Sample Category Title

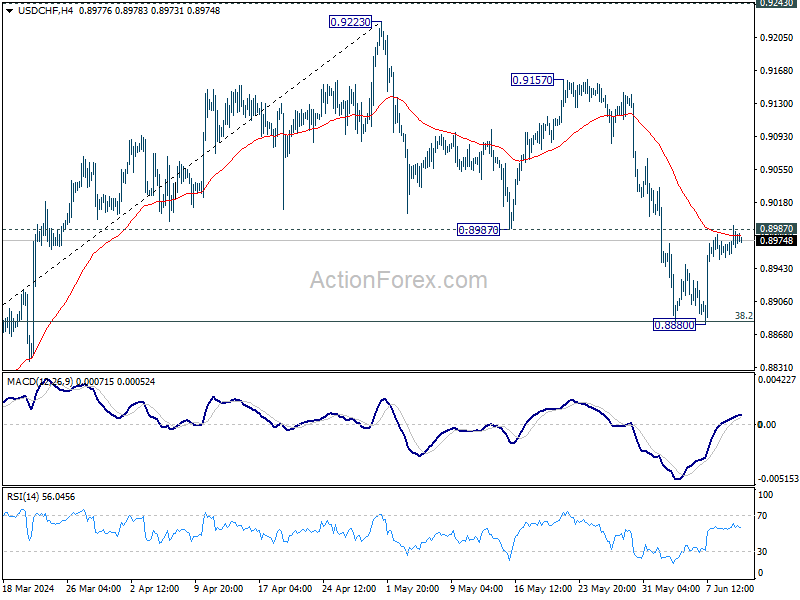

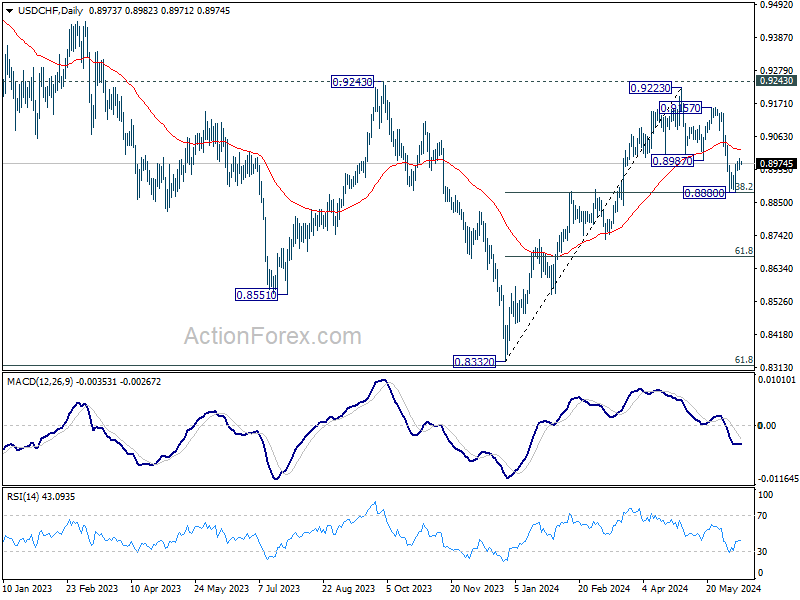

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8955; (P) 0.8974; (R1) 0.8996; More….

USD/CHF failed to break through 0.8987 support turned resistance decisively despite breaching it. Intraday bias stays neutral first. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone. Nevertheless, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Risk-On Sentiment Holds; Key US Inflation and Fed Announcements Loom

The forex markets are predominantly range-bound today as traders eagerly anticipate two pivotal events: US Consumer Price Index release and Federal Reserve's economic projections. These announcements have the potential to trigger significant market volatility, given their implications for future monetary policy. While Euro struggles amid ongoing political turmoil in France, other major currencies remain steady in anticipation of today's developments.

Currently, risk sentiment in the markets remains strong, evidenced by NASDAQ and S&P 500 reaching new record highs overnight. However, there is a palpable sense of caution as traders consider the possibility that a hawkish stance from Fed could maintain higher interest rates for an extended period, potentially dampening the current optimism.

As of now, New Zealand Dollar leads as the strongest currency of the week, followed by Australian Dollar and British Pound. Euro remains the weakest due to political instability in France and broader concerns within the EU. Japanese Yen and Swiss Franc are also underperforming, indicating a prevailing risk-on mood among investors. Dollar and Canadian Dollar are in a neutral position as the market awaits further cues.

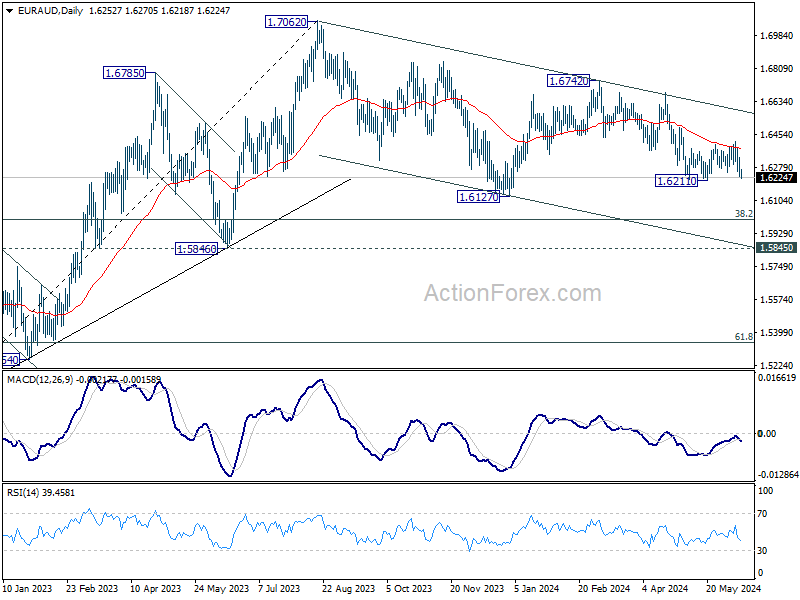

Technically, EUR/AUD is worth a note today as it's falling back towards 1.6211 support. Decisive break there would confirm resumption of the decline from 1.6742, which is seen as the third leg of the corrective pattern from 1.7062. In this case, deeper fall should then be seen to 1.6127 support and below. The downward movement could be catalyzed by escalating risk-on sentiment in the markets or worsening political conditions in the European Union.

In Asia, at the time of writing, Nikkei is down -0.57%. Hong Kong HSI is down -1.27%. China Shanghai SSE is up 0.15%. Singapore Strait Times is up 0.11%. Japan 10-year JGB yield is down -0.0292 at 0.987. Overnight, DOW fell -0.31%. S&P 500 rose 0.27%. NASDAQ rose 0.88%. 10-year yield fell -0.065 to 4.404.

US CPI and Fed awaited, NASDAQ surges to new record

Global financial markets are on high alert today as they await two critical announcements from the US, including the release of May's CPI and FOMC rate decision accompanied by new economic projections. These events are expected to play a crucial role in shaping market sentiment and monetary policy outlooks.

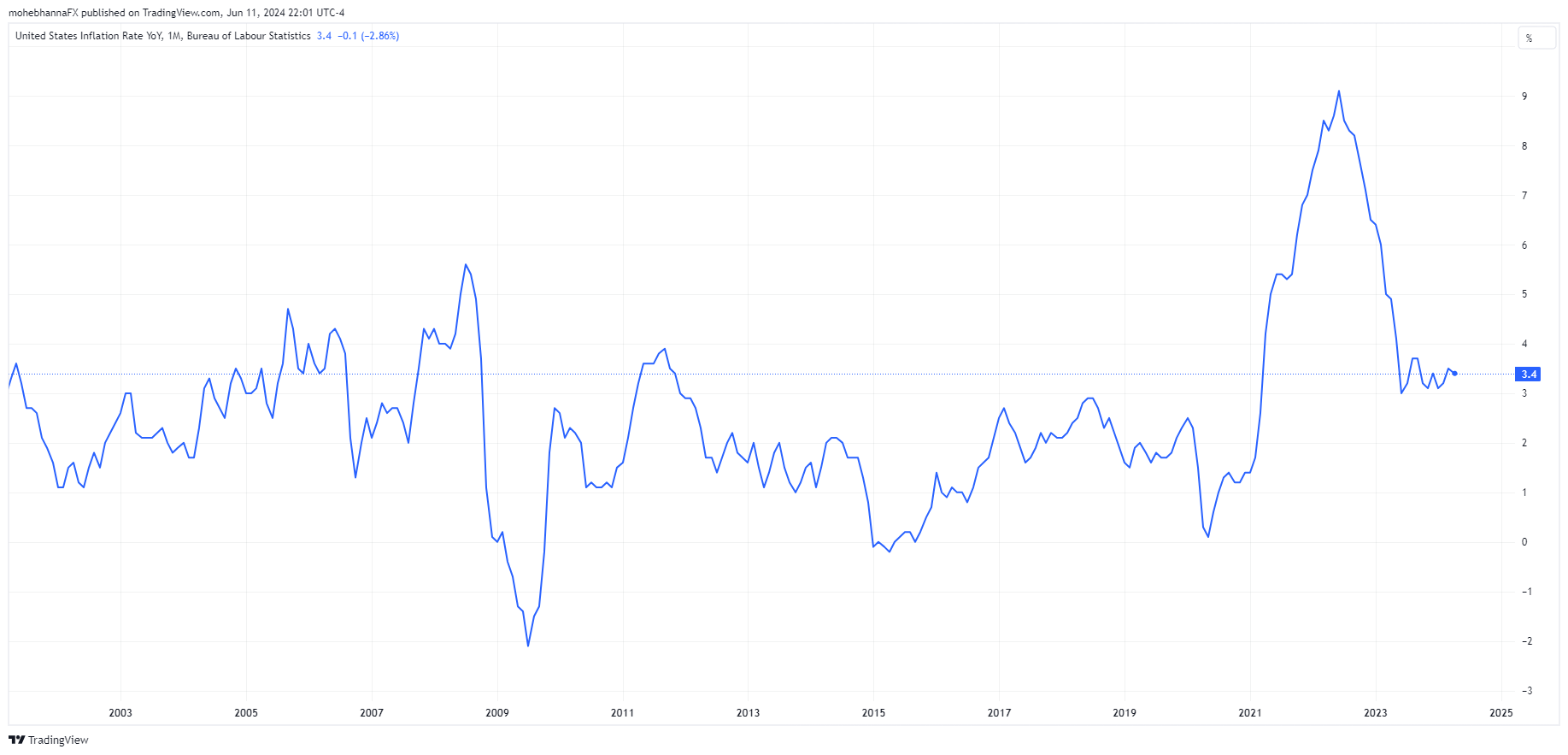

Analysts expect headline CPI to remain steady at 3.4% yoy, while core CPI, which strips out volatile food and energy prices, is anticipated to dip further from 3.6% yoy to 3.5% yoy. On a month-over-month basis, headline CPI is projected to rise by 0.2% mom, and core CPI by 0.3% mom.

Regarding Fed's upcoming decision, the consensus is that interest rates will be held steady at 5.25-5.50%. However, the focus will be on the updated dot plot, which reflects the rate expectations of Fed policymakers. Key questions include how many policymakers now foresee fewer than two rate cuts this year and whether any still see the need for further hikes.

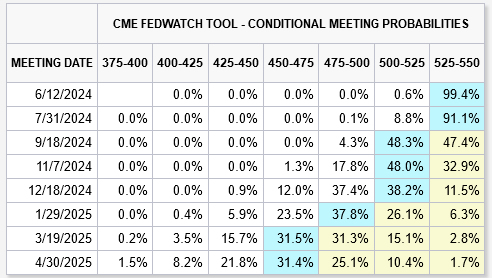

Current market sentiment suggests that Fed might only cut rates once this year, with an 88.5% probability of a cut by December. The chances of a rate cut in September stand at 52.6%, while the likelihood of a cut in November is slightly higher at 67.1%. These expectations will be closely scrutinized against the backdrop of today's announcements.

Ahead of theses key events, NASDAQ is looking unstoppable as it surged to fresch all-time highs. S&P 500 also closed at record but its gain was dwarfed by the tech index, while DOW lagged further behind with a loss.

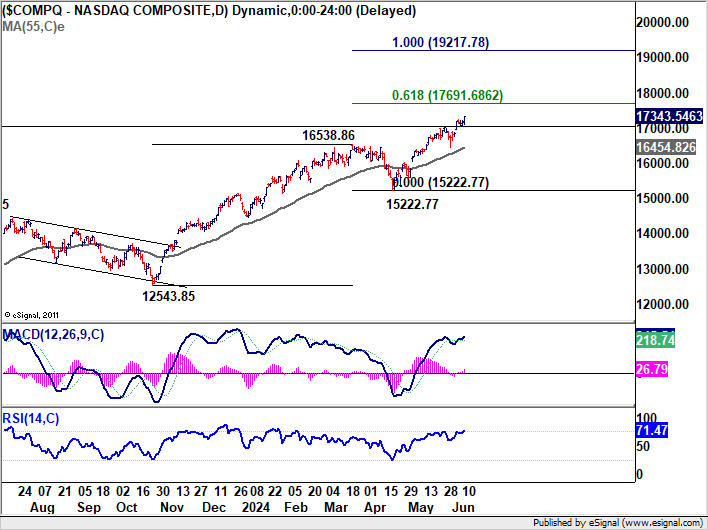

Technically, further rise is expected in NASDAQ as long as 17343.54 support holds. Next target is 61.8% projection of 12543.85 to 16538.86 from 1522.77 at 17691.68. Firm break there could prompt upside acceleration to 100% projection at 19217.78. On the downside, break of 17343.54 will bring consolidations first before staging another rally.

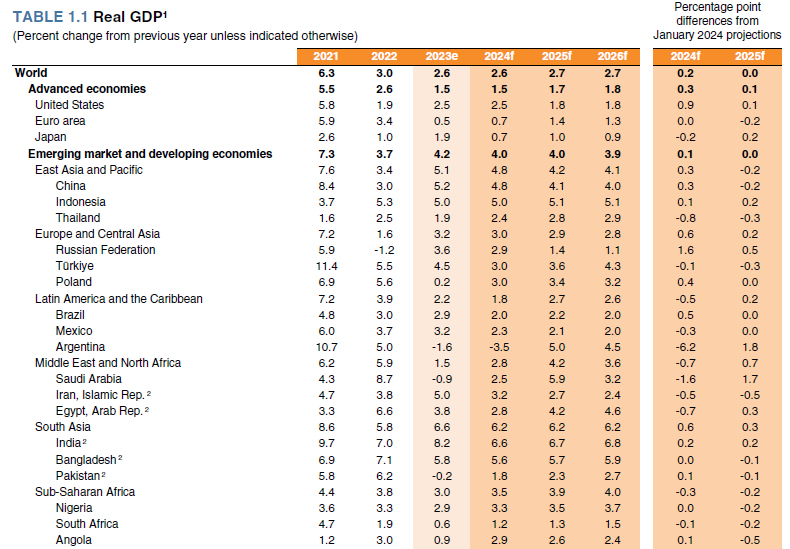

World Bank raises 2024 global growth forecast but warns of persistent slowdown

In the Global Economic Prospects, the World Bank raised its global growth forecast for 2024 by 0.2% to 2.6%, which matches the pace of 2023. Growth is expected to rise slightly to 2.7% in both 2025 and 2026, but still well below the pre-pandemic average of 3.1%.

"In a sense, we see the runway for a soft landing," said World Bank Deputy Chief Economist Ayhan Kose. "That's the good news. What is not good news is that we may be stuck in the slow lane."

The report includes an alternative scenario where persistent inflation in advanced economies keeps interest rates about 40 basis points higher than the baseline forecast, potentially cutting 2025 global growth to 2.4%.

For the US, the World Bank now predicts 2.5% growth in 2024, consistent with the 2023 rate and up from January's forecast of 1.6%. Growth is expected to slow to 1.8% in both 2025 and 2026.

In the Eurozone, growth is projected to accelerate to 0.7% in 2024, unchanged from previous forecasts, and then increase to 1.4% in 2025 before slightly dipping to 1.3% in 2026.

Japan's growth forecast for 2024 has been revised down to 0.7% from 0.9%, due to weak consumption and slowing exports, though growth is expected to improve to 1.0% in 2025 and 0.9% in 2026.

China's growth forecast for 2024 has been upgraded to 4.8% from 4.5%, driven by increased exports. However, growth is expected to decline to 4.1% in 2025 and 4.0% in 2026, due to weak investment, low consumer confidence, and a struggling property sector.

Japan's CGPI rises to 2.4% yoy, highest in nine months

Japan's corporate goods price index accelerated from 1.1% yoy to 2.4% yoy in May, surpassing expectations of 2.0% yoy increase. This marks the fastest annual rise in nine months. The Yen-based import goods price index also rose 6.9% yoy , up from a 6.6% yoy gain in April, indicating that the Yen's depreciation is driving up the cost of raw material imports.

In a related development, a draft government policy blueprint released today emphasizes Japan's commitment to using "all policy tools" to sustain wage hikes. These wage increases are deemed crucial for ending deflation and achieving consistent economic growth above 1%, despite the country's rapidly shrinking population.

China's CPI stagnates in May, PPI remains in negative territory

China's CPI rose 0.3% yoy in May, unchanged from the previous month's reading and falling short of the expected 0.4% yoy increase. Food prices declined by -2.0% yoy, while non-food prices saw a modest increase of 0.8% yoy. Prices of consumer goods remained flat, and service prices rose by 0.8% yoy .

On a monthly basis, CPI edged down by -0.1% mom, missing the expectation of no change. Food prices were stable, but non-food prices fell by -0.2% mom, consumer goods prices decreased by -0.1% mom, and service prices also fell by 0.1% mom.

PPI dropped by -1.4% yoy, an improvement from the previous month's -2.5% yoy decline and better than the expected -1.8% yoy fall. Despite this improvement, PPI has been negative for the 20th consecutive month, indicating ongoing deflationary pressures in the industrial sector.

Looking ahead

UK GDP is the main focus in European session. Later in the day, all eyes are on US CPI, FOMC rate decision and new economic projections.

USD/CHF Daily Outlook

Daily Pivots: (S1) 0.8955; (P) 0.8974; (R1) 0.8996; More….

USD/CHF failed to break through 0.8987 support turned resistance decisively despite breaching it. Intraday bias stays neutral first. On the upside, firm break of 0.8987 support turned resistance will argue that correction from 0.9223 has completed, after drawing support from 0.8883 fibonacci level. Intraday bias will be back on the upside for 0.9157/9223 resistance zone. Nevertheless, sustained break of 0.8883 fibonacci level will carry larger bearish implications and bring deeper decline.

In the bigger picture, price actions from 0.8332 medium term bottom are tentatively seen as developing into a corrective pattern to the down trend from 1.0146 (2022 high). Rejection by 0.9243 resistance, followed by sustained break of 38.2% retracement of 0.8332 to 0.9223 at 0.8883 will strengthen this case, and maintain medium term bearishness. However, decisive break of 0.9243 will argue that the trend has already reversed and turn medium term outlook bullish for 1.0146.

Economic Indicators Update

| GMT | Ccy | Events | Actual | Forecast | Previous | Revised |

|---|---|---|---|---|---|---|

| 23:50 | JPY | Money Supply M2+CD Y/Y May | 1.90% | 2.10% | 2.20% | |

| 01:30 | AUD | NAB Business Confidence May | -3 | 1 | ||

| 01:30 | AUD | NAB Business Conditions May | 6 | 7 | ||

| 06:00 | GBP | ILO Unemployment Rate (3M) Apr | 4.40% | 4.30% | 4.30% | |

| 06:00 | GBP | Average Earnings Including Bonus 3M/Y Apr | 5.90% | 5.70% | 5.70% | 5.90% |

| 06:00 | GBP | Average Earnings Excluding Bonus 3M/Y Apr | 6.00% | 6.00% | 6.00% | |

| 06:00 | GBP | Claimant Count Change May | 50.4K | 10.2K | 8.9K | 8.4K |

| 10:00 | USD | NFIB Business Optimism Index May | 90.5 | 89.8 | 89.7 | |

| 12:30 | CAD | Building Permits M/M Apr | 20.50% | 5.20% | -11.70% | -12.30% |

US CPI and FOMC Rate Decision – EUR/USD and USD/JPY Technical Analysis

This week, financial markets are focused on the FOMC interest rate decision, as well as key economic indicators such as CPI and PPI. The Fed’s decision comes on the heels of rate cuts by the ECB and BOC, with expectations of a hold on rates in June. Investors are also looking for signals from the Bank of Japan amidst the Yen’s historic lows. In this context, we analyze market expectations and recent price actions, particularly focusing on EUR/USD and USD/JPY, which has shown resilience with a decade-long uptrend.

FOMC Meeting and Key Economic Indicators: Awaiting the Fed’s Decision

This week, the financial world is waiting with anticipation for the FOMC interest rate decision, statement, press conference, and the dot plot. This follows rate cuts by both the European Central Bank (ECB) and the Bank of Canada (BOC), each by 25 basis points, in response to declining inflation.

In the US, inflation has significantly decreased from its 2022 peak. However, recent CPI and PCE readings indicate persistent inflation in sectors like housing and services. Fed Chair Jerome Powell has emphasized that any future rate cuts hinge on sustained disinflation. Other Fed officials echo these concerns.

Bloomberg analyst surveys, media polls, and CME Group data suggest the Fed will maintain the current 525-550 interest rate in June. Traders now anticipate only two rate cuts in 2024, starting in September, a shift influenced by robust job numbers. Market participants are also keen to see updates in this quarter’s dot plot, particularly regarding the projected rate cuts for 2024.

The upcoming Consumer Price Index (CPI) report, expected to be released on the same day as the FOMC meeting, is also in the spotlight. Forecasts suggest CPI Y/Y will remain at 3.4%, with Core CPI Y/Y also holding steady at 3.6%. CPI M/M is projected to dip to 0.1% from 0.3%, likely due to falling oil prices. The services sector, a recent concern, has shown signs of stabilization within Core CPI. Additionally, a noted increase in medical services costs has brought prices back to their averages.The timing of the CPI report’s release during the FOMC meeting adds another layer of intrigue, as traders and the Fed navigate this uncommon scenario.

The PPI report is due this week, with expectations of a decline in both PPI M/M and Core PPI M/M. Similar to CPI, the services component of PPI has risen since January 2024, returning to pre-COVID levels.

Bank of Japan Expected to Hold Rates Amidst Yen’s Weakness

Meanwhile, later in the week, the Bank of Japan (BOJ) is expected to maintain its current interest rate of 0.10%. However, traders will be watching for any signs of quantitative tightening (QT), which could impact the market. The Japanese Yen, currently trading near a 34-year low, adds another element of uncertainty. Despite the interest rate differential between the US and Japan, carry trades on USDJPY remain attractive to some investors, albeit with inherent risks.

EUR/USD Technical Analysis – Daily Chart

- Price action broke out and closed above the upper border of the narrowing formation identified on the above chart, two throwbacks took place as well as a shortfall as the price found support above a confluence of support, represented by monthly PP and Weekly support S1 near 1.0797.

- However, last week Non-Farm Payroll surprised the markets with higher-than-expected numbers, this caused price action to complete a third throwback which took price action back to the same border discussed on the above point.

- Price action broke and closed below three moving averages: EMA9, MA9, and MA21.

- Non-smoothed RSI7 aligns with price action and is currently at oversold territory.

- The potential double bottom formation (or triple bottom) discussed last time has materialized and still has potential as price found support above the resistance line connecting the three bottoms, if price action fails above this line and trades within the narrowing formation, the pattern may be invalidated.

- Weekly Chart update: Price action remains below the lower border of the previously discussed ascending channel; multiple pullback attempts have failed so far, and price continues to trade below the pattern.

- Monthly Chart update: Last month candle was a bullish engulfing candle after price rallied where it was met by resistance at its annual pivot point of 1.0920, taking price action down to 1.0760 where it found support above its intermediate MA21.

USD/JPY Technical Analysis – Daily Chart

- The USD/JPY price has demonstrated remarkable resilience, maintaining an extended uptrend for over ten years. The latter part of the uptrend, influenced by the fundamental economies of the USA and Japan, is marked by the blue lines on the chart. Price action was trading within an ascending channel; it broke below the channel’s lower border during late 2023. However, it has been attempting to re-enter the channel since the breakout. (Unchanged from last week)

- Following the latest 2024 Bank of Japan meeting, price action was able to break above the channel’s lower border and reenter. However, the break was met by fierce resistance represented by a strong bearish engulfing candle, which closed below the lower border by the end of the trading day.

- Following the failed breakout, Price action has attempted three pullbacks, and was met by resistance for every attempt so far as indicated on the chart, on all occasions, price action has failed to enter the channel again, formed bearish engulfing candles and shortfalls as price action was met by resistance at its last week PP of 157.12.

- Price broke below a confluence of moving averages; however, it didn’t last long as price reversed back up and closed above the three averages as well as this week’s pivot point of 156.26, a break and a close below this level may invalidate the recent upside price move.

- Negative Divergence between the latest upside move and tick volume as price rose on a declining volume.

- Fast RSI7 still aligns with price action and has reversed from overbought territory.

Conclusion

In conclusion, market participants are keenly awaiting the FOMC’s interest rate decision and the release of key economic indicators, particularly CPI. The Fed’s decision, alongside potential policy shifts from the Bank of Japan, will significantly influence currency markets. Technical analysis of EUR/USD and USD/JPY suggests potential volatility and highlights key levels to watch. Traders should closely monitor these events and indicators for potential trading opportunities, while also considering the broader economic context and geopolitical risks.

Elliott Wave Intraday Analysis: S&P 500 (SPX) Sequence Remains Bullish

Short Term Elliott Wave in S&P 500 (SPX) suggests the rally from 4.20.2024 low is in progress as an impulse. Up from 4.20.2024 low, wave 1 ended at 5341.88 and pullback in wave 2 ended at 5191.68. Internal subdivision of wave 2 unfolded as a double three Elliott Wave structure. Down from wave 1, wave ((w)) ended at 5256.93 and wave ((x)) ended at 5311.65. The Index then extended lower in wave ((y)) as a zigzag structure. Wave (a) ended at 5269.67, wave (b) ended at 5282.06 and wave (c) ended at 5191.74. This completed wave ((y)) of 2 in higher degree.

The Index has turned higher in wave 3. Up from wave 2, wave (i) ended at 5292.25 and dips in wave (ii) ended at 5234.32. The Index resumed higher in wave (iii) towards 5370.3 and pullback in wave (iv) ended at 5347.09. Wave (v) higher ended at 5375.08 which completed wave ((i)). Pullback in wave ((ii)) is proposed complete as a shallow zigzag Elliott Wave structure. Down from wave ((i)), wave (a) ended at 5341.88 and wave (b) ended at 5360.79. Wave (c) lower ended at 5340.51 which completed wave ((ii)). The Index has turned higher in wave ((iii)). Near term, as far as pivot at 5191.74 low stays intact, expect dips to find support in 3, 7, or 11 swing for further upside.

S&P 500 (SPX) 30 Minutes Elliott Wave Chart

SPX Elliott Wave Video

https://www.youtube.com/watch?v=4bZ22Mz2Loo

US CPI and Fed awaited, NASDAQ surges to new record

Global financial markets are on high alert today as they await two critical announcements from the US, including the release of May's CPI and FOMC rate decision accompanied by new economic projections. These events are expected to play a crucial role in shaping market sentiment and monetary policy outlooks.

Analysts expect headline CPI to remain steady at 3.4% yoy, while core CPI, which strips out volatile food and energy prices, is anticipated to dip further from 3.6% yoy to 3.5% yoy. On a month-over-month basis, headline CPI is projected to rise by 0.2% mom, and core CPI by 0.3% mom.

Regarding Fed's upcoming decision, the consensus is that interest rates will be held steady at 5.25-5.50%. However, the focus will be on the updated dot plot, which reflects the rate expectations of Fed policymakers. Key questions include how many policymakers now foresee fewer than two rate cuts this year and whether any still see the need for further hikes.

Current market sentiment suggests that Fed might only cut rates once this year, with an 88.5% probability of a cut by December. The chances of a rate cut in September stand at 52.6%, while the likelihood of a cut in November is slightly higher at 67.1%. These expectations will be closely scrutinized against the backdrop of today's announcements.

Ahead of theses key events, NASDAQ is looking unstoppable as it surged to fresch all-time highs. S&P 500 also closed at record but its gain was dwarfed by the tech index, while DOW lagged further behind with a loss.

Technically, further rise is expected in NASDAQ as long as 17343.54 support holds. Next target is 61.8% projection of 12543.85 to 16538.86 from 1522.77 at 17691.68. Firm break there could prompt upside acceleration to 100% projection at 19217.78. On the downside, break of 17343.54 will bring consolidations first before staging another rally.

Bitcoin Under Pressure: Dips Ahead of Crucial Fed Meeting

Key Highlights

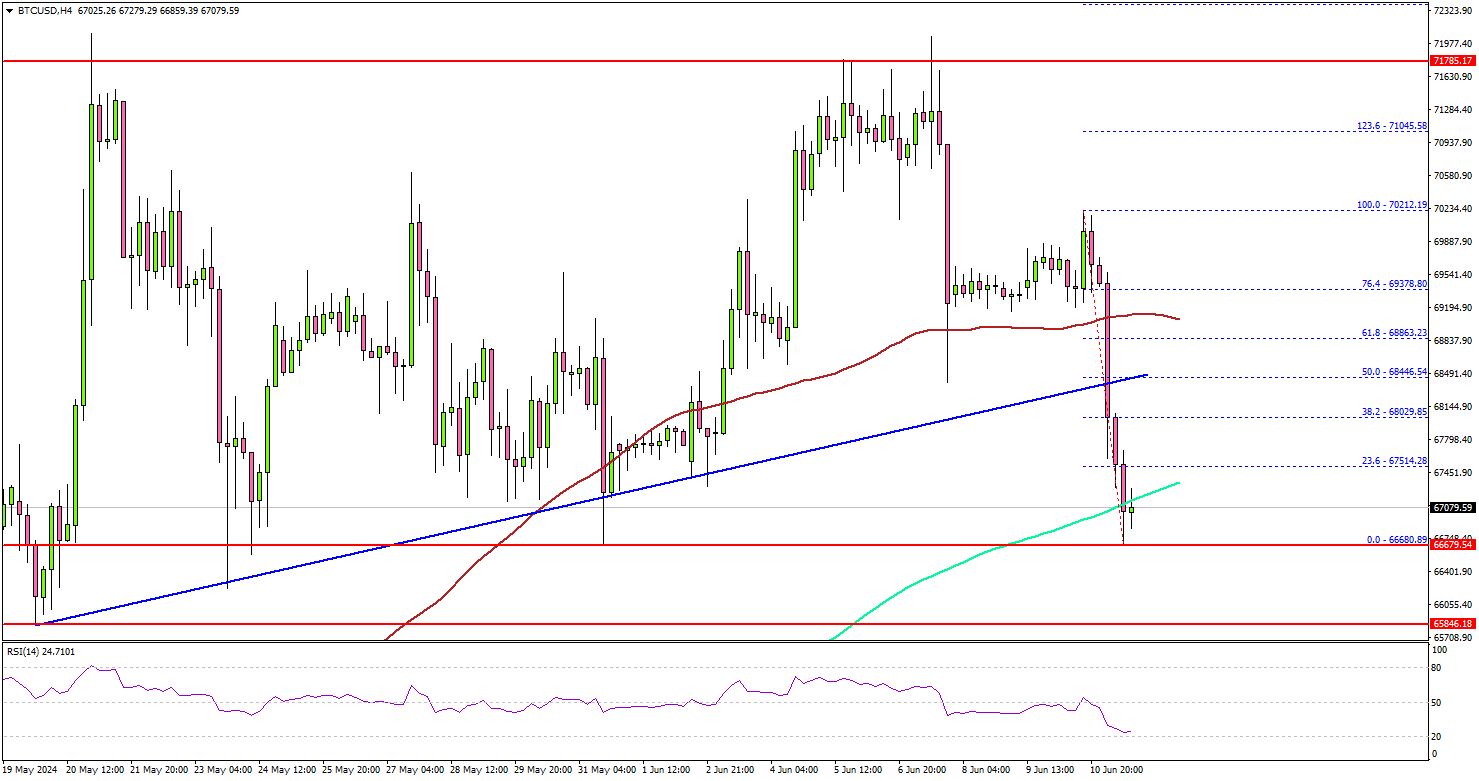

- Bitcoin price started another decline from the $72,000 resistance zone.

- BTC traded below a key bullish trend line with support near $68,250 on the 4-hour chart.

- Gold prices consolidate near the $2,320 resistance zone.

- The Fed is likely to keep interest rates at 5.5%.

Bitcoin Price Technical Analysis

Bitcoin price failed to clear the $72,000 resistance zone and started a fresh decline. BTC/USD traded below many supports such as $70,000 and $69,200.

Looking at the 4-hour chart, the price traded below a key bullish trend line with support near $68,250. The price settled well below the 100 simple moving average (red, 4 hours) and tested the 200 simple moving average (green, 4 hours).

However, the bulls are now active near the $66,500 support zone. If there is another increase, the price could face resistance near the $67,800 level.

The first key resistance is near the $68,400 zone. The next resistance is near $69,200 and the 100 simple moving average (red, 4 hours). A successful close above $69,200 might start another steady increase. In the stated case, the price may perhaps rise toward the $70,000 level.

Conversely, Bitcoin might extend losses. Immediate support is near the $66,500 level. The main support sits at $66,000. Any more losses might send the price toward the $62,500 support zone.

Immediate resistance is near the $72,000 level.

Today’s Economic Releases

- US Consumer Price Index for May 2024 (MoM) – Forecast +0.1%, versus +0.3% previous.

- US Consumer Price Index for May 2024 (YoY) – Forecast +3.4%, versus +3.4% previous.

- Fed Interest Rate Decision - Forecast 5.5%, versus 5.5% previous.

China’s CPI stagnates in May, PPI remains in negative territory

China's CPI rose 0.3% yoy in May, unchanged from the previous month's reading and falling short of the expected 0.4% yoy increase. Food prices declined by -2.0% yoy, while non-food prices saw a modest increase of 0.8% yoy. Prices of consumer goods remained flat, and service prices rose by 0.8% yoy .

On a monthly basis, CPI edged down by -0.1% mom, missing the expectation of no change. Food prices were stable, but non-food prices fell by -0.2% mom, consumer goods prices decreased by -0.1% mom, and service prices also fell by 0.1% mom.

PPI dropped by -1.4% yoy, an improvement from the previous month's -2.5% yoy decline and better than the expected -1.8% yoy fall. Despite this improvement, PPI has been negative for the 20th consecutive month, indicating ongoing deflationary pressures in the industrial sector.

Japan’s CGPI rises to 2.4% yoy, highest in nine months

Japan's corporate goods price index accelerated from 1.1% yoy to 2.4% yoy in May, surpassing expectations of 2.0% yoy increase. This marks the fastest annual rise in nine months. The Yen-based import goods price index also rose 6.9% yoy , up from a 6.6% yoy gain in April, indicating that the Yen's depreciation is driving up the cost of raw material imports.

In a related development, a draft government policy blueprint released today emphasizes Japan's commitment to using "all policy tools" to sustain wage hikes. These wage increases are deemed crucial for ending deflation and achieving consistent economic growth above 1%, despite the country's rapidly shrinking population.

World Bank raises 2024 global growth forecast but warns of persistent slowdown

In the Global Economic Prospects, the World Bank raised its global growth forecast for 2024 by 0.2% to 2.6%, which matches the pace of 2023. Growth is expected to rise slightly to 2.7% in both 2025 and 2026, but still well below the pre-pandemic average of 3.1%.

"In a sense, we see the runway for a soft landing," said World Bank Deputy Chief Economist Ayhan Kose. "That's the good news. What is not good news is that we may be stuck in the slow lane."

The report includes an alternative scenario where persistent inflation in advanced economies keeps interest rates about 40 basis points higher than the baseline forecast, potentially cutting 2025 global growth to 2.4%.

For the US, the World Bank now predicts 2.5% growth in 2024, consistent with the 2023 rate and up from January's forecast of 1.6%. Growth is expected to slow to 1.8% in both 2025 and 2026.

In the Eurozone, growth is projected to accelerate to 0.7% in 2024, unchanged from previous forecasts, and then increase to 1.4% in 2025 before slightly dipping to 1.3% in 2026.

Japan's growth forecast for 2024 has been revised down to 0.7% from 0.9%, due to weak consumption and slowing exports, though growth is expected to improve to 1.0% in 2025 and 0.9% in 2026.

China's growth forecast for 2024 has been upgraded to 4.8% from 4.5%, driven by increased exports. However, growth is expected to decline to 4.1% in 2025 and 4.0% in 2026, due to weak investment, low consumer confidence, and a struggling property sector.

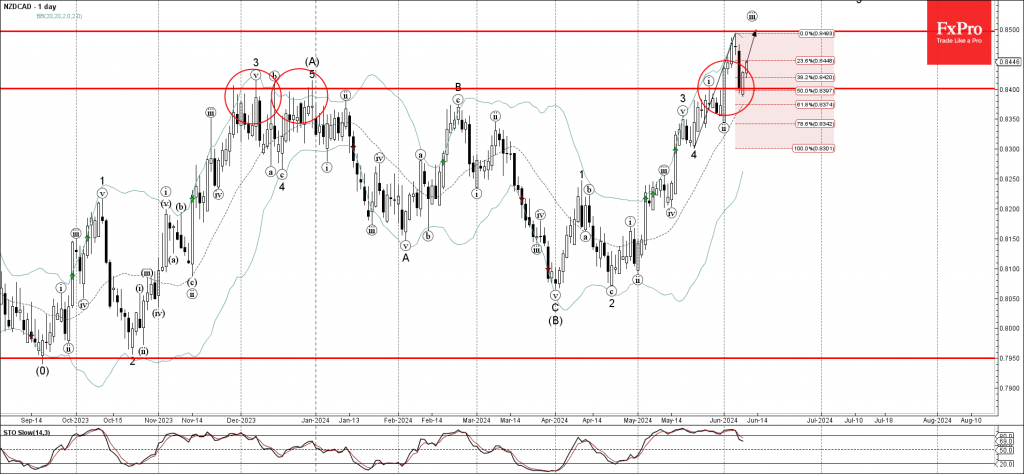

NZDCAD Wave Analysis

- NZDCAD reversed from support level 0.8400

- Likely to rise to resistance 0.8500

NZDCAD currency pair recently reversed up with the daily Piercing Line from the support level 0.8400 (former strong resistance from November, December and May).

The support level 0.8400 was strengthened by the nearby 20-day moving average and by the 50% Fibonacci correction of the previous upward impulse from May.

Given the clear daily uptrend, NZDCAD be expected to rise further to the next resistance 0.8500, top of the Evening Star from the start of this month.