Sample Category Title

AUD/USD Range-Bound: What Could Spark Fresh Increase?

Key Highlights

- AUD/USD is trading in a range below the 0.6700 resistance.

- A key rising channel is forming with support at 0.6625 on the 4-hour chart.

- Oil prices extended gains and approached the $85.00 resistance.

- The US ISM Manufacturing Index could remain below 50.0 at 49.0 in June 2024.

AUD/USD Technical Analysis

The Aussie Dollar remained above 0.6600 against the US Dollar. AUD/USD recovered losses, but it remained in a range below the 0.6700 resistance.

Looking at the 4-hour chart, the pair seems to be trading in a broad range below the 0.6700 resistance. However, it is stable above the 100 simple moving average (red, 4-hour) and the 200 simple moving average (green, 4-hour).

There is also a key rising channel forming with support at 0.6625 on the same chart. The pair is now facing resistance near the 0.6675 level or the 76.4% Fib retracement level of the downward move from the 0.6689 swing high to the 0.6634 low.

The next resistance sits at 0.6690. The main hurdle sits at 0.6700. A clear move above the 0.6700 resistance might send it toward the 0.6740 level. Any more gains might open the doors for a test of the 0.6800 zone in the coming days.

Immediate support is near the 0.6650 level. The next major support is near the 0.6625 level. A downside break and close below the 0.6625 support zone could open the doors for a larger decline. In the stated case, the pair could decline toward the 0.6520 level.

Looking at Oil, the bulls remained in action and soon they might aim for more upsides above the $85.00 resistance zone in the near term.

Economic Releases

- Euro Zone Services PMI for June 2024 – Forecast 52.6, versus 52.6 previous.

- UK Services PMI for June 2024 – Forecast 51.2, versus 51.2 previous.

- US Services PMI for June 2024 – Forecast 55.1, versus 55.1 previous.

- US ISM Services PMI for June 2024 – Forecast 52.5, versus 53.8 previous.

- US Initial Jobless Claims - Forecast 235K, versus 233K previous.

- US ADP Employment Change for June 2024 - Forecast 160K, versus 152K previous.

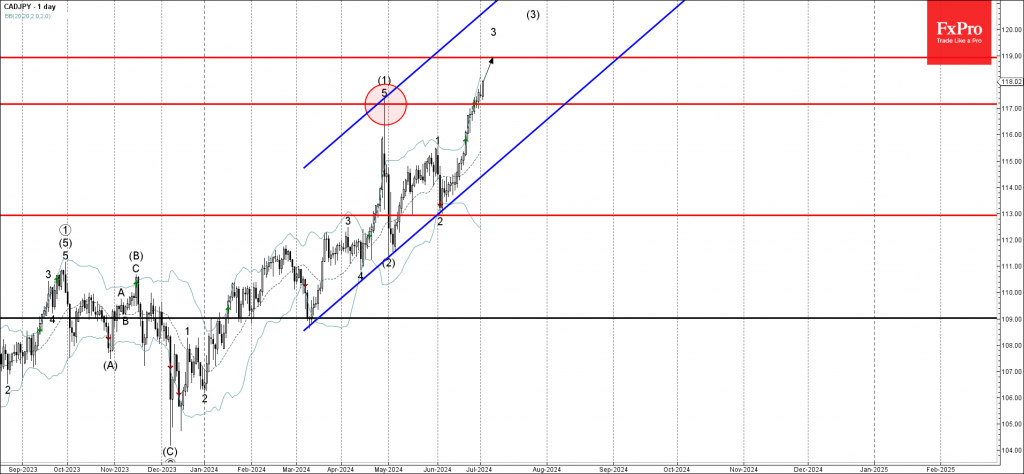

CADJPY Wave Analysis

- CADJPY broke key resistance level 117.00

- Likely to reach resistance level 119.00

CADJPY currency pair recently broke through the key resistance level 117.00 (which stopped the pervious sharp upward impulse wave (1) at the end of April, as can be seen below).

The breakout of the resistance level 117.00 accelerated the active impulse wave 3 of the higher order impulse wave (3) from the start of May.

Given the clear daily uptrend and the continuation of the strong yen sales, CADJPY currency pair can be expected to rise further toward the next resistance level 119.00.

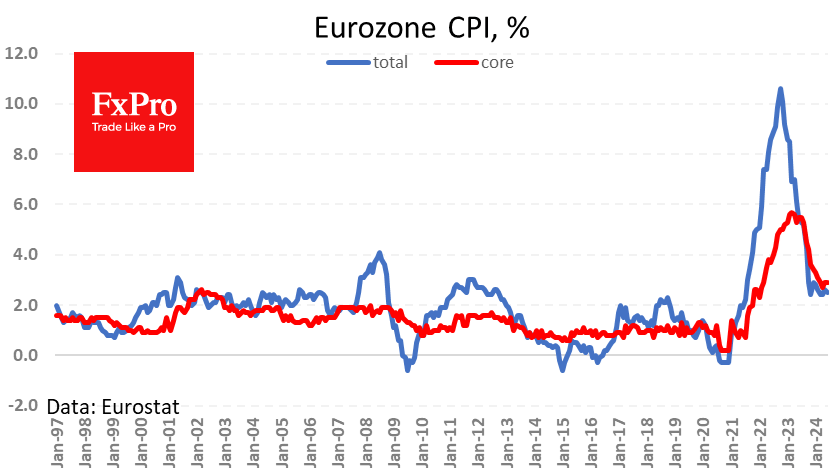

Eurozone: Inflation Deceleration Stalled

According to the Eurostat Flash estimate, the euro area CPI stood at 2.5% y/y, hovering between 2.4% and 2.6% for the past five months. There has been no apparent slowing since November when the rate first touched 2.4%.

Core CPI maintained a 2.9% y/y in May and June after touching 2.7% in April. The index has also stabilised at levels above the ‘below but close to 2%’ target for the ECB.

The stabilisation at higher levels is due to increased demand, as producer prices have been losing more than a year’s worth of annual growth, falling 5.7% y/y, according to the latest data for April.

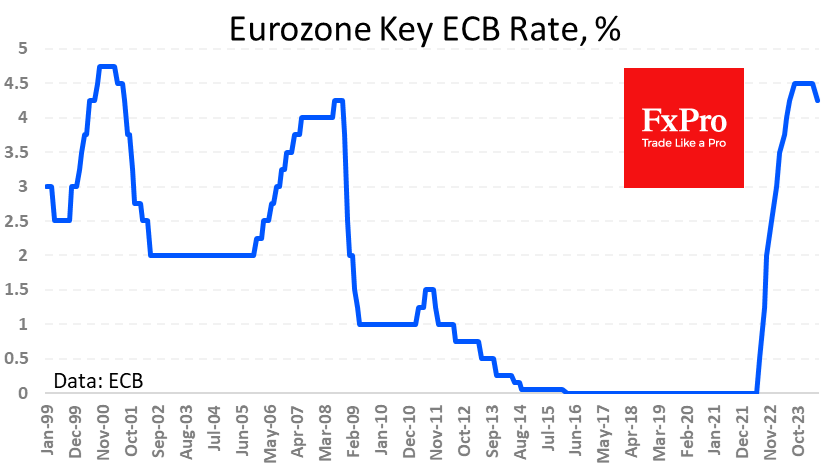

The resilience of inflation is unlikely to allow the ECB to cut rates as aggressively as it has been raising them. This may be more akin to the 2011-2015 easing cycle than the emergency cuts of 2008-2009 or smoother 2001-2002 cuts.

Such a scenario is relatively optimistic for markets, as emergency rate cuts have come with sudden deterioration in financial conditions, requiring liquidity injections to save markets from collapse.

XTIUSD: Strengthened and Reaching Supply Zone

Bearish Scenario:

Sell below 83.63 (if a PAR* forms) with TP1: 83.00, 82.31, 82.11, and 81.70 in extension with an S.L. above 84.00 or at least 1% of account capital.

Bullish Scenario after a Pullback to Demand Zone:

Wait for a decline towards 82.00 and the formation of a bullish PAR* with TP1: 84.16 and TP2: 85.53, with an S.L. below 81.60 or at least 1% of account capital. Apply Trailing Stop.

Fundamental Analysis

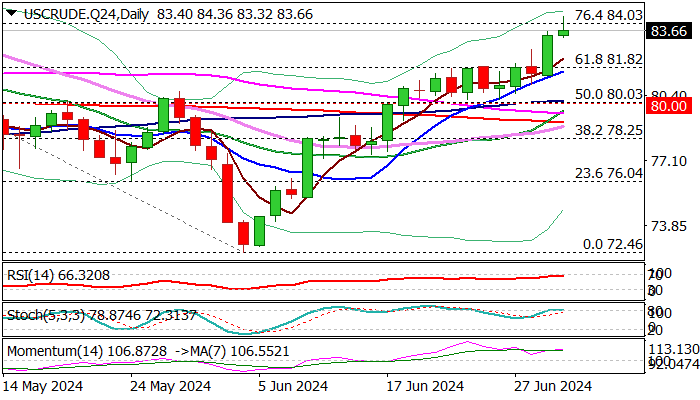

Expectations of Increased Oil Demand in the U.S.

- WTI crude oil prices continue to extend gains, trading around $83.10 per barrel, driven by expectations of higher fuel demand during the summer travel season.

- The American Automobile Association (AAA) projects a 5.2% increase in travel, with a 4.8% rise in car travel compared to last year. This suggests higher fuel consumption, pushing oil prices higher.

Technical Analysis.

WTIUSD, H4

- Supply Zones (Sell): 83.63

- Demand Zones (Buy): 82.94 / 81.70

Crude oil prices have already reached a supply zone at 83.63, from where a pullback towards the day's opening near the early sessions' POC at 82.94 is expected. Bulls may reactivate from this level for an additional rally during the U.S. session towards 84.16 or the average daily bullish range at 84.26 intraday, paving the way for further buys in the coming days.

Conversely, with stronger selling that breaks the daily demand zone around 82.94, a more extensive correction towards the broken resistance now acting as support at 82.31, the bearish range at 82.10, and possibly more extended to yesterday's POC at 81.70 is expected, from where bulls may reactivate as a demand zone.

The bullish scenario after the correction remains valid as long as the last relevant support of the uptrend at 80.60 is not decisively broken.

*POC uncovered: POC = Point of Control: The level or zone where the highest concentration of volume occurred. If there was a bearish movement from it previously, it is considered a selling zone and forms a resistance area. Conversely, if there was a previous bullish impulse, it is considered a buying zone, usually situated at lows forming support zones.

Fed’s Powell: We’re getting back on disinflation path

At the ECB forum, Fed Chair Jerome Powell highlighted the "quite a big of progress" made in reducing inflation toward 2% target. He also acknowledged the recent inflation readings, stating, "The last reading and the one before it, to a lesser extent, suggest that we are getting back on the disinflationary path."

Powell emphasized the need for Fed to be confident that inflation is sustainably moving toward the 2% target before considering policy easing.

He also cautioned against premature rate cuts, "We're well aware that if we go too soon, we can undo the good work we've done. If we do it too late, we could unnecessarily undermine the recovery and the expansion."

When asked about the possibility of a rate cut in September, Powell refrained from providing a specific timeline, saying, "I'm not going to be landing on any specific dates here today."

At the same panel, ECB President Christine Lagarde said Eurozone is "very advanced on that disinflationary path". "We are in that slow recovery that came about in the first quarter and which we hope will persevere but all of that is (fraught) with uncertainty and big question marks about the future," she added.

WTI Oil Outlook: Price Rises Above $84 for the First Time in Over Two Months

WTI oil price rose to nine-week high on Tuesday, in extension of strong Monday’s strong rally (up almost 2.5% for the day).

Increased demand due to summer driving season and persisting supply fears on heated geopolitical situation inflate oil price, which rose above $84 per barrel for the first time since late April.

Bullish technical studies on daily chart (MA’s in bullish setup / strong / positive momentum / price broke above daily cloud) contribute to positive outlook.

Bulls cracked $84.00 round-figure barrier but need to register a daily close above here to confirm signal for 85+ extension.

Meanwhile, bulls may pause for consolidation, with dips to find ground above daily cloud top ($81.87, reverted to solid support) to keep bulls intact and offer better buying opportunities.

Res: 84.03; 83.43; 85.00; 85.59.

Sup: 83.32; 82.27; 81.87; 81.60.

Sunset Market Commentary

Markets

The pace of Eurozone inflation remained steady at 0.2% M/M in June. The outcome was in line with consensus as could be expected following earlier national prints. The Y/Y-figure slowed from 2.8% to 2.5%. Core inflation rose somewhat faster (0.3% M/M), but this was the slowest pace since January (steady Y/Y at 2.9%). Services inflation was more sticky at 0.6% M/M (and 4.1% Y/Y; matching highest level since November 2023). The latter strengthened comments by ECB chief economist Lane this morning who indicated that the June print won’t settle questions the central bank still has on the persistence of (services) inflation: “what we need to see is whether higher services inflation is a backward element and is a legacy of the rapid disinflation or is it a persistent element”. The questions for the July meeting are going to be on the economic side in a clear nod to skipping at least a meeting in further lowering policy rates. Other ECB comments in the sidelines of the ECB forum in Sintra all point in the direction of making monetary policy less restrictive in coming months. ECB Wunsch labels the first two rate cuts as relatively easy as long as inflation hovers around 2.5% because the ECB will still be clearly restrictive then. ECB Muller and Vasle are on the same page. ECB Simkus aligns with markets expectations of two more 25 bps rate cuts this year, in an echo to comments of ECB Rehn last week. ECB Lagarde and Fed chair Powell featured in a panel discussion. In her opening speech, the ECB president yesterday already warned that the inflation battle isn’t over yet. Fed Powell observes a similar stickier services inflation in the US, linked to wages. On the labour market front, he sees it coming off over time as hoped. We believe that the next couple of labour market data (ADP employment change tomorrow and payrolls on Friday) could be key in shaping Fed policy expectations for coming months.

Today’s market story isn’t really vibrant. Core bonds recover some of the recently lost ground in a more risk-averse market setting. Daily changes on the German and US yield curves amount to some -3 to -4 bps. French OAT’s outperform (OAT/swap at 44 bps from intraday high of 48 bps) perhaps linked to news on a significant number of dropouts (front républicain) for next Sunday’s second round of parliamentary elections. The cutoff date is tonight at 6 pm. Key European stock indices lose 0.75% to 1%. EUR/USD after an initial blip trades back near opening levels at 1.0740.

News & Views

Brent oil is testing the upper bound of a short term triangle formation that’s keeping a lid on price action since mid-June. A barrel is currently sold for $87.27, the highest since end April with a combination of supply-side factors supporting prices more recently. One of them includes the rumble in the Middle East. Tensions between Israel and Lebanon-based Hezbollah rose further in the wake of a drone attack last Sunday, causing concerns the initial conflict with Gaza may spread and involve countries including Iran. Another supply-driven boost came from an unusual start of the oil-production disrupting hurricane season. Hurricane Beryl strengthened to the highest category (5). It’s the strongest storm to have ever formed in the Atlantic this time of the year, triggering fears this season could be more severe.

S&P Global warned that countries including the US, France and other major economies, are unlikely to halt the rise in their debt levels in the next several years, Reuters reported based on a publication issued by the rating agency. "We estimate that --for the U.S., Italy, and France-- the primary balance would have to improve by more than 2% of GDP cumulatively for their debt to stabilize; this is unlikely to happen over the next three years”, S&P noted. Given the electoral cycle, S&P thinks that only a sharp deterioration of the borrowing conditions could push governments into more forceful budgetary consolidation.

Graphs

Brent crude: supply-related worries push oil prices to highest level since end of April

US 10-yr yield: small correction after fiscal/election-related increase

DXY (trade-weighted dollar): this month’s upward trend channel remains in place despite recent standstill

EUR/GBP: 0.85 a bridge to far going into Thursday’s ballot

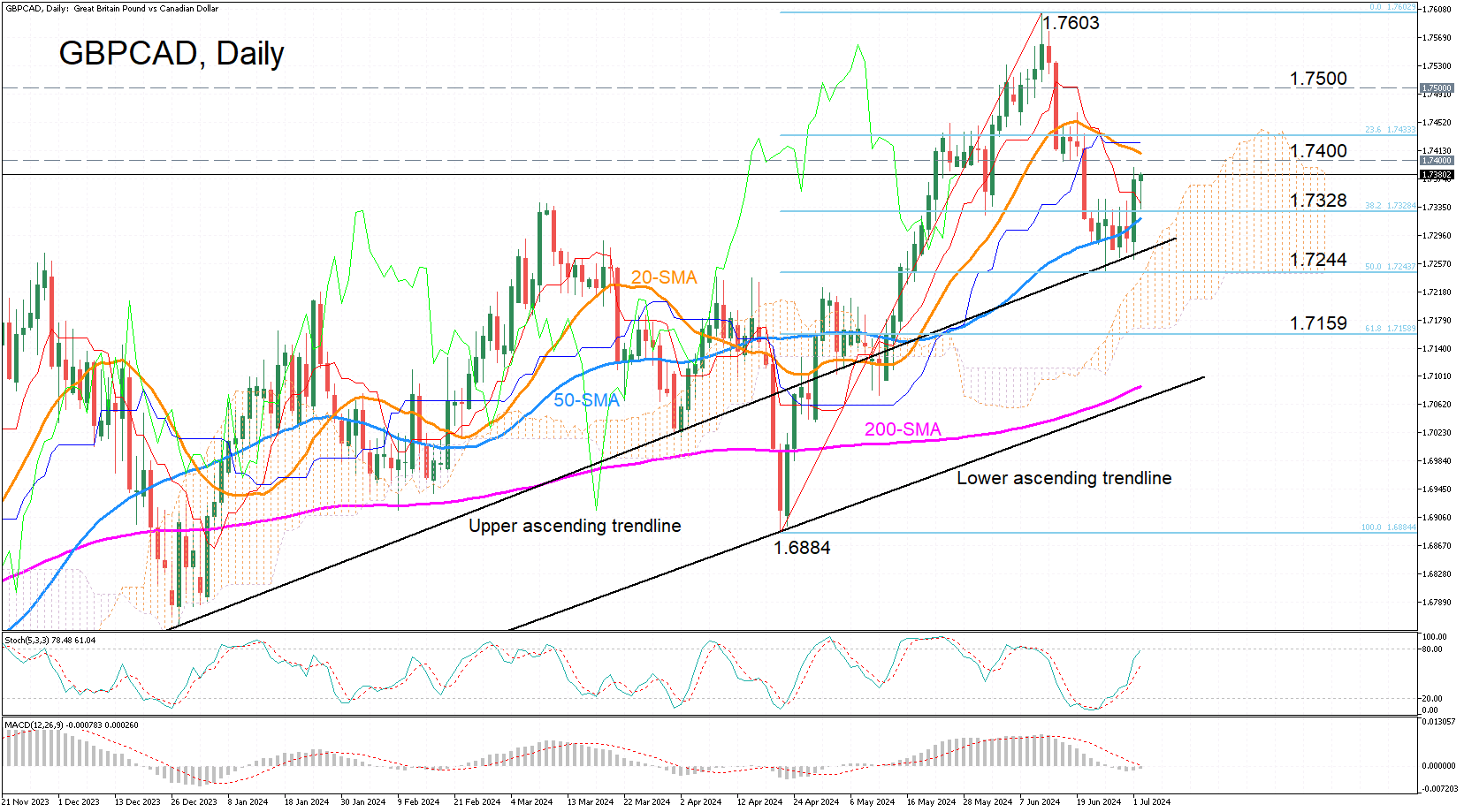

GBPCAD Uptrend Intact After Latest Correction

- GBPCAD bounces off uptrend line

- But strength of rebound is in question

- 20-day SMA is nearest challenge for the bulls

GBPCAD has rebounded back above the 50-day simple moving average (SMA) after a 2% correction in June took the price below it towards the upper ascending trendline that’s been in place since the autumn of 2023.

The momentum indicators are positive again, but there are also signs that the upswing could already be faltering. The %K line of the stochastic oscillator appears to be slowing its ascent, though it remains positively aligned with the %D line for now. The MACD has been steadily edging higher, but the gains haven’t been strong enough to turn it positive or lift it above its red signal line.

Should the bullish momentum hold, it will be crucial to extend the rebound at least until the 20-day SMA, which is about to meet the 1.7400 level, to reinforce the uptrend. A break above this resistance zone would switch attention first to the 1.7500 level and then the June peak of 1.7603.

However, if the bears regain the upper hand, the 50-day SMA is likely to again act as support in the 1.7319 area, before testing the upper ascending trendline. Breaching it would open the way for the 61.8% Fibonacci retracement of the April-June upleg at 1.7159. Slightly below, the lower ascending trendline, which lies close to the 200-day SMA, could block further declines.

Summing up, although the longer-term bullish picture has not altered after the latest selloff, the short-term bounce back is not on a completely solid footing just yet.

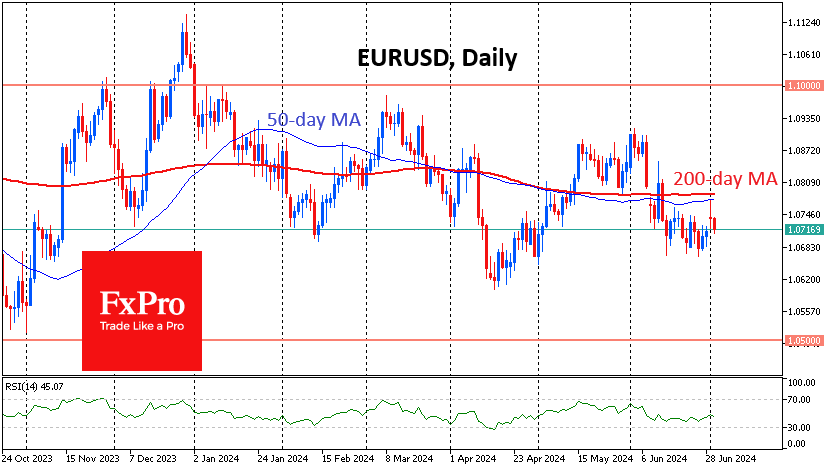

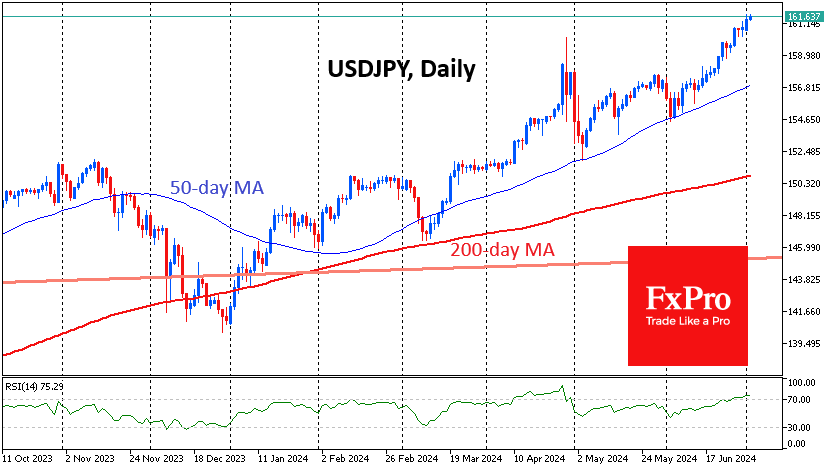

Dollar Rises on Other Currencies’ Problems

The US dollar has been settling near two-month highs since late last week, but this is a pick of the best among the worst. Expectations for the Fed’s key year-end rate have changed little over the past roughly three weeks. Still, the dollar’s main competitors have faced their difficulties one after another, coming under selling pressure.

Political uncertainty remains over France and the UK due to expectations of opposition parties coming to power. Some investors fear accelerating de-globalisation, which is seen as negative by global investors. The results of the first round in France spurred the euro only briefly, and by midday on Tuesday, EURUSD again approached 1.0710, where it spent the second half of June. It is worth noting that this euro sell-off is also supported by declines in bonds and the equity market.

The slightly less one-note but highly dramatic story in the yen continues. The USDJPY has been hitting highs since 1986, rising to 161.6. The pair has been selling off since the beginning of the week, touching 161.7, but minor pullbacks do not allow for shock-and-awe interventions that could reverse the momentum. Japan’s stock market is taking advantage of the yen’s weakness, trying to return to levels above 40000 on the Nikkei225, despite the decline in key global benchmarks.

The Swiss franc is giving up ground almost daily following the Swiss Central Bank’s second consecutive policy easing on 20 June, taking USDCHF back above 0.90, a one-month high.

Technically, the DXY Dollar Index continues to hover near the lower boundary of the rising channel. The dollar needs to rise another 0.5% to confirm this upward trend, breaking the area of previous peaks. If the bulls are successful at this stage, the dollar will be able to grow to the upper boundary of the corridor (now at 109), which has the potential to strengthen by about 3% to the current levels.

A more hawkish tone of the central bank officials compared to Europe and more robust economic growth figures will help the USD on this growth path, promising less active easing of monetary policy conditions in the foreseeable future. A continued bullish bias for the dollar threatens to push EURUSD back below 1.05 before the end of summer, where the pair briefly dipped in early October 2023.