Sample Category Title

Oil Jumps on Hurricane Beryl, July 4th Demand

The week started on a positive note but the positive vibes will likely leave their place to the chatter of scenarios regarding how the French will prevent Marine Le Pen from gaining a majority in the parliament in the second round of the legislative election this weekend. Will the opposition parties form a sufficiently convincing alliance to prevent National Rally from gaining an outright majority, or will Marine Le Pen’s National Rally amass the majority despite all efforts? Both scenarios mean some political uncertainty for France and beyond its borders, but investors’ hearts are pounding toward the first option: a hung government – which would at least prevent Le Pen from exploding the national debt and jeopardize/reverse Macron’s efforts to pull the national debt back to levels acceptable by EU rules. The latter would help tame the spread between the French and the German bonds – which already retreated below 80pb on Monday on hope and pricing that Le Pen won’t secure a parliamentary majority, and support euro. The EURUSD rallied to 1.0776 yesterday, flirted with its 50-DMA but retreated to around 1.0730 this morning. The CAC 40 opened the week with a bang, gained as much as 2.7% before paring losses and closing just 1% up. The European futures are in the negative this morning.

On the data front, European Central Bank (ECB) Chief Lagarde warned that the bank doesn’t have enough evidence that inflation threat is over, hinting that the ECB will probably bypass a second rate cut when it meets later this month. Inflation numbers revealed by major Eurozone countries since Friday are mixed: as expected in France, a bit higher than expected in Spain and a bit lower than expected in Italy and Germany. So far, the actual CPI numbers didn’t deviate much from expectations – clearly not enough to deviate the attention from the French election jitters. The aggregate inflation figure for early June is due today, both headline and core inflation are expected to have eased slightly in June. If that’s the case, we could see the ECB doves breathe a sigh of relief, if not, the euro could see a minor support but in both cases, the euro will remain under the pressure of French political uncertainties throughout the week, and any rally attempts could limited into the second election weekend in France.

In the US, data released yesterday posted softer-than-expected ISM manufacturing numbers in June and a decline in construction spending in May. Atlanta Fed’s GDP Now plunged to 1.7%. All that softness could’ve pulled the US yields lower but the political news – there - interfere with the market pricing as well. According to the latest, the Supreme Court said that Donald Trump will benefit from some immunity from criminal charges for trying to reverse the 2020 election, making him a step closer to winning this year’s presidential election after last week’s worrying debate for Joe Biden. The Trump win expectation makes US curve steeping an active bet according to Morgan Stanley analysts who say that Trump in the White House will slow growth and boost inflation – with increased trade tensions and more tariffs.

In the FX, the US dollar index fell yesterday on a kneejerk jump in the euro but is upbeat this morning. The USDJPY continues its hike above the 161.50 level, preparing to test the 162 with limited upside potential given the direct FX intervention threat. The franc is giving back the safe haven gains of late. The euro-franc is back above the 100-DMA while the USDCHF takes over the 50-DMA offers. The Swiss National Bank’s (SNB) dovish stance should keep the franc on a softening path, apart from periods of sudden appreciation due to safe haven flows.

In equities, the S&P500 consolidated gains near record on Monday, s Tesla jumped more than 6% to above its 200-DMA ahead of quarterly deliveries report that’s due today, and that could confirm a second quarter decline in deliveries. The Chinese rival BYD on the other hand is down in Hong Kong after announcing to have sold 1 million cars in Q2 – around 426K of them being purely electric.

In energy, crude oil started the week strong ahead of the July 4th holiday in the US, which AAA predicts will see a record number of drivers, and Hurricane Beryl, which is not expected to impact operations in the Gulf of Mexico immediately but could cause disruptions later in the week. US crude rallied 2.4% and hit the $84pb mark for the first time since April. Risks remain tilted to the upside, the next target for the bulls stands at $85pb level, where we should see support and rebound given that the soft manufacturing data from the US and China at the start of the week don’t give a further support.

Elsewhere, Cable remains under pressure ahead of Thursday’s general election while the FTSE 100 couldn’t really benefit from a softer sterling and a rapid rise in oil prices yesterday and closed the session near flat. The election uncertainty seemingly keeps the bulls on the sidelines even though a Labour win is seen as a net positive for the British stocks. The price pullbacks in the FTSE 100 are likely interesting opportunities to strengthen long positions in energy-heavy British stocks that should fully benefit from reflation trades once the election is behind. Zooming out, the FTSE 100 didn’t do bad at all over the past few quarters. The index posted a fourth quarter gain in the Q2, has hit a record high in May and remains upbeat as we enter the second half on expectation of more political stability, an upcoming Bank of England (BoE) rate cut and improved reflation flows.

RBA Minutes: Gaps Are Narrowing, And So Is The Path

The RBA’s strategy relies on assessing gaps between supply and demand. There are uncertainties involved in this approach, but so far, the inflation outlook hasn’t changed enough to spur a rate increase.

The minutes for the RBA Board’s June 2024 meeting highlighted that levels matter in the RBA’s view of the economy, as well as growth rates. The brief section on international developments noted that it was the economies with negative output gaps (where aggregate demand is below aggregate supply), such as Canada and Sweden, where services inflation was still declining. On the domestic side, the minutes started by noting that the staff assessed that ‘aggregate demand had continued to exceed aggregate supply’. Likewise, the labour market ‘was still assessed as tight relative to full employment’. Both the output gap and the labour market tightness were assessed as narrowing.

The discussions on considerations for monetary policy are increasingly being framed as assessments of these gaps. This is not a complete departure from past approaches, but as the apparent gaps narrow, the evidence base for these estimates will face intensified scrutiny. So will the Board’s assessment that global growth has troughed, noting the current uncertainties around trade policy and geopolitics more broadly.

Given the uncertainties around these ‘gap’ estimates, the point at which the gaps are assessed to have closed will be something of a judgement call, a point acknowledged in the minutes. The June quarter CPI and the revised forecasts will, therefore, be important inputs to the August Board meeting.

One point to watch in future RBA communication is how the central bank reconciles its view that the labour market is still tighter than the full employment level, with its view – which we share – that wages growth has peaked. The minutes also noted the easing in growth in unit labour costs, as has been previously highlighted by Westpac Economics colleague Pat Bustamante. These developments might help explain why the Board highlighted that it was not following the practice of other central banks in assuming that ‘some spare capacity was necessary to bring inflation back to target within a reasonable timeframe’.

The RBA had been surprised by the stronger durable goods inflation in the April inflation indicator. However, there was little new information on services inflation, which has been more of a focus recently. The May monthly inflation indicator, which was released after the meeting, was above consensus, but the services component showed further moderation; that said, the pace of decline is slow, as it has been overseas. Again, we expect that the Board will look to the full quarterly data to form a revised view.

The minutes highlighted an increased risk that inflation could take longer to return to target than previously expected. However, actual outcomes implied that ‘the economy was still broadly tracking on a path consistent with returning inflation to target in 2026’. If future developments point to this no longer being the case, the Board would act. But as the output and labour market gaps narrow, the case to take out insurance against heightened perceived risks alone would weaken.

The revisions to overseas holiday spending were seen as bringing household consumption behaviour more in line with past relationships. But the implications for future household spending are not clear. The implied level of household saving is now very low, though this is often revised and extra payments into mortgages are higher than the pre-pandemic average. There is probably a distributional angle here; the minutes do not tease this out but did mention ‘clear evidence that many households were experiencing financial stress’. Also noteworthy in the minutes is the mention of household debt growing more slowly than incomes, especially once extra payments into offset accounts were included.

Several of the developments mentioned in the minutes highlight the awkwardness of the current policy environment. This is not a situation of needing to lean against strong private sector demand that is driving inflation higher. Rather, we see weak demand and declining inflation. The policy decision therefore rests on views on whether demand is weak enough to bring inflation down fast enough, given the factors working in the wrong direction.

Among these factors, it is noteworthy that the minutes highlighted the role of public sector demand in driving both GDP and employment growth. In addition, the minutes noted that if aggregate supply were more constrained than previously assumed, this might also strengthen the case to raise rates. Ongoing slow (but positive) productivity growth was also highlighted. If that scenario does play out, the case for other policymakers to do what they can to repair the supply side becomes more urgent.

Overall, these minutes confirm our view that the Board would raise rates if the outlook shifted to imply a slower or stalled decline in inflation. But it has not come to that point yet. And given the increased focus on the Bank’s full employment mandate, one can readily imagine that the Board is hoping that it doesn’t come to that point, either.

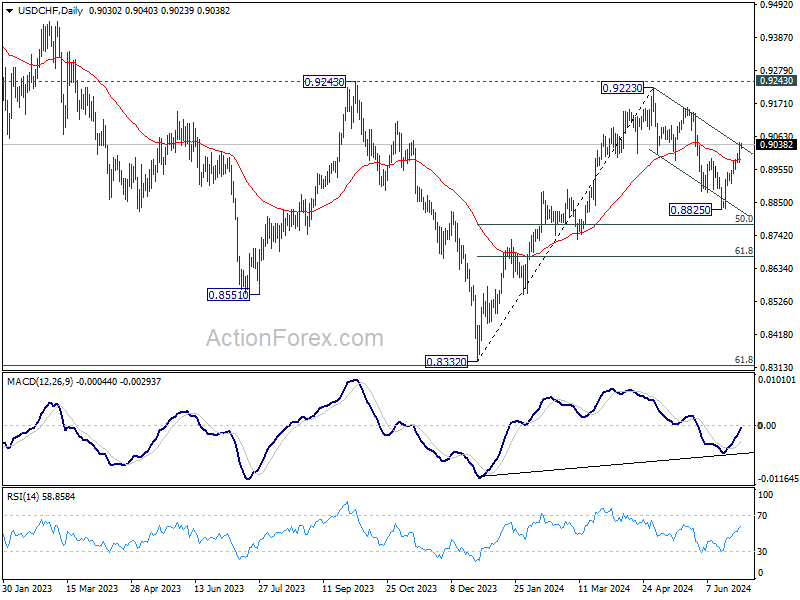

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8986; (P) 0.9016; (R1) 0.9057; More…

Intraday bias in USD/CHF remains on the upside for the moment. Fall from 0.9223 might have completed as a three-wave corrective move to 0.8825. Sustained trading above the near term falling channel resistance will bring further rally to 0.9157 resistance next. On the downside, below 0.8977 minor support will turn intraday bias neutral gain first.

In the bigger picture, focus remains is now on 0.9223/9243 resistance zone. Decisive break there would complete a head and shoulder bottom pattern (ls: 0.8551; h: 0.8332; rs: 0.8825). That would indicate larger bullish trend reversal. Nevertheless, rejection by 0.9223/43 will keep medium term outlook neutral at best, for more range trading between 0.8332/9243 first.

Dollar Rallies as Treasury Yields Surge With Trump’s Election Prospects

Dollar surged across the board overnight and stayed firm in Asian session, fueled by the strong rally in benchmark US Treasury yields. This rally is partly attributed to rising expectations of a Donald Trump victory in the upcoming presidential election. Analysts suggest that a Trump win would likely lead to heightened tariffs and expanded fiscal policies, both of which could stimulate inflation. Trump's performance in the recent debate against President Joe Biden has boosted these expectations, prompting some economists to recommend hedging against inflation as a precautionary measure.

Conversely, Kiwi faced substantial selling pressure following release of sharply deteriorated business confidence report for Q2. RBNZ had projected the timing for the first rate cut to be in Q3 next year, but the worsening business confidence and economic outlook have led some analysts to speculate that this cut could be brought forward to as early as Q1. There is even speculation that the first rate cut might occur as soon as Q4 of this year.

Across the broader currency markets, Euro is following closely behind Dollar as the second strongest currency of the day. However, it remains volatile due to ongoing political developments in France, where uncertainty is still high. Canadian Dollar is currently the third strongest currency. Conversely, Aussie is the second weakest, following Kiwi, despite hawkish minutes from RBA that highlighted significant concerns over upside inflation risks. Swiss Franc, British Pound, and Japanese Yen are mixed, occupying middle positions in the currency rankings.

Technically, the surprisingly strong rally in US 10-year yield overnight argues that fall from 4.737 has completed with three waves down to 4.188. That came just ahead of 61.8% retracement of 3.785 to 4.737 at 4.148. More importantly, this development suggest that rise from 3.785 is not over and could be seen to resume. Further rise is now expected as long as 55 D EMA (now at 4.376) holds. Next target is a retest on 4.737 resistance.

In Asia, at the time of writing, Nikkei is up 1.03% and back above 40k handle. Hong Kong HSI is up 0.40%. China Shanghai SSE is up 0.13%. Singapore Strait Times is up 0.52%. Japan 10-year JGB yield is up 0.0193 at 1.084. Overnight, DOW rose 0.13%. S&P 500 rose 0.27%. NASDAQ rose 0.83%. 10-year yield jumped sharply by 0.136 to 4.479.

RBA minutes: The narrow path is becoming narrower

Minutes of RBA's June meeting emphasize the need to remain "vigilant to upside risks to inflation". The RBA noted that the information received since the previous meeting reinforced this need, underscoring the "extent of uncertainty" in the current economic environment, which makes it "difficult either to rule in or rule out" future changes in interest rates.

Concerns were raised about the "narrow path" to bringing inflation back to target within a reasonable timeframe without significantly deviating from full employment. This path, according to the minutes, is "becoming narrower."

The decision to keep the cash rate target unchanged at 4.35% was deemed the stronger option compared to another rate hike. Data received since May meeting "had not been sufficient" to alter RBA's assessment that inflation would return to target by 2026, despite "some elevated upside risk" surrounding the forecast. Moreover, the minutes revealed that the members felt there was "not enough evidence" to suggest that the outlook for aggregate demand had strengthened.

NZIER survey shows rising pessimism among New Zealand firms

The NZIER Quarterly Survey of Business Opinion for Q2 reveals increasing pessimism among New Zealand firms. A net 44% of firms are now pessimistic about the economy's outlook over the next six months, up from 25% in Q1. Additionally, a net 28% reported a deterioration in their own trading during the three months through March, marking the weakest reading since mid-2020 during the COVID-19 pandemic.

Employment figures are equally concerning. A net 25% of firms laid off workers in Q2, the highest level since the global financial crisis in 2009. Furthermore, a net 10% expect to reduce staff numbers in the three months through September. Profit expectations are also bleak, with a net 34% of firms anticipating weaker profits in the third quarter, accompanied by falling investment intentions.

On a slightly more positive note, only a net 23% of firms expect to increase prices in Q3, the lowest since 2021. Additionally, companies are finding it easier to recruit workers, signaling reduced wage pressure. Fewer companies also reported rising costs, suggesting some relief from inflationary pressures.

ECB's Lagarde: No rush for further rate cuts as data-dependent approach prevails

At the ECB Forum on Central Banking overnight, ECB President Christine Lagarde hinted that the central bank is not in a hurry to cut interest rates again following its initial rate cut in June.

She highlighted that the central bank is facing "several uncertainties" concerning future inflation. These uncertainties primarily revolve around the dynamics of profits, wages, and productivity, and the potential impact of new supply-side shocks.

Lagarde emphasized that it will take time to accumulate sufficient data to be confident that the "risks of above-target inflation have passed."

The "strong labor market" was noted as a positive factor, allowing the ECB to "take time" to gather more information before making further decisions. However, Lagarde also acknowledged that "growth outlook remains uncertain," indicating that the ECB must remain vigilant and adaptable to changing economic conditions.

She reiterated, "All of this underpins our determination to be data-dependent and to take our policy decisions meeting by meeting."

Looking ahead

Eurozone CPI flash is the main focus of the day while unemployment rate will be released too. Canada will publiah PMI manufacturing.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8986; (P) 0.9016; (R1) 0.9057; More…

Intraday bias in USD/CHF remains on the upside for the moment. Fall from 0.9223 might have completed as a three-wave corrective move to 0.8825. Sustained trading above the near term falling channel resistance will bring further rally to 0.9157 resistance next. On the downside, below 0.8977 minor support will turn intraday bias neutral gain first.

In the bigger picture, focus remains is now on 0.9223/9243 resistance zone. Decisive break there would complete a head and shoulder bottom pattern (ls: 0.8551; h: 0.8332; rs: 0.8825). That would indicate larger bullish trend reversal. Nevertheless, rejection by 0.9223/43 will keep medium term outlook neutral at best, for more range trading between 0.8332/9243 first.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 22:45 | NZD | Building Permits M/M May | -1.70% | -1.90% | -2.10% | |

| 01:30 | AUD | RBA Meeting Minutes | ||||

| 09:00 | EUR | Eurozone Unemployment Rate May | 6.40% | 6.40% | ||

| 09:00 | EUR | Eurozone CPI Y/Y Jun P | 2.50% | 2.60% | ||

| 09:00 | EUR | Eurozone CPI Core Y/Y Jun P | 2.80% | 2.90% | ||

| 13:30 | CAD | Manufacturing PMI Jun | 50.2 | 49.3 |

RBA minutes: The narrow path is becoming narrower

Minutes of RBA's June meeting emphasize the need to remain "vigilant to upside risks to inflation". The RBA noted that the information received since the previous meeting reinforced this need, underscoring the "extent of uncertainty" in the current economic environment, which makes it "difficult either to rule in or rule out" future changes in interest rates.

Concerns were raised about the "narrow path" to bringing inflation back to target within a reasonable timeframe without significantly deviating from full employment. This path, according to the minutes, is "becoming narrower."

The decision to keep the cash rate target unchanged at 4.35% was deemed the stronger option compared to another rate hike. Data received since May meeting "had not been sufficient" to alter RBA's assessment that inflation would return to target by 2026, despite "some elevated upside risk" surrounding the forecast. Moreover, the minutes revealed that the members felt there was "not enough evidence" to suggest that the outlook for aggregate demand had strengthened.

(RBA) Minutes of the Monetary Policy Meeting of the Reserve Bank Board

Hybrid – 17 and 18 June 2024

Members participating

Michele Bullock (Governor and Chair), Andrew Hauser (Deputy Governor), Ian Harper AO, Carolyn Hewson AO, Steven Kennedy PSM, Iain Ross AO, Elana Rubin AM, Carol Schwartz AO, Alison Watkins AM

Others participating

Sarah Hunter (Assistant Governor, Economic), Christopher Kent (Assistant Governor, Financial Markets), James Holloway (Deputy Head, Economic Analysis Department)

Anthony Dickman (Secretary), David Norman (Deputy Secretary)

Meredith Beechey Osterholm (Future Hub), Sally Cray (Chief Communications Officer), Marion Kohler (Head, Economic Analysis Department), Carl Schwartz (Acting Head, Domestic Markets Department), Penelope Smith (Head, International Department)

International economic conditions

Members began their discussion of international economic developments by noting that recent data had confirmed that output growth in most advanced economies had troughed and that upside risks might be crystallising in some regions. Forecasters had revised up their expectations for growth in advanced economies for the current year, reflecting stronger-than-expected data for the March quarter amid improving global business sentiment. Nonetheless, restrictive monetary policy was still weighing on demand in most advanced economies and conditions in labour markets were also easing, although generally they remained tight.

Members observed that inflation was still above central bank targets in most economies, and services price inflation had generally been stronger than expected since the start of the year. However, in some economies where output gaps were clearly negative, such as Canada and Sweden, services price inflation had continued to moderate.

Indicators of activity for the Chinese economy had softened a little following strong growth in the March quarter, but the staff's outlook for growth in 2024 had not changed. China's external demand remained strong and was being supported by the nascent recovery in activity in advanced economies. Members observed that the recent announcement of new US and EU tariffs on some Chinese imports was further evidence of the increasing risk of broader trade tensions.

Domestic economic conditions

Turning to the domestic economy, members discussed the national accounts data for the March quarter. They noted the staff's assessment that aggregate demand had continued to exceed aggregate supply but that the gap was closing. Growth in GDP had been weak, reflecting subdued activity in the more interest rate-sensitive parts of the economy, such as retail spending and housing construction. Relative to expectations, growth in overall household and public consumption in the March quarter had been stronger than expected while other components had surprised on the downside. Members considered the implications for future growth of developments in these components.

The level of consumer spending over the preceding 18 months had been revised upwards. Much of the upside surprise had been driven by large revisions to overseas travel, which were recorded as imports and so did not alter the measure of overall GDP. Estimates of household income had been little changed, implying downward revisions to estimates of the saving rate. These revisions had brought consumption growth more into line with the usual historical relationships with household income and wealth. Members assessed the signal to take from these revisions. One interpretation was that, on average, households were not being as cautious in their spending as previously thought. Another was that the fall in the saving rate would leave households even more financially squeezed than previously assessed. Members agreed that distinguishing between these alternative hypotheses was important in assessing the outlook for activity and inflation. But any conclusion could only be tentative, given that estimates of savings are prone to significant revision. Further, the latest estimates portrayed a different picture than that derived from data on mortgage-holders' offset accounts, which showed that households were making larger extra payments than prior to the pandemic.

Since the previous meeting, a number of Australian governments had released their budgets for 2024/25. Energy rebates and rent assistance would lower headline inflation in 2024, though this direct effect would be reversed later in 2025. Members noted that the staff would incorporate an assessment of the impact of the budgets on the outlook for output and inflation in the August forecasting round.

The labour market was still assessed as tight relative to full employment, though conditions had continued to ease gradually in recent months as expected. The easing in the labour market since late 2022 had occurred through an increase in the unemployment rate, a decline in average hours worked and fewer job vacancies. Employment growth had slowed over this period to be around the pace of growth in the working-age population. Recent employment growth had been supported by growth in industries where public funding was important.

Members noted that wages growth had likely passed its peak for the current cycle. The easing in wages growth over the year to the March quarter had been broadly based, but outcomes in public and private enterprise bargaining agreements had been a little below expectations. Nonetheless, it was too early to determine if this signalled a more rapid easing in aggregate wages growth than currently expected. The Fair Work Commission's decision on award wages, which had been largely in line with expectations, would see award-linked wages growth step down this year. The implication of wages growth for inflation depended on its effect on unit labour costs, growth in which had moderated recently but remained high.

Members discussed recent information from the RBA's liaison program. Firms were continuing to report upward pressure on costs, stemming from a range of sources. At the same time, firms in consumer-facing industries were reporting that it was becoming more difficult to raise prices, resulting in a narrowing of margins. Members noted that businesses appeared to be more focused on improving efficiency than they had been for some time, but obtaining internal approval for investments to automate processes was sometimes difficult as firms continued to look for ways to manage cashflow. They also noted the data showing a sharp increase in business insolvencies, although the share of firms entering bankruptcy remained in line with its historical average.

Inflation remained above the target range and had been a little higher than expected in prior months. The monthly CPI indicator for April had exceeded expectations because of stronger-than-expected durable goods price inflation. However, there had been limited information about market services price inflation since the May meeting. Members acknowledged that these (limited) inflation data had increased the risk that sustainable progress towards the inflation target may be slower than forecast.

Members judged that longer term inflation expectations in Australia were still anchored but should continue to be monitored closely. Several measures of inflation expectations had drifted up in recent years to be around the midpoint of the target band, after having been below target during the low-inflation period prior to the pandemic. Part of the increase in market-implied measures of inflation compensation over preceding years appeared to reflect larger premia to compensate for the risk that inflation turned out to be higher than expected. Members acknowledged that if inflation expectations were to rise materially from current levels, it could require significantly higher interest rates to bring inflation back to target, with adverse implications for growth in output and employment.

Financial conditions

Market participants' expectations for the path of central bank policy rates in advanced economies were little changed since the May meeting, after increasing steadily in the first few months of the year. Market participants' implied expectation continued to be that policy rates for most major central banks were around their peak, with cuts priced in over the second half of 2024. As expected, the Bank of Canada, the European Central Bank and Sveriges Riksbank had reduced their policy rates in response to weaker-than-expected indicators of economic activity, the emergence of spare capacity and progress on disinflation. However, these central banks had stated that they judged their monetary policy settings still to be restrictive and may need to remain so for some time. Other advanced economy central banks were waiting for more evidence that inflation would return to target sustainably. In particular, the US Federal Reserve had highlighted the persistence of inflation, resilient economic activity and ongoing labour market tightness.

Sovereign bond yields in most advanced economies had declined a little since the May meeting. But yields were still higher than at the start of the year and when central banks had commenced raising policy rates. At the same time, some measures of global financial conditions had eased since late 2023. A range of risk asset prices, including equity prices, had risen further. Corporate bond yields had also risen by less than government bond yields since the start of the year, and conditions in international wholesale funding markets remained favourable. Members noted the volatility in European financial markets that had occurred following the European parliamentary elections.

In China, credit growth had moderated, particularly for the household sector, against the backdrop of ongoing stress for property developers. The authorities had implemented new measures to address weakness in the property sector, including by providing funding to allow state-owned enterprises to purchase unsold homes from developers. Members noted assessments that these measures would provide helpful support to the property market but were not sufficiently large to affect prospects for the sector materially.

For Australia, members concluded that overall financial conditions were restrictive, based on a range of measures. This was most notable for households and less so for large businesses.

Required household debt payments had risen further. The rise in these payments had put pressure on the budgets of debtors and had contributed to the weakness in consumption growth. Despite the drag on income from cost-of-living pressures and higher required debt payments, extra mortgage payments were now a little above their pre-pandemic average. This is consistent with the incentive for debtors to reduce their net debts where possible when interest rates are high. Members acknowledged, alternatively, that this could reflect concerns about the economic outlook. By contrast, the (gross) saving rate had declined to be around 2½ percentage points below its pre-pandemic average, following substantial revisions to consumption in the March quarter national accounts. Members discussed how the fall in the measured saving rate and the rise in extra mortgage payments might be reconciled.

Household credit growth was somewhat below average but had picked up a little in 2024. After accounting for the extra payments into offset accounts, housing credit growth had been further below average and had not picked up. Moreover, household credit outstanding had been declining as a share of household disposable income. By contrast, business credit growth had remained a little above its post-global financial crisis average and larger firms had continued to raise significant funds from bond markets this year, despite materially higher interest rates.

Market pricing implied that markets were not expecting a near-term change in the cash rate, having earlier priced in some prospect of an increase. A rate cut was now not fully priced in until March 2025. The median expectation of market economists was also for the first reduction in the cash rate to occur in March 2025, about three months later than expected at the time of the previous meeting. Further ahead, market pricing implied that the cash rate was expected to converge to a similar level to the policy rates in many other advanced economies in coming years. The expectation by market participants of later and fewer cuts than in other advanced economies might have reflected their assessment that the cash rate was closer to estimates of the neutral rate, in large part because the cash rate had not been increased to the same extent in Australia.

The Australian dollar had appreciated slightly since the May meeting and, on a trade-weighted basis, was near the top of the range observed since early 2022.

Considerations for monetary policy

Turning to considerations for the policy decision, members noted that there had been several pieces of information since the May meeting that indicated a need to remain alert to upside risks to inflation.

There had been further evidence that global growth had troughed in late 2023 and was gradually picking up, while disinflation had slowed in several countries. In Australia, inflation had also been higher than expected in April. And the revisions to historical estimates of consumer spending meant that consumption growth, while still weak, had been more resilient than previously assessed.

Against this, members noted that GDP growth in Australia in the March quarter had been very weak and slightly lower than had been expected. There had also been further evidence that wages growth had likely peaked in late 2023. The labour market was continuing to ease gradually, broadly in line with expectations.

Members noted that, despite restrictive financial conditions overall in Australia, growth in business debt had been a little above its post-global financial crisis average and the equity risk premium was low. A few other central banks had moved to a less restrictive policy stance by reducing their policy rates, while others were waiting for more evidence that inflation would return to target sustainably before easing.

Members discussed the evolution of some key judgements relative to those underpinning the staff's forecasts in May. They noted that, on one view, the revisions to historical estimates of consumption challenged the earlier judgement that consumer spending would pick up only modestly as aggregate real disposable income recovered. At the same time, it was possible to interpret the revisions as implying that households were under more financial pressure than previously assessed, given the decline in the saving rate. Members noted that the August forecast round would provide an opportunity for the staff to carefully review the extent of spare capacity in the labour market and the economy more broadly. They observed that judgements about measures of spare capacity were very uncertain and should be treated with caution when setting policy. And while monetary policy was restrictive, an important judgement was whether policy settings were sufficiently restrictive to return inflation to target within the timeframe implicit in the Board's strategy.

Given these observations, members considered their decision on the cash rate.

Raising the cash rate at this meeting could be appropriate if members formed the view that policy settings were not sufficiently restrictive to return inflation to target within a reasonable timeframe. This could be the case if it was judged that inflation was returning to target more slowly than previously assumed or that the gap between aggregate demand and aggregate supply was not closing quickly enough.

Members noted that several pieces of new information could imply that demand was likely to hold up better than expected. The staff's forecasts from May had incorporated significantly more weakness in consumption than implied by historical relationships with the forecasts for income and wealth; the revisions to the consumption profile had brought these variables into closer alignment over the prior 18 months. A gradual strengthening of the global economic cycle would also support demand in Australia. And financial conditions for businesses appeared to have eased a little over preceding months for some larger businesses. Collectively, these developments could limit the extent to which current policy settings were sufficient to bring aggregate demand back into line with aggregate supply. Moreover, recent inflation data – both domestically and from abroad – suggested some upside risk to the May forecast profile, since inflation was taking longer to abate than had previously been assumed. Members observed that the forecasts of several other central banks could be interpreted as implying that some spare capacity was necessary to bring inflation back to target within a reasonable timeframe, but that this was not the approach that had been adopted by the Board.

The case to raise the cash rate could be further strengthened if members judged that aggregate supply was likely to be more constrained than had been assumed. Members noted that productivity growth remained very weak. And while inflation expectations were judged to be consistent with the inflation target, the increase in the market-implied risk premium suggested a higher risk of an increase in inflation expectations more widely.

By contrast, the case to hold the cash rate steady at this meeting was based on the view that the economy was still broadly tracking on a path consistent with returning inflation to target in 2026, while preserving as many of the gains in employment as possible. Inflation had fallen significantly from its peak in late 2022, inflation expectations were assessed to be consistent with the Board's target and there was evidence that the pace of wages growth had peaked in late 2023. Output growth had continued to be weak and the output gap was closing. Members also acknowledged that it might be wise to give little weight to the signal for inflation from some pieces of information received since the May meeting. In particular, there were several reasons not to place too much weight on the revisions to consumption, including that much of the upside surprise had been related to imports, and it was extremely difficult to assess spare capacity accurately in real time.

The case to hold the cash rate steady at this meeting would also be strengthened to the extent that risks to the outlook for the labour market were seen to be to the downside. Members observed that the fall in vacancy rates, for example, could be taken as an indication that labour market conditions were already weaker than implied by trends in employment. Moreover, the unemployment rate could rise quickly once it did start to rise, as had occurred in the past. Members acknowledged that, while the current rate of business failures as a share of all businesses was not unusual, a continuation of the rapid rise in insolvencies over coming months would have adverse implications for labour demand.

In weighing up these options, members judged that the case to leave the cash rate unchanged at this meeting was the stronger one. Members agreed that the collective data received since the May meeting had not been sufficient to change their assessment that inflation would return to target by 2026, despite some elevated upside risk around the forecast. In addition, members judged that there had not been enough evidence that the outlook for aggregate demand had strengthened, noting uncertainty around the data for consumption and clear evidence that many households were experiencing financial stress. Members also affirmed their assessment that it was still possible to achieve the Board's strategy of returning inflation to target in a reasonable timeframe without moving away significantly from full employment, even though this 'narrow path' was becoming narrower. With economic uncertainty heightened at present, members emphasised the importance of paying close attention to developments in the economic data.

In finalising the Board's statement, members agreed that it was important to convey that the information received since the previous meeting had reinforced the need to be vigilant to upside risks to inflation, and that the extent of uncertainty at present meant it was difficult either to rule in or rule out future changes in the cash rate target. The Board will continue to pay close attention to developments in the global economy, trends in domestic demand, and the outlook for inflation and the labour market. Returning inflation to target remains the Board's highest priority and it will do what is necessary to achieve that outcome.

The decision

The Board decided to leave the cash rate target unchanged at 4.35 per cent, and the interest rate on Exchange Settlement balances unchanged at 4.25 per cent.

NZIER survey shows rising pessimism among New Zealand firms

The NZIER Quarterly Survey of Business Opinion for Q2 reveals increasing pessimism among New Zealand firms. A net 44% of firms are now pessimistic about the economy's outlook over the next six months, up from 25% in Q1. Additionally, a net 28% reported a deterioration in their own trading during the three months through March, marking the weakest reading since mid-2020 during the COVID-19 pandemic.

Employment figures are equally concerning. A net 25% of firms laid off workers in Q2, the highest level since the global financial crisis in 2009. Furthermore, a net 10% expect to reduce staff numbers in the three months through September. Profit expectations are also bleak, with a net 34% of firms anticipating weaker profits in the third quarter, accompanied by falling investment intentions.

On a slightly more positive note, only a net 23% of firms expect to increase prices in Q3, the lowest since 2021. Additionally, companies are finding it easier to recruit workers, signaling reduced wage pressure. Fewer companies also reported rising costs, suggesting some relief from inflationary pressures.

NZ First Impressions: NZIER Survey of Business Opinion, Q2 2024

Business activity measures remained weak in June, while the inflation gauges are steadily heading in the right direction.

Key results (seasonally adjusted):

- General business confidence: -35.4 (Previous: -24.9)

- Trading activity, past three months: -27.8 (Previous: -24.2)

- Trading activity, next three months: -10.4 (Previous: -12.3)

- % reporting a rise in operating costs over the past 3 months: 41.3 (Previous: 52.0)

- % who increased output prices over the past 3 months: 22.4 (Previous: 33.4)

Businesses remained downbeat on their prospects and the wider economy in the June quarter survey of business opinion. Meanwhile, the measures of cost and price pressures suggest that inflation will continue to recede from its highs, though no faster or slower than the Reserve Bank would have expected.

A net 35% of firms were negative on the outlook for the economy in the June quarter, compared to a net 25% in March. While this is a very weak reading compared to history, it’s still higher than it was last year; this measure of business sentiment hasn’t fully given back its post-election bounce.

Firms’ views on their own activity were mixed compared to the March quarter, with past performance slightly weaker but expectations slightly higher. These measures tend to have a closer correspondence with GDP and are consistent with growth remaining somewhere either side of zero.

Other indicators of activity were generally weaker in June. Notably, the labour shortage has become a distant memory: workers have become much easier to find, and indeed on balance firms said that they were rapidly shedding workers in the last quarter.

One positive aspect of the survey is that the inflation indicators have continued to head in the direction that the RBNZ would have hoped. A net 41% of firms reported cost increases over the last three months, down from 52% last quarter and a peak of 80% at the end of 2022. There were similar falls in firms’ past and expected pricing.

These measures are consistent with inflation falling below 3% before the end of this year, though they’re still higher than what has historically been consistent with the 2% target. That direction of progress will be welcomed by the RBNZ. However, it doesn’t indicate that inflation is coming off any faster or slower than we or the RBNZ have been forecasting.

Our view for some time has been that the RBNZ will begin reducing the OCR from February next year – much earlier than the RBNZ’s own projections of a start somewhere in Q3 next year. Today’s survey is in line with our view. We’ll be publishing our OCR preview later this week, detailing what we expect the policy committee to conclude after its 10 July meeting.

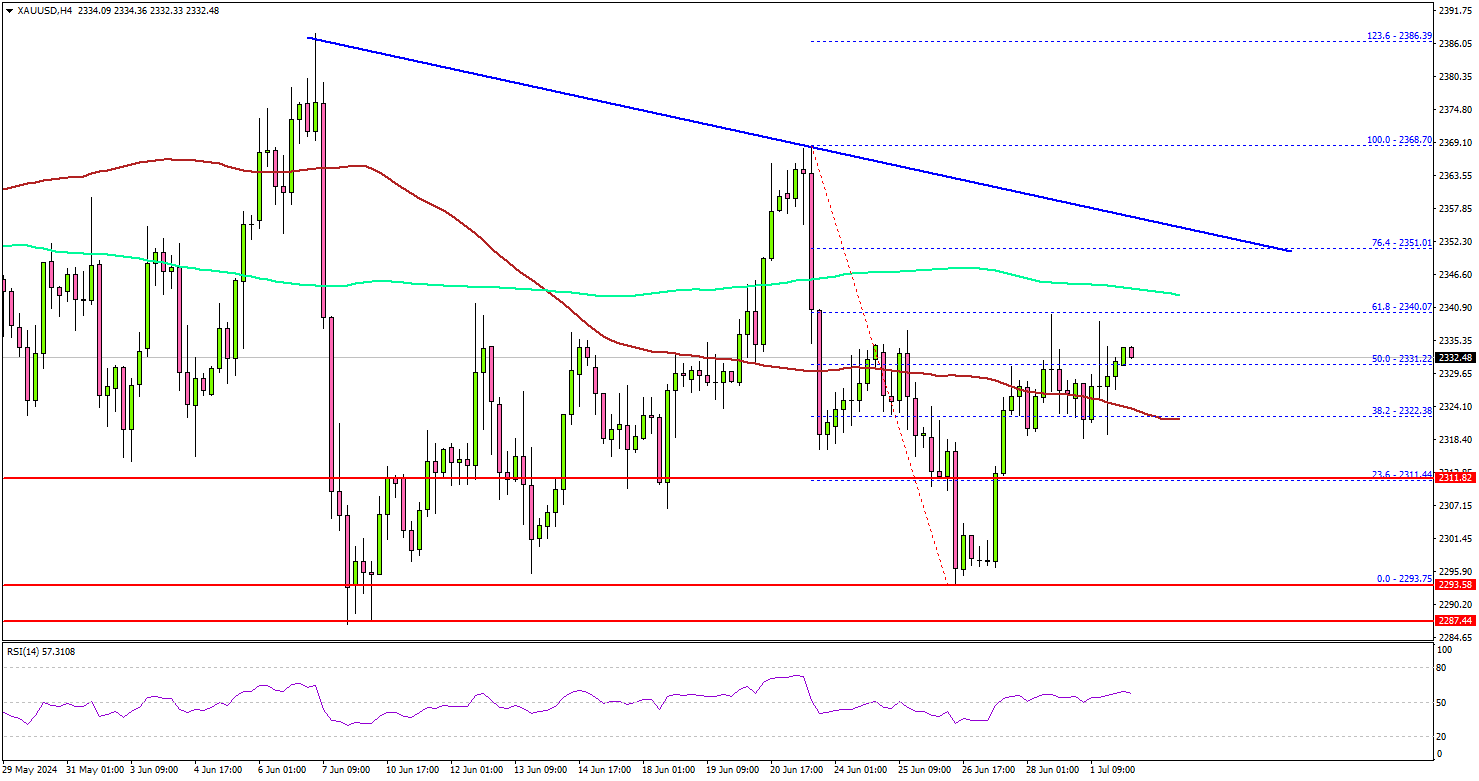

Gold Bulls on Shaky Ground: Key Obstacles Ahead

Key Highlights

- Gold is attempting a fresh increase from the $2,292 support zone.

- A major bearish trend line is forming with resistance at $2,355 on the 4-hour chart.

- EUR/USD could gain bullish momentum if it clears the 1.0780 resistance.

- Oil prices might continue to move up toward the $85.00 resistance.

Gold Price Technical Analysis

Gold prices remained well-bid above the $2,292 zone against the US Dollar. The bulls took control and were able to push the price above the $2,310 and $2,315 levels.

The 4-hour chart of XAU/USD indicates that the price climbed above the $2,325 resistance and the 100 Simple Moving Average (red, 4 hours). It even spiked above the 50% Fib retracement level of the downward move from the $2,368 swing high to the $2,293 low.

However, the bulls seem to be facing many hurdles. Immediate resistance is near the $2,340 level. The first major resistance is near the $2,345 level and the 200 Simple Moving Average (green, 4 hours).

The main resistance sits at $2,355 and the 76.4% Fib retracement level of the downward move from the $2,368 swing high to the $2,293 low. There is also a major bearish trend line forming with resistance at $2,355 on the same chart.

A clear move above the trend line resistance could open the doors for a steady increase. The next major resistance is now near $2,368, above which the price could accelerate higher toward the $2,380 level. Any more gains might send Gold toward the $2,388 resistance.

On the downside, there is a key support forming near the $2,310 level. A downside break below the $2,310 support might call for more downsides. The next major support is near the $2,292 level. Any more losses might send Gold prices toward $2,265.

Looking at Oil, the bulls were able to push the price above the $82.00 resistance and they could aim for more upsides.

Economic Releases to Watch Today

- Federal Reserve Chair Jerome Powell’s speech.

- ECB's President Lagarde speech.

ECB’s Lagarde: No rush for further rate cuts as data-dependent approach prevails

At the ECB Forum on Central Banking overnight, ECB President Christine Lagarde hinted that the central bank is not in a hurry to cut interest rates again following its initial rate cut in June.

She highlighted that the central bank is facing "several uncertainties" concerning future inflation. These uncertainties primarily revolve around the dynamics of profits, wages, and productivity, and the potential impact of new supply-side shocks.

Lagarde emphasized that it will take time to accumulate sufficient data to be confident that the "risks of above-target inflation have passed."

The "strong labor market" was noted as a positive factor, allowing the ECB to "take time" to gather more information before making further decisions. However, Lagarde also acknowledged that "growth outlook remains uncertain," indicating that the ECB must remain vigilant and adaptable to changing economic conditions.

She reiterated, "All of this underpins our determination to be data-dependent and to take our policy decisions meeting by meeting."