Sample Category Title

Could Post-UK Elections Market Moves Resemble 1997 and 2010?

- Thursday's UK elections expected to bring political change

- Similar developments in both 1997 and 2010 weighed on the pound

- History points to a significant easing in pound volatility across the board

- Recent FTSE 100 performance matches the 2015 pre-election moves

General election in sight

The UK general election will be held this Thursday, July 4, the day that the US will be celebrating its 248th anniversary from the adoption of the Declaration of Independence. The Labour party is expected to comfortably win the elections with the last unanswered question being the size of its parliamentary majority. It could win more than 400 seats in the next parliament, the biggest Labour majority since 2001, giving its leader the ability to govern untroubled over the next 5 years.

The market has understandably analysed and dissected the economic plans of the new government, but it appears to be in a waiting mode ahead of such an important event. The FTSE 100 index is around 3% lower since the May 22 announcement day while the pound has had a mixed performance against both the dollar and the euro, despite the increased market volatility.

What’s next for key UK assets?

Historical analysis is a useful way of mapping the possible market reaction following risk events. Therefore, a detailed look at the post-election performances since 1997 could be interesting. However, one has to take into consideration that external developments, like the euro area debt crisis, or one-off events, like Brexit, could gravely affect the outcome of the elections and the market reaction.

1997 and 2010 – a repeat of history?

Having said that, there are two elections that stand out and match the current setup. In 1997, the Labour Party under Tony Blair managed to reclaim the government after 18 years of Conservative dominance. Similarly, in 2010, the Tories returned to power, winning four consecutive elections and staying in charge until July 4, 2024. So, what happened to the key market assets before and after these elections?

An analysis of the market's performance on the day of the election, one day and one week after the key dates reveals some interesting findings. For example, Brent oil prices tend to drop both on the day of the elections and on the following day as the markets are still digesting the outcome.

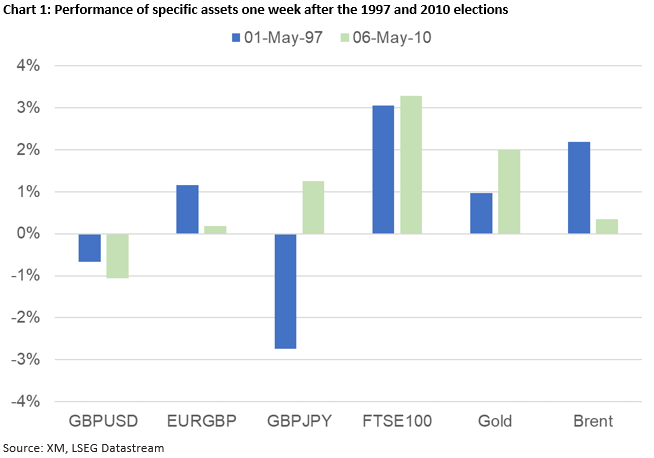

More importantly, market changes one week after the election give the strongest signals. As seen in chart 1 below, in both 1997 and 2010, the pound underperformed against both the US dollar and the euro, while the FTSE 100 index jumped by around 3%. Additionally, both gold and Brent oil prices show a tendency to rise, with the latter greatly affected by the new energy initiatives expected to be implemented by the new government.

Volatility in the last four elections

Another popular way of trading significant market events is through volatility. Analysis of the one-month implied volatility for both the euro/pound and pound/dollar pairs in the last four elections, since 2010, shows some promising results.

Volatility in both pairs tends to drop one day after the elections are held, with the sole exception of 2010 when the unfolding euro area debt crisis caused a small increase in one-month volatility. Interestingly, this correction in currency volatility persists one week after the election date with drops of around 10-35% recorded in the past four elections, as the market reacts to the lower political risk. This easing in volatility is also maintained when examining longer time periods, up to six months after the election dates.

Could the recent performance give us hints on the short-term outlook?

Finally, an alternative way of analysing historical trends is to try and match the pre-event performance of the key assets during previous elections with the current one. The logic behind this process is that similar performances point to similar risks priced in both periods and could thus reveal the short-term outlook for the analysed assets.

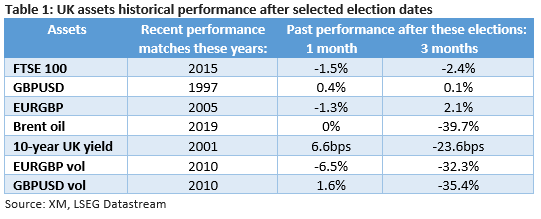

Table 1 below shows the matched election periods for the various assets. For example, this year’s price action of the FTSE 100 index matches the pre-election performance of the index before the 2015 elections, when the Tories won another term in the government. In 2015, the FTSE 100 was 1.5% down one month after the election date with its losses increasing to 2.4% in the three-month period.

Investors Await NFP to Validate Their Fed Rate Cut Bets

- Investors expect two rate cuts, even though Fed signals one

- Recent data corroborates investors’ take

- Nonfarm payrolls waited for more confirmation

- The report comes out on Friday, at 12:30 GMT

Fed appears hawkish, but data paint a different picture

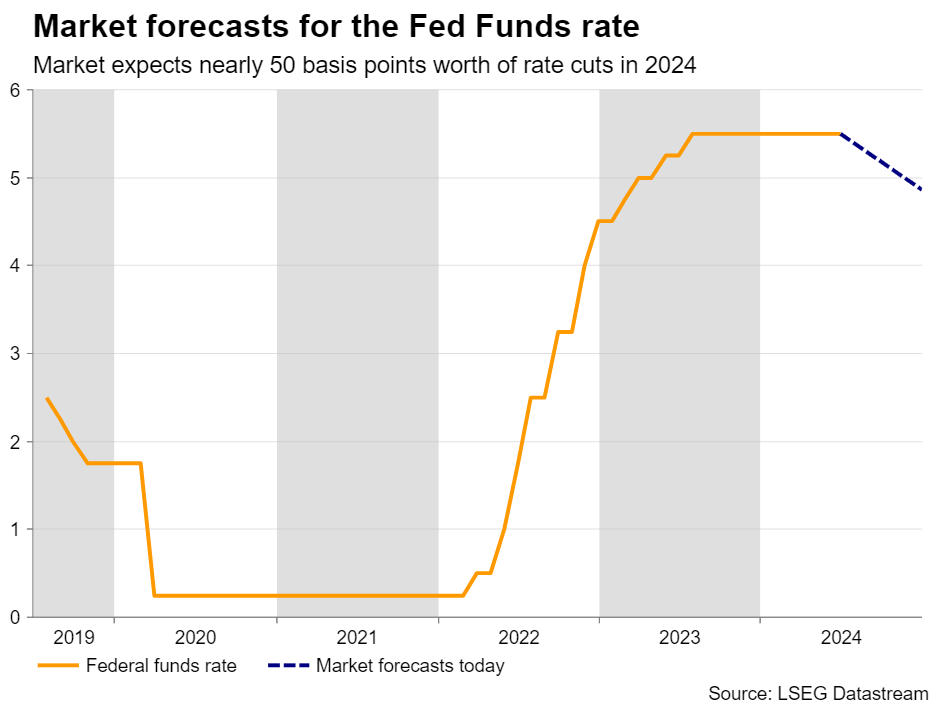

At its latest gathering, the FOMC appeared more hawkish than expected, revising its interest rate projections from three quarter-point reductions by the end of the year to just one. That said, the softer-than-expected CPI numbers a few hours ahead of the decision did not convince market participants about policymakers’ intentions.

The weaker than expected retail sales numbers for May and the slowdown in the core PCE price index for the same month corroborated that view. Indeed, according to Fed funds futures, investors are penciling in 48bps worth of reductions by December, assigning around a 75% probability for the first quarter-point rate cut to be delivered in September.

That said, the S&P Global PMIs for June suggested that the economy expanded at a faster pace than in May, which justifies remarks by Fed policymakers that there is no urgency in beginning to lower borrowing costs. However, the ISM manufacturing PMI on Monday came in weaker than expected, pointing to a third straight month of contraction in June.

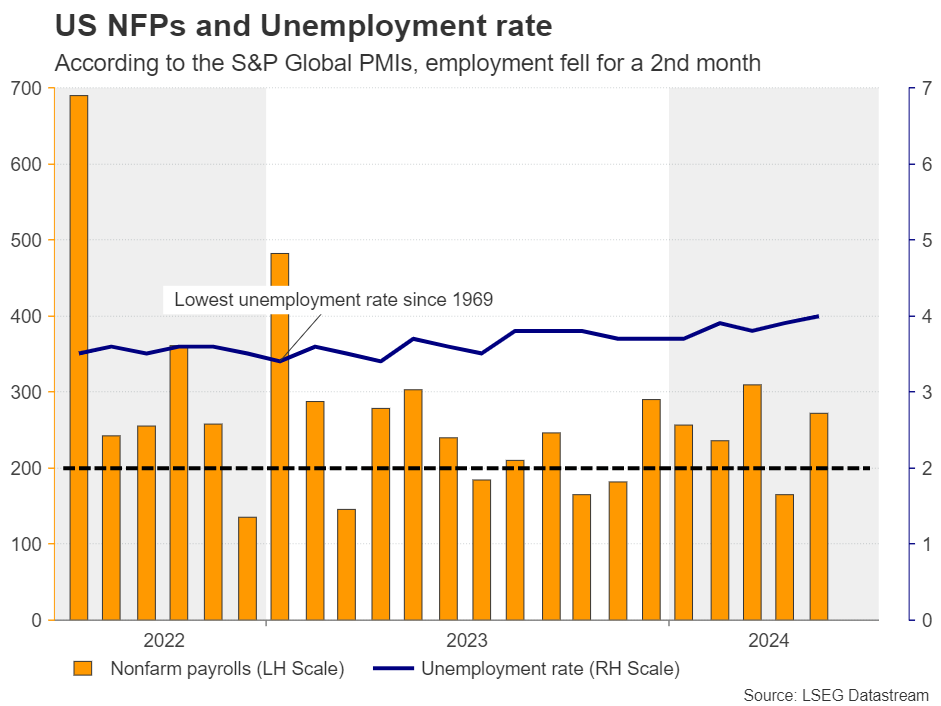

Job gains and wage growth to slow

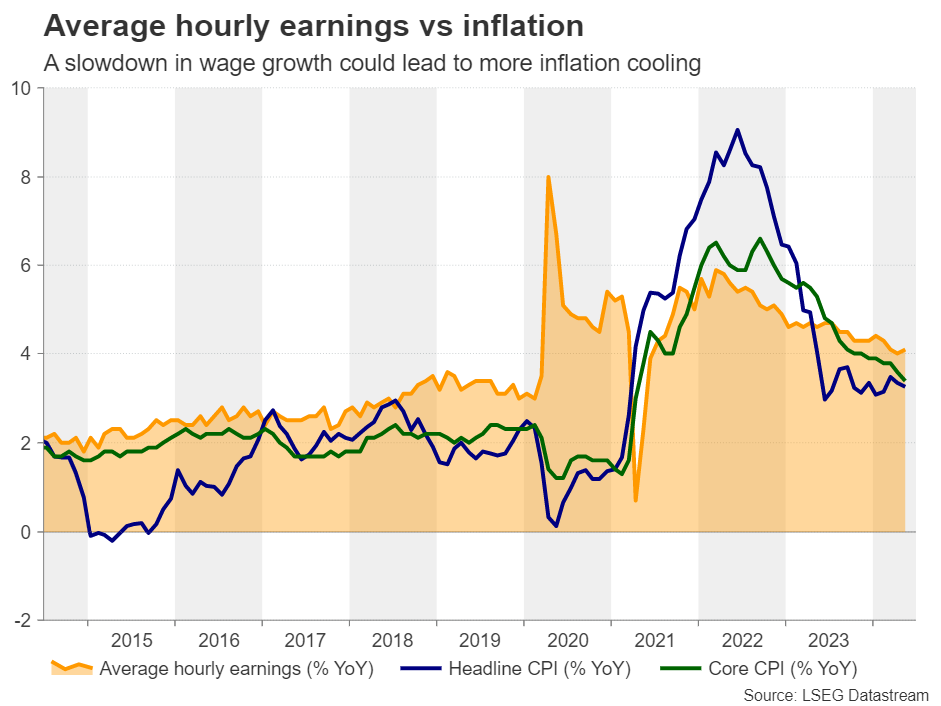

What could make the picture somewhat clearer may be Friday’s employment report for June. Nonfarm payrolls in the world’s largest economy are forecast to have increased by 195k, which is a notable slowdown from the astounding 272k a month before. The unemployment rate is expected to have held steady at 4.0%, while average hourly earnings are projected to have slowed to 3.9% from 4.1% y/y.

A potential slowdown in job gains is underscored by the increase in initial jobless claims during the month, which is indirectly supporting the notion of a pay slowdown, as having more available workers to choose from is allowing firms to offer less.

This could result in lower inflation in the months to come and thereby add more credence to investors’ view that interest rates in the US may need to be cut twice this year.

Dollar may come under pressure

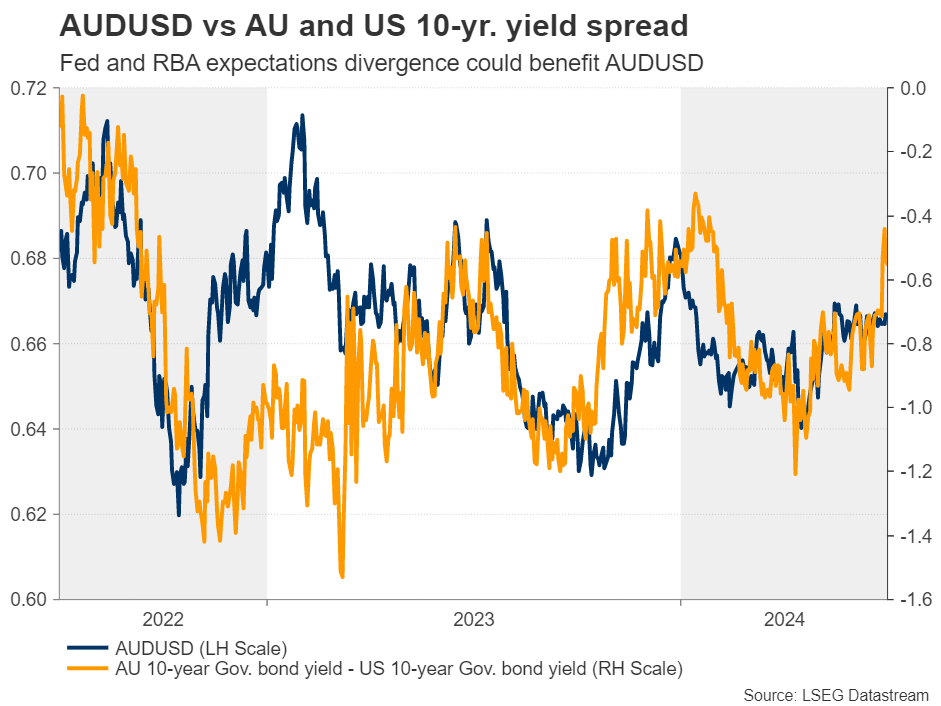

Ergo, in case of a weak employment report, Treasury yields could slip, thereby exerting pressure on the US dollar, which could suffer the most against its Australian counterpart. At its latest gathering, the RBA maintained its neutral stance, while Governor Bullock revealed that they discussed the option of raising rates. Due to that, the market is currently assigning a more than 50% chance for an RBA rate hike by November.

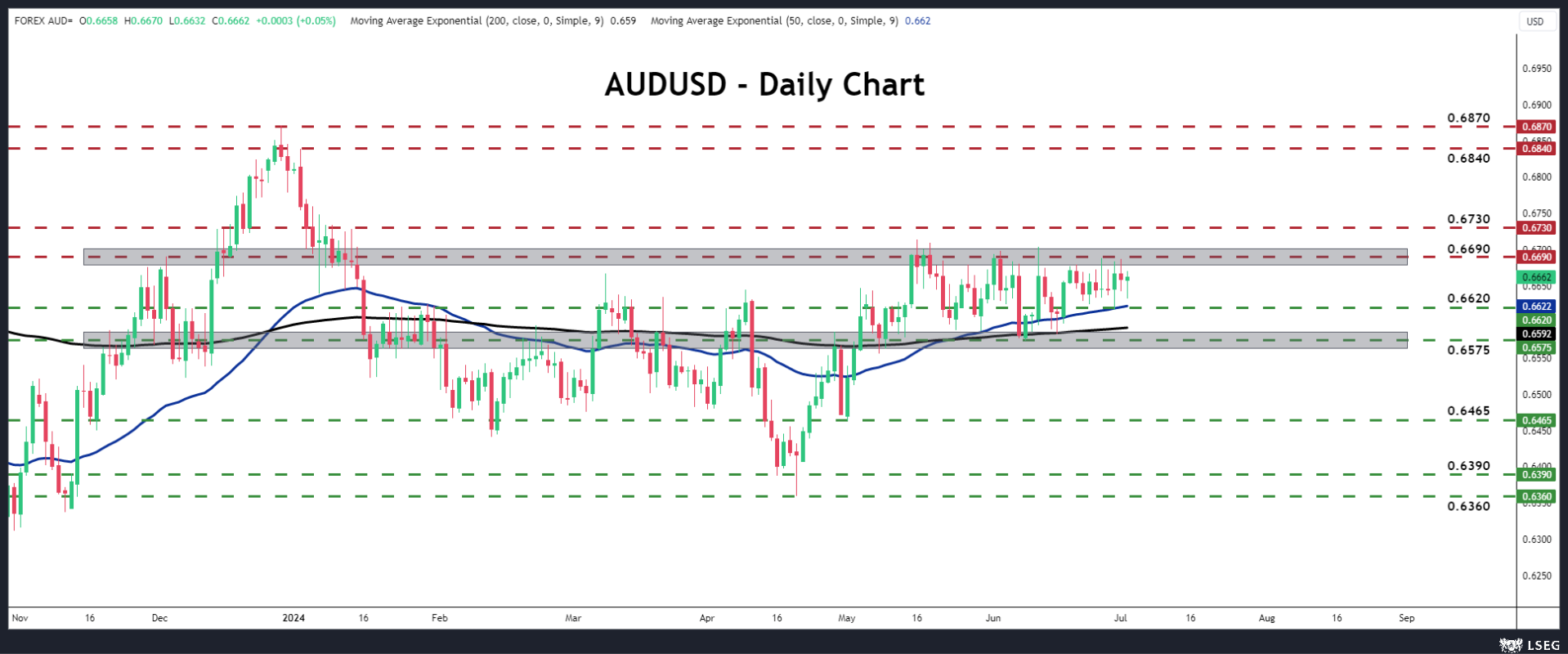

From a technical standpoint, aussie/dollar has been trading in a sideways range since May 3, between the 0.6575 and 0.6690 levels. Although the price is closer to the upper bound, until and if this barrier is breached, the outlook remains neutral.

A decisive break above 0.6690 could initiate a shift towards a more positive outlook, but the move carrying larger bullish implications may be a break above 0.6730. Such a move could pave the way towards the high of January 2, at around 0.6840. For the outlook to turn negative, the pair may need to slide below the 0.6575 zone, which is the lower end of the range.

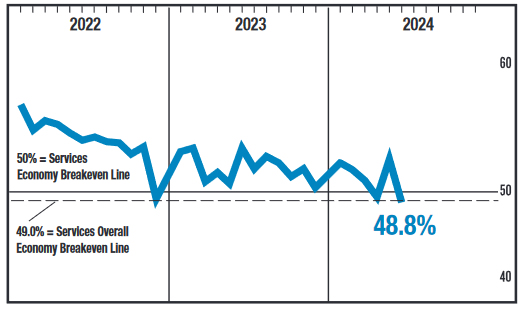

ISM Shows Services Sector Shrinks in June

The ISM Services index tumbled to 48.8 in June from 53.8 in May, well short of the 52.7 consensus expectation. Only eight of 18 industries reported growth for the month – down from 13 in May.

The business activity sub-index and new orders signaled shrinking activity, falling 11.6 and 6.8 percentage points, respectively, to 49.6 and 47.3.

The prices paid sub-component pulled back to 56.3 percentage points (pp) from 58.1 in May, while the supplier deliveries sub-index was little changed at 52.2 (52.7 in May).

The employment sub-component remained in contraction (46.1), indicating a fifth consecutive month of employment declines.

Key Implications

Things are getting choppy in the services sector. After a healthy bounce-back in activity last month, the ISM report showed the sector contracted again in June. While April's print was just on the wrong side of 50 (49.4), June's figure is now the second time in three months that the index is showing activity in the sector slowed. Moreover, unlike in April, both the business activity sub-index and the new orders index flashed contraction.

The employment index has been signaling contraction for five months now, and new orders and activity joined it in the red this month. After a long run of growth, the services sector looks to be running up against the weight of restrictive monetary policy and slowing consumer spending. For the Fed, this is another welcome signal that monetary policy is proving effective in cooling consumer demand beyond just the interest-rate sensitive goods sector.

Sunset Market Commentary

Markets

European markets today enjoyed some kind of a risk-on catch up move. A record close of the US S&P 500 above the 5500 mark yesterday apparently also inspired European investors (Eurostoxx 50 +1.3%). On French/intra-EMU bond markets, the risk premia also narrowed slightly further. The French 10-y spread over Bunds eased to 68 bps vs 74 bps two days ago and a peak of 82 bps last week. It suggests that the ‘Republican Front’ of the left-wing Nouveau Front Populair and President’s Macron’s Ensemble withdrawing more than 200 candidates from Sunday’s ballot to join forces, is seen as reducing the prospect for the Rassemblement National securing an absolute majority, in turn also tempering the risk of fiscal profligacy. Even so, the risk-on repositioning had only modest directional impact on European interest rate markets. German Bund yields are varying between +2.5 bps (2-y) and -3 bps (30-y) in a daily perspective (before the release of the US services ISM), tentatively backtracking on recent steepening move. Bunds also slightly underperform swaps. US markets still had some data to cope with going into an early close ahead of tomorrow’s 4th of July national holiday. Printing a 150k June job growth, the ADP private labour market report was marginally softer than expected (consensus 165k) and this also was the case for the jobless claims (initial claims 238k vs 235k expected, continuing claims raising further to 1858k, the highest since end 2021). US yields lost 2-3 bps across the curve after the data. In an appearance at the ECB symposium at Sintra NY Fed Williams didn’t join the recent ‘popular’ analyses of a higher neutral rate post the pandemic. He doesn’t see a U-turn in the longstanding decline in the R-star, but the high degree of uncertainty about the concept means one should not overly rely on it when setting appropriate monetary policy at a given point in time.

At time of finishing this report, the US services ISM fell off a cliff unexpectedly tumbling in contraction territory (48.8 from 53.8 vs 52.7 expected) with new orders (47.3 from 54.1) indicating more trouble ahead. Employment also eased further in contraction territory. Still prices paid remain elevated at 56.3. After modest declines in the wake of the softer labour market data, US yields extended decline to 5-7 bps across the curve.

Major FX cross rates mostly hold within established ranges. The European risk-on and softer US data help EUR/USD extending its rebound within the ST 1.0666/1.0916 trading range (1.08 from 1.0745). DXY retreats further from the 106+ area tested last week. The yen continues its negative record race even against a weaker dollar, with USD/JPY reaching the highest level since December 1986. Question remains was pace of decline Japanese authorities see as too disorderly to warrant FX interventions. No pre-election stress for sterling, with the UK currency even gaining a few ticks against a well-performing euro (EUR/GBP 0.8465).

News & Views

The Swedish services PMI rebounded more than expected in June, bouncing back to growth (51.8) following two months in contractionary territory. Details were encouraging. Accelerating new orders (52.5) suggest that business volumes will increase from the current modest expansion (50.2). Planned business volumes effectively point to stronger growth (55.5). Firms held the employment status quo (50.1) after downsizing in May. Simultaneously, the disinflationary trend in suppliers’ input prices is extended (53.7 from 54.2), giving backing to the Riksbank’s policy guidance of two or three more policy rate cuts this year. The Swedish krone is a tad stronger at EUR/SEK 11.35.

News agency Reuters suggests that (at least) six ECB policy makers are urging a review of the aggressive monetary stimulus policies the ECB employed for nearly a decade to tackle low inflation, judging that they may have done more harm than good. Especially the massive liquidity injection via asset purchases is under scrutiny. The Bank of International Settlements in its recent annual review also questioned the debate about QE’s effectiveness. Especially when it is used intensively and for very long to respond to long-term issues which should actually be tackled by governments rather than central banks. The now symmetric 2% inflation target could help avoiding the same mistakes in the future.

Graphs

EUR/PLN zloty well protected as NBP confirms hawkish hold.

Eurostoxx 50 rebounds as EMU risk premia ease as France’s Republican Front joins forces.

USD/JPY: yen at 38-year low as Japanese authorities stay sidelined for now.

French 10-y yields eases of the second consecutive day as countdown to second round of elections continues.

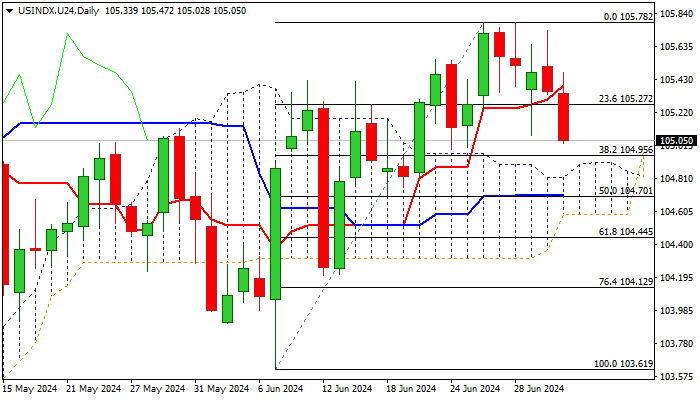

Dollar Index Outlook: Dollar Extends Weakness after Downbeat ADP Data

The dollar index fell to one week low on Thursday, extending weakness into second consecutive day, after being pressured by dovish comments from Fed Chair Powell, while weaker than expected ADP private sector payrolls report further soured the sentiment.

Fresh acceleration lower broke below daily Tenkan-sen and is pressuring pivotal supports at 105.00/104.90 zone (psychological / Fibo 38.2% of 103.61/105.78 / daily cloud top).

Firm break here to generate initial reversal signal and open way for further retracement of 103.61/105.78 rally.

Technical picture is weakening on daily chart and supports scenario, however, increased headwinds likely to be expected at 105 zone.

Markets await release of US services PMI (June 56.7 f/c vs May 58.1) which could further weaken near-term structure on June figure at / below consensus).

US Labor report on Friday will be also closely watched as one of this week’s key economic events.

Res: 105.27; 105.39; 105.50; 105.78.

Sup: 105.00; 104.90; 104.70; 104.44.

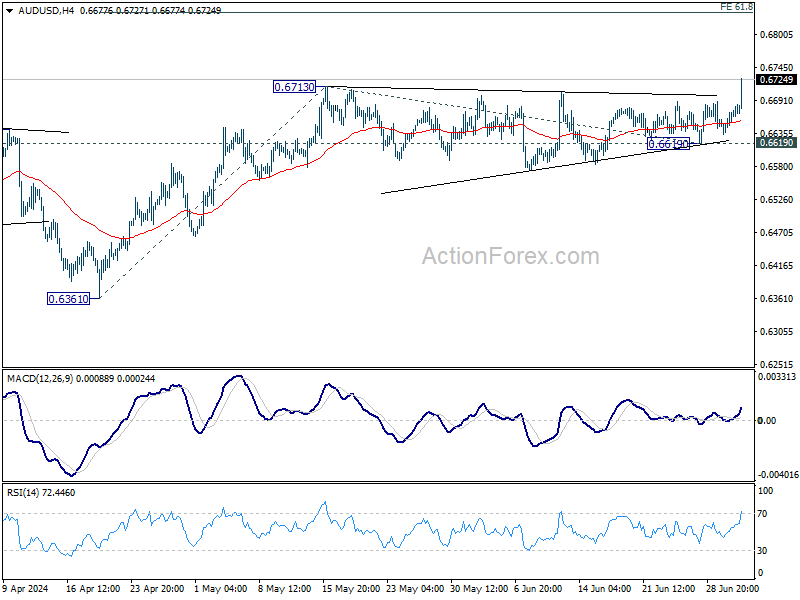

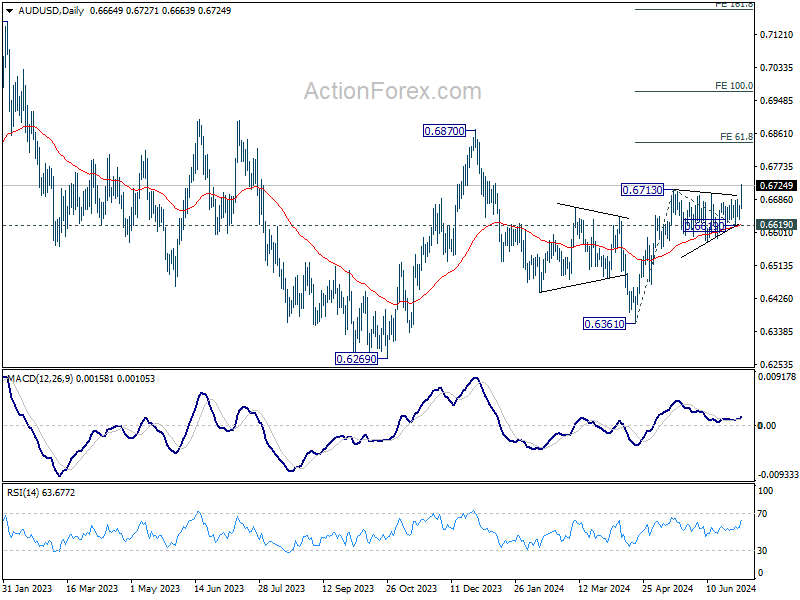

AUD/USD Daily Report

Daily Pivots: (S1) 0.6644; (P) 0.6657; (R1) 0.6681; More...

AUD/USD's rally from 0.6361 finally resumed by breaking through 0.6713 resistance and intraday bias is back on the upside. Further rise should be seen to 61.8% projection of 0.6361 to 0.6713 from 0.6619 at 0.6837 next. For now, near term outlook will stay bullish as long as 0.6619 support holds, in case of retreat.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

US ISM services falls sharply to 48.8, lowest in four years

US ISM Services PMI fell sharply from 53.8 to 48.8 in June, well below expectation of 52.5. That's also the worst reading in four years. Looking at some details, business activity/production fell sharply from 61.2 to 49.6. New orders fell from 54.1 to 47.3. Employment fell from 47.1 to 46.1. Prices fell slightly from 58.1 to 42.9.

ISM said: "The past relationship between the Services PMI and the overall economy indicates that the Services PMI for June (48.8 percent) corresponds to no increase in real gross domestic product (GDP) on an annualized basis."

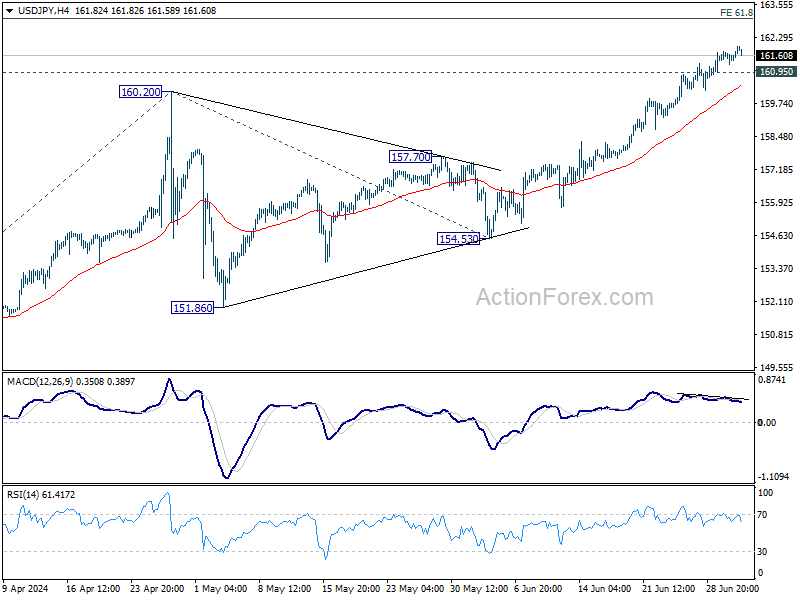

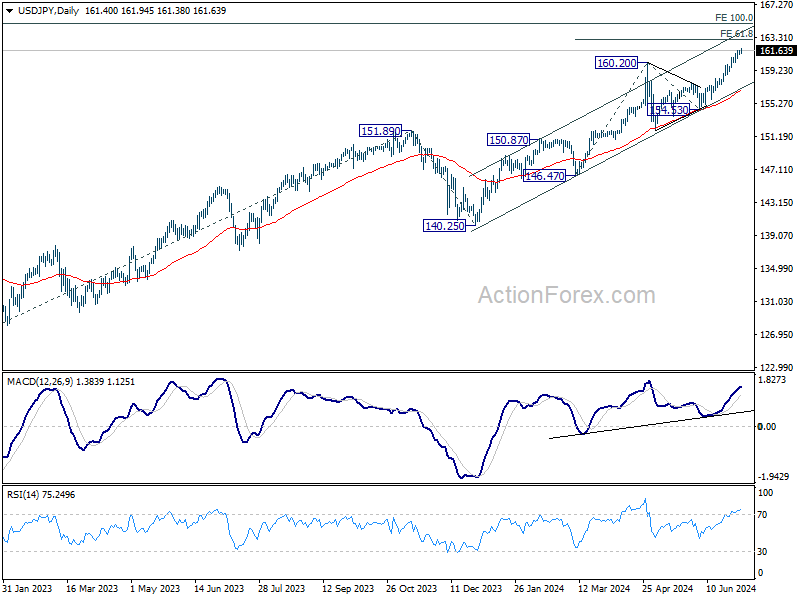

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 161.22; (P) 161.52; (R1) 161.76; More...

Intraday bias in USD/JPY remains on the upside for the moment. Current up trend should target 61.8% projection of 146.47 to 160.20 from 154.53 at 163.01. On the downside, below 160.95 minor support will turn intraday bias neutral and bring consolidations again, before staging another rally.

In the bigger picture, long term up trend is still in progress. Further rise is expected as long as 154.53 support holds. Next target is 100% projection of 127.20 (2023 low) to 151.89 (2023 high) from 140.25 at 164.94.

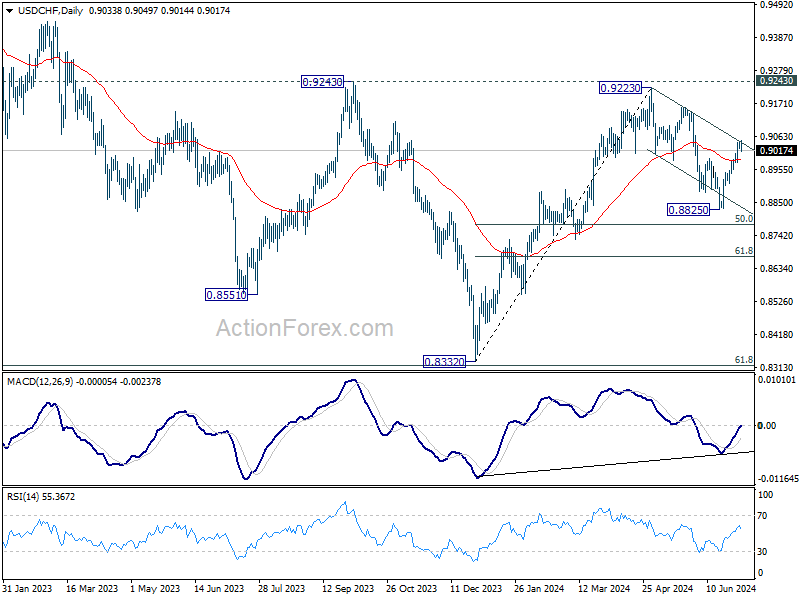

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.9026; (P) 0.9038; (R1) 0.9052; More…

Intraday bias in USD/CHF is turned neutral first with current retreat. Further rise is mildly in favor as long as 0.8956 support holds. Above 0.9049 will affirm the case that corrective fall from 0.9223 has completed at 0.8825. Further rally would then be seen to 0.9157 resistance next. However, firm break of 0.8956 will bring retest of 0.8825 support instead.

In the bigger picture, focus remains is now on 0.9223/9243 resistance zone. Decisive break there would complete a head and shoulder bottom pattern (ls: 0.8551; h: 0.8332; rs: 0.8825). That would indicate larger bullish trend reversal. Nevertheless, rejection by 0.9223/43 will keep medium term outlook neutral at best, for more range trading between 0.8332/9243 first.

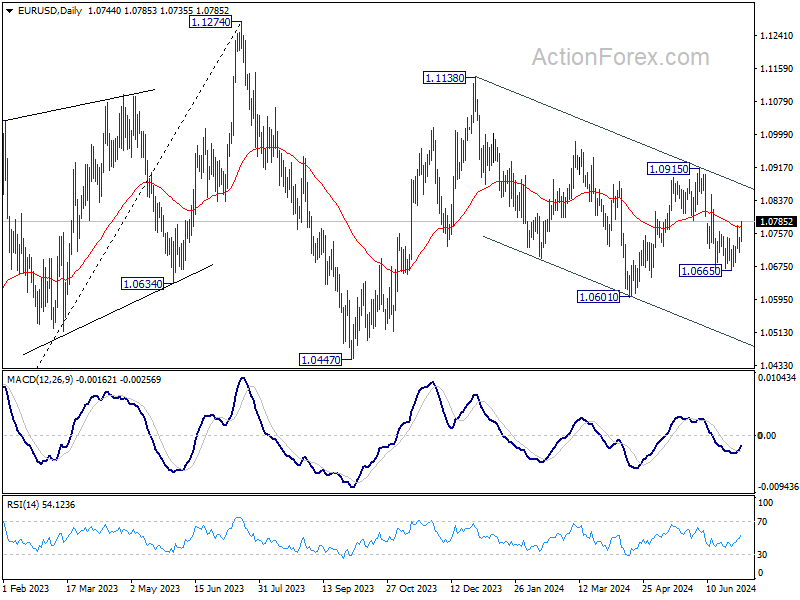

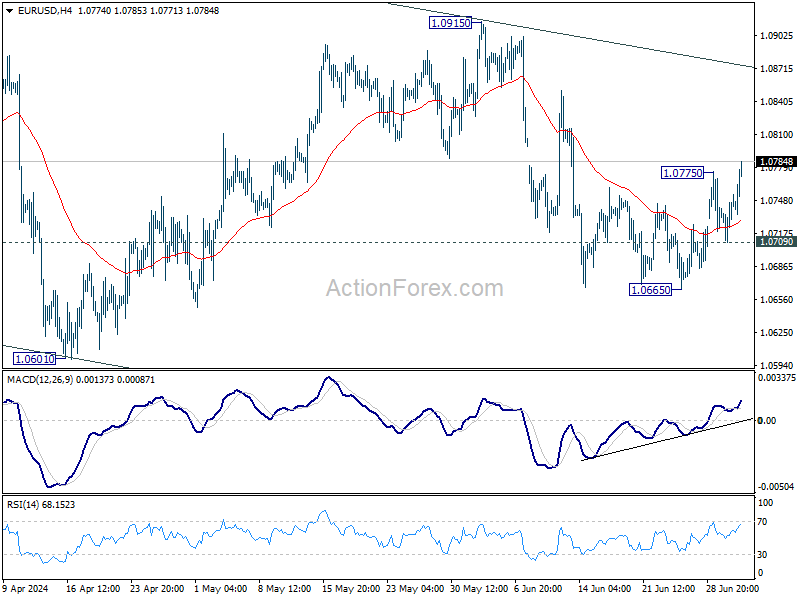

EUR/USD Mid-Day Outlook

Daily Pivots: (S1) 1.0721; (P) 1.0735; (R1) 1.0760; More....

EUR/USD's rebound from 1.0665 resumed by breaking 1.0775 minor resistance today. Current development suggests that pull back from 1.0915 has completed. Intraday bias is back on the upside for 1.0915 resistance next. For now, risk will stay on the upside as long as 1.0709 support holds, in case of retreat.

In the bigger picture, price actions from 1.1274 are viewed as a corrective pattern that's still in progress. Break of 1.0601 will target 1.0447 support and possibly below. On the upside, firm break of 1.0915 resistance will start another rising leg back to 1.1138 resistance instead.