Sample Category Title

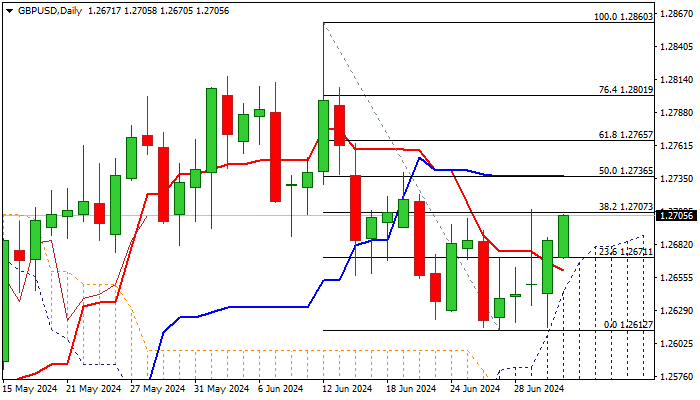

GBP/USD Outlook: Lifted Further by Better Than Expected UK PMI Data

Cable advances for the second consecutive day, underpinned by better than expected UK services PMI (dominant sector of the economy) released earlier today.

Fresh bulls cracked psychological 1.2700 barrier and nearby pivotal Fibo resistance at 1.2707 (38.2% of 1.2860/1.2612 bear-leg) with bounce from 1.2612 higher base being underpinned by rising and thickening daily Ichimoku cloud.

Sustained break of 1.2700/07 barriers to generate bullish signal for extension towards next targets at 1.2736 and 1.2765 (Fibo 50% and 61.8% retracement).

On the other hand, 14-d momentum is still in the negative territory and requires caution, though near-term bullish bias to remain in play as long as price action stays above daily cloud top, reinforced by daily Tenkan-sen (1.2661).

Res: 1.2670; 1.2715; 1.2736; 1.2765.

Sup: 1.2687; 1.2661; 1.2638; 1.2612.

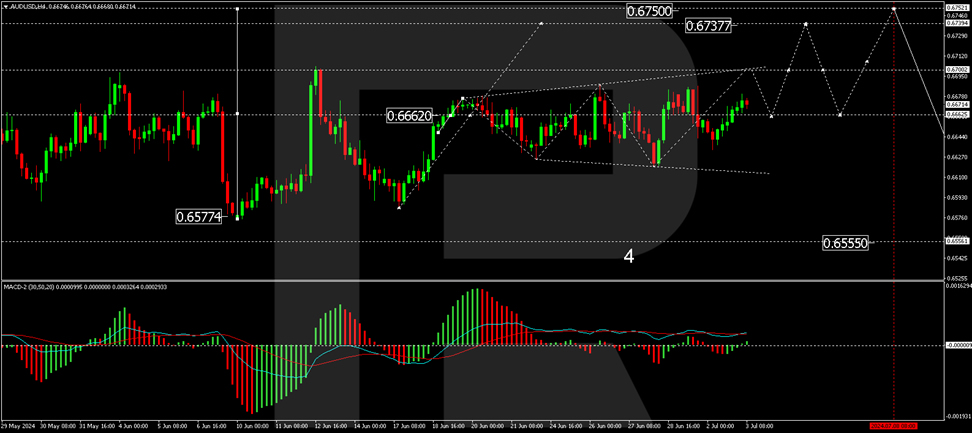

AUD/USD Sees Uptick Amidst Mixed Sentiment

AUD/USD has climbed to 0.6676 yet remains in a "sideways" pattern, indicating a lack of clear directional momentum in the market.

The Australian dollar's appreciation is linked to a softening in the US dollar's stance, influenced by remarks from Federal Reserve Chair Jerome Powell. Powell highlighted the need for further economic data to assess the disinflationary trends, suggesting a cautious approach to rate adjustments. This uncertainty around US monetary policy has led to a dip in the USD, boosting AUD.

Conversely, the Reserve Bank of Australia (RBA) maintains a vigilant stance on inflation, with recent minutes suggesting a potential rate hike if inflationary pressures escalate. This possibility lends some support to the Australian dollar. Recent economic data from Australia, including a spike in May's retail sales and continued private sector growth in June, further bolsters this perspective.

Market speculation hints at a potential RBA rate increase in August, with forthcoming data likely to provide clearer indicators of this likelihood.

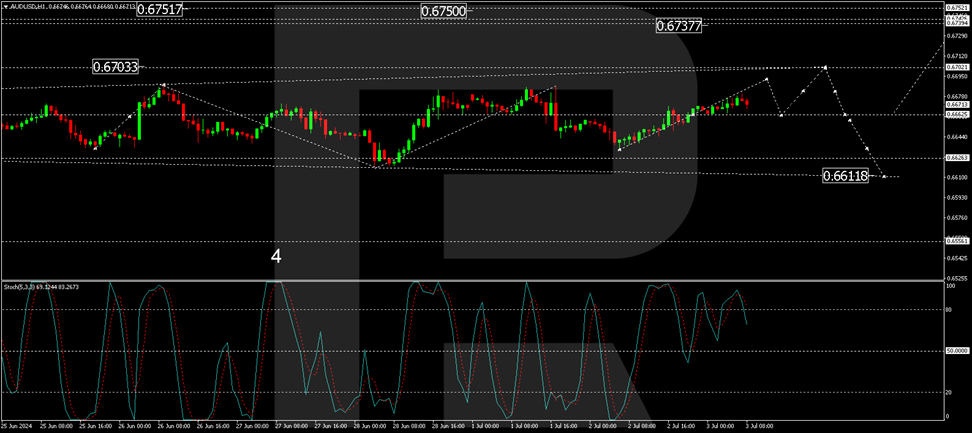

Technical analysis of AUD/USD

The AUD/USD pair navigates within a broad consolidation range, forming a diverging "Triangle" around 0.6662. Currently, there is potential for the price to ascend to 0.6702. Upon reaching this level, a retraction to 0.6662 is anticipated, with a potential downward break targeting 0.6555 before resuming upward movements towards 0.6737. The MACD indicator supports this growth scenario, with its signal line positioned above zero and upwards.

On the hourly chart, a tight consolidation has been observed around 0.6662. The expected trajectory involves an ascent to 0.6690, potentially extending to 0.6702. This growth forecast is underscored by the Stochastic oscillator, whose signal line is above 80, suggesting an impending downward adjustment to around 50.

Market outlook

As the global financial landscape navigates through mixed economic signals and central bank policies, the AUD/USD pair will likely continue to experience volatility. Investors and traders will closely monitor upcoming economic releases and central bank communications to gauge the potential shifts in monetary policy, especially from the RBA and the Fed, which could significantly influence the currency pair's movements in the near term.

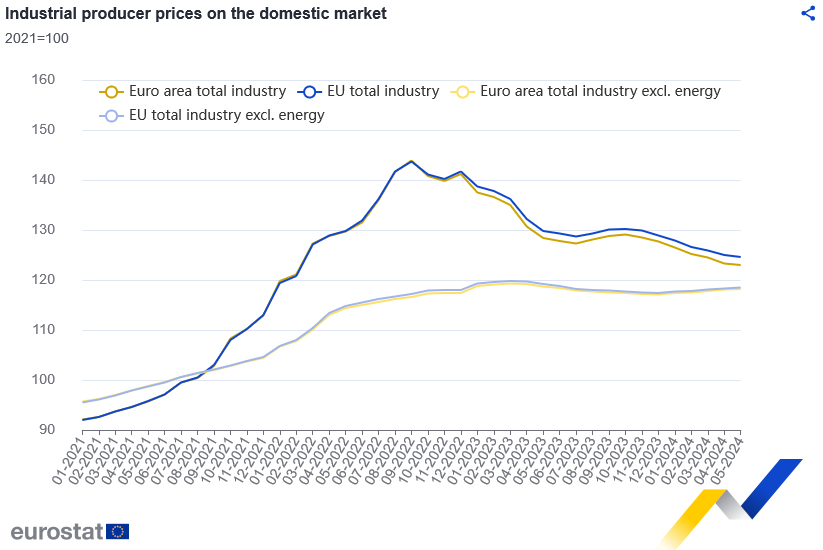

Eurozone PPI falls -0.2% mom, -4.2% yoy in May

Eurozone PPI fell -0.2% mom, -4.2% yoy in May, versus expectation of 0.0% mom, -4.1% yoy.

For the month, industrial producer prices increased by 0.1% for intermediate goods, 0.1% for capital goods, and 0.1% for non-durable consumer goods. Prices decreased by -1.1% for energy, and -0.1% for durable consumer goods.

EU PPI was down -0.3% mom, -4.0% yoy. The largest monthly decreases were recorded in Croatia (-4.1%), Greece (-2.9%) and Sweden (-1.8%). The highest increases were observed in Ireland (+7.7%), Bulgaria (+4.5%) and Estonia (+2.1%).

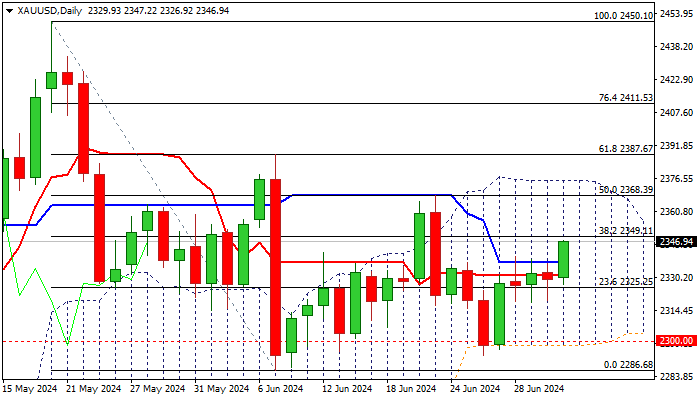

XAU/USD outlook: Gold Price Rises Ahead of Key Economic Data But Still Holding Within Broader Range

Gold price rose during early trading on Wednesday, after being stuck within a narrow congestion in past three days.

Fresh strength hit the highest in almost two weeks, though the wider picture shows the price moving within larger range ($2368/$2286) for the past couple of weeks.

Traders look for fresh direction signals, with Fed monetary policy and geopolitical situation being metal’s key drivers.

Markets await release of the minutes of FOMC last meeting (due later today) to get more information about Fed’s next steps, after the central bank’s Chairman Jerome Powell said on Tuesday that the US was in disinflationary path, but Fed needs more data before starts cutting rates.

The data from the US labor sector are also in focus, with ADP report from private sector due today and more significant NFP release on Friday.

Technical picture turned firmly bullish on lower timeframes and improved on daily chart, although no clear direction to be expected while the price action stays within current range (also defined by the boundaries of daily Ichimoku cloud).

This signals that traders could play the range as long as short-term action is in sideways mode, with violation of any of range boundaries $2368/75 (50% retracement of $2450/$2286 / daily cloud top) at the upside or $2300/$2286 (psychological / daily cloud base / June 7 low) at the downside, to generate initial direction signal.

Res: 2350; 2368; 2375; 2387.

Sup: 2325; 2319; 2300; 2286.

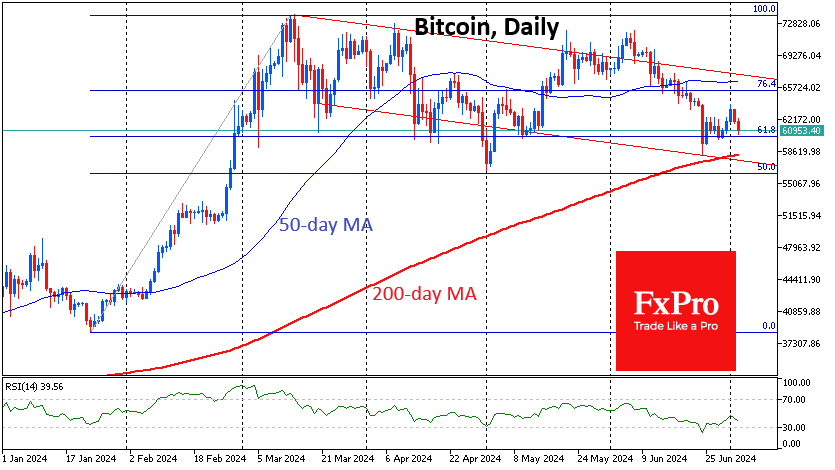

Crypto Stays Under Pressure

Market picture

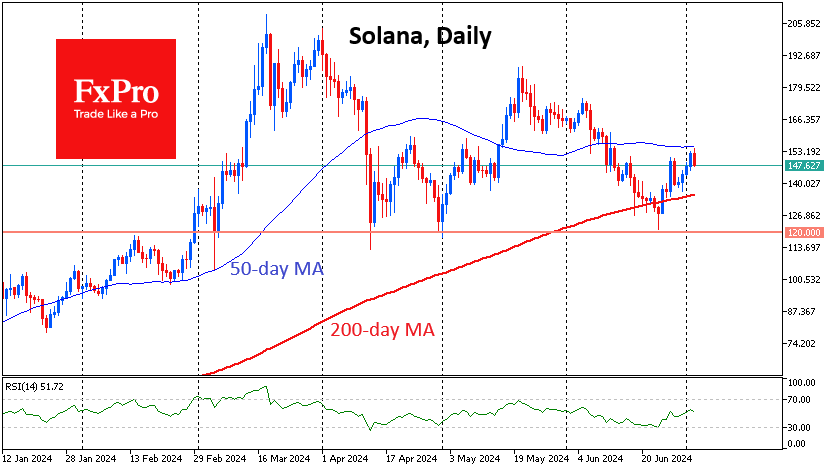

The pressure on the crypto has been more sustained than on the stocks. Over the past 24 hours, the total crypto cap has fallen by 2.6%, with most of the downward momentum starting in the US session. The stock market, on the other hand, was supported by Powell’s comments and closed at all-time highs, supporting risk appetite in Asia. Bitcoin, Ethereum, and BNB returned to their lows in the last seven days. At the same time, there is still interest in buying smaller coins: Solana, XRP, and Toncoin.

Bitcoin retreated to $60.5K at the lows of the Asian session, partially recovering to $61K at the time of writing. The cryptocurrency is under pressure but remains in a technical correction after the upward momentum. Only a drop below $58K will disrupt the bullish picture, breaking the concentrated support area in the form of the 61.8% level ($60.3K), the 200-day moving average ($58.3K) and the previous low ($58.2K). In this case, be prepared for a drop to $51.0K with alarming consequences for the entire cryptocurrency market.

Solana has been up over the last 24 hours but is down 3% since the start of the day on Wednesday, having found technical resistance in the form of its 50-day moving average. The fundamental picture is one of a worrying sell-off in the major cryptocurrencies despite the overall positivity in equities.

News background

Bitfinex notes that long-term Bitcoin holders, who stopped taking profits in early May, have resumed selling assets. This trend could put significant short-term pressure on BTC.

Bitcoin may face selling pressure in July due to the upcoming start of payments to Mt. Gox creditors. Crypto assets worth $9.4 billion are to be distributed to around 127,000 users of the exchange, which went bankrupt in 2014.

Another negative factor is the potential selling pressure following the recent BTC transfers to exchanges by the DFI authorities. Over the past month, ~$193 million worth of coins have been transferred from the wallets of the FRG authorities to CEX.

Swiss state-owned bank PostFinance launched trading services for its customers in five cryptocurrencies: Ripple (XRP), Solana (SOL), Avalanche (AVAX), Cardano (ADA) and Polkadot (DOT), in addition to Bitcoin and Ethereum.

South Korea’s largest cryptocurrency exchanges plan to review the status of more than 1,300 cryptocurrencies under updated, stricter self-regulatory standards that take effect on 19 July. Altcoins are far more popular in the country than the two flagship cryptocurrencies.

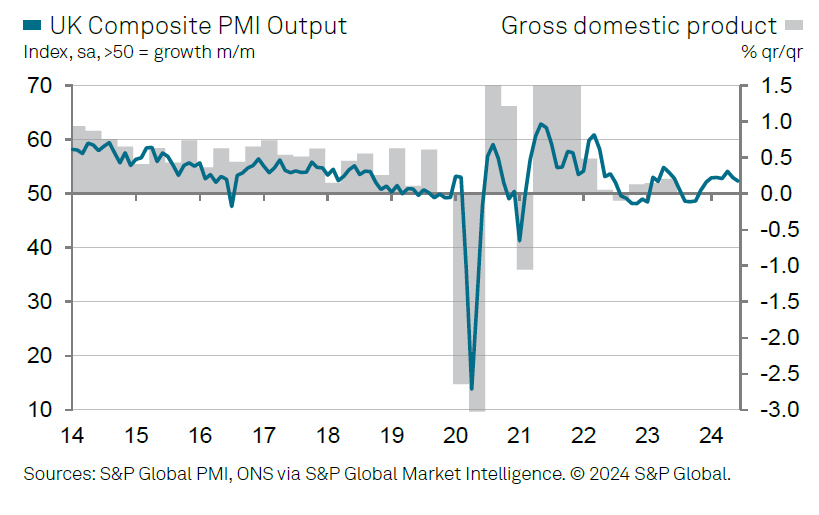

UK PMI services finalized at 52.1, growth slows amid election uncertainty

UK PMI Services index was finalized at 52.1 in June, down from May's 52.9, marking the slowest growth rate since November of last year. PMI Composite also fell to 52.3, from the previous month's 53.0, a six-month low.

Joe Hayes, Principal Economist at S&P Global Market Intelligence, noted signs of a "pre-general election seize up" in the UK services sector. He observed that business activity growth slowed to a seven-month low, as the prospect of a change in government led some businesses to adopt a "wait-and-see" approach, restraining sales. Despite the slowdown, Hayes indicated that the UK is still on track for another quarter of GDP growth, though it will be less robust than the first quarter's 0.7%.

Prices in the UK service sector remain high, though input cost inflation trended lower. This is encouraging for BoE, but the survey also showed an increase in prices charged by companies, as some reported strong pricing power. While wage costs have been a major driver of services inflation, the UK's economic recovery adds another factor for policymakers to consider, especially if improving conditions lead more companies to raise prices.

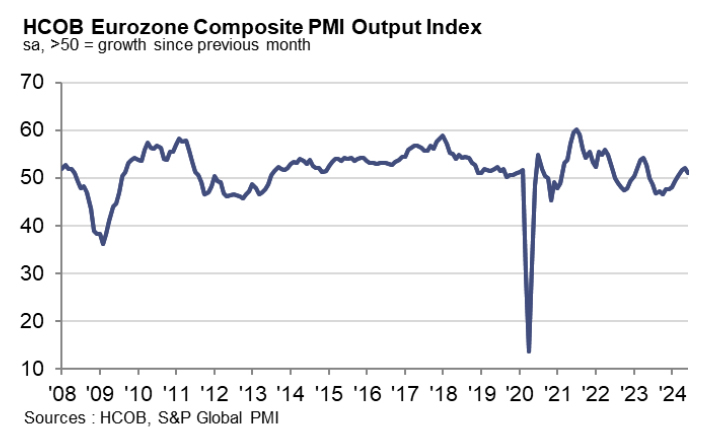

Eurozone PMI services finalized at 52.8, composite at 50.9

In June, Eurozone PMI Services index was finalized at 52.8, slightly down from May's 53.2. PMI Composite also dropped, finalizing at 50.9 compared to the previous month's 52.2.

The countries ranked by Composite PMI Output Index are as follows: Spain at 55.8 (a 2-month low), Italy at 51.3 (a 4-month low), Germany at 50.4 (a 3-month low), Ireland at 50.1 (an 8-month low), and France at 48.8 (a 3-month low).

Cyrus de la Rubia, Chief Economist at Hamburg Commercial Bank, noted that Eurozone's growth is driven entirely by the service sector. While manufacturing activity "weakened considerably", the services sector continued to grow "nearly as robust as" the month before. De la Rubia emphasized that service providers will be crucial in maintaining overall economic growth throughout the year.

The recovery in service sector is broad-based across the top four Eurozone economies. Spain led with significant growth, followed by solid performances in Germany and Italy. However, France's service providers were unable to increase their activity.

ECB, which cut interest rates in June, found some validation in the price indices. Input prices and prices charged to clients rose at the slowest pace in three years. Nonetheless, ECB would remain cautious, as these price increases are still above pre-pandemic levels and remain high considering the economy's fragile state.

Gold Price Prospects for H2

As shown by the daily XAU/USD chart:

→ Since November 2022, the price has been moving in an upward channel, marked in orange;

→ Since the start of 2024, the price has risen by approximately 12.5%.

What are the gold price forecasts for the end of 2024?

According to Investing.com, Georgette Boele, a senior sustainability economist at ABN Amro, published a cautious forecast on 27 June, predicting a gold price of $2000 per ounce by the end of the year. In her view:

→ Gold prices peaked at the beginning of the year but have since lost momentum.

→ Anticipated easing measures by central banks have not provided the expected support to gold prices.

→ Concerns about physical gold shortages, which were a factor during the COVID crisis, are unfounded in the current market.

On the other hand, longer-term forecasts are optimistic. Analysts at Bank of America believe the gold price could rise to $3000 within 12-18 months. Their arguments include:

→ Lowering Federal Reserve rates could trigger an inflow of funds into ETFs backed by physical gold;

→ The desire to reduce USD holdings in portfolios is likely to lead to increased gold purchases by central banks.

Technical analysis of the XAU/USD chart shows that:

→ After the price reached the upper boundary of the channel twice in the first half of the year (indicated by numbers), the bulls lost momentum;

→ This resulted in a consolidation pattern resembling a triangle (shown by blue lines), within which the gold price fluctuated throughout June.

Note that a similar consolidation was observed at the beginning of 2024, and a bullish breakout led to a sharp rally.

It is possible that a breakout of the current pattern could lead to a trend that significantly influences which gold price forecast—BofA’s bullish or ABN Amro’s bearish—proves more accurate.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

S&P 500: Mid-Year Prospects Analysis

As shown by the daily chart of the S&P 500 (US SPX 500 mini on FXOpen):

→ Since the beginning of 2023, the price has been moving in an upward blue channel. To date, the increase has been over 42%;

→ Since the start of 2024, the price has formed a steeper upward channel (shown in orange). In the first half of the year, the growth has exceeded 14%.

How realistic is it for bullish sentiment to persist? And what might the index quotations be by the end of 2024?

Yahoo Finance reports a decidedly bearish outlook for the S&P 500 (US SPX 500 mini on FXOpen) at the end of 2024, held by Marko Kolanovic, the chief strategist at JPMorgan Chase & Co. He cites the following factors:

→ Economic slowdown;

→ Downward revision of company profits;

→ The Federal Reserve may cut interest rates less than the market expects, which would put additional pressure on the economy and stock prices in the second half of the year.

Kolanovic predicts the S&P 500 (US SPX 500 mini on FXOpen) will be at 4200 points by the end of 2024. In the context of the attached chart, this implies not only a bearish breakout of the lower boundary of the blue upward channel but also a decline to the year's minimum.

On the other hand, strategists and analysts from other reputable financial institutions tracked by Yahoo Finance hold a more optimistic view:

→ Evercore ISI analysts predict the S&P 500 (US SPX 500 mini on FXOpen) will reach 6000 points by the end of 2024. This means the price will remain within the blue channel.

→ The average estimate from analysts points to a target of 5300.

Based on these estimates, the lower boundary of the upward orange channel, which has been in place since the start of the year, will likely be broken, potentially leading to a significant correction.

In addition to traditional fundamental factors (such as inflation, the Federal Reserve's interest rate, the labour market, and company profits), the S&P 500 (US SPX 500 mini on FXOpen) price in the second half of the year could be influenced by:

→ The presidential election in November;

→ The unusually high weight of the top 10 leading technology companies (including Nvidia, Microsoft, and Google) in the index.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.

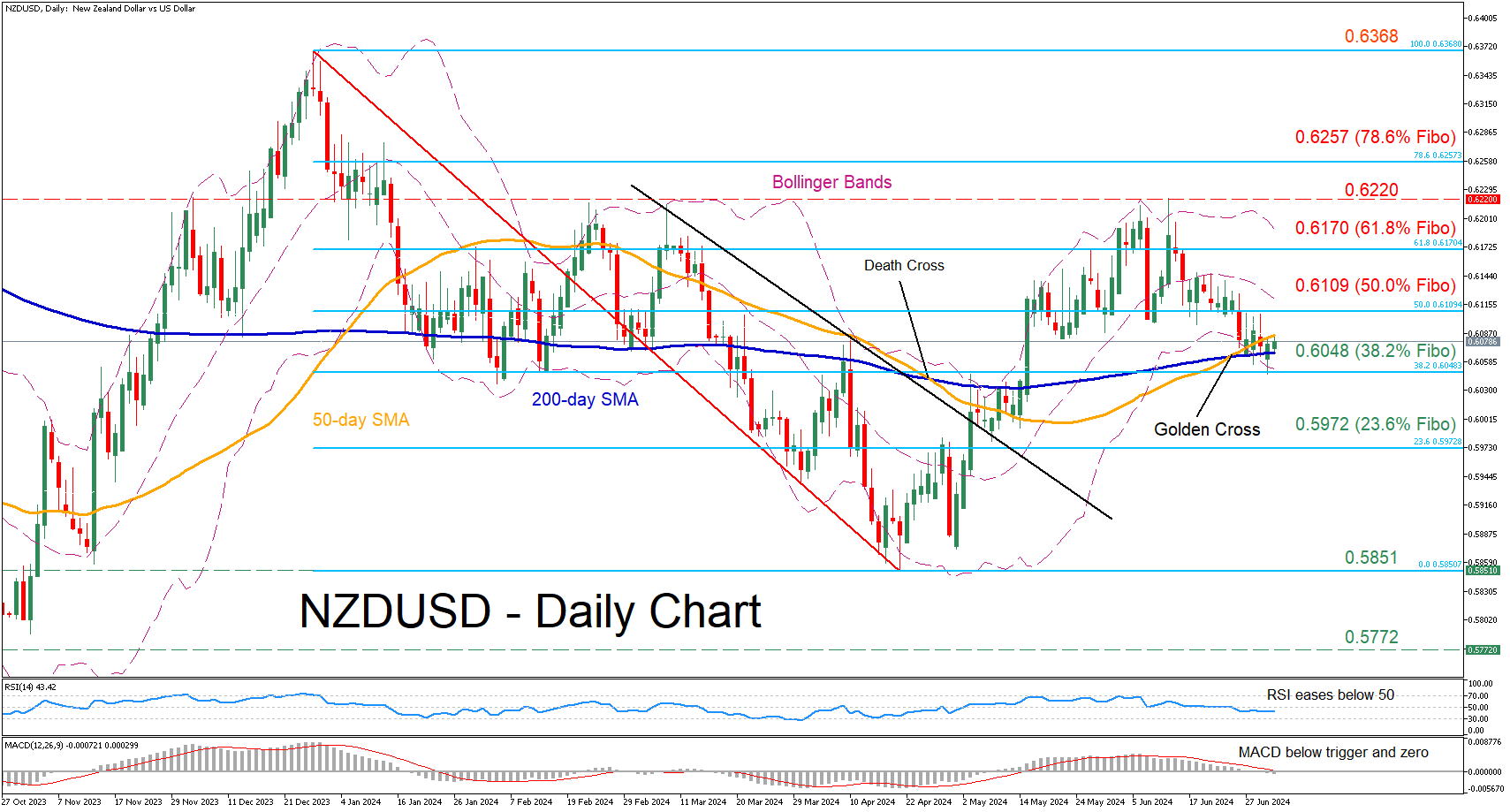

NZDUSD Meets Support at 38.2% Fibo

- NZDUSD is in a steady decline since early June

- Completion of golden cross fails to trigger a recovery

- Oscillators are tilted to the bearish side

NZDUSD had been in an aggressive uptrend following its 2024 bottom of 0.5851 in mid-April, surging to a six-month high of 0.6220 in June. However, the pair has come under severe selling pressure since then, with the 200-day simple moving average (SMA) preventing further declines for now.

Should the bears attempt to push the price lower, immediate support could be found at 0.6048, which is the 38.2% Fibonacci retracement of the 0.6368-0.5851 downleg. Lower, the 23.6% Fibo of 0.5972 could provide downside protection. A violation of that zone could open the door for the 2024 low of 0.5851.

Alternatively, if the pair stages a recovery, the 50.0% Fibo of 0.6109 could prove to be the first barricade for the bulls to overcome. Further advances could then cease at the 61.8% Fibo of 0.6170 ahead of the six-month peak of 0.6220. Even higher, the 78.6% Fibo of 0.6257 could curb the pair’s upside.

In brief, NZDUSD has been undergoing a pullback in the short term, while the completion of a golden cross between the 50- and 200-day SMAs has failed to reverse this slide. Nevertheless, things could get even worse in the case that the price breaks decisively below its 200-day SMA.