Sample Category Title

Fed Can End US Indices’ Divergence

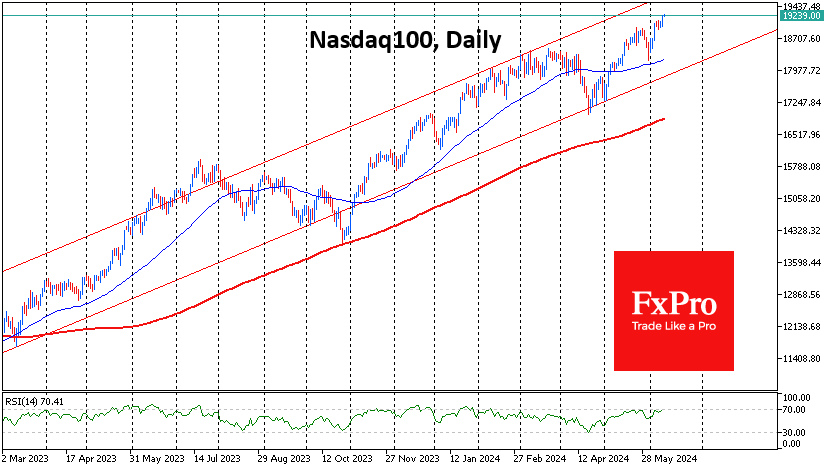

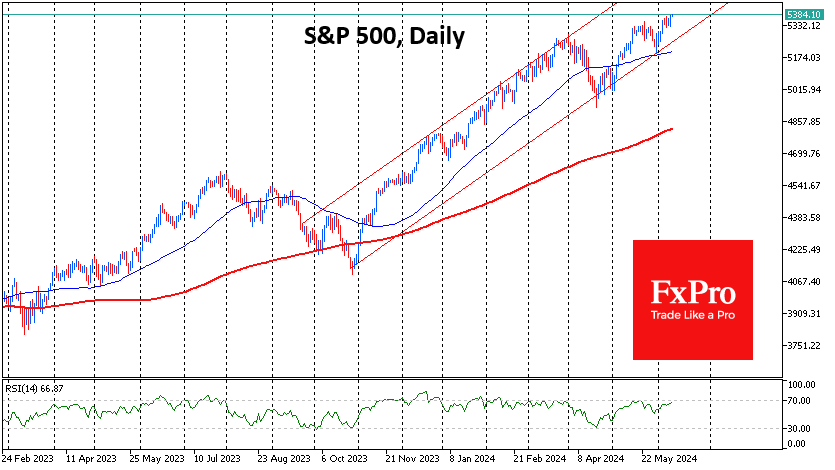

The US indices, S&P500 and Nasdaq100, closed at new all-time highs, largely due to Apple’s positive performance. However, other markets and indices are far from similarly positive. This both leaves room for growth and indicates investor wariness.

The Nasdaq100 index is above 19200, adding 0.7% over the last day and adding 16.1% YTD. Futures are trading in a slight plus on Thursday. The S&P500 rose 0.3% to 5375, bringing its YTD advance to 13.3%. Both have maintained positive momentum since the beginning of the month after a quick correction in late May.

The immediate driver of the gains was a 7.3% jump in Apple shares in a single day. The market’s initial negative reaction to the announcement of the AI strategy, which took away 2% at the premarket, turned into an abundant short squeeze by the opening of trading, sending the stock well into the territory of all-time highs. Interestingly, Apple continues to lag in the market, adding 11.6% YTD.

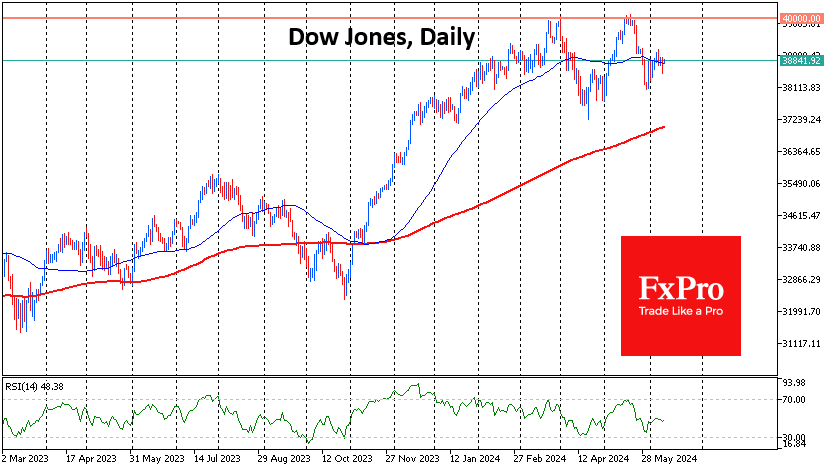

At the same time, we note the slippage of the Dow Jones, which lost 0.3% on Thursday and is adding just 2.7% YTD. This index formed a double top at the 40,000 touches in March and May and is now 3% below that resistance.

Smaller companies are feeling even worse. The Russell 2000 lost 0.4% the day before and has added 0.6% since the beginning of the year. The index needs to rise another 17% to the all-time high reached in November 2021, and it has been in a downtrend for almost a month.

The inflation data and FOMC comments released today have enough potential to synchronise the dynamics of not only the US indices but also the global risk appetite in general.

Investors are focused on how all of today’s events will impact year-end key rate expectations. Right now, rate futures suggest an 88% chance of a cut before year-end, with a 13% chance of a cut of more than 50 points. In other words, markets are plotting a 40-point decline in 2024.

A sharp rise in that number could support the markets’ upswing by making it broader. In this case, the Nasdaq100 can reach 20,000 before the end of the month and the S&P500 to 5,600, while the road to all-time highs would open for the Dow Jones and Russell 2000 in the perspective of a couple of months.

If inflation or Fed sentiment shifts expectations to one or less downside, however, it would prove to be a blow to the markets, capable of taking 5% or even 10% away from them in the next few weeks.

Crypto Market Took a Break from Support

Market picture

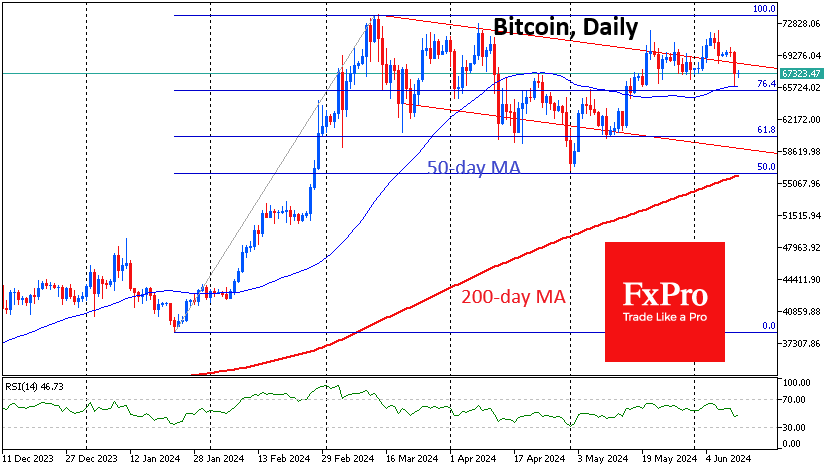

The crypto market cap lost another 0.9% over the last 24 hours, pulling back to $2.44 trillion and extending losses from Friday’s peak to 8%. Since the end of the day on Tuesday, market volatility has noticeably decreased as more traders are taking a wait-and-see stance ahead of the inflation report and FOMC meeting results.

Technically, Bitcoin’s 50-day moving average acted as support, which stopped the active sell-off. If the decline develops, the next support is seen only in the area of $60K. If risk appetite returns to the markets, the price may not only quickly exceed $70K but also head for the renewal of all-time highs.

Bitcoin’s average annualised rate of return over its time on the market has exceeded 103%, Curvo calculates. That’s higher than the annual growth rate of the portfolio of America’s most famous investor, Warren Buffett (10%).

News background

The record, 19-day series of inflows into spot bitcoin-ETFs has come to an end. On 10 June, BTC-ETFs saw a net outflow of $64.9 million. Cumulatively, about $4 billion has flowed into spot bitcoin-ETFs during the longest wave and $15.62 billion since the instruments were approved in January.

“Dormant” for more than five years, 8,000 BTC were moved to Binance, Lookonchain pointed out. The coins were purchased at the bottom of a bear market in December 2018 for $3800.

Billionaire Mark Cuban has said that attitudes towards cryptocurrencies will be a key difference between US presidential candidates Donald Trump and Joe Biden, although both are not versed in the issue.

Japanese public company Metaplanet said it bought 23,351 BTC ($1.58 million), bringing its total balance in the first cryptocurrency to 141.07 BTC ($9.54 million). The average purchase price of 1 BTC was ~$65,300. In April, Metaplanet announced the transfer of funds in its treasury to BTC, explaining the decision with the continued weakening of the yen.

Ernst & Young Hong Kong said institutional investors in Hong Kong may significantly increase their investments in crypto-assets in the next two to three years. Investments in digital assets by institutional investors and family funds in Hong Kong could reach $500bn.

According to a survey conducted by crypto exchange Easy Crypto, about 14% of New Zealanders surveyed own or previously owned cryptocurrencies. In 2022, the figure was 10%.

USDT issuer Tether is investing more than $1bn over the next 12 months in AI, new payment solutions and biotechnology.

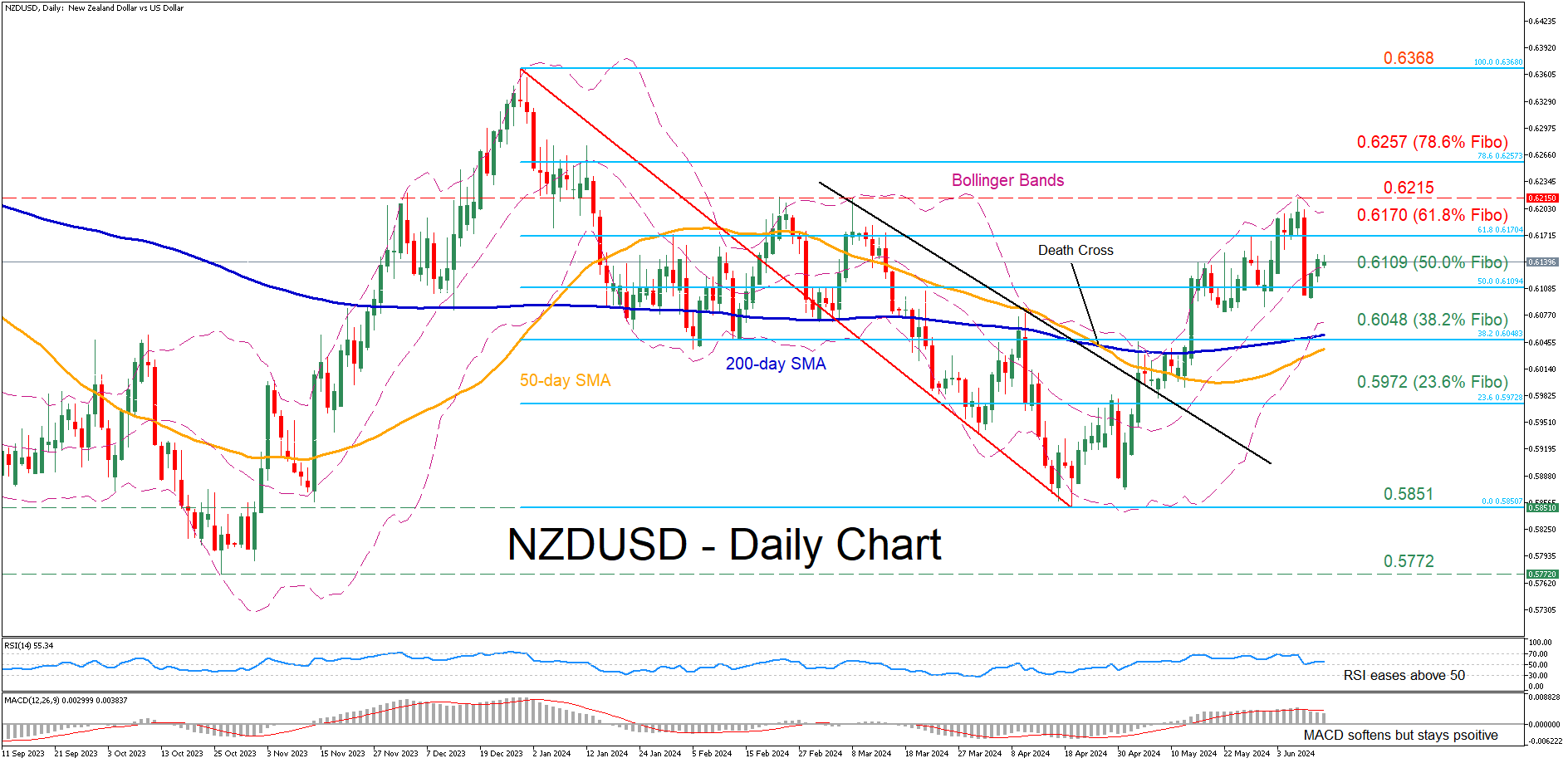

NZDUSD Recoups Post-NFP Slide

- NZDUSD surges to its highest since March 8

- But undergoes a setback after strong NFP report

- Oscillators ease but remain in positive zones

NZDUSD has been in an aggressive uptrend following its 2024 bottom of 0.5851 in mid-April, posting a fresh three-month high last week. Although the pair came under severe selling pressure on Friday due to a stronger-than-expected NFP report, it has been trying to erase its losses in the past couple of sessions.

Should the bulls attempt to push the price higher, immediate resistance could be found at 0.6170, which is the 61.8% Fibonacci retracement of the 0.6368-0.5851 downleg. Higher, the February-March double top region of 0.6215 could prevent further advances. A violation of that zone could pave the way for the 78.6% Fibo of 0.6257.

On the flipside, if the recovery falters, the 50.0% Fibo of 0.6109 could act as the first line of defence. Sliding beneath that floor, the price could descend towards the 38.2% Fibo of 0.6048. Should that barricade fail, the 23.6% Fibo of 0.5972 might provide downside protection.

In brief, NZDUSD pulled back from its three-month peak but quickly recouped part of its losses. However, traders should be cautious as the FOMC meeting and US CPI report on Wednesday could spark volatility in the pair.

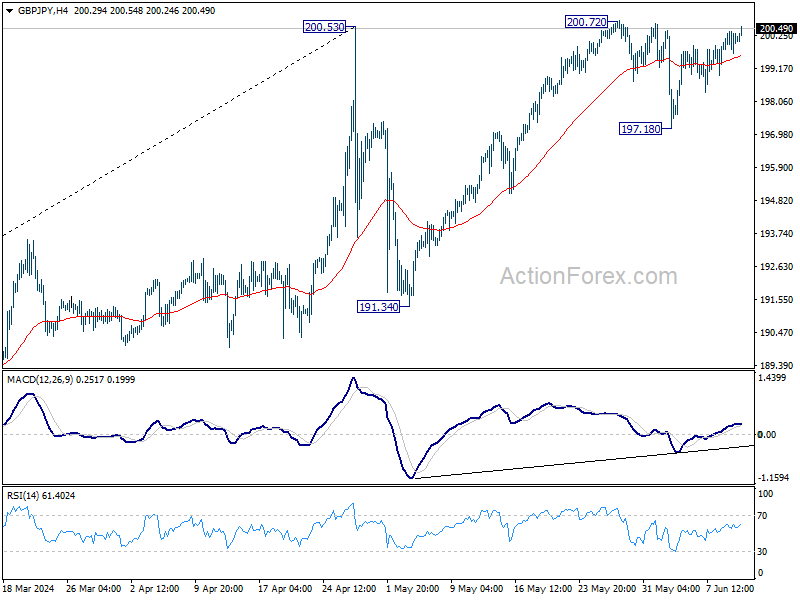

GBP/JPY Daily Outlook

Daily Pivots: (S1) 199.77; (P) 200.09; (R1) 200.49; More...

Intraday bias in GBP/JPY remains neutral for the moment. On the upside, decisive break of 200.72 will resume larger up trend. Nevertheless, break of 197.18 will turn bias to the downside and extend the corrective pattern from 200.53 with another falling leg.

In the bigger picture, as long as 188.63 resistance turned support holds, long term up trend is expected to continue. Sustained trading above 200.53 will pave the way to 100% projection of 155.33 to 188.63 from 178.32 at 211.62.

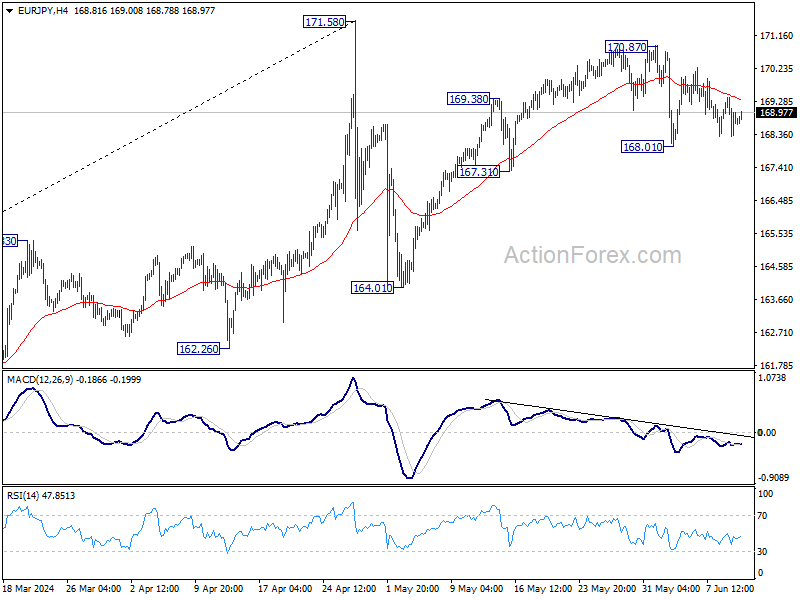

EUR/JPY Daily Outlook

Daily Pivots: (S1) 168.24; (P) 168.83; (R1) 169.37; More...

Intraday bias in EUR/JPY remains neutral as range trading continues. On the downside, break of 168.01 support will strengthen the case that rise from 164.31 has completed at 170.78 already. Intraday bias will be back on the downside for 167.31 support, and then 164.01. Nevertheless, break of 170.87 will resume the rally to retest 171.58 high instead.

In the bigger picture, a medium top was formed at 171.58 after brief breach of 169.96 (2008 high). But as long as 55 W EMA (now at 159.51) holds, price actions from there is seen as correcting the rise from 153.15 only. That is, larger up trend remains in favor to continue. However, sustained break of 55 W EMA will argue that larger scale correction is underway and target 153.15 support.

EUR/GBP Daily Outlook

Daily Pivots: (S1) 0.8440; (P) 0.8456; (R1) 0.8472; More...

Intraday bias in EUR/GBP remains on the downside. Current down trend should target 0.8376 projection level next. On the upside, above 0.8446 minor resistance will turn intraday bias neutral and bring consolidations first, before staging another decline.

In the bigger picture, down trend from 0.9267 (2022 high) is in progress. Next target is 100% projection of 0.8764 to 0.8497 from 0.8643 at 0.8376. Sustained break there will target 161.8% projection at 0.8211 next. For now, outlook will remain bearish as long as 0.8643 resistance holds, even in case of stronger rebound.

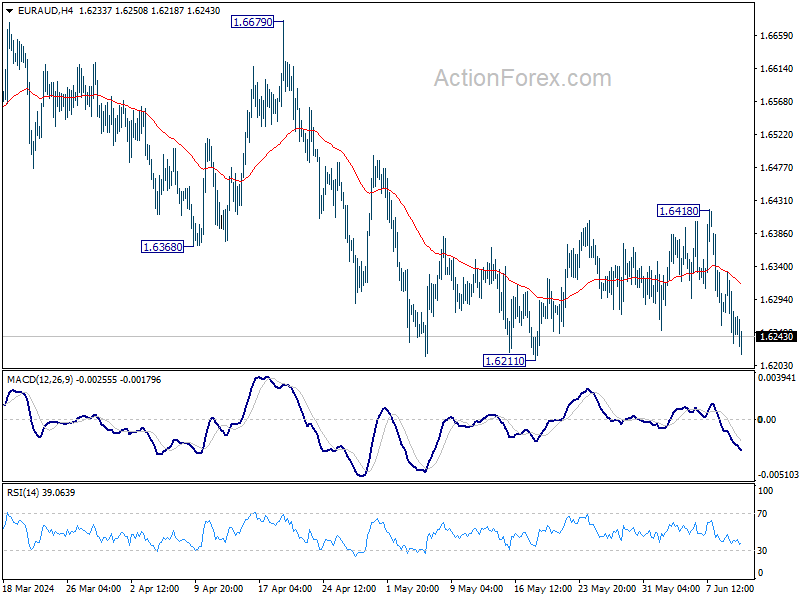

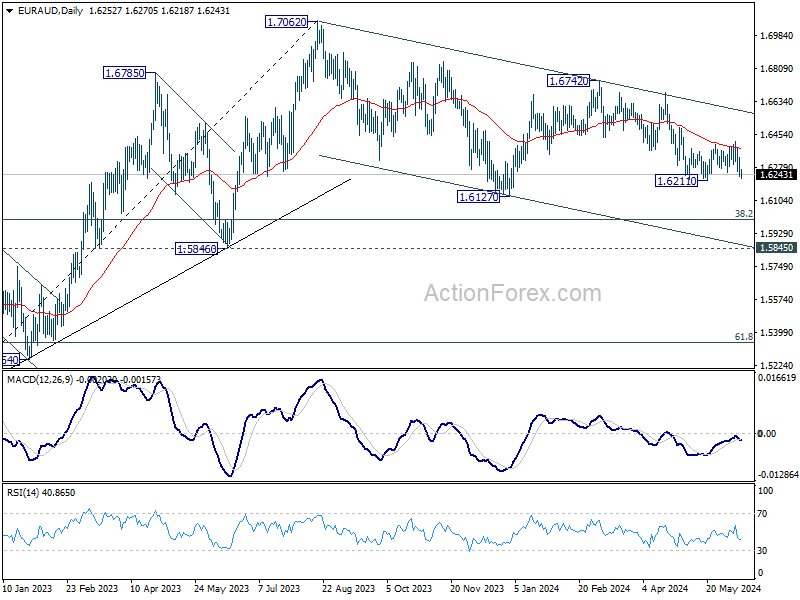

EUR/AUD Daily Outlook

Daily Pivots: (S1) 1.6217; (P) 1.6277; (R1) 1.6318; More...

EUR/AUD is still bounded in range above 1.6211 and intraday bias stays neutral. On the downside, firm break of 1.6211 support will resume the whole decline from 1.6742, as the third leg of the correction from 1.7062. Further fall should be seen through 1.6127 support. On the upside, sustained break 1.6418 resistance will resume the rebound from 1.6211 instead.

In the bigger picture, fall from 1.7062 medium term top is seen as a correction to the up trend from 1.4281 (2022 low). In case of deeper fall, strong support is expected around 1.5846 and 38.2% retracement of 1.4281 to 1.7062 at 1.6000 to bring rebound. Break of 1.7062 is in favor as a later stage.

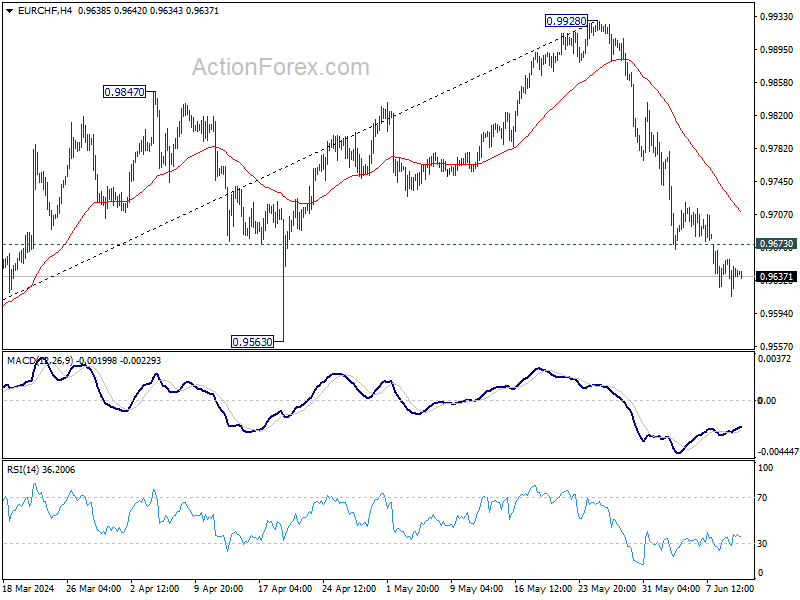

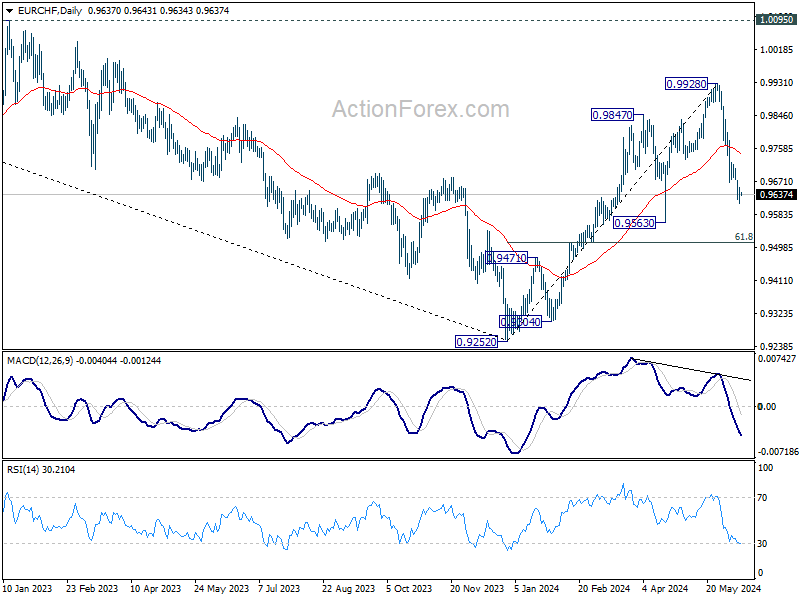

EUR/CHF Daily Outlook

Daily Pivots: (S1) 0.9618; (P) 0.9639; (R1) 0.9661; More....

No change in EUR/CHF's outlook and intraday stays on the downside. Deeper fall would be seen to 0.9563 support. Decisive break there will argue that whole rise from 0.9252 has completed, and bring deeper fall to 61.8% retracement of 0.9252 to 0.9928 at 0.9510. On the upside, above 0.9673 minor resistance will turn intraday bias neutral first.

In the bigger picture, as long as 0.9563 support holds, rise from 0.9252 medium term bottom is still in favor to continue. Next target is 38.2% retracement of 1.2004 (2018 high) to 0.9252 (2023 low) at 1.0303, even just as a correction to the down trend from 1.2004. However, firm break of 0.9563 will suggest that the rally has completed and retain medium term bearishness.

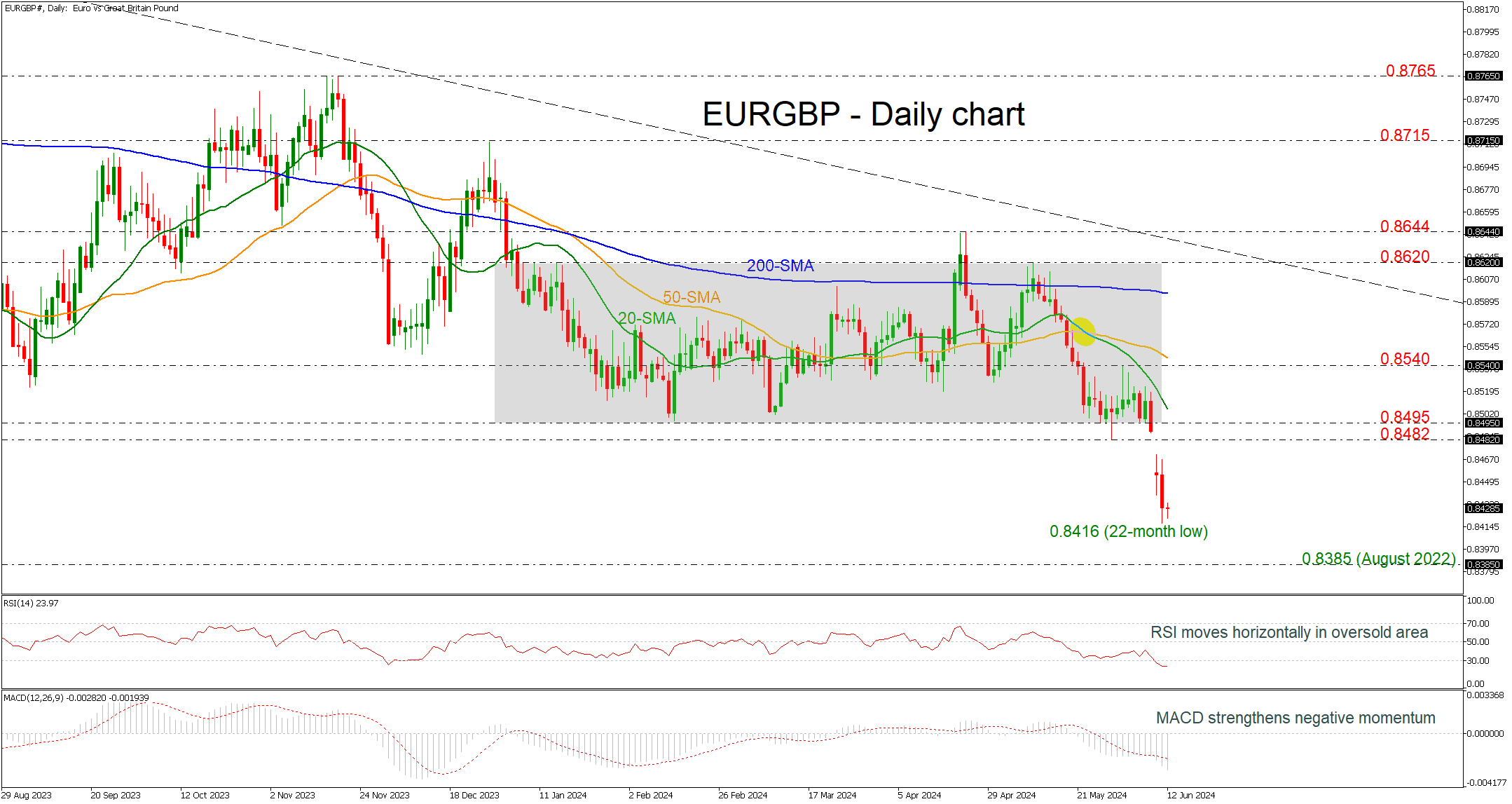

EURGBP Prints New 22-Month Low

- EURGBP continues to fall after bearish gap

- Price shifts neutral outlook to negative

- MACD and RSI hold in oversold regions

EURGBP opened with a significant bearish gap on Monday after the European elections on Sunday, sending the pair towards a fresh 22-month low of 0.8416. The pair is holding well below the medium-term trading range of 0.8495-0.8620, switching the outlook to negative.

Technically, the RSI is standing in the oversold region, while the MACD is looking extremely bearish as it is strengthening its downside momentum beneath its trigger and zero lines. The 20- and the 50-day simple moving averages (SMAs) are also pointing south.

In case of a tumble beneath the multi-month low of 0.8416, this could send the pair until the August 2022 bottom at 0.8385. Even lower, the 0.8340 support level, taken from the lows in July 2022 may halt bearish actions.

On the flip side, a potential rebound near the latest low could take traders to recoup the negative gap and meet the 0.8482-0.8495 resistance region. Above these obstacles, the 20- and the 50-day SMAs at 0.8500 and 0.8545 could be the next targets for the bulls to look for.

To sum up, EURGBP plunged beneath the consolidation area and changed the bias to a more negative one. A climb back above 0.8495 could endorse the view for a possible upside correction.

Market Analysis: EUR/USD Dives While USD/JPY Continues To Rise

EUR/USD gained bearish momentum below the 1.0810 support. USD/JPY is rising and might take out the 157.40 resistance.

Important Takeaways for EUR/USD and USD/JPY Analysis Today

- The Euro started a fresh decline below the 1.0810 support zone.

- There is a connecting bearish trend line forming with resistance at 1.0760 on the hourly chart of EUR/USD at FXOpen.

- USD/JPY climbed higher above the 155.25 and 156.25 levels.

- There is a connecting bullish trend line forming with support at 156.85 on the hourly chart at FXOpen.

EUR/USD Technical Analysis

On the hourly chart of EUR/USD at FXOpen, the pair struggled to clear the 1.0900 resistance zone. The Euro started a fresh decline and traded below the 1.0810 support zone against the US Dollar, as mentioned in the previous analysis.

The pair even declined below 1.0760 and tested the 1.0720 zone. A low was formed near 1.0719 and the pair is now consolidating losses. On the upside, the pair is now facing resistance near the 23.6% Fib retracement level of the recent decline from the 1.0901 swing high to the 1.0719 low at 1.0760.

There is also a connecting bearish trend line forming with resistance at 1.0760 and the 50-hour simple moving average. The next key resistance is near the 1.0780 level.

The main resistance is 1.0810 or the 50% Fib retracement level of the recent decline from the 1.0901 swing high to the 1.0719 low. A clear move above the 1.0810 level could send the pair toward the 1.0860 resistance.

An upside break above 1.0860 could set the pace for another increase. In the stated case, the pair might rise toward 1.0900. If not, the pair might resume its decline. The first major support on the EUR/USD chart is near 1.0720.

The next key support is at 1.0680. If there is a downside break below 1.0680, the pair could drop toward 1.0650. The next support is near 1.0620, below which the pair could start a major decline.

USD/JPY Technical Analysis

On the hourly chart of USD/JPY at FXOpen, the pair started a strong increase from the 155.25 zone. The US Dollar gained bullish momentum above 156.25 against the Japanese Yen.

It even cleared the 50-hour simple moving average and 157.00. The current price action above the 157.00 level is positive. A high is formed at 157.40 and the pair might continue to rise. Immediate resistance on the USD/JPY chart is near 157.40.

The first major resistance is near 157.80. If there is a close above the 157.80 level and the RSI moves above 60, the pair could rise toward 158.50. The next major resistance is near 159.20, above which the pair could test 160.00 in the coming days.

On the downside, the first major support is near the 23.6% Fib retracement level of the upward move from the 155.11 swing low to the 157.40 high at 156.85. There is also a connecting bullish trend line forming with support at 156.85.

The next major support is visible near the 50% Fib retracement level of the upward move from the 155.11 swing low to the 157.40 high at 156.25. If there is a close below 156.25, the pair could decline steadily.

In the stated case, the pair might drop toward the 155.25 support zone. The next stop for the bears may perhaps be near the 154.60 region.

Trade over 50 forex markets 24 hours a day with FXOpen. Take advantage of low commissions, deep liquidity, and spreads from 0.0 pips. Open your FXOpen account now or learn more about trading forex with FXOpen.

This article represents the opinion of the Companies operating under the FXOpen brand only. It is not to be construed as an offer, solicitation, or recommendation with respect to products and services provided by the Companies operating under the FXOpen brand, nor is it to be considered financial advice.