Sample Category Title

ECB Preview – Holiday Season

The ECB meeting next week is expected to be largely a stock taking meeting and not a place to send new policy signals. The meeting by meeting and data dependent approach is clear and Lagarde has highlighted that the profit, wages and productivity data will be key, albeit those data points will only come from the middle of August and thus the focus turns to the September meeting.

Comments from ECB's GC point to a 'reasonable' market pricing and thus we do not expect that the ECB will want to send signals to alter the market pricing of monetary policy restrictiveness in the months and quarters to come.

June CPI: September Rate Cut Incoming

Summary

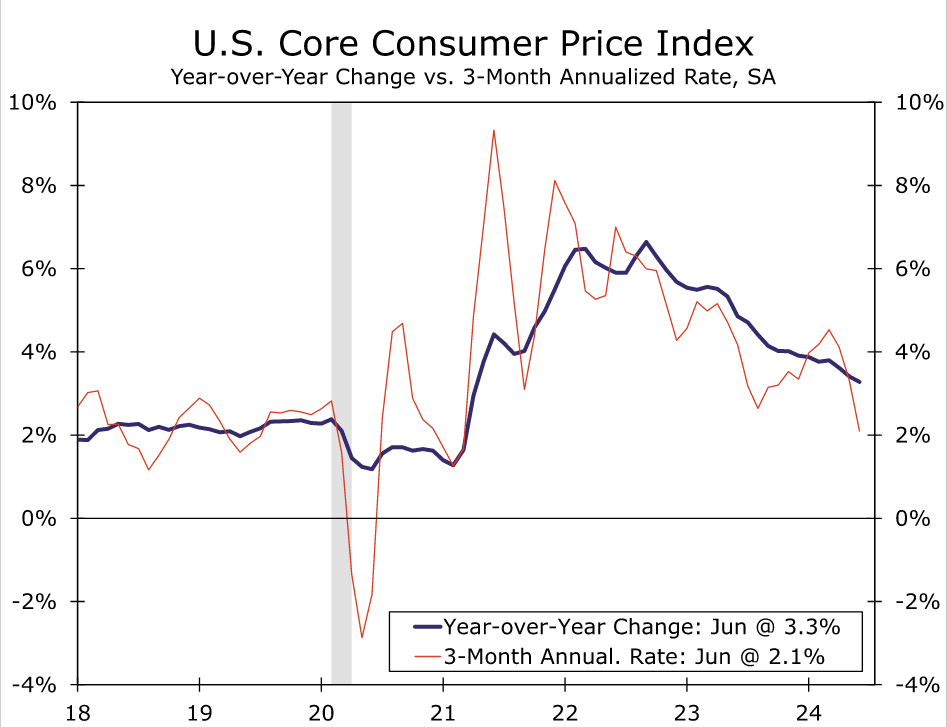

This morning's CPI report was arguably the most encouraging one the FOMC has received since it began its inflation fight nearly two and a half years ago. Consumer prices declined by 0.1%, led lower by a drop in energy prices and a modest increase in food prices. Excluding food and energy, the core CPI increased by just 0.1% (0.06% unrounded), which was the smallest increase since January 2021, a time when high inflation was far from most minds. The slowdown in core CPI inflation was broad-based, with core goods prices once again declining and core services inflation advancing only 0.1% compared to the previous six-month average gain of 0.4%. A leg down in shelter inflation was a key contributor, but drops in more discretionary spending categories like airfares (-5%), lodging away from home (-2%) and recreation services (-0.1%) also played a role in the softer reading.

On balance, the economic data are the most supportive of a rate cut that they have been all year. Over the past three months, the core CPI has increased at a 2.1% annualized pace. This marks the smallest three-month change in core prices since March 2021. Furthermore, it is not just the inflation data that have shown signs of cooling in recent months. A deceleration in employment and a rise in the unemployment rate are just a couple of the numerous indicators that are pointing to less heat in the U.S. labor market. Chair Powell nodded to these trends in public comments this week, saying that "elevated inflation is not the only risk we face." A rate cut as soon as the July 31 FOMC meeting is unlikely, but we remain of the view that the FOMC will cut the federal funds rate by 25 bps at its September meeting and reduce the fed funds rate by another 25 bps in December.

A Cool CPI Reading to Kick Off Summer

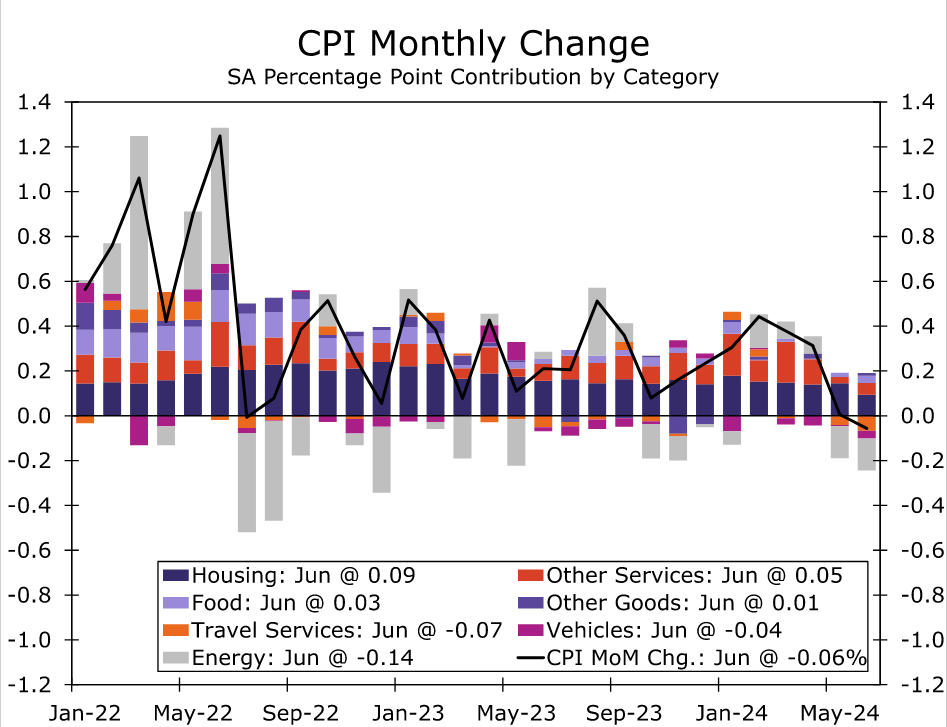

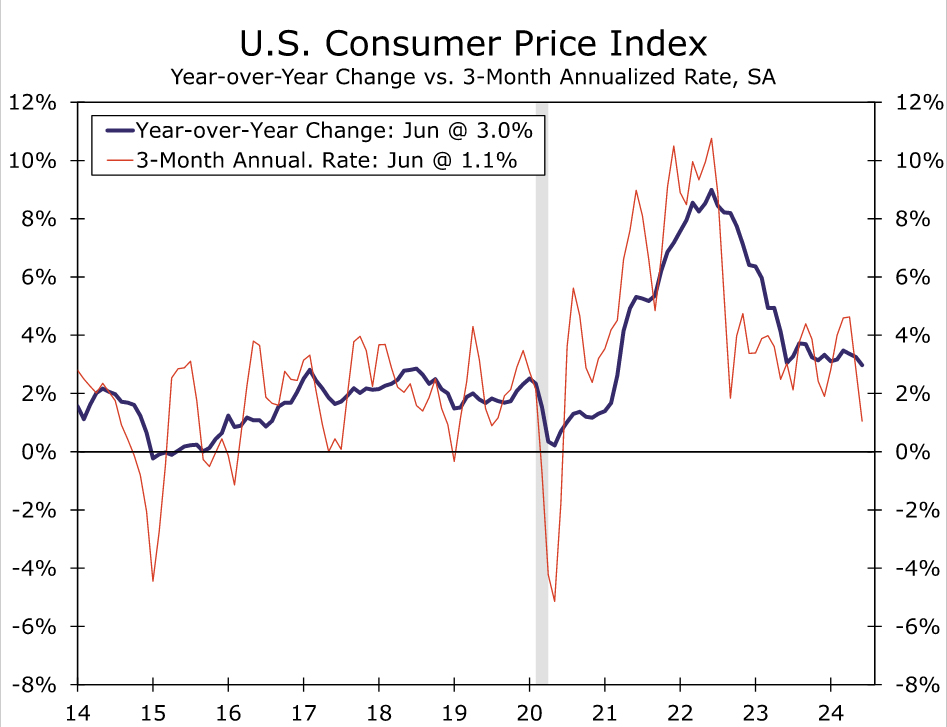

Consumer prices declined 0.1% in June, a surprisingly soft reading relative to consensus expectations for a gain of 0.1%. This was the first outright decline in the headline CPI since the spring of 2020 when the U.S. economy was in the throes of the COVID pandemic. Falling prices for gasoline (-3.8%) and electricity (-0.7%) helped offset a 2.4% rise in utility gas service, bringing overall energy prices down by 2% for the second consecutive month. Food inflation strengthened slightly in June compared to May, but the 0.2% increase in the month was well within the range of outcomes that was common pre-pandemic. Energy deflation and relatively restrained food price increases helped reduce the year-over-year change in the headline CPI from 3.3% in May to 3.0% in June (chart).

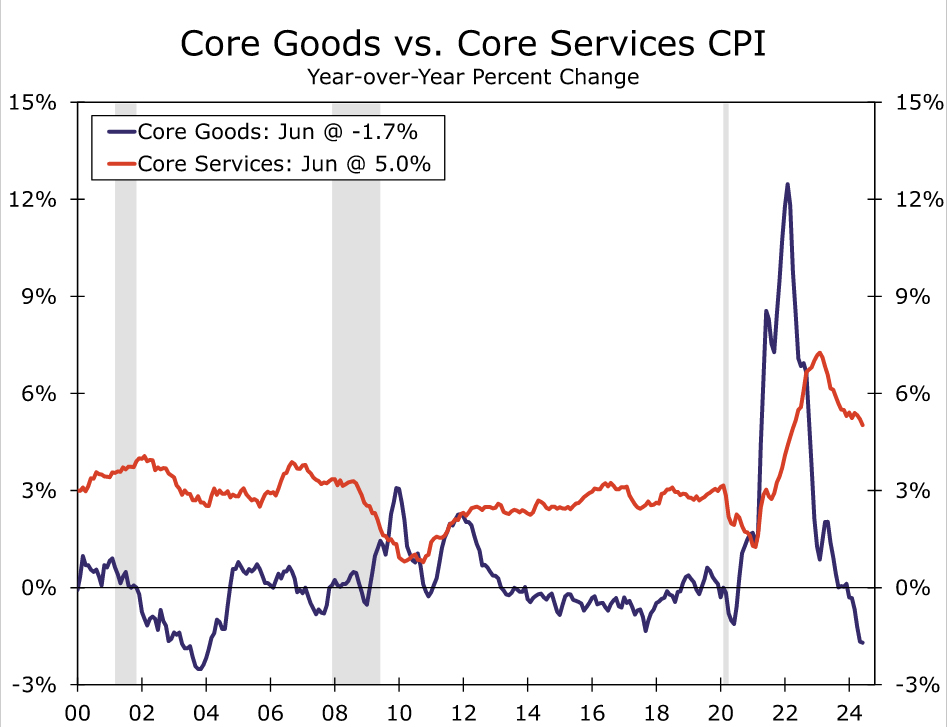

Fading price pressures across the economy were evident in the core index. Excluding food and energy, prices rose 0.1% (0.06% before rounding), which was the smallest increase since January 2021 and well below consensus expectations for a 0.2% increase. The softening was broad based, with goods prices once again falling and services rising just 0.1%.

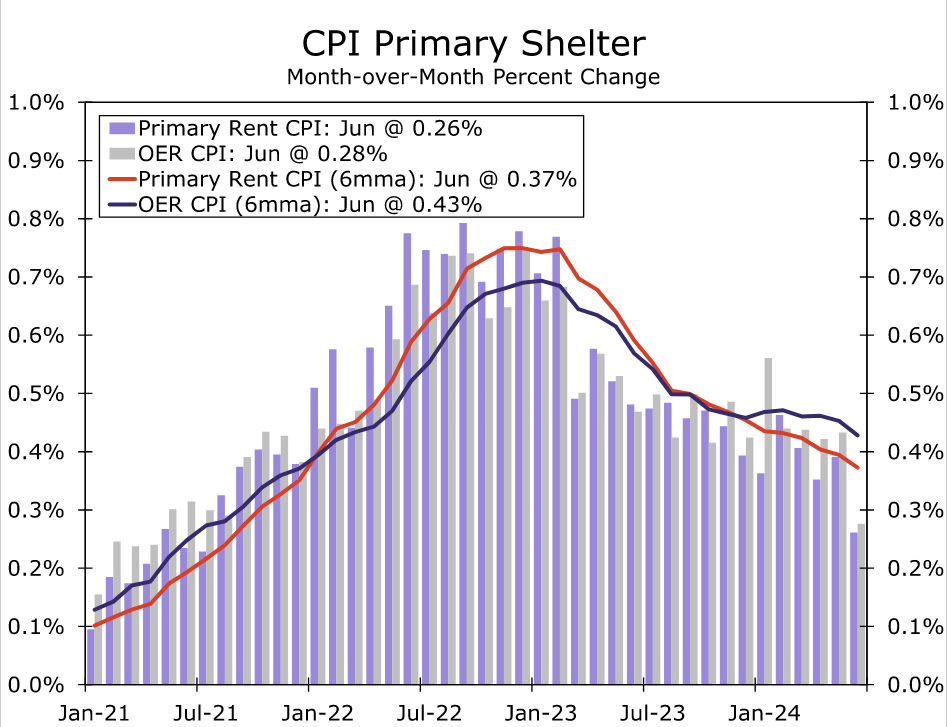

The shelter-disinflation-faithful were rewarded with owners' equivalent rent rising just 0.28% and rent of primary residences also lurching lower to see the smallest increases since 2021 (chart). Forward-looking "spot" measures of rent from the private sector as well as the BLS's New Tenant Rent Index suggest the monthly pace of shelter inflation can remain in the 0.25%-0.35% range through year-end. The slowdown in core services inflation extended beyond shelter. The squeeze on discretionary spending was clear in further price declines in lodging away from home, airfares and recreation services. Medical care services posted only a modest gain, while the muted rebound in motor vehicle insurance after last month's abrupt decline further points to the weaker pricing environment for vehicles and parts finally feeding into related services. To that end, June's drop in core goods was fueled by additional declines in used and new vehicle prices, while remaining core goods prices firmed slightly.

The case for a rate cut in September from the FOMC continues to build. Disinflation has broadened with goods no longer the sole driver of slower price growth (chart). The core CPI has increased at a 2.1% annualized rate over the past three months. This marks the smallest three-month change in core prices since March 2021. We will know more about the outlook for the June reading of the PCE deflator, the Fed's preferred inflation measure due at the end of the month, after tomorrow's release of the Producer Price Index. That said, our current expectation is that core PCE increased 0.1% in June, pushing the three-month annualized rate to 1.9%, under the Fed's target.

The case to start cutting rates extends beyond just the recent run of softer inflation data. Nonfarm payrolls grew by 176K per month over the three months ending in June, the slowest three-month pace of job growth since January 2021. Employment growth has been carried by less cyclically-sensitive industries such as government and healthcare, a trend we covered in a recent special report. The unemployment rate is above its pre-pandemic low and its 2019 average, while the share of workers quitting their jobs, the level of temporary help workers and business hiring plans all remain below their pre-COVID marks. Chair Powell nodded to these trends in public comments this week, saying that "elevated inflation is not the only risk we face." We remain of the view that the FOMC will cut the federal funds rate by 25 bps at its September meeting and reduce the fed funds rate by another 25 bps in December.

EUR/GBP Technical: Make the Pound Great Again

- EUR/GBP has resumed its downward trajectory since the start of the year, now trading close to a 2-year low at 0.8320.

- Unfavourable political environment in France versus a newly formed Labour-led UK government that favours pro-growth policies may see further underperformance of the Euro against the Pound.

- EUR/GBP continues to oscillate within a short-term downtrend phase with key resistance at 0.8500.

Since our last publication, the price actions of the EUR/GBP have inched lower below the prior 0.8540 key short-term pivotal resistance and hit the 0.8440 short-term support as highlighted in our report.

The EUR/GBP cross pair continued to drift lower to print a recent intraday low of 0.8397 on 14 June before it traded sideways and inched lower ex-post UK general election and the second round of the French legislation election.

The Euro has started to lose its shine against the Pound

Fig 1: EUR/GBP major trend as of 11 Jul 2024 (Source: TradingView, click to enlarge chart)

After the outcome of the Brexit referendum held on 23 June 2016, the EUR/GBP cross pair gained by 25% in the next four years and rocketed to a high of 0.9500 in March 2020 on the onset of the Covid-19 pandemic.

One of the key primary drivers of the underperformance of the GBP against the EUR during the period from 2016 to 2020 has been the negotiation process of Brexit which was both politically challenging and deeply divisive within the UK that led to two snap elections in 2017 and 2019.

Another episode of GBP’s significant underperformance was from August 2022 to September 2022 under the premiership of former UK Conservative Party Prime Minster Liz Truss sparked a mini-crisis in the Glit market due to the proposed unfunded mini-budget where EUR/GBP spiked by 10% within a month to print a high of 0.9278 on 22 September 2022.

Since the start of the year, the EUR/GBP has traded lower below its 200-day moving average (see Fig 1), and it is now hovering at close to a 2-year low of 0.8420 at this time of the writing.

Unfavourable political environment in France with a lack of pro-growth initiatives may see a shift towards UK financial assets

A change in the political climate in the UK and EU seems to be the driving force again; the newly formed UK government under the Labour Party has advocated growth policies via public-private partnerships that in turn lower the chances of a tax hike or cut fiscal spending to balance the budget books; a shift away from its traditional socialist roots.

On the flip side, the political climate of France is now in limbo as the second round of the French legislation election has led to a hung parliament with the far-left socialist alliance New Popular Front managed to take the top spot from the initial leading far-right National Rally but without a clear absolute majority to push for its aggressive fiscal spending policies coupled with higher taxes on businesses and wealthy people.

However, it will still be a challenge for French President Macron’s centrist alliance which has taken the second position in the French parliament to push out pro-growth policies and allow the current 5% budget deficit to shrink towards the 3% limit set up by the EU standard due to loggerheads with the far left.

Therefore, a lack of new growth fiscal initiatives from France, one of the economic growth engine pillars in the EU is likely to dampen the prospects of the Eurozone financial assets in favour of UK assets that also have a lower valuation.

Watch the 0.8500 key short-term resistance on EUR/GBP

Fig 2: EUR/GBP short-term trend as of 11 Jul 2024 (Source: TradingView, click to enlarge chart)

In the lens of technical analysis, the EUR/GBP has continued to trade within a short-term downtrend phase as price actions continue to oscillate within a minor descending channel since the 23 April 2024 high of 0.8645 and below its 20-day moving average (see Fig 2).

If the 0.8500 short-term pivotal resistance (also confluences with the downward slopping 50-day moving average) is not surpassed to the upside, the EUR/GBP may see a break below its recent14 June minor low area of 0.8400 for a further potential impulsive bearish down move to expose the next near-term support at 0.8345 (also the lower boundary of the minor descending channel) in the first step.

However, a clearance above 0.8500 negates the bearish tone for a minor squeeze up to see the next intermediate resistances coming in at 0.8530 and 0.8580 (also the key 200-day moving average).

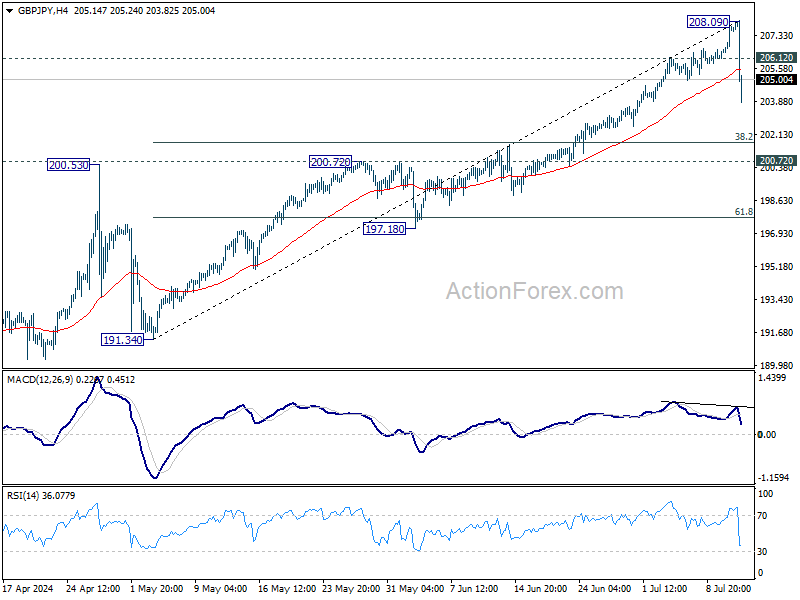

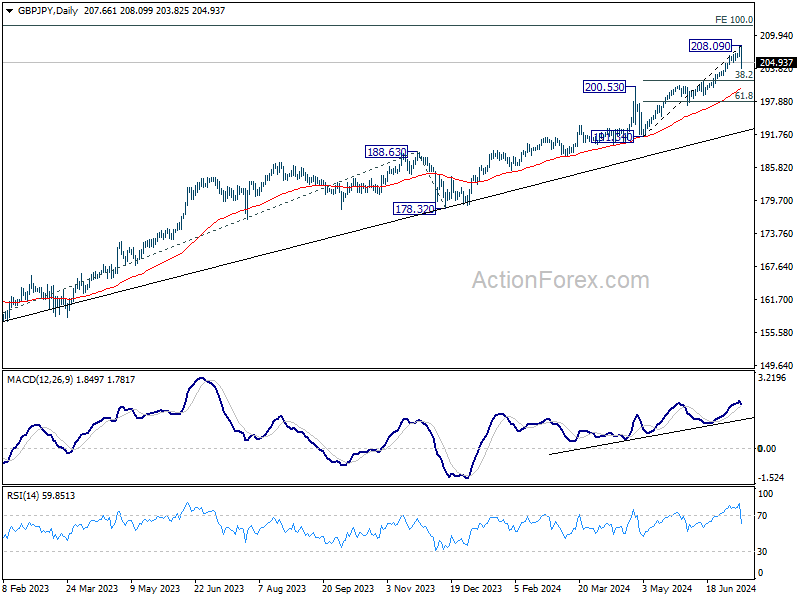

GBP/JPY Mid-Day Outlook

Daily Pivots: (S1) 206.68; (P) 207.25; (R1) 208.34; More...

GBP/JPY's steep decline and strong break of 206.12 support suggest that a short term top is formed at 208.09, on bearish divergence condition in 4H MACD. While deeper decline cannot be ruled out, downside should be contained by 38.2% retracement of 191.34 to 208.09 at 201.69 to bring rebound, and set the range of consolidations below 208.09.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62. Outlook will stay bullish as long as 200.72 resistance turned support holds, even in case of deep pullback.

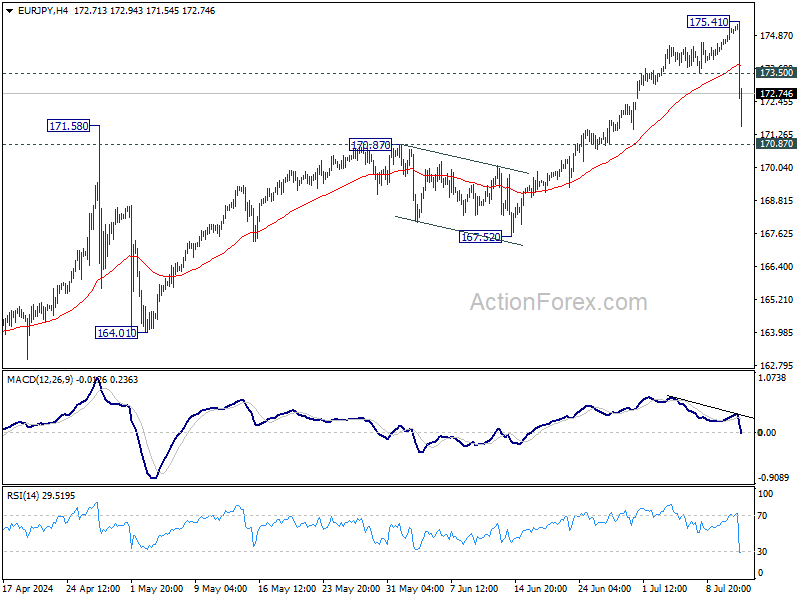

EUR/JPY Mid-Day Outlook

Daily Pivots: (S1) 174.50; (P) 174.83; (R1) 175.45; More...

EUR/JPY's strong break of 173.50 support suggests that a short term top was formed at 175.41, on bearish divergence condition in 4H MACD. But there is no clear sign of trend reversal yet. While deeper pullback cannot be ruled out, downside could be contained by 170.87 resistance turned support to bring rebound to set the range for near term consolidations below 175.41. Nevertheless, firm break of 170.87 will argue that larger correction is already underway.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 139.05 to 164.29 from 153.15 at 178.38. For now outlook will stay bullish as long as 170.87 resistance turned support holds, even in case of deep pullback. However, firm break of 170.87 will bring deeper fall to 167.52 support. Decisive break there will confirm that larger correction in in progress for 153.15/164.29 support zone.

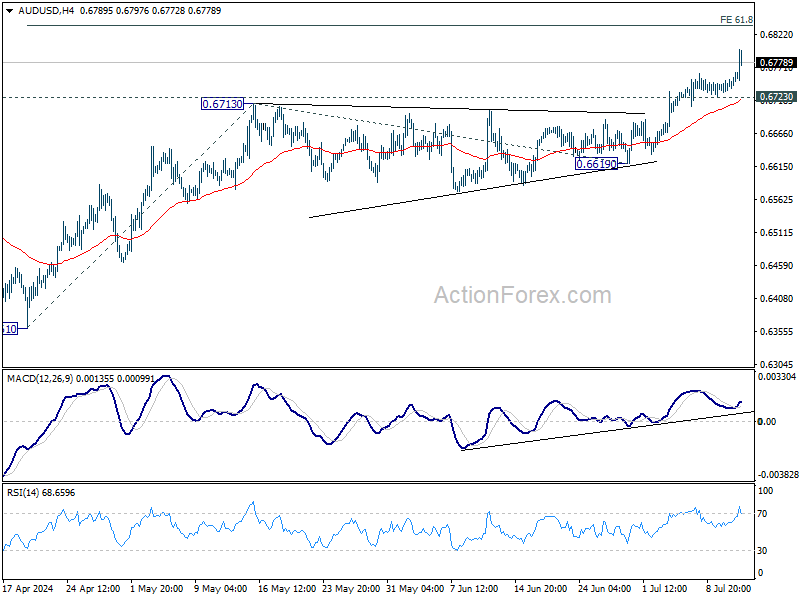

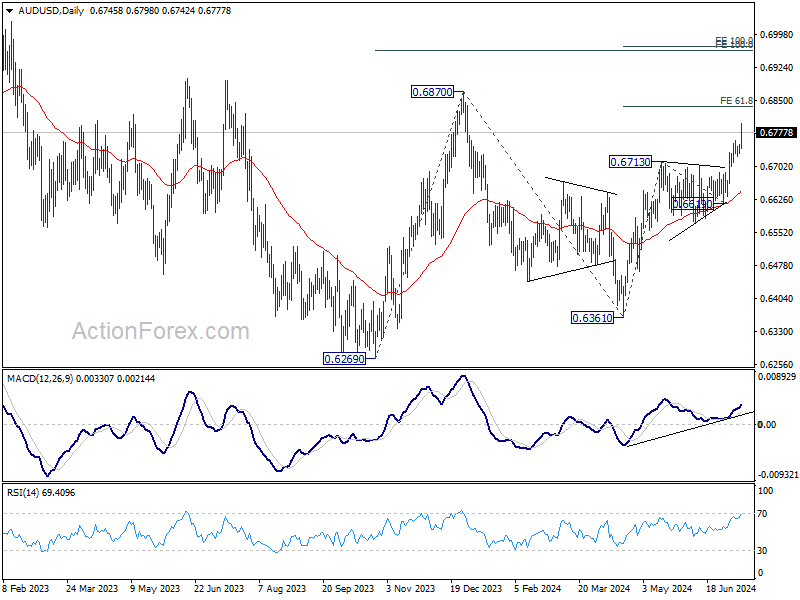

AUD/USD Mid-Day Report

Daily Pivots: (S1) 0.6735; (P) 0.6744; (R1) 0.6755; More...

Intraday bias in AUD/USD remains on the upside as current rally continues to 61.8% projection of 0.6361 to 0.6713 from 0.6619 at 0.6837. Decisive break there could prompt upside acceleration through 0.6870 resistance to 100% projection at 0.6971. For now, risk will stay on the upside as long as 0.6723 minor support holds, in case of retreat.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg. Break of 0.6870 will target 100% projection of 0.6269 to 0.6870 from 0.6361 at 0.6962.

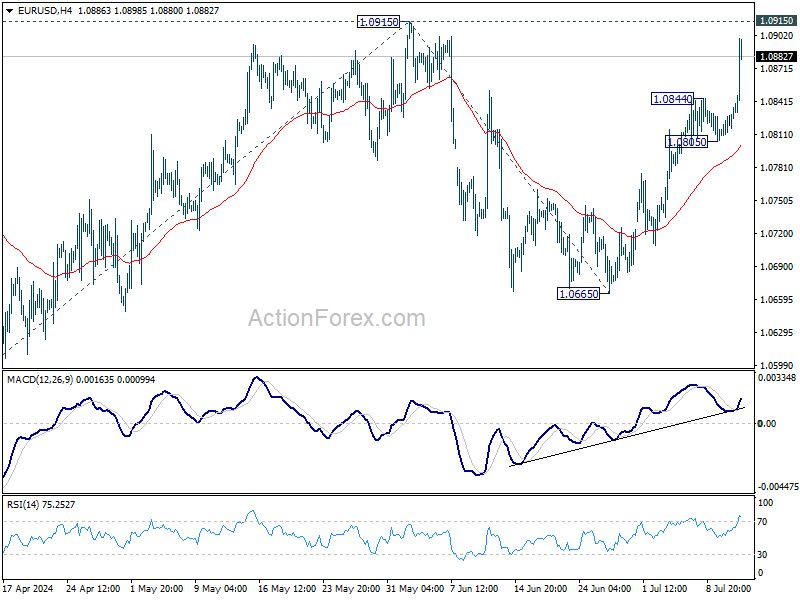

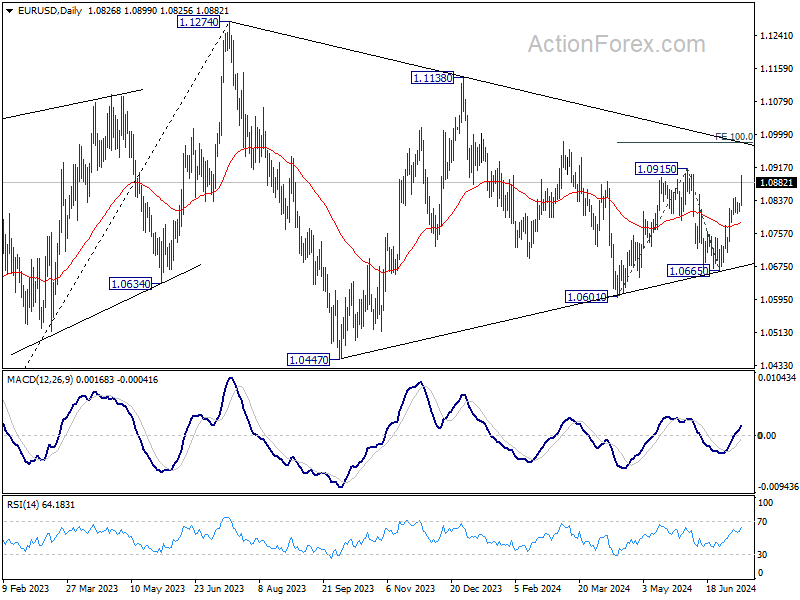

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0817; (P) 1.0824; (R1) 1.0838; More....

EUR/USD's rise from 1.0665 resumed by breaking through 1.0844 temporary top and intraday bias is back on the upside for 1.0915 resistance. Firm break there will resume whole rally from 1.0601 and target 100% projection of 1.0601 to 1.0915 from 1.0665 at 1.0919 next. For now, risk will stay on the upside as long as 1.0805 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that could still be in progress. Break of 1.0601 will target 1.0447 support and possibly below. On the upside, firm break of 1.0915 resistance will start another rising leg back to 1.1138 resistance instead.

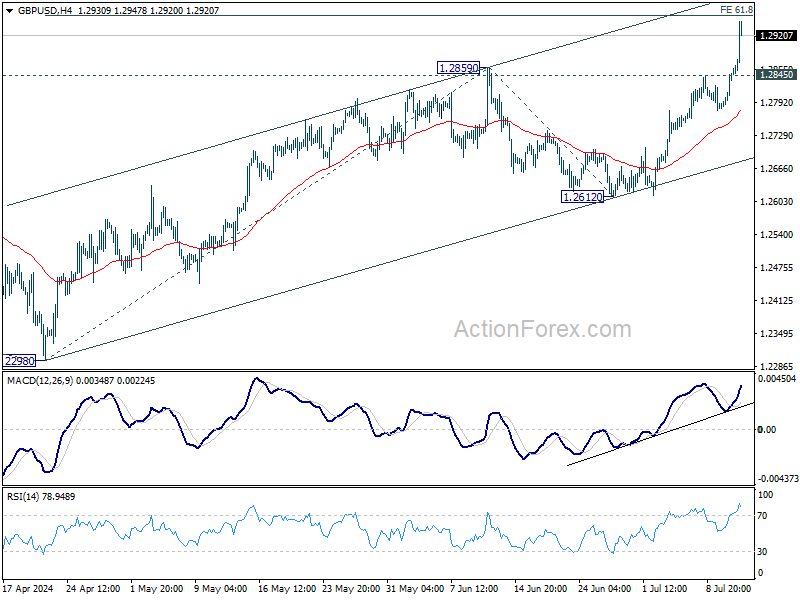

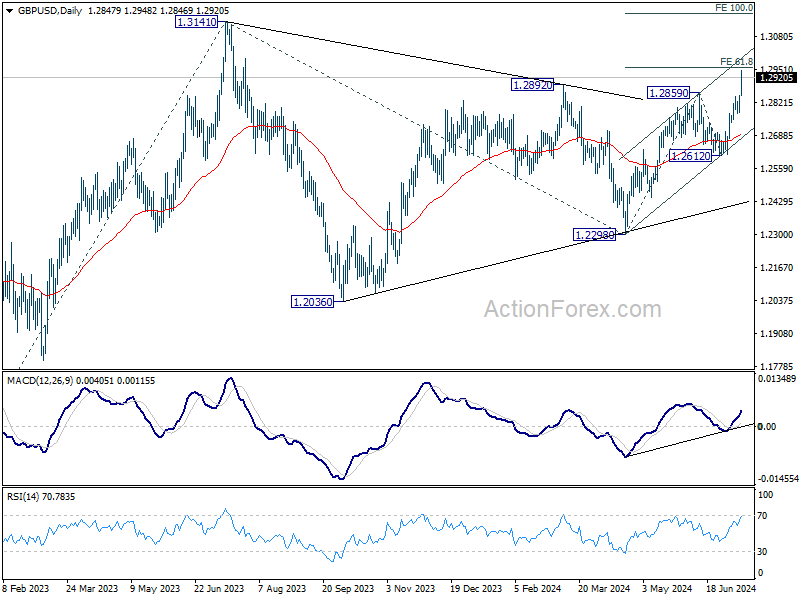

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2800; (P) 1.2825; (R1) 1.2872; More...

GBP/USD's rally continues today and intraday bias stays on the upside for 61.8% projection of 1.2298 to 1.2859 from 1.2612 at 1.2959. Decisive break there would prompt upside acceleration through 1.3141 to 100% projection at 1.3173. On the downside, below 1.2845 resistance turned support will turn intraday bias neutral first.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern which might have completed with three waves to 1.2298 already. This will now remain the favored case as long as 1.2612 support holds. Firm break of 1.3141 will target 61.8% projection of 1.0351 (2022 low) to 1.3141 (2023 high) from 1.2298 at 1.4022.

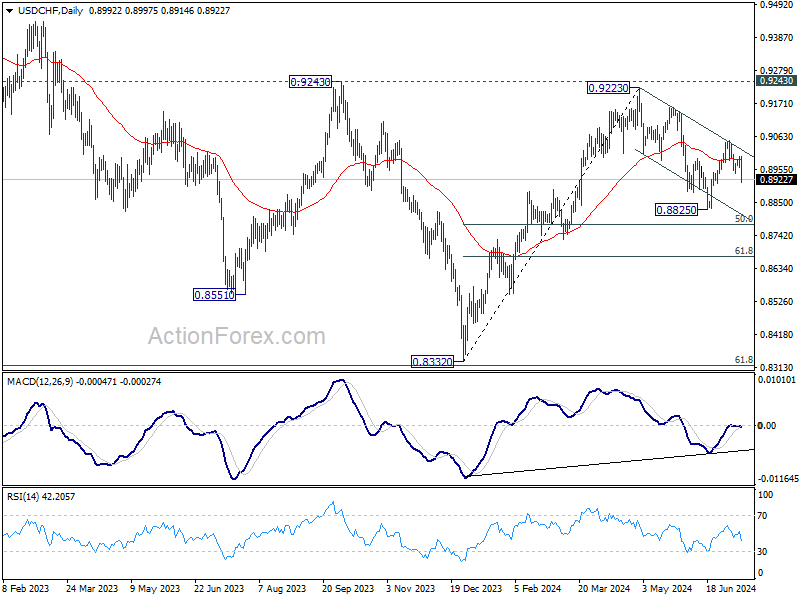

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8973; (P) 0.8987; (R1) 0.9011; More…

USD/CHF's decline from 0.9049 resumed by breaking through 0.8942 support and intraday bias remains is back on the downside for retesting 0.8825. Fall from 0.9223 should be in progress with near term channel intact. Break of 0.8825 will target 50% retracement of 0.8332 to 0.9223 at 0.8778 next. For now, risk will stay on the downside as long as 0.9000 resistance holds, in case of recovery.

In the bigger picture, focus remains on 0.9223/9243 resistance zone. Decisive break there would suggest larger bullish trend reversal and turn outlook bullish. Nevertheless, rejection by 0.9223/43 will keep medium term outlook neutral at best, for more range trading between 0.8332/9243 first.