Sample Category Title

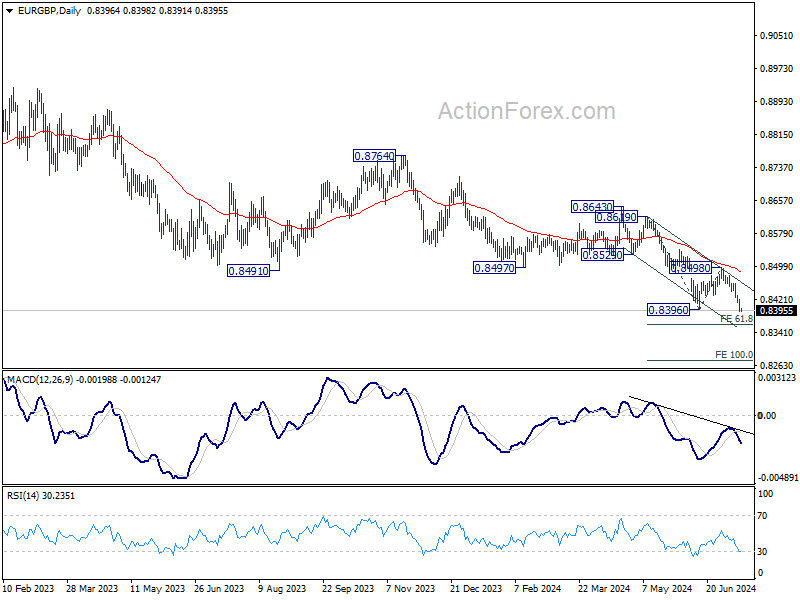

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8385; (P) 0.8404; (R1) 0.8415; More....

Intraday bias in EUR/GBP stays on the downside at this point. Larger down trend is resuming and should target 61.8% projection of 0.8619 to 0.8396 from 0.8498 at 0.8360. Firm break there could prompt downside acceleration to 100% projection at 0.8275. On the upside, above 0.8421 minor resistance will delay the bearish case and turn intraday bias neutral first.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 0.8201 key support (2022 low). For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

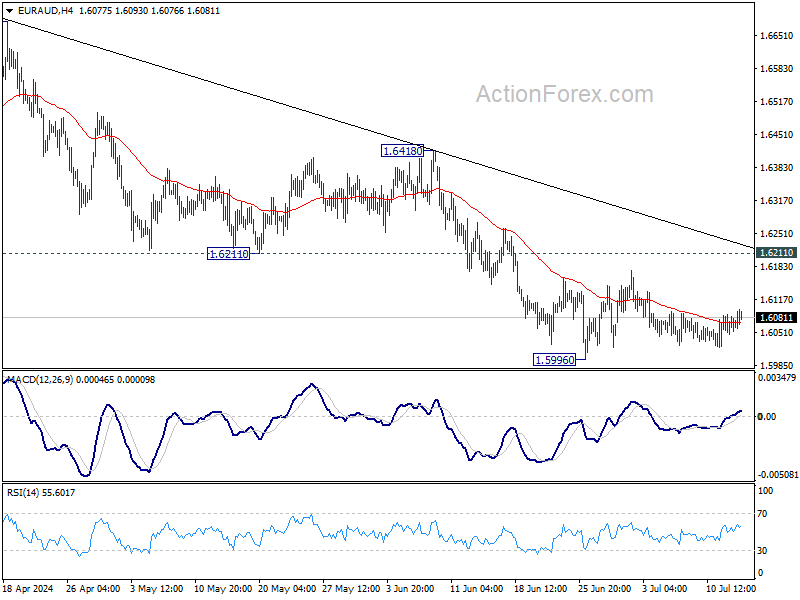

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6054; (P) 1.6072; (R1) 1.6096; More...

Intraday bias in EUR/AUD remains neutral as consolidation from 1.5996 continues. While another recovery cannot be ruled out, further decline is expected as long as 1.6211 resistance holds. Break of 1.5996 will resume larger fall to 1.5846 support next.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low) only. Strong support is still expected between 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.6148 resistance will argue that the correction has completed.

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9719; (P) 0.9739; (R1) 0.9777; More....

Intraday bias in EUR/CHF remains on the upside at this point. Rise from 0.9476 is in progress and should target 0.9928 high next. On the downside, however, break of 0.9677 will turn bias to the downside for deeper pullback.

In the bigger picture, rebound from 0.9252 medium term bottom might not be completed yet. But even in case of resumption, strong resistance could emerge from 1.0095 to limit upside. Medium term outlook will be neutral at best as long as 1.0094 structural resistance holds. Meanwhile, break of 0.9476 will bring retest of 0.9252 low.

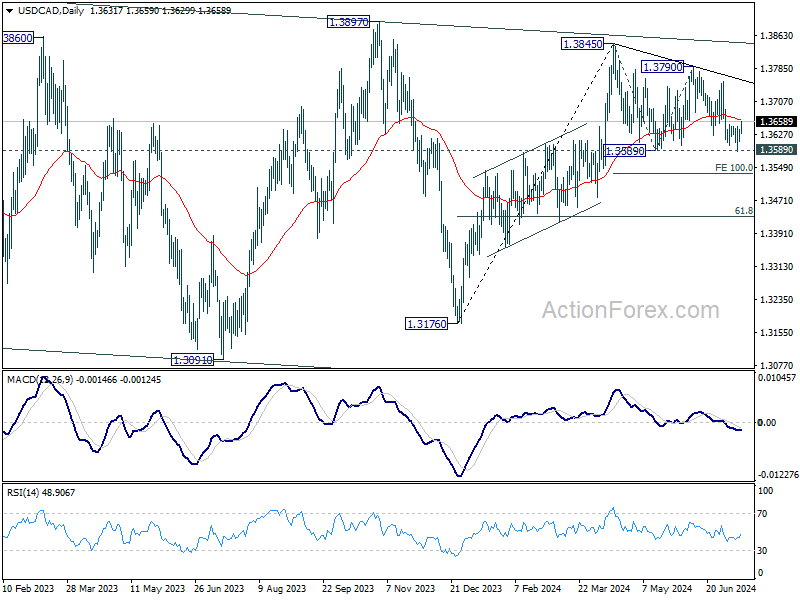

USD/CAD Daily Outlook

Daily Pivots: (S1) 1.3616; (P) 1.3630; (R1) 1.3649; More...

Break of 1.3652 resistance suggests that a short term bottom was formed at 1.3588, after hitting 1.3589 support. Intraday bias is back on the upside for 13790 resistance. On the downside, firm break of 1.3589 will extend the corrective pattern from 1.3845 to 100% projection of 1.3845 to 1.3589 from 1.3790 at 1.3534.

In the bigger picture, price actions from 1.3976 (2022 high) are viewed as a corrective pattern. In case of another fall, strong support should emerge above 1.2947 resistance turned support to bring rebound. Firm break of 1.3976 will confirm up resumption of whole up trend from 1.2005 (2021 low). Next target is 61.8% projection of 1.2401 to 1.3976 from 1.3176 at 1.4149.

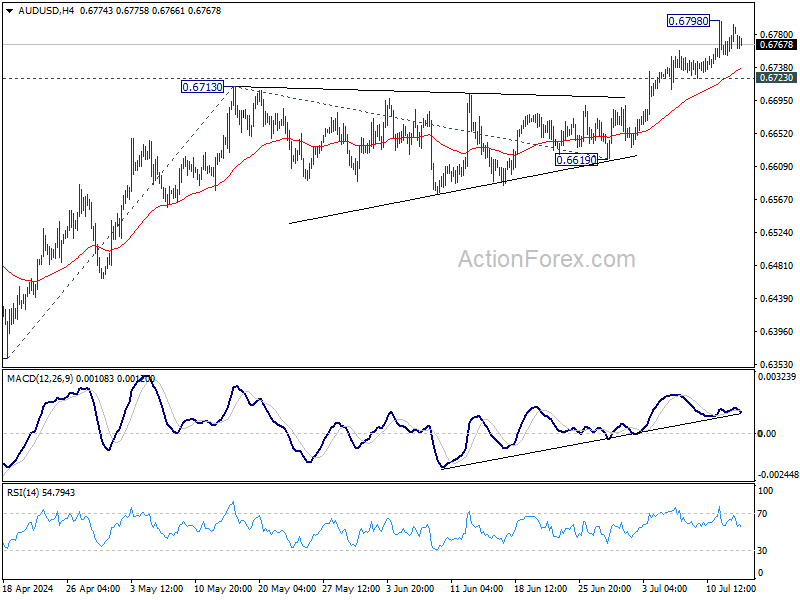

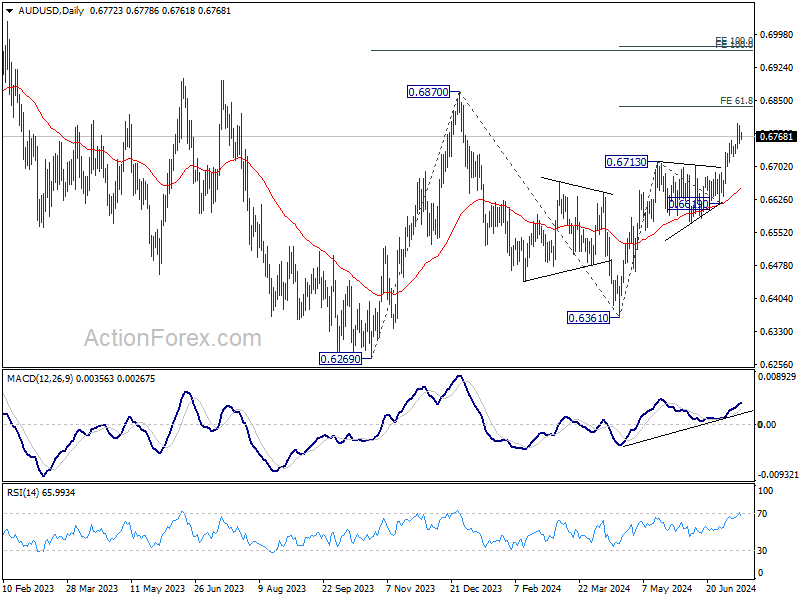

AUD/USD Daily Report

Daily Pivots: (S1) 0.6761; (P) 0.6777; (R1) 0.6801; More...

Intraday bias in AUD/USD is turned neutral for some consolidations. On the upside, above 0.6898 will target 61.8% projection of 0.6361 to 0.6713 from 0.6619 at 0.6837. Decisive break there could prompt upside acceleration through 0.6870 resistance to 100% projection at 0.6971. On the downside, however, break of 0.6723 support will turn intraday bias to the downside for deeper pullback.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg. Break of 0.6870 will target 100% projection of 0.6269 to 0.6870 from 0.6361 at 0.6962.

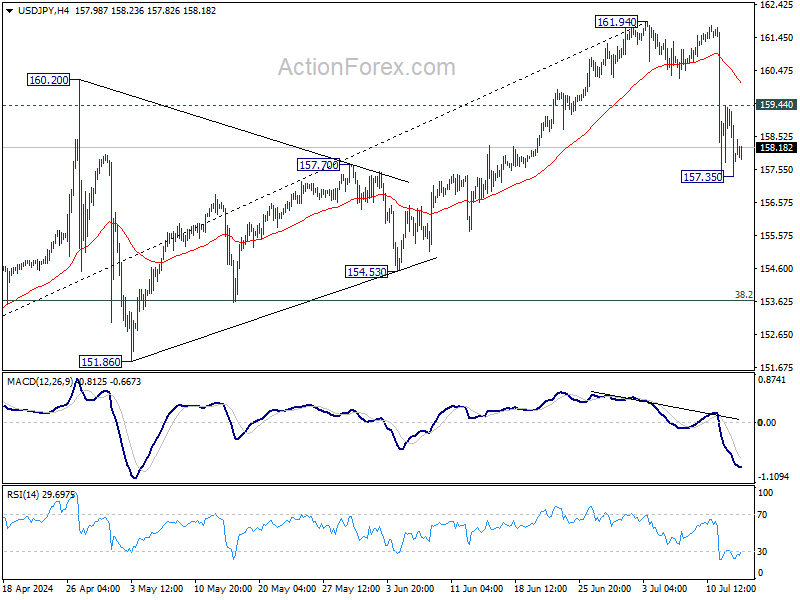

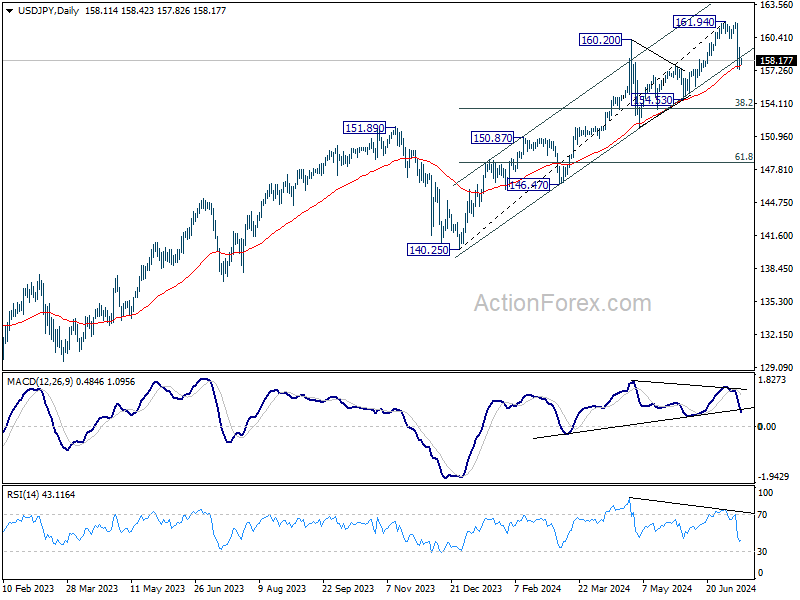

USD/JPY Daily Outlook

Daily Pivots: (S1) 157.03; (P) 158.24; (R1) 159.12; More...

Fall from 161.94 is seen as correcting the whole five-wave rally from 140.25. Deeper decline is in favor and sustained trading below 55 D EMA (now at 157.67) will affirm this bearish case. Next target will be 38.2% retracement of 140.25 to 161.94 at 163.65. Nevertheless, break of 159.44 will turn bias back to the upside for stronger rebound.

In the bigger picture, as long as 151.89 resistance turned support holds, long term up trend could still continue through 161.94 at a later stage. Next target will depend on the depth of the current correction from 161.94. However, sustained break of 151.89 will argue that larger scale correction or trend reversal is underway.

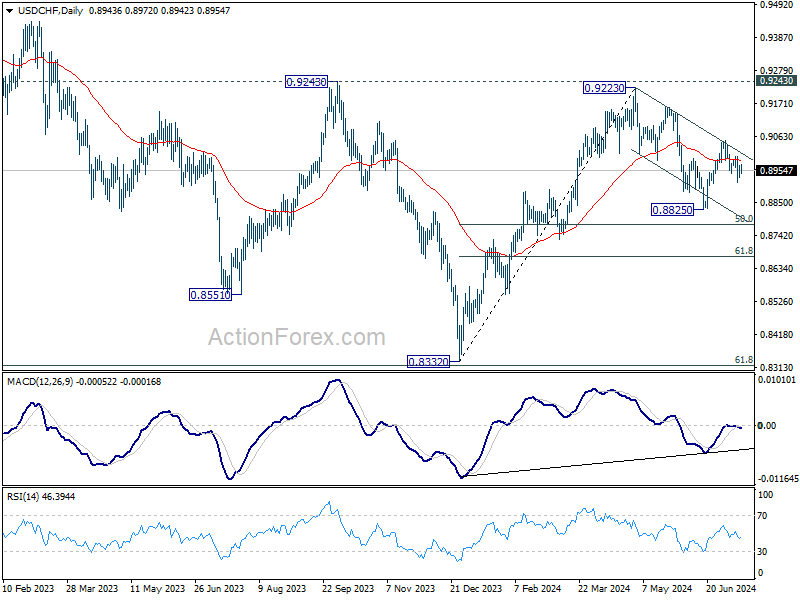

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8927; (P) 0.8949; (R1) 0.8966; More…

Further decline is in favor in USD/CHF with 0.9000 resistance intact. Below 0.8914 will target 0.8825 low. Break of 0.8825 will target 50% retracement of 0.8332 to 0.9223 at 0.8778 next. However, break of 0.9000 will turn bias back to the upside for 0.9049 resistance instead.

In the bigger picture, with 0.9243 resistance intact, medium term outlook in USD/CHF is neutral at best. For now, more sideway trading is likely between 0.8332/9243. However, firm break of 0.9243 will indicate larger bullish trend reversal.

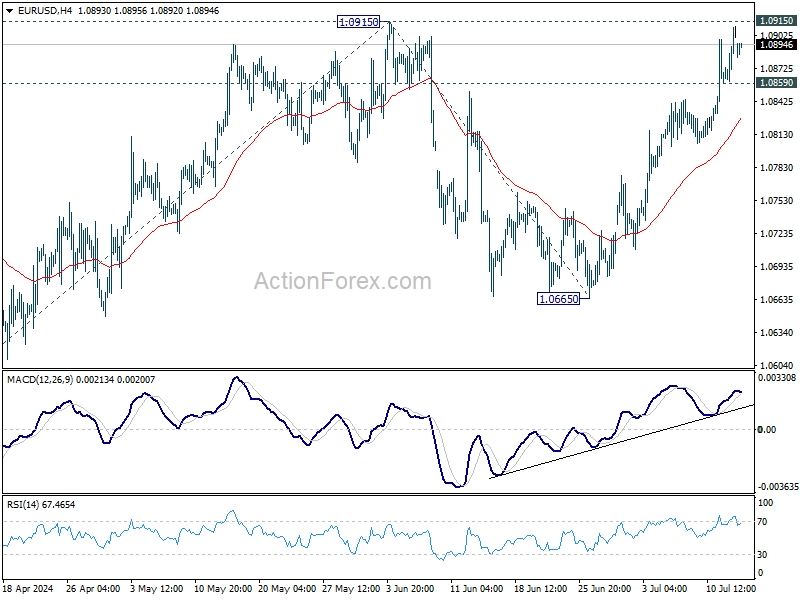

EUR/USD Daily Outlook

Daily Pivots: (S1) 1.0876; (P) 1.0893; (R1) 1.0925; More....

Intraday bias in EUR/USD remains on the upside at this point. Decisive break of 1.0915 resistance will resume whole rise from 1.0601 to 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0979. On the downside, below 1.0859 minor support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern, possibly a triangle, that's still be in progress. Break of 1.1138 resistance will be the first signal that rise from 0.9534 (2022 low) is ready to resume through 1.1274 (2023 high). This will now remain the favored case as long as 1.0601 support holds.

Trump Assassination Attempt Boosts His Chances of Winning November Election

Donald Trump got this close to being assassinated this weekend while he was giving a speech in an election rally. He was lucky that the bullet only grazed his ear, but he showed his resilience by demonstrating strength and defiance just minutes after being shot. The image of strong and heroic Trump with blood on his face, fist up in the air and with an American flag waving behind him as security guards were taking him away from the scene marked the weekend – and came as a perfect contrast to old and weakened Biden since the TV debate. Cherry top, Trump said that he would attend the Republican National Convention next week. All in all, even though the assassination incident on Trump was shocking – and spurred the worries of a deeply divided America where political violence is taking over – it boosted the chances that Trump will win the presidential election in November from 61% before the shooting to 67% after, according to PredictIt. And if history is any indication, such events have been a boon for a candidate in past elections.

Bitcoin – which has been struggling since the beginning of June – jumped past the $62K after the incident on flight to safety and because Trump backs the asset, the US dollar opened the week slightly higher and gold remains surprisingly unreactive to the news. US futures, on the other hand, are in the positive this morning as the S&P500 performed well under Trump and increased odds for Trump victory are also perceived as good news for the market. Happy Monday!

Other than that

It feels like ages ago but another set of good news for the market came last week, remember, when Federal Reserve (Fed) President Jerome Powell said that the only risk to the US economy is no longer inflation but also the cooling jobs market – a speech that sent the probability of a September rate hike to above 90% although Powell didn’t want to give any hint regarding the timing of the first rate cut. The latest set of CPI figures came in softer-than-expected and investors greatly overlooked the stronger-than-expected PPI figures released Friday.

It’s worth noting that producer prices in the US unexpectedly jumped last month, PPI rose from 2.4% to 2.6% while core PPI jumped from 2.6% to 3%. It’s soothing that the Fed is no longer only focused on inflation but it does not mean that they will completely disregard the inflation numbers. They still matter.

But anyway, the markets didn’t panic much on PPI but decided to focus on soft Michigan index that revealed softer inflation expectations and murkier sentiment. As such, the US 2-year yield dived to 2.45% and the 10-year closed last week below 4.20% mark. The S&P500 hit a fresh record, Nasdaq gained, but the real winner of the week was the small caps. The Russell 200 jumped more than 6% in just three sessions and traded at the highest levels since January 2022 on hope that the Fed rate cuts would benefit more to the small caps than to Big Tech.

Data and earnings

Inflation data came in slightly higher than expected in France and in Spain, and cemented the idea that the European Central Bank (ECB) will stay pat when it meets this Thursday. Traders will be looking for hints of another cut in September. The EURUSD is slightly lower this morning on the back of a broadly stronger US dollar on Trump assassination attempt, but the rising odds of September cut from the Fed remain supportive of a further rise and we can see the EURUSD settle within the 1.10/1.12 range between now and September.

Across the Channel, Brits will reveal their latest CPI numbers on Wednesday and according to some predictions, headline CPI may have eased below the 2% mark in June – which could spur the Bank of England (BoE) cut expectations for the August meeting and bring in the topsellers near the 1.30 psychological mark against the US dollar.

On the earnings front, the first big US bank earnings were mixed on Friday. JP Morgan fell 1.21% despite reporting a record profit after a surge in dealmaking boosted investment fees by 50%. Yet expenses exceeded expectations and net interest income came below estimates. Citigroup fell 1.81%. As JPM, Citi benefit from increased investment banking revenue – that jumped 60% at Citi – but expenses didn’t please investors. While Wells Fargo tanked 6% despite better-than-expected earnings and revenue because net interest income, there, fell 9% as customers preferred higher yielding products.

Today, Goldman Sachs and Balckrock are due to report earnings, tomorrow: Morgan Stanley, Thursday: Netflix and TSM and on Friday: American Express.

All I know is that earnings, especially the Big Tech earnings, would better meet and beat expectations for the rally in major US indices to continue. Otherwise, even the Fed cut bets may not prevent a meaningful downside correction.

China announces disappointing GDP as communist party kicks off important meeting

In China, the week starts with bad news. The Q2 GDP growth dived below 5% to 4.7% level, retail sales grew slower than expected and the slump in house prices accelerated. The communist party will hold a once-in-five-years meeting to address the issues and could come with some measures to help give investors some hope – especially measures to stop bleeding in the crumbling property market and measures to further boost production to make up for the feeble consumer spending,. It’s certainly why the CSI 300 is better bid this morning, while US crude opens the week under pressure, as copper futures hardly find buyers to test the 50-DMA to the upside on fear that the sluggish Chinese growth will keep the global demand prospects under a certain downside pressure.

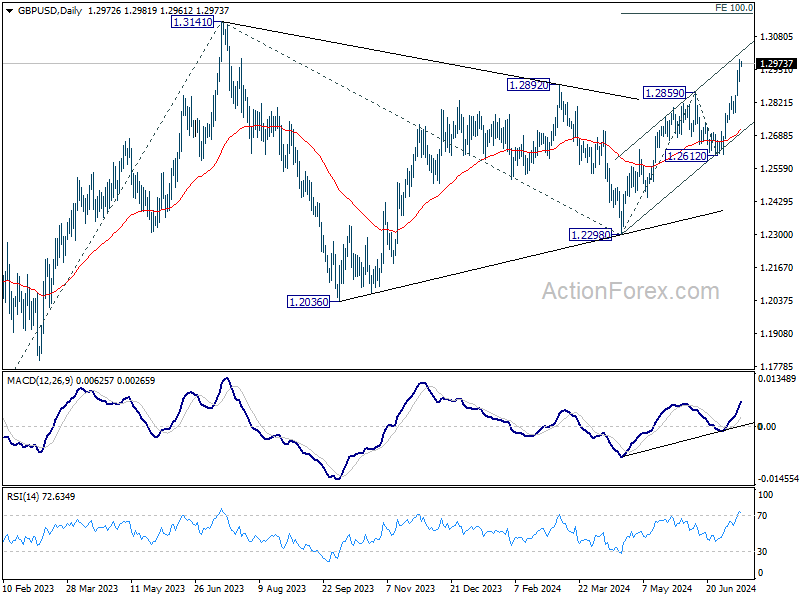

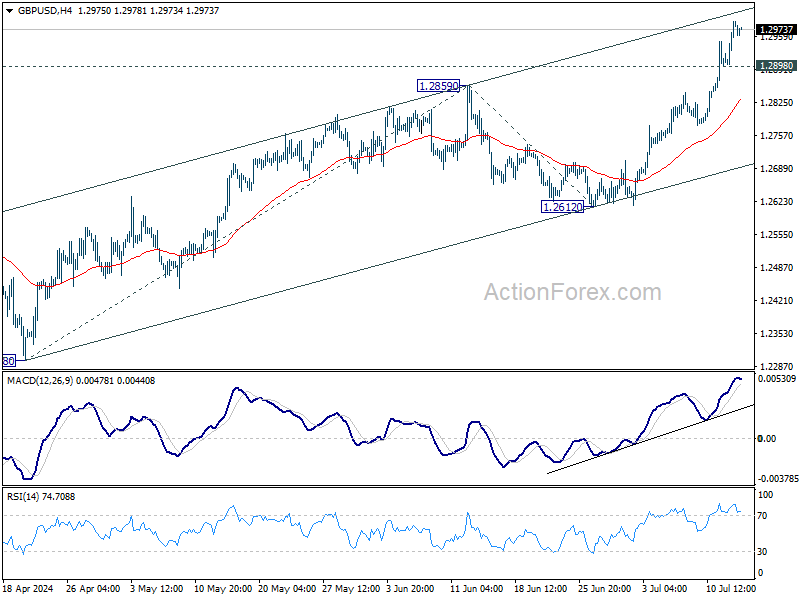

GBP/USD Daily Outlook

Daily Pivots: (S1) 1.2930; (P) 1.2960; (R1) 1.3019; More...

Intraday bias in GBP/USD remains on the upside despite current retreat. Rise fro 1.2298 is in progress for 100% projection of 1.2298 to 1.2859 from 1.2612 at 1.3173, which is slightly above 1.3141 key medium term resistance. On the downside, below 1.2898 minor support will turn bias neutral and bring consolidations first, before staging another rally.

In the bigger picture, corrective pattern from 1.3141 medium term top (2023 high) could have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 from 1.2298 at 1.4022.