Sample Category Title

Australian Dollar Eyes Retail Sales

The Australian dollar has posted slight losses on Tuesday. AUD/USD is trading at 0.6649 in the European session, down 0.15% on the day.

Australian retail sales expected to improve

Australian consumers have been in frugal mood and have reduced their discretionary spending. Consumers have been squeezed by high borrowing costs and the high cost of living. Retail sales ticked upwards by only 0.1% m/m in April. The gain was negligible, considering that Australia’s population has been swelling due to an increase in immigration. The May retail sales report on Wednesday is expected to show some improvement, with a market estimate of 0.3% m/m.

RBA minutes: higher rates could be needed

The RBA minutes from the meeting earlier this month noted that the Board decided that the case to hold rates was stronger than for hiking. The RBA held rates at 4.35% for a fifth straight time but the Board raised concerns about the rise in inflation expectations and warned that it might have to raise rates if the current policy was not “sufficiently restrictive”.

The takeaway is that the RBA won’t be abandoning its “higher for longer” stance anytime soon. The second-quarter inflation report will be released on July 31 and will be a key factor in the RBA’s rate decision a week later.

The weak Australian economy could use a rate cut but the Reserve Bank of Australia is handcuffed due to rising inflation, particularly service inflation. CPI jumped to 4.0% in May, up from 3.6% in April and higher than the market estimate of 3.8%. The RBA may have to delay an initial rate cut until 2025 if there is no significant progress in the battle against inflation.

The RBA’s target range is 2% to 3% and the final phase of bringing inflation back down to the target range has proven elusive despite high interest rates. There is a real possibility that the RBA could raise rates in order to dampen inflation, a specter that consumers and businesses hope does not materialize.

AUD/USD Technical

AUD/USD tested resistance at 0.6660 earlier. Above, there is resistance at 0.6699

0.6630 and 0.6591 are the next support levels

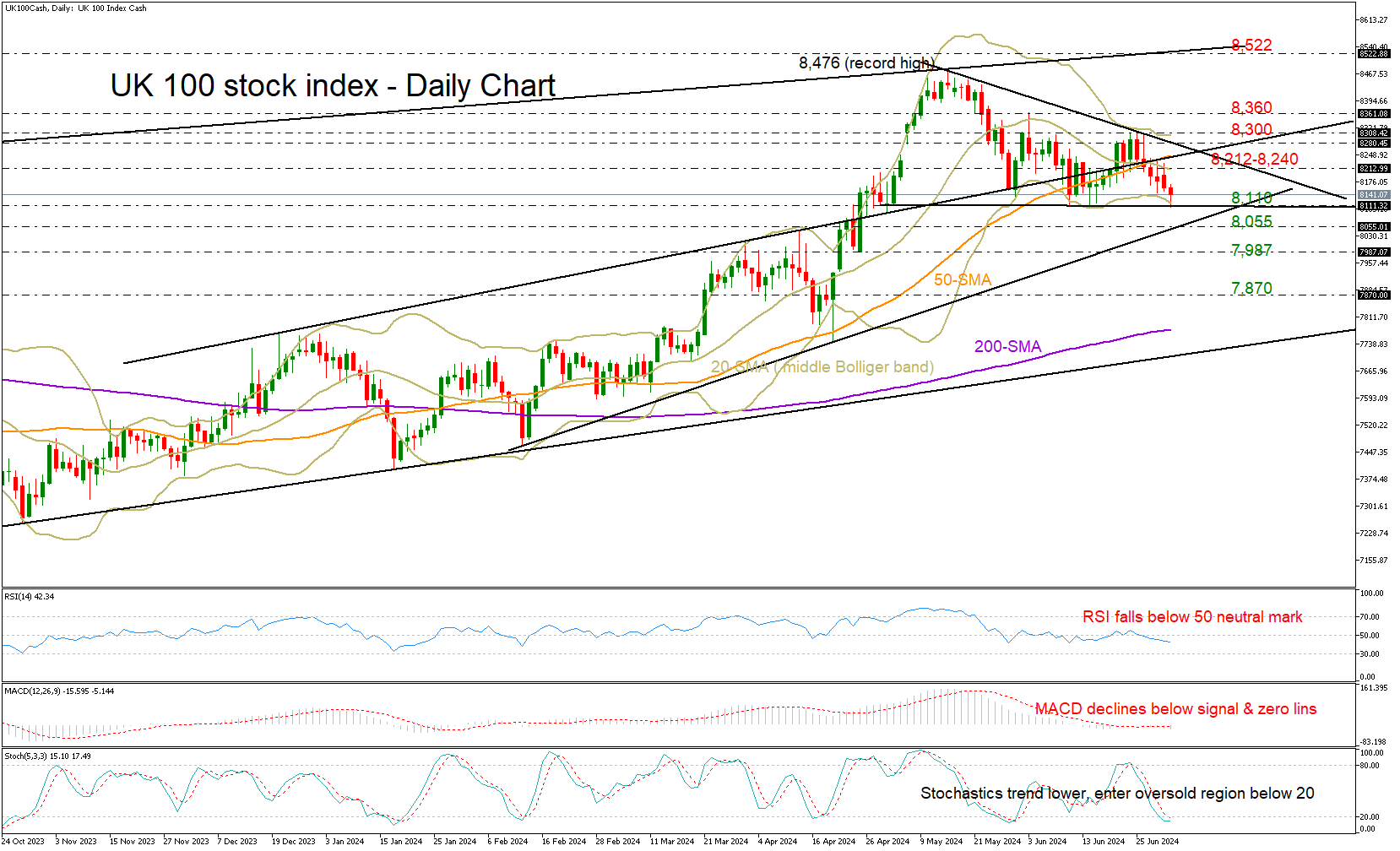

UK 100 Index Experiences Pre-election Decline

- UK 100 index erases June’s recovery attempt as the UK election looms

- A break below 8,055 could worsen short-term outlook

The UK 100 stock index (cash) continues to suffer for the sixth consecutive trading day, extending its downleg aggressively to the critical support zone of 8,110 on Tuesday ahead of the election day on July 4.

The index could not mark a new higher high above the key resistance area of 8,300 and the important resistance line from February 2022, increasing fears that the negative reversal from the 8,476 record high could gain more legs.

Discouragingly, the 20- and 50-day simple moving averages (SMAs) have already posted a bearish cross, promoting the case of a bearish continuation. In addition to this, the RSI is currently losing ground below its 50 neutral mark and the MACD is diminishing below its zero and signal lines, both reflecting a clear bearish bias.

A step below the base of 8,110 could dampen market sentiment, but traders may not rush to sell the index until the price drops decisively below the ascending trendline at 8,055. Note that the stochastic oscillator is already within the oversold region, while the price itself is hovering near the lower Bollinger band. Hence, a pause in the ongoing bearish phase is likely. Yet, if the bears claim the 8,055 area, the next stop could be around April’s constraining region of 7,987, a break of which could cause a sharper downfall towards the 7,870 zone.

On the upside, the bulls must exit the triangle and knock down the wall at 8,300 in order to boost buying appetite towards the 8,360-8,400 barrier, but before that, they should first claim the 20- and 50-day SMAs at 8,212 and 8,245 respectively. Long-term traders might wait for a bullish trend extension above the crucial resistance line at 8,522 before driving towards the 8,600 psychological mark.

In summary, the UK 100 stock index is holding a bearish bias in the short-term picture, but selling interest could stay balanced until the price slides below 8,055.

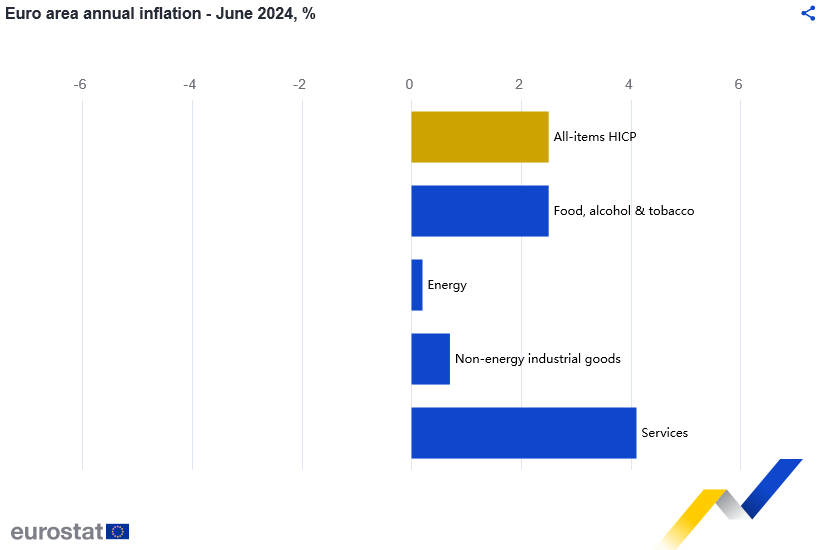

Eurozone CPI slowed to 2.5% in Jun, but core unchanged at 2.9%

Eurozone CPI slowed from 2.6% yoy to 2.5% yoy in June, matched expectations. CPI core (ex-energy, food, alcohol & tobacco) was unchanged at 2.9% yoy, above expectation of 2.8% yoy.

Looking at the main components, services is expected to have the highest annual rate in June (4.1%, stable compared with May), followed by food, alcohol & tobacco (2.5%, compared with 2.6% in May), non-energy industrial goods (0.7%, stable compared with May) and energy (0.2%, compared with 0.3% in May).

Full Eurozone CPI release here.

Silver Price Analysis: Awaiting Powell’s Comments

Today, at 16:30 GMT+3, the Federal Reserve Chairman is scheduled to speak. Market participants are looking for more clarity on the Fed's plans regarding interest rate cuts following the release of inflation data last Friday.

According to Trading Economics, Fed officials have repeatedly called for caution before cutting rates, and Federal Reserve Board member Michelle Bowman stated that she is open to further rate hikes if progress in combating inflation stalls or reverses.

Powell's speech will significantly impact many financial markets, including the precious metals market, as lowering interest rates could increase the appeal of gold and silver as "safe haven" assets compared to bonds.

It is important to note that besides the Fed's monetary policy, the XAG/USD price is significantly influenced by news about the Chinese economy – the largest consumer of silver. The demand outlook remains uncertain, considering that official data for June indicated a second consecutive month of production decline.

Technical analysis of the XAG/USD chart provides more useful information:

→ Silver prices were in an upward trend (indicated by a blue channel), peaking at a multi-year high reached in late May above the $31 per ounce level.

→ The ATR indicator pointed to increased activity during those days. It is likely that major players used the buoyant market, supported by optimistic news, to close long positions.

→ Regardless, silver prices have since started forming a downward trend (indicated by a red colour). The $31 level has shown signs of resistance, and the lower boundary of the blue channel has been broken.

→ The $28.75 level (former resistance) is now showing signs of support.

It is possible that the broad range of $28.75 - $31.00 will become a zone where the silver price finds equilibrium, resilient to various influencing factors, including today's speech by Powell. Be prepared for volatility spikes.

Start trading commodity CFDs with tight spreads. Open your trading account now or learn more about trading commodity CFDs with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

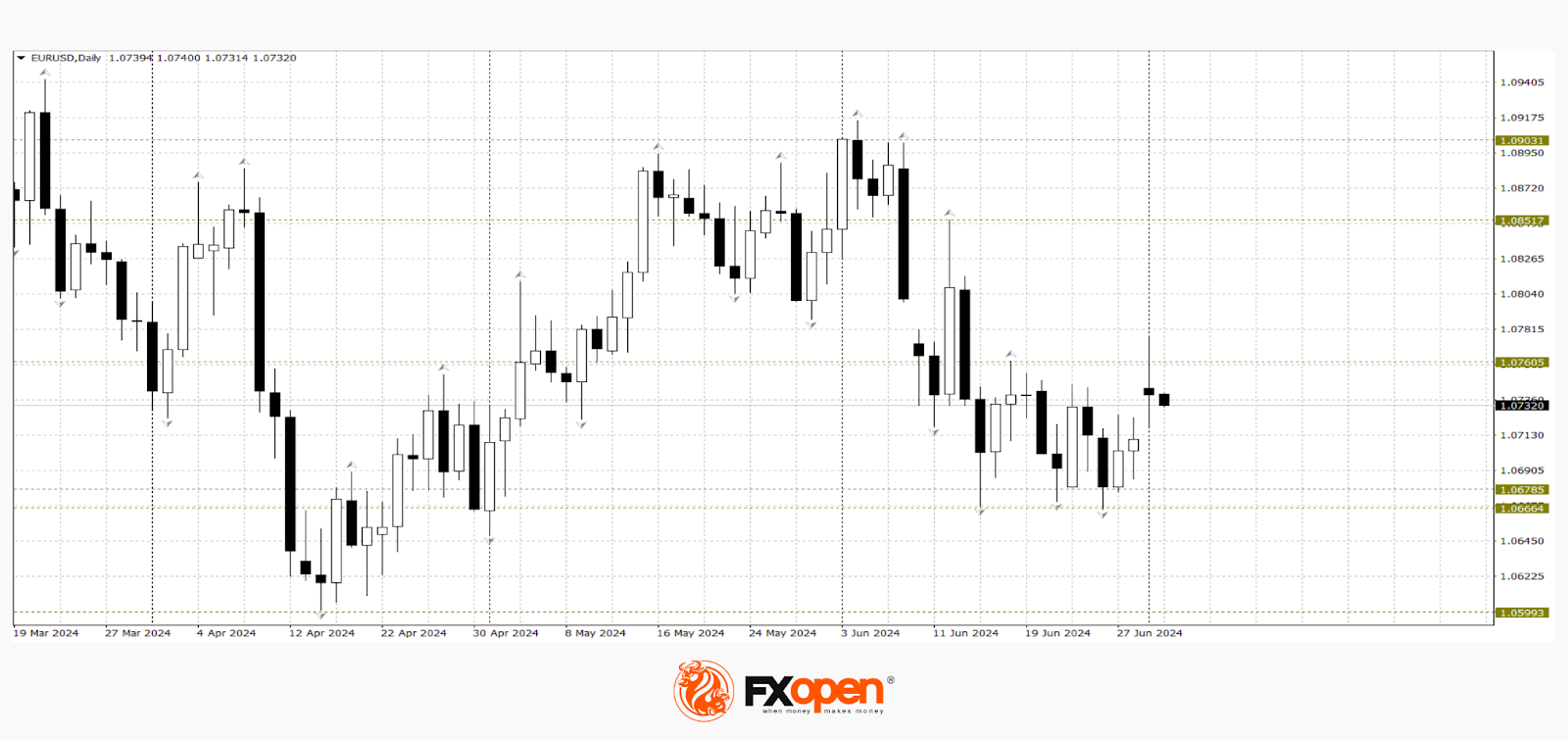

EUR/USD Struggles to Maintain Gains Amid Mixed Economic Signals

The EUR/USD pair experienced a noticeable uptick yesterday, but failed to sustain its peak, settling at 1.0732 today. Early gains were buoyed by the initial outcomes from France's parliamentary elections, which did not reflect the worst-case scenario, sparking a temporary surge in risk appetite and bolstering the euro.

However, last evening's economic indicators from the U.S. painted a mixed picture, dampening the initial enthusiasm. The ISM Manufacturing Index for June dipped to 48.5 from 48.7, falling short of expectations and remaining below the pivotal 50-point mark that delineates expansion from contraction. Conversely, Markit's Manufacturing PMI indicated a slight improvement, rising to 51.6 from 51.3.

Additionally, a report showed a 0.1% month-on-month decline in U.S. construction spending for May, a reversal from the previous increase of 0.3% and weaker than anticipated, suggesting a potential slowdown in the construction sector and broader economic support.

Market participants are now turning their attention to an upcoming speech by Jerome Powell, Chair of the Federal Reserve, for further clues on the direction of U.S. monetary policy.

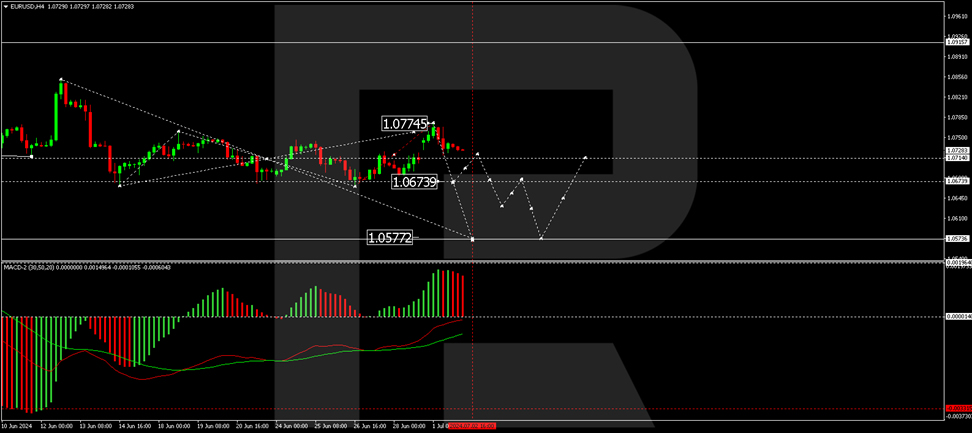

Technical analysis of EUR/USD

The EUR/USD pair completed a correction to 1.0774 but is now forming a declining wave towards 1.0675. Should this level be reached, a minor correction to 1.0714 may occur before a potential further drop to 1.0630, and potentially extending down to 1.0573. The MACD indicator underlines this bearish outlook with its signal line positioned below zero and histograms trending downwards.

On the hourly chart, the pair is currently crafting a declining structure with an initial target at 1.0675. Following this, a correction towards 1.0714 is plausible, before a continuation of the downtrend to 1.0640. The Stochastic oscillator corroborates this view, with its signal line approaching the 20 level, indicating a potential for further declines before a rebound towards 50 might occur.

Market outlook

Investors will continue to assess the blend of economic data and central bank signals, particularly from the Fed, to gauge the potential trajectory of interest rates and their impact on currency valuations. Today's speech by Jerome Powell could be particularly pivotal in setting market expectations moving forward.

Pound and Euro Test Key Support Levels: Is a Breakout Possible?

European currencies are showing surprising resilience. Despite the general strengthening of the dollar and strong macroeconomic data from the US, EUR/USD and GBP/USD continue to trade above strategically important levels:

- EUR/USD has been testing 1.0660 for over three weeks but cannot establish itself below this level.

- GBP/USD buyers have been holding off sellers for a second week at the 1.2610-1.2600 level.

EUR/USD

The recent parliamentary elections in France, with the first round concluding last Sunday, have contributed to a slight strengthening of the euro. The pair opened with a small price gap and managed to strengthen by over 60 pips within a few hours. Experts attribute the rise in the single European currency to the possibility that Le Pen's far-right party might outpace President Emmanuel Macron's centrist alliance and the left-wing "New People's Front" with fewer votes than needed for an absolute majority after the second and final round of voting.

Technical analysis of the EUR/USD pair indicates continued range-bound trading between 1.0760-1.0660. A breakout and consolidation above 1.0760 could lead to a renewed rise towards 1.0900-1.0850. Breaking the three-week support at 1.0660 could result in a retest of the April low this year at 1.0590.

Events that could impact the pair's pricing include:

- Today at 12:00 (GMT+3): Eurozone core Consumer Price Index (CPI) for June

- Today at 13:30 (GMT+3): Speech by European Central Bank (ECB) representative Elizabeth Schnabel

- Today at 16:30 (GMT+3): Speech by US Federal Reserve Chairman Jerome Powell

GBP/USD

For the second week, the GBP/USD currency pair is trading within a relatively narrow 100-pip range, which is unusual for it. Yesterday, the price surged sharply to 1.2700 but just as sharply fell, closing the day with a candle featuring a long upper shadow, which may indicate weakness among pound buyers. According to technical analysis of the GBP/USD pair, a break below 1.2600 could renew the downward trend towards 1.2560-1.2450. The bearish scenario could be nullified if the price confidently consolidates above 1.2700.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

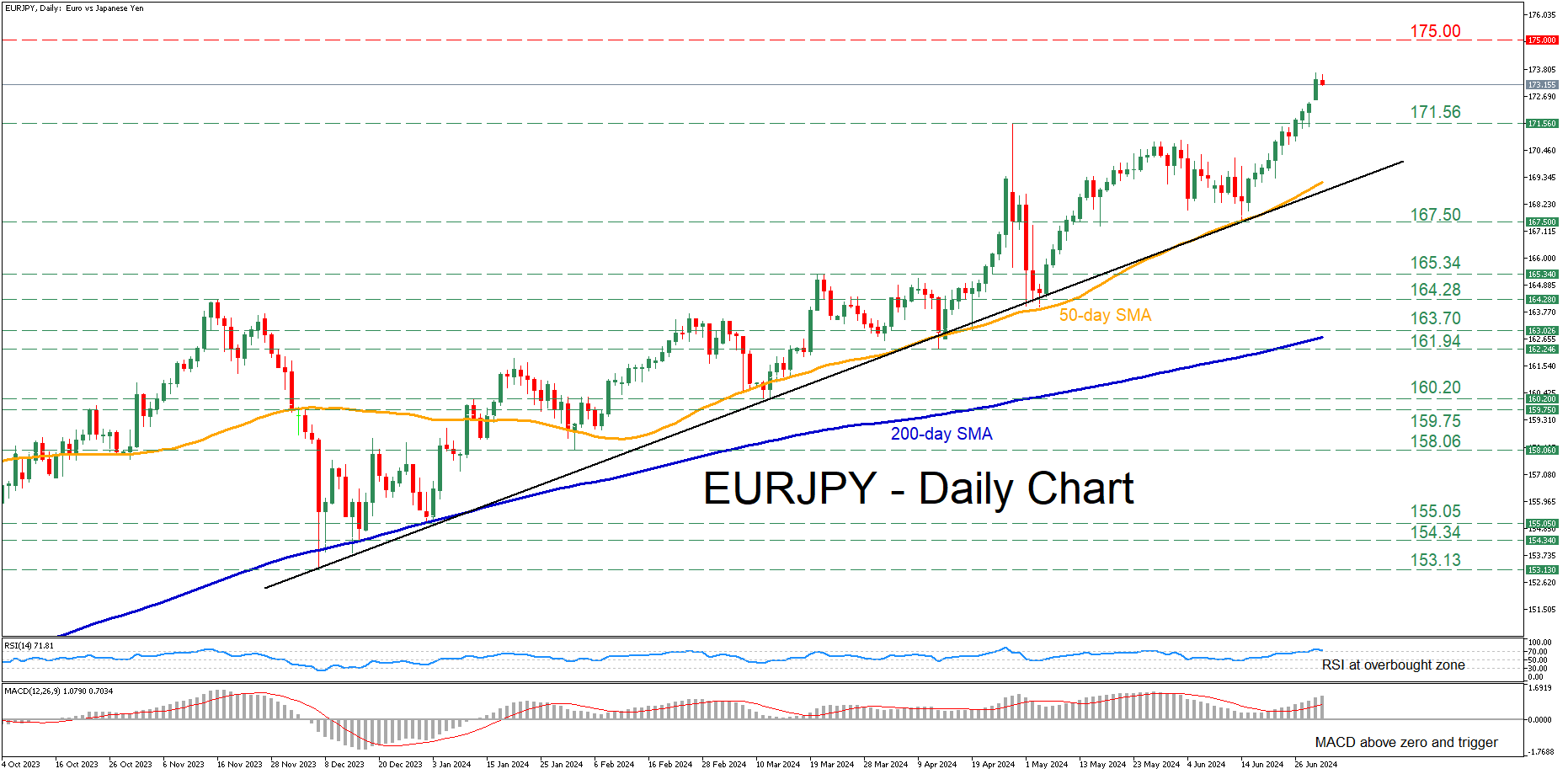

EURJPY Sails in Uncharted Waters

- EURJPY advances above 32-year high

- Fears of a Japanese intervention increase

- Oscillators point to overbought conditions

EURJPY has been in an uptrend since the beginning of the year, storming to consecutive multi-year highs. Despite a strong pullback following a currency intervention from Japan in late April, the market has been steadily moving higher above levels that the Japanese authorities were willing to protect.

Should the upward trajectory resume, the pair could meet resistance at psychological levels such as 175.00 or 180.00 last observed in 1992.

On the flipside, if the pair experiences a pullback, initial support could be found at the April peak of 171.56. Lower, the June support of 167.50 could prevent further declines. A break below that zone could trigger a retreat towards 165.34 ahead of 164.28, two previous resistance regions that could serve as support in the future.

In brief, EURJPY has been on the rise, constantly defying overbought signals. Will the Japanese side intervene?

ECB’s Lane highlights need for more data on services inflation

ECB Chief Economist Philip Lane emphasized today that June inflation data alone will not suffice to address questions surrounding services inflation, suggesting the ECB may delay further interest rate cuts until additional data is available.

Lane noted, "The key is really services inflation. What we've seen in the last days is that services inflation remains the outlier, and what we need to see is whether higher services inflation is a backward element and is a legacy of the rapid disinflation or is it a persistent element. We need time to work on it."

On the political front, Lane downplayed concerns about France's recent political turmoil impacting markets significantly, stating, "It is clearly natural in an election for the market to reprice. There are elections all the time, there are movements in spreads all the time. Of course, France is an important country, but this looks like an ordinary repricing to me."

Other ECB Governing Council members also shared their perspectives at the ECB forum. Lithuania's Gediminas Simkus aligned with expectations for further rate cuts, stating, "Expectations for two more cuts this year are in line with my own thinking, if data evolve as expected." Similarly, Belgium's Pierre Wunsch remarked, "The first two rate cuts are relatively easy as long as inflation hovers around 2.5% because we will still clearly be restrictive."

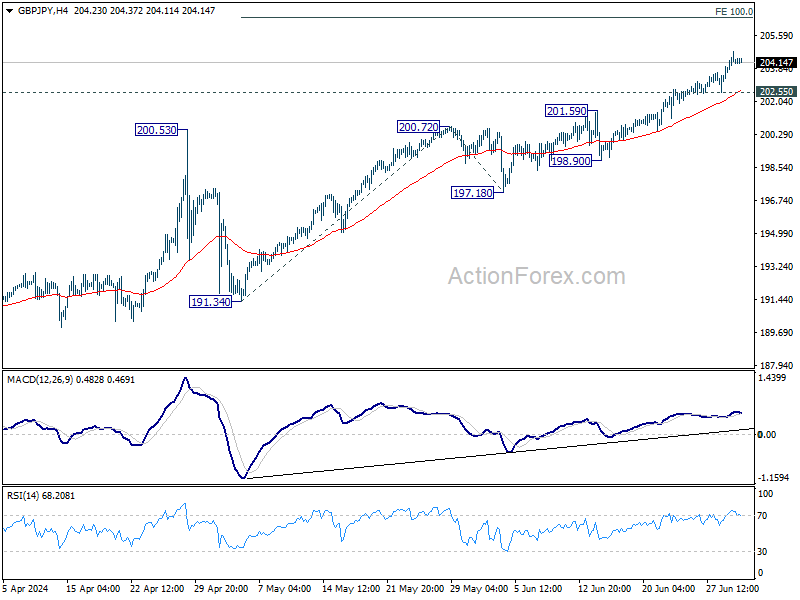

GBP/JPY Daily Outlook

Daily Pivots: (S1) 203.45; (P) 204.09; (R1) 204.93; More...

Intraday bias in GBP/JPY remains on the upside for the moment. Current up trend should target 100% projection of 191.34 to 200.72 from 197.18 at 206.56 next. On the downside, below 202.55 minor support will turn intraday bias neutral and bring consolidations. But outlook will remain bullish as long as 200.72 resistance turned support holds, in case of retreat.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 155.33 to 188.63 from 178.32 at 211.62. Outlook will stay bullish as long as 197.18 support holds, even in case of deep pullback.

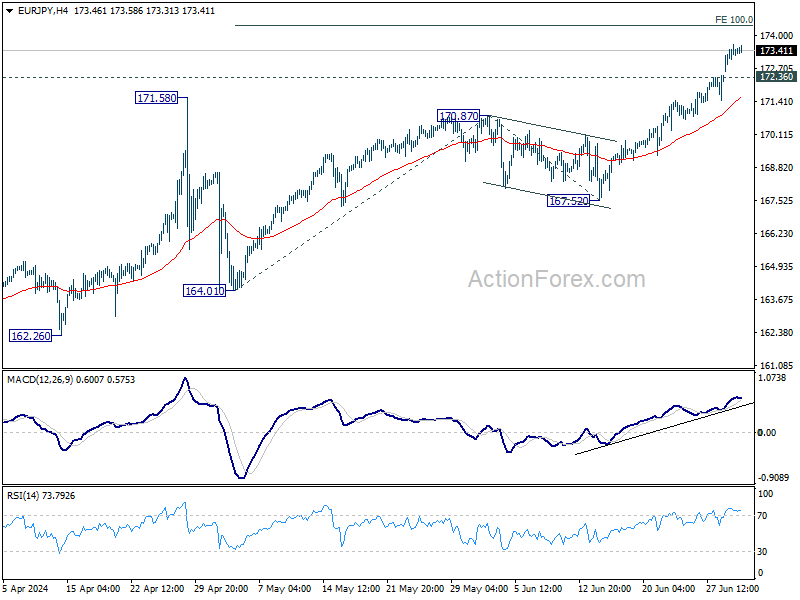

EUR/JPY Daily Outlook

Daily Pivots: (S1) 172.78; (P) 173.22; (R1) 173.85; More...

Intraday bias in EUR/JPY remains on the upside. Current up trend should target 100% projection of 164.01 to 170.87 from 167.52 at 174.38. On the downside, below 171.36 minor support will turn intraday bias neutral and bring consolidations first. But outlook will remain bullish as long as 170.87 resistance turned support holds.

In the bigger picture, long term up trend is still in progress. Next target is 100% projection of 139.05 to 164.29 from 153.15 at 178.38. For now outlook will stay bullish as long as 167.52 support holds, even in case of deep pullback.