Sample Category Title

AUD/USD Daily Report

Daily Pivots: (S1) 0.6588; (P) 0.6599; (R1) 0.6623; More...

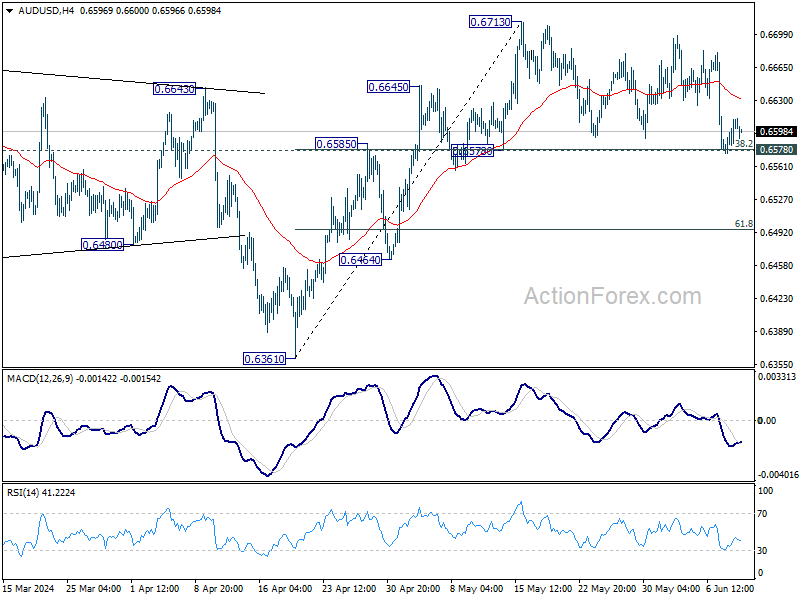

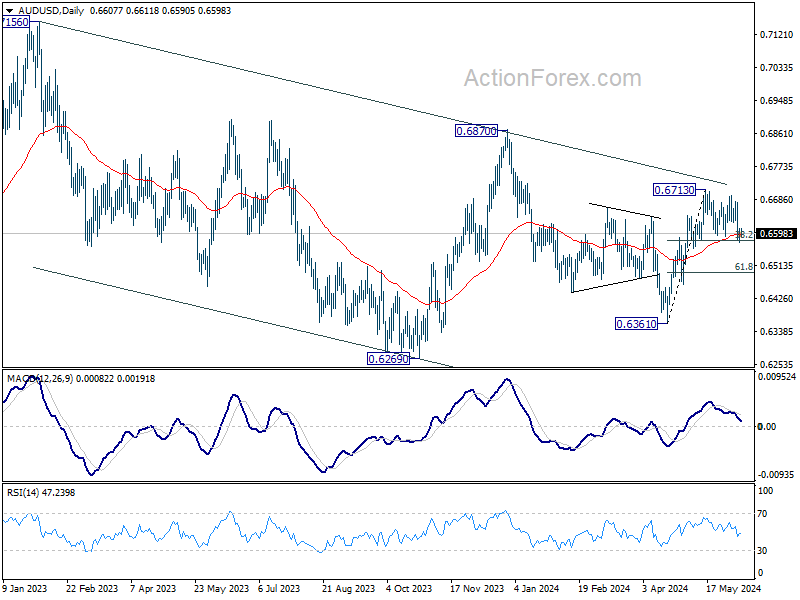

Intraday bias in AUD/USD remains neutral at this point. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

Aussie Down on Risk Sentiment and Business Confidence, Yen Also Soft

Australian Dollar is trading broadly lower today, primarily due to selloff in stocks in Hong Kong and China as markets reopened after holiday. This downward pressure is compounded by the decline in Australian business confidence, which turned negative. ANZ has become the first of the big four banks to push its forecast for RBA next rate cut from November this year to February 2025. However, this adjustment has provided little immediate support for Aussie .

Japanese Yen is also experiencing selling pressure, making it the second weakest currency for the day at this point. Japanese Finance Minister Shunichi Suzuki did not make any new comments about Yen's recent depreciation. Nevertheless his remarks last Friday emphasized that any foreign exchange intervention would depend on necessity and effectiveness. Investors are now closely watching the upcoming BoJ meeting, with speculation that the central bank might start tapering its bond purchases.

Meanwhile, Euro is making a modest recovery from yesterday's selloff but remains the weakest performer for the week. Euro's rebound is limited, indicating persistent concerns about the region's political uncertainty. In contrast, British Pound is showing mild strength as markets anticipate upcoming job data.

Dollar is holding onto some of its recent gains, though it lacks the momentum for a significant rally. Market participants are cautious, likely waiting for tomorrow's US. CPI data release and FOMC rate decision, along with the updated dot plot, which will provide clearer guidance on Fed's policy easing path.

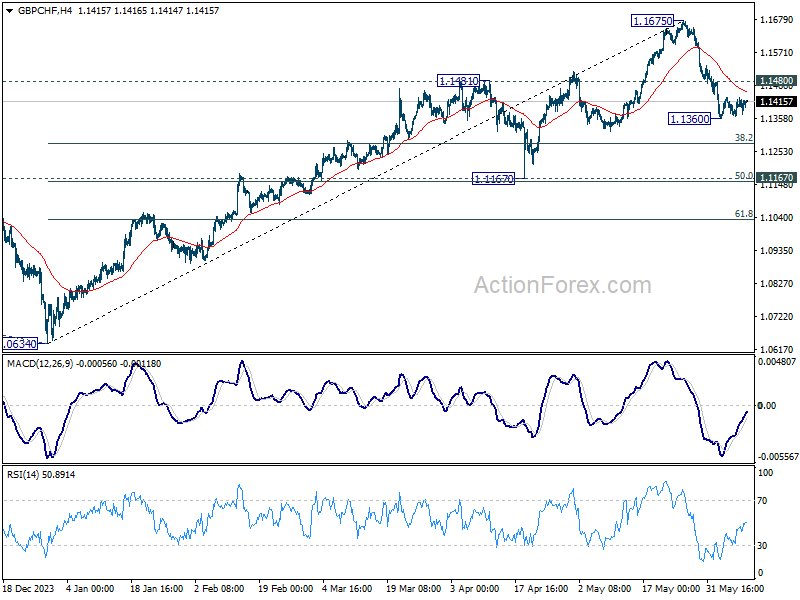

Technically, GBP/CHF stabilized after dipping to 1.1360 last week but lacked momentum for recovery. Risk will stay on the downside as long as 1.1480 minor resistance holds. Below 1.1360 will target 38.2% retracement of 1.0634 to 1.1675 at 1.1277 and below. But strong support should be seen around 1.1167 (50% retracement at 1.1155) to bring rebound, at least on first attempt.

In Asia, at the time of writing, Nikkei is up 0.36%. Hong Kong HSI is down -1.66%. China Shanghai SSE is down -1.15%. Singapore Strait Times is down -0.24%. Japan 10-year JGB yield is down -0.016 at 1.023. Overnight, DOW rose 0.18%. S&P 500 rose 0.26%. NASDAQ rose 0.35%. 10-year yield rose 0.039 to 4.469.

ECB's Lagarde: No linear path for interest rate cuts

In a joint interview with four European newspapers, ECB President Christine Lagarde dismissed the notion that last week's quarter-point rate cut would be the start of a series of similar moves. Lagarde made it clear that "interest rates will not necessarily move downward in a straightforward manner."

"We are not following a pre-determined path," she explained, noting that "there could be periods where we leave interest rates unchanged."

When asked if rates could remain unchanged for multiple meetings, Lagarde said, "It's possible. We need to observe how labor costs evolve and ensure that earnings continue to absorb the recent increases."

Lagarde emphasized ECB's ongoing efforts to control inflation, stating, "We are still in tightening territory and will continue as long as necessary to bring inflation back to 2 percent."

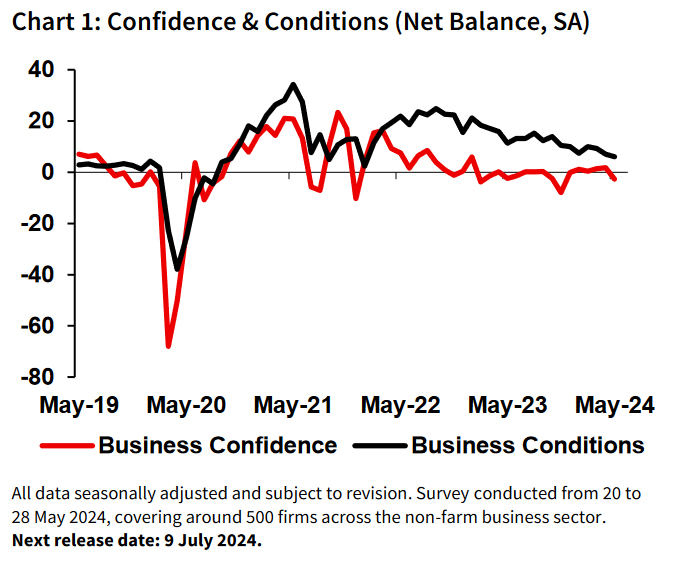

Australia's NAB business confidence returns to negative, inflation pressures re-emerge

Australia's NAB Business Confidence fell from 2 to -3 in May, returning to negative territory. Business conditions also saw a slight decline, dropping from 7 to 6. Specifically, trading conditions decreased from 13 to 10, and profitability conditions fell from 6 to 3. However, employment conditions improved, rising from 2 to 5.

NAB Chief Economist Alan Oster noted pointed out that forward orders are particularly weak in retail, wholesale, and construction sectors, indicating potential challenges ahead. Despite a slowdown in activity, capacity utilization remains above average, suggesting that the "process of bringing supply and demand back into balance remains incomplete".

Inflationary pressures are re-emerging, with labor cost growth increasing to 2.3% on a quarterly basis, up from 1.5% in April. Purchase cost growth also rose to 1.9%, compared to 1.3% previously. Overall product price growth climbed to 1.1%, up from 0.8%, with retail price growth increasing to 1.6% from 1.0%, and recreation and personal services prices edging up to 1.0% from 0.9%.

Oster concluded that the data presents a "mixed" picture for RBA. There are clear signs of growth challenges, yet inflationary pressures remain a concern. "We expect the RBA to keep rates on hold for some time yet as they navigate through these contrasting risks."

Looking ahead

UK job data is the main focus in European session. Later in the day, US will release NFIB business optimism index. Canada will publish building permits.

AUD/USD Daily Report

Daily Pivots: (S1) 0.6588; (P) 0.6599; (R1) 0.6623; More...

Intraday bias in AUD/USD remains neutral at this point. On the upside, firm break of 0.6713 will resume whole rise from 0.6361 to 0.6870 resistance next. However, sustained break of 0.6578 cluster support (38.2% retracement of 0.6361 to 0.6713 at 0.6579) will dampen this bullish view, and bring deeper fall to 61.8% retracement at 0.6495.

In the bigger picture, price actions from 0.6169 (2022 low) are seen as a medium term corrective pattern to the down trend from 0.8006 (2021 high). Fall from 0.7156 (2023 high) is seen as the second leg, which could have completed at 0.6269 already. Rise from there is seen as the third leg which is now trying to resume through 0.6870 resistance.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y May | 1.90% | 2.10% | 2.20% | |

| 01:30 | AUD | NAB Business Confidence May | -3 | 1 | ||

| 01:30 | AUD | NAB Business Conditions May | 6 | 7 | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Apr | 4.30% | 4.30% | ||

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Apr | 5.70% | 5.70% | ||

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Apr | 6.00% | 6.00% | ||

| 06:00 | GBP | Claimant Count Change May | 10.2K | 8.9K | ||

| 10:00 | USD | NFIB Business Optimism Index May | 89.8 | 89.7 | ||

| 12:30 | CAD | Building Permits M/M Apr | 5.20% | -11.70% |

Elliott Wave Analysis Expects Gold (XAUUSD) to Pullback a Bit More

Short Term Elliott Wave in Gold (XAUUSD) suggests the rally from 5.03.2024 low ended a wave 3 at 2450.10 high. Wave 4 pullback is currently in progress. The internal subdivision of wave 4 takes the form of a double three Elliott Wave structure. Down from wave 3, wave (a) ended at 2407.15 low and wave (b) bounce ended at 2433.90. The stock extended lower in wave (c) towards 2325.20 which completed wave ((w)) in higher degree.

The market rallied starting wave ((x)) taking the form expanded flat structure. Up from wave ((w)), wave (a) ended at 2364.12 and pullback in wave (b) ended at 2314.40. Wave (c) higher finish at 2387.71 which completed wave ((x)). XAUUSD continued lower strongly in wave ((y)) of 4. Down from wave ((x)) Wave (a) of ((y)) ended at 2286.50 as an impulsive structure. Wave (b) bounce could already end at 2313.8 and the metal has turned lower in wave (c). Near term, while below 2387, it should continue lower in wave (c) of ((y)) to the extreme 100% – 161.8% Fibonacci area of wave ((a)). This area comes at 2262 – 2185 area where buyers should be waiting to continue the rally or see 3 swings higher at least.

XAUUSD 60 Minutes Elliott Wave Chart

XAUUSD Elliott Wave Video

https://www.youtube.com/watch?v=F4Gw2rjIACs

Australia’s NAB business confidence returns to negative, inflation pressures re-emerge

Australia's NAB Business Confidence fell from 2 to -3 in May, returning to negative territory. Business conditions also saw a slight decline, dropping from 7 to 6. Specifically, trading conditions decreased from 13 to 10, and profitability conditions fell from 6 to 3. However, employment conditions improved, rising from 2 to 5.

NAB Chief Economist Alan Oster noted pointed out that forward orders are particularly weak in retail, wholesale, and construction sectors, indicating potential challenges ahead. Despite a slowdown in activity, capacity utilization remains above average, suggesting that the "process of bringing supply and demand back into balance remains incomplete".

Inflationary pressures are re-emerging, with labor cost growth increasing to 2.3% on a quarterly basis, up from 1.5% in April. Purchase cost growth also rose to 1.9%, compared to 1.3% previously. Overall product price growth climbed to 1.1%, up from 0.8%, with retail price growth increasing to 1.6% from 1.0%, and recreation and personal services prices edging up to 1.0% from 0.9%.

Oster concluded that the data presents a "mixed" picture for RBA. There are clear signs of growth challenges, yet inflationary pressures remain a concern. "We expect the RBA to keep rates on hold for some time yet as they navigate through these contrasting risks."

ECB’s Lagarde: No linear path for interest rate cuts

In a joint interview with four European newspapers, ECB President Christine Lagarde dismissed the notion that last week's quarter-point rate cut would be the start of a series of similar moves. Lagarde made it clear that "interest rates will not necessarily move downward in a straightforward manner."

"We are not following a pre-determined path," she explained, noting that "there could be periods where we leave interest rates unchanged."

When asked if rates could remain unchanged for multiple meetings, Lagarde said, "It's possible. We need to observe how labor costs evolve and ensure that earnings continue to absorb the recent increases."

Lagarde emphasized ECB's ongoing efforts to control inflation, stating, "We are still in tightening territory and will continue as long as necessary to bring inflation back to 2 percent."

Instrument of the Week (June 10—14): GBPJPY Insight

The GBPJPY pair reflects the exchange rate between the British Pound and the Japanese Yen, influenced by the economic conditions and monetary policies in the United Kingdom and Japan. The British Pound is affected by UK economic indicators, political events, and the Bank of England decisions. On the other hand, the Japanese Yen is impacted by the health of Japan's economy, global risk sentiment, and the monetary policies of the Bank of Japan. This currency pair is known for its volatility, making it attractive for traders interested in the dynamic interplay between these two major economies.

Japan gross domestic product (GDP) QoQ, June 10, 01:50 (GMT+2)

The forecast for Japan’s GDP indicates a contraction of -0.5% this quarter, down from the previous growth of 0.1%. If the GDP drops more severely than the expected -0.5%, it would suggest a worsening economic situation in Japan. This will potentially drive investors toward safer assets and weaken the Yen against the Pound, thus increasing the GBPJPY rate. Conversely, if the GDP shows a reduction that is less than expected or unexpectedly grows, it would enhance investor confidence in the Japanese economy, strengthening the Yen and potentially decreasing the GBPJPY rate as the Yen appreciates.

UK gross domestic product (GDP) MoM, June 12, 08:00 (GMT+2)

The forecast for the UK’s monthly GDP is an increase of 0.2%, signaling a slowdown from the previous month’s growth of 0.4%. Meeting or surpassing this forecast could reinforce the positive outlook on the UK’s economic resilience, thereby supporting the Pound’s strength and potentially pushing the GBPJPY rate up. Conversely, if GDP growth is less than expected, suggesting economic stagnation or a downturn, it could weaken the Pound due to fading investor confidence. This weaker stance would likely push the GBPJPY rate downward as market participants might shift their investments towards safer or more stable currencies, including the Yen.

In the daily timeframe, GBPJPY, in a long-term bullish trend, has formed an upward channel and reached an important resistance area. The market has strong bullish sentiments, and many indicators show further upside opportunities.

- If the bulls push the price above the 200,000 resistance, GBPJPY will reach 206,000, which corresponds to 161.8 Fibonacci;

- However, if the price bounces off the resistance, it could correct to 197.000 and then start rising to 206.000.

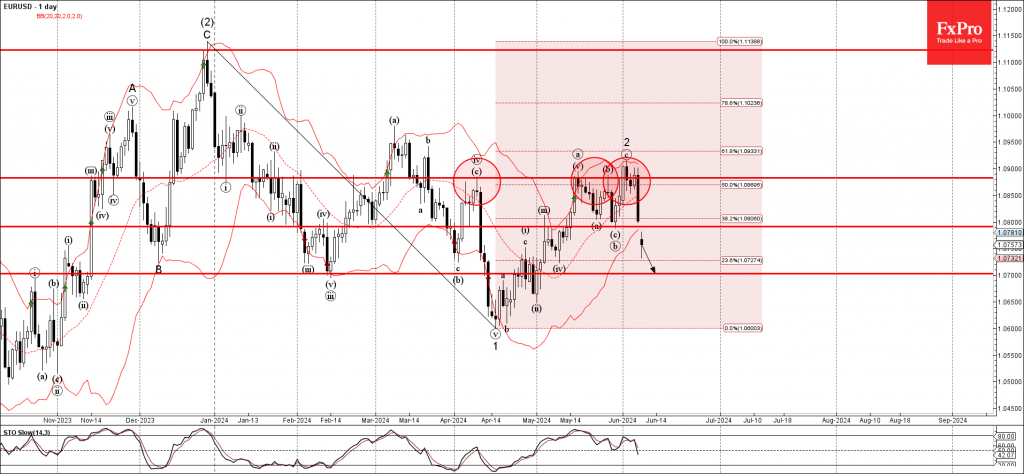

EURUSD Wave Analysis

- EURUSD under bearish pressure

- Likely to fall to support level 1.0700

EURUSD currency pair under the bearish pressure after the earlier breakout of the support level 1.0800 (which stopped the previous wave (b) at the end of May).

The breakout of the support level 1.0800 accelerated the active short-term impulse wave 3 from the start of June.

Given the strongly bearish euro sentiment and the continuation of the bullish USD sentiment, EURUSD currency pair be expected to fall further to the next support level 1.0700.

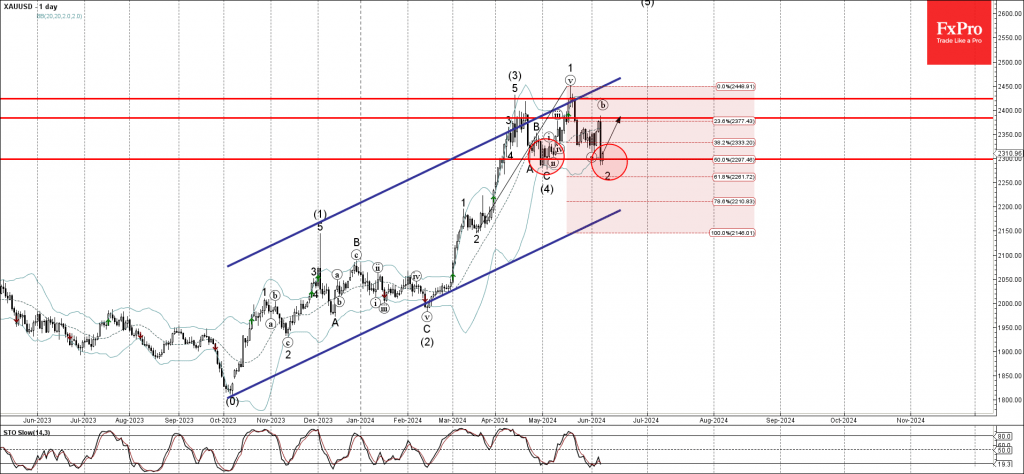

Gold Wave Analysis

- Gold reversed from support level 2300.00

- Likely to rise to resistance 2385.00

Gold recently reversed up from the pivotal support level 2300.00 (which stopped the previous waves A, (4) and ii, as can be seen below).

The support level 2300.00 was strengthened by the lower daily Bollinger Band and by the 50% Fibonacci correction of the previous upward impulse from March.

Given the clear daily uptrend and the still oversold daily Stochastic, Gold be expected to rise further to the next resistance 2385.00, top of the previous correction b.

Fed Pivot Less Likely After Strong NFP, Focus on CPI Report and Dot Plot

- A dovish pivot by the Fed is looking less likely at the June meeting

- Will Fed officials flag two or just one rate cut after strong jobs data?

- CPI report will also be crucial on Wednesday (12:30 GMT)

- Statement due at 18:00 GMT will be followed by press conference at 18:30 GMT

One step forward, two steps back

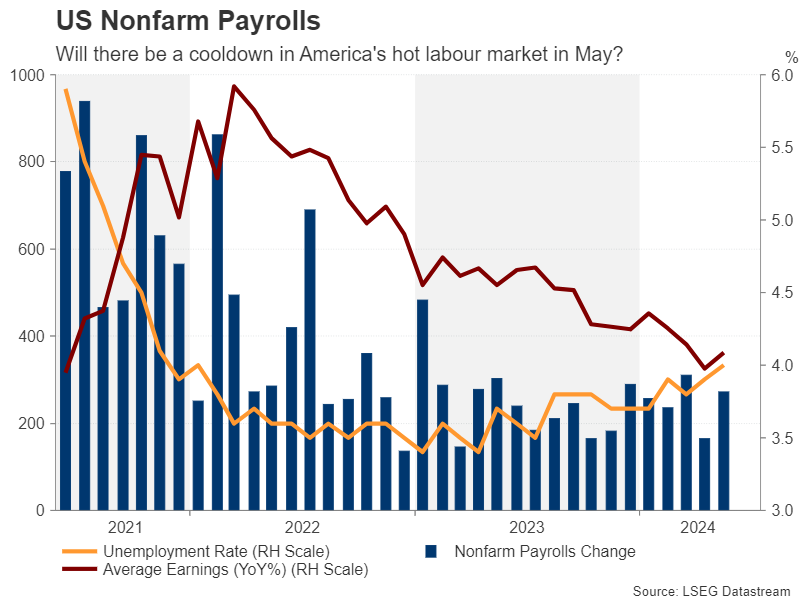

After a run of consistently hot data on inflation and the economy all year, it briefly seemed like the tide was turning for early rate cut hopes. The last two sets of inflation readings were somewhat soft, while recent growth indicators have been a bit patchy. But the optimism didn’t last long as Friday’s nonfarm payrolls report threw a spanner in the works, dashing expectations that the long-anticipated Fed pivot could come as early as the June policy meeting.

The Fed is now not only certain to keep interest rates unchanged on Wednesday, but it’s also likely to maintain its higher for longer stance. The May jobs report has given Federal Open Market Committee (FOMC) members little room to manoeuvre. A payrolls print of 272k is hardly a sign that the labour market or the economy as a whole are in trouble. The slight pickup in yearly wage growth is also slightly concerning.

Making sense of the data

The only ‘relief’ in the jobs numbers was the unexpected increase in the unemployment rate to 4.0%, which broke a 27-month streak of holding below that level. Usually, whenever the payrolls establishment survey diverges from the separate household survey that’s conducted to gauge the jobless rate, one of them tends to get revised.

Hence, policymakers will probably avoid trying to read too much into the data, but at the very least, the May figures have lessened the urgency for a dovish tilt. With the mixed data continuing to cast a cloud over the policy path, the Fed will not want to deviate much from its recent language in the statement.

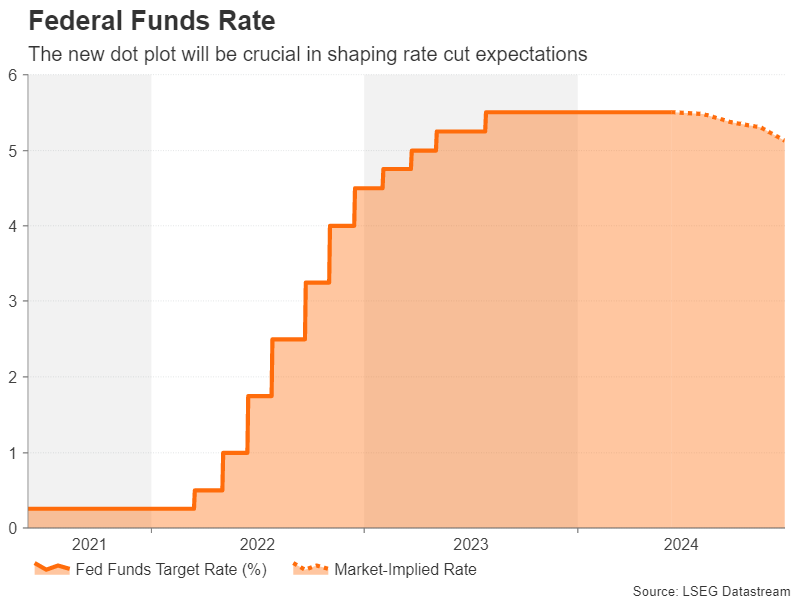

Dot plot: one vs two cuts

However, the central bank will also be publishing updated economic projections, including its famous dot plot. A number of Fed officials have hinted at just one rate cut this year so should the median dot plot point to a single 25-basis-point reduction compared to three in the March dot plot, that would be perceived as a hawkish signal. But if FOMC members pencil in two cuts, that would keep alive hopes of a September move.

At the moment, the odds seem to be swaying towards just one cut, while the markets are caught somewhere between one and two. The CPI numbers to be released earlier in the day could prove decisive for the tone of the statement as well as Chair Powell’s press conference, though they might come too late for influencing the dot plot.

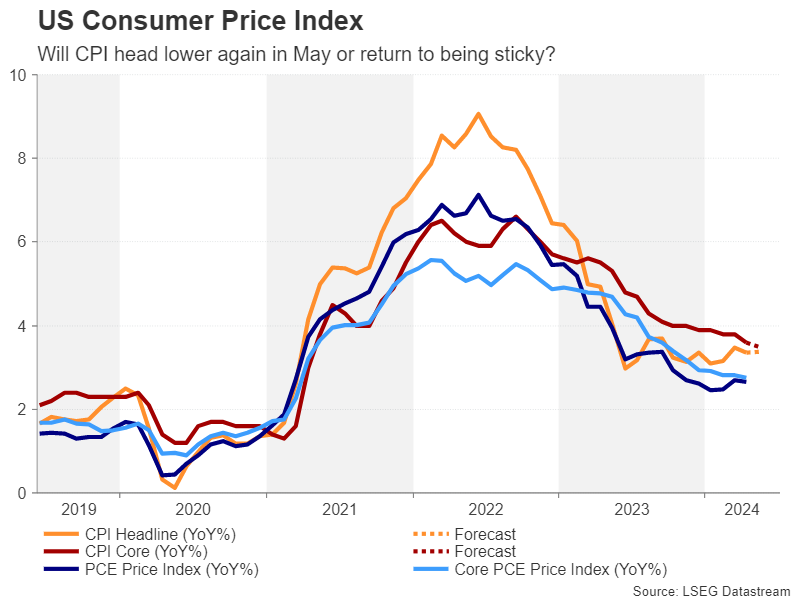

One eye on CPI

After easing to 3.4% y/y in April, headline CPI is forecast to have stayed unchanged in May, although the month-on-month print is expected to have moderated from 0.3% to 0.1%. It’s the opposite case for core CPI, with the month-on-month rate maintaining a 0.3% pace, but the annual rate is forecast to ease from 3.6% to 3.5%.

If the CPI figures are more or less in line with expectations, that would keep the Fed on its current path, which means a September cut is still possible but unlikely unless there’s a significant drop in inflation or a deterioration in the labour market over the summer.

Dollar bulls back in charge

For the US dollar, a reaffirmation of ‘higher for longer’ would help to keep it on the front foot, although against the Japanese yen, investors should also keep an eye on the Bank of Japan policy decision due on Friday.

Last week’s strong ISM services PMI and robust payrolls readings aided the greenback to bounce off the 50-day moving average (MA) and climb back above 156.00 yen. A mostly hawkish outcome on Wednesday could push the pair above the May top of 157.76 before the 161.8% Fibonacci extension of the November-December downtrend comes into view at 159.14.

However, a dovish outcome could push the pair below the 50-day (MA), which would clear the way for a retest of the May low near the 152.00 level.

A lot can happen until September

In a nutshell, there’s a sizeable risk of both a dovish and hawkish surprise at the June meeting depending on how hot or soft the CPI stats are. However, in either scenario the Fed might prefer not to reveal much about its future course of action. After all, there’s still the July meeting to communicate a policy shift before September, not to mention the Jackson Hole symposium in August.

As tempting as it might be for Powell to drop some hints should he get asked to comment on last week’s ECB and Bank of Canada rate cuts, he’ll probably strike a balanced tone as he has done in recent public appearances.

For the markets, the biggest fear is stagflation. But the NFP report just slashed those risks, making a soft landing the base case once again and therefore a panic selloff on Wall Street from upbeat CPI data less likely.