Sample Category Title

ECB’s Lagarde: No rush for further rate cuts as data-dependent approach prevails

At the ECB Forum on Central Banking overnight, ECB President Christine Lagarde hinted that the central bank is not in a hurry to cut interest rates again following its initial rate cut in June.

She highlighted that the central bank is facing "several uncertainties" concerning future inflation. These uncertainties primarily revolve around the dynamics of profits, wages, and productivity, and the potential impact of new supply-side shocks.

Lagarde emphasized that it will take time to accumulate sufficient data to be confident that the "risks of above-target inflation have passed."

The "strong labor market" was noted as a positive factor, allowing the ECB to "take time" to gather more information before making further decisions. However, Lagarde also acknowledged that "growth outlook remains uncertain," indicating that the ECB must remain vigilant and adaptable to changing economic conditions.

She reiterated, "All of this underpins our determination to be data-dependent and to take our policy decisions meeting by meeting."

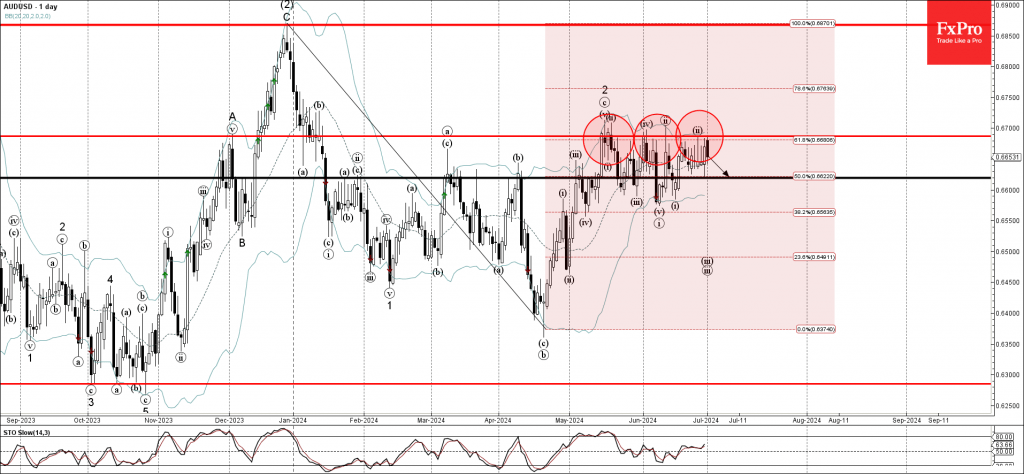

AUDUSD Wave Analysis

- AUDUSD reversed from strong resistance zone

- Likely to fall to support level 0.6620

AUDUSD currency pair recently reversed down from the strong resistance zone located between the key resistance level 0.6685 (which has been steadily reversing the price from the start of May) and the upper daily Bollinger Band.

This resistance zone was further strengthened by the 61.8% Fibonacci correction of the previous downward impulse from December.

AUDUSD currency pair can be expected to fall further toward the next support level 0.6620 (former minor support from the end of June).

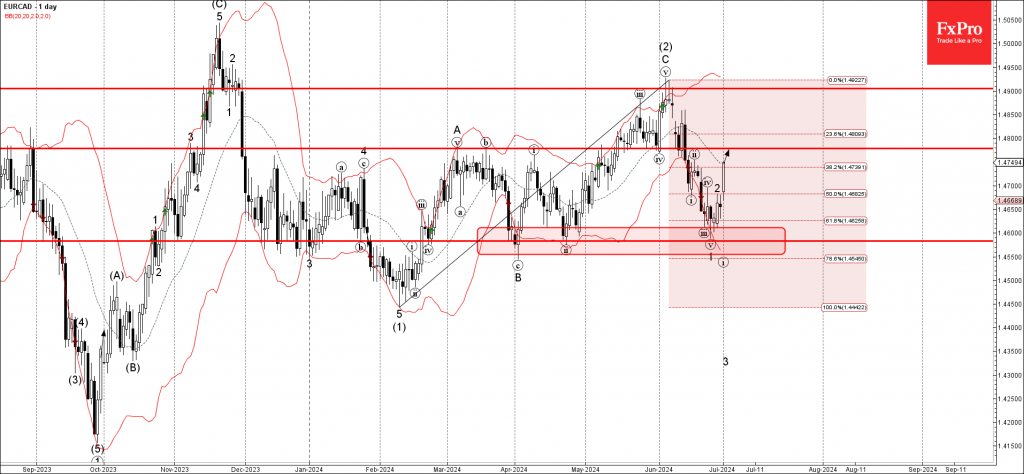

EURCAD Wave Analysis

- EURCAD reversed from support zone

- Likely to rise to resistance level 1.4780

EURCAD recently reversed up with the daily Hammer from the support zone located between the key support level 1.4580 (which has been reversing the price from the start of April) and the lower daily Bollinger Band.

The upward reversal from this support zone started the active minor ABC correction 2.

Given the strength of the support level 1.4580, EURCAD currency pair can be expected to rise further toward the next resistance level 1.4780 (former pivotal support from May).

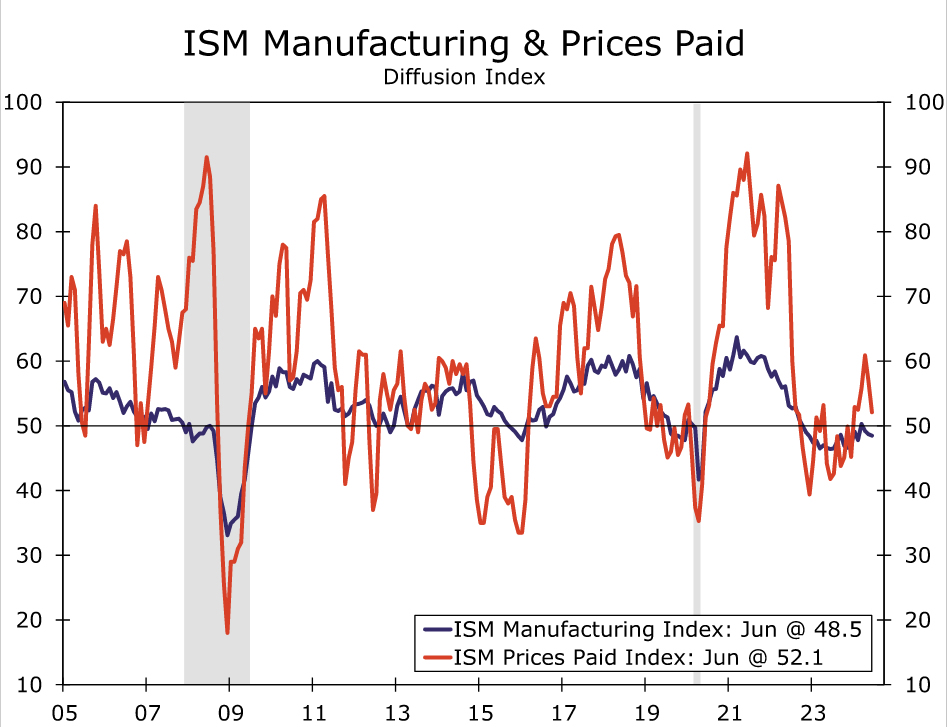

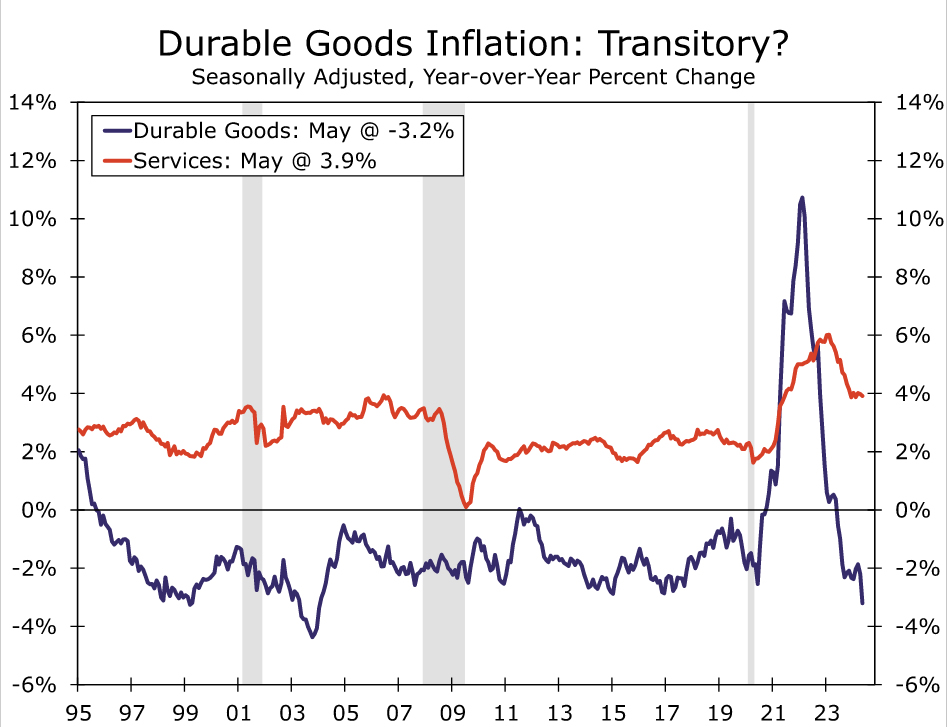

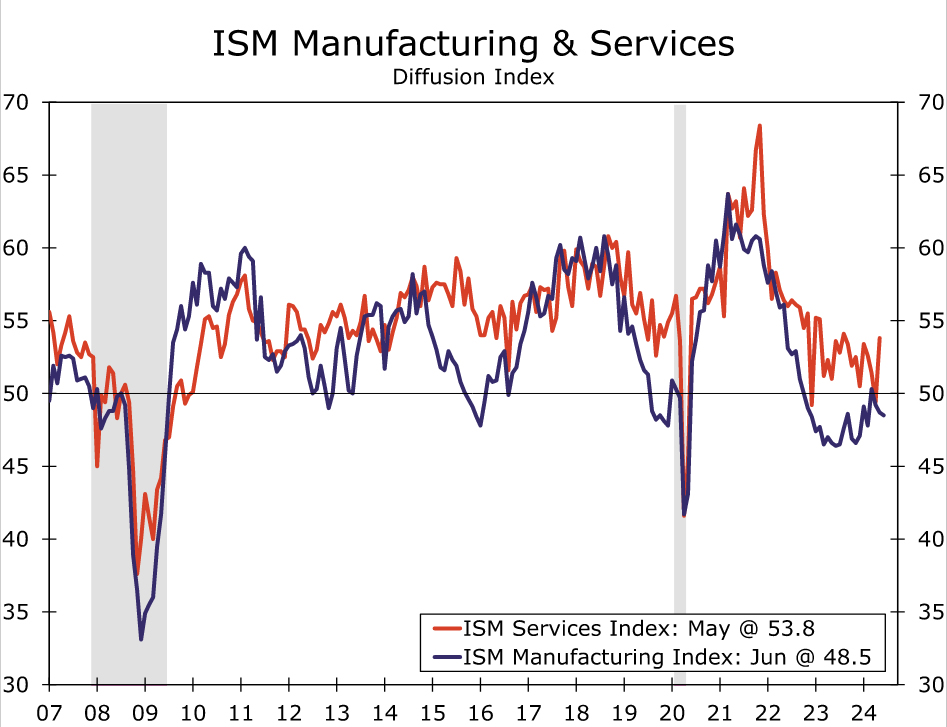

June ISM: Activity Still Soft, but Prices Cooling

Summary

Manufacturing activity remained in contraction territory in June, but in a sign of moderating inflation pressure, the prices paid component fell 4.9 points. New orders rose more than any other component but remains in contraction.

Prices Cool

The ISM manufacturing index slipped to 48.5 in May as tight credit conditions and elevated borrowing costs continue to constrain activity in the factory sector. The headline reading marks a 0.2 point decrease from last month while the prices paid measures at 52.1 represents a 4.9 point monthly decline, the single biggest drop of any component (chart). Price pressures have not gone away, but they have abated.

A bounce in the orders component to 49.3 after slipping to 45.4 in May suggests that the decline in both orders and shipments of core capital goods in May could be short-lived. The 3.9 point jump here was the biggest gain of any component.

One interesting thing to watch is the emerging difficulties in shipping and supply chains. The ongoing attacks in the Suez Canal and the associated re-routing is both expensive and time-consuming. We have heard from a number of clients on this topic in recent weeks, but it was conspicuously absent from the respondent comments. For now at least, the supply chain disruptions are more of an annoyance than they are a massive disruption. The supplier deliveries measure came in at 49.8, up a bit from May's reading.

The Great Divergence

One could make the argument that since the Federal Reserve starting raising rates in this cycle, the manufacturing sector has been taking it in the chin while the service sector has been taking it in stride. What explains this dynamic?

Prior to raising rates in the current cycle around 2021, policymakers at the Federal Reserve suspected that because supply chains were disrupted and because factories at home and overseas had shut down in compliance with COVID protocols, inflation was merely transitory. With the benefit of hindsight, it is clear now that inflation dynamics were not transitory. Yet a glance at the nearby chart shows that when it comes to durable goods prices, inflation was transitory. It is service sector pricing that has proved to be longer lasting.

The Federal Reserve began raising rates in March 2022. At that moment, the manufacturing sector may not have been humming along at full tilt the way it was in 2021, but the ISM manufacturing index at the time was firmly in expansion territory at 57.3. As rates continued to rise, the ISM began a trend decline, and by year's end this trusted barometer for the factory sector broke through the 50 line of demarcation between expansion and contraction. It has remained mired there for 19 of the past 20 months. During the same time period, the service sector ISM has reported only two months of contraction (chart).

While higher financing costs do make big-ticket durable goods items harder to afford, there is more to the deteriorating picture for manufacturing than just Fed rate hikes. During 2020 and 2021, consumers were largely unable to fully engage in dining, travel and other in-person activity. Flush with cash from stimulus programs, many households bought new furniture for the homes where they were spending much more time. Sellers of boats, RVs, jet-skis and snowmobiles all had difficulty keeping product in stock. In short: lots of demand was pulled forward.

By 2022, even the most COVID restriction-abiding consumers were back in action crowding airports and hotels, and making reservations became an absolute requirement for dining out in many locales. While this catch-up spending in the service sector is finally losing a bit of momentum, it does offer some perspective on why service prices have been slower to come down.

The June jobs report will be published on Friday morning; our forecast is for a net gain of 200K jobs. The employment component in today's report came in at 49.3. That does not move the needle for our forecast, nor do we suspect it to make much of a dent in consensus expectations. Manufacturing jobs have not added or subtracted more than 8K jobs in any given month so far this year.

More broadly, the latest GDP revisions revealed that growth in equipment outlays grew at an annualized pace of 1.6% in Q1; that comes after equipment spending fell in three out of four quarters in 2023. But overall business fixed investment in Q1 was actually stronger and boosted the headline by more than a full percentage point. Intellectual property outlays shot up at a 7.7% annualized rate in the first quarter, the fastest growth in a year and a half. We look for soft BFI spending in the second half of 2024 before a measured increase in capital outlays in 2025.

Sunset Market Commentary

Markets

Marine Le Pen’s Rassemblement National scored broadly as expected in the first round of French parliamentary elections. They won the ballot with around 33% of the vote, ahead of the left front (28%) and Macron’s alliance (21%). In 485 out of 577 districts, the RN and its allies won outright or made it to next week’s second round. In more than half of the districts, it could be a 3-way race in theory though the likes of PM Attal already called for tactical redraws to keep the far right from power. The deadline for eligible candidates is tomorrow at 6pm after which ballot polls will become more precise. A hung parliament with a large, but no absolute, majority for RN remains the most likely outcome but the power-sharing cohabitation scenario is still at play as well. It explains today’s “muted” relief move. EUR/USD moved up from 1.07 to currently 1.0760. French assets outperform with the 10-yr OAT/swap spread currently trading around 46 bps compared to last week’s high of 50 bps. Ahead of the European elections, this was only 25 bps. European stock markets add 0.75%-1.25% with the French CAC40 rising 1.85%. German Bund yields rise around 8-9 bps across the curve with Bunds underperforming US Treasuries. US yields add 3-4 bps, extending the move that started in the run-up to and after last week’s presidential election debate which triggered a significant change in polling results in favour of former president Trump.

Today’s eco calendar only contained German inflation data. Prices rose by 0.2% on a monthly basis, the same pace as in May and exactly in line with forecasts. The Y/Y-figure slowed as expected from 2.8% to 2.5%. Regional data suggest that the drop was mainly due to a negative contribution from road-fuel prices. Lower price gains for package holidays and miscellaneous goods and services also dragged inflation slightly down. Spanish and French CPI data were last week in line with forecasts as well suggesting that tomorrow’s EMU number could be a non-event. Consensus stands at 0.2% M/M and 2.5% Y/Y (from 2.6%) for headline CPI and 2.8% (from 2.9%) for core CPI. Today’s data had no impact. After European close, attention will turn to ECB Lagarde’s opening speech at the ECB forum on central banking in Sintra. Tomorrow and on Wednesday, an avalanche of central bankers will discuss topics like drivers of equilibrium interest rates, productivity in the short and long run, geopolitical shocks and inflation,…

News & Views

The Polish minister for development and technology Paszyk informed the Polish financial website Money.pl about a plan that would subsidize up to 175000 mortgages over the next five years. The minister said that high loan costs are both hampering Polish home purchases. His interest-trimming proposal marks a sharp U-turn with the Tusk-led coalition government as recently as mid-May. Cautiousness back then ruled, saying that additional mortgage support could overstimulate a housing market that was already benefitting from support under the previous government. Prices as a result rose at the EU’s sharpest pace last year. New mortgages in Poland are the most expensive in the EU, driven in part by a central bank that’s refraining from cutting rates. The National Bank of Poland is meeting this Wednesday and is widely anticipated to keep the policy rate at 5.75% for a ninth time straight. There’s a broad consensus within the MPC not to cut rates before 2025 given high (fiscal) policy uncertainty and its impact on inflation for the second half of this year.

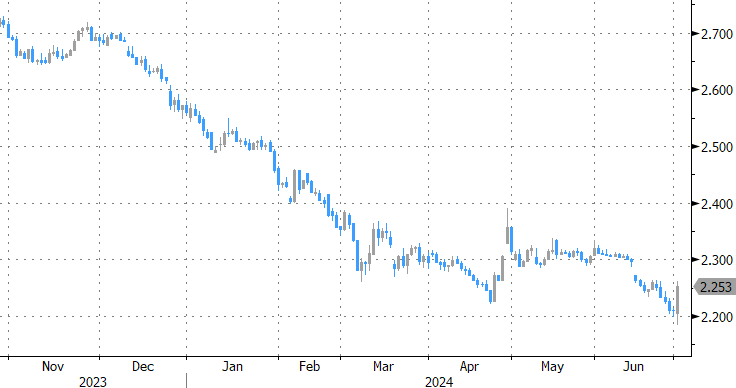

China’s central bank said it will borrow government bonds from primary dealers “in order to maintain the steady operation of the bond market”. The announcement came after China’s 10-yr yield dipped to the lowest level since data collection began in 2002. Chinese authorities have become wary of the bond bull rally, driven by investors looking for safe haven assets against the backdrop of a weak economy and expectations for ongoing (or increasingly) supportive monetary policy. The likes of the PBOC fear for the interest-rate risk implications. A market reversal could saddle up large bondholders (e.g. banks) with significant losses, posing financial stability risks. One of the ways the PBOC could operate is to borrow the bonds and sell them into the market. It is unlikely to significantly and permanently push up government bond yields though it may offer a bottom. China’s 10-yr yield rebounded intraday after the word got out, going from as low as 2.18% to 2.25% in the close.

Graphs

10yr OAT/swap spread: muted relief after first round of French elections

EUR/USD: similar ray of hope

Chinese 10-y bond yield rises from all-time low after PBOC announces programme to borrow bonds from primary dealers

Eurostoxx 50: again more firmly within the sideways trading range of the past months

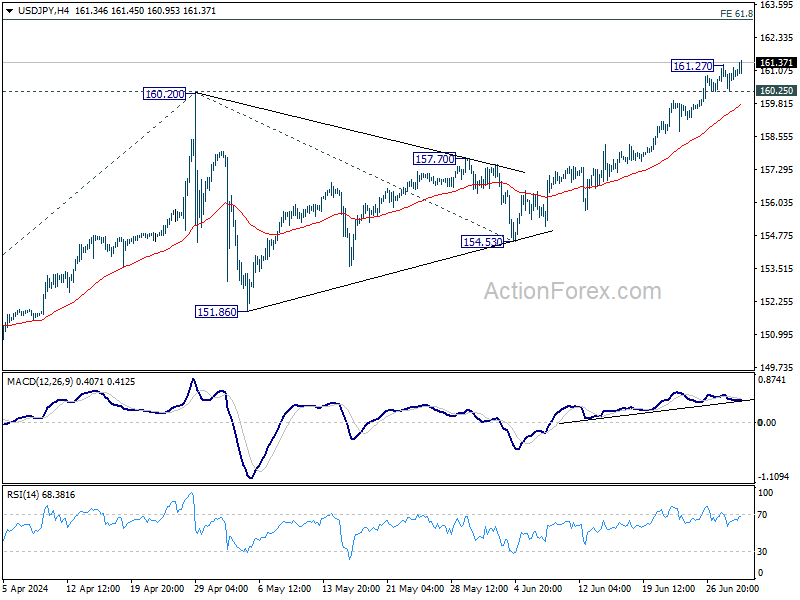

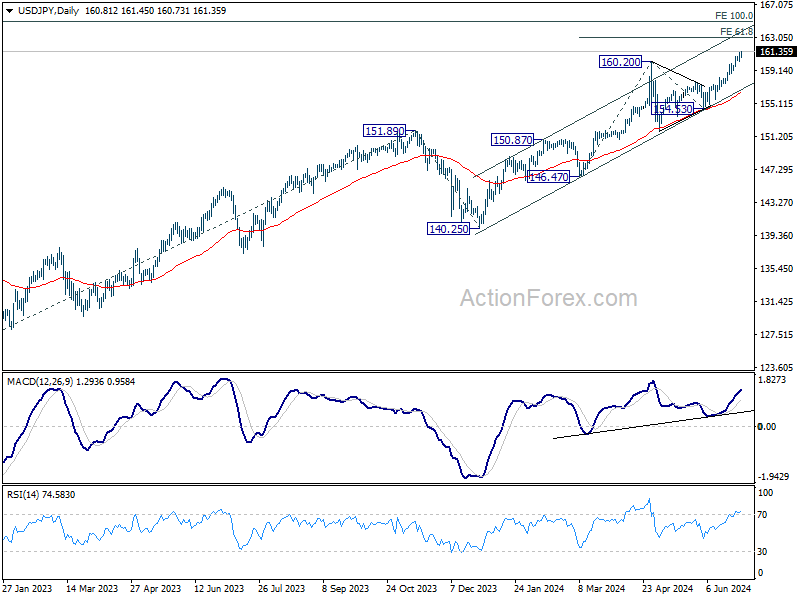

USD/JPY Rises Up After GDP Downgrade

The Japanese yen has dropped below the 161 line on Monday. The yen is trading at 161.39 early in the North American session, down 0.35% on the day.

Japan’s GDP revised sharply lower

Japan revised its first-quarter GDP report to -2.9%, y/y, sharply lower than the initial reading of -1.8%. On a quarterly basis, GDP was revised lower to -4.0%, compared to -3.7% in the fourth quarter. The downward revision was due to corrections in construction orders. The rare unscheduled revision will dampen hopes for a rate hike at the BoJ’s July meeting and points to a bumpy economic recovery.

At the same time, Japan’s Tankan quarterly survey indicated that business confidence had improved and corporate inflation expectations edged higher. These factors support a rate hike in the near term, which leaves BoJ policy makers in a bit of a quandary regarding rate policy due to the conflicting data.

What may tip the scale in favor of rate hike, perhaps as soon as July, is the significant slide of the Japanese yen. The yen is trading closes to 38-year lows against the US dollar and has plunged a staggering 14% this year. The BoJ intervened twice in the currency market in late April and early May and purchased some $61 billion worth of yen, but that proved to be only a stopgap measure as the yen has surrendered all of the gains which followed the interventions.

In the US, the economy has performed well but the manufacturing sector has posted only one month of expansion since November 2022. The ISM Manufacturing PMI is projected to improve to 49.1 in June, compared to 48.7 a month earlier. The 50 level separates contraction from expansion.

USD/JPY Technical

- USD/JPY pushed above resistance at 160.82 earlier and is testing resistance at 161.37. The next line of resistance is 162.38

- There is support at 160.36 and 159.81

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 160.36; (P) 160.82; (R1) 161.37; More...

Intraday bias in USD/JPY is back on the upside with break of 161.27 temporary top. Current up trend should target 61.8% projection of 146.47 to 160.20 from 154.53 at 163.01. On the downside, below 160.25 minor support will turn intraday bias neutral and bring consolidations again, before staging another rally.

In the bigger picture, long term up trend is still in progress. Further rise is expected as long as 154.53 support holds. Next target is 100% projection of 127.20 (2023 low) to 151.89 (2023 high) from 140.25 at 164.94.

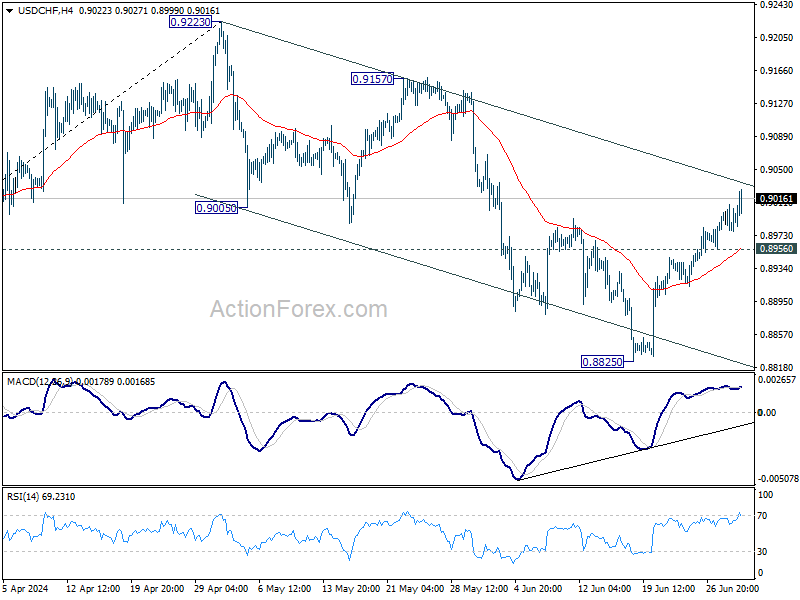

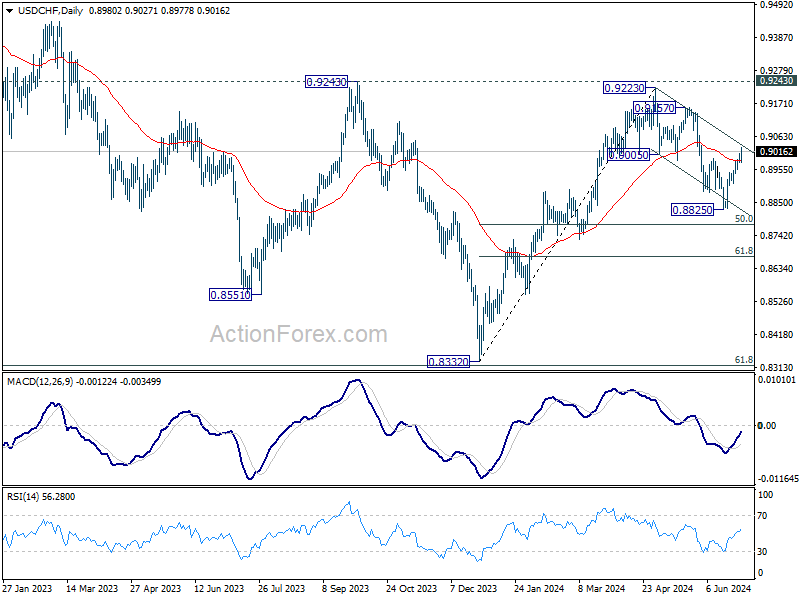

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8971; (P) 0.8990; (R1) 0.9007; More…

Intraday bias in USD/CHF remains on the upside at this point, for channel resistance (now at 0.9034). Fall from 0.9223 might have completed as a three-wave corrective move to 0.8825. Firm break of channel resistance will target 0.9157 resistance next. On the downside, below 0.8956 minor support will turn intraday bias neutral gain first.

In the bigger picture, price actions from 0.8332 medium term bottom are seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance affirms this case, and maintains medium term bearishness. While more range trading could be seen between 0.8332/0.9243 first, downside breakout is mildly in favor at a later stage.

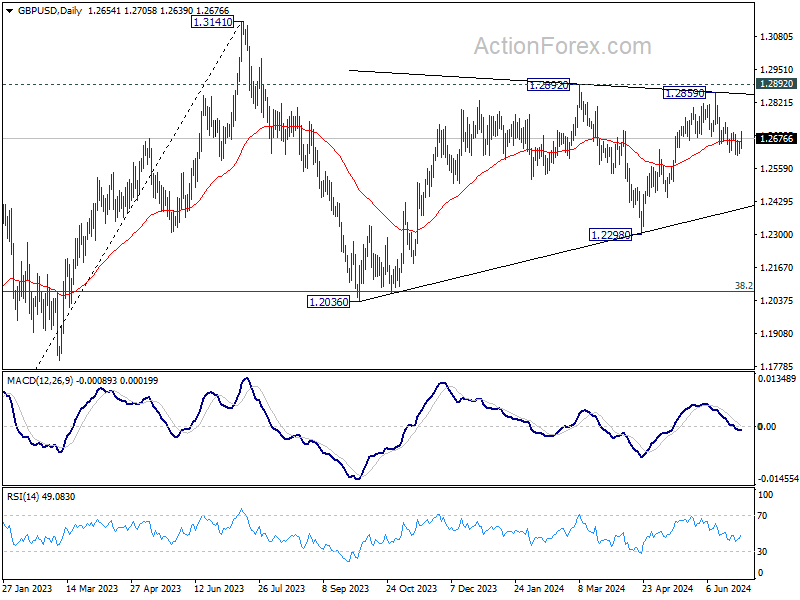

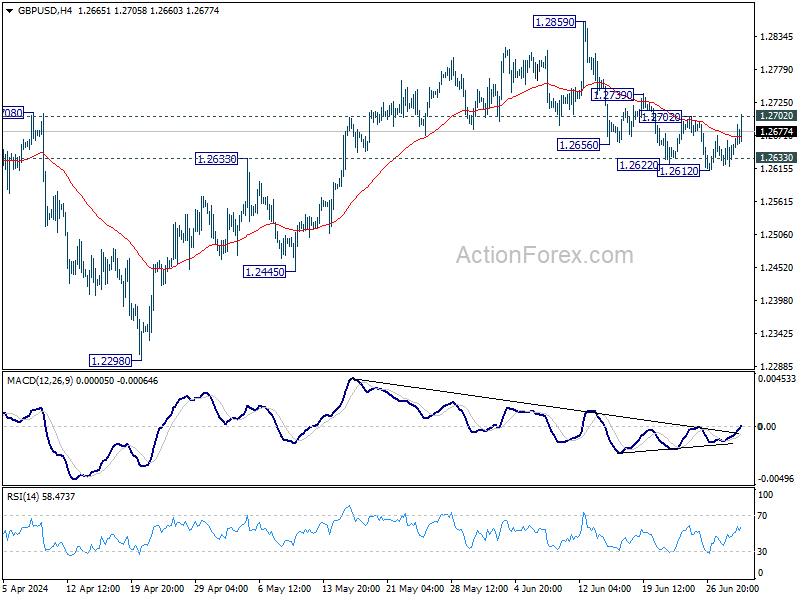

GBP/USD Mid-Day Outlook

Daily Pivots: (S1) 1.2623; (P) 1.2642; (R1) 1.2665; More...

Intraday bias in GBP/USD remains neutral at this point. On the upside, firm break of 1.2702 resistance will argue that pull back from 1.2859 has completed, and bring retest of this high instead. Nevertheless, rejection by 1.2702 will keep risk on the downside. Sustained trading below 1.2633 resistance turned support will argue that whole rise from 1.2298 has completed, and target 1.2445 and below.

In the bigger picture, price actions from 1.3141 medium term top are seen as a corrective pattern that is still in progress. Break of 1.2445 support will confirm that another falling leg has started and target 1.2036 cluster support again (38.2% retracement of 1.0351 (2022 low) to 1.3141 at 1.2075. Nevertheless, break of 1.2892 resistance will argue that larger up trend from 1.0351is ready to resume through 1.3141.