Sample Category Title

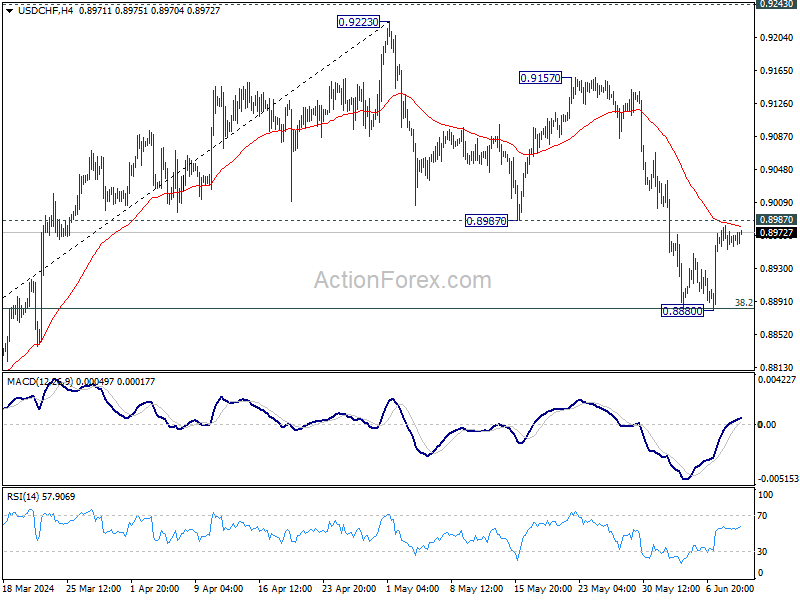

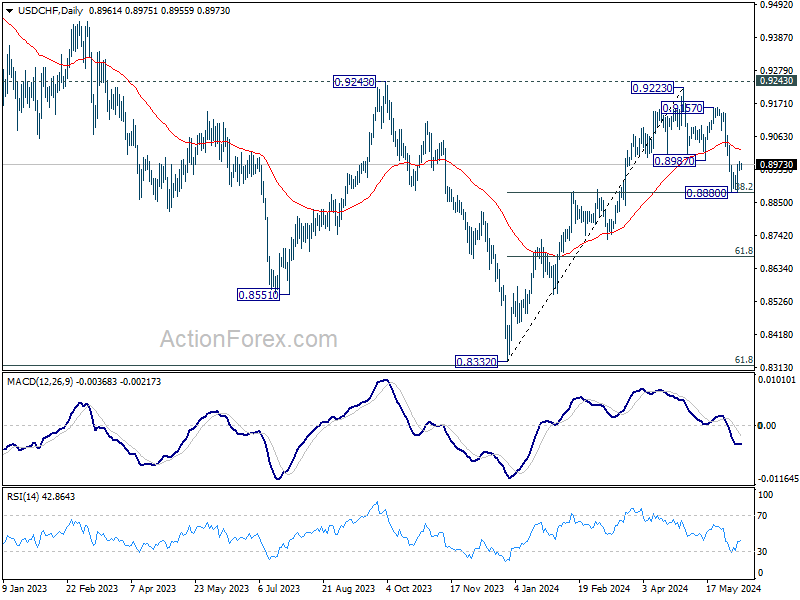

USD/CHF Mid-Day Outlook

Daily Pivots: (S1) 0.8952; (P) 0.8969; (R1) 0.8982; More….

USD/CHF is still bounded in range of 0.8880/8987 and intraday bias remains neutral. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone. Nevertheless, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

USD/JPY Mid-Day Outlook

Daily Pivots: (S1) 155.57; (P) 156.33; (R1) 157.52; More...

USD/JPY retreats ahead of 157.70 resistance and intraday bias stays neutral. On the upside, break of 157.70 will resume the whole rise from 151.86 and target 160.20 high. Nevertheless, break of 154.53 will turn bias to the downside for 151.86 support and possibly below, as the third leg of the corrective pattern from 160.20.

In the bigger picture, a medium term top should be formed at 160.20. As long as 55 W EMA (now at 147.77) holds, fall from 160.20 is seen as correcting the rise from 140.25 only. However, sustained break of 55 W EMA will argue that larger correction is possibly underway, and target 146.47 support next.

Aussie Edges Lower as Business Confidence Slips

The Australian dollar has declined by 0.28% on Tuesday. AUD/USD is trading at 0.6600 in the European session, down 0.16% on the day. On the data calendar, Australian NAB business confidence was weak and there are no economic releases out of the US.

Australian business confidence falls to six-month low

Australia’s NAB business confidence index slipped to -3 in May, down from a revised 2 in April and shy of the forecast of zero. This was the first negative reading since January and its worst performance since December 2023. The results suggest that sluggish economic conditions have continued into the second quarter.

It is difficult to see the business sector showing more optimism until the Reserve Bank of Australia delivers a rate cut, which might not happen until late in the year or early 2025. Inflation has been stubbornly high and Governor Bullock has said that if the downtrend in inflation stalls, the central bank could raise rates. This is an unlikely scenario but illustrates that the RBA remains hawkish and rate cuts are not around the corner.

Wednesday will be busy in the US, with the release of the May inflation report and the Fed rate announcement. Headline CPI is expected to remain unchanged at 3.4% y/y while Core CPI is projected to drop from 3.6% to 3.5%. . Inflation remains a headache for the Federal Reserve as bringing it down to the 2% target as proven elusive.

The Fed is virtually certain to hold the benchmark rate at 5.25% to 5.50% and the markets will be looking for clues as to future rate cuts. A quarter-point cut in September is around a 50/50 likelihood, according to the CME FedWatch.

AUD/USD Technical

- AUD/USD is putting pressure on resistance at 0.6619. Above, there is resistance at 0.6660.

- 0.6540 and 0.6499 are the next support levels

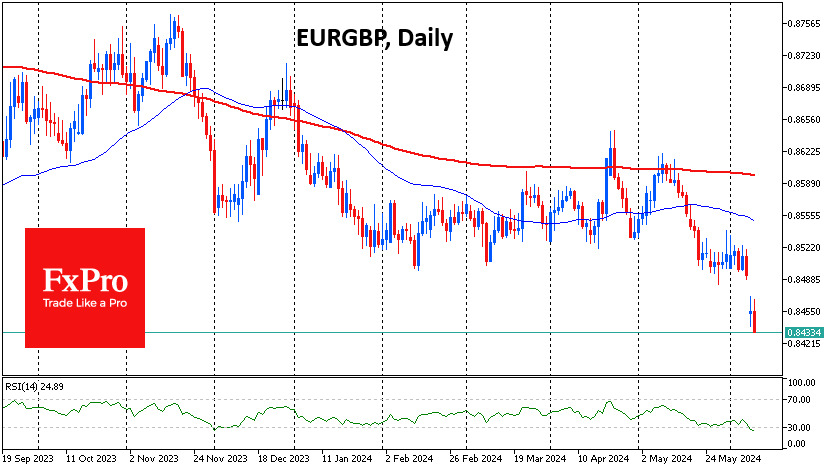

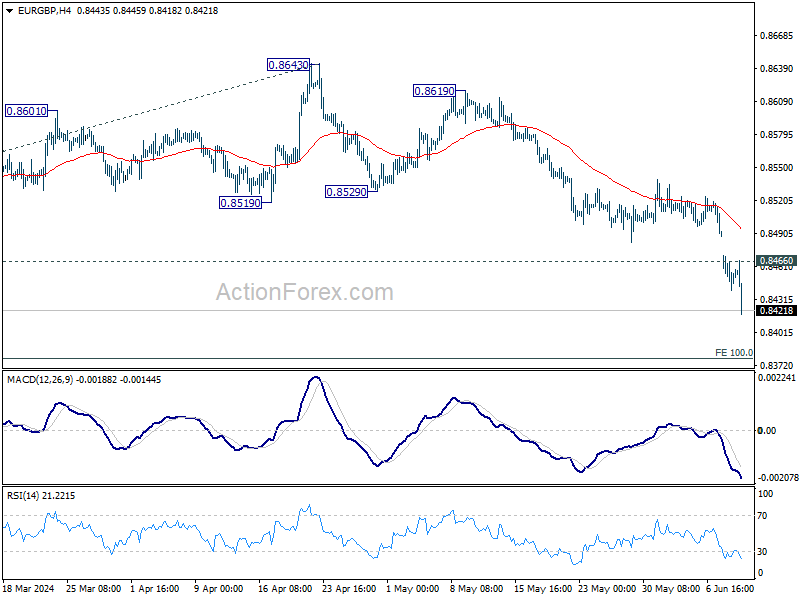

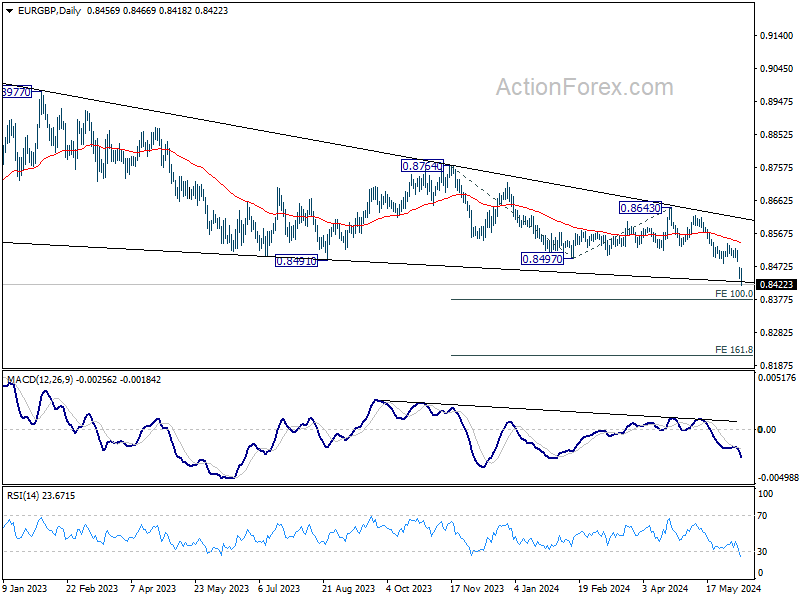

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8440; (P) 0.8456; (R1) 0.8472; More...

EUR/GBP's decline continues to as low as 0.8418 so far. Intraday bias remains on the downside for 0.8376 projection level next. On the upside, above 0.8446 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

Euro’s Brief Respite Ends, Renewed Selloff Driven by French Political Woes

Euro continues to be under significant pressure due to increasing political uncertainty in France. President Emmanuel Macron's call for a snap election has heightened fiscal consolidation risks, with Moody's describing this development as "credit negative." Investor confidence has further eroded following a poll suggesting the National Rally could significantly increase its seats in the upcoming election, though not enough to secure an absolute majority. This political instability is exerting substantial downward pressure on the Euro, which selloff resumes after brief consolidations.

In stark contrast, British Pound is emerging as the strongest currency today, despite mixed employment data. The latest figures showed an unexpected rise in the claimant count and stagnant payrolled employment growth. However, average earnings continued to grow at elevated rate. This data suggests persistent domestic inflationary pressures, contributing to Sterling's resilience.

Elsewhere in the currency markets, Australian Dollar and Canadian Dollar are among the weakest, following Euro. Meanwhile, Dollar and New Zealand Dollar are performing robustly, just behind the strengthening Sterling. Swiss Franc and Japanese Yen are experiencing less volatility, positioning them in the middle of the pack.

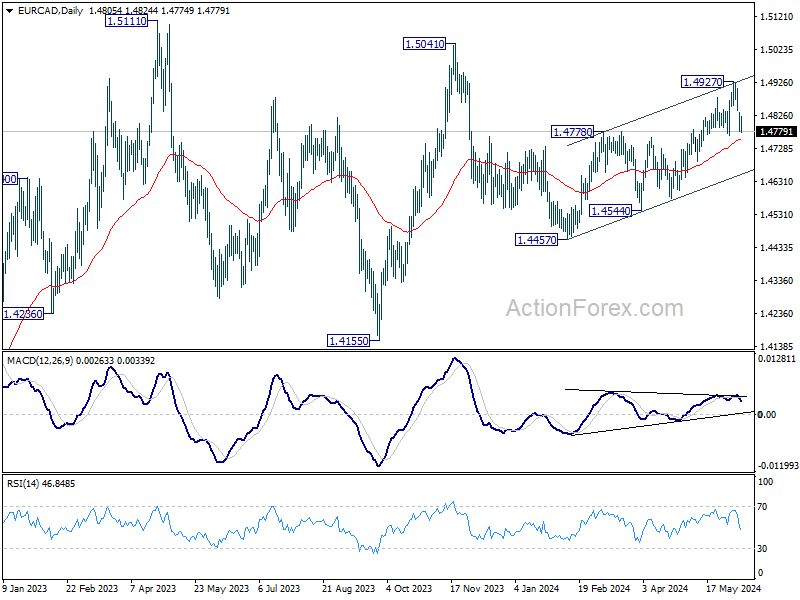

Technically, EUR/CAD is eyeing 55 D EMA (now at 1.4756) with this week's decline. Sustained break there will argue that corrective rebound from 1.4457 has completed with three waves up to 1.4927, after meeting channel resistance. Deeper fall would then be seen to channel support (now at 1.4648) first. Firm break there will argue that fall from 1.5041 is ready to resume through 1.4457 support.

In Europe, at the time of writing, FTSE is down -0.91%. DAX is down -0.76%. CAC is down -1.18%. UK 10-year yield is down -0.047 at 4.286. Germany 10-year yield is down -0.045 at 2.639. Earlier in Asia, Nikkei rose 0.25%. Hong Kong HSI fell -1.04%. China Shanghai SSE fell -0.76%. Singapore Strait Times fell -0.39%. Japan 10-year JGB yield fell -0.0228 to 1.017.

ECB's Lane: Not pre-committing to a particular rate path

In a speech today, ECB Chief Economist Philip Lane noted that the central bank's baseline projections reflect the market yield curve and anticipate "a set of rate cuts" in 2024 and 2025. He noted that with a clearly restrictive deposit facility rate of 3.75%, ECB could address potential "upside shocks to inflation" by adopting a "slower pace of rate reductions." Conversely, maintaining a policy rate of 3.75% offers "more protection against downside shocks" compared to staying at 4.0%.

Lane emphasized the high level of uncertainty and the persistent price pressures reflected in domestic inflation, services inflation, and wage growth indicators. These factors necessitate a continued restrictive monetary stance, with decisions being made on a data-dependent, meeting-by-meeting basis.

He reaffirmed ECB's commitment to ensuring that inflation returns to the 2% medium-term target "in a timely manner" and stressed that policy rates will remain "sufficiently restrictive" for as long as necessary to achieve this goal.

Lane emphasized that ECB is "not pre-committing to a particular rate path" and will continue to assess the appropriate level and duration of restriction at each meeting.

ECB's Villeroy downplays month-to-month inflation noises

ECB Governing Council member Francois Villeroy de Galhau highlighted today at a conference that month-to-month inflation data will be volatile due to base effects, particularly related to energy prices.

He cautioned that this "noise" in the data is not very meaningful, and the ECB remains "outlook driven" and will focus more closely on inflation forecasts.

Villeroy expressed confidence that, barring any external shocks, ECB will bring inflation back to its 2% target by next year, achieving this with a "soft rather than a hard landing."

He reiterated the need for a gradual approach to future rate adjustments and emphasized that ECB has "significant leeway" to cut rates before monetary policy becomes restrictive.

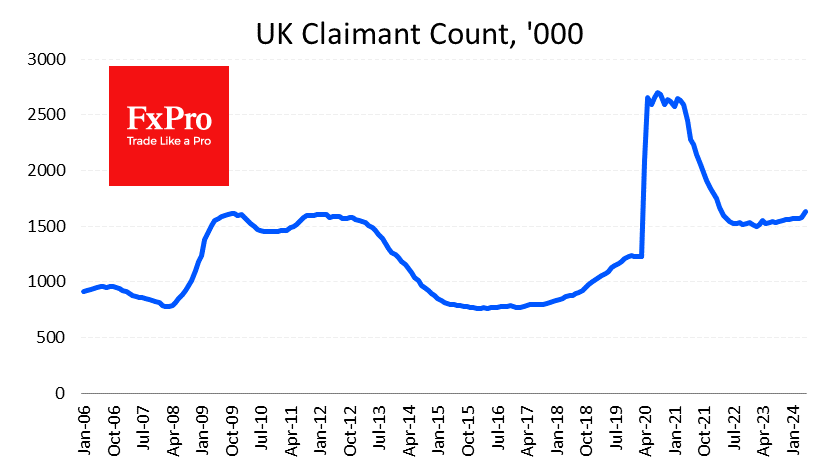

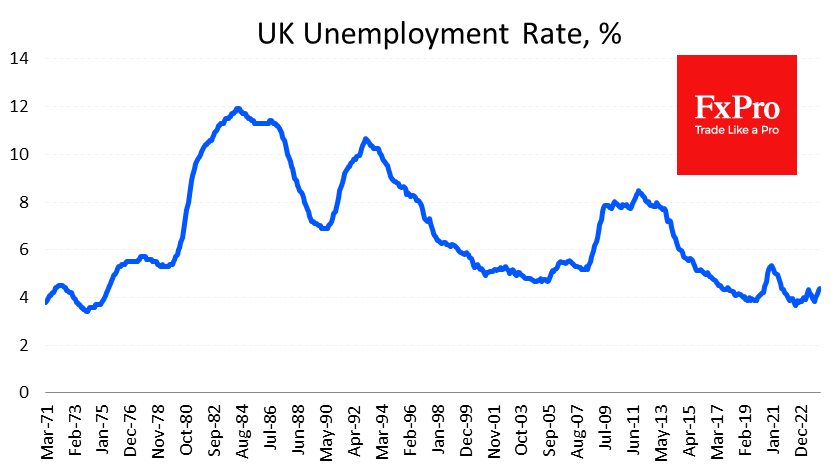

UK payrolled employment fell -3k in May, unemployment rate rises to 4.4% in Apr

UK payrolled employment fell slightly by -3k in May, following -85k monthly decline in April. Annual growth rate of payrolled employment slowed further from 0.7% yoy to 0.6% yoy. Annual growth in median pay was at 5.2% yoy, down sharply from April's 6.8% yoy. Claimant count jumped 50.4k, versus expectation of 10.2k.

In the three months to April, unemployment rate rose to 4.4%, above expectation of 4.3%. Average earnings including bonus rose 5.9% yoy, above expectation of 5.7% yoy. Average earnings excluding bonus rose 6.0% yoy, matched expectations.

Australia's NAB business confidence returns to negative, inflation pressures re-emerge

Australia's NAB Business Confidence fell from 2 to -3 in May, returning to negative territory. Business conditions also saw a slight decline, dropping from 7 to 6. Specifically, trading conditions decreased from 13 to 10, and profitability conditions fell from 6 to 3. However, employment conditions improved, rising from 2 to 5.

NAB Chief Economist Alan Oster noted pointed out that forward orders are particularly weak in retail, wholesale, and construction sectors, indicating potential challenges ahead. Despite a slowdown in activity, capacity utilization remains above average, suggesting that the "process of bringing supply and demand back into balance remains incomplete".

Inflationary pressures are re-emerging, with labor cost growth increasing to 2.3% on a quarterly basis, up from 1.5% in April. Purchase cost growth also rose to 1.9%, compared to 1.3% previously. Overall product price growth climbed to 1.1%, up from 0.8%, with retail price growth increasing to 1.6% from 1.0%, and recreation and personal services prices edging up to 1.0% from 0.9%.

Oster concluded that the data presents a "mixed" picture for RBA. There are clear signs of growth challenges, yet inflationary pressures remain a concern. "We expect the RBA to keep rates on hold for some time yet as they navigate through these contrasting risks."

EUR/GBP Mid-Day Outlook

Daily Pivots: (S1) 0.8440; (P) 0.8456; (R1) 0.8472; More...

EUR/GBP's decline continues to as low as 0.8418 so far. Intraday bias remains on the downside for 0.8376 projection level next. On the upside, above 0.8446 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y May | 1.90% | 2.10% | 2.20% | |

| 01:30 | AUD | NAB Business Confidence May | -3 | 1 | ||

| 01:30 | AUD | NAB Business Conditions May | 6 | 7 | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Apr | 4.40% | 4.30% | 4.30% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Apr | 5.90% | 5.70% | 5.70% | 5.90% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Apr | 6.00% | 6.00% | 6.00% | |

| 06:00 | GBP | Claimant Count Change May | 50.4K | 10.2K | 8.9K | 8.4K |

| 10:00 | USD | NFIB Business Optimism Index May | 90.5 | 89.8 | 89.7 | |

| 12:30 | CAD | Building Permits M/M Apr | 20.50% | 5.20% | -11.70% | -12.30% |

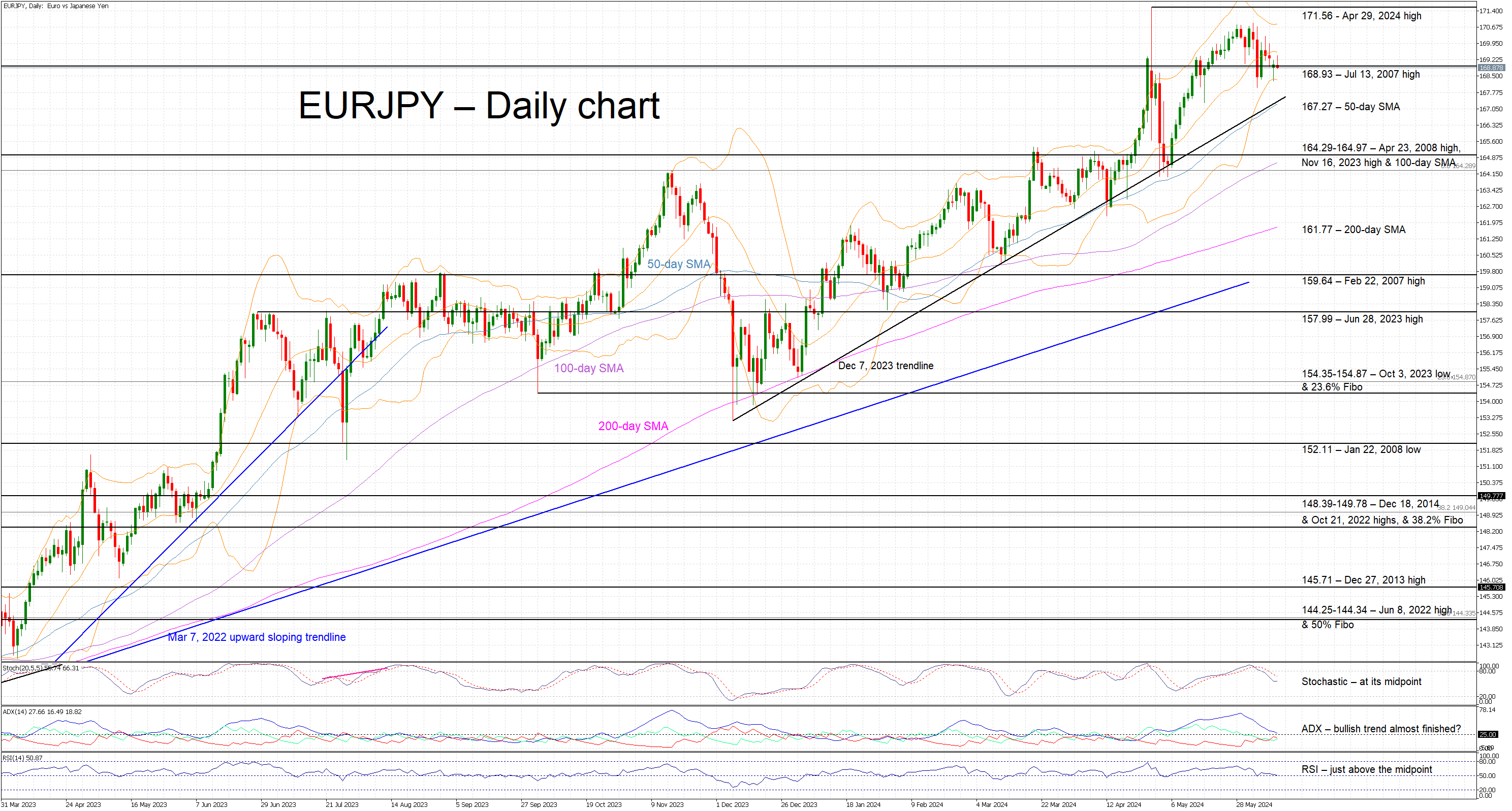

EURJPY Trades Sideways Ahead of Key Events

- EURJPY is hovering below the recent 171.56 high

- Yen failed to benefit from Monday’s euro weakness

- Momentum indicators point to weakening bullish pressure

EURJPY is trading sideways today as the yen has failed to benefit from the euro’s weakness following Sunday’s European parliamentary election results. The pair is still hovering close to its recent 171.56 high with Japanese officials probably feeling a bit more relaxed compared to the end-April market pressure.

This week’s BoJ meeting could prove critical for the short-term outlook of EURJPY as the lack of hawkish commentary on Friday could give the green light to market participants to retest the BoJ’s intervention appetite.

In the meantime, momentum indicators show diminishing bullish pressure. More specifically, the RSI is just above its midpoint and the Average Directional Movement Index (ADX) is signaling an aggressively weakening bullish trend in EURJPY. More importantly, the stochastic oscillator is tentatively hovering above its midpoint and confirming that most participants are probably waiting on the sidelines ahead of this week’s key events.

Should the bulls remain confident, they would try to push EURJPY comfortably above the July 13, 2007 high at 168.93 and gradually lay the foundations for a retest of the April 29, 2024 high at 171.56.

On the other hand, the bears are desperate to recoup part of their significant losses. They could attempt to push the EURJPY below both the 168.93 level and the 50-day simple moving average (SMA) at 167.27. If successful, they could then test their determination against the much busier 164.29-164.97 area, which is populated by the April 23, 2008 high, the November 16, 2023 high and the 100-day SMA.

To sum up, the bulls remain optimistic as the euro’s widespread underperformance has not impacted EURJPY. They are now possibly preparing for another round of bullish pressure if market events allow it.

Euro Under Pressure as Macron Calls Snap Election

The euro is down for a third straight day and has dropped 1.3% since Thursday. EUR/USD is trading at 1.0731 in the European session, down 0.32% on the day. There are no releases out of the US or the eurozone today.

It was a busy weekend in Europe, as voters went to the ballot box for European Parliament elections. The far right parties made gains, including in Germany and France. This result was not a surprise but French President Macron delivered a bombshell after the vote results when he announced a snap election which will take place on June 30th and July 7th. Macron’s job is not at stake but he is taking a massive risk as the election could boost the far right as it did in the European Parliament vote. The uncertainty in France in the next few weeks could weigh on the euro.

On Wednesday, Germany releases the final estimate for May inflation. The preliminary estimate showed CPI rising by just 0.1% m/m after a 0.5% gain in April. Yearly, the preliminary estimate rose to 2.4%, up from 2.2% in April. Germany has projected an inflation rate of 2.4% for 2024 and the ECB will be keeping a careful eye on inflation in Germany and the eurozone after cutting rates last week for the first time since it started its rate-tightening cycle in July 2022.

Also on Wednesday, the US will release the May inflation report and the Fed announces its rate decision. Headline CPI is expected to remain unchanged at 3.4% y/y, while Core CPI is projected to drop from 3.6% to 3.5%. The Fed is virtually certain to hold the benchmark rate at 5.25% to 5.50% and the markets will be looking for clues as to future rate cuts.

.

EUR/USD Technical

- EUR/USD is putting pressure on support at 1.0724. Below, there is support at 1.0647

- 1.0840 and 1.0879 are the next resistance lines

ECB’s Lane: Not pre-committing to a particular rate path

In a speech today, ECB Chief Economist Philip Lane noted that the central bank's baseline projections reflect the market yield curve and anticipate "a set of rate cuts" in 2024 and 2025. He noted that with a clearly restrictive deposit facility rate of 3.75%, ECB could address potential "upside shocks to inflation" by adopting a "slower pace of rate reductions." Conversely, maintaining a policy rate of 3.75% offers "more protection against downside shocks" compared to staying at 4.0%.

Lane emphasized the high level of uncertainty and the persistent price pressures reflected in domestic inflation, services inflation, and wage growth indicators. These factors necessitate a continued restrictive monetary stance, with decisions being made on a data-dependent, meeting-by-meeting basis.

He reaffirmed ECB's commitment to ensuring that inflation returns to the 2% medium-term target "in a timely manner" and stressed that policy rates will remain "sufficiently restrictive" for as long as necessary to achieve this goal.

Lane emphasized that ECB is "not pre-committing to a particular rate path" and will continue to assess the appropriate level and duration of restriction at each meeting.

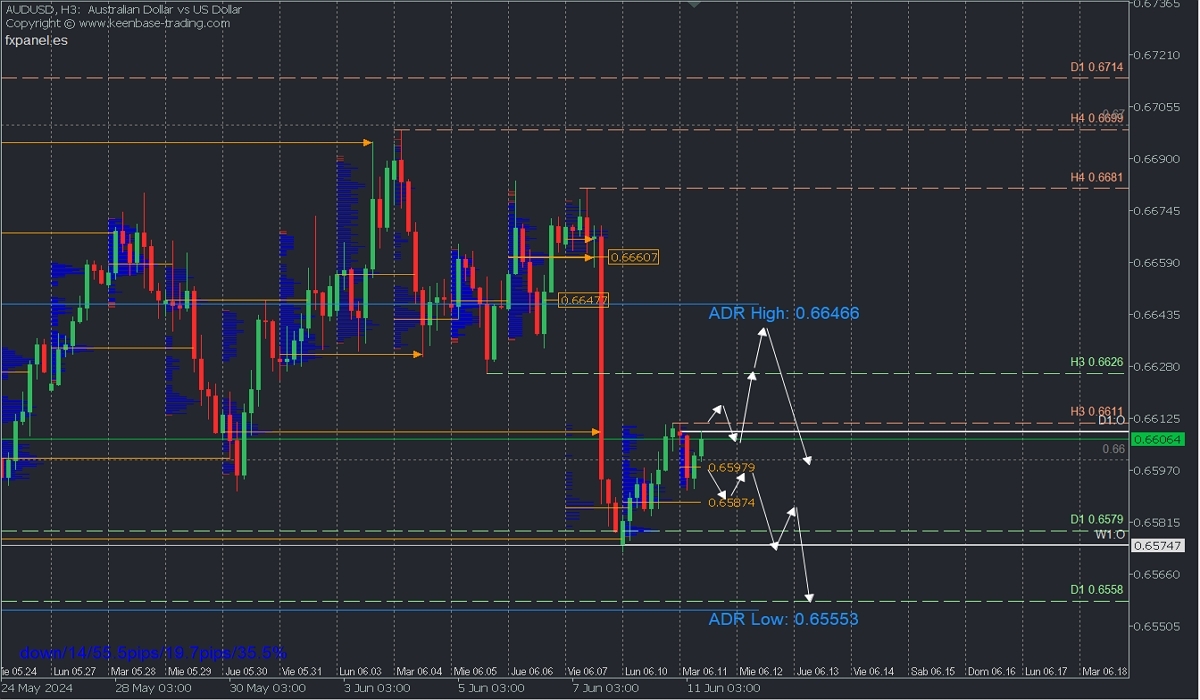

Key Factors Influencing AUDUSD: Analysis and Trading Scenarios

Bearish scenario: Sell below 0.6597 with TP1: 0.6587, TP2: 0.6579, and TP3: 0.6558, with an S.L. above 0.6611 or at least 1% of account capital.

Bullish scenario: Buy above 0.6611 with TP1: 0.6626 and TP2: 0.6646, with an S.L. below 0.6597 or at least 1% of account capital. Apply a trailing stop.

Fundamental Analysis

The fundamental analysis of the AUDUSD pair is influenced by several key factors:

- USD Strength: The US dollar has strengthened due to robust US employment data, which reduces the likelihood of interest rate cuts by the Federal Reserve this year.

- RBA Policy: The Australian dollar might find support as the Reserve Bank of Australia (RBA) plans to keep interest rates high to control inflation. The RBA is willing to increase rates if inflation does not fall within the target range of 1% to 3%.

- Fed Expectations and US Inflation Data: The market will be focused on the Fed's decision and the US inflation data to be released on Wednesday, June 11, 2024. The Fed is expected to maintain current rates to bring inflation down to its 2% target, with May's annual CPI projected to increase by 3.4% overall and 3.5% for the core CPI, excluding food and energy.

These factors create an environment where the strength of the USD and the monetary policies of both the RBA and the Fed are crucial in determining the movement of the AUDUSD pair.

Technical Analysis

Average Daily Range High (ADR High): 0.6646// Average Daily Range Low (ADR Low): 0.6555

Supply Zones (sell zones): 0.6608 / 0.6647// Demand Zones (buy zones): 0.6597 / 0.6587

After better-than-expected US employment data on Friday, the pair dropped more than 1.5%, now establishing two contiguous demand zones around 0.6587, which triggered a push towards the broken zone at 0.6608. Therefore, two potential intraday scenarios are proposed:

Bullish Extension:

This scenario will be confirmed after a decisive break above Monday's resistance at 0.6611, targeting the 0.6626 level and the extended daily bullish average range at 0.6646, filling the volume gap left by Friday's rapid decline. From there, new sell positions can be considered. This scenario will be invalidated with prices below the demand zones between 0.6597 and 0.6587.

Bearish Continuation:

If the price fails to break the 0.6611 resistance and subsequently breaks below the Asian session demand zone at 0.6597, it points to selling towards Monday's uncovered POC at 0.6587. A decisive break on a second touch indicates bear dominance, leading to a decline towards the weekly opening zone at 0.6574 and, more extended, the support at 0.6558, close to the average daily bearish range.

*Uncovered POC: POC = Point of Control: This is the level or zone where the highest volume concentration occurred. If there was a previous bearish movement from it, it is considered a sell zone forming a resistance area. Conversely, if there was a previous bullish impulse, it is considered a buy zone, usually located at lows, thus forming support zones.

Alarming UK Labour Market Data

Unexpected weakness in the UK labour market could signal an important turnaround in the economy and raise the urgency of monetary easing. The short-term impact on the Pound has been relatively limited, but the currency market has now adopted a wait-and-see approach ahead of Wednesday’s US news.

This morning’s batch of data from the UK saw a 50.4K jump in Claimant Count in May after 8.4K a month earlier. This is the biggest monthly increase since the first COVID lockdowns, and before that, the last time there was such a jump was in the depths of the 2009 recession. A frightening acceleration of the upward trend in the indicator has been seen since March last year.

In a separate indicator, the Unemployment Rate for the February-April period climbed to 4.4%. This is still low by historical standards, but it is a three-year high and 0.6 percentage points above the one we saw in January last year. More actual Claimant claims are points to accelerate the unemployment growth.

Wage growth remained at an impressive 5.9% y/y, including bonuses (above the expected 5.7%). However, this is the typical acceleration in wages that we see in the early stages of mass layoffs when the lowest-paid employees are given the chop.

A fresh labour market report has every chance of shifting the Bank of England’s focus from fighting inflation to supporting the economy. This is even more so because, at this stage, reducing the tightness of monetary policy will only be necessary. If this process is delayed, the situation could easily lead to a repeat of the abnormal stimulus we saw in 2008/09 or 2020/21.

Reacting to the news, the GBP initially lost 0.15% against the USD and EUR but soon recovered almost completely. GBPUSD is dominated by a wait-and-see mood as all attention and volatility are deferred to inflation figures and monetary policy assessments from the FOMC on Wednesday. EURGBP remains under pressure due to the uncertainty surrounding the unexpected French elections and the disappointing (market-side) results of the European Parliament elections.

UK labour market data is already digging a hole for the Pound, and it remains a matter of days before it could fall into it.