Sample Category Title

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8971; (P) 0.8990; (R1) 0.9007; More…

Intraday bias in USD/CHF remains on the upside at this point, for channel resistance (now at 0.9034). Fall from 0.9223 might have completed as a three-wave corrective move to 0.8825. Firm break of channel resistance will target 0.9157 resistance next. On the downside, below 0.8956 minor support will turn intraday bias neutral gain first.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside breakout is mildly in favor at a later stage.

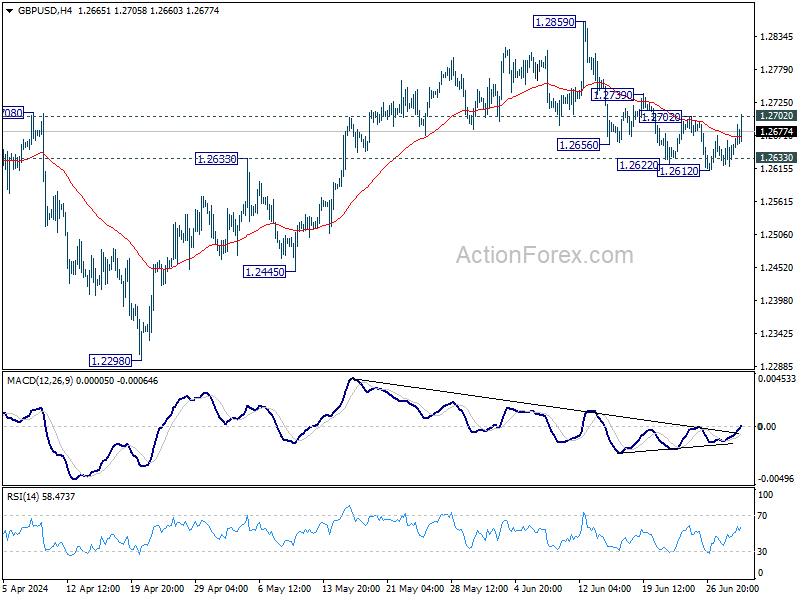

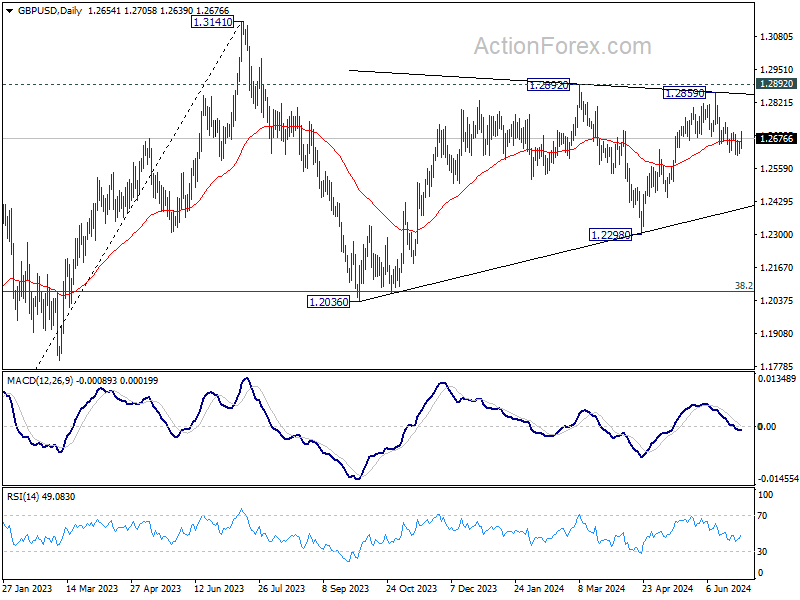

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2623; (P) 1.2642; (R1) 1.2665; More...

Intraday bias in GBP/USD remains neutral at this point. On the upside, firm break of 1.2702 resistance will argue that pull back from 1.2859 has completed, and bring retest of this high instead. Nevertheless, rejection by 1.2702 will keep risk on the downside. Sustained trading below 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.

Gold Price Update: XAU/USD Rises as Search for Catalyst Rumbles On

- Gold rises as a weaker US Dollar and uncertainty around monetary policy continues.

- ISM data later today before all attention turns to US jobs data later in the week.

- Trendline break and price action hint at at a potential rise toward the $2370 resistance handle.

Market participants are closely watching for a new catalyst to drive gold prices in a definitive direction. After experiencing gains of up to 13% in the first half of the year and reaching a record high near $2440 per ounce, there is growing concern among market participants about the potential for a significant pullback in the price of the precious metal.

The geopolitical context which added to gold appeal in the first half of 2024 is yet to be resolved, but has quieted down of late. The chance of a wider war in the Middle East remains and for now this could continue to provide a modicum of support for gold prices.

The constant back and forth on the rate path from the US Federal Reserve is set to continue. The Fed have trimmed down their expectations to one rate cut in 2024, but market participants continue to price in three, starting in September 2024. Lower rates would appeal to gold bulls as the lower yield and weaker US dollar could facilitate a push to fresh highs…. In short an interesting quarter ahead that is packed with potential outcomes. Once more, a shorter-term outlook may prove more beneficial in the constantly changing landscape of monetary policy.

US PMI, NFP Data and Independence Day Holiday

There are a host of market moving events ahead this week. The most pertinent for the US dollar and gold prices will be the NFP and unemployment report due on Friday. This could significantly impact the rate cut expectations and thus lead to significant volatility around Gold prices.

Later today however, eyes will be focused on S&P and ISm manufacturing data from the US.Once again traders will be focused on the overall health of the US economy as well as order numbers. This would provide valuable insight into spending and an idea of how well the US consumer is coping with higher rates. A robust number later today is likely to inject some strength into the US dollar while a miss will likely benefit gold and weigh on the US dollar.

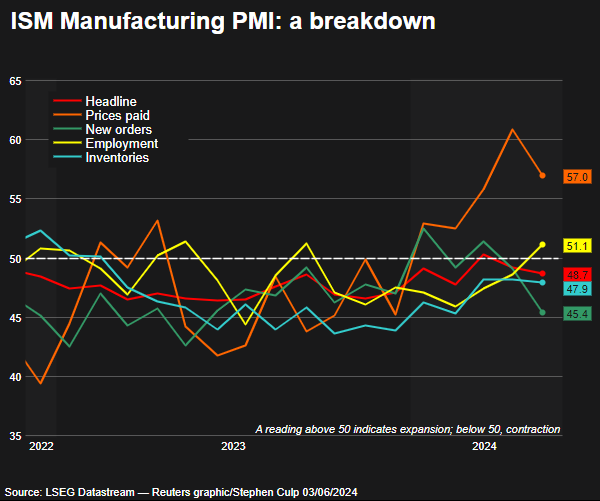

The previous ISM print recorded a significant drop off in new orders which is a slight concern and something market participants will be keeping a watch on. The chart below provides a visual representation of all the key data points around the ISM and S&P manufacturing data.

Source: LSEG (click to enlarge)

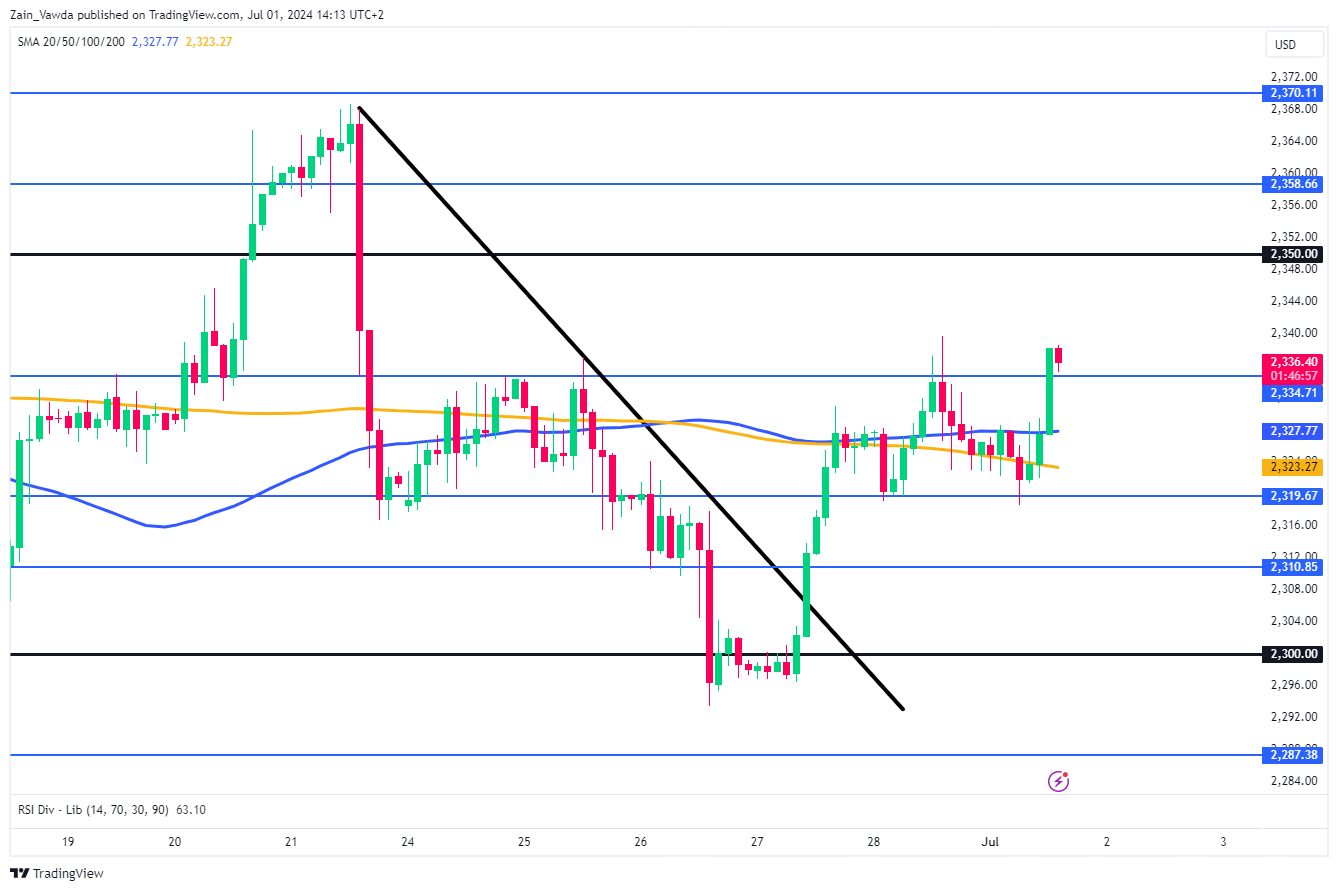

Technical Analysis on Gold (XAU/USD)

Gold put in a stellar recovery on Thursday and Friday last week, following a brief stint below $2300 (discussed in last week’s Gold article). The brief dip was met with significant buying pressure and some mixed US data which saw the precious metal break back above the key $2320 resistance handle.

The $2320 resistance break was preceded by a trendline break on the H2 timeframe which added another layer of confluence. The rally gathered pace and looks set to close above the $2334 resistance handle which opens up a potential retest of the $2350 psychological level.

Alternatively a rejection at $2334 could see the price filter back toward the $2320 mark which held firm this morning. A break of $2320 and the $2300 handle comes into focus before last week’s lows around $2293.

Gold (XAU/USD) H2 Chart, July 1, 2024

Source: TradingView.com (click to enlarge)

Key Levels to Keep an Eye on:

Support

- 2334

- 2320

- 2310

Resistance

- 2340 (last weeks high)

- 2350

- 2358

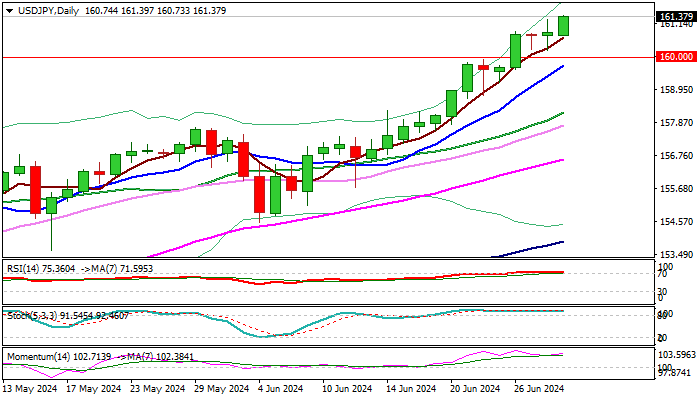

USD/JPY Outlook: Hits New Multi-Decade High Despite Persisting Intervention Threats

USDJPY rose further on Monday, signaling continuation after bulls paused for consolidation on Thu/Fri.

Although traders remain cautious over looming intervention, after Japanese authorities reiterated their stance of intervening again to support weakening yen, bulls hold grip for now.

Fresh strength hit new highest level since Oct 1986 and on track for daily close above 161 level, which would add to bullish stance, boosted by strong monthly gains in June.

Bulls eye targets at 162.00/16 (round-figure / FE 123.6% of the upleg from 151.85 higher low) and may extend towards 163.38 (FE 138.2%) however, strongly overbought daily studies and intervention talks will continue to keep traders alerted.

Immediate supports lay at 161.00 and 160.19/00, followed by pivot at 159.50 (daily Tenkan-sen).

Res: 162.00; 162.16; 163.38; 164.00.

Sup: 161.00; 160.19; 160.00; 159.50.

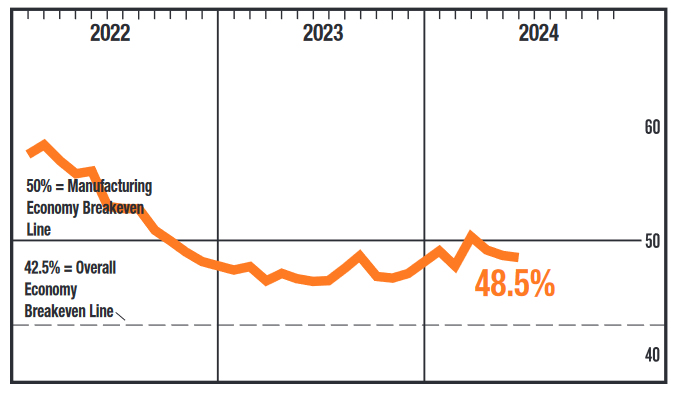

US ISM manufacturing falls to 48.5, prices down to 52.1

US ISM Manufacturing PMI fell from 48.7 to 48.5 in June, missed expectation of 49.3. That's the third month of contraction reading.

Looking at some details, new orders rose from 45.4 to 49.3. Production fell from 50.2 to 48.5. Employment fell from 51.1. to 49.3. Prices tumbled sharply from 57.0 to 52.1.

ISM said: "The past relationship between the Manufacturing PMI and the overall economy indicates that the June reading (48.5 percent) corresponds to a change of plus-1.7 percent in real gross domestic product (GDP) on an annualized basis."

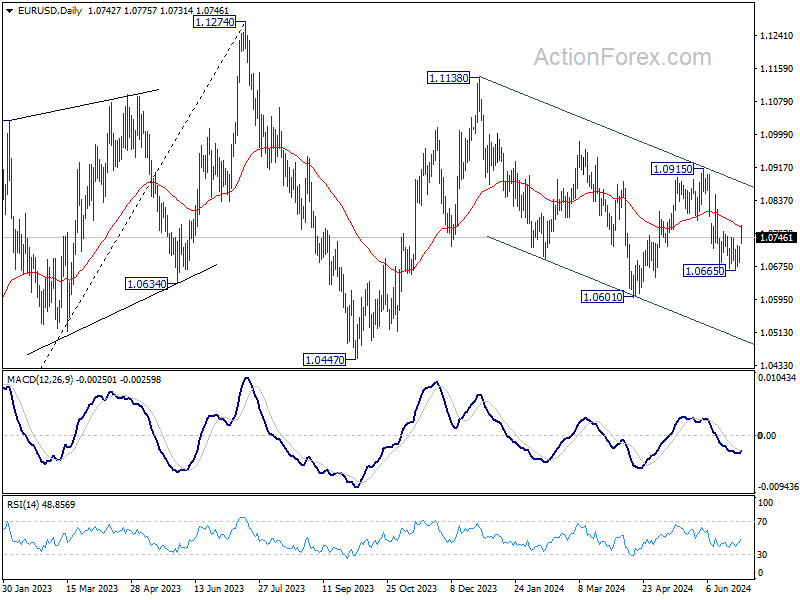

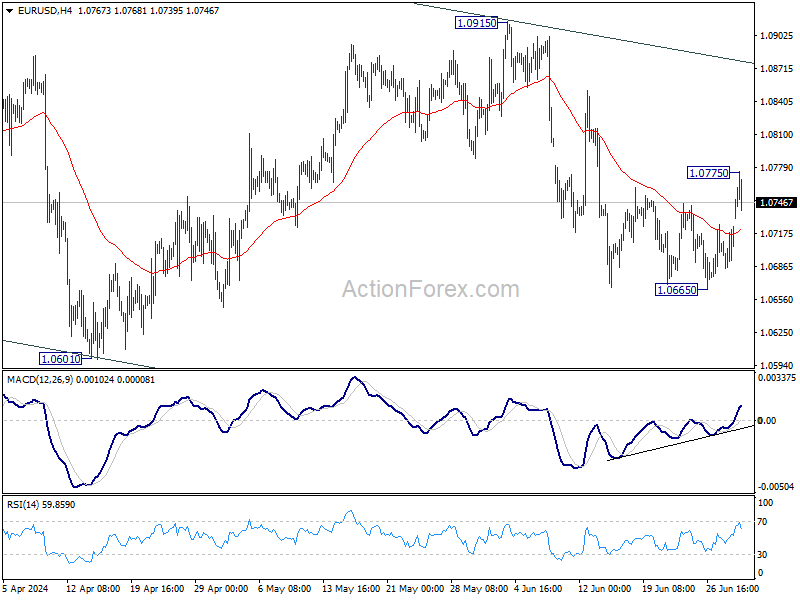

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0692; (P) 1.0708; (R1) 1.0731; More....

EUR/USD edged higher to 1.0775 earlier today but failed to break through 55 D EMA (now at 1.0773) and retreated. Intraday bias stays neutral first. On the upside, firm break of 55 D EMA will argue that pull back from 1.0915 has completed. Further rise should be seen back to 1.0915 resistance. However, break of 1.0665 will resume larger down trend through 1.0601 low instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly below . For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

Euro Rebound Stalls as Sterling and Dollar Mount a Comeback

Euro has seen a notable rebound as the new week commenced, though the lack of follow-through buying momentum is evident. The initial results from French parliamentary elections were not as dire as investors had feared. The far-right National Rally's victory was not as overwhelming as anticipated. However, significant uncertainty remains as political parties scramble to form a coalition to block the National Rally from gaining power.

Leaders of both the left-wing New Popular Front and President Macron's centrist alliance announced on Sunday night that they would withdraw their candidates in districts where another candidate stands a better chance of defeating the National Rally in the upcoming run-off on Sunday. Despite this strategic move, it remains unclear how such a coalition will be effectively implemented and whether it will succeed in preventing the far-right from gaining a foothold in the government.

Currently, Euro remains the strongest currency for the day, but the second-placed Sterling and third-placed Dollar are attempting to fight back. On the other hand, Swiss Franc is the weakest performer, followed by Yen and then Canadian Dollar. Aussie and Kiwi are positioned somewhere in the middle of the performance chart.

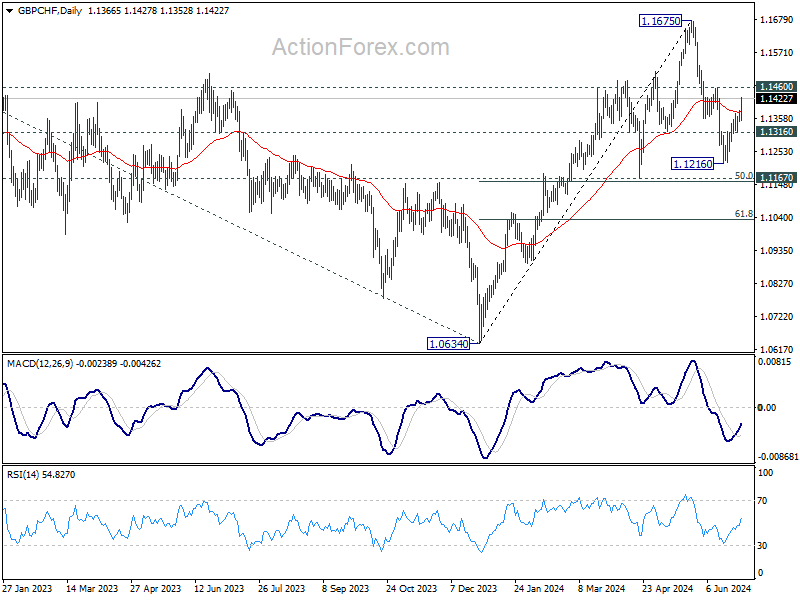

Technically, GBP/CHF's extended rebound suggests that corrective pullback from 1.1675 has completed at 1.1216, ahead of 1.1167 key support level. Further rise is now in favor as long as 1.1316 minor support holds. Break of 1.1460 resistance will pave the way back to retest 1.1675 high.

In Europe, at the time of writing, FTSE is up 0.36%. DAX is up 0.51%. CAC is up strongly by 1.58%. UK 10-year yield is up 0.0642 at 4.241. Germany 10-year yield is up 0.082 at 2.583. Earlier in Asia, Nikkei rose 0.12%. Hong Kong was on holiday. China Shanghai SSE rose 0.92%. Singapore Strait Times rose 0.17%. Japan 10-year JGB yield rose 0.160 to 1.064.

UK's PMI manufacturing finalized at 50.9, renewed cost pressures despite growth

UK's PMI Manufacturing was finalized at 50.9 in June, slightly down from May's 22-month high of 51.2. This marks a continued period of growth for the sector, but with some emerging concerns.

Rob Dobson, Director at S&P Global Market Intelligence, commented, "The UK manufacturing sector is enjoying its strongest spell of growth for over two years". Performance of the domestic market remains a "real positive." However, he noted the persistent challenges in export markets, with manufacturers struggling to secure new business in the US, China, and mainland Europe.

Despite the overall optimism for future growth, manufacturers are focusing heavily on cost minimization and cash flow protection. This cautious approach has resulted in further job losses, cuts to non-essential spending, and leaner stock holdings. The renewed cost inflation pressure is also a significant concern, with input prices rising at the fastest pace since early 2023.

This surge in manufacturing costs will likely heighten worries among hawkish policymakers at BoE regarding the persistence of underlying inflationary pressures.

Eurozone PMI manufacturing finalized at 45.8, recovery pushed to late summer

Eurozone manufacturing PMI for June was finalized at 45.8, down from May's 47.3, signaling continued contraction in the manufacturing sector. This decline indicates ongoing challenges for manufacturers, with only Italy showing some improvement among the member countries.

Country-specific data for June showed Greece at 54.0, Spain at 52.3, the Netherlands at 50.7, and Ireland at 47.4. Italy recorded a slight improvement at 45.7, while France was at 45.4, Austria at 43.6, and Germany at 43.5. All these figures reflect either multi-month lows that are insufficient to suggest a strong recovery.

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, highlighted that despite the decline in PMI indices across most Eurozone countries, the trend appears to be a "temporary blip" rather than a sign of a prolonged downturn. He pointed out that the global recovery provides a "supportive backdrop" for Eurozone manufacturers. Moreover, optimism about future production remains high, similar to levels seen in May, indicating sustained confidence among businesses for the upcoming year.

However, de la Rubia also noted a troubling trend in new orders, which are falling at an accelerated pace. This decline follows a record stretch of 25 consecutive months of falling demand. Despite a brief improvement in May, the June data suggests that any significant recovery will likely be "postponed" until at least the end of summer or early fall.

Japan's Tankan manufacturing improves but non-manufacturing may have peaked

BoJ's closely watched Tankan survey revealed that while manufacturing sector showed continued improvement, sentiment among non-manufacturers appeared to have peaked, which may complicate BoJ's considerations for another rate hike later this month.

The Tankan survey reported that large manufacturing index rose from 11 to 13, reaching its highest level since March 2022. Large manufacturing outlook also increased from 10 to 14. However, non-manufacturing index dipped slightly from 34 to 33, marking its first decline in 16 quarters, and non-manufacturing outlook remained unchanged at 27.

Long-term corporate inflation expectations edged up, with companies forecasting inflation to hit 2.3% in three years and 2.2% in five years. Despite these rising expectations, the mixed sentiment data do not strongly support another imminent rate hike by BoJ.

In a separate development, an unscheduled revision to historical data indicated that Japan's real GDP contracted at an annualized rate of -2.9% in January-March, a much steeper decline than the previously estimated -1.8% contraction. This significant revision is likely to impact BoJ's upcoming quarterly growth and price forecasts, which are due at the July 30-31 policy meeting.

Japan's PMI manufacturing finalized at 50, stagnation amid cost pressures and weak demand

Japan's PMI Manufacturing index for June was finalized at 50.0, slightly down from May's 50.4, indicating a stagnation in the sector. S&P Global highlighted a marginal increase in manufacturing production, but new orders continued to decline, albeit slightly. Employment in the sector expanded, with business confidence reaching a six-month high.

Pollyanna De Lima at S&P Global Market Intelligence stated, "Notably, the latest PMI data revealed the first rise in Japanese factory production for over a year, and a rebound in business confidence."

However, she also pointed out significant challenges, including heightened cost pressures due to Yen depreciation, which increased the price of imported materials. Labor costs also strained budgets.

"There was clear evidence that the sharp rise in overall purchasing prices was not caused by supply-chain issues, as delivery times improved to the greatest extent in over 15 years," she added.

Consequently, manufacturers raised their selling prices at the highest rate in over a year, a move seen as unfavorable given the weak domestic and external demand.

China's Caixin PMI manufacturing rises to 51.8, growth continues but optimism dips

China's Caixin PMI Manufacturing index edged up from 51.7 to 51.8 in June, surpassing expectations of 51.2 and marking its highest level since May 2021. This rise keeps the index in expansionary territory for the eighth consecutive month. Notably, output price inflation reached an eight-month high, reflecting increased activity in the sector.

Wang Zhe, Senior Economist at Caixin Insight Group, noted, "Overall, the manufacturing sector kept improving in June, with supply, domestic demand, and exports continuing to grow." He highlighted that manufacturers increased their purchases, resulting in higher inventory and price levels. Despite this positive trend, optimism among surveyed companies fell significantly, suggesting that market expectations need further strengthening.

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0692; (P) 1.0708; (R1) 1.0731; More....

EUR/USD edged higher to 1.0775 earlier today but failed to break through 55 D EMA (now at 1.0773) and retreated. Intraday bias stays neutral first. On the upside, firm break of 55 D EMA will argue that pull back from 1.0915 has completed. Further rise should be seen back to 1.0915 resistance. However, break of 1.0665 will resume larger down trend through 1.0601 low instead.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly below . For now, this will remain the favored case as long as 1.0915 resistance holds, in case of rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Tankan Large Manufacturing Index Q2 | 13 | 11 | 11 | |

| 23:50 | JPY | Tankan Large Manufacturing Outlook Q2 | 14 | 10 | ||

| 23:50 | JPY | Tankan Non - Manufacturing Index Q2 | 33 | 33 | 34 | |

| 23:50 | JPY | Tankan Non - Manufacturing Outlook Q2 | 27 | 27 | ||

| 23:50 | JPY | Tankan Large All Industry Capex Q2 | 11.10% | 4% | ||

| 00:30 | JPY | Manufacturing PMI Jun F | 50 | 50.1 | 50.1 | |

| 01:45 | CNY | Caixin Manufacturing PMI Jun | 51.8 | 51.2 | 51.7 | |

| 05:00 | JPY | Consumer Confidence Jun | 36.4 | 36.5 | 36.2 | |

| 06:30 | CHF | Real Retail Sales Y/Y May | 0.40% | 2.50% | 2.70% | 2.20% |

| 07:30 | CHF | Manufacturing PMI Jun | 43.9 | 44.9 | 46.4 | |

| 07:45 | EUR | Italy Manufacturing PMI Jun | 45.7 | 44.5 | 45.6 | |

| 07:50 | EUR | France Manufacturing PMI Jun F | 45.4 | 45.3 | 45.3 | |

| 07:55 | EUR | Germany Manufacturing PMI Jun F | 43.5 | 43.4 | 43.4 | |

| 08:00 | EUR | Eurozone Manufacturing PMI Jun F | 45.8 | 45.6 | 45.6 | |

| 08:30 | GBP | Manufacturing PMI Jun F | 50.9 | 51.4 | 51.4 | |

| 08:30 | GBP | M4 Money Supply M/M May | -0.10% | 0.20% | 0.10% | 0.00% |

| 08:30 | GBP | Mortgage Approvals May | 60K | 61K | 61K | |

| 12:00 | EUR | Germany CPI M/M Jun P | 0.10% | 0.20% | 0.10% | |

| 12:00 | EUR | Germany CPI Y/Y Jun P | 2.20% | 2.30% | 2.40% | |

| 13:45 | USD | Manufacturing PMI Jun F | 51.7 | 51.7 | ||

| 14:00 | USD | ISM Manufacturing PMI Jun | 49.3 | 48.7 | ||

| 14:00 | USD | ISM Manufacturing Prices Paid Jun | 55.9 | 57 | ||

| 14:00 | USD | ISM Manufacturing Employment Index Jun | 51.1 | |||

| 14:00 | USD | Construction Spending M/M May | 0.30% | -0.10% |

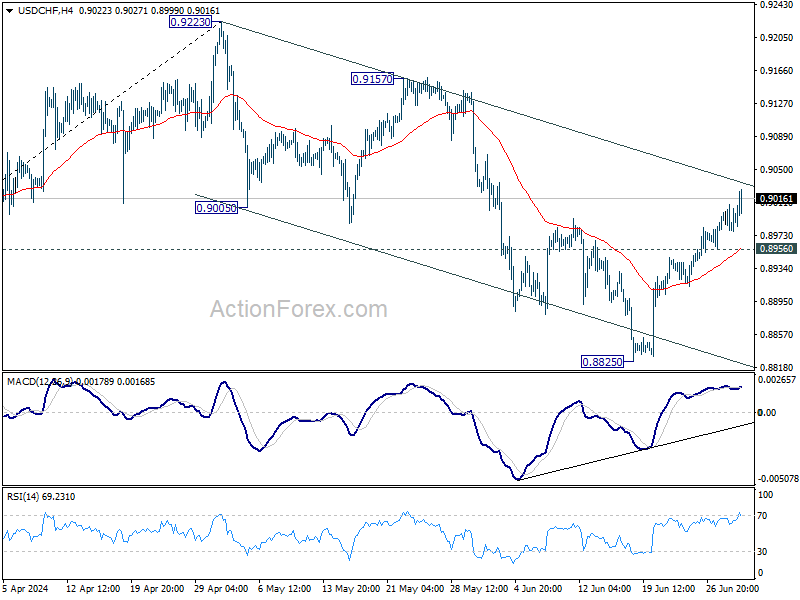

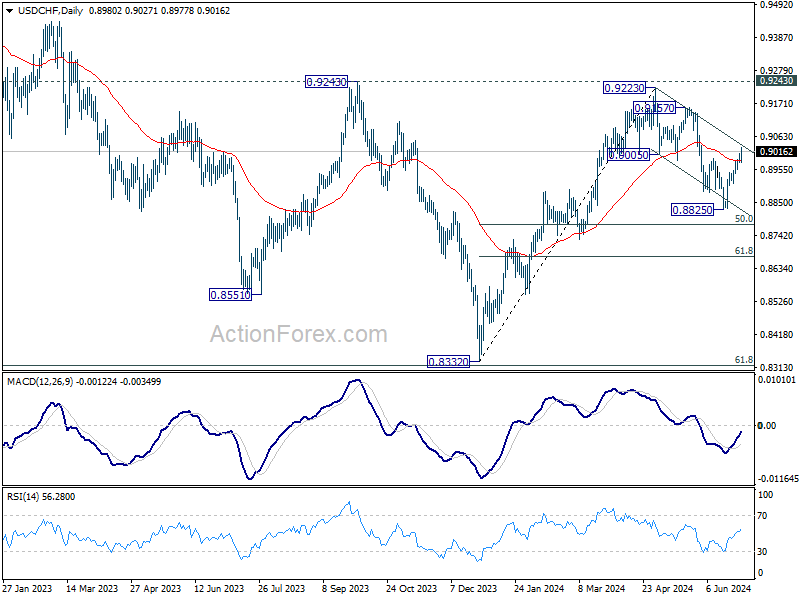

Instrument of the Week (July 1—5): USDCHF Review!

The USDCHF pair, commonly called the "Swissie," represents the exchange rate between the US Dollar and the Swiss Franc, providing insights into the economic dynamics between the United States and Switzerland. The US Dollar is influenced by the broader economic trends in the United States and decisions by the Federal Reserve, particularly concerning interest rates and monetary policy. The Swiss Franc, known for its stability, is impacted by Switzerland’s economic policies and its status as a global "safe haven" currency. This status often leads to its appreciation during periods of international economic uncertainty.

Switzerland Consumer Price Index (CPI) MoM, July 4, 8:30 (GMT+2)

This CPI release is key for traders, affecting the Swiss Franc’s valuation. The upcoming release of Switzerland’s CPI is projected at a 0.2% increase, slightly under the prior month’s 0.3%. If the actual CPI exceeds this forecast, indicating higher inflation than expected, it could prompt the Swiss National Bank (SNB) to adopt a more hawkish monetary policy stance, potentially strengthening the Swiss Franc against the US Dollar. This would likely lead to a decline in the USDCHF exchange rate. Conversely, if the CPI is lower than forecast, suggesting weaker inflation, it may soften the Franc, causing an increase in the USDCHF rate as confidence in the Swiss economy’s strength wanes.

US Nonfarm Payrolls, July 5, 14:30 (GMT+2)

The US Nonfarm Payrolls for July are expected to add 180 000 jobs, down from the previous month’s 272 000. This data is pivotal as it reflects the health of the US job market, potentially impacting Federal Reserve policy. Should the payroll numbers exceed this forecast, it would signal a stronger US labor market than anticipated, potentially leading to tighter US monetary policy. This scenario likely bolsters the US Dollar, causing an upward movement in the USDCHF rate. However, if the job addition is less than expected, indicating a slowing in economic growth, this could weaken the US Dollar against the Swiss Franc and result in a downward trend for the USDCHF pair as confidence in the US economic outlook diminishes.

Last time, on June 7, US NFP data far exceeded forecasts, which contributed to a strong USDCHF rally!

In the Daily timeframe, USDCHF started a short-term bearish trend after a prolonged rise. After reaching the lower trend line, the price bounced and reached the critical resistance area, previously a support, testing MA100. There are two options to consider in this case.

-

- If the price passes the resistance at 0.9000 and MA100, the growth will start with the target of 0.9150;

- Otherwise, the rebound from the resistance will continue the fall to 0.8840;

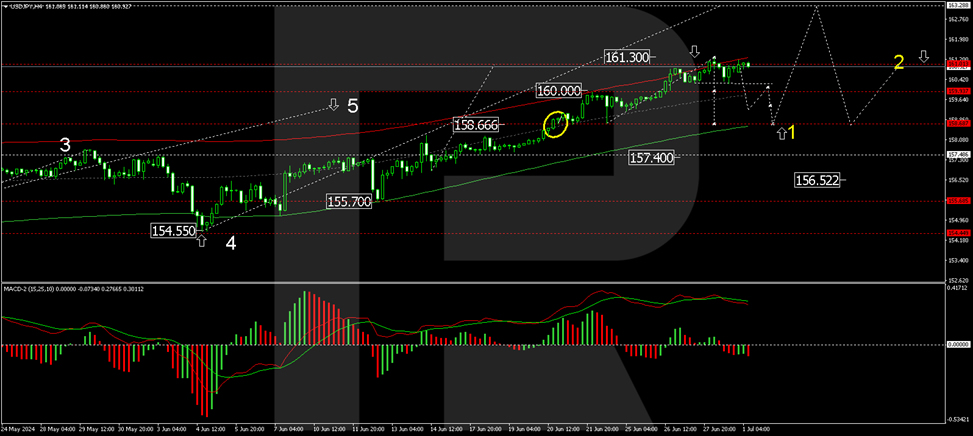

Japanese Yen Faces Further Depreciation Amid Rate Differentials

The USD/JPY pair continues to escalate, currently positioned at 160.88, nearing the 37-year peak of 161.27 achieved last Friday.

Early today, the yen temporarily strengthened following Japan’s Q2 Tankan survey results, which indicated a slight improvement in industrial sentiment to 13 points from 11. However, the services sector displayed mixed results, maintaining 27 points against predictions of an increase, with future expectations slightly downgraded.

Despite these data points, the predominant driver of the yen’s weakness remains the significant interest rate differential between the Bank of Japan (BoJ) and the US Federal Reserve.

The BoJ has no immediate plans to adjust interest rates but might alter its government bond purchases, hinting at potential monetary tightening. However, market sentiment remains sceptical about such changes, contributing to the yen’s downward pressure.

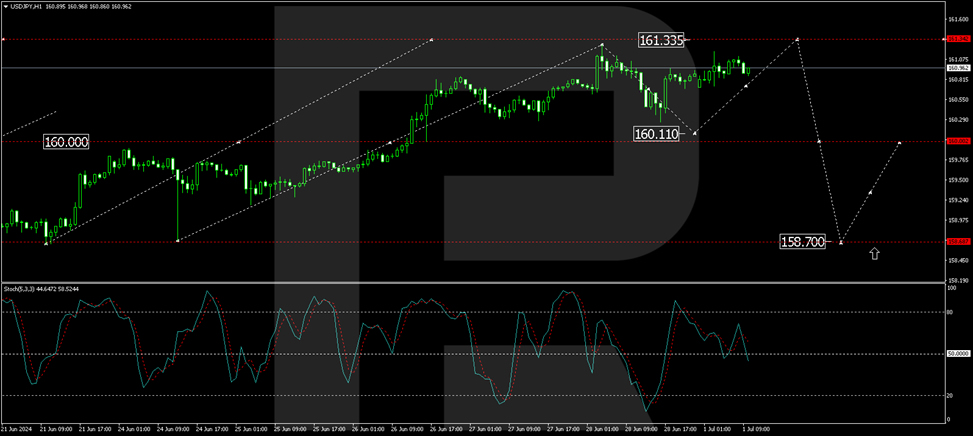

USD/JPY technical analysis

The USD/JPY is creating a consolidation range just below the 161.26 level. A brief surge to 161.33, considered a local peak within this upward trend, is possible. After this level, a corrective movement to 158.66 might initiate, potentially followed by another upward wave aiming for 163.30. This forecast is supported by the MACD indicator, with its signal line positioned above zero but pointing downwards, suggesting upcoming corrections.

The pair completed an upward movement to 161.26, followed by a correction to 160.26. Currently, it has surged to 160.88, forming a consolidation range. Breaking above this range could lead to a rise towards 161.30. Conversely, a downward break might lead to a correction to at least 160.11 before another potential rise to 161.30. The Stochastic oscillator indicates that the signal line, currently above 50, is poised to drop to 20, reflecting potential short-term declines before further gains.

Market outlook

As investors navigate these fluctuations, the broader focus remains on global central bank policies, particularly any shifts by the BoJ or the Fed that could influence the USD/JPY trajectory. The upcoming economic releases and central bank updates will be crucial in shaping market dynamics and the yen’s valuation against the dollar.

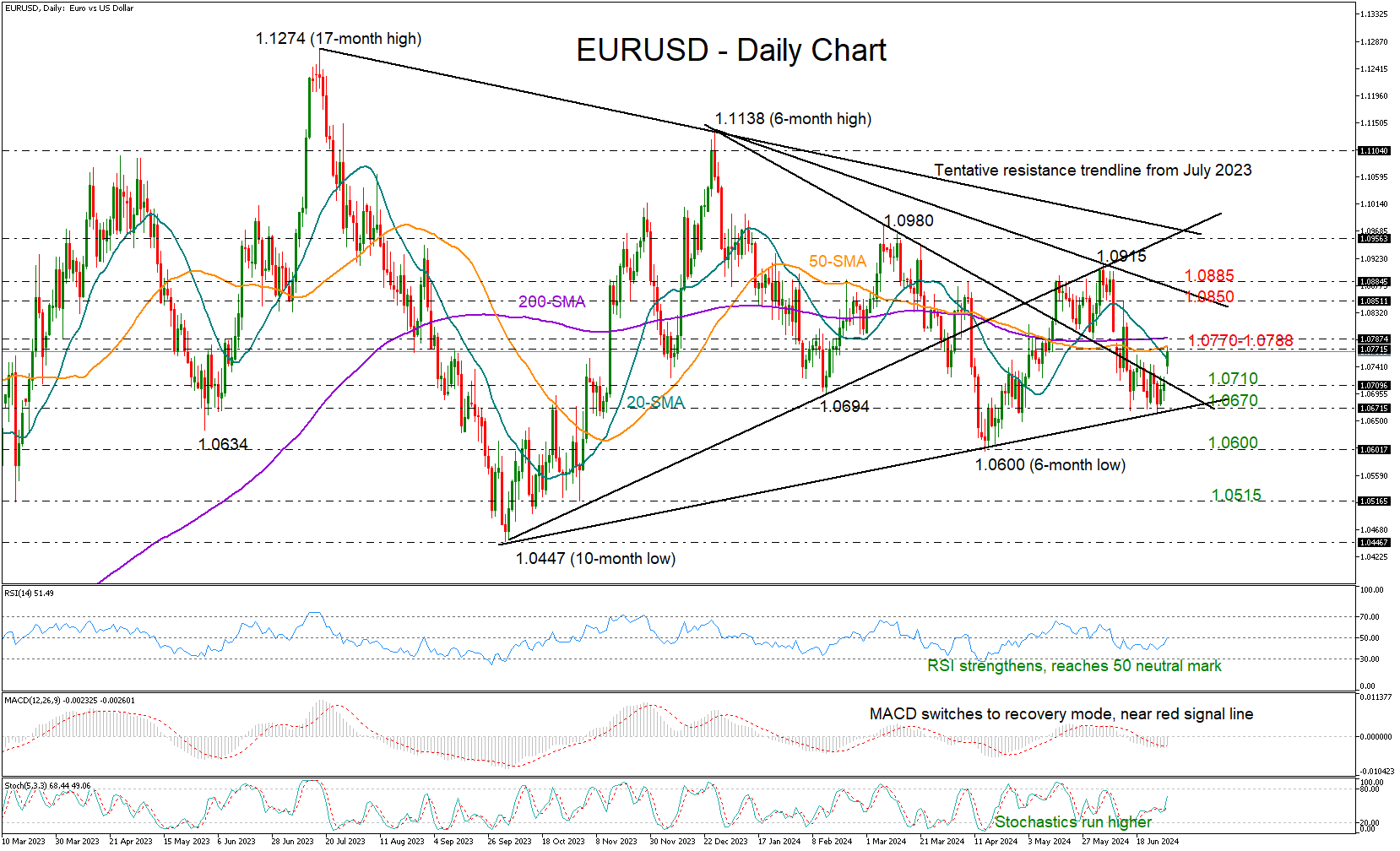

EURUSD Gaps Higher Over Potential French Hung Parliament

- EURUSD surges after French far-right party wins first race with weaker majority

- Bullish bias expected to come above 1.0788; sellers could take control below 1.0670

EURUSD opened with a positive gap on Monday after Le Pen’s far right party dominated the first round of the election on Sunday with a smaller margin than analysts expected, increasing speculation that an absolute majority on July 7 might be a struggle for the Euro-sceptic party.

The pair ran to an almost three-week high of 1.0742, but the 20- and 50-day simple moving averages (SMAs) kept the price action limited. Also, a close above 1.0788 and the nearby 200-day SMA is still required for an advance towards the 1.0850-1.0885 constraining territory. Beyond the latter, the price could experience a significant appreciation towards the ascending line from October 2023 seen around 1.0955.

A new bullish phase is looking more likely after the latest rebound near the critical support trendline at 1.0660. The upward move in the technical indicators is another encouraging sign that the bulls could stay in play, although some caution is still necessary as the RSI has yet to climb above its 50 neutral mark and the MACD is around its red signal line in the negative region.

Nevertheless, sellers might not show up until the price tumbles below the crucial support trendline seen at 1.0670. In the event that the bearish scenario plays out, the pair could decline to 1.0600, and if it breaks below that level, it could result in more dramatic movements, ultimately shifting focus to the 1.0515 restrictive region.

Overall, EURUSD appears to have located a favorable starting point for its next bullish stage, and a move above 1.0788 may be required to trigger new buying.