auto sales and sales at gas stations were down. Control sales should hold flat during that month.

We expect U.S. industrial production to inch higher by 0.4% in June with higher output in the manufacturing and mining sectors offsetting lower output in the utility sector.

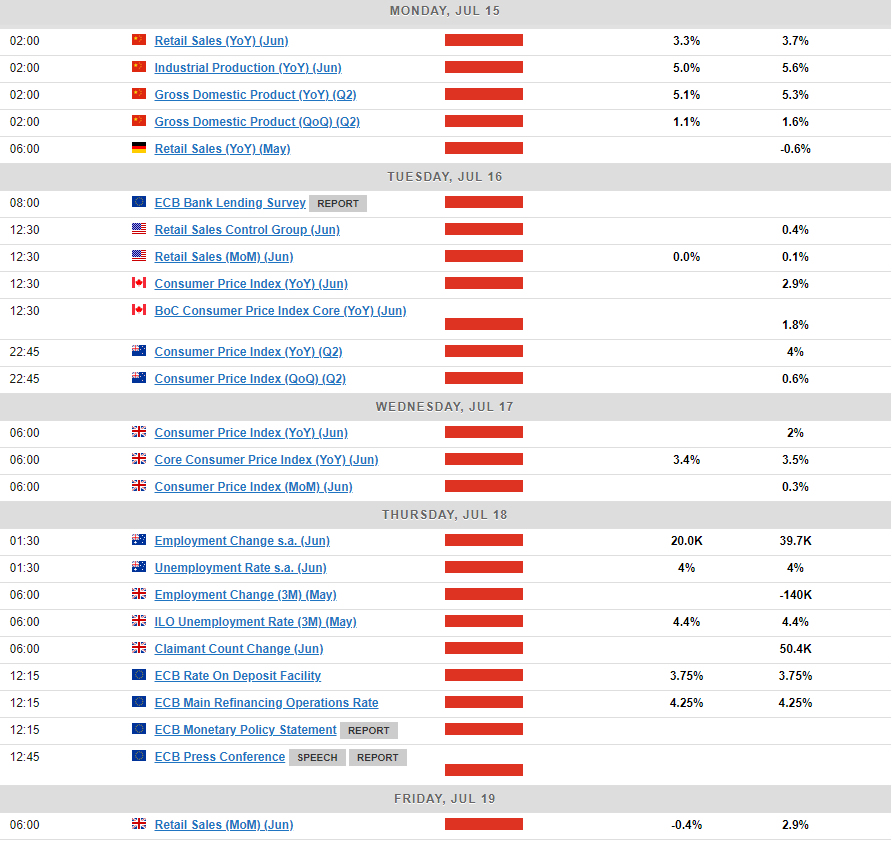

Summary 7/15 – 7/19

Monday, Jul 15, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Jun | 43 | |

| 23:01 | GBP | Rightmove House Price Index M/M Jul | 0% | |

| 02:00 | CNY | GDP Y/Y Q2 | 5.10% | 5.30% |

| 02:00 | CNY | Industrial Production Y/Y Jun | 5.00% | 5.60% |

| 02:00 | CNY | Retail Sales Y/Y Jun | 3.30% | 3.70% |

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jun | 3.90% | 4.00% |

| 02:00 | CNY | GDP Q/Q Q2 | 1.10% | 1.60% |

| 06:00 | EUR | Germany Retail Sales M/M May | 0.00% | -1.20% |

| 06:30 | CHF | PPI M/M Jun | 0.10% | -0.30% |

| 06:30 | CHF | PPI Y/Y Jun | -1.80% | |

| 09:00 | EUR | Eurozone Industrial Production M/M May | -1.00% | -0.10% |

| 12:30 | USD | Empire State Manufacturing Index Jul | -8 | -6 |

| 12:30 | CAD | Manufacturing Sales M/M May | 0.20% | 1.10% |

| 12:30 | CAD | Wholesale Sales M/M May | 2.00% | 2.40% |

| 14:30 | CAD | BoC Business Outlook Survey |

| GMT | Ccy | Events | |

|---|---|---|---|

| 22:30 | NZD | Business NZ PSI Jun | |

| Forecast: | Previous: 43 | ||

| 23:01 | GBP | Rightmove House Price Index M/M Jul | |

| Forecast: | Previous: 0% | ||

| 02:00 | CNY | GDP Y/Y Q2 | |

| Forecast: 5.10% | Previous: 5.30% | ||

| 02:00 | CNY | Industrial Production Y/Y Jun | |

| Forecast: 5.00% | Previous: 5.60% | ||

| 02:00 | CNY | Retail Sales Y/Y Jun | |

| Forecast: 3.30% | Previous: 3.70% | ||

| 02:00 | CNY | Fixed Asset Investment YTD Y/Y Jun | |

| Forecast: 3.90% | Previous: 4.00% | ||

| 02:00 | CNY | GDP Q/Q Q2 | |

| Forecast: 1.10% | Previous: 1.60% | ||

| 06:00 | EUR | Germany Retail Sales M/M May | |

| Forecast: 0.00% | Previous: -1.20% | ||

| 06:30 | CHF | PPI M/M Jun | |

| Forecast: 0.10% | Previous: -0.30% | ||

| 06:30 | CHF | PPI Y/Y Jun | |

| Forecast: | Previous: -1.80% | ||

| 09:00 | EUR | Eurozone Industrial Production M/M May | |

| Forecast: -1.00% | Previous: -0.10% | ||

| 12:30 | USD | Empire State Manufacturing Index Jul | |

| Forecast: -8 | Previous: -6 | ||

| 12:30 | CAD | Manufacturing Sales M/M May | |

| Forecast: 0.20% | Previous: 1.10% | ||

| 12:30 | CAD | Wholesale Sales M/M May | |

| Forecast: 2.00% | Previous: 2.40% | ||

| 14:30 | CAD | BoC Business Outlook Survey | |

| Forecast: | Previous: | ||

Tuesday, Jul 16, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M May | 0.20% | 1.90% |

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | 20.3B | 19.4B |

| 09:00 | EUR | Germany ZEW Economic Sentiment Jul | 44.3 | 47.5 |

| 09:00 | EUR | Germany ZEW Current Situation Jul | -73 | -73.8 |

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jul | 50.2 | 51.3 |

| 12:15 | CAD | Housing Starts Y/Y Jun | 259K | 265K |

| 12:30 | CAD | CPI M/M Jun | 0.10% | 0.60% |

| 12:30 | CAD | CPI Y/Y Jun | 2.90% | |

| 12:30 | CAD | CPI Median Y/Y Jun | 2.70% | 2.80% |

| 12:30 | CAD | CPI Trimmed Y/Y Jun | 2.80% | 2.90% |

| 12:30 | CAD | CPI Common Y/Y Jun | 2.40% | 2.40% |

| 12:30 | USD | Retail Sales M/M Jun | -0.20% | 0.10% |

| 12:30 | USD | Retail Sales ex Autos M/M Jun | 0.10% | -0.10% |

| 12:30 | USD | Import Price Index M/M Jun | 0.20% | -0.40% |

| 14:00 | USD | Business Inventories May | 0.30% | 0.30% |

| 14:00 | USD | NAHB Housing Market Index Jul | 44 | 43 |

| 22:45 | NZD | CPI Q/Q Q2 | 0.50% | 0.60% |

| 22:45 | NZD | CPI Y/Y Q2 | 4.00% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 04:30 | JPY | Tertiary Industry Index M/M May | |

| Forecast: 0.20% | Previous: 1.90% | ||

| 09:00 | EUR | Eurozone Trade Balance (EUR) May | |

| Forecast: 20.3B | Previous: 19.4B | ||

| 09:00 | EUR | Germany ZEW Economic Sentiment Jul | |

| Forecast: 44.3 | Previous: 47.5 | ||

| 09:00 | EUR | Germany ZEW Current Situation Jul | |

| Forecast: -73 | Previous: -73.8 | ||

| 09:00 | EUR | Eurozone ZEW Economic Sentiment Jul | |

| Forecast: 50.2 | Previous: 51.3 | ||

| 12:15 | CAD | Housing Starts Y/Y Jun | |

| Forecast: 259K | Previous: 265K | ||

| 12:30 | CAD | CPI M/M Jun | |

| Forecast: 0.10% | Previous: 0.60% | ||

| 12:30 | CAD | CPI Y/Y Jun | |

| Forecast: | Previous: 2.90% | ||

| 12:30 | CAD | CPI Median Y/Y Jun | |

| Forecast: 2.70% | Previous: 2.80% | ||

| 12:30 | CAD | CPI Trimmed Y/Y Jun | |

| Forecast: 2.80% | Previous: 2.90% | ||

| 12:30 | CAD | CPI Common Y/Y Jun | |

| Forecast: 2.40% | Previous: 2.40% | ||

| 12:30 | USD | Retail Sales M/M Jun | |

| Forecast: -0.20% | Previous: 0.10% | ||

| 12:30 | USD | Retail Sales ex Autos M/M Jun | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 12:30 | USD | Import Price Index M/M Jun | |

| Forecast: 0.20% | Previous: -0.40% | ||

| 14:00 | USD | Business Inventories May | |

| Forecast: 0.30% | Previous: 0.30% | ||

| 14:00 | USD | NAHB Housing Market Index Jul | |

| Forecast: 44 | Previous: 43 | ||

| 22:45 | NZD | CPI Q/Q Q2 | |

| Forecast: 0.50% | Previous: 0.60% | ||

| 22:45 | NZD | CPI Y/Y Q2 | |

| Forecast: | Previous: 4.00% | ||

Wednesday, Jul 17, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Jun | 0% | |

| 06:00 | GBP | CPI M/M Jun | 0.30% | |

| 06:00 | GBP | CPI Y/Y Jun | 2.00% | 2.00% |

| 06:00 | GBP | Core CPI Y/Y Jun | 3.40% | 3.50% |

| 06:00 | GBP | RPI M/M Jun | 0.40% | |

| 06:00 | GBP | RPI Y/Y Jun | 2.90% | 3.00% |

| 06:00 | GBP | PPI Input M/M Jun | 0.10% | 0.00% |

| 06:00 | GBP | PPI Input Y/Y Jun | -0.10% | |

| 06:00 | GBP | PPI Output M/M Jun | 0.10% | -0.10% |

| 06:00 | GBP | PPI Output Y/Y Jun | 1.70% | |

| 06:00 | GBP | PPI Core Output M/M Jun | 0.20% | |

| 06:00 | GBP | PPI Core Output Y/Y Jun | 1.00% | |

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | 2.50% | 2.50% |

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | 2.90% | 2.90% |

| 12:30 | USD | Building Permits Jun | 1.40M | 1.40M |

| 12:30 | USD | Housing Starts Jun | 1.30M | 1.28M |

| 13:15 | USD | Industrial Production M/M Jun | 0.30% | 0.90% |

| 13:15 | USD | Capacity Utilization Jun | 78.60% | 78.70% |

| 14:30 | USD | Crude Oil Inventories | -3.4M | |

| 18:00 | USD | Beige Book | ||

| 23:50 | JPY | Trade Balance (JPY) Jun | -0.89T | -0.62T |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:00 | AUD | Westpac Leading Index M/M Jun | |

| Forecast: | Previous: 0% | ||

| 06:00 | GBP | CPI M/M Jun | |

| Forecast: | Previous: 0.30% | ||

| 06:00 | GBP | CPI Y/Y Jun | |

| Forecast: 2.00% | Previous: 2.00% | ||

| 06:00 | GBP | Core CPI Y/Y Jun | |

| Forecast: 3.40% | Previous: 3.50% | ||

| 06:00 | GBP | RPI M/M Jun | |

| Forecast: | Previous: 0.40% | ||

| 06:00 | GBP | RPI Y/Y Jun | |

| Forecast: 2.90% | Previous: 3.00% | ||

| 06:00 | GBP | PPI Input M/M Jun | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 06:00 | GBP | PPI Input Y/Y Jun | |

| Forecast: | Previous: -0.10% | ||

| 06:00 | GBP | PPI Output M/M Jun | |

| Forecast: 0.10% | Previous: -0.10% | ||

| 06:00 | GBP | PPI Output Y/Y Jun | |

| Forecast: | Previous: 1.70% | ||

| 06:00 | GBP | PPI Core Output M/M Jun | |

| Forecast: | Previous: 0.20% | ||

| 06:00 | GBP | PPI Core Output Y/Y Jun | |

| Forecast: | Previous: 1.00% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jun F | |

| Forecast: 2.50% | Previous: 2.50% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun F | |

| Forecast: 2.90% | Previous: 2.90% | ||

| 12:30 | USD | Building Permits Jun | |

| Forecast: 1.40M | Previous: 1.40M | ||

| 12:30 | USD | Housing Starts Jun | |

| Forecast: 1.30M | Previous: 1.28M | ||

| 13:15 | USD | Industrial Production M/M Jun | |

| Forecast: 0.30% | Previous: 0.90% | ||

| 13:15 | USD | Capacity Utilization Jun | |

| Forecast: 78.60% | Previous: 78.70% | ||

| 14:30 | USD | Crude Oil Inventories | |

| Forecast: | Previous: -3.4M | ||

| 18:00 | USD | Beige Book | |

| Forecast: | Previous: | ||

| 23:50 | JPY | Trade Balance (JPY) Jun | |

| Forecast: -0.89T | Previous: -0.62T | ||

Thursday, Jul 18, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 01:30 | AUD | Employment Change Jun | 20.0K | 39.7K |

| 01:30 | AUD | Unemployment Rate Jun | 4.10% | 4.00% |

| 06:00 | CHF | Trade Balance (CHF) Jun | 5.05B | 5.81B |

| 06:00 | GBP | Claimant Count Change Jun | 50.4K | |

| 06:00 | GBP | ILO Unemployment Rate (3M) May | 4.40% | 4.40% |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y May | 5.70% | 5.90% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y May | 6.00% | |

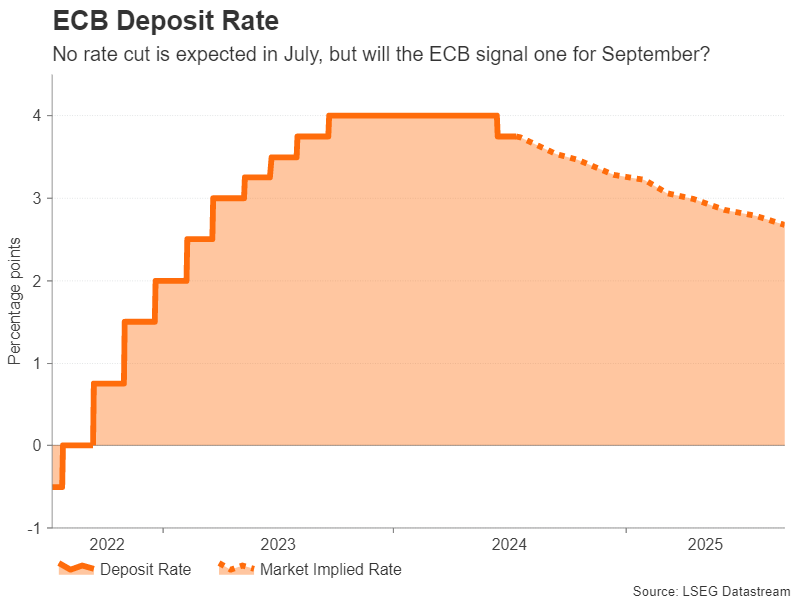

| 12:15 | EUR | ECB Deposit Rate | 3.75% | 3.75% |

| 12:15 | EUR | ECB Main Refinancing Rate | 4.25% | 4.25% |

| 12:30 | USD | Initial Jobless Claims (Jul 12) | 225K | 222K |

| 12:30 | USD | Philadelphia Fed Manufacturing Jul | 2.9 | 1.3 |

| 12:45 | EUR | ECB Press Conference | ||

| 14:30 | USD | Natural Gas Storage | 55B | 65B |

| 23:01 | GBP | GfK Consumer Confidence Jul | -11 | -14 |

| 23:30 | JPY | National CPI Y/Y Jun | 2.80% | |

| 23:30 | JPY | National CPI Core Y/Y Jun | 2.70% | 2.50% |

| 23:30 | JPY | National CPI Core-Core Y/Y Jun | 2.10% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 01:30 | AUD | Employment Change Jun | |

| Forecast: 20.0K | Previous: 39.7K | ||

| 01:30 | AUD | Unemployment Rate Jun | |

| Forecast: 4.10% | Previous: 4.00% | ||

| 06:00 | CHF | Trade Balance (CHF) Jun | |

| Forecast: 5.05B | Previous: 5.81B | ||

| 06:00 | GBP | Claimant Count Change Jun | |

| Forecast: | Previous: 50.4K | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) May | |

| Forecast: 4.40% | Previous: 4.40% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y May | |

| Forecast: 5.70% | Previous: 5.90% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y May | |

| Forecast: | Previous: 6.00% | ||

| 12:15 | EUR | ECB Deposit Rate | |

| Forecast: 3.75% | Previous: 3.75% | ||

| 12:15 | EUR | ECB Main Refinancing Rate | |

| Forecast: 4.25% | Previous: 4.25% | ||

| 12:30 | USD | Initial Jobless Claims (Jul 12) | |

| Forecast: 225K | Previous: 222K | ||

| 12:30 | USD | Philadelphia Fed Manufacturing Jul | |

| Forecast: 2.9 | Previous: 1.3 | ||

| 12:45 | EUR | ECB Press Conference | |

| Forecast: | Previous: | ||

| 14:30 | USD | Natural Gas Storage | |

| Forecast: 55B | Previous: 65B | ||

| 23:01 | GBP | GfK Consumer Confidence Jul | |

| Forecast: -11 | Previous: -14 | ||

| 23:30 | JPY | National CPI Y/Y Jun | |

| Forecast: | Previous: 2.80% | ||

| 23:30 | JPY | National CPI Core Y/Y Jun | |

| Forecast: 2.70% | Previous: 2.50% | ||

| 23:30 | JPY | National CPI Core-Core Y/Y Jun | |

| Forecast: | Previous: 2.10% | ||

Friday, Jul 19, 2024

| GMT | Ccy | Events | Consensus | Previous |

|---|---|---|---|---|

| 06:00 | GBP | Retail Sales M/M Jun | -0.40% | 2.90% |

| 06:00 | EUR | Germany PPI M/M Jun | 0.10% | 0.00% |

| 06:00 | EUR | Germany PPI Y/Y Jun | -2.20% | |

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | 12.0B | 14.1B |

| 08:00 | EUR | Eurozone Current Account (EUR) May | 38.6B | |

| 12:30 | CAD | Industrial Product Price M/M Jun | 0.00% | |

| 12:30 | CAD | Raw Material Price Index Jun | -1.00% | |

| 12:30 | CAD | Retail Sales M/M May | -0.20% | 0.70% |

| 12:30 | CAD | Retail Sales ex Autos M/M May | 1.20% | 1.80% |

| GMT | Ccy | Events | |

|---|---|---|---|

| 06:00 | GBP | Retail Sales M/M Jun | |

| Forecast: -0.40% | Previous: 2.90% | ||

| 06:00 | EUR | Germany PPI M/M Jun | |

| Forecast: 0.10% | Previous: 0.00% | ||

| 06:00 | EUR | Germany PPI Y/Y Jun | |

| Forecast: | Previous: -2.20% | ||

| 06:00 | GBP | Public Sector Net Borrowing (GBP) Jun | |

| Forecast: 12.0B | Previous: 14.1B | ||

| 08:00 | EUR | Eurozone Current Account (EUR) May | |

| Forecast: | Previous: 38.6B | ||

| 12:30 | CAD | Industrial Product Price M/M Jun | |

| Forecast: | Previous: 0.00% | ||

| 12:30 | CAD | Raw Material Price Index Jun | |

| Forecast: | Previous: -1.00% | ||

| 12:30 | CAD | Retail Sales M/M May | |

| Forecast: -0.20% | Previous: 0.70% | ||

| 12:30 | CAD | Retail Sales ex Autos M/M May | |

| Forecast: 1.20% | Previous: 1.80% | ||

A September Fed Rate Cut Could Lead to Easing Spree During end-2024

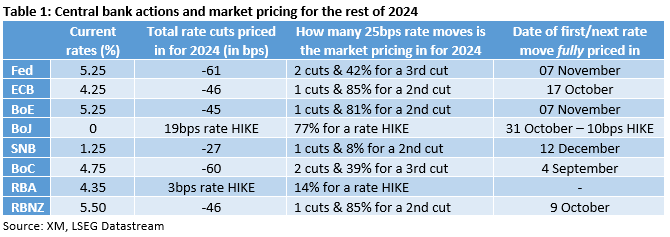

- Market prices in at least two rate cuts from Fed

- ECB, BoE expected to follow suit despite divergent economic conditions

- SNB and BoC could ease further; RBNZ possibly close to a summer rate cut

- BoJ and RBA could surprise with rate hikes during 2024

We are halfway into 2024 and the countdown for this year’s key event, the US presidential election, has already started. With geopolitics taking a backseat lately, despite both the Ukrainian-Russian and Israeli-Hamas conflicts remaining unresolved, political risk is expected to affect market sentiment, as seen lately in the euro area.

Amidst these developments, the key central banks are trying to implement their strategy. The ECB, the Swiss National Bank and the Bank of Canada have already started to ease their monetary policy stance while the Bank of Japan has managed to hike once so far in 2024. The remaining central banks, and predominantly the Fed, remain on the sidelines. Ahead of the next round of central bank meetings, what is the market pricing in for the rest of 2024?

The Fed to follow in the ECB's footsteps?

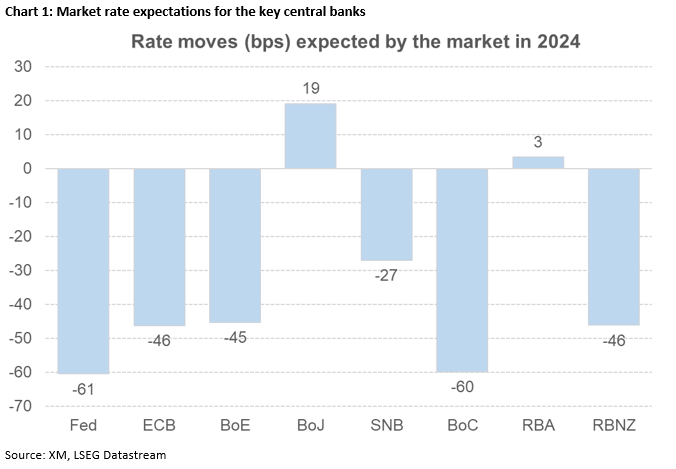

The recent US labour market data and the June CPI report have probably firmly opened the door to the much-discussed rate cuts by the Fed. The market is currently pricing in 61bps of rate easing in 2024, which translates to two 25bps rate cuts and a 41% chance for a third similarly sized move. Considering the November presidential election and the June 2024 dot plot penciling in one rate cut, the market might be getting too optimistic, especially if the data improves over the summer.

Turning to the ECB, when a central bank announces its first rate cut, the path is assumed to be fixed towards further accommodation. As made evident by recent ECB members' comments, this is not the case now. Having said that, the market is currently expecting 46bps of easing in 2024, which means one full 25bps rate move and around 90% possibility of a second rate cut. Interestingly, political developments in France could tip the balance in favour of more rate cuts down the line.

The market expects both the BoE and the RBZN to start cutting soon

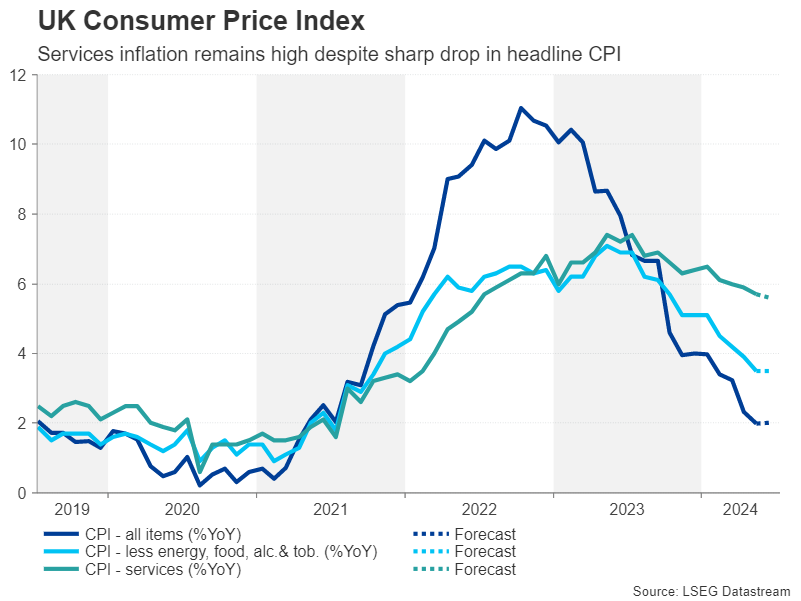

The market expects almost two rate cuts by both the Bank of the England and the Reserve Bank of New Zealand in 2024. The recent aggressive drop in UK headline inflation could have opened the door to a rate cut by the BoE, but the political developments forced it to go into a brief hibernation. With the general election out of the picture, another weak CPI report on July 17 could materially increase the chance of a rate cut at the August 1 meeting, which includes the quarterly monetary policy report.

Similarly, the RBNZ’S dovish shift at its most recent meeting surprised the market since just 40 days ago the RBNZ was considering the rate hike option. The market has quickly adapted to the new status quo by pricing in a total easing of 46bps by year-end, with a considerable probability of a summer rate cut if the imminent quarterly CPI surprises on the downside.

BoC and SNB cut rates, market expects more

Responding to easing inflation, both the BoC and the SNB eased their monetary policy stance over the past few months. In the case of the former, the Canadian economy has not been firing into all cylinders with unemployment rising to the highest level since February 2022. Ignoring the recent upside surprise in monthly inflation, the market continues to fully price in two rate cuts in 2024, with a sizeable possibility of a third one towards the end of the year.

Turning to the SNB and the two rate cuts already announced were partly unexpected but probably justified due to the low inflation rate and the continued strengthening of the franc. The SNB stands ready to ease further, with the market currently fully pricing in another 25bps rate cut at the December meeting.

BoJ to hike again, RBA thinking about it

The BoJ remains on the lonely path of tightening its monetary policy stance. The April rate hike was welcomed by the market, but BoJ’s recent inactivity has raised a few eyebrows, weakening the yen. Japanese authorities could be hoping that a sustained worsening of US data and the mild hawkishness of the BoJ could help the yen recover. The market is looking for 19bps of rate hikes by the BoJ in 2024 with the next 10bps rate hike expected at the September meeting. Firstly though, the market awaits the full details of the bond buying programme tapering.

The Reserve Bank of Australia is the only other central bank thinking about rate hikes. Stickier inflation and a tight labour market are keeping Governor Bullock et al on their toes with the minutes from the June meeting confirming the RBA’s intention to hike rates if needed. The market is tentatively pricing in 3bps of tightening in 2024 but RBA’s rates outlook will probably be gravely affected by the July 31 CPI print for the second quarter of 2024.

Week Ahead – ECB Set to Hold Rates, Plethora of Data on the Way

- ECB is not expected to cut in July but will it signal one for next meeting?

- Retail sales will be the main highlight in the United States

- UK CPI report will be vital for BoE’s August decision

- China GDP data to kickstart busy week

ECB meets amid sticky inflation

The European Central Bank concludes its two-day policy meeting on Thursday but no change in interest rates is anticipated after trimming them by 25 basis points at last month’s gathering. The June decision proved to be somewhat controversial, as policymakers inadvertently locked themselves into cutting rates before all the data was in. An uptick in both inflation and wage growth right before the meeting was not something that the Governing Council wanted to see, but not cutting rates would probably have been even more embarrassing.

The ECB justified its decision by pointing out the risk of undershooting its inflation target if it waited too long. Since then, inflation has fallen back marginally and there’s indications that pay pressures are cooling even though wage growth remains elevated.

Hence, there seems to be a strong majority for at least one more cut in 2024, but views vary about a third reduction. However, this is a debate for another day and policymakers are almost certain to keep rates unchanged on Thursday and reassess the risks when they regroup in September.

Markets are not fully convinced about a third cut either and if President Lagarde refrains from providing any explicit forward guidance, the euro could extend its recent gains. But should she commit to a cut in September, that would be negative for the single currency.

Markets are not fully convinced about a third cut either and if President Lagarde refrains from providing any explicit forward guidance, the euro could extend its recent gains. But should she commit to a cut in September, that would be negative for the single currency.

Also to keep an eye on next week are the ZEW economic sentiment survey out of Germany on Tuesday, and the final estimates of Eurozone CPI for June on Wednesday.

Pound bulls face CPI test

The British pound has been enjoying a sizeable rally in July, helped by a softer US dollar as well as by Labour winning a large majority in the UK general election, ending years of a turmoil under the Tories. But that’s not all. Despite headline inflation falling to the Bank of England’s 2% target in June, services inflation remains too high for comfort at 5.7%, something that the Bank’s chief economist Huw Pill stressed just this week. In addition, with the British economy seeing a revival in growth momentum, there isn’t a very strong urgency to lower rates imminently.

With markets split 50/50 about an August cut and policymakers probably undecided too, next week’s updates on inflation, employment and retail sales could be decisive.

The June CPI report is out first on Wednesday, labour market stats for May will follow on Thursday, and retail sales for June are due on Friday.

Any further moderation in core and services CPI, as well as in wage growth, could seal the deal for an August rate cut, potentially knocking sterling lower. Yet, given the euro’s and yen’s woes, plus the improving outlook for the UK economy, further progress on the inflation front that gives the BoE the green light to cut rates soon might not be too catastrophic for the pound.

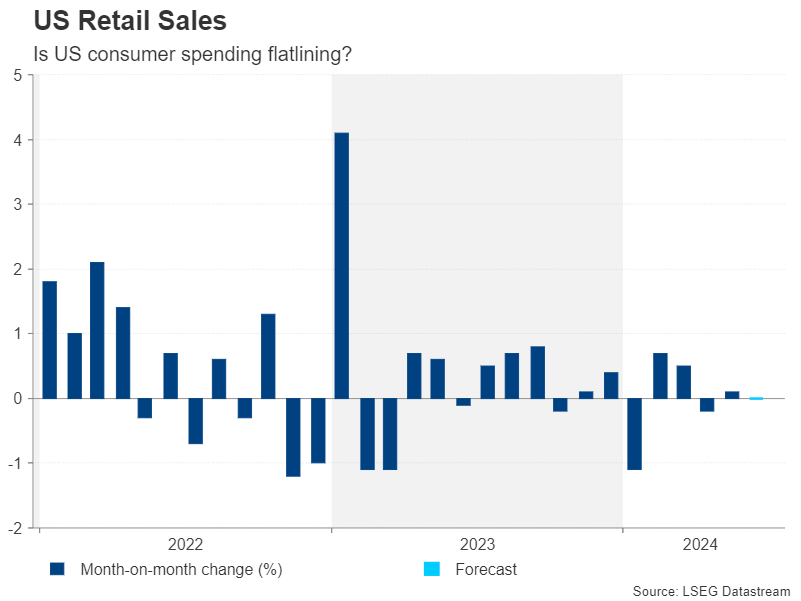

Are US consumers tightening their belts?

Over in the US, the Federal Reserve is also not in a hurry to start slashing rates, but investors are increasingly confident about a move in September. Inflation is edging down again after stalling earlier in the year, while Chair Powell noted that the labour market has cooled lately. Consumer spending also appears to be slowing and there could be more evidence of this in Tuesday’s retail sales figures.

Retail sales are expected to have stayed unchanged at 0.0% m/m in June after rising by just 0.1% in May. Any unexpected bounce back in retail sales could bring a halt to the dollar’s slide.

Investors will also be tracking manufacturing gauges from the New York and Philadelphia Feds on Monday and Thursday, respectively, while on Wednesday, there will be a flurry of releases, including building permits, housing starts and industrial production.

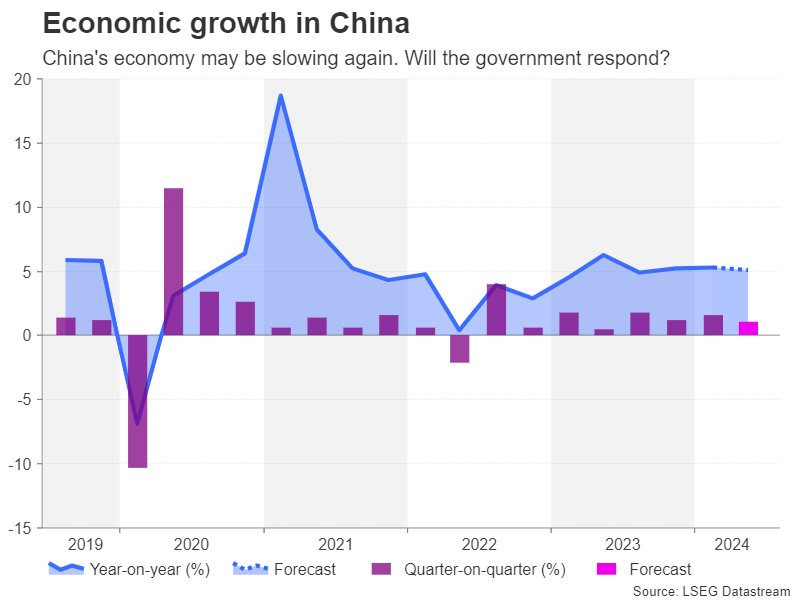

China’s economy likely slowed in Q2

Despite numerous efforts to boost the flagging economy, the Chinese government has been unable to turn things around. Although the downturn in the property market has started to ease, the crisis is far from being over, and the stock market is struggling to recover from a three-year slump.

Investor and consumer confidence therefore remain low, weighing on business and household spending. Industrial production has started to show some signs of life this year, but retail sales have been sluggish. The June readings for both will be watched on Monday alongside the GDP estimate for the second quarter.

China’s economy likely grew by 1.1% on a quarterly basis in the three months to June, a slowdown from the 1.6% pace in the first quarter. The year-on-year rate is also forecast to have eased from 5.3% to 5.1%.

Whilst investors have come to expect less-than-spectacular GDP numbers out of China in recent quarters, a downside surprise could still hurt market sentiment at the start of the trading week, hitting regional stocks and risk-sensitive currencies such as the Australian dollar.

However, a bad set of figures might prompt policymakers to come up with bolder measures. The country’s Communist Party leaders meet on July 15-18 for what is called the Third Plenum, which is typically held every five years, usually in the autumn but was delayed in 2023. The meeting focuses on long-term economic reforms and goals but it’s unclear if it will be followed by any immediate policy responses.

Meanwhile, aussie traders will additionally be monitoring domestic employment numbers on Thursday.

Canada, Japan New Zealand also awaiting CPI data

Inflation in Canada unexpectedly ticked higher in May, dampening hopes for a back-to-back rate cut in July. Unless the June report that’s out on Tuesday points to some easing in price pressures, the Bank of Canada will likely stay on hold at least until September. On the other side of the argument is the weakening of the labour market, which is limiting the loonie’s upside amid the greenback’s broad selloff.

The BoC’s survey on the business outlook due on Monday and Friday’s retail sales data might shed more light on the state of economy but the focus will primarily be on the CPI readings.

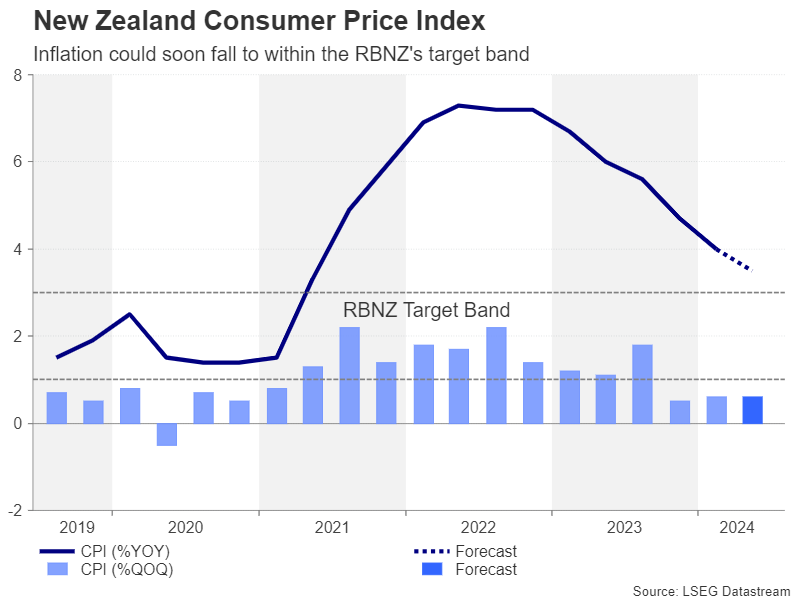

In New Zealand, the quarterly CPI publication on Wednesday will be just as crucial for rate cut bets. The Reserve Bank of New Zealand leaned to the dovish side at its latest meeting, sounding upbeat about the prospect of inflation hitting its 1-3% target band in the second half of the year. The kiwi could face fresh selling pressure if the Q2 CPI print takes the RBNZ one step closer to its target range.

Wrapping up the week on Friday will be Japan’s CPI numbers. As the Bank of Japan’s July 31 meeting approaches, the CPI data will be scrutinized for final clues as to whether a rate hike is likely this month. The BoJ has hinted that the expected announcement on bond tapering at the next gathering should not be seen as putting the rate hike decision on hold. But investors are still not convinced there’s a strong enough case to raise rates further, so any upside surprises in June CPI could lift the yen.

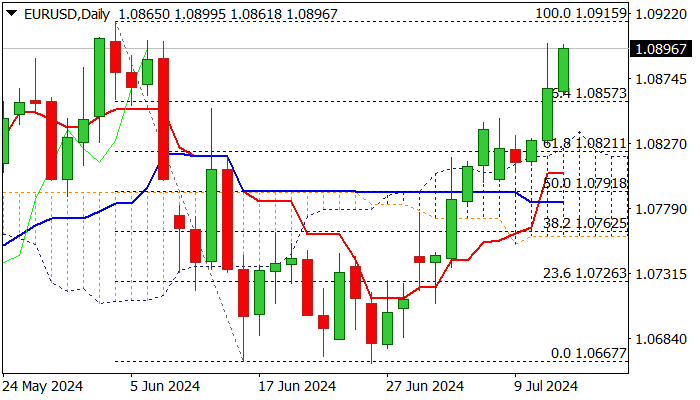

EUR/USD Outlook: Bulls Hold Grip for Further Advance

EURUSD continues to trend higher, with minimal negative impact from hotter than expected US PPI data (Jun 0.2% m/m vs 0.1% f/c and 0.0% in May).

The latest bull-leg extends into third straight and day pressuring Thursday’s post US CPI spike high (1.0898) which guards pivotal barriers at 1.0919 (Jun 4), 1.0981 (Mar 8) and 1.10 (psychological).

The pair is also on track for the third consecutive weekly gain, with expectations for further upside, should fundamentals remain favorable.

Broken Fibo 76.4% barrier (1.0857) offers initial support, followed by more significant daily cloud top (1.0835)

Res: 1.0900; 1.0919; 1.0981; 1.1000.

Sup: 1.0857; 1.0835; 1.0821; 1.0800.